Leymann Inventory of Psychological Terror Scale: Development and Validation for Portuguese Accounting Professionals

Abstract

:1. Introduction

2. Literature Review

Leymann Inventory of Psychological Terror Scale

3. Goal and Research Questions

4. Methodology

4.1. Adaptation of LIPT to ALIPT

4.2. Pilot Study Using ALIPT

4.3. Participants

4.4. Data Analysis

5. Results

5.1. Exploratory Factor Analysis (EFA)

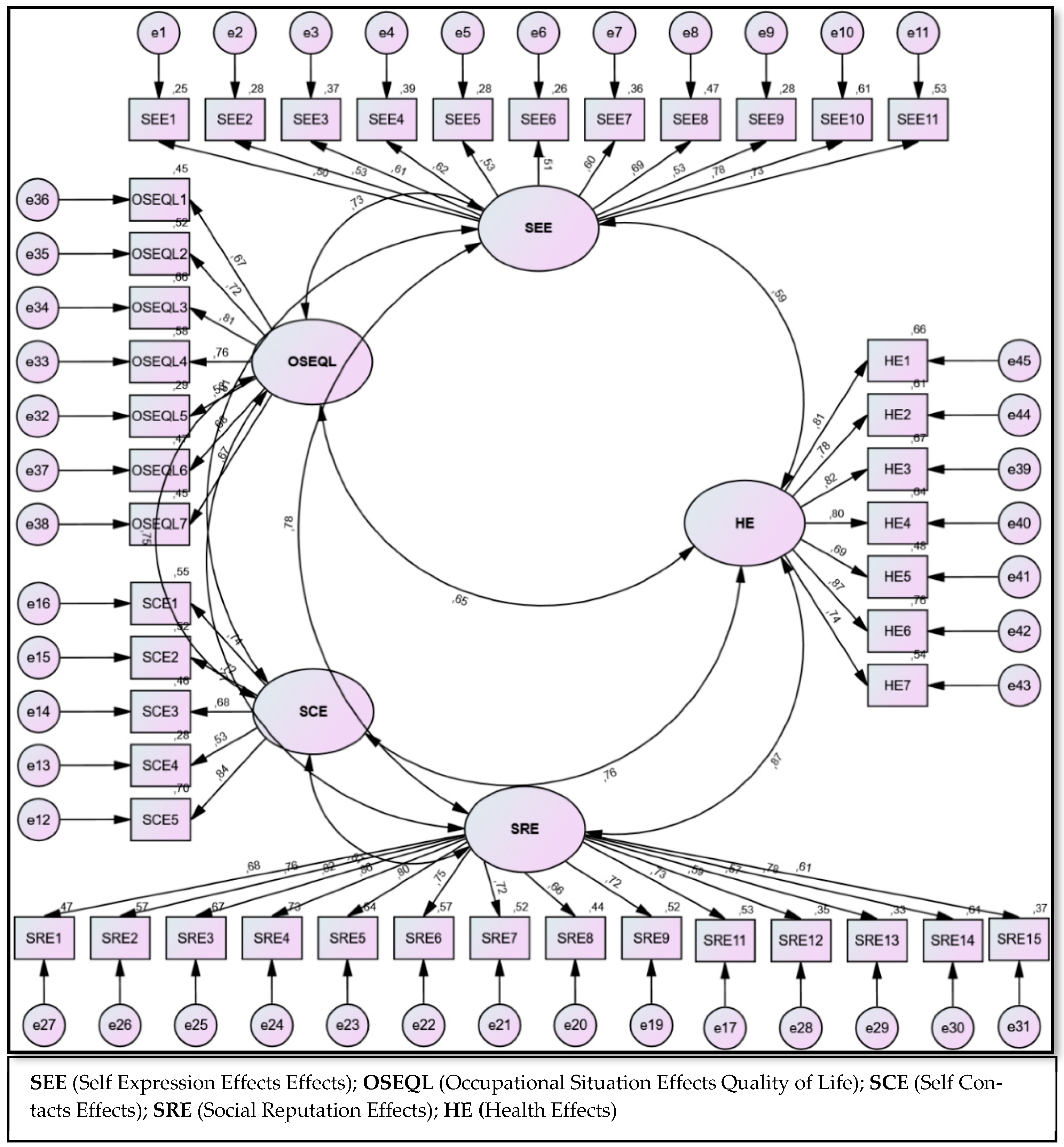

5.2. Confirmatory Factor Analysis (CFA)

5.3. Final Model Analysis

6. Discussion

7. Final Remarks

8. Limitations of the Study and Proposals for Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Al-Kandari, Noriah. M., and Ian T. Jolliffe. 2001. Variable selection and interpretation of covariance principal components. Communications in Statistics-Simulation and Computation 30: 339–54. [Google Scholar] [CrossRef]

- Barbera, Jack, and Jessica R. VandenPlas. 2011. All assessment materials are not created equal: The myths about instrument development, validity, and reliability. In Investigating Classroom Myths through Research on Teaching and Learning. Washington: ACS Publications, pp. 177–93. [Google Scholar]

- Cameron, A. Colin, and Frank A.G. Windmeijer. 1997. An R-squared measure of goodness of fit for some common nonlinear regression models. Journal of Econometrics 77: 329–42. [Google Scholar] [CrossRef]

- Bowling, Nathan A., and Terry A. Beehr. 2006. Workplace harassment from the victim’s perspective: A theoretical model and meta-analysis. Journal of Applied Psychology 91: 998. [Google Scholar] [CrossRef] [PubMed]

- Brown, Timothy A. 2006. Confirmatory Factor Analysis for Applied Research. New York: Guilford. [Google Scholar]

- Byrne, Barbara. M. 2010. Structural Equation Modeling with AMOS: Basic Concepts, Applications, and Programming (Multivariate Applications Series). New York: Taylor & Francis Group, vol. 396, p. 7384. [Google Scholar]

- Cooper, Cary L., Helge Hoel, and Brian Faragher. 2004. Bullying is detrimental to health, but all bullying behaviours are not necessarily equally damaging. British Journal of Guidance & Counselling 32: 367–87. [Google Scholar]

- Costello, Anna B., and Jason Osborne. 2005. Best practices in exploratory factor analysis: Four recommendations for getting the most from your analysis. Practical Assessment, Research & Evaluation 10: 1–9. [Google Scholar]

- de Freitas, Maria Ester. 2001. Assédio moral e assédio sexual: Faces do poder perverso nas organizações. Revista de Administração de Empresas 41: 8–19. [Google Scholar] [CrossRef] [Green Version]

- de Matos, Catarina Garcia. 2016. A Responsabilidade Dos Contabilistas Certificados no Exercício da Sua Atividade Profissional. Coimbra: Edições Almedina, S.A. [Google Scholar]

- Diário da República n.o 87/2017. 2017. Available online: https://dre.pt/home/-/dre/106971782/details/maximized (accessed on 12 May 2020).

- Duffy, Maureen, and Len Sperry. 2007. Workplace mobbing: Individual and family health consequences. The Family Journal 15: 398–404. [Google Scholar] [CrossRef]

- Einarsen, Stale, Helge Hoel, Dieter Zapf, and Cary L. Cooper. 2011. The concept of bullying and harassment at work: The European tradition. Bullying and Harassment in the Workplace: Developments in Theory, Research, and Practice 2: 3–40. [Google Scholar]

- Figueiredo-Ferraz, Hugo, Pedro R. Gil-Monte, and Victor E. Olivares-Faúndez. 2015. Influence of mobbing (workplace bullying) on depressive symptoms: A longitudinal study among employees working with people with intellectual disabilities. Journal of Intellectual Disability Research 59: 39–47. [Google Scholar] [CrossRef]

- Grau-Alberola, Ester, Hugo Figueiredo-Ferraz, and Pedro R. Gil-Monte. 2019. Violencia Laboral: Discriminacion, Hostigamiento y violencia de genero. In Topicos en violencia: Perspectivas, Reflexiones y Aportaciones. Edited by Angelica Maria Lechuga Quinones, Maria de la Luz Sanchez Soto and Martina Patricia Flores Saucedo. Mexico City: AM Editors. [Google Scholar]

- Hair, Joseph. F., William C. Black, Barry. J. Babin, and Rolph E. Anderson. 2010. Multivariate Data Analysis. London: Pearson Education Limited. [Google Scholar]

- Hasin, Hanafiah Haji, and Normah Haji Omar. 2007. An empirical study on job satisfaction, job-related stress and intention to leave among audit staff in public accounting firms in Melaka. Journal of Financial Reporting and Accounting 5: 21–39. [Google Scholar] [CrossRef]

- Hauge, Lars Johan, Anders Skogstad, and Stale Einarsen. 2010. The relative impact of workplace bullying as a social stressor at work. Scandinavian Journal of Psychology 51: 426–33. [Google Scholar] [CrossRef]

- Hershcovis, M. Sandy, Tara C. Reich, and Karen Niven. 2015. Workplace Bullying: Causes, Consequences, and Intervention Strategies. London: Society for Industrial and Organizational Psychology. [Google Scholar]

- Hirigoyen, Marie France. 1999. El acoso Moral, el Maltrato Psicológico en la Vida Cotidiana (en Español). Barcelona: Ediciones Paidós, Mexico City: Buenos Aires. [Google Scholar]

- IASB. 2021. International Financial Reporting Standards. Available online: https://www.ifrs.org/ (accessed on 12 May 2020).

- Korukcu, Öznur, Okan Bulut, Ayla Tuzcu, Zehila Bayram, and Hafize Ozturk Turkmen. 2014. An adaptation of Leymann Inventory of Psychological Terror to health sciences programs in Turkey. Anatolian Journal of Psychiatry/Anadolu Psikiyatri Dergisi 15: 335–43. [Google Scholar] [CrossRef] [Green Version]

- Leymann, Heinz. 1990. Mobbing and psychological terror at workplaces. Violence and Victims 5: 119–26. [Google Scholar] [CrossRef]

- Leymann, Heinz. 1996. The content and development of mobbing at work. European Journal of Work and Organizational Psychology 5: 165–84. [Google Scholar] [CrossRef]

- Luna, Manuel, Carmen Yela, and Alicia Antón. 2003. Acoso Psicológico en el Trabajo (Mobbing). Madrid: Ediciones GPS. [Google Scholar]

- Maximo, Cristiana, Jose Soares Martins, Sergio Dominguez-Lara, Abilio Lourenço, and Margarida Simões. 2020a. Adaptação e Análise da Estrutura Interna da Escala de Mobbing de Leymann (LIPT45 ) Para O Contexto Português. Avaliação Psicológica 242: 56–66. [Google Scholar] [CrossRef]

- Maximo, Cristiana, Jose Soares Martins, Sergio Dominguez-Lara, Abilio Lourenço, and Margarida Simões. 2020b. Adaptation and Analysis of the Internal Structure of the Scale of Mobbing in Leymann (LIPT45) for the Portuguese Context. Avaliação Psicológica 19: 56–66. [Google Scholar] [CrossRef]

- Mikkelsen, Eva G., and Stale Einarsen. 2001. Bullying in Danish work-life: Prevalence and health correlates. European Journal of Work and Organizational Psychology 10: 393–413. [Google Scholar] [CrossRef]

- Monteiro, Ana Paula, Pedro Cunha, Jose Soares Martins, and Margarida Simões. 2021. Mobbing e conflito em contextos de saúde. In Gestão de Conflitos na saúde. Edited by Cunha Pedro and Ana Paula Monteiro. Lisboa: Pactor, pp. 171–96. [Google Scholar]

- Netemeyer, Richard G., William O. Bearden, and Subhash Sharma. 2003. Scaling Procedures: Issues and Applications. Thousand Oaks: Sage Publications. [Google Scholar]

- Niedhammer, Isabelle, Simon David, and Stephanie Degioanni. 2006. Association between workplace bullying and depressive symptoms in the French working population. Journal of Psychosomatic Research 61: 251–59. [Google Scholar] [CrossRef] [PubMed]

- Ozkan, Azzem, and Mahmut Ozdevecioğlu. 2013. The effects of occupational stress on burnout and life satisfaction: A study in accountants. Quality & Quantity 47: 2785–98. [Google Scholar]

- Pestana, Maria Helena, and Joao Nunes Gageiro. 2003. Análise de Dados Para Ciências Sociais: A Complementaridade do SPSS. Lisboa: Edições Silabo. [Google Scholar]

- Raykov, Tenko, and George A. Marcoulides. 2006. Estimation of generalizability coefficients via a structural equation modeling approach to scale reliability evaluation. International Journal of Testing 6: 81–95. [Google Scholar] [CrossRef]

- Rayner, Charlotte, Helge Hoel, and Cary Cooper. 2003. Workplace Bullying: What We Know, Who Is to Blame and What Can We Do? Boca Raton: CRC Press. [Google Scholar]

- Salin, Denise. 2006. Organizational Measures Taken against Workplace Bullying: The Case of Finnish Municipalities. Stockholm: Svenska handelshögskolan. [Google Scholar]

- Thofehrn, Maria Buss, Simone Coelho Amestoy, Karen Knopp de Carvalho, Francine Pereira Andrade, and Viviane Marten Milbrath. 2008. Assédio moral no trabalho da enfermagem. Cogitare Enfermagem 13: 597–601. [Google Scholar] [CrossRef] [Green Version]

- Thompson, Bruce. 2004. Exploratory and Confirmatory Factor Analysis: Understanding Concepts and Applications. Washington: American Psychological Association. [Google Scholar]

- Torres, Analia, Dalia Costa, Helena Sant’Ana, Bernardo Coelho, and Isabel Sousa. 2016. Assédio Sexual e Moral no Local de Trabalho. Lisboa: CITE/CIEG. [Google Scholar]

- Zachariadou, Theodora, Savvas Zannetos, Stella Elia Chira, Sofia Gregoriou, and Andreas Pavlakis. 2018. Prevalence and Forms of Workplace Bullying Among Health-care Professionals in Cyprus: Greek Version of “Leymann Inventory of Psychological Terror” Instrument. Safety and Health at Work 9: 339–46. [Google Scholar] [CrossRef] [PubMed]

- Zapf, Dieter, and Stale Einarsen. 2005. Counterproductive Work Behavior: Investigations of Actors and Targets. Edited by Suzy Fox and Paul E. Spector. Washington: American Psychological Association. [Google Scholar]

- Zapf, Dieter, and Claudia Gross. 2001. Conflict escalation and coping with workplace bullying: A replication and extension. European Journal of Work and Organizational Psychology 10: 497–522. [Google Scholar] [CrossRef]

- Zhou, Xiang, Samma Faiz Rasool, and Dawei Ma. 2020. The relationship between workplace violence and innovative work behavior: The mediating roles of employee wellbeing. Healthcare 8: 332. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

| Dimensions | Variables | Original Scale (LIPT45)—ITEMS | Items Changed |

|---|---|---|---|

| Self Expression Effects | SEE1 | Your superior restricts the opportunity for you to express yourself | Your technical accounting manager restricts the opportunity for you to express yourself. |

| SEE2 | You are constantly interrupted. | You are constantly interrupted. | |

| SEE3 | Colleagues restrict your opportunity to express yourself. | Colleagues restrict your opportunity to express yourself. | |

| SEE4 | You are yelled at and loudly scolded. | You are yelled at and loudly scolded. | |

| SEE5 | Your work is constantly criticized. | Your work is constantly criticized. | |

| SEE6 | There is constant criticism about your personal life. | There is constant criticism about your personal life. | |

| SEE7 | You are terrorized on the telephone. | You are terrorized on the telephone by other accounting officers. | |

| SEE8 | Oral threats are made. | Oral threats are made. | |

| SEE9 | Written threats are sent. | Written threats are sent. | |

| SEE10 | Contact is denied through looks or gestures. | Contact is denied through looks or gestures. | |

| SEE11 | Contact is denied through innuendo. | Contact is denied through innuendo. | |

| Self Contacts Effects | SCE1 | People do not speak with you anymore. | Accountants do not speak with you anymore. |

| SCE2 | You cannot talk to anyone; access to others is denied. | You cannot talk to anyone accountant; access to others is denied. | |

| SCE3 | You are relocated to another room far away from colleagues. | You are relocated to another office far away from colleagues. | |

| SCE4 | Colleagues are forbidden to talk with you. | Colleagues are forbidden to talk with you. | |

| SCE5 | You are treated as if you are invisible. | Colleagues are treated as if you are invisible. | |

| Social Reputation Effects | SRE1 | People talk badly about you behind your back. | Colleagues talk badly about you behind your back. |

| SRE2 | Unfounded rumours about you are circulated. | Unfounded rumours about you are circulated. | |

| SRE3 | You are ridiculed. | You are ridiculed. | |

| SRE4 | You are treated as if you are mentally ill. | You are treated as if you are mentally ill. | |

| SRE5 | You are forced to undergo a psychiatric evaluation. | You are forced to undergo a psychiatric evaluation. | |

| SRE6 | Your handicap is ridiculed. | Your handicap is ridiculed. | |

| SRE7 | People imitate your gestures, walk, or voice to ridicule you. | Colleagues imitate your gestures, walk, or voice to ridicule you. | |

| SRE8 | Your political or religious beliefs are ridiculed. | Your political or religious beliefs are ridiculed. | |

| SRE9 | Your private life is ridiculed. | Your private life is ridiculed. | |

| SRE10 | Your nationality is ridiculed. | Your nationality is ridiculed. | |

| SRE11 | You are forced to do a job that affects your self-esteem. | You are forced to do a job that affects your self-esteem. | |

| SRE12 | Your efforts are judged in a wrong and demeaning way. | Your efforts are judged in a wrong and demeaning way. | |

| SRE13 | Your decisions are always questioned. | Your decisions are always questioned. | |

| SRE14 | You are called demeaning names. | You are called demeaning names. | |

| SRE15 | Sexual innuendoes are present. | Sexual innuendoes are present. | |

| Occupational Situation Effects and Quality of Life | OSEQL1 | There are no special tasks for you. | There are no special new accounting tasks for you. |

| OSEQL2 | Supervisors take away assignments so that you cannot invent new tasks to do. | Accounting technical manager take away assignments so that you cannot invent new tasks to do. | |

| OSEQL3 | You are given meaningless jobs to carry out. | You are given meaningless jobs to carry out. | |

| OSEQL4 | You are given jobs that are below your qualifications. | You are given jobs that are below your qualifications. | |

| OSEQL5 | You are continually given new tasks. | You are continually given new tasks. | |

| OSEQL6 | You are given tasks that affect your self-esteem. | You are given tasks that affect your self-esteem. | |

| OSEQL7 | You are given tasks that are way beyond your qualifications in order to discredit you. | You are given tasks that are way beyond your qualifications in order to discredit you. | |

| Health Effects | HE1 | You are forced to do a physically strenuous job. | You are forced to do a physically strenuous job. |

| HE2 | Threats of physical violence are made. | Threats of physical violence are made. | |

| HE3 | Light violence is used to threaten you. | Light violence is used to threaten you. | |

| HE4 | Physical abuse is present. | Physical abuse is present. | |

| HE5 | Causing general damages that create financial costs to you. | Causing general damages that create financial costs to you. | |

| HE6 | Damaging your workplace or home. | Damaging your workplace or home. | |

| HE7 | Outright sexual harassment is present. | Outright sexual harassment is present. |

| Rotated Component Matrix | ||||||

|---|---|---|---|---|---|---|

| Dimensions | Variables | Factors | ||||

| 1 | 2 | 3 | 4 | 5 | ||

| Self Expression Effects | SEE1 | 0.569 | ||||

| SEE2 | 0.582 | |||||

| SEE3 | 0.599 | |||||

| SEE4 | 0.517 | |||||

| SEE5 | 0.565 | |||||

| SEE6 | 0.505 | |||||

| SEE7 | 0.595 | |||||

| SEE8 | 0.633 | |||||

| SEE9 | 0.573 | |||||

| SEE10 | 0.688 | |||||

| SEE11 | 0.657 | |||||

| Self Contacts Effects | SCE1 | 0.677 | ||||

| SCE2 | 0.657 | |||||

| SCE3 | 0.650 | |||||

| SCE4 | 0.537 | |||||

| SCE5 | 0.751 | |||||

| Social Reputation Effects | SRE1 | 0.674 | ||||

| SRE2 | 0.731 | |||||

| SRE3 | 0.787 | |||||

| SRE4 | 0.809 | |||||

| SRE5 | 0.795 | |||||

| SRE6 | 0.733 | |||||

| SRE7 | 0.724 | |||||

| SRE8 | 0.662 | |||||

| SRE9 | 0.720 | |||||

| SRE10 | 0.377 | |||||

| SRE11 | 0.760 | |||||

| SRE12 | 0.620 | |||||

| SRE13 | 0.616 | |||||

| SRE14 | 0.764 | |||||

| SRE15 | 0.613 | |||||

| Occupational Situation Effects and Quality of Life | OSEQL1 | 0.566 | ||||

| OSEQL2 | 0.631 | |||||

| OSEQL3 | 0.647 | |||||

| OSEQL4 | 0.577 | |||||

| OSEQL5 | 0.535 | |||||

| OSEQL6 | 0.666 | |||||

| OSEQL7 | 0.710 | |||||

| Health Effects | HE1 | 0.793 | ||||

| HE2 | 0.678 | |||||

| HE3 | 0.725 | |||||

| HE4 | 0.690 | |||||

| HE5 | 0.654 | |||||

| HE6 | 0.758 | |||||

| HE7 | 0.604 | |||||

| Adjustment Index | Model 1 5 Factors—45 Variables | Model 2 5 Factors—44 Variables |

|---|---|---|

| χ2 Satorra Bentler | 7635.583 | 7404.786 |

| 935 | 892 | |

| p-value | p < 0.001 | p < 0.001 |

| Satorra Bentler | 8.166 | 8.301 |

| RMSEA | 0.131 | 0.082 |

| SRMR | 0.0671 | 0.0625 |

| NFI | 0.766 | 0.896 |

| GFI | 0.740 | 0.898 |

| AGFI | 0.701 | 0.882 |

| CFI | 0.787 | 0.878 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Silva, R.; Simões, M.; Monteiro, A.P.; Dias, A. Leymann Inventory of Psychological Terror Scale: Development and Validation for Portuguese Accounting Professionals. Economies 2021, 9, 94. https://doi.org/10.3390/economies9030094

Silva R, Simões M, Monteiro AP, Dias A. Leymann Inventory of Psychological Terror Scale: Development and Validation for Portuguese Accounting Professionals. Economies. 2021; 9(3):94. https://doi.org/10.3390/economies9030094

Chicago/Turabian StyleSilva, Rui, Margarida Simões, Ana Paula Monteiro, and António Dias. 2021. "Leymann Inventory of Psychological Terror Scale: Development and Validation for Portuguese Accounting Professionals" Economies 9, no. 3: 94. https://doi.org/10.3390/economies9030094

APA StyleSilva, R., Simões, M., Monteiro, A. P., & Dias, A. (2021). Leymann Inventory of Psychological Terror Scale: Development and Validation for Portuguese Accounting Professionals. Economies, 9(3), 94. https://doi.org/10.3390/economies9030094