A Thoughtful Insight on Women Entrepreneur’s Investment Attitude

Abstract

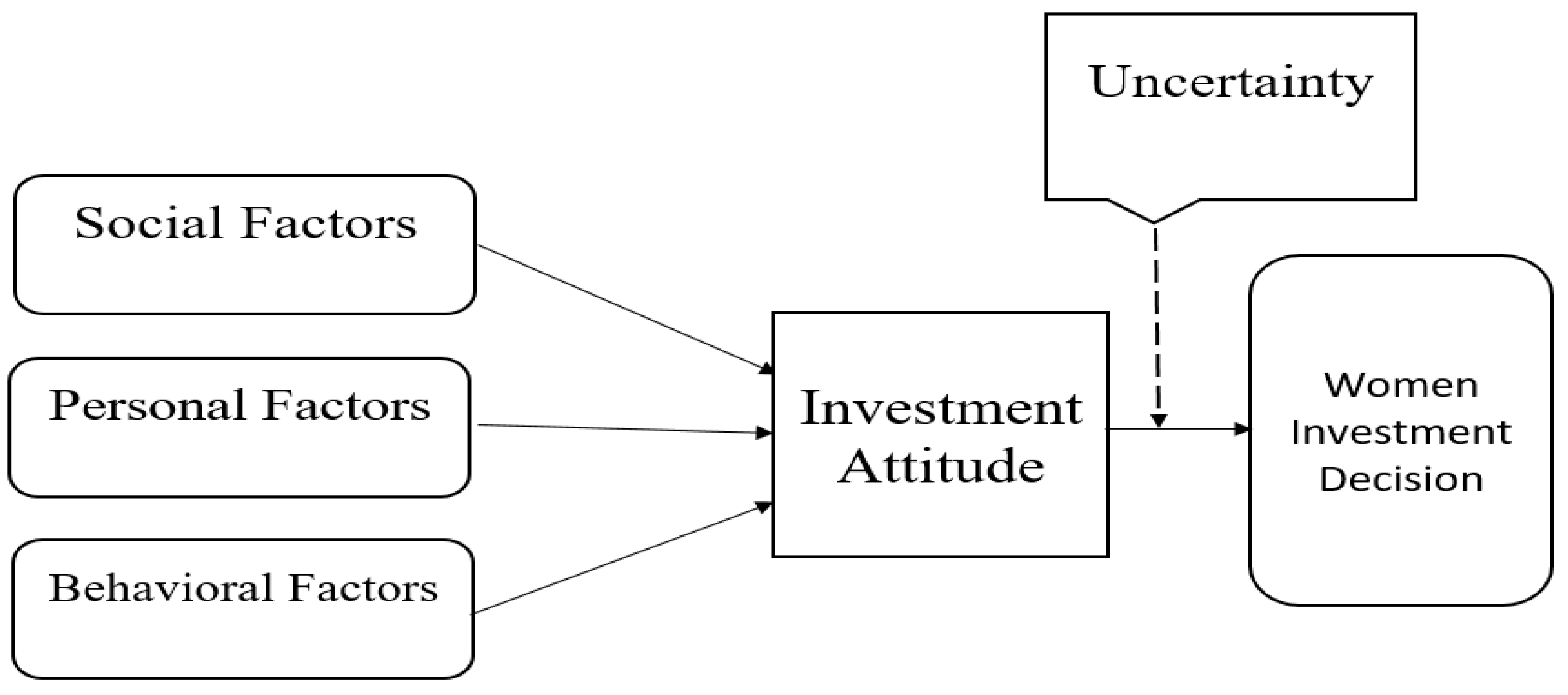

:1. Introduction

2. Literature Review

3. Methodology

4. Results

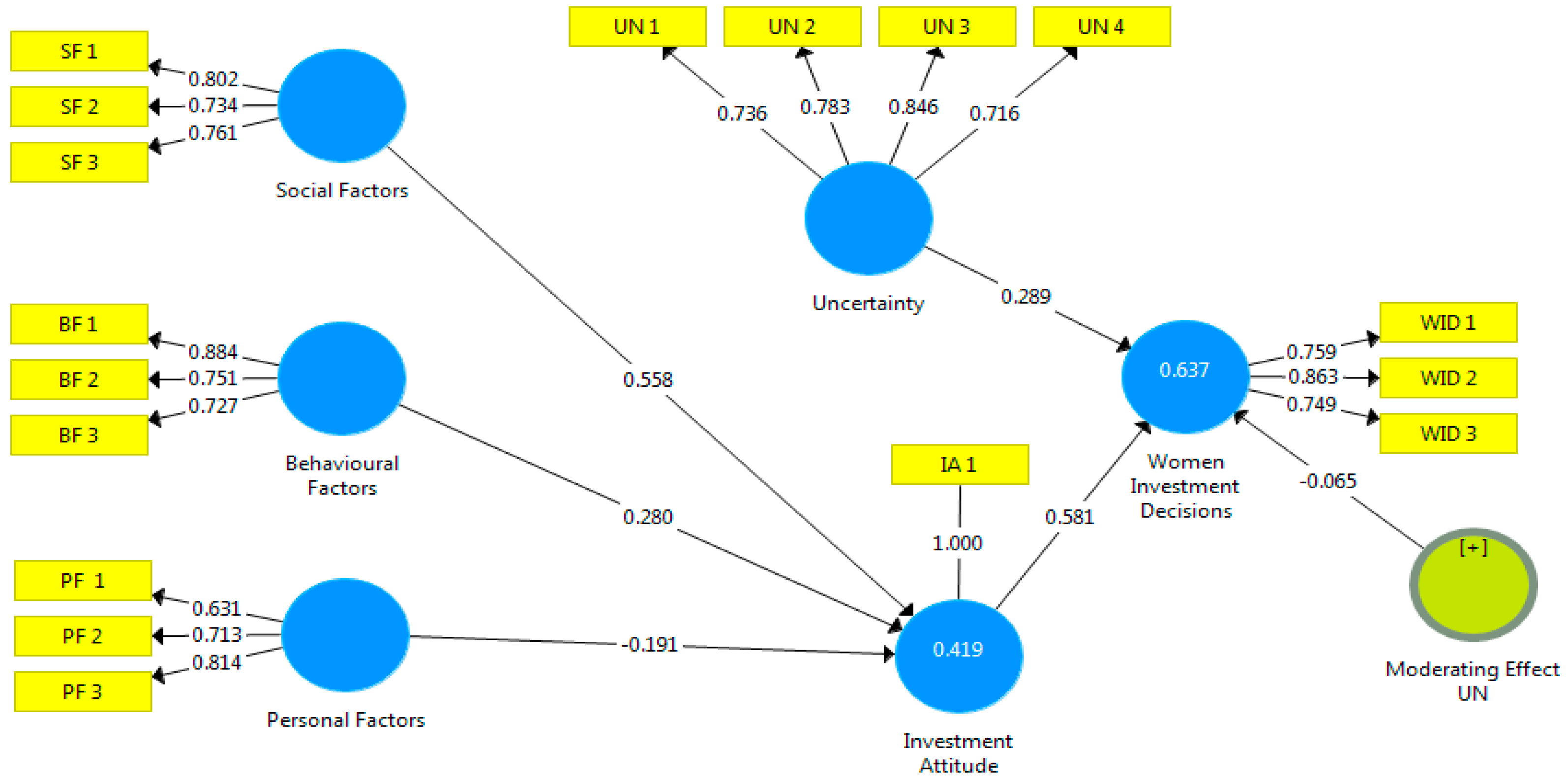

4.1. Assessment of Measurement Model

4.2. Assessing Structural Model

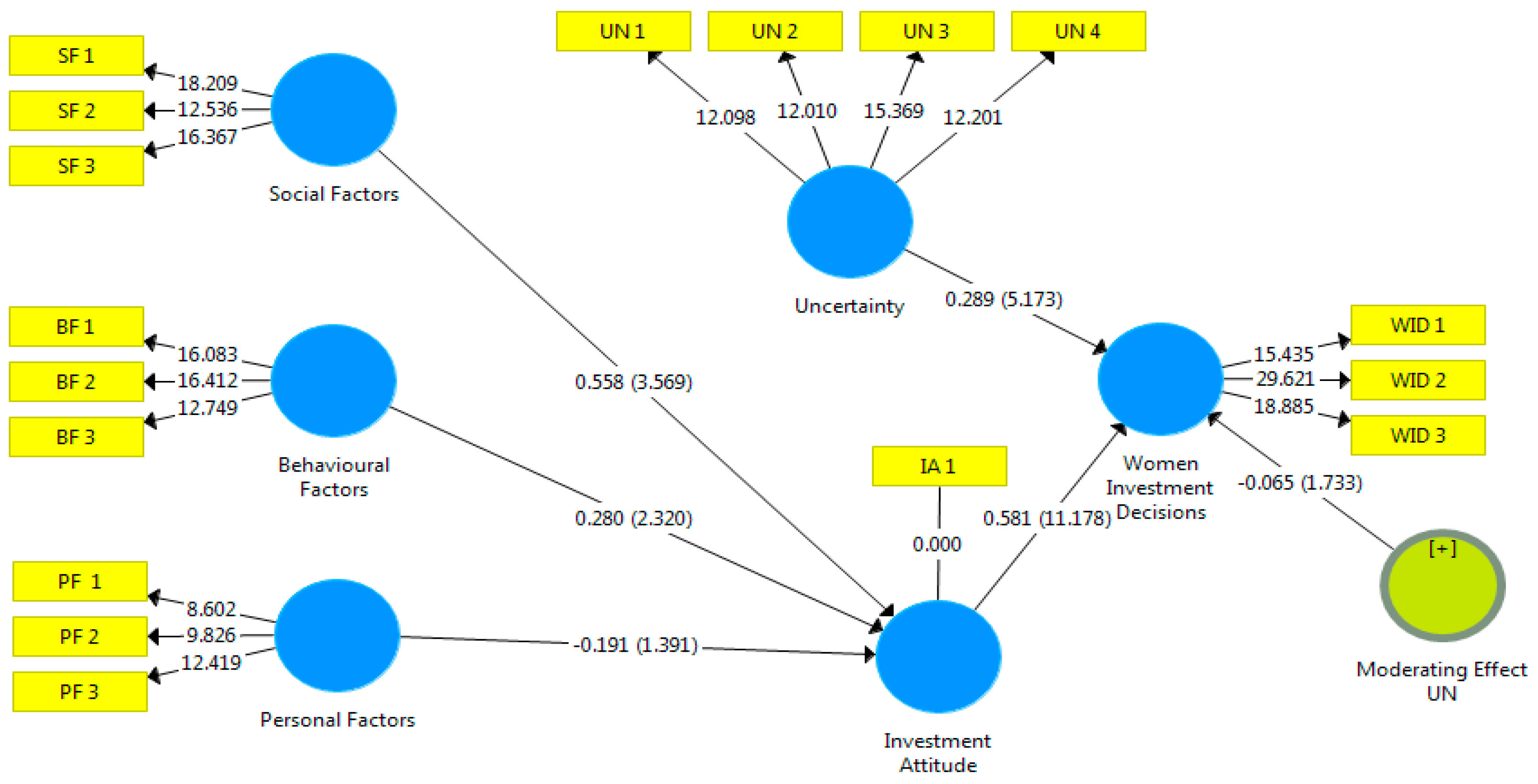

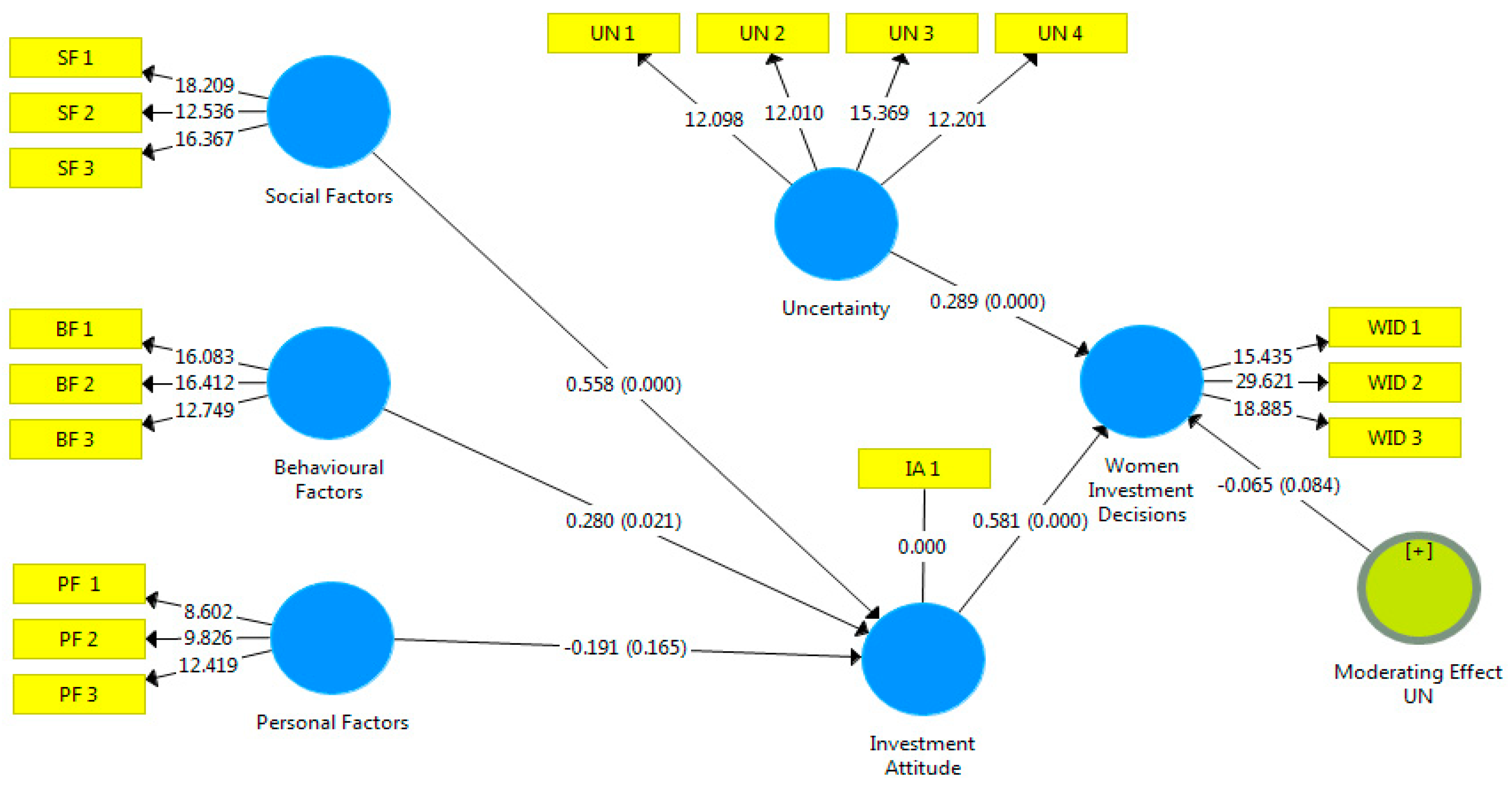

4.3. Significance of Hypothesis

4.4. Path Coefficient Analysis

5. Discussions

6. Conclusions

7. Implications

8. Limitation

9. Contribution to the Society

10. Future Scope

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Agarwal, Sucheta, and Usha Lenka. 2018. Why research is needed in women entrepreneurship in India: A viewpoint. International Journal of Social Economics 45: 1042–57. [Google Scholar] [CrossRef]

- Akhtar, Fatima, K. S. Thyagaraj, and Niladri Das. 2018. The impact of social influence on the relationship between personality traits and perceived investment performance of individual investors: Evidence from Indian stock market. International Journal of Managerial Finance 14: 130–48. [Google Scholar] [CrossRef]

- Almenberg, Johan, and Anna Dreber. 2015. Gender, stock market participation and financial literacy. Economics Letters 137: 140–42. [Google Scholar] [CrossRef] [Green Version]

- Anderson, Anders, Forest Baker, and David T. Robinson. 2017. Precautionary savings, retirement planning and misperceptions of financial literacy. Journal of Financial Economics 126: 383–98. [Google Scholar] [CrossRef] [Green Version]

- Arafat, Mohd Yasir, Javed Ali, Amit Kumar Dwivedi, and Imran Saleem. 2020. Social and Cognitive Aspects of Women Entrepreneurs: Evidence from India. The Journal for Decision Makers 45: 223–39. [Google Scholar] [CrossRef]

- Baig, Umair, Batool Muhammad Hussain, Vida Davidaviciene, and Ieva Meidute-Kavaliauskiene. 2021. Exploring Investment Behaviour of Women Entrepreneur: Some Future Directions. International Journal of Financial Studies 9: 20. [Google Scholar] [CrossRef]

- Baker, H. Kent, Satish Kumar, and Harsh Pratap Singh. 2018. Behavioural biases among SME owners. International Journal of Management Practice 11: 259–83. [Google Scholar] [CrossRef]

- Baporikar, Neeta, and Sigried Shikokola. 2020. Enhancing Innovation Adoption to Boost SMEs Performance. International Journal of Innovation in the Digital Economy 11: 1–20. [Google Scholar] [CrossRef]

- Baporikar, Neeta, and Susan Akino. 2020. Financial Literacy Imperative for Success of Women Entrepreneurship. International Journal of Innovation in the Digital Economy 11: 1–21. [Google Scholar] [CrossRef]

- Barber, Brad, and Terrance Odean. 1998. The Common Stock Investment Performance of Individual Investors. SSRN Electronic Journal 2: 773–806. [Google Scholar] [CrossRef] [Green Version]

- Baum and Ingram. 1998. Survival-Enhancing Learning in the Manhattan Hotel Industry, 1898–980. Management Science 44: 996–1016. [Google Scholar] [CrossRef]

- Bazley, William J., Yosef Bonaparte, and George M. Korniotis. 2020. Financial Self-awareness: Who Knows What They Don’t Know? Finance Research Letters 38: 101445. [Google Scholar] [CrossRef]

- Benartzi, Shlomo, and Richard Thaler. 1995. Myopic Loss Aversion and the Equity Premium Puzzle. The Quarterly Journal of Economics 110: 73–92. [Google Scholar] [CrossRef] [Green Version]

- Bianchi, Milo. 2018. Financial Literacy and Portfolio Dynamics: Financial Literacy and Portfolio Dynamics. The Journal of Finance 73: 831–59. [Google Scholar] [CrossRef] [Green Version]

- Bracha, Anat, and Donald J. Brown. 2012. Affective decision making: A theory of optimism bias. Games and Economic Behavior 75: 67–80. [Google Scholar] [CrossRef] [Green Version]

- Brown, Sarah, and Karl Taylor. 2014. Household finances and the ‘Big Five’ personality traits. Journal of Economic Psychology 45: 197–212. [Google Scholar] [CrossRef] [Green Version]

- Bucciol, Alessandro, and Luca Zarri. 2017. Do personality traits influence investors’ portfolios? Journal of Behavioral and Experimental Economics 68: 1–12. [Google Scholar] [CrossRef]

- Bucciol, Alessandro, and Marcella Veronesi. 2014. Teaching children to save: What is the best strategy for lifetime savings? Journal of Economic Psychology 45: 1–17. [Google Scholar] [CrossRef]

- Calcagno, Riccardo, and Chiara Monticone. 2015. Financial literacy and the demand for financial advice. Journal of Banking and Finance 50: 363–80. [Google Scholar] [CrossRef]

- Camerer, Colin, and Dan Lovallo. 1999. Overconfidence and Excess Entry: An Experimental Approach. The American Economic Review 89: 13. [Google Scholar] [CrossRef] [Green Version]

- Chandra, Abhijeet, and Ravinder Kumar. 2012. Factors Influencing Indian Individual Investor Behaviour: Survey Evidence. SSRN Electronic Journal 39: 141–167. [Google Scholar] [CrossRef]

- Chavali, Kavita, and Prasanna Mohan Raj. 2016. Impact of demographic variables and risk tolerance on investment decisions: An empirical analysis. International Journal of Economics and Financial Issues 6: 169–75. [Google Scholar]

- Chin, Wynne. 2010. How to Write Up and Report PLS Analyses. In Handbook of Partial Least Squares. Edited by Vincenzo Esposito Vinzi, Wynne W. Chin, Jörg Henseler and Huiwen Wang. Berlin/Heidelberg: Springer, pp. 655–90. [Google Scholar] [CrossRef]

- Cooke, Fang Lee, and Mengtian Xiao. 2021. Women entrepreneurship in China: Where are we now and where are we heading. Human Resource Development International 24: 104–21. [Google Scholar] [CrossRef]

- Davis, Aeron. 2006. The role of the mass media in investor relations. Journal of Communication Management 10: 7–17. [Google Scholar] [CrossRef]

- Elam, Amanda B., Candida G. Brush, Patricia G. Greene, Benjamin Baumer, Monica Dean, and René Heavlow. 2019. Women’s Entrepreneurship Report 2018/2019. Wellesley: Babson College, Smith College, and the Global Entrepreneurship Research Association (GERA), GEM Consortium. [Google Scholar]

- Eysenck, Hans Jurgen. 1991. Dimensions of personality: 16, 5 or 3? Criteria for a taxonomic paradigm. Personality and Individual Differences 12: 773–90. [Google Scholar] [CrossRef]

- Filbeck, Greg, Patricia Hatfield, and Philip Horvath. 2005. Risk Aversion and Personality Type. Journal of Behavioral Finance 6: 170–80. [Google Scholar] [CrossRef]

- Fisher, Kenneth, and Meir Statman. 2000. Cognitive Biases in Market Forecasts. The Journal of Portfolio Management 27: 72–81. [Google Scholar] [CrossRef] [Green Version]

- Fornell, Claes, and David Larcker. 1981. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research 12: 39–50. [Google Scholar] [CrossRef]

- Godoi, Christiane Kleinübing, Rosilene Marcon, and Anielson Barbosa DaSilva. 2005. Loss aversion: A qualitative study in behavioural finance. Managerial Finance 31: 46–56. [Google Scholar] [CrossRef]

- Griffin, Mark, and Gudela Grote. 2020. When Is More Uncertainty Better? A Model of Uncertainty Regulation and Effectiveness. Academy of Management Review 45: 745–65. [Google Scholar] [CrossRef]

- Grohmann, Antonia, Roy Kouwenberg, and Lukas Menkhoff. 2015. Childhood roots of financial literacy. Journal of Economic Psychology 51: 114–33. [Google Scholar] [CrossRef] [Green Version]

- Hair, Joe, Christian Ringle, and Marko Sarstedt. 2011. PLS-SEM: Indeed, a silver bullet. Journal of Marketing Theory and Practice 19: 139–52. [Google Scholar] [CrossRef]

- Hair, Joseph, Jeffrey Risher, Marko Sarstedt, and Christian Ringle. 2019. When to use and how to report the results of PLS-SEM. European Business Review 31: 2–24. [Google Scholar] [CrossRef]

- Hair, Joe F., Jr., Marko Sarstedt, Lucas Hopkins, and Volker G. Kuppelwieser. 2014. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review 26: 106–21. [Google Scholar] [CrossRef]

- Heaton, James. 2002. Managerial Optimism and Corporate Finance. Financial Management 31: 33. [Google Scholar] [CrossRef]

- Henseler, Jörg, Christian M. Ringle, and Rudolf R. Sinkovics. 2009. The use of partial least squares path modeling in international marketing. In Advances in International Marketing. Edited by R. R. Sinkovics and P. N. Ghauri. Bingley: Emerald Group Publishing Limited, vol. 20, pp. 277–319. [Google Scholar] [CrossRef] [Green Version]

- Hibbert, Jeffery, Ivan Beutler, and Todd Martin. 2004. Financial Prudence and Next Generation Financial Strain. Journal of Financial Counseling and Planning 15: 9. [Google Scholar]

- Hsu, Dan, Johan Wiklund, and Richard Cotton. 2017. Success, Failure, and Entrepreneurial Reentry: An Experimental Assessment of the Veracity of Self–Efficacy and Prospect Theory. Entrepreneurship Theory and Practice 41: 19–47. [Google Scholar] [CrossRef]

- Hsu, Yuan-Lin, Hung-Ling Chen, Po-Kai Huang, and Wan-Yu Lin. 2020. Does financial literacy mitigate gender differences in investment behavioral bias? Finance Research Letters 2020: 101789. [Google Scholar] [CrossRef]

- Imtiaz, Rozina, Syeda Qurat ul Ain Kazmi, Maheen Amjad, and Atif Aziz. 2019. The impact of social network marketing on consumer purchase intention in Pakistan: A study on female apparel. Management Science Letters 9: 1093–104. [Google Scholar] [CrossRef]

- Jöreskog, Karl G. 1971. Simultaneous factor analysis in several populations. Psychometrika 36: 409–26. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1988. Prospect theory: An analysis of decision under risk. In Decision, Probability and Utility, 1st ed. Edited by P. Gärdenfors and N.-E. Sahlin. Cambridge: Cambridge University Press, pp. 183–214. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, Daniel, and Dan Lovallo. 1993. Timid Choices and Bold Forecasts: A Cognitive Perspective on Risk Taking. Management Science 39: 17–31. [Google Scholar] [CrossRef]

- Kannadhasan, M., S. Aramvalarthan, S. K. Mitra, and Vinay Goyal. 2016. Relationship between Biopsychosocial Factors and Financial Risk Tolerance: An Empirical Study. The Journal for Decision Makers 41: 117–31. [Google Scholar] [CrossRef]

- Kappal, Jyoti, and Shailesh Rastogi. 2020. Investment behaviour of women entrepreneurs. Qualitative Research in Financial Markets 12: 485–504. [Google Scholar] [CrossRef]

- Khresna Brahmana, Rayenda, Chee-Wooi Hooy, and Zamri Ahmad. 2012. Psychological factors on irrational financial decision making: Case of day-of-the week anomaly. Humanomics 28: 236–57. [Google Scholar] [CrossRef] [Green Version]

- Kumar, Satish, and Nisha Goyal. 2015. Behavioural biases in investment decision making—A systematic literature review. Qualitative Research in Financial Markets 7: 88–108. [Google Scholar] [CrossRef]

- Kumar, Satish, Nisha Goyal, and Rituparna Basu. 2018. Profiling emerging market investors: A segmentation approach. International Journal of Bank Marketing 36: 441–55. [Google Scholar] [CrossRef]

- Lakshmi, B. 2015. Factors affecting the investment behaviour of women. International Journal in Management & Social Science 3: 185–97. [Google Scholar]

- Lassoued, Awad, and R. Guirat. 2020. The impact of managerial empowerment on problem solving and decision making skills: The case of Abu Dhabi University. Management Science Letters 10: 769–80. [Google Scholar] [CrossRef]

- Lee, Charles, Andrei Shleifer, and Richard Thaler. 1991. Investor Sentiment and the Closed-End Fund Puzzle. The Journal of Finance 46: 75–109. [Google Scholar] [CrossRef]

- Liao, Li, Jing Jian Xiao, Weiqiang Zhang, and Congyi Zhou. 2017. Financial literacy and risky asset holdings: Evidence from China. Accounting and Finance 57: 1383–415. [Google Scholar] [CrossRef]

- Litt, Mark, Howard Tennen, Glenn Affleck, and Susan Klock. 1992. Coping and Cognitive factors in adaptation toin vitro fertilization failure. Journal of Behavioural Medicine 15: 171–87. [Google Scholar] [CrossRef]

- Marín, Longinos, Catalina Nicolás, and Alicia Rubio. 2019. How Gender, Age and Education Influence the Entrepreneur’s Social Orientation: The Moderating Effect of Economic Development. Sustainability 11: 4514. [Google Scholar] [CrossRef] [Green Version]

- Mayfield, Cliff, Grady Perdue, and Kevin Wooten. 2008. Investment management and personality type. Financial Services Review 17: 219–36. [Google Scholar]

- McColl-Kennedy, Janet, and Ronald Anderson. 2005. Subordinate manager gender combination and perceived leadership style influence on emotions, self-esteem and organizational commitment. Journal of Business Research 58: 115–25. [Google Scholar] [CrossRef]

- McKay, Ruth. 2001. Women entrepreneurs: Moving beyond family and flexibility. International Journal of Entrepreneurial Behaviour and Research 7: 148–65. [Google Scholar] [CrossRef]

- Mishra, K. C., and Mary J. Metilda. 2015. A study on the impact of investment experience, gender, and level of education on overconfidence and self-attribution bias. IIMB Management Review 27: 228–39. [Google Scholar] [CrossRef] [Green Version]

- Muhammad, Said, Ximei Kong, Shahab Saqib, and Nicholas Beutell. 2021. Entrepreneurial Income and Wellbeing: Women’s Informal Entrepreneurship in a Developing Context. Sustainability 13: 10262. [Google Scholar] [CrossRef]

- Nath, Leda, Lori Holder-Webb, and Jeffrey Cohen. 2013. Will Women Lead the Way? Differences in Demand for Corporate Social Responsibility Information for Investment Decisions. Journal of Business Ethics 118: 85–102. [Google Scholar] [CrossRef]

- Nigam, Rupali Misra, Sumita Srivastava, and Devinder Kumar Banwet. 2018. Behavioral mediators of financial decision making—A state-of-art literature review. Review of Behavioral Finance 10: 2–41. [Google Scholar] [CrossRef]

- Pandian, Alagu, and G. Thangadurai. 2013. A Study of Investors Preference towards Various Investments Avenues in Dehradun District. International Journal of Management and Social Sciences Research (IJMSSR) 2: 10. [Google Scholar]

- Parsaeemehr, Mahsa, Farzin Rezeai, and Darshana Sedera. 2013. Personality type of investors and perception of financial information to make decisions. Asian Economic and Financial Review 11: 283–293. [Google Scholar]

- Pompian, Michael M. 2006. Behavioral Finance and Wealth Management: How to Build Optimal Portfolios that Account for Investor Biases. Hoboken: John Wiley & Sons. [Google Scholar]

- Rashid, Sumayya, and Vanessa Ratten. 2020. Commodifying skills for survival among artisan entrepreneurs in Pakistan. International Entrepreneurship and Management Journal 17: 1091–1110. [Google Scholar] [CrossRef]

- Rigdon, Edward E. 2012. Rethinking partial least squares path modeling: In praise of simple methods. Long Range Planning 45: 341–58. [Google Scholar] [CrossRef]

- Ritter, Jay R. 2003. Behavioral finance. Pacific-Basin Finance Journal 11: 429–37. [Google Scholar] [CrossRef]

- Sahi, Shalini Kalra, Ashok Pratap Arora, and Nand Dhameja. 2013. An Exploratory Inquiry into the Psychological Biases in Financial Investment Behavior. Journal of Behavioral Finance 14: 94–103. [Google Scholar] [CrossRef]

- Sajjad, Muhammad, Nishat Kaleem, Muhammad Irfan Chani, and Munir Ahmed. 2020. Worldwide role of women entrepreneurs in economic development. Asia Pacific Journal of Innovation and Entrepreneurship 14: 151–60. [Google Scholar] [CrossRef]

- Salim, Ansa Savad, Mohammed Ahmed Hamood Al Jahdhami, and S. N. S. A. Al Handhali. 2016. A study on Customer preferences towards selected local Omani (FMCG) products. International Journal of Science and Research (IJSR) 6: 1273–77. [Google Scholar]

- Salim, Ansa, and Sania Khan. 2020. The effects of factors on making investment decisions among Omani working women. Accounting. Accounting 6: 657–64. [Google Scholar] [CrossRef]

- Sarkar, Arup Kumar, and Tarak Nath Sahu. 2018. Investment Behaviour: Towards an Individual-Centred Financial Policy in Developing Economies. Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Shakeel, Muhammad, Yaokuang Li, and Ali Gohar. 2020. Identifying the Entrepreneurial Success Factors and the Performance of Women-Owned Businesses in Pakistan: The Moderating Role of National Culture. SAGE Open 10. [Google Scholar] [CrossRef]

- Shiller, Robert J. 2000. Measuring Bubble Expectations and Investor Confidence. Journal of Psychology and Financial Markets 1: 49–60. [Google Scholar] [CrossRef]

- Shiller, Robert, and John Pound. 1989. Survey evidence on diffusion of interest and information among investors. Journal of Economic Behavior and Organization 12: 47–66. [Google Scholar] [CrossRef]

- Shmueli, Galit, and Otto Koppius. 2011. Predictive Analytics in Information Systems Research. MIS Quarterly 35: 553–72. [Google Scholar] [CrossRef] [Green Version]

- Son, JeongWook, and Eddy Rojas. 2011. Impact of Optimism Bias Regarding Organizational Dynamics on Project Planning and Control. Journal of Construction Engineering and Management 137: 147–57. [Google Scholar] [CrossRef]

- Soomro, Bahadur Ali, Hassan Almahdi, and Naimatullah Shah. 2020. Perceptions of young entrepreneurial aspirants towards sustainable entrepreneurship in Pakistan. Kybernetes 50: 2134–54. [Google Scholar] [CrossRef]

- Stefan, Daniel, Valentina Vasile, Anca Oltean, Calin-Adrian Comes, Anamari-Beatrice Stefan, Liviu Ciucan-Rusu, Elena Bunduchi, Maria-Alexandra Popa, and Mihai Timus. 2021. Women Entrepreneurship and Sustainable Business Development: Key Findings from a SWOT–AHP Analysis. Sustainability 13: 5298. [Google Scholar] [CrossRef]

- Stolper, Oscar. 2018. It takes two to Tango: Households’ response to financial advice and the role of financial literacy. Journal of Banking and Finance 92: 295–310. [Google Scholar] [CrossRef]

- Tang, Ning, and Andrew Baker. 2016. Self-esteem, financial knowledge and financial behavior. Journal of Economic Psychology 54: 164–76. [Google Scholar] [CrossRef]

- Thaler, Richard H. 2008. Mental accounting and consumer choice. Marketing Science 27: 15–25. [Google Scholar] [CrossRef] [Green Version]

- Trevelyan, Rose. 2008. Optimism, overconfidence and entrepreneurial activity. Management Decision 46: 986–1001. [Google Scholar] [CrossRef]

- Van Rooij, Maarten, Annamaria Lusardi, and Rob Alessie. 2011. Financial literacy and stock market participation. Journal of Financial Economics 101: 449–72. [Google Scholar] [CrossRef] [Green Version]

- Van Truong, Doan, Nguyen Giao, and Le Thi Thuy Ly. 2020. Factors affecting the role of women in the economic development of rural household families in Vietnam: A case study in Trieu Son district Thanh Hoa province. Accounting 6: 267–72. [Google Scholar] [CrossRef]

- Webley, Paul, and Ellen Nyhus. 2006. Parents’ influence on children’s future orientation and saving. Journal of Economic Psychology 27: 140–64. [Google Scholar] [CrossRef]

- Wetzels, Martin, Gaby Odekerken-Schröder, and Claudia Van Oppen. 2009. Using PLS path modelling for assessing hierarchical construct models: Guidelines and empirical illustration. MIS Quarterly 33: 177–95. [Google Scholar] [CrossRef]

- Wing Yan Man, Thomas. 2006. Exploring the behavioural patterns of entrepreneurial learning: A competency approach. Education & Training 48: 309–21. [Google Scholar] [CrossRef]

- Yaqoob, Samina. 2020. The Emerging trend Women entrepreneurship in Pakistan: Women entrepreneurship. Journal of Arts and Social Sciences 7: 217–30. [Google Scholar] [CrossRef]

- Zahera, Syed Aliya, and Rohit Bansal. 2018. Do investors exhibit behavioural biases in investment decision making? A systematic review. Qualitative Research in Financial Markets 10: 210–51. [Google Scholar] [CrossRef]

- Zeb, Arooj, and Anjum Ihsan. 2020. Innovation and the entrepreneurial performance in women-owned small and medium-sized enterprises in Pakistan. Women’s Studies International Forum 79: 102342. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Profile | Karachi % | Lahore % |

|---|---|---|

| Age (in Years) | ||

| 25 to 30 | 15% | 20% |

| 31 to 35 | 25% | 19% |

| 36 to 40 | 26% | 45% |

| Above 40 | 34% | 16% |

| Marital Status | ||

| Unmarried | 10% | 7% |

| Married | 30% | 35% |

| Divorced | 5% | 16% |

| Widow | 55% | 42% |

| Qualification | ||

| Non-Graduate | 12% | 13% |

| Graduate | 14% | 26% |

| Post Graduate | 67% | 56% |

| PhD | 7% | 5% |

| Experience (in Years) | ||

| 1 to 5 | 8% | 11% |

| 6 to 10 | 26% | 36% |

| 11 to 15 | 33% | 23% |

| 16 to 20 | 28% | 20% |

| Above 20 | 5% | 10% |

| Income After Tax (000) | ||

| Rs. 100 and above | 4% | 3% |

| Rs. 300 and above | 8% | 6% |

| Rs. 500 and above | 30% | 25% |

| Rs. 700 and above | 27% | 21% |

| Rs. 900 and above | 31% | 45% |

| Where n = 330 | n = 178 | n = 152 |

| 54% | 46% |

| Constructs | CR | AVE | Items | Factor Loadings |

|---|---|---|---|---|

| Behavioral Factors | 0.832 | 0.625 | BF 1 | 0.884 |

| BF 2 | 0.751 | |||

| BF 3 | 0.727 | |||

| Investment Attitude | 1.000 | 1.000 | IA 1 | 1.000 |

| Personal Factors | 0.765 | 0.523 | PF 1 | 0.631 |

| PF 2 | 0.713 | |||

| PF 3 | 0.814 | |||

| Social Factors | 0.810 | 0.587 | SF 1 | 0.802 |

| SF 2 | 0.734 | |||

| SF 3 | 0.761 | |||

| Uncertainty | 0.854 | 0.596 | UN 1 | 0.736 |

| UN 2 | 0.783 | |||

| UN 3 | 0.846 | |||

| UN 4 | 0.716 | |||

| Women Investment Decisions | 0.834 | 0.628 | WID 1 | 0.759 |

| WID 2 | 0.863 | |||

| WID 3 | 0.749 |

| BF | IA | PF | SF | UN | WID | |

|---|---|---|---|---|---|---|

| Behavioral Factors | 0.790 | |||||

| Investment Attitude | 0.577 | 1.000 | ||||

| Personal Factors | 0.754 | 0.475 | 0.723 | |||

| Social Factors | 0.791 | 0.814 | 0.624 | 0.766 | ||

| Uncertainty | 0.803 | 0.823 | 0.991 | 0.491 | 0.772 | |

| Women Investment Decisions | 0.732 | 0.752 | 0.516 | 0.67 | 0.592 | 0.792 |

| Indicators | VIF |

|---|---|

| SF 1 | 1.959 |

| SF 2 | 1.642 |

| SF 3 | 1.780 |

| PF 1 | 1.502 |

| PF 2 | 1.543 |

| PF 3 | 1.609 |

| BF 1 | 1.945 |

| BF 2 | 2.000 |

| BF 3 | 1.811 |

| IA 1 | 1.000 |

| Investment Attitude * Uncertainty | 1.000 |

| UN 1 | 3.122 |

| UN 2 | 1.474 |

| UN 3 | 1.751 |

| UN 4 | 3.706 |

| WID 1 | 1.802 |

| WID 2 | 2.564 |

| WID 3 | 1.933 |

| Construct | R-Square |

|---|---|

| Women Investment Decisions | 0.637 |

| Hypothesis | STDEV | T-Values | p-Values | Decisions |

|---|---|---|---|---|

| H1: SF -> IA -> WID | 0.09 | 3.597 | 0.000 | Supported |

| H2: PF -> IA -> WID | 0.08 | 1.377 | 0.169 | Not Supported |

| H3: BF -> IA -> WID | 0.075 | 2.173 | 0.030 | Supported |

| H4: IA -> IA * UN -> WID | 0.037 | 1.733 | 0.084 | Not Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hussain, B.M.; Baig, U.; Davidaviciene, V.; Meidute-Kavaliauskiene, I. A Thoughtful Insight on Women Entrepreneur’s Investment Attitude. Economies 2021, 9, 187. https://doi.org/10.3390/economies9040187

Hussain BM, Baig U, Davidaviciene V, Meidute-Kavaliauskiene I. A Thoughtful Insight on Women Entrepreneur’s Investment Attitude. Economies. 2021; 9(4):187. https://doi.org/10.3390/economies9040187

Chicago/Turabian StyleHussain, Batool Muhammad, Umair Baig, Vida Davidaviciene, and Ieva Meidute-Kavaliauskiene. 2021. "A Thoughtful Insight on Women Entrepreneur’s Investment Attitude" Economies 9, no. 4: 187. https://doi.org/10.3390/economies9040187

APA StyleHussain, B. M., Baig, U., Davidaviciene, V., & Meidute-Kavaliauskiene, I. (2021). A Thoughtful Insight on Women Entrepreneur’s Investment Attitude. Economies, 9(4), 187. https://doi.org/10.3390/economies9040187