Do Commodities React More to Time-Varying Rare Disaster Risk? A Comparison of Commodity and Financial Assets

Abstract

:1. Introduction

2. Literature Review

3. Econometric Methodology

3.1. Time-Varying Parameter VAR Model

3.2. Nonparametric Causality-in-Quantiles Method

4. Data and Preliminary Analysis

4.1. Measure of Rare Disaster Risk

4.2. Data of Asset Prices

4.3. Preliminary Analysis

5. Empirical Results

5.1. Impact of Rare Disaster Risk on Asset Prices

5.1.1. Variance Decomposition Results

5.1.2. Time-Varying Impulse Response Analysis

5.1.3. Impulse Response Analysis of Typical Episodes

5.2. Causal Relationship between Rare Disaster Risk and Asset Prices

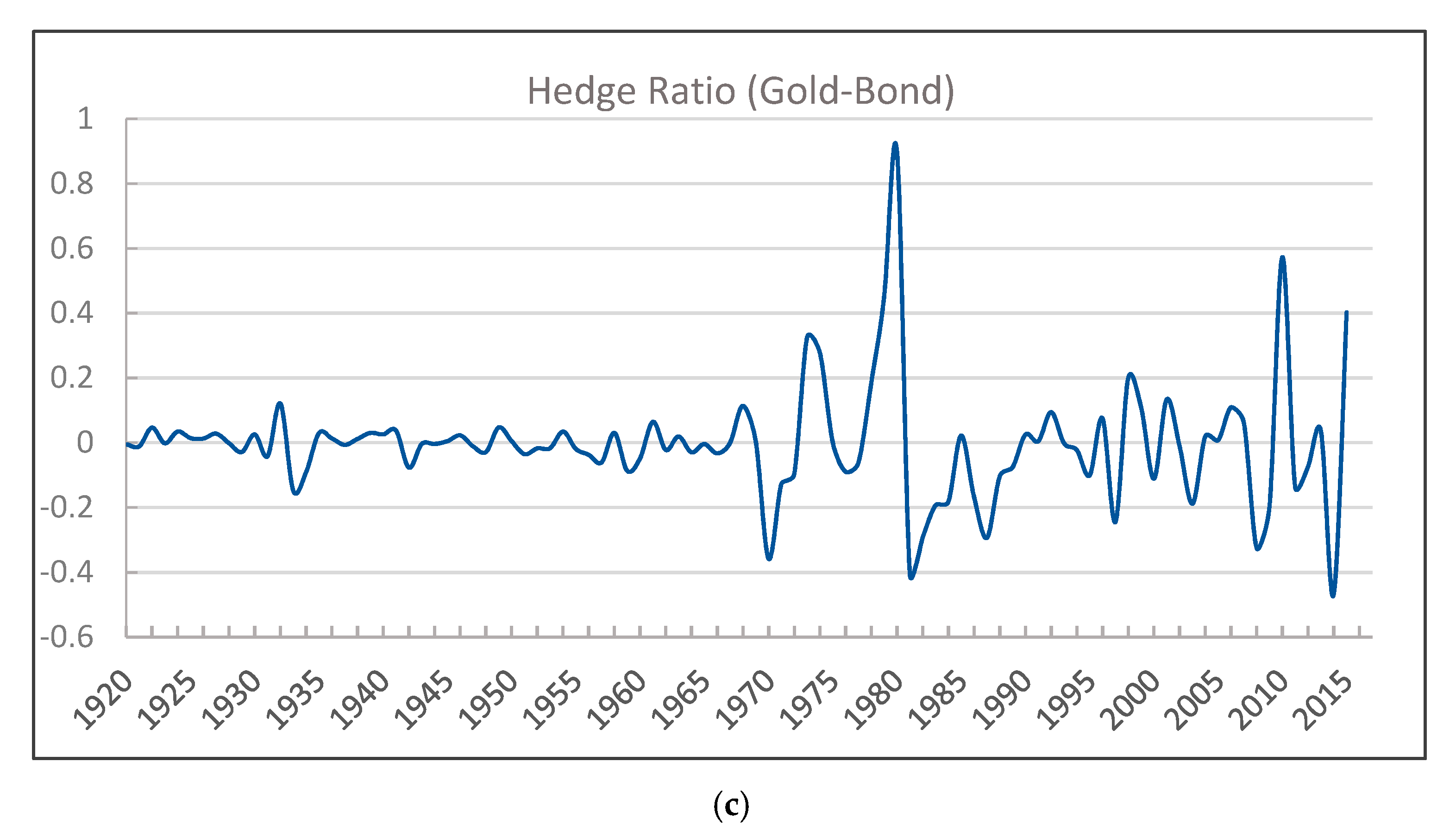

5.3. Implications for Portfolio Diversification

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rietz, T.A. The equity risk premium a solution. J. Monet. Econ. 1988, 22, 117–131. [Google Scholar] [CrossRef]

- Gabaix, X. Variable Rare Disasters: A Tractable Theory of Ten Puzzles in Macro-Finance. Am. Econ. Rev. 2008, 98, 64–67. [Google Scholar] [CrossRef] [Green Version]

- Barro, R.J. Rare disasters and asset markets in the twentieth century. Q. J. Econ. 2006, 121, 823–866. [Google Scholar] [CrossRef]

- Gabaix, X. Variable Rare Disasters: An Exactly Solved Framework for Ten Puzzles in Macro-Finance. Q. J. Econ. 2012, 127, 645–700. [Google Scholar] [CrossRef] [Green Version]

- Veronesi, P. The Peso problem hypothesis and stock market returns. J. Econ. Dyn. Control 2004, 28, 707–725. [Google Scholar] [CrossRef]

- Berkman, H.; Jacobsen, B.; Lee, J.B. Time-varying rare disaster risk and stock returns. J. Financ. Econ. 2011, 101, 313–332. [Google Scholar] [CrossRef]

- Wachter, J.A. Can time-varying risk of rare disasters explain aggregate stock market volatility? J. Financ. 2013, 68, 987–1035. [Google Scholar] [CrossRef] [Green Version]

- Seo, S.B.; Wachter, J.A. Option prices in a model with stochastic disaster risk. Manag. Sci. 2019, 65, 3449–3469. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Q. One hundred years of rare disaster concerns and commodity prices. J. Futures Mark. 2021, 41, 1891–1915. [Google Scholar] [CrossRef]

- Farhi, E.; Gabaix, X. Rare Disasters and Exchange Rates. Q. J. Econ. 2016, 131, 1–52. [Google Scholar] [CrossRef] [Green Version]

- Berkman, H.; Jacobsen, B.; Lee, J.B. Rare disaster risk and the expected equity risk premium. Account. Financ. 2015, 57, 351–372. [Google Scholar] [CrossRef]

- Lee, C.C.; Lee, C.C.; Li, Y.Y. Oil price shocks, geopolitical risks, and green bond market dynamics. N. Am. J. Econ. Financ. 2021, 55, 101309. [Google Scholar] [CrossRef]

- Demirer, R.; Gupta, R.; Suleman, T.; Wohar, M.E. Time-varying rare disaster risks, oil returns and volatility. Energy Econ. 2018, 75, 239–248. [Google Scholar] [CrossRef] [Green Version]

- Cunado, J.; Gupta, R.; Lau, C.K.M.; Sheng, X. Time-Varying Impact of Geopolitical Risks on Oil Prices. Def. Peace Econ. 2020, 31, 692–706. [Google Scholar] [CrossRef]

- Gkillas, K.; Gupta, R.; Pierdzioch, C. Forecasting (downside and upside) realized exchange-rate volatility: Is there a role for realized skewness and kurtosis? Phys. A Stat. Mech. Appl. 2019, 532, 121867. [Google Scholar] [CrossRef]

- Salisu, A.A.; Cunado, J.; Gupta, R. Geopolitical risks and historical exchange rate volatility of the BRICS. Int. Rev. Econ. Financ. 2022, 77, 179–190. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Liu, L.; Wang, E.Z.; Lee, C.C. Impact of the COVID-19 pandemic on the crude oil and stock markets in the US: A time-varying analysis. Energy Res. Lett. 2020, 1, 13154. [Google Scholar] [CrossRef]

- Umar, Z.; Jareño, F.; Escribano, A. Dynamic return and volatility connectedness for dominant agricultural commodity markets during the COVID-19 pandemic era. Appl. Econ. 2021, 1–25. [Google Scholar] [CrossRef]

- Barro, R.J.; Jin, T. On the Size Distribution of Macroeconomic Disasters. Econometrica 2011, 79, 1567–1589. [Google Scholar] [CrossRef] [Green Version]

- Balcilar, M.; Bekiros, S.; Gupta, R. The role of news-based uncertainty indices in predicting oil markets: A hybrid nonparametric quantile causality method. Empir. Econ. 2017, 53, 879–889. [Google Scholar] [CrossRef] [Green Version]

- Gourio, F. Time-Varying Risk of Disaster, Time-Varying Risk Premia, and Macroeconomic Dynamics. In Time-Varying Risk Premia, and Macroeconomic Dynamics (18 March 2009); SSRN: New York, NY, USA, 2009. [Google Scholar]

- Gourio, F.; Siemer, M.; Verdelhan, A. International risk cycles. J. Int. Econ. 2013, 89, 471–484. [Google Scholar] [CrossRef] [Green Version]

- Tsai, J.; Wachter, J.A. Rare booms and disasters in a multisector endowment economy. Rev. Financ. Stud. 2016, 29, 1113–1169. [Google Scholar] [CrossRef] [Green Version]

- Barro, R.J.; Misra, S. Gold Returns. Econ. J. 2016, 126, 1293–1317. [Google Scholar] [CrossRef]

- Barro, R.J.; Liao, G.Y. Rare disaster probability and options pricing. J. Financ. Econ. 2021, 139, 750–769. [Google Scholar] [CrossRef]

- Skoufias, E. Economic Crises and Natural Disasters: Coping Strategies and Policy Implications. World Dev. 2003, 31, 1087–1102. [Google Scholar] [CrossRef]

- Huang, T.; Wu, F.; Yu, J.; Zhang, B. Political risk and dividend policy: Evidence from international political crises. J. Int. Bus. Stud. 2015, 46, 574–595. [Google Scholar] [CrossRef]

- Meng, Y.W.; Imran, M.; Zakaria, M.; Linrong, Z.; Farooq, M.U.; Muhammad, S.K. Impact of terrorism and political instability on equity premium: Evidence from Pakistan. Phys. A Stat. Mech. Appl. 2018, 492, 1753–1762. [Google Scholar] [CrossRef]

- Gkillas, K.; Floros, C.; Suleman, M.T. Quantile dependencies between discontinuities and time-varying rare disaster risks. Eur. J. Financ. 2021, 27, 932–962. [Google Scholar] [CrossRef]

- Gupta, R.; Suleman, T.; Wohar, M.E. The role of time-varying rare disaster risks in predicting bond returns and volatility. Rev. Financ. Econ. 2019, 37, 327–340. [Google Scholar] [CrossRef]

- van Eyden, R.; Gupta, R.; Nel, J.; Bouri, E. Rare Disaster Risks and Volatility of the Term-Structure of US Treasury Securities: The Role of El Nino and La Nina Events (No. 202155); Dept. of Economics Working Paper Series; University of Pretoria: Pretoria, South Africa, 2021. [Google Scholar]

- Demirer, R.; Gupta, R.; Nel, J.; Pierdzioch, C. Effect of rare disaster risks on crude oil: Evidence from El Niño from over 145 years of data. Theor. Appl. Climatol. 2021, 147, 691–699. [Google Scholar] [CrossRef]

- Adekoya, O.B.; Oliyide, J.A. How COVID-19 drives connectedness among commodity and financial markets: Evidence from TVP-VAR and causality-in-quantiles techniques. Resour. Policy 2020, 70, 101898. [Google Scholar] [CrossRef] [PubMed]

- Bissoondoyal-Bheenick, E.; Do, H.; Hu, X.; Zhong, A. Learning from SARS: Return and volatility connectedness in COVID-19. Financ. Res. Lett. 2021, 41, 101796. [Google Scholar] [CrossRef] [PubMed]

- Mensi, W.; Sensoy, A.; Vo, X.V.; Kang, S.H. Impact of COVID-19 outbreak on asymmetric multifractality of gold and oil prices. Resour. Policy 2020, 69, 101829. [Google Scholar] [CrossRef] [PubMed]

- Harjoto, M.A.; Rossi, F.; Lee, R.; Sergi, B.S. How do equity markets react to COVID-19? Evidence from emerging and developed countries. J. Econ. Bus. 2021, 115, 105966. [Google Scholar] [CrossRef] [PubMed]

- Primiceri, G.E. Time varying structural vector autoregressions and monetary policy. Rev. Econ. Stud. 2005, 72, 821–852. [Google Scholar] [CrossRef]

- Nakajima, J. Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Monet. Econ. Stud. 2011, 29, 107–142. [Google Scholar]

- Degiannakis, S.; Filis, G.; Panagiotakopoulou, S. Oil price shocks and uncertainty: How stable is their relationship over time? Econ. Model. 2018, 72, 42–53. [Google Scholar] [CrossRef] [Green Version]

- Paul, P. The time-varying effect of monetary policy on asset prices. Rev. Econ. Stat. 2020, 102, 690–704. [Google Scholar] [CrossRef] [Green Version]

- Nishiyama, Y.; Hitomi, K.; Kawasaki, Y.; Jeong, K. A consistent nonparametric test for nonlinear causality—Specification in time series regression. J. Econ. 2011, 165, 112–127. [Google Scholar] [CrossRef] [Green Version]

- Jebabli, I.; Arouri, M.; Teulon, F. On the effects of world stock market and oil price shocks on food prices: An empirical investigation based on TVP-VAR models with stochastic volatility. Energy Econ. 2014, 45, 66–98. [Google Scholar] [CrossRef]

- Chib, S.; Greenberg, E. Hierarchical analysis of SUR models with extensions to correlated serial errors and time-varying parameter models. J. Econ. 1995, 68, 339–360. [Google Scholar] [CrossRef]

- Chib, S. Markov Chain Monte Carlo Methods: Computation and Inference. Handb. Econom. 2001, 5, 3569–3649. [Google Scholar] [CrossRef]

- Kim, S.; Shepherd, N.; Chib, S. Stochastic Volatility: Likelihood Inference and Comparison with ARCH Models. Rev. Econ. Stud. 1998, 65, 361–393. [Google Scholar] [CrossRef]

- Omori, Y.; Chib, S.; Shephard, N.; Nakajima, J. Stochastic volatility with leverage: Fast and efficient likelihood inference. J. Econ. 2007, 140, 425–449. [Google Scholar] [CrossRef] [Green Version]

- Jeong, K.; Härdle, W.K.; Song, S. A consistent nonparametric test for causality in quantile. Econ. Theory 2012, 28, 861–887. [Google Scholar] [CrossRef] [Green Version]

- Sim, N.; Zhou, H. Oil prices, US stock return, and the dependence between their quantiles. J. Bank. Financ. 2015, 55, 1–8. [Google Scholar] [CrossRef]

- Baur, D.G.; Lucey, B.M. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financ. Rev. 2010, 45, 217–229. [Google Scholar] [CrossRef]

- Goyenko, R.Y.; Ukhov, A.D. Stock and bond market liquidity: A long-run empirical analysis. J. Financ. Quant. Anal. 2009, 44, 189–212. [Google Scholar] [CrossRef] [Green Version]

- Lieber, R.J. Oil and power after the Gulf War. Int. Secur. 1992, 17, 155–176. [Google Scholar] [CrossRef]

- Rigobon, R.; Sack, B. The effects of war risk on US financial markets. J. Bank. Financ. 2005, 29, 1769–1789. [Google Scholar] [CrossRef] [Green Version]

- Leigh, A.; Wolfers, J.; Zitzewitz, E. What Do Financial Markets Think of War in Iraq? Working Paper No. 9587; National Bureau of Economic Research: Cambridge, MA, USA, 2003. [Google Scholar] [CrossRef]

- Urquhart, A. An Empirical Analysis of the Adaptive Market Hypothesis and Investor Sentiment in Extreme Circumstances. Doctoral Dissertation, Newcastle University, Newcastle, UK, 2013. [Google Scholar]

- Kroner, K.F.; Ng, V.K. Modeling asymmetric movement of asset prices. Rev. Financ. Stud. 1998, 11, 844–871. [Google Scholar] [CrossRef]

- Kroner, K.F.; Sultan, J. Time-Varying Distributions and Dynamic Hedging with Foreign Currency Futures. J. Financ. Quant. Anal. 1993, 28, 535. [Google Scholar] [CrossRef]

- Ku, Y.H.H.; Chen, H.C.; Chen, K. On the application of the dynamic conditional correlation model in estimating optimal time-varying hedge ratios. Appl. Econ. Lett. 2007, 14, 503–509. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Description | Value |

|---|---|---|

| BREAK ) | Crisis that began with a violent act | value 9: Violent act |

| VIOL ) | Violence used during the crisis or full-scale wars | value 3: Serious clashes; value 4: Full-scale wars. |

| WAR ) | Full-scale wars | value 4: Full-scale wars. |

| GRAVCR ) | Subset of “Gravity of value threat”—grave threat | value 3: Territorial threat; value 5: Threat of grave damage; value 6: Threat to existence. |

| PROTRAC ) | - | value 3: Long power protracted conflict. |

| GPINV ) | Great power or Superpower is involved on both sides of conflict | value 3: One or more powers high involvement; value 4: One or two powers as crisis actors, the others low or no involvement; value 5: One or two powers as crisis actor, the others high, low or no involvement; value 6: More than two powers as crisis actors, the other low or no involvement; value 7: More than two powers as crisis actors, the other high, low or no involvement |

| Variables | BREAK | VIOL | WAR | GRAVCR | MAJPOW | PROTRAC |

|---|---|---|---|---|---|---|

| Total | 194 | 211 | 83 | 258 | 159 | 66 |

| Mean | Median | Max | Min | Std. Dev. | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| CSI | 62.316 | 54.500 | 279.000 | 0.000 | 43.737 | 1.797 | 9.126 |

| Returns | |||||||

| Stock | 5.466 | 8.970 | 39.649 | −65.508 | 18.775 | −0.978 | 4.507 |

| Bond | −0.827 | 0.405 | 40.372 | −54.280 | 16.400 | −0.297 | 4.005 |

| Oil | 3.586 | 0.000 | 125.839 | −64.706 | 26.118 | 0.774 | 8.191 |

| Gold | 4.197 | 0.048 | 69.804 | −29.040 | 15.400 | 1.421 | 6.658 |

| Period | Stock | Bond | Oil | Gold |

|---|---|---|---|---|

| 1 | 0.39 | 0.00 | 3.23 | 0.36 |

| 2 | 0.40 | 2.19 | 3.14 | 1.49 |

| 3 | 8.08 | 2.01 | 2.74 | 2.57 |

| 4 | 10.09 | 2.58 | 2.69 | 4.15 |

| 5 | 10.02 | 2.46 | 7.34 | 3.93 |

| 10 | 13.17 | 2.79 | 9.70 | 4.55 |

| 15 | 13.04 | 2.93 | 9.83 | 4.85 |

| 20 | 13.07 | 2.97 | 9.85 | 4.85 |

| 25 | 13.07 | 2.97 | 9.85 | 4.85 |

| 30 | 13.07 | 2.97 | 9.85 | 4.85 |

| Parameter | Mean | Std Dev. | 95% U | 95% L | Geweke CD | Inefficiency |

|---|---|---|---|---|---|---|

| 0.2305 | 0.0414 | 0.1575 | 0.32 | 0.734 | 14.13 | |

| 0.0023 | 0.0003 | 0.0018 | 0.0029 | 0.078 | 5.35 | |

| 0.0059 | 0.0017 | 0.0035 | 0.0102 | 0.243 | 40.69 | |

| 0.0087 | 0.0032 | 0.0043 | 0.0166 | 0.000 | 87.62 | |

| 0.0055 | 0.0015 | 0.0034 | 0.0094 | 0.812 | 27.09 | |

| 0.0056 | 0.0017 | 0.0034 | 0.0101 | 0.971 | 39.11 |

| Quantiles | Stock–Mean | Stock–Variance | Bond–Mean | Bond–Variance | Oil–Mean | Oil–Variance | Gold–Mean | Gold–Variance |

|---|---|---|---|---|---|---|---|---|

| 0.05 | 0.04 | 1.64 | 0.00 | 1.38 | 0.79 | 5.74 | 0.15 | 3.93 |

| 0.1 | 0.00 | 2.36 | 0.04 | 1.65 | 1.44 | 3.89 | 0.19 | 2.95 |

| 0.15 | 0.01 | 2.50 | 0.00 | 1.73 | 1.12 | 3.19 | 0.13 | 3.00 |

| 0.2 | 0.01 | 2.84 | 0.01 | 2.06 | 1.13 | 3.16 | 0.18 | 3.14 |

| 0.25 | 0.01 | 3.44 | 0.01 | 2.01 | 1.06 | 3.18 | 0.20 | 3.05 |

| 0.3 | 0.01 | 3.40 | 0.01 | 2.26 | 1.00 | 3.19 | 0.28 | 3.13 |

| 0.35 | 0.02 | 3.30 | 0.02 | 2.71 | 0.99 | 3.39 | 0.20 | 3.63 |

| 0.4 | 0.00 | 3.39 | 0.02 | 2.44 | 2.96 | 3.35 | 0.10 | 3.75 |

| 0.45 | 0.03 | 3.30 | 0.03 | 2.49 | 1.94 | 3.29 | 0.71 | 3.60 |

| 0.5 | 0.00 | 3.16 | 0.00 | 2.42 | 1.25 | 3.23 | 0.23 | 3.17 |

| 0.55 | 0.01 | 3.03 | 0.01 | 3.05 | 0.77 | 3.18 | 0.19 | 2.89 |

| 0.6 | 0.01 | 3.03 | 0.01 | 2.67 | 0.82 | 3.33 | 0.40 | 2.74 |

| 0.65 | 0.01 | 2.99 | 0.00 | 2.57 | 0.73 | 3.11 | 0.24 | 2.50 |

| 0.7 | 0.02 | 2.64 | 0.00 | 2.56 | 0.45 | 2.97 | 0.66 | 2.11 |

| 0.75 | 0.03 | 2.38 | 0.03 | 2.42 | 0.80 | 2.51 | 1.24 | 2.00 |

| 0.8 | 0.04 | 2.34 | 0.00 | 1.95 | 0.89 | 2.35 | 0.66 | 1.58 |

| 0.85 | 0.00 | 1.76 | 0.01 | 1.66 | 0.72 | 2.32 | 0.54 | 1.25 |

| 0.9 | 0.01 | 1.46 | 0.00 | 1.19 | 0.38 | 1.91 | 0.61 | 0.99 |

| 0.95 | 0.00 | 1.42 | 0.02 | 0.66 | 0.26 | 1.71 | 0.19 | 0.33 |

| Stock | Bond | Oil | Gold | |

|---|---|---|---|---|

| Mean | - | - | 0.35–0.45 | - |

| Variance | 0.10–0.85 | 0.20–0.80 | 0–0.85 | 0–0.75 |

| Portfolios | |||

|---|---|---|---|

| Gold–Stock | 0.588 | 0.412 | −0.009 |

| Gold–Oil | 0.652 | 0.348 | 0.099 |

| Gold–Bond | 0.727 | 0.273 | −0.004 |

| Portfolios | Gold–Stock | Gold–Oil | Gold–Bond |

|---|---|---|---|

| Variance | 0.013 | 0.026 | 0.014 |

| HE | 0.443 | −0.113 | 0.397 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, P.; Huang, T. Do Commodities React More to Time-Varying Rare Disaster Risk? A Comparison of Commodity and Financial Assets. Mathematics 2022, 10, 445. https://doi.org/10.3390/math10030445

Chen P, Huang T. Do Commodities React More to Time-Varying Rare Disaster Risk? A Comparison of Commodity and Financial Assets. Mathematics. 2022; 10(3):445. https://doi.org/10.3390/math10030445

Chicago/Turabian StyleChen, Peng, and Ting Huang. 2022. "Do Commodities React More to Time-Varying Rare Disaster Risk? A Comparison of Commodity and Financial Assets" Mathematics 10, no. 3: 445. https://doi.org/10.3390/math10030445

APA StyleChen, P., & Huang, T. (2022). Do Commodities React More to Time-Varying Rare Disaster Risk? A Comparison of Commodity and Financial Assets. Mathematics, 10(3), 445. https://doi.org/10.3390/math10030445