The evolution of economic models from input–output analysis to dynamic Computable General Equilibrium (CGE) models represents a significant advancement in the field of economic modeling, reflecting a progression toward greater complexity and realism.

Input–output analysis marked the beginning of this journey. It provided a mathematical framework for understanding the interdependencies between different economic sectors using linear equations. While this model offered insights into the structural characteristics of the economy, it was limited in scope, primarily capturing direct interdependencies among sectors and overlooking broader income-induced effects across markets.

Building on this, Linear General Equilibrium Models emerged, utilizing the social accounting matrix (SAM) framework. These models expanded the analytical scope to include all transactions of goods, services, and income among various agents and sectors, providing a more comprehensive view of economic flows. However, the linear nature of these models imposed constraints such as constant returns to scale and fixed relative prices, limiting their ability to reflect real-world economic complexities.

To address these limitations, applied general equilibrium models (AGEMs) were developed. AGE, with its non-linear mathematical structure, integrated more complex economic behaviors like optimization in competitive markets, substitution processes, and endogenous labor market dynamics. This model represented a significant leap in capturing the nuanced interactions and functions of various market sectors and economic institutions.

The dynamic CGE model represents the culmination of this evolution. It builds upon the foundations laid by the earlier models but surpasses their limitations by incorporating dynamic elements into the CGE framework. Utilizing the SAM as its database, the dynamic CGE model can simulate the evolution of an economy over time, factoring in changes in technology, demographics, and policy. This model’s ability to incorporate dynamic transitions and adjustments offers a more realistic and nuanced understanding of economic phenomena, representing the forefront of current economic modeling practices.

Upon estimating the social accounting matrix, a robust statistical framework is established. This framework not only facilitates the calculation of linear multipliers but also underpins the development of applied general equilibrium models. Specifically, the social accounting matrix for the Community of Madrid, as calculated for the year 2005, offers an appropriate database. This database is instrumental in simulating the mathematical model, effectively applying the formulated mathematical model to real-world scenarios.

The selection of the year 2005 for the social accounting matrix in this study was dictated by the availability of relevant data for the Madrid economy. Due to the absence of an official matrix, the 2005 matrix was constructed using the available macroeconomic data. The creation of such matrices is not straightforward and demands extensive research. Specifically for this model, the Madrid 2005 matrix was meticulously estimated, signifying a notable research endeavor. This process underscores the complexity and significance of accessing and utilizing databases in research. The primary objective of this specific exercise is to demonstrate that the mathematical model is functional and applicable, using an appropriate database. By choosing this particular set of data, the study acknowledges the ever-evolving nature of economies and prioritizes the model’s formulation over the mere assembly of a database, thus shedding light on the study’s core principles and inherent constraints.

The mathematical formulation of the mathematical program is encoded with a computational algorithm that will be solved using the GAMS® software (39.1.1). The dynamic CGE includes, among its assumptions, optimizing behavior in competitive markets and allows for the incorporation of substitution processes, an endogenous labor market, price incentives, and shadow prices, as well as technological differences between various sectors.

The simulation of the impact on the economy, in this case the Community of Madrid, allows for the analysis of the transformation of its productive structure as a result of an investment shock in each of the selected sectors.

3.2. Mathematical Formulation of the Dynamic Applied General Equilibrium Model

To achieve the goal of constructing applied models that accurately represent the most significant economic sectors and capture the unique features of the economy under study, the researcher’s approach centers around two main axes:

- -

The specification of the intervening agents and their assumed behavior.

- -

The definition or concept of equilibrium used.

Building upon these foundational aspects, policy impact simulation has recently evolved due to modern prospective tools such as dynamic CGE models for macroeconomic analysis. The original model is the Ramsey (1928) model and is the one which allowed Solow [

18] and Swan [

32] to develop the methodological basis of later models. They depicted the assumptions and hypotheses that are to be incorporated into such models to capture and synthesize agents’ behavior.

The mathematical foundations of dynamic modeling are summarized in [

33], so now we face the challenge of adapting and applying them to the wide range of situations that are given in real economies. Since modeling involves a certain degree of approximation to reality, these models are subject to continuous revision and updated. In the specific case of Madrid´s region, a social accounting matrix (SAM) referring to the year 2005 [

34] was constructed so that it provides the framework linking together the economic behavior of the representative aggregate agents.

The following figure (

Figure 2) can be observed for an overview of the problem statement and to summarize the analysis method applied in this work by means of the dynamic CGE model:

The present formulation of our dynamic CGE model is based on the rational expectations hypothesis of the agents; thus, the proposed architecture consists of a detailed sector breakdown where the main markets appear, as well as capital and labor.

The assumption of rational expectations in applied general equilibrium models is a crucial concept in modern economic theory. It refers to the hypothesis that agents within an economy—individuals, businesses, and other organizations—make decisions based on a rational outlook, the available information, and their past experiences. Here is a breakdown of how this assumption plays out in these models:

Agents are presumed to make forecasts about future economic variables in a way that optimally utilizes all available information. This means their predictions are not systematically biased and are as accurate as the model and available information allow.

Agents are assumed to consider all relevant and available information when forming their expectations about future economic conditions. This includes historical data, current economic indicators, and an understanding of economic policy and its potential impacts.

In a general equilibrium model, rational expectations imply that agents’ predictions about economic variables are consistent with the model itself. Their expectations are formed in such a way that, on average, they will coincide with the model’s predictions.

An important implication of rational expectations in these models is that economic policies will not have systematic and predictable effects if agents adjust their behavior in anticipation of these policies. For instance, if a government announces an inflation target, agents will anticipate this and adjust their behavior accordingly, which will be reflected in the equilibrium of the model.

In dynamic general equilibrium models, rational expectations also play a key role in how economies adjust over time. Agents form expectations not just about current conditions but also about how the economy will evolve in the future, influencing their current decisions.

The assumption of rational expectations in applied general equilibrium models posits that all agents in an economy make informed, forward-looking decisions that are consistent with the model’s structure. This has significant implications for understanding how economies respond to policy changes and how equilibria are formed and adjusted over time.

The dynamic Computable General Equilibrium (CGE) model presented in this section is based on the hypothesis of the rational expectations of the economic agents. This hypothesis is a crucial concept in modern economic theory and assumes that agents make decisions based on a rational perspective, the available information, andtheir past experiences. It is highlighted that agents make forecasts about future economic variables by optimally utilizing all available information, implying that their predictions are not systematically biased and are as accurate as the model and information allow.

This formulation of the dynamic CGE model is important as it captures the anticipatory behavior of agents in the economy, allowing for a more realistic and detailed analysis of how economies respond to policy changes and how equilibria are formed and adjusted over time. However, the assumption of rational expectations also entails certain limitations, as it presupposes a high level of information processing and foresight by the agents, which may not always reflect decision-making in the real world. In addition, models based on rational expectations can be complex and demanding in computational terms.

The assumptions of the dynamic CGE model, although strict, are fundamental for its application and relevance in economic analysis. These assumptions allow the model to realistically simulate how economic agents, such as individuals, companies, and other organizations, make informed and anticipatory decisions that are consistent with the structure of the model.

These assumptions are key to understanding how economies respond to policy changes and how equilibria are adjusted over time. The incorporation of rational expectations ensures that the model not only simulates immediate reactions to policy changes but also takes into account how agents adjust their behavior in anticipation of these changes. This feature is crucial for analyzing the long-term impact of policies and investments, especially in the context of expectations and market dynamics.

Although disciplines such as behavioral economics and institutional economics may question some of these assumptions, arguing that agents do not always act fully rationally or are not informed, these criticisms do not invalidate the usefulness of the dynamic CGE model. Instead, they provide important context and highlight the need to interpret the model’s results within a broader framework that includes behavioral and institutional considerations. These additional considerations can enrich the analysis and offer a more nuanced perspective on economic impacts.

Outlined below are the key aspects and critical decisions that a researcher must consider in modeling the most common economic agents in any CGE model. These agents are categorized into:

- (a)

Productive sectors

- (b)

Consumers

- (c)

The public sector

- (d)

Investment and savings

- (e)

The external sector

The model constructed here incorporates the conduct of these representative agents of the economy: 31 production sectors, a representative consumer of Madrid’s households, the owners of the production factors (capital and labor), the public sector (which collects taxes, provides public goods and services, and performs transfers), and finally the so-called aggregate rest of the world, which brings together the entire foreign sector as a single aggregate account.

A comprehensive description of the equations comprising the constructed model is provided below.

3.2.1. Producers

When modeling productive sectors, it is necessary to make adjustments not only to the number of productive branches but also ti the type of grouping or disaggregation that is most convenient for the analysis of the economy to be conducted. It should be considered that excessive disaggregation of the productive sector could complicate the interpretation of the results that the model will eventually provide.

Another assumption that must be established in the model is the functioning of the markets for produced goods, as this will determine the behavior of each of the producers. In relation to this assumption, there are two types of modeling in the literature: on the one hand, traditional and more orthodox models with the concept of Arrow–Debreu equilibrium that employ the assumption of perfect competition in all markets, and on the other, models that incorporate the existence of imperfect competition in some markets.

Models that incorporate imperfect competition show great diversity, making it difficult to present a common structure among them. This diversity is due to the multiple forms of competition (monopoly, collusion, oligopoly, etc.) and the variety of rivals’ reactions, represented using conjectural variations, Cournot/Bertrand models, etc. [

35]. On the other hand, the geographical framework in which companies compete (integrated or segmented markets) is also relevant, as the demands and competition they face in each framework can vary. In this work, we have included only a description of the formulation of models with perfect competition. A detailed review of the different types of models with imperfect competition can be found in [

36].

The next consideration to be made is to determine the functional form through which the combinations of factors and other inputs (intermediate consumption, imports, etc.) are related to determine the production technology function of the hypothetical homogeneous good manufactured by each of the productive branches represented in the model.

Under the assumption of perfect competition, it is usual for this productive technology to be described using production functions that have constant returns to scale, and the most commonly chosen forms are a Leontief or fixed coefficient, Cobb–Douglas type, CES (constant elasticity of substitution), LES (Linear Expenditure System), and Translog.

The choice of a specific form will normally depend on how the elasticities will be used in the model and on the availability of statistical data related to these elasticities, which allow their numerical specification in the calibration process.

Moreover, in the description of productive relationships, there is the possibility of incorporating nested structures of supply, thus defining different levels of combination of the inputs of the productive process. In most of the applied models existing in the literature, this is usually divided into three levels of nesting: at the first level, the composite good or added value is obtained by combining the productive factors (capital, labor, etc.). The domestic production function is the result of the second level of nesting through the combination of the composite good and intermediate inputs. Finally, at the third level, in the case of open economies, domestic products are combined with imported products to determine the total production function. This is illustrated in the diagram featured in

Figure 3.

In the first level of nesting, we propose the total production equation of the goods offered by each sector in each period. We adopt the Armington assumption, commonly used in the literature on the subject in these cases, by which we define the total production as a composite good of the domestic production and imports, combining both inputs using a Cobb–Douglas function:

where

represents the efficiency coefficient of the total production function. The coefficients

and

represent the technical coefficients of the domestic production and imports, respectively.

In the second level of nesting, the domestic or interior production function

, of each sector

at each moment

is obtained by combining intermediate consumption and value-added using a fixed coefficient transformation function, Leontief-type:

With being the requirement of good to produce one unit of good and the value-added component per unit of production of sector .

In the third level of nesting, we assume that each sector produces in perfect competition and with constant returns to scale, which is reflected in a value-added equation

, with Cobb–Douglas technology that combines the capital and labor factors:

where

is the capital factor of sector

in the period

,

the labor factor used by the sector

in the period

, and

and

represent the technical coefficients of the production factors, capital and labor, respectively. The parameter

is the efficiency coefficient of the added value that represents the technology with which the productive factors are combined at this third level of nesting.

We will consider producers to be maximizing agents with two types of objectives: an intertemporal long-term goal and, on the other hand, a set of intratemporal goals.

The last consideration refers to the behavior of firms, as rational behavior will facilitate the determination of the demanded quantities of factors and other inputs, as well as their corresponding prices. The rational behavior of the producers is assumed to be directed at maximizing their profits, subject to their technological constraints.

However, specifying production functions with constant returns to scale implies that no activity offers positive profits at market prices. Therefore, the necessary condition for profit maximization is that producers minimize their production costs, and solving these mathematical programs will provide the model’s equations for the demands of the productive factors and other inputs of the productive process.

Producers will be considered maximizing agents with two types of targets: an intertemporal long-term objective and, secondly, a set of intratemporal objectives solved as in any static CGE model of a certain period.

Under the dynamic approach, and in relation to every producer´s evolution of capital, we assume that the capital stock of each company at the beginning of each period

is equal to that in the previous period

, underestimated by the depreciation plus the investment made

at the end the previous period, i.e.:

where

is the rate of depreciation for the capital factor, whereas the capital stock for the first period is exogenously fixed.

If the representative producer behaves under rational forward-looking expectations, which involve no uncertainty or absence of money illusion, the producer uses in each period an amount of labor and capital inputs such that the firm value is maximized. As a result of this decision, the level of investment is obtained, which makes the degree of capitalization of the company vary period after period.

Under this approach, we refer to the dividend payments made by the company, calling them , with the value of the production of the company proving to be lowered by the cost of the labor factor, taking into account social security payments and minus the costs related to investment, and .

Thus, we obtain the expression of dividend payments, which becomes:

The last two terms refer to the aforementioned costs associated with investment in each period: the first one is associated with the part of the producer investment financed by the retained earnings, , and the second term, , represents the adjustment costs associated with the new investments made by each firm in each period. The latter collect losses arising, for example, in the adjustment process after the implementation of a technological improvement in a company or any progress toward successful implementation, applicable to any other similar situation. The existence of such adjustment costs implies that companies lose part of their production in the investment process, so the desired capital stock is achieved over time gradually and not instantly, in an abrupt way.

In the context of this long-term vision of the producer, as the objective is to maximize the financial value of the company, labeled

, it is defined as the present value of the flow of future dividend payments by the company, proving to be its expression as follows:

The optimizing behavior of the producer implies achieving a balance in the financial value of the companies using different interest rates, , for each period.

In this equation,

is the interest rate at any time previous to year

,

is the market value of company

at time

,

are the dividends paid by the company

in the year

, and

is the market value of the company

at time

. So, the market value of the company

at time

is given by the expression:

where

is the new shares issued by the company

at time

. These new shares are to be part of the investment, which is not financed with retained earnings, i.e.,:

Given that is the coefficient of the retained earnings by the company, will then be the partition coefficient to the shareholders of the company.

With this approach and substituting in Equation (6), which represents the expression of the dividend payments, we obtain the equation for the financial value of the company, which turns out to be the objective function in the optimization program of the company, subject to the constraints of added value (3) and capital (4).

Thus, we obtain the program for maximizing the value of the company, which the producer faces in the long term, formulated as follows:

where producers allocate their optimal investment strategies and use of factors,

, to maximize the present value of the company, taking into account the expected price of sale of production, the cost of investment, and the labor costs,

, subject to the constraints on capital accumulation. Thus, solving the above equations, we obtain the model equations related to the intertemporal equilibrium values of the model variables.

Thus, by solving the previous program, we obtain the following equations of the model:

A feature of the dynamic approach is the treatment of capital in the last period of the formulation, which we call the final period or year “T” [

37], representing the model´s terminal period. Empirical models can only be solved for a finite number of periods, and a numerical solution cannot be obtained in a formulation which foresees an infinite number of periods. Thus, it is necessary to make some adjustments in order to approximate our infinite horizon model into a finite horizon one.

A specific formulation allowing capital stock to reach its steady-state level in the terminal period was therefore introduced. According to Lau et al. (1997), the level of post-terminal capital stock as a variable is incorporated, and a constraint on the growth rate of investment in the terminal period is added [

37]. The advantage of using this constraint is that it imposes growth in accordance with the previous path; hence, the constraint on investment in the terminal period can be formulated:

This method assumes that the economy is in a steady state after simulation by the terminal period T; it is a method of approximating infinite-horizon choices, but it is solved over a finite horizon, following [

38].

Producers’ Intratemporal Optimization

Producers, in addition to maximizing the long-term financial value of the company, maximize profits (or equivalently, minimize production costs, given that the production function exhibits constant returns to scale) in each time period at each of the last two nesting levels. The resolution of the following program for minimizing the production costs, at the second nesting level, leads us to an optimal use of intermediate goods and added value for each sector.

With the aim of optimizing the cost function of domestic production for each sector and taking into account the Leontief technology, proposed at the second nesting level, the demanded quantity of inputs, intermediate goods, and added value is obtained, namely:

Under the assumption of constant returns to scale, we obtain the unit price of sectoral domestic production as the minimum average cost by substituting the optimal values into the previous objective function (Regarding the parameters a_ij and a_ij(t), as well as v_j and v_j(t), the subscript (t) is used to denote the computation of intertemporal equilibria. Thus, a_ij and v_j pertain to the technical coefficients for domestic production relative to the intermediate consumption and value added per unit of production for the base year and for each generic intratemporal equilibrium, respectively. They represent the requirement of good j to produce one unit of good i and the value-added component per unit of production of sector j for the base year and intratemporal equilibria. The terms a_ij(t) and v_j(t) extend this representation to successive periods, reflecting the calibration of the model’s equilibrium values over time.):

On the other hand, the equilibrium levels of domestic production and imports result from the minimization of costs corresponding to the first level of nesting:

By solving the previous program, these levels of production are calculated:

Similarly to the calculation of prices at the second nesting level, we calculate the final price of the good in each period:

The final price faced by the consumer is considered to be taxed by a tax rate, which represents the tax on products and production and Value-Added Tax.

3.2.2. Consumers

As in the dynamic version of the general equilibrium models, we take a representative consumer behavior of all consumers. This consumer has to find the consumption and income path that maximizes their total utility function subject to the budget constraints for each period. Under the approach of the dynamic Ramsey model, they faces their decisions under the assumption of rational forward-looking expectations with an infinite horizon.

The representative consumer of the dynamic model has the goal of maximizing the present value of their utility function over their expected lifetime, so we define the aggregate utility function, which is to maximize the utility over an infinite horizon, with the long run as an aggregation of the time in each of the periods:

The function reflects the value, which represents the aggregate utility function as the aggregation over time of utility in each period; is the intertemporal discount factor; is the long-term rate growth of the economy; and the logarithmic utility stands for the level of utility derived from consumption in each period .

On the one hand, the representative consumer receives income from their work, profitability derived from capital earnings, and transfers from the government. On the other hand, income is allocated by consumption, savings, and paying taxes. We assume, therefore, that in each period the consumer is subject to the budget constraint that dictates the equation of the disposable income

of households in each moment in time

:

This equation shows how the household’s disposable income is the result of subtracting indirect taxes on income from the total income, which is the sum of labor income, , returns on capital, , and transfers from the rest of the world and the government, .

The aggregate consumption function

is generated from the consumption of final goods by maximizing a Cobb–Douglas utility function:

Thus, the equations of our consumer program become:

Solving the mathematical program, we obtain the following model equation, which incorporates the consumption Euler condition:

The Euler equation summarizes the intertemporal consumer behavior, the relationship between today’s and tomorrow’s consumption.

3.2.3. Public Sector

In this model, we assign to the government the role of intermediary in certain economic flows. The government represents all public institutions, whether state, regional, or local, that carry out this task of redistributing income and affecting the economic sphere of the Community of Madrid. Through the collection of taxes on production, labor, and consumption, and following a principle of budgetary balance, such resources are dedicated to providing public goods and making transfers to consumers.

The composition of the tax collection carried out by the government consists of direct tax collection from households and their income, collection from social contributions, and the collection of indirect taxes on products.

The following equations allow us to calculate the tax revenue collected by the government in the Madrid economy:

With these revenues, the government finances public spending on the consumption of goods and transfers made to the rest of the institutional sectors. Therefore, the equation for public deficit/surplus is:

where

represents the dividend income received by the public sector from the productive sectors,

captures the income from transfers from the external sector, and, finally,

reflects the transfers made by the government to households.

In the model, we have considered keeping the levels of consumption of goods at the government constant, and determining the public deficit/surplus endogenously.

3.2.4. Investment and Savings

Savings and investment have a dynamic character: the former represents a deferred consumption and the latter affects the productive capacity of later periods. Defining investment as the purchase of capital goods makes it a component of final demand. Equally, it is considered that the total aggregate level of investment matches the total savings.

Regarding the composition of the investment made by each sector, we have proposed aggregate investment, which includes the investment made by the sectors, to act as a composite investment asset which is added to the capital stock of each of them:

All productive sectors buy or invest in this investment asset and add it to their capital stock:

In short, all exposed equations describe the optimal path, reaching in every period the neoclassical Arrow–Debreu equilibrium of Walrasian-type character, including the government and foreign sector.

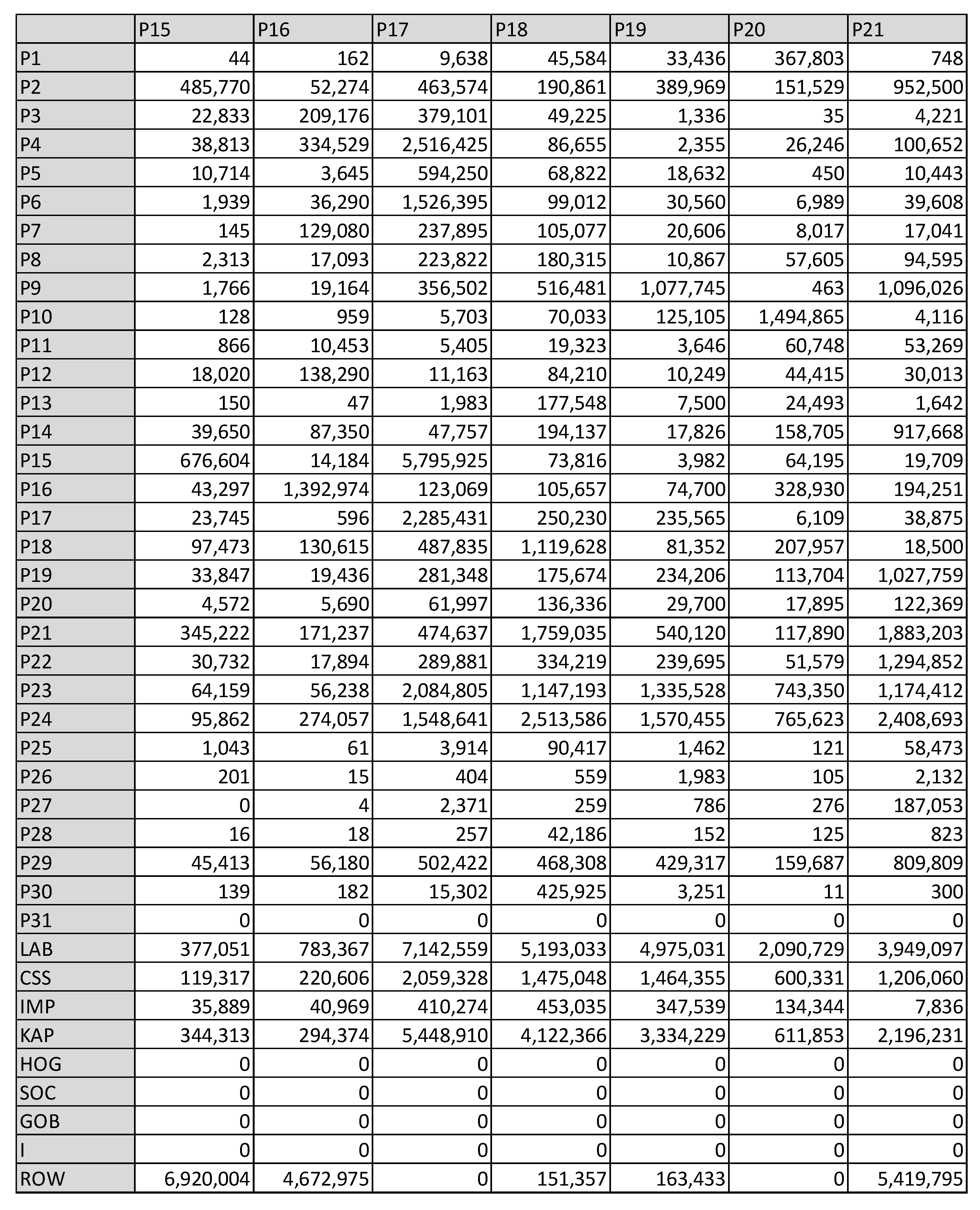

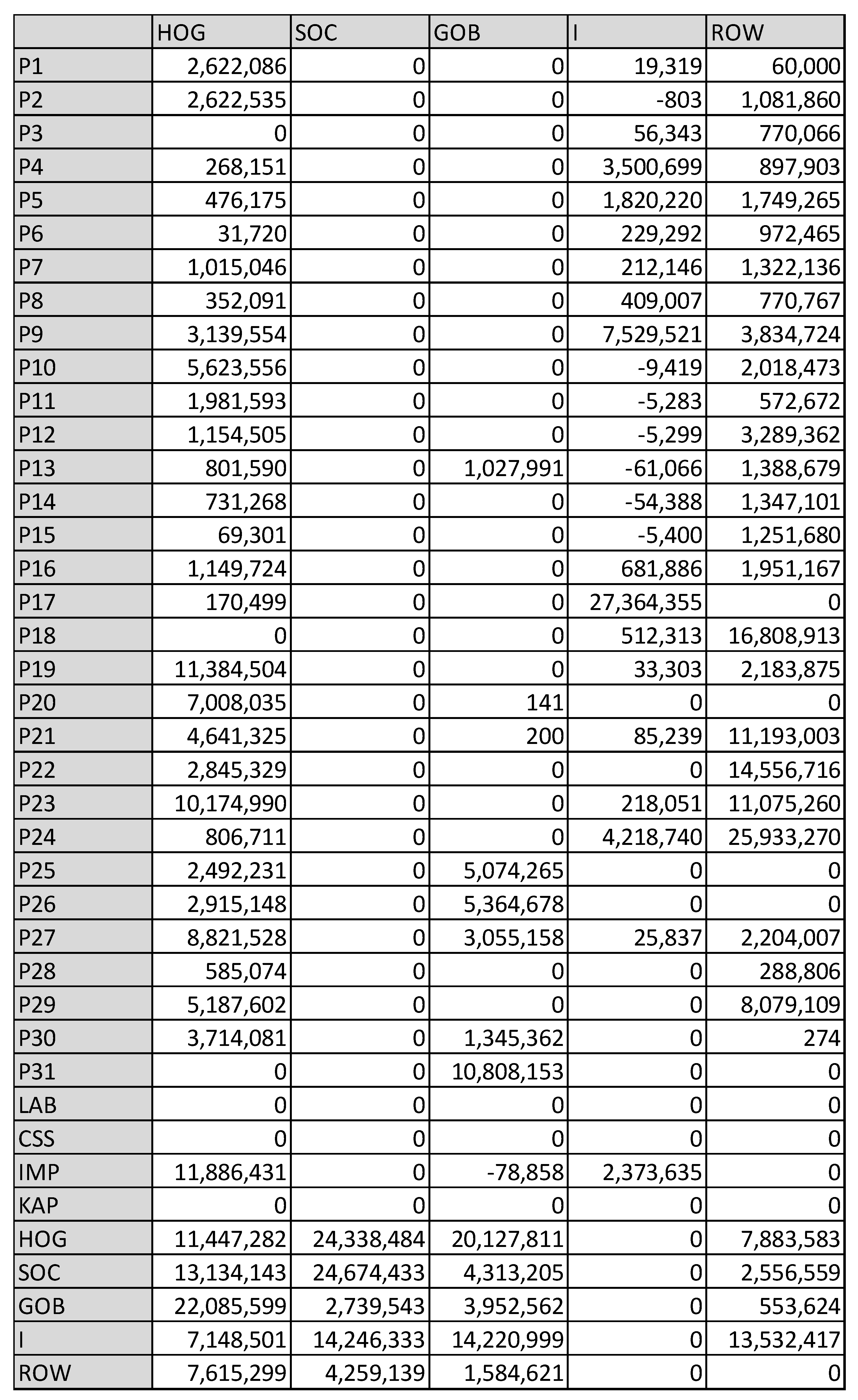

Then, to make the formulated model applicable to the empirical data, we proceed to its calibration, that is, determining the numerical values of all parameters of the model.

The calibrated parameters’ numerical values are available for reference in

Figure A4, located in

Appendix A. Additionally, specific parameters and their initial values are set, with the scalar

rho established at 5%. For this simulation, the scalar

g, which represents the steady state (long-term growth rate), has been kept constant to isolate the effect of the impact of investment.

3.2.5. The External Sector or “the Rest of the World”

Incorporating the relationships of the analyzed economy with foreign economies means that CGE models can differ substantially from one another, due to the wide range of possibilities when introducing the external sector.

In this regard, the pure neoclassical model assumes perfect substitution between domestic production and imported production, while structuralist models include imports as complements to domestic production. In practice, an intermediate stance is often adopted using the Armington assumption (1969), which suggests imperfect substitution between national and imported goods and services and is usually the most suitable for small economies.

Considering that in a CGE model the level of sectoral disaggregation is always limited, confined to the SAM that will be used as a database, the basket of imported products included in each sector usually differs from the domestic one classified in the same sector; therefore, the law of perfect substitutability between imports and domestic goods (the law of one price) within each sector is highly unlikely. Thus, the neoclassical method presented by Armington, with imperfect substitution, is the most widespread. In this method, the demand for imports and domestic goods is derived from a CES-type technological function, aggregating the demand for imported products and that of national products into a composite good (third level of nesting, referred to when describing productive sectors).

Regarding exports, with the consideration of a small country for the economy analyzed, the most realistic assumption tends to be to consider exports and domestic production imperfect substitutes.

3.2.6. Consumer Price Index

Analyzing the temporal evolution of the consumer price index (CPI) in this dynamic applied general equilibrium model involves several steps and is supported by specific equations that capture the movement of prices over time. Here is a detailed explanation of the process:

In the dynamic applied general equilibrium (AGE) model, the economy is depicted using the interconnected markets and agents such as households, firms, and government, with decisions influenced by prices, incomes, and other economic factors over multiple periods. The consumer price index (CPI), representing the weighted average of a basket of goods and services, is calculated by comparing the basket’s price in each period to the baseline year. Within the AGE model, the CPI is affected by variables like production costs, market demand and supply, policy shifts, and external factors. The model’s dynamics are encapsulated in equations of motion, with the CPI equation formulated as according to the inflation rate, where is the consumer price index in period , is the index in the previous period, and is the rate of inflation between period and . The model simulates the economy across various periods, updating the CPI for each time period to analyze its temporal evolution. This analysis, using GAMS, provides insights into inflation trends and the effects of economic policies over time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}