Greening the Financial System in USA, Canada and Brazil: A Panel Data Analysis

,

,

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

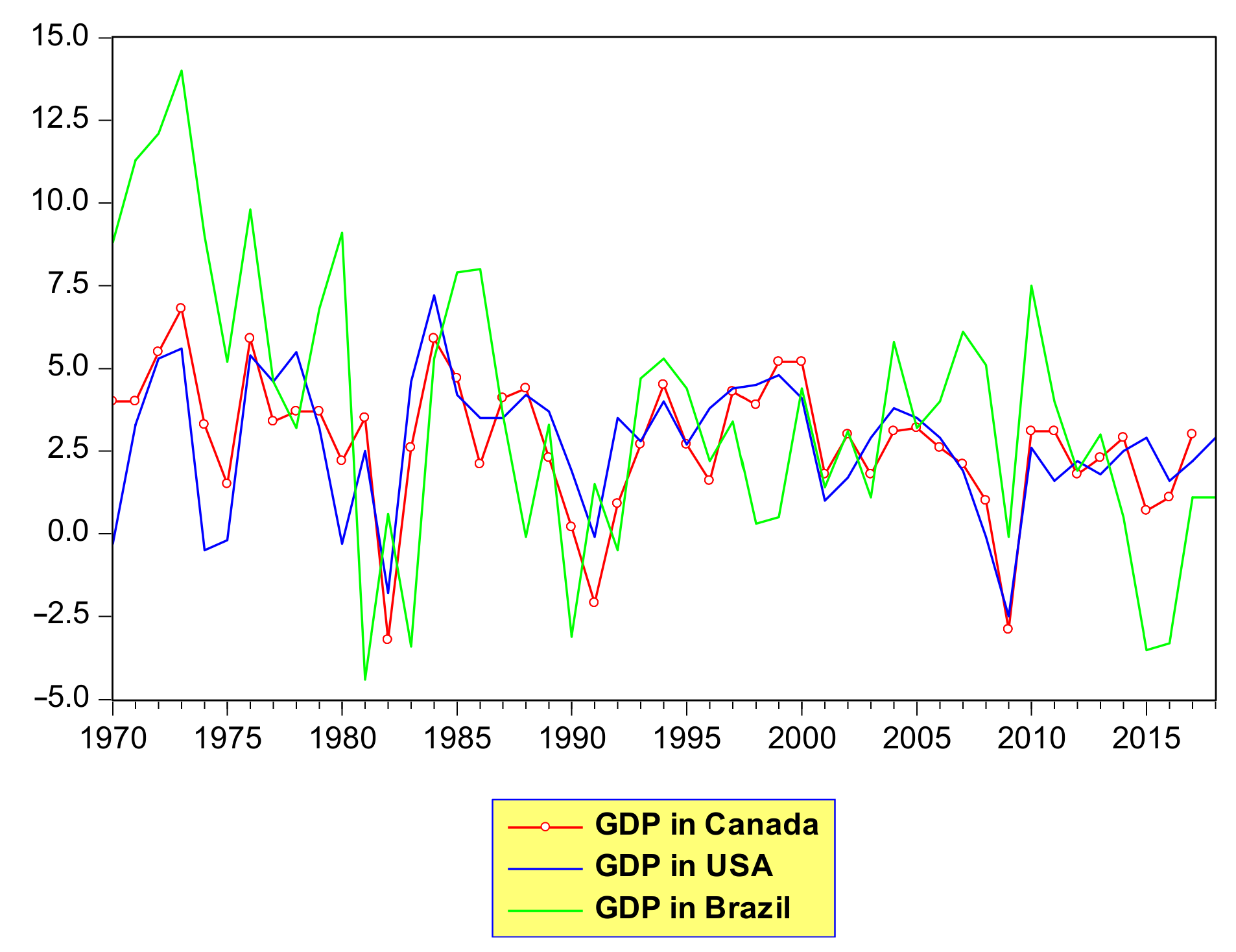

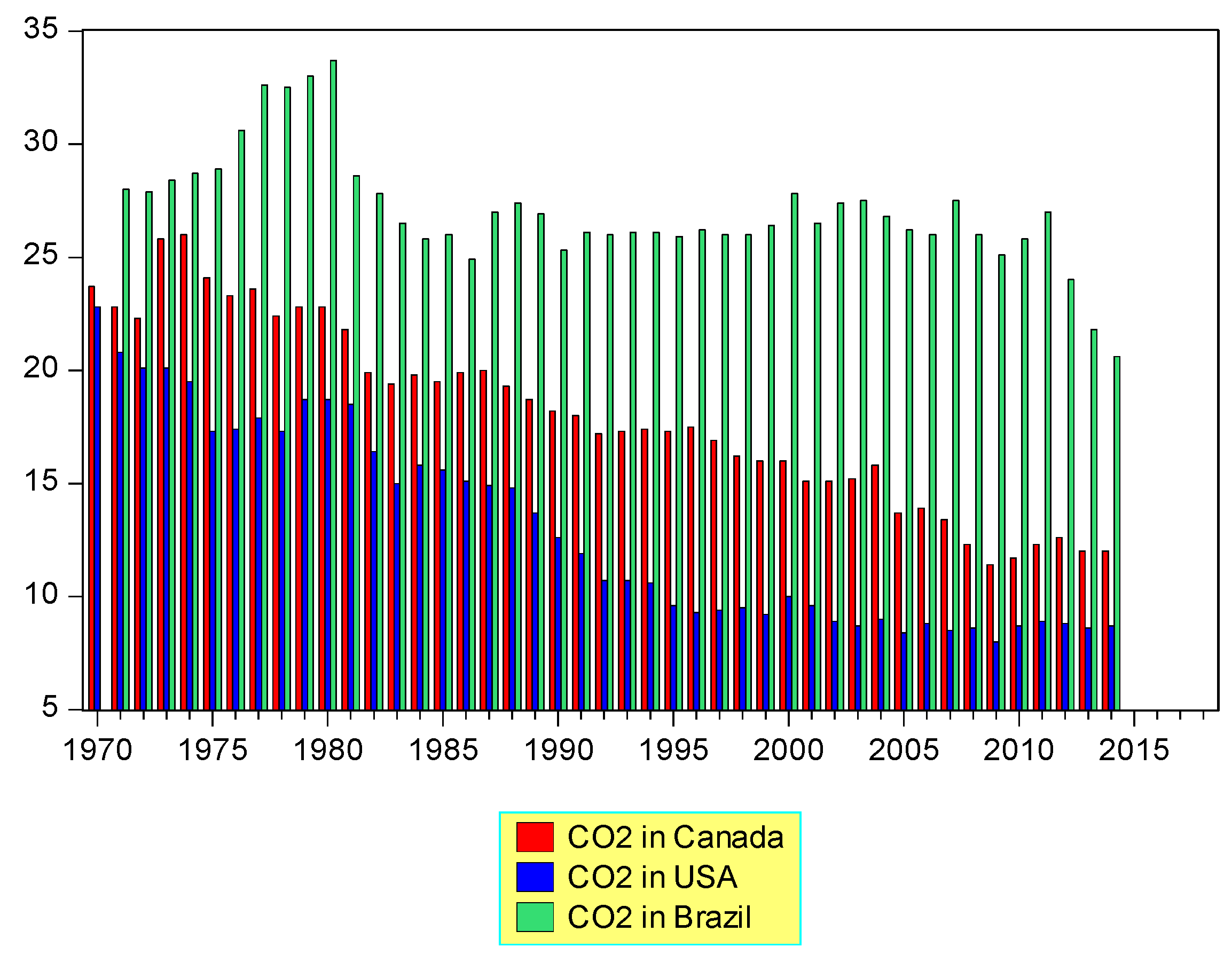

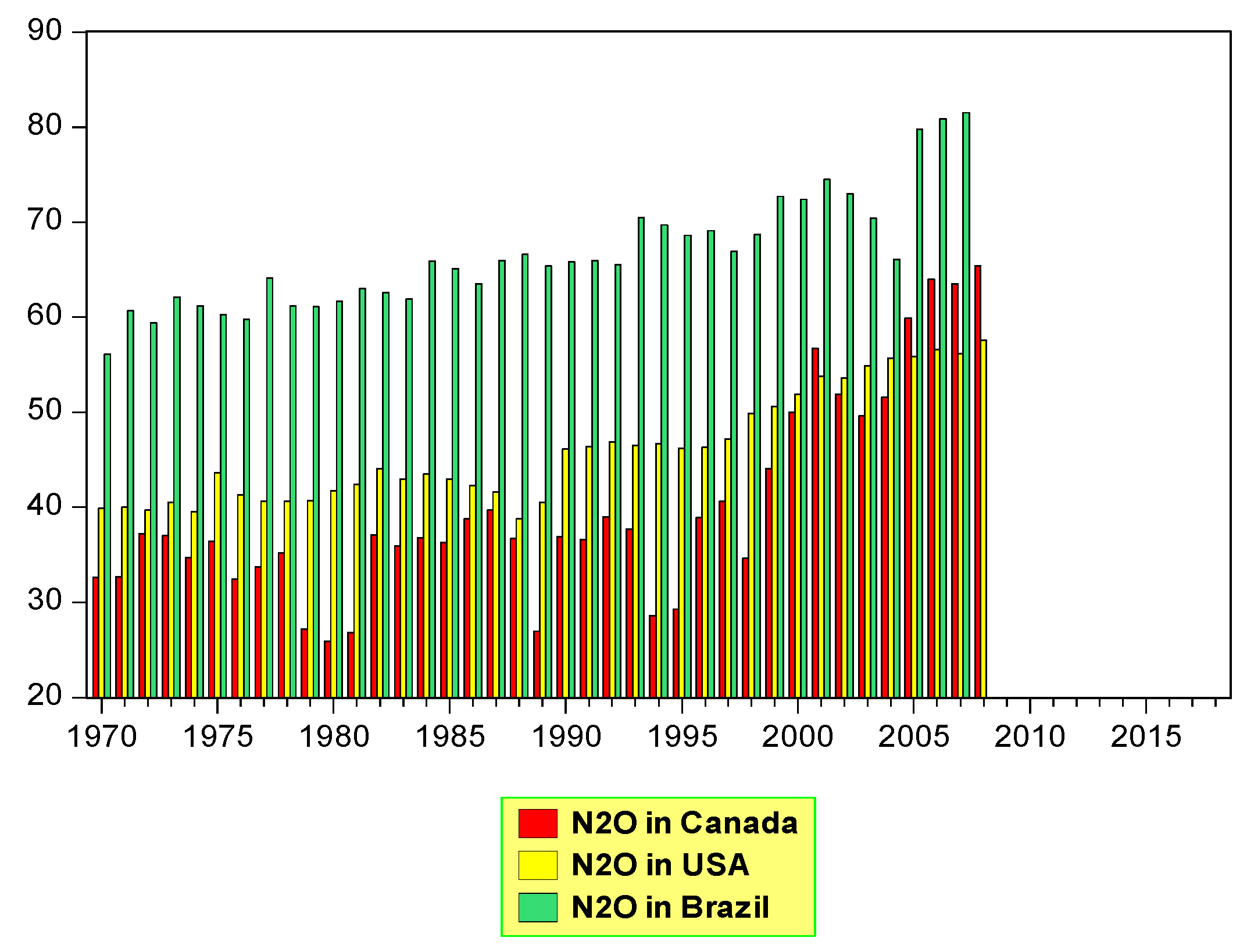

3.1. Analysis of Key Statistical Indicators of Central Tendency and Variation

3.2. Analysis of Correlation

3.3. Econometric Models

4. Discussion

- (1)

- capping global warming at 1.5 °C;

- (2)

- improving the capacity of adaptation to extreme weather conditions triggered by climate change;

- (3)

- directing financial flows towards projects that efficiently mitigate greenhouse gas emissions and support climate-resilient development.

5. Conclusions and Policy Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- FAO; IFAD; UNICEF; WFP; WHO. State of Food Security and Nutrition in the World 2018. Building Climate Resilience for Food Security and Nutrition; FAO: Rome, Italy, 2018. [Google Scholar]

- UNEP. Green Finance for Developing Countries: Needs, Concerns and Innovations; UNEP: Geneva, Switzerland, 2016. [Google Scholar]

- Inter-American Development Bank. Transforming Green Bond Markets; Inter-American Development Bank: Washington, DC, USA, 2017. [Google Scholar]

- Climate Bonds Initiative. Latin America & Caribbean: Green Finance State of the Market; Climate Bonds Initiative: London, UK, 2019. [Google Scholar]

- IFC. Climate Investment Opportunities in Emerging Markets: An IFC Analysis; IFC: Washington, DC, USA, 2016. [Google Scholar]

- Damerow, F.; Kidney, S.; Clanaghan, S. How Covered Bond Markets Can be Adapted for Renewable Energy Finance and How This Could Catalyze Innovation in Low Carbon Capital Markets; Climate Bonds Initiative: London, UK, 2012. [Google Scholar]

- IMF. IMF Annual Report; International Monetary Fund: Washington, DC, USA, 2007. [Google Scholar]

- IMF. IMF Annual Report; International Monetary Fund: Washington, DC, USA, 2016. [Google Scholar]

- Global Sustainable Investment Alliance. Global Sustainable Investment Review 2018; Global Sustainable Investment Alliance: Washington, DC, USA, 2018. [Google Scholar]

- Climate & Development Knowledge Network. Policy Brief Report; Climate & Development Knowledge Network: London, UK, 2013. [Google Scholar]

- FAO. Linking Sustainability and Climate Financing: Implications for Agriculture; FAO: Rome, Italy, 2011. [Google Scholar]

- IEA. Redrawing the Energy-Climate Map; World Energy Outlook Special Report; IEA: Paris, France, 2013. [Google Scholar]

- FAO. Agriculture, Forestry and Other Land Use Emissions by Sources and Removals by Sinks; FAO Statistics Division Working Paper Series; FAO: Rome, Italy, 2014. [Google Scholar]

- Shyamsundar, P.; Springer, N.; Tallis, P.; Polasky, S.; Jat, M.L.; Sidhu, H.S.; Krishnapriya, P.P. Fields on fire: Alternatives to crop residue burning in India. Science 2019, 365, 536–538. [Google Scholar] [CrossRef] [PubMed]

- Tubiello, F.N.; Salvatore, M.; Rossi, S.; Ferrara, A.; Fitton, N.; Smith, P. The FAOSTAT database of greenhouse gas emissions from agriculture. Environ. Res. Lett. 2013, 8, 015009. [Google Scholar] [CrossRef]

- Kasman, A.; Duman, Y.S. CO2 emissions, economic growth, energy consumption, trade and urbanization in new EU member and candidate countries: A panel data analysis. Econ. Model. 2015, 44, 97–103. [Google Scholar] [CrossRef]

- Uddin, G.A.; Salahuddin, M.; Alarm, K.; Gow, I. Ecological footprint and real income: Panel data evidence from the 27 emitting countries. Ecol. Indic. 2017, 77, 166–175. [Google Scholar] [CrossRef]

- Alshubiri, F.; Elhehhad, M. Foreign finance, economic growth and CO2 emissions nexus in OECD countries. Int. J. Clim. Change Strateg. Manag. 2020, 12, 161–181. [Google Scholar] [CrossRef]

- ADBI. Why is Green Finance Important? ADBI Working Paper Series; No. 917; ADBI: Tokyo, Japan, 2019. [Google Scholar]

- Chowdhury, T.M.; Datta, R.; Mojahan, H. Green finance is essential for economic development and sustainability. Int. J. Res. Commer. Econ. Manag. 2013, 3, 104–108. [Google Scholar]

- Akinlo, A.E. Energy consumption and economic growth: Evidence from 11 African countries. Energ. Econ. 2008, 30, 2391–2400. [Google Scholar] [CrossRef]

- Lee, C.C.; Chang, C.P.; Chen, P.F. Energy-income causality in OECD countries revisited: The key role of capital stock. Energ. Econ. 2008, 30, 2359–2373. [Google Scholar] [CrossRef]

- Narayan, P.K.; Smyth, R. Energy consumption and GDP in G7 countries: New evidence from panel co-integration with structural banks. Energ. Econ. 2008, 30, 2331–2341. [Google Scholar] [CrossRef]

- Squalli, J. Electricity consumption and economic growth bounds and causality analyses for OPEC members. Energ. Econ. 2007, 29, 1192–1205. [Google Scholar] [CrossRef]

- Wolde-Rufael, Y. Energy consumption and economic growth: The experience of African economies revisited. Energ. Econ. 2009, 31, 217–224. [Google Scholar] [CrossRef]

- Kahlenborn, W.; Cochu, A.; Georgiev, I.; Eisinger, F.; Hogg, D. Defining “Green” in the Context of Green Finance. Final Report; European Commision: Luxemburg, 2017. [Google Scholar]

- Zhang, D.; Zhang, Z.; Managi, S. A bibliometric analysis in green finance: Current status, development, and future directions. Financ. Res. Lett. 2019, 29, 425–430. [Google Scholar] [CrossRef]

- Zhou, X.; Tang, X.; Zhang, R. Impact of green finance on economic development and environmental quality: A study based on provincial panel data from China. Environ. Sci. Pollut. R. 2020, 27, 19915–19932. [Google Scholar] [CrossRef] [PubMed]

- Falcone, P.M. Environmental regulation and green investments: The role of green finance. Int. J. Green Econ. 2020, 14, 159–173. [Google Scholar] [CrossRef]

- Cui, H.; Wang, R.; Wang, H. An evolutionary analysis of green finance sustainability based on multi-agent game. J. Clean. Prod. 2020, 269, 121799. [Google Scholar] [CrossRef]

- Wang, Y.; Zhi, Q. The role of green finance in environmental protection: Two aspects of market mechanism and policies. Energy Procedia 2016, 104, 311–316. [Google Scholar] [CrossRef]

- Ghouali, Y.Z.; Belmokaddem, M.; Sahraoui, M.A.; Guelli, M.S. Factors affecting CO2 emissions in the BRICS countries: A panel data analysis. Procedia Econ. Fin. 2015, 26, 114–125. [Google Scholar]

- Morgan Stanley. Sustainable Reality: Analyzing Risk and Returns of Sustainable Funds; Morgan Stanley: New York, NY, USA, 2019. [Google Scholar]

- Climate Transparency. Brown to Green Report: The G20 Transition towards a Net-Zero Emissions Economy; Climate Transparency: Berlin, Germany, 2019. [Google Scholar]

- Climate Transparency. Brown to Green Report: The G20 Transition to a Low-Carbon Economy; Climate Transparency: Berlin, Germany, 2018. [Google Scholar]

- Batrancea, L.; Nichita, A.; Batrancea, I.; Gaban, L. The strength of the relationship between shadow economy and corruption: Evidence from a worldwide country-sample. Soc. Indic. Res. 2018, 138, 1119–1143. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Nichita, R.A.; Batrancea, I.; Moldovan, B.A. Tax compliance models: From economic to behavioral approaches. Transylv. Rev. Adm. Sci. 2012, 36E, 13–26. [Google Scholar]

- Batrancea, L.; Nichita, A.; Olsen, J.; Kogler, C.; Kirchler, E.; Hoelzl, E.; Weiss, A.; Torgler, B.; Fooken, J.; Fuller, J.; et al. Trust and power as determinants of tax compliance across 44 nations. J. Econ. Psych. 2019, 74, 102191. [Google Scholar] [CrossRef]

- Kogler, C.; Batrancea, L.; Nichita, A.; Pantya, J.; Belianin, A.; Kirchler, E. Trust and power as determinants of tax compliance: Testing the assumptions of the slippery slope framework in Austria, Hungary, Romanian and Russia. J. Econ. Psychol. 2013, 34, 169–180. [Google Scholar] [CrossRef]

- Batrancea, L.; Nichita, A. Which is the best government? Colligating tax compliance and citizens’ insights regarding authorities’ actions. Transylv. Rev. Adm. Sci. 2015, 44E, 5–22. [Google Scholar]

- Nichita, A.; Batrancea, L.; Pop, C.M.; Batrancea, I.; Morar, I.D.; Masca, E.; Roux-Cesar, A.M.; Forte, D.; Formigoni, H.; da Silva, A.A. We learn not for school but for life: Empirical evidence of the impact of tax literacy on tax compliance. Eastern Eur. Econ. 2019, 57, 397–429. [Google Scholar] [CrossRef]

- Available online: www.preventionweb.net/news/view/62408 (accessed on 20 July 2020).

- Climate Bonds Initiative. Post-Issuance Reporting in the Green Bond Market; Climate Bonds Initiative: London, UK, 2019. [Google Scholar]

- HM Government. Green Finance Strategy: Transforming Finance for a Greener Future; HM Government: London, UK, 2019.

- CARIMA. Carbon Risks and Financed Emissions of Financial Assets and Portfolios: Measurement, Management and Reporting based on Capital Market Data; University of Augsburg: Augsburg, Germany, 2019. [Google Scholar]

- OECD. OECD Work in Support of Climate Action; OECD Publishing: Paris, France, 2018. [Google Scholar]

- Yujun, C. Analyzing Green Finance Incentives: An Empirical Study of the Chinese Banking Sector. Master’s Thesis, University of Waterloo, Waterloo, ON, Canada, 2017. [Google Scholar]

- Burniaux, J.M.; Chanteau, J.; Dellink, R.; Duval, R.; Jamet, S. The Economics of Climate Change Mitigation: How to Build the Necessary Global Action in a Cost-Effective Manner; OECD Working Papers, No. 701; OECD Publishing: Paris, France, 2009. [Google Scholar]

- IMF. Energy Subsidy Reform: Lessons and Implications; International Monetary Fund: Washington, DC, USA, 2013. [Google Scholar]

- Keen, M. Trends and Reform Options for Fossil Fuel Subsidies; UNEP-IMF-GIZ Workshop: Geneva, Switzerland, 2012. [Google Scholar]

- Batrancea, L.; Rathnaswamy, M.M.; Batrancea, I.; Nichita, A.; Rus, M.-I.; Tulai, H.; Fatacean, G.; Masca, E.S.; Morar, I.D. Adjusted net savings of CEE and Baltic nations in the context of sustainable economic growth: A panel data analysis. J. Risk Financial Manag. 2020, 13, 234. [Google Scholar] [CrossRef]

- Batrancea, I.; Rathnaswamy, M.K.; Batrancea, L.; Nichita, A.; Gaban, L.; Fatacean, G.; Tulai, H.; Bircea, I.; Rus, M.-I. A panel data analysis on sustainable economic growth in India, Brazil, and Romania. J. Risk Financial Manag. 2020, 13, 170. [Google Scholar] [CrossRef]

- UNEP. Energy Subsidies: Lessons Learnt in Assessing Their Impacts and Designing Policy Reforms; UNEP: Geneva, Switzerland, 2003. [Google Scholar]

- UNCSD. The Future We Want; UNCSD: Rio de Janeiro, Brazil, 2012. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Specifications | GDP | DCB | DCF | N2O | CO2 | AFF |

|---|---|---|---|---|---|---|

| Mean | 3.068493 | 57.12555 | 121.3291 | 50.73362 | 19.32687 | 4.426596 |

| Median | 3.100000 | 52.50000 | 111.4500 | 48.40000 | 19.35000 | 1.750000 |

| Maximum | 14.00000 | 213.5000 | 249.7000 | 81.50000 | 33.70000 | 37.20000 |

| Minimum | −4.400000 | 14.00000 | 36.80000 | 25.90000 | 8.000000 | −8.000000 |

| Std. dev. | 2.924799 | 26.32449 | 58.85286 | 13.76802 | 6.929789 | 8.013043 |

| Skewness | 0.388585 | 2.413944 | 0.592624 | 0.210890 | −0.024878 | 2.918510 |

| Kurtosis | 4.790197 | 12.18662 | 2.228616 | 1.989273 | 1.861056 | 11.74779 |

| Jarque–Bera | 23.17019 *** | 614.8015 *** | 11.16580 *** | 5.797431 * | 7.256487 ** | 433.1626 *** |

| Observations | 146 | 137 | 134 | 116 | 134 | 94 |

| GDP | DCB | DCF | N2O | CO2 | AFF | |

|---|---|---|---|---|---|---|

| GDP | 1 | |||||

| DCB | −0.2019 | 1 | ||||

| DCF | −0.2914 | 0.6255 ** | 1 | |||

| N2O | −0.11084 | −0.07485 | −0.1583 | 1 | ||

| CO2 | 0.2320 | −0.3986 * | −0.8543 *** | 0.4103 * | 1 | |

| AFF | 0.1276 | –0.2328 | –0.3819 * | –0.4984 * | 0.2203 | 1 |

| Model 1: | Model 2: | Model 3: | Model 4: | Model 5: | |

|---|---|---|---|---|---|

| GDP = a0 + a1N2O + a2CO2 + a3DCB | GDP = a0 + a1N2O + a2CO2 + a3DCF | DCB = a0 + a1N2O + a2CO2 + a3GDP + a4DCF | DCF = a0 + a1N2O + a2CO2 + a3GDP + a4DCB | AFF = a0 + a1GDP + a2N2O + a3CO2 | |

| Constant | 14.253 *** (2.815) | 14.846 *** (2.907) | −175.707 *** (−4.946) | 228.710 *** (5.497) | −94.697 *** (−5.995) |

| DCB | −0.007 (−0.576) | - | 0.893 *** (9.0002) | - | |

| DCF | −0.012 (−1.126) | 0.613 *** (9.0002) | - | - | |

| N2O | −0.040 (−0.496) | −0.018 (−0.251) | 2.055 *** (4.326) | −0.915 (−1.431) | 0.421 ** (2.758) |

| CO2 | −0.421 *** (−2.893) | −0.465 *** (−2.885) | 3.001 *** (2.680) | −5.918 *** (−4.827) | 3.625 *** (9.495) |

| AFF | - | - | - | - | - |

| GDP | - | - | 0.292 (0.367) | −0.977 (−1.024) | −0.927 *** (−2.895) |

| Prob.>F | 0.0002 | 0.0002 | 0.0000 | 0.0000 | 0.0000 |

| Cross-section effects | Fixed | Fixed | Fixed | Fixed | Fixed |

| Time fixed effects | Yes | Yes | Yes | Yes | Yes |

| R2 | 0.610 | 0.626 | 0.832 | 0.931 | 0.973 |

| Adjusted R-squared | 0.374 | 0.390 | 0.721 | 0.885 | 0.920 |

| F statistic | 2.581 | 2.652 | 7.516 | 20.394 | 18.492 |

| Observations | 115 | 112 | 112 | 112 | 66 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Batrancea, I.; Batrancea, L.; Maran Rathnaswamy, M.; Tulai, H.; Fatacean, G.; Rus, M.-I. Greening the Financial System in USA, Canada and Brazil: A Panel Data Analysis. Mathematics 2020, 8, 2217. https://doi.org/10.3390/math8122217

Batrancea I, Batrancea L, Maran Rathnaswamy M, Tulai H, Fatacean G, Rus M-I. Greening the Financial System in USA, Canada and Brazil: A Panel Data Analysis. Mathematics. 2020; 8(12):2217. https://doi.org/10.3390/math8122217

Chicago/Turabian StyleBatrancea, Ioan, Larissa Batrancea, Malar Maran Rathnaswamy, Horia Tulai, Gheorghe Fatacean, and Mircea-Iosif Rus. 2020. "Greening the Financial System in USA, Canada and Brazil: A Panel Data Analysis" Mathematics 8, no. 12: 2217. https://doi.org/10.3390/math8122217

APA StyleBatrancea, I., Batrancea, L., Maran Rathnaswamy, M., Tulai, H., Fatacean, G., & Rus, M. -I. (2020). Greening the Financial System in USA, Canada and Brazil: A Panel Data Analysis. Mathematics, 8(12), 2217. https://doi.org/10.3390/math8122217