Volatility Timing: Pricing Barrier Options on DAX XETRA Index

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Methodology

3.1.1. Option Pricing Models

3.1.2. Heteroscedasticity Methods

3.2. Data

4. Results and Discussion

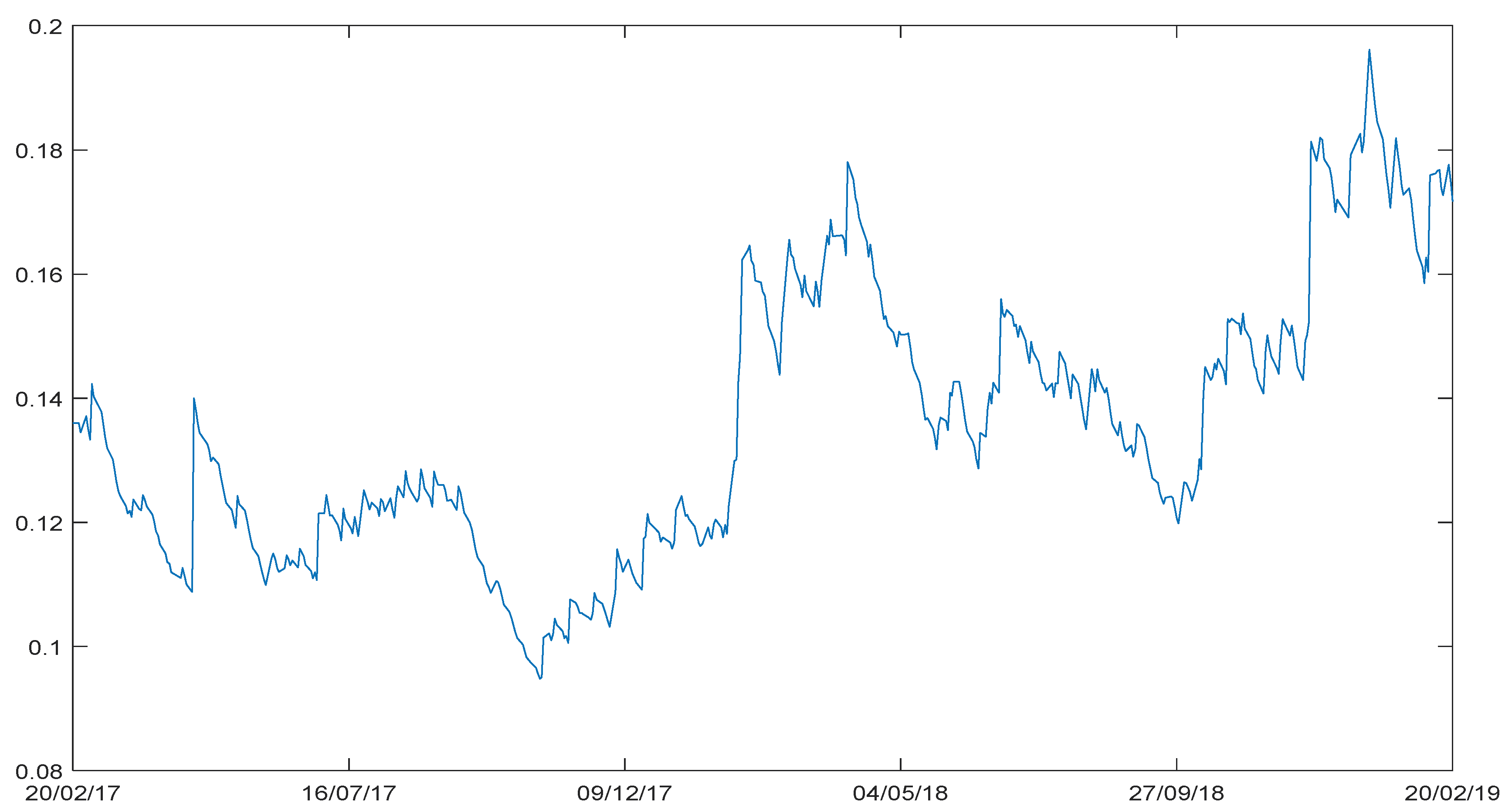

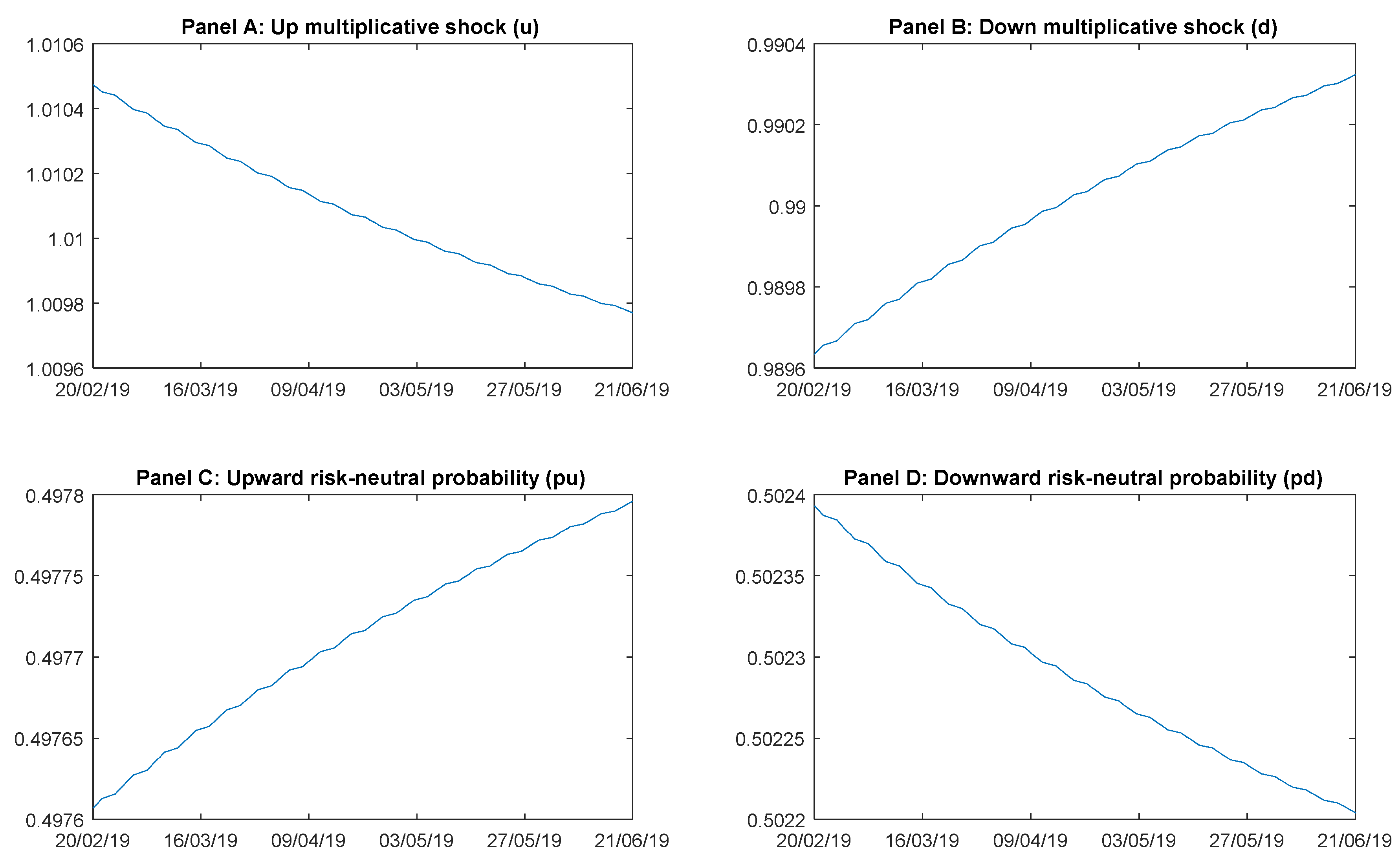

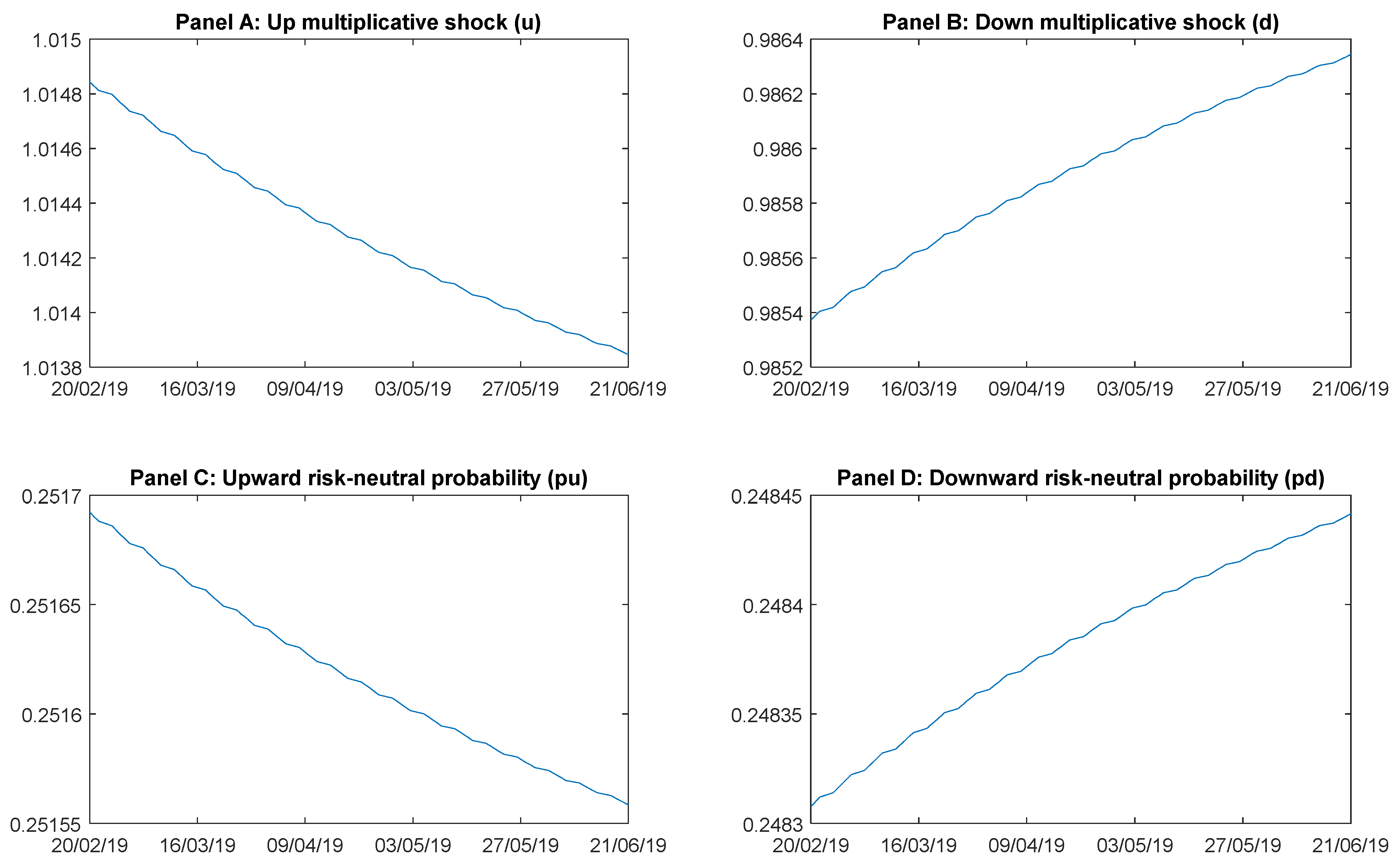

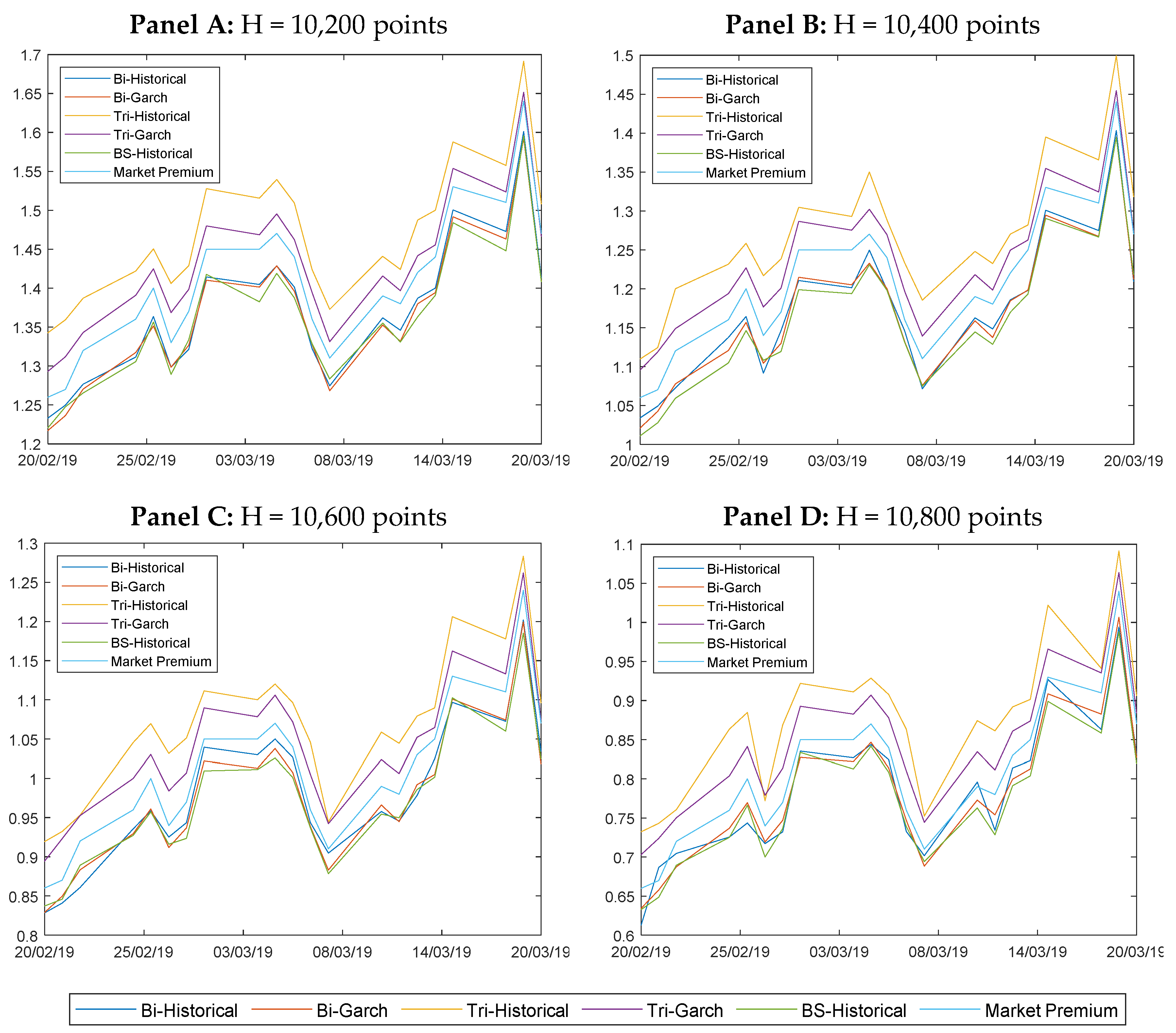

4.1. Conducting the Volatility. In-Sample and Out-of-Sample Analysis

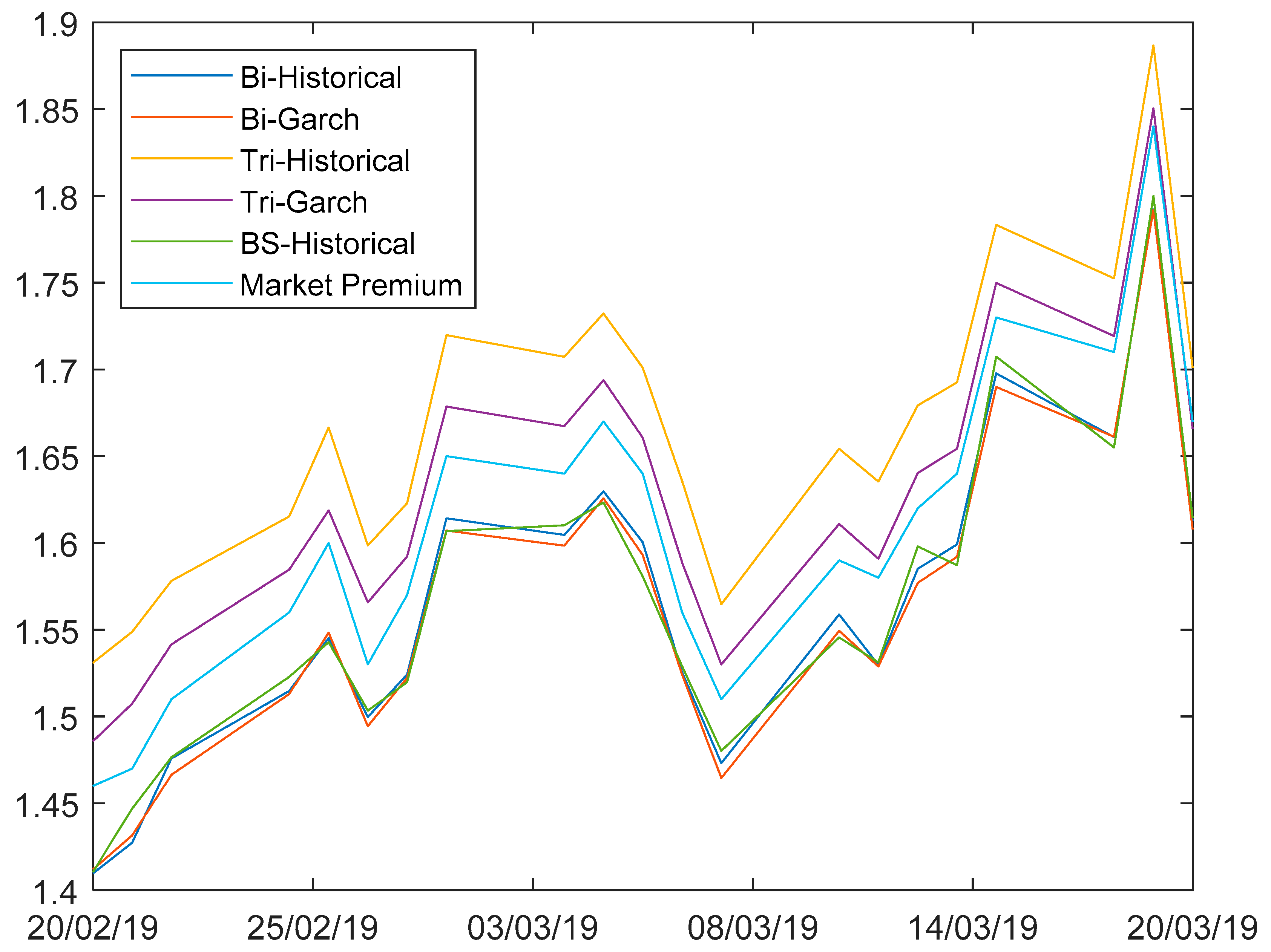

4.2. Out-of-Sample Risk Neutral Density Forecasting

4.3. Robustness Check. Accuracy Forecasting Assessment for Option Premiums

5. Conclusions and Remarks

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

Appendix A. Estimation by Maximum Log-Likelihood (MLE)

Appendix B. Derivation of the Traditional Black–Scholes Equation for European Option Pricing

Appendix C. Robustness Forecasting Accuracy Methods

Appendix D

References

- Kokholm, T. Pricing and hedging of derivatives in contagious markets. J. Bank. Financ. 2016, 66, 19–34. [Google Scholar] [CrossRef]

- Akhigbe, A.; Makar, S.; Wang, L.; Whyte, A.M. Interest rate derivatives use in banking: Market pricing implications of cash flow hedges. J. Bank. Financ. 2018, 86, 113–126. [Google Scholar] [CrossRef]

- Hull, J.C. Options, Futures, and Other Derivatives, 8th ed.; Prentice Hall: Upper saddle river, NJ, USA, 2012. [Google Scholar]

- Klein, P.; Inglis, M. Pricing vulnerable European options when the option’s payoff can increase the risk of financial distress. J. Bank. Financ. 2001, 25, 993–1012. [Google Scholar] [CrossRef]

- Li, S.; Peng, C.; Bao, Y.; Zhao, Y. Explicit expressions to counterparty credit exposures for Forward and European Option. N. Am. J. Econ. Financ. 2019, 101130, in press. [Google Scholar] [CrossRef]

- Chan, T.L.R. Efficient computation of european option prices and their sensitivities with the complex fourier series method. N. Am. J. Econ. Financ. 2019, 50, 100984. [Google Scholar] [CrossRef]

- Roul, P. A high accuracy numerical method and its convergence for time-fractional Black-Scholes equation governing European options. Appl. Numer. Math. 2020, 151, 472–493. [Google Scholar] [CrossRef]

- Zhao, J.; Li, S. Efficient pricing of European options on two underlying assets by frame duality. J. Math. Anal. Appl. 2020, 486, 123873. [Google Scholar] [CrossRef]

- Barone-Adesi, G.; Whaley, R.E. The valuation of American call options and the expected ex-dividend stock price decline. J. Financ. Econ. 1986, 17, 91–111. [Google Scholar] [CrossRef]

- Medvedev, A.; Scaillet, O. Pricing American options under stochastic volatility and stochastic interest rates. J. Financ. Econ. 2010, 98, 145–159. [Google Scholar] [CrossRef] [Green Version]

- Atmaz, A.; Basak, S. Option prices and costly short-selling. J. Financ. Econ. 2019, 134, 1–28. [Google Scholar] [CrossRef]

- Vidal Nunes, J.P.; Ruas, J.P.; Dias, J.C. Early Exercise Boundaries for American-Style Knock-Out Options. Eur. J. Oper. Res. 2020, in press. [Google Scholar] [CrossRef]

- Detemple, J.; Laminou Abdou, S.; Moraux, F. American step options. Eur. J. Oper. Res. 2020, 282, 363–385. [Google Scholar] [CrossRef] [Green Version]

- Chung, S.-L.; Shih, P.-T. Static hedging and pricing American options. J. Bank. Financ. 2009, 33, 2140–2149. [Google Scholar] [CrossRef]

- Lim, H.; Lee, S.; Kim, G. Efficient pricing of Bermudan options using recombining quadratures. J. Comput. Appl. Math. 2014, 271, 195–205. [Google Scholar] [CrossRef]

- Jain, S.; Oosterlee, C.W. The Stochastic Grid Bundling Method: Efficient pricing of Bermudan options and their Greeks. Appl. Math. Comput. 2015, 269, 412–431. [Google Scholar] [CrossRef] [Green Version]

- Borovykh, A.; Pascucci, A.; Oosterlee, C.W. Pricing Bermudan options under local Lévy models with default. J. Math. Anal. Appl. 2017, 450, 929–953. [Google Scholar] [CrossRef] [Green Version]

- Ballestra, L.V.; Pacelli, G.; Zirilli, F. A numerical method to price exotic path-dependent options on an underlying described by the Heston stochastic volatility model. J. Bank. Financ. 2007, 31, 3420–3437. [Google Scholar] [CrossRef]

- Fujiwara, H.; Kijima, M. Pricing of path-dependent American options by Monte Carlo simulation. J. Econ. Dyn. Control 2007, 31, 3478–3502. [Google Scholar] [CrossRef]

- Wong, H.Y.; Lo, Y.W. Option pricing with mean reversion and stochastic volatility. Eur. J. Oper. Res. 2009, 197, 179–187. [Google Scholar] [CrossRef]

- Park, S.H.; Kim, J.H.; Choi, S.Y. Matching asymptotics in path-dependent option pricing. J. Math. Anal. Appl. 2010, 367, 568–587. [Google Scholar] [CrossRef] [Green Version]

- Fuh, C.D.; Luo, S.F.; Yen, J.F. Pricing discrete path-dependent options under a double exponential jump-diffusion model. J. Bank. Financ. 2013, 37, 2702–2713. [Google Scholar] [CrossRef]

- Jeon, J.; Yoon, J.H.; Kang, M. Pricing vulnerable path-dependent options using integral transforms. J. Comput. Appl. Math. 2017, 313, 259–272. [Google Scholar] [CrossRef]

- Christoffersen, P.; Heston, S.; Jacobs, K. Option valuation with conditional skewness. J. Econom. 2006, 131, 253–284. [Google Scholar] [CrossRef] [Green Version]

- Tian, M.; Yang, X.; Zhang, Y. Barrier option pricing of mean-reverting stock model in uncertain environment. Math. Comput. Simul. 2019, 166, 126–143. [Google Scholar] [CrossRef]

- Dhaene, G.; Wu, J. Incorporating overnight and intraday returns into multivariate GARCH volatility models. J. Econom. 2019, in press. [Google Scholar] [CrossRef]

- Díaz-Hernández, A.; Constantinou, N. A multiple regime extension to the Heston–Nandi GARCH (1,1) model. J. Empir. Financ. 2019, 53, 162–180. [Google Scholar] [CrossRef]

- Xiong, L.; Zhu, F. Robust quasi-likelihood estimation for the negative binomial integer-valued GARCH (1,1) model with an application to transaction counts. J. Stat. Plan. Inference 2019, 203, 178–198. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S.A.; Rubinstein, M. Option pricing: A simplified approach. J. Financ. Econ. 1979, 7, 229–263. [Google Scholar] [CrossRef]

- Boyle, P.P. Option valuation using a tree-jump process. Int. Options J. 1986, 3, 7–12. [Google Scholar]

- Tian, Y. A modified lattice approach to option pricing. J. Futures Mark. 1993, 13, 563–577. [Google Scholar] [CrossRef]

- Figlewski, S.; Gao, B. The adaptive mesh model: A new approach to efficient option pricing. J. Financ. Econ. 1999, 53, 313–351. [Google Scholar] [CrossRef]

- Rubinstein, M. On the relation between binomial and trinomial option pricing models. J. Deriv. 2000, 8, 47–50. [Google Scholar] [CrossRef] [Green Version]

- Liu, R.H. Regime-switching recombining tree for option pricing. Int. J. Theor. Appl. Financ. 2010, 13, 479–499. [Google Scholar] [CrossRef]

- Liu, R.H. A new tree method for pricing financial derivatives in a regime-switching mean-reverting model. Nonlinear Anal. Real World Appl. 2012, 13, 2609–2621. [Google Scholar] [CrossRef]

- Yuen, F.L.; Yang, H. Option pricing with regime switching by trinomial tree method. J. Comput. Appl. Math. 2010, 233, 1821–1833. [Google Scholar] [CrossRef] [Green Version]

- Yuen, F.L.; Yang, H. Pricing Asian options and equity-indexed annuities with regime switching by the trinomial tree method. N. Am. Actuar. J. 2010, 14, 256–272. [Google Scholar] [CrossRef]

- Liu, B.; Xu, L.; Zheng, S.; Tian, G.L. A new test for the proportionality of two large-dimensional covariance matrices. J. Multivar. Anal. 2013, 131, 293–308. [Google Scholar] [CrossRef] [Green Version]

- Lo, C.C.; Nguyen, D.; Skindilias, K. A unified tree approach for options pricing under stochastic volatility models. Financ. Res. Lett. 2017, 20, 260–268. [Google Scholar] [CrossRef]

- Xing, J.; Ma, J. Numerical Methods for System Parabolic Variational Inequalities from Regime-Switching American Option Pricing. Numer. Math. Theory Methods Appl. 2019, 12, 566–593. [Google Scholar]

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef] [Green Version]

- Boyle, P.P. Options: A Monte Carlo approach. J. Financ. Econ. 1977, 4, 323–338. [Google Scholar] [CrossRef]

- Acworth, P.A.; Broadie, M.; Glasserman, P. A comparison of some Monte Carlo and quasi Monte Carlo techniques for option pricing. In Monte Carlo and Quasi-Monte Carlo Methods 1996. Lecture Notes in Statistics; Niederreiter, H., Hellekalek, P., Larcher, G., Zinterhof, P., Eds.; Springer: New York, NY, USA, 1998; Volume 127, pp. 1–18. [Google Scholar]

- Clément, E.; Lamberton, D.; Protter, P. An analysis of a least squares regression method for American option pricing. Financ. Stoch. 2002, 6, 449–471. [Google Scholar] [CrossRef]

- Meinshausen, N.; Hambly, B.M. Monte Carlo Methods for the Valuation of Multiple-Exercise Options. Math. Financ. Int. J. Math. Stat. Financ. Econ. 2004, 14, 557–583. [Google Scholar] [CrossRef] [Green Version]

- Yamada, T.; Yamamoto, K. A second-order discretization with Malliavin weight and Quasi-Monte Carlo method for option pricing. Quant. Financ. 2018, 1–13. [Google Scholar] [CrossRef]

- Bormetti, G.; Callegaro, G.; Livieri, G.; Pallavicini, A. A backward Monte Carlo approach to exotic option pricing. Eur. J. Appl. Math. 2018, 29, 146–187. [Google Scholar] [CrossRef] [Green Version]

- Markowitz, H. Portfolio Selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Black, F.; Litterman, R. Global Portfolio Optimization. Financ. Anal. J. 1992, 48, 28–43. [Google Scholar] [CrossRef]

- Siegel, A.F.; Woodgate, A. Performance of Portfolios Optimized with Estimation Error. Manag. Sci. 2007, 53, 1005–1015. [Google Scholar] [CrossRef] [Green Version]

- Ledoit, O.; Wolf, M. A well-conditioned estimator for large-dimensional covariance matrices. J. Multivar. Anal. 2004, 88, 365–411. [Google Scholar] [CrossRef] [Green Version]

- Levy, M.; Roll, R. The Market Portfolio May Be Mean/Variance Efficient After All. Rev. Financ. Stud. 2010, 23, 2464–2491. [Google Scholar] [CrossRef]

- Li, H.; Bai, Z. Extreme eigenvalues of large dimensional quaternion sample covariance matrices. J. Stat. Plan. Inference 2015, 159, 1–14. [Google Scholar] [CrossRef]

- Wu, T.L.; Li, P. Projected tests for high-dimensional covariance matrices. J. Stat. Plan. Inference 2020, 207, 73–85. [Google Scholar] [CrossRef]

- Christie, A.A. The stochastic behavior of common stock variances: Value, leverage and interest rate effects. J. Financ. Econ. 1982, 10, 407–432. [Google Scholar] [CrossRef]

- Poterba, J.M.; Summers, L.H. The Persistence of Volatility and Stock Market Fluctuations. Am. Econ. Rev. 1986, 76, 1142–1151. [Google Scholar]

- French, K.R.; Schwert, G.W.; Stambaugh, R.F. Expected stock returns and volatility. J. Financ. Econ. 1987, 19, 3–29. [Google Scholar] [CrossRef] [Green Version]

- Bruno, S.; Chincarini, L. A historical examination of optimal real return portfolios for non-US investors. Rev. Financ. Econ. 2010, 19, 161–178. [Google Scholar] [CrossRef]

- Ning, C.; Xu, D.; Wirjanto, T.S. Is volatility clustering of asset returns asymmetric? J. Bank. Financ. 2015, 52, 62–76. [Google Scholar] [CrossRef] [Green Version]

- He, X.Z.; Li, K.; Wang, C. Volatility clustering: A nonlinear theoretical approach. J. Econ. Behav. Organ. 2016, 130, 274–297. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.F. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Ding, Z.; Granger, C.W.J.; Engle, R.F. A long memory property of stock market returns and a new model. J. Empir. Financ. 1993, 1, 83–106. [Google Scholar] [CrossRef]

- Yip, I.W.H.; So, M.K.P. Simplified specifications of a multivariate generalized autoregressive conditional heteroscedasticity model. Math. Comput. Simul. 2009, 80, 327–340. [Google Scholar] [CrossRef]

- Chan, W.S.; Wong, C.S.; Chung, A.H.L. Modelling Australian interest rate swap spreads by mixture autoregressive conditional heteroscedastic processes. Math. Comput. Simul. 2009, 79, 2779–2786. [Google Scholar] [CrossRef]

- Zambom, A.Z.; Kim, S. Lag selection and model specification testing in nonparametric autoregressive conditional heteroscedastic models. J. Stat. Plan. Inference 2017, 186, 13–27. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Hull, J.; White, A. The Pricing of Options on Assets with Stochastic Volatilities. J. Financ. 1987, 42, 281–300. [Google Scholar] [CrossRef]

- Engle, R.F.; Rosenberg, J.V. GARCH Gamma. J. Deriv. 1995, 2, 47–59. [Google Scholar] [CrossRef]

- Duan, J.-C. The GARCH option pricing model. Math. Financ. 1995, 5, 13–32. [Google Scholar] [CrossRef]

- Amin, K.I.; NG, V.K. Option Valuation with Systematic Stochastic Volatility. J. Financ. 1993, 48, 881–910. [Google Scholar] [CrossRef]

- Härdle, W.; Hafner, C.M. Discrete time option pricing with flexible volatility estimation. Financ. Stoch. 2000, 4, 189–207. [Google Scholar] [CrossRef] [Green Version]

- Muroi, Y.; Suda, S. Discrete Malliavin calculus and computations of greeks in the binomial tree. Eur. J. Oper. Res. 2013, 231, 349–361. [Google Scholar] [CrossRef]

- Kim, K.I.; Park, H.S.; Qian, X.S. A mathematical modeling for the lookback option with jumpdiffusion using binomial tree method. J. Comput. Appl. Math. 2011, 235, 5140–5154. [Google Scholar] [CrossRef] [Green Version]

- Schwert, G.W. Why Does Stock Market Volatility Change Over Time? J. Financ. 1989, 44, 1115–1153. [Google Scholar] [CrossRef]

- Bollerslev, T. A conditionally heteroskedastic time series model for speculative prices and rates of return. Rev. Econ. Stat. 1987, 69, 542–547. [Google Scholar] [CrossRef] [Green Version]

- Hansen, P.R.; Lunde, A. A forecast comparison of volatility models: Does anything beat a GARCH (1,1)? J. Appl. Econom. 2005, 20, 873–889. [Google Scholar] [CrossRef] [Green Version]

- Harvey, A.; Ruiz, E.; Shephard, N. Multivariate Stochastic Variance Models. Rev. Econ. Stud. 1994, 61, 247–264. [Google Scholar] [CrossRef] [Green Version]

- Ljung, G.M.; Box, G.E.P. On a measure of lack of fit in time series models. Biometrika 1978, 65, 297–303. [Google Scholar] [CrossRef]

- Said, S.E.; Dickey, D.A. Testing for unit roots in autoregressive-moving average models of unknown order. Biometrika 1984, 71, 599–607. [Google Scholar] [CrossRef]

- Hwang, S.; Valls Pereira, P.L. Small sample properties of GARCH estimates and persistence. Eur. J. Financ. 2006, 12, 473–494. [Google Scholar] [CrossRef]

- Kwok, Y.K. Mathematical Models of Financial Derivatives; Springer: Berlin, Germany, 2008. [Google Scholar]

- Diebold, F.X.; Mariano, R.S. Comparing Predictive Accuracy. J. Bus. Econ. Stat. 1995, 13, 253–263. [Google Scholar]

- Harvey, D.; Leybourne, S.; Newbold, P. Testing the equality of prediction mean squared errors. Int. J. Forecast. 1997, 13, 281–291. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| ISIN | Option | Underlying | |||||

|---|---|---|---|---|---|---|---|

| LU1910406781 | CALL | DAX XETRA | 11,401.9697 | 10,000 | 10,000 | 20/02/2019 | 20/06/2019 |

| LU1910406864 | CALL | DAX XETRA | 11,401.9697 | 10,200 | 10,200 | 20/02/2019 | 20/06/2019 |

| LU1910406948 | CALL | DAX XETRA | 11,401.9697 | 10,400 | 10,400 | 20/02/2019 | 20/06/2019 |

| LU1910407086 | CALL | DAX XETRA | 11,401.9697 | 10,600 | 10,600 | 20/02/2019 | 20/06/2019 |

| LU1910407169 | CALL | DAX XETRA | 11,401.9697 | 10,800 | 10,800 | 20/02/2019 | 20/06/2019 |

| Panel A: Mean Equation | |||||

| Estimate | t-statistic | Statistic | p-value | ||

| −0.0202 | (−0.4508) | 0.0406 | (0.8402) | ||

| 0.0420 | (0.9221) | 1.4408 | (1.0000) | ||

| 0.0578 | (1.2815) | 4.6828 | (0.9969) | ||

| −0.0929 | (−2.0524) ** | ||||

| Panel B: Variance Equation | |||||

| Estimate | t-statistic | Statistic | p-value | ||

| 0.0000 | (0.484) | 0.6697 | (0.4132) | ||

| 0.0309 | (1.9086) * | 1.2142 | (0.6706) | ||

| 0.9603 | (51.841) *** | 1.6574 | (0.7893) | ||

| Panel C: Information Criteria | |||||

| Criteria | SBT | ||||

| −6.6969 | −6.6303 | −6.6974 | −6.6708 | 1709.023 | |

| Panel A: H = 10,000 points | |||||

| MSE | RMSE | MAE | DM | HLN | |

| Historical Binomial Tree | 0.0018 | 0.0421 | 0.0414 | (−6.0215) *** | (−5.8764) *** |

| GARCH (1,1) Binomial Tree | 0.0021 | 0.0456 | 0.0453 | (−8.0947) *** | (−7.8997) *** |

| Historical Trinomial Tree | 0.0037 | 0.0609 | 0.0598 | (−14.3151) *** | (−13.9701) *** |

| GARCH (1,1) Trinomial Tree | 0.0005 | 0.0233 | 0.0217 | ||

| Black Scholes | 0.0018 | 0.0426 | 0.0408 | (−4.6595) *** | (−4.5472) *** |

| Panel B: H = 10,200 points | |||||

| MSE | RMSE | MAE | DM | HLN | |

| Historical Binomial Tree | 0.0015 | 0.0384 | 0.0376 | (−3.9991) *** | (−3.9027) *** |

| GARCH (1,1) Binomial Tree | 0.0019 | 0.0437 | 0.0432 | (−5.8409) *** | (−5.7001) *** |

| Historical Trinomial Tree | 0.0041 | 0.0637 | 0.0624 | (−11.7658) *** | (−11.4822) *** |

| GARCH (1,1) Trinomial Tree | 0.0007 | 0.0255 | 0.0239 | ||

| Black Scholes | 0.0022 | 0.0472 | 0.0457 | (−5.0449) *** | (−4.9233) *** |

| Panel C: H = 10,400 points | |||||

| MSE | RMSE | MAE | DM | HLN | |

| Historical Binomial Tree | 0.0014 | 0.0369 | 0.0351 | (−1.8947) ** | (−1.8490) ** |

| GARCH (1,1) Binomial Tree | 0.0016 | 0.0402 | 0.0395 | (−3.2823) *** | (−3.2032) *** |

| Historical Trinomial Tree | 0.0037 | 0.0610 | 0.0596 | (−8.8007) *** | (−8.5886) *** |

| GARCH (1,1) Trinomial Tree | 0.0008 | 0.0291 | 0.0273 | ||

| Black Scholes | 0.0023 | 0.0475 | 0.0468 | (−6.0777) *** | (−5.9312) *** |

| Panel D: H = 10,600 points | |||||

| MSE | RMSE | MAE | DM | HLN | |

| Historical Binomial Tree | 0.0010 | 0.0314 | 0.0285 | ||

| GARCH (1,1) Binomial Tree | 0.0012 | 0.0340 | 0.0332 | (−0.9514) | (−0.9284) |

| Historical Trinomial Tree | 0.0039 | 0.0625 | 0.0598 | (−5.0877) *** | (−4.9651) *** |

| GARCH (1,1) Trinomial Tree | 0.0011 | 0.0333 | 0.0316 | (−0.4572) | (−0.4462) |

| Black Scholes | 0.0015 | 0.0382 | 0.0370 | (−2.1074) ** | (−2.0567) ** |

| Panel E: H = 10,800 points | |||||

| MSE | RMSE | MAE | DM | HLN | |

| Historical Binomial Tree | 0.0010 | 0.0312 | 0.0274 | (1.3958) * | (−1.3622) * |

| GARCH (1,1) Binomial Tree | 0.0007 | 0.0266 | 0.0256 | ||

| Historical Trinomial Tree | 0.0049 | 0.0703 | 0.0667 | (−5.8032) *** | (−5.6633) *** |

| GARCH (1,1) Trinomial Tree | 0.0014 | 0.0374 | 0.0362 | (−3.0474) *** | (−2.9739) *** |

| Black Scholes | 0.0013 | 0.0360 | 0.0343 | (−4.3492) *** | (−4.2443) *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Esparcia, C.; Ibañez, E.; Jareño, F. Volatility Timing: Pricing Barrier Options on DAX XETRA Index. Mathematics 2020, 8, 722. https://doi.org/10.3390/math8050722

Esparcia C, Ibañez E, Jareño F. Volatility Timing: Pricing Barrier Options on DAX XETRA Index. Mathematics. 2020; 8(5):722. https://doi.org/10.3390/math8050722

Chicago/Turabian StyleEsparcia, Carlos, Elena Ibañez, and Francisco Jareño. 2020. "Volatility Timing: Pricing Barrier Options on DAX XETRA Index" Mathematics 8, no. 5: 722. https://doi.org/10.3390/math8050722

APA StyleEsparcia, C., Ibañez, E., & Jareño, F. (2020). Volatility Timing: Pricing Barrier Options on DAX XETRA Index. Mathematics, 8(5), 722. https://doi.org/10.3390/math8050722