Did Institutional Investors’ Behavior Affect U.S.-China Equity Market Sentiment? Evidence from the U.S.-China Trade Turbulence

Abstract

:1. Introduction

2. Literature Review and Hypothesis

3. Methodology

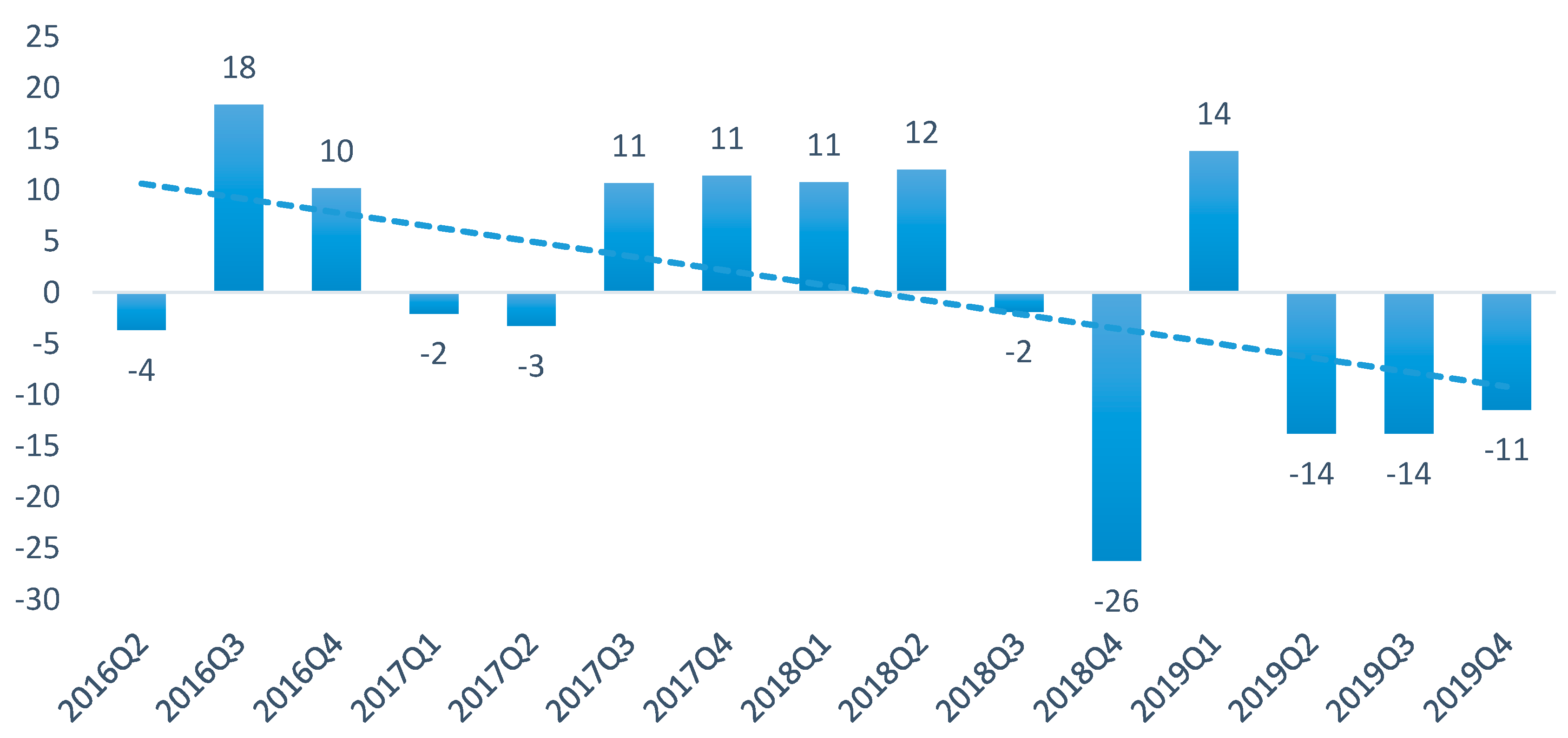

3.1. Equity Market Sentiment Index

3.2. Institutional Ownership

- Independent institutional ownership (): institutional ownership by independent institutions (a1: hedge fund managers; a2: investment managers; a3: sovereign wealth funds, and a4: VC/PE firms) as a percentage of shares outstanding:

- Gray institutional ownership (): institutional ownership by gray institutions (b1: banks, b2: insurance companies, b3: family offices/trusts, b4: REITs, b5: corporate pensions, b6: government pensions, b7: union pension sponsors, b8: charitable foundations, b9: educational/cultural endowments, and b10: unclassified funds) as a percentage of shares outstanding:

3.3. Control Variables

- Market capitalization (SIZE): the logarithm of quarterly market capitalization:

- Price-to-earnings ratio (P/E): the current share price relative to its quarterly earnings per share (EPS):

4. Empirical Results

4.1. Descriptive Statistics

4.2. Spearman Correlation between Variables

4.3. Dynamic Panel Data Estimation Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- US Manufacturing Survey Shows Worst Reading in a Decade. Available online: https://www.cnbc.com/2019/10/01/us-manufacturing-economy-contracts-to-worst-level-in-a-decade.html (accessed on 1 October 2019).

- Carvalho, M.; De Azevedo, A.F.Z.; Massuquetti, A. Emerging Countries and the Effects of the Trade War between US and China. Economies 2019, 7, 45. [Google Scholar] [CrossRef] [Green Version]

- Feng, Z.; Zhou, W.; Ming, Q. Embodied Energy Flow Patterns of the Internal and External Industries of Manufacturing in China. Sustainability 2019, 11, 438. [Google Scholar] [CrossRef] [Green Version]

- Zhang, D.; Lei, L.; Ji, Q.; Kutan, A.M. Economic policy uncertainty in the US and China and their impact on the global markets. Econ. Model. 2019, 79, 47–56. [Google Scholar] [CrossRef]

- ROB Manufacturing Data. Available online: https://www.instituteforsupplymanagement.org/news/content.cfm?ItemNumber=28859&SSO=1 (accessed on 15 October 2019).

- McNulty, T.; Nordberg, D. Ownership, Activism and Engagement: Institutional Investors as Active Owners. Corp. Gov. Int. Rev. 2015, 24, 346–358. [Google Scholar] [CrossRef] [Green Version]

- Lin, S.L.; Lu, J.; Su, J.-B.; Chen, W.-P. Sustainable Returns: The Effect of Regional Industrial Development Policy on Institutional Investors’ Behavior in China. Sustainability 2018, 10, 2769. [Google Scholar] [CrossRef] [Green Version]

- Lu, J. The Behavior of Institutional Investors on Regional Industrial Development Policy and Stock Return Volatility in China. Ph.D. Thesis, National Taipei University of Technology, Taipei, Taiwan, 2019. [Google Scholar]

- Lin, S.-L.; Lu, J. Institutional Investors and Corporate Performance: Insights from China. Sustainability 2019, 11, 6010. [Google Scholar] [CrossRef] [Green Version]

- Renault, T. Intraday online investor sentiment and return patterns in the U.S. stock market. J. Bank. Financ. 2017, 84, 25–40. [Google Scholar] [CrossRef]

- Brown, G.W.; Cliff, M.T. Investor Sentiment and Asset Valuation. J. Bus. 2005, 78, 405–440. [Google Scholar] [CrossRef]

- Bandopadhyaya, A.; Jones, A.L. Measuring Investor Sentiment in Equity Markets. J. Asset Manag. 2006, 6, 258–269. [Google Scholar] [CrossRef]

- Eichengreen, B.; Mody, A. Interest Rates in the North and Capital Flows to the South: Is There a Missing Link? Int. Financ. 1998, 1, 35–57. [Google Scholar] [CrossRef] [Green Version]

- Baek, I.; Bandopadhyaya, A.; Du, C. Determinants of market-assessed sovereign risk: Economic fundamentals or market risk appetite? J. Int. Money Financ. 2005, 24, 533–548. [Google Scholar] [CrossRef]

- Feng, X.; Zhou, M.; Chan, K.C. Smart money or dumb money? A study on the selection ability of mutual fund investors in China. N. Am. J. Econ. Financ. 2014, 30, 154–170. [Google Scholar] [CrossRef]

- Hirshleifer, D.; Teoh, S.H. Herd Behaviour and Cascading in Capital Markets: A Review and Synthesis. Eur. Financ. Manag. 2003, 9, 25–66. [Google Scholar] [CrossRef]

- Shleifer, A. Overconfident Investors, Predictable Returns, and Excessive Trading. J. Econ. Perspect. 2015, 29, 61–88. [Google Scholar]

- Foucault, T.; Sraer, D.; Thesmar, D.J. Individual Investors and Volatility. J. Financ. 2011, 66, 1369–1406. [Google Scholar] [CrossRef]

- Naughton, B. Transitions and Growth; Massachusetts Institute of Technology Press: Cambridge, MA, USA, 2007; p. 528. ISBN 13: 978-0262640640. [Google Scholar]

- Li, N.; Nguyen, Q.N.; Pham, P.K.; Wei, S. Large Foreign Ownership and Firm-Level Stock Return Volatility in Emerging Markets. J. Financ. Quant. Anal. 2011, 46, 1127–1155. [Google Scholar] [CrossRef] [Green Version]

- Gillan, S.L.; Starks, L.T. Corporate Governance, Corporate Ownership, and the Role of Institutional Investors: A Global Perspective. SSRN Electron. J. 2003, 13, 4–22. [Google Scholar] [CrossRef] [Green Version]

- Roach, L. The UK Stewardship Code. J. Corp. Law Stud. 2011, 11, 463–493. [Google Scholar] [CrossRef]

- Lin, J.-C.; Lee, Y.-T.; Liu, Y.-J. IPO auctions and private information. J. Bank. Financ. 2007, 31, 1483–1500. [Google Scholar] [CrossRef]

- West, K.D. Dividend Innovations and Stock Price Volatility. Econometrica 1988, 56, 37. [Google Scholar] [CrossRef]

- Grinblatt, M. The investment behavior and performance of various investor types: A study of Finland’s unique data set. J. Financ. Econ. 2000, 55, 43–67. [Google Scholar] [CrossRef]

- Kaniel, R.; Saar, G.; Titman, S. Individual Investor Trading and Stock Returns. J. Financ. 2008, 63, 273–310. [Google Scholar] [CrossRef]

- Ahmed, W. The trading patterns and performance of individualvis-à-visinstitutional investors in the Qatar Exchange. Rev. Account. Financ. 2014, 13, 24–42. [Google Scholar] [CrossRef]

- Panda, B.; Leepsa, N.M. Institutional Ownership Activism, Market Performance, and Financial Crisis: Evidence from an Emerging Market. Asia Pac. Soc. Sci. Rev. 2018, 17, 44–62. [Google Scholar]

- Arora, R.K. The Relation between Investment of Domestic and Foreign Institutional Investors and Stock Returns in India. Glob. Bus. Rev. 2016, 17, 654–664. [Google Scholar] [CrossRef]

- De Long, J.B.; Shleifer, A.; Summers, L.H.; Waldmann, R.J. Positive feedback investment strategies and destabilizing rational speculation. J. Financ. 1990, 45, 379–395. [Google Scholar] [CrossRef] [Green Version]

- Bikhchandani, S.; Hirshleifer, D.; Welch, I. A Theory of Fads, Fashion, Custom, and Cultural Change as Informational Cascades. J. Political Econ. 1992, 100, 992–1026. [Google Scholar] [CrossRef]

- Hirshleifer, D.; Subrahmanyam, A.; Titman, S. Security analysis and trading patterns when some investors receive information before others. J. Financ. 1994, 49, 1665–1698. [Google Scholar] [CrossRef]

- Hong, H.; Stein, J.C. A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets. J. Financ. 1999, 54, 2143–2184. [Google Scholar] [CrossRef] [Green Version]

- Gruber, M.J. Another puzzle: The growth in actively managed mutual funds. J. Financ. 1996, 51, 783–810. [Google Scholar] [CrossRef]

- Zheng, L. Is Money Smart? A Study of Mutual Fund Investors’ Fund Selection Ability. J. Financ. 1999, 54, 901–933. [Google Scholar] [CrossRef]

- Sapp, T.; Tiwari, A. Does Stock Return Momentum Explain the “Smart Money” Effect? J. Financ. 2004, 59, 2605–2622. [Google Scholar] [CrossRef]

- Munoz, F.; Vargas, M.; Vicente, R. Fund flow bias in market timing skill. Evidence of the clientele effect. Int. Rev. Econ. Financ. 2014, 33, 257–269. [Google Scholar] [CrossRef]

- Zhang, Y.; Cao, X.; He, F.; Zhang, W. Network topology analysis approach on China’s QFII stock investment behavior. Phys. A Stat. Mech. Its Appl. 2017, 473, 77–88. [Google Scholar] [CrossRef]

- Feng, X.; Hu, N.; Johansson, A.C. Ownership, analyst coverage, and stock synchronicity in China. Int. Rev. Financ. Anal. 2016, 45, 79–96. [Google Scholar] [CrossRef] [Green Version]

- Korkeamäki, T.; Virk, N.; Wang, H.; Wang, P. Learning Chinese? The changing investment behavior of foreign institutions in the Chinese stock market. Int. Rev. Financ. Anal. 2019, 64, 190–203. [Google Scholar] [CrossRef]

- Zou, L.; Tang, T.; Li, X.-M. The stock preferences of domestic versus foreign investors: Evidence from Qualified Foreign Institutional Investors (QFIIs) in China. J. Multinatl. Financ. Manag. 2016, 37, 12–28. [Google Scholar] [CrossRef]

- Ferreira, M.A.; Matos, P. The colors of investors’ money: The role of institutional investors around the world. J. Financ. Econ. 2008, 88, 499–533. [Google Scholar] [CrossRef]

- Aggarwal, R.; Erel, I.; Ferreira, M.A.; Matos, P. Does governance travel around the world? Evidence from institutional investors. J. Financ. Econ. 2011, 100, 154–181. [Google Scholar] [CrossRef]

- Aggarwal, R.; Hu, M.; Yang, J. Fraud, Market Reaction, and the Role of Institutional Investors in Chinese Listed Firms. J. Portf. Manag. 2015, 41, 92–109. [Google Scholar] [CrossRef]

- Almazan, A.; Hartzell, J.C.; Starks, L.T. Active Institutional Shareholders and Costs of Monitoring: Evidence from Executive Compensation. Financ. Manag. 2005, 34, 5–34. [Google Scholar] [CrossRef]

- Baur, D.G.; Lucey, B.M. Is Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds and Gold. Financ. Rev. 2010, 45, 217–229. [Google Scholar] [CrossRef]

- Baur, D.G.; McDermott, T.K. Is gold a safe haven? International evidence. J. Bank. Financ. 2010, 34, 1886–1898. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | No. of Obs. | Minimum | Maximum | Mean | Std. Dev. |

|---|---|---|---|---|---|

| Dependent variable | |||||

| EMSI of S&P 500 | 36,077 | −26.231 | 18.369 | 0.530 | 12.584 |

| Institutional ownership variables (%) | |||||

| Total institutions (Total_IOu) | 36,077 | 0.001 | 100.000 | 62.926 | 27.764 |

| Independent institutions (Indep_IOu) | 36,077 | 0.000 | 98.620 | 57.048 | 26.574 |

| Hedge fund managers | 36,077 | 0.000 | 54.050 | 4.628 | 4.667 |

| Investment managers | 36,077 | 0.000 | 96.350 | 51.903 | 25.243 |

| Sovereign wealth funds | 36,077 | 0.000 | 6.160 | 0.064 | 0.339 |

| VC/PE firms | 36,077 | 0.000 | 17.030 | 0.454 | 0.880 |

| Gray institutions (Gray_IOu) | 36,077 | 0.000 | 97.513 | 5.881 | 5.255 |

| Banks | 36,077 | 0.000 | 86.100 | 2.267 | 2.514 |

| Charitable foundations | 36,077 | 0.000 | 41.470 | 0.128 | 1.041 |

| Corporate pensions | 36,077 | 0.000 | 29.720 | 0.265 | 0.921 |

| Educational/cultural endowments | 36,077 | 0.000 | 59.870 | 0.100 | 1.414 |

| Family offices/trusts | 36,077 | 0.000 | 94.040 | 0.740 | 2.182 |

| Government pensions | 36,077 | 0.000 | 31.640 | 1.873 | 1.830 |

| Insurance companies | 36,077 | 0.000 | 25.490 | 0.125 | 0.937 |

| REITs | 36,077 | 0.000 | 80.940 | 0.277 | 2.586 |

| Unclassified | 36,077 | 0.000 | 63.760 | 0.096 | 1.184 |

| Union pension sponsors | 36,077 | 0.000 | 9.870 | 0.010 | 0.198 |

| Firm-level control variables | |||||

| Log market capitalization (SIZEu) | 36,077 | 1.320 | 13.950 | 7.926 | 1.909 |

| Price-to-earnings ratio (P/Eu) | 36,077 | 0.010 | 299.300 | 30.832 | 36.332 |

| Variables | No. of Obs. | Minimum | Maximum | Mean | Std. Dev. |

|---|---|---|---|---|---|

| Dependent variable | |||||

| EMSI of CSI 300 | 43,954 | −24.346 | 26.747 | −1.431 | 14.716 |

| Institutional ownership variables (%) | |||||

| Total institutions (Total_IOc) | 43,954 | 0.001 | 86.180 | 9.468 | 8.660 |

| Independent institutions (Indep_IOc) | 43,954 | 0.000 | 82.350 | 7.723 | 7.260 |

| Hedge fund managers | 43,954 | 0.000 | 4.250 | 0.024 | 0.200 |

| Investment managers | 43,954 | 0.000 | 80.010 | 5.788 | 6.678 |

| Sovereign wealth funds | 43,954 | 0.000 | 9.520 | 0.892 | 1.254 |

| VC/PE firms | 43,954 | 0.000 | 21.030 | 1.019 | 2.084 |

| Gray institutions (Gray_IOc) | 43,954 | 0.000 | 60.347 | 1.742 | 4.032 |

| Banks | 43,954 | 0.000 | 59.600 | 0.513 | 1.661 |

| Charitable foundations | 43,954 | 0.000 | 11.560 | 0.009 | 0.228 |

| Corporate pensions | 43,954 | 0.000 | 9.210 | 0.013 | 0.228 |

| Educational/cultural endowments | 43,954 | 0.000 | 53.210 | 0.103 | 1.834 |

| Family offices/trusts | 43,954 | 0.000 | 1.380 | 0.000 | 0.017 |

| Government pensions | 43,954 | 0.000 | 4.780 | 0.056 | 0.209 |

| Insurance companies | 43,954 | 0.000 | 38.310 | 0.238 | 1.463 |

| REITs | 43,954 | 0.000 | 42.950 | 0.034 | 0.931 |

| Unclassified | 43,954 | 0.000 | 57.930 | 0.775 | 2.677 |

| Union pension sponsors | 43,954 | 0.000 | 0.088 | 0.000 | 0.001 |

| Firm-level control variables | |||||

| Log market capitalization (SIZEc) | 43,954 | 4.138 | 12.797 | 7.080 | 1.002 |

| Price-to-earnings ratio (P/Ec) | 43,954 | 1.370 | 299.600 | 55.536 | 52.742 |

| Variables | EMSI of S&P 500 | Total_IOu | Indep_IOu | Gray_IOu | SIZEu | P/Eu |

|---|---|---|---|---|---|---|

| EMSI of S&P 500 | 1 | |||||

| Total_IOu | −0.0038 | 1 | ||||

| Indep_IOu | −0.0032 | 0.9797 | 1 | |||

| Gray_IOu | −0.0009 | 0.4737 | 0.3506 | 1 | ||

| SIZEu | 0.0010 | 0.3735 | 0.3457 | 0.4236 | 1 | |

| P/Eu | 0.0407 | 0.1614 | 0.1673 | −0.0017 | 0.0916 | 1 |

| Variables | EMSI of CSI 300 | Total_IOc | Indep_IOc | Gray_IOc | SIZEc | P/Ec |

|---|---|---|---|---|---|---|

| EMSI of CSI 300 | 1 | |||||

| Total_IOc | 0.0124 | 1 | ||||

| Indep_IOc | 0.0147 | 0.9224 | 1 | |||

| Gray_IOc | 0.0116 | 0.4777 | 0.2107 | 1 | ||

| SIZEc | 0.0020 | 0.4482 | 0.4351 | 0.3331 | 1 | |

| P/Ec | 0.0021 | −0.1459 | −0.1337 | −0.1821 | −0.2415 | 1 |

| Variables | EMSI of S&P 500 | |||

|---|---|---|---|---|

| Coeff. | p-Value | Coeff. | p-Value | |

| EMSI S&P 500 (t − 1) | −0.0632 *** | 0.0000 | −0.0633 *** | 0.0000 |

| (0.001) | (0.001) | |||

| Total_IOu | −0.4284 *** | 0.0000 | ||

| (0.026) | ||||

| Indep_IOu | −0.4160 *** | 0.0000 | ||

| (0.027) | ||||

| Gray_IOu | −0.5561 *** | 0.0000 | ||

| (0.073) | ||||

| SIZEu | −1.7934 *** | 0.0002 | −1.7904 *** | 0.0001 |

| (0.476) | (0.472) | |||

| P/Eu | 0.0207 *** | 0.0000 | 0.0207 *** | 0.0000 |

| (0.004) | (0.004) | |||

| Firm fixed | yes | yes | ||

| J-statistic | 2821.19 | 2824.71 | ||

| Prob (J-statistic) | 0.0000 | 0.0000 | ||

| Variables | EMSI of CSI 300 | |||

|---|---|---|---|---|

| Coeff. | p-Value | Coeff. | p-Value | |

| EMSI CSI 300 (t − 1) | −0.2959 *** | 0.0000 | −0.2956 *** | 0.0000 |

| (0.001) | (0.001) | |||

| Total_IOc | 0.4205 *** | 0.0000 | ||

| (0.032) | ||||

| Indep_IOc | 0.4603 *** | 0.0000 | ||

| (0.033) | ||||

| Gray_IOc | 0.3949 *** | 0.0013 | ||

| (0.123) | ||||

| SIZEc | 5.3405 *** | 0.0000 | 5.2461 *** | 0.0000 |

| (0.269) | (0.270) | |||

| P/Ec | −0.0387 *** | 0.0000 | −0.0389 *** | 0.0000 |

| (0.003) | (0.003) | |||

| Firm fixed | yes | yes | ||

| J-statistic | 3410.79 | 3411.97 | ||

| Prob (J-statistic) | 0.0000 | 0.0000 | ||

| Variables | EMSI of S&P 500 | |||

|---|---|---|---|---|

| Coeff. | p-Value | Coeff. | p-Value | |

| EMSI S&P 500(−1) | −0.0274 *** | 0.0000 | −0.0273 *** | 0.0000 |

| (0.002) | (0.002) | |||

| EMSI S&P 500(−2) | −0.0918 *** | 0.0000 | −0.0916 *** | 0.0000 |

| (0.001) | (0.001) | |||

| Total_IOu | −0.1405 *** | 0.0000 | ||

| (0.023) | ||||

| Total_IOu(−1) | −0.2905 *** | 0.0000 | ||

| (0.027) | ||||

| Indep_IOu | −0.1207 *** | 0.0000 | ||

| (0.024) | ||||

| Indep_IOu(−1) | −0.3014 *** | 0.0000 | ||

| (0.028) | ||||

| Gray_IOu | −0.3552 *** | 0.0000 | ||

| (0.067) | ||||

| Gray_IOu(−1) | −0.1670 | 0.0569 | ||

| (0.088) | ||||

| SIZEu | 5.3046 *** | 0.0000 | 5.3080 *** | 0.0000 |

| (0.464) | (0.466) | |||

| P/Eu | 0.0136 ** | 0.0017 | 0.0140 ** | 0.0014 |

| (0.004) | (0.004) | |||

| P/Eu(−1) | 0.0137 *** | 0.0006 | 0.0131 ** | 0.0011 |

| (0.004) | (0.004) | |||

| Firm fixed | yes | yes | ||

| J-statistic | 2682.6 | 2679.97 | ||

| Prob (J-statistic) | 0.0000 | 0.0000 | ||

| Variables | EMSI of CSI 300 | |||

|---|---|---|---|---|

| Coeff. | p-Value | Coeff. | p-Value | |

| EMSI CSI 300(−1) | −0.2736 *** | 0.0000 | −0.2726 *** | 0.0000 |

| (0.002) | (0.002) | |||

| EMSI CSI 300(−2) | 0.0526 *** | 0.0000 | 0.0529 *** | 0.0000 |

| (0.002) | (0.002) | |||

| Total_IOc | 0.4109 *** | 0.0000 | ||

| (0.038) | ||||

| Total_IOc(−1) | 0.2687 *** | 0.0000 | ||

| (0.035) | ||||

| Indep_IOc | 0.4898 *** | 0.0000 | ||

| (0.040) | ||||

| Indep_IOc(−1) | 0.2261 *** | 0.0000 | ||

| (0.036) | ||||

| Gray_IOc | 0.1952 | 0.1470 | ||

| (0.135) | ||||

| Gray_IOc(−1) | 0.4468 *** | 0.0005 | ||

| (0.129) | ||||

| SIZEc | 7.1444 *** | 0.0000 | 7.0698 *** | 0.0000 |

| (0.331) | (0.334) | |||

| P/Ec | 0.0207 *** | 0.0000 | 0.0200 *** | 0.0000 |

| (0.004) | (0.004) | |||

| P/Ec(−1) | −0.0718 *** | 0.0000 | −0.0717 *** | 0.0000 |

| (0.004) | (0.004) | |||

| Firm fixed | yes | yes | ||

| J-statistic | 3361.39 | 3360.88 | ||

| Prob (J-statistic) | 0.0000 | 0.0000 | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lin, S.-L.; Lu, J. Did Institutional Investors’ Behavior Affect U.S.-China Equity Market Sentiment? Evidence from the U.S.-China Trade Turbulence. Mathematics 2020, 8, 952. https://doi.org/10.3390/math8060952

Lin S-L, Lu J. Did Institutional Investors’ Behavior Affect U.S.-China Equity Market Sentiment? Evidence from the U.S.-China Trade Turbulence. Mathematics. 2020; 8(6):952. https://doi.org/10.3390/math8060952

Chicago/Turabian StyleLin, Shu-Ling, and Jun Lu. 2020. "Did Institutional Investors’ Behavior Affect U.S.-China Equity Market Sentiment? Evidence from the U.S.-China Trade Turbulence" Mathematics 8, no. 6: 952. https://doi.org/10.3390/math8060952

APA StyleLin, S. -L., & Lu, J. (2020). Did Institutional Investors’ Behavior Affect U.S.-China Equity Market Sentiment? Evidence from the U.S.-China Trade Turbulence. Mathematics, 8(6), 952. https://doi.org/10.3390/math8060952