Optimal Reinsurance Problem under Fixed Cost and Exponential Preferences

Abstract

:1. Introduction

2. Problem Formulation

2.1. Model Formulation

2.2. The Utility Maximization Problem

3. The Pure Reinsurance Problem

4. Reduction to an Optimal Stopping Problem

5. The Optimal Stopping Problem

- If the stopping region is not empty, that is , , we know that , hence , which implies and is optimal for problem (24).

- If the stopping region is not empty, for , we have that , otherwise, by continuity of both the functions, if (or ), the same inequality holds in a neighborhood of , which contradicts that , . Then, and is optimal for problem (24).

- If the continuation region is not empty, that is , , repeating the localization argument with the stopping time , we getas a consequence and is optimal for problem (24).

- Finally, for , by assumption, , , is optimal for problem (24) and this concludes the proof.

- 1.

- Ifthen and , so that , implying that .

- 2.

- Ifthen and ; in this case .

- 3.

- Ifthen and , so that .

- If , then .

- If , then there exists such that and .

- (i)

- When , we have that by Remark 3 and it easy to verify that H is increasing in , while it is decreasing in . Hence, it takes the maximum value at . As a consequence, if we have that , being .Otherwise, if there exists such that , that is , and , that is .

- (ii)

- When , by Lemma 2 we get that H is increasing in and we can repeat the same arguments as in the previous case to distinguish the two casese and , obtaining the same results.

- (iii)

- When , by Remark 3, we know that H is decreasing in , so that , that is , . Moreover, in this case, .

- If , then .

- If , then , where is the unique solution to equation

- (1)

- If , then the continuation region is , the value function isand is an optimal stopping time.

- (2)

- If , then , where is the unique solution to , the value function isand , given byis an optimal stopping time.

6. Solution to the Original Problem

- (1)

- If , then , that is no reinsurance is purchased.

- (2)

- If , then , that is the optimal choice for the insurer consists in stipulating the contract at the initial time, selecting the optimal retention level (as in the pure reinsurance problem).

- If , thenand , that is no reinsurance is purchased.

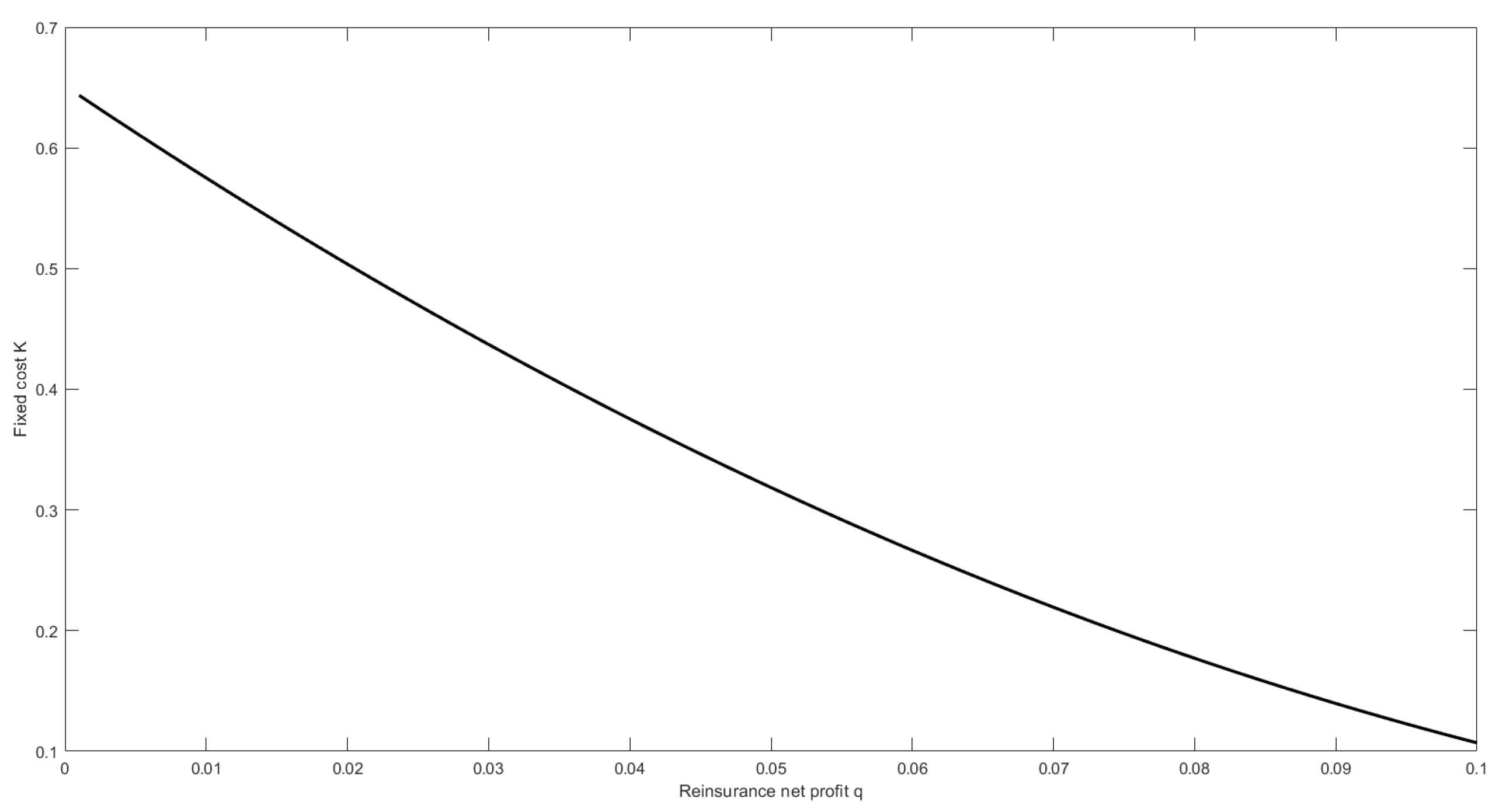

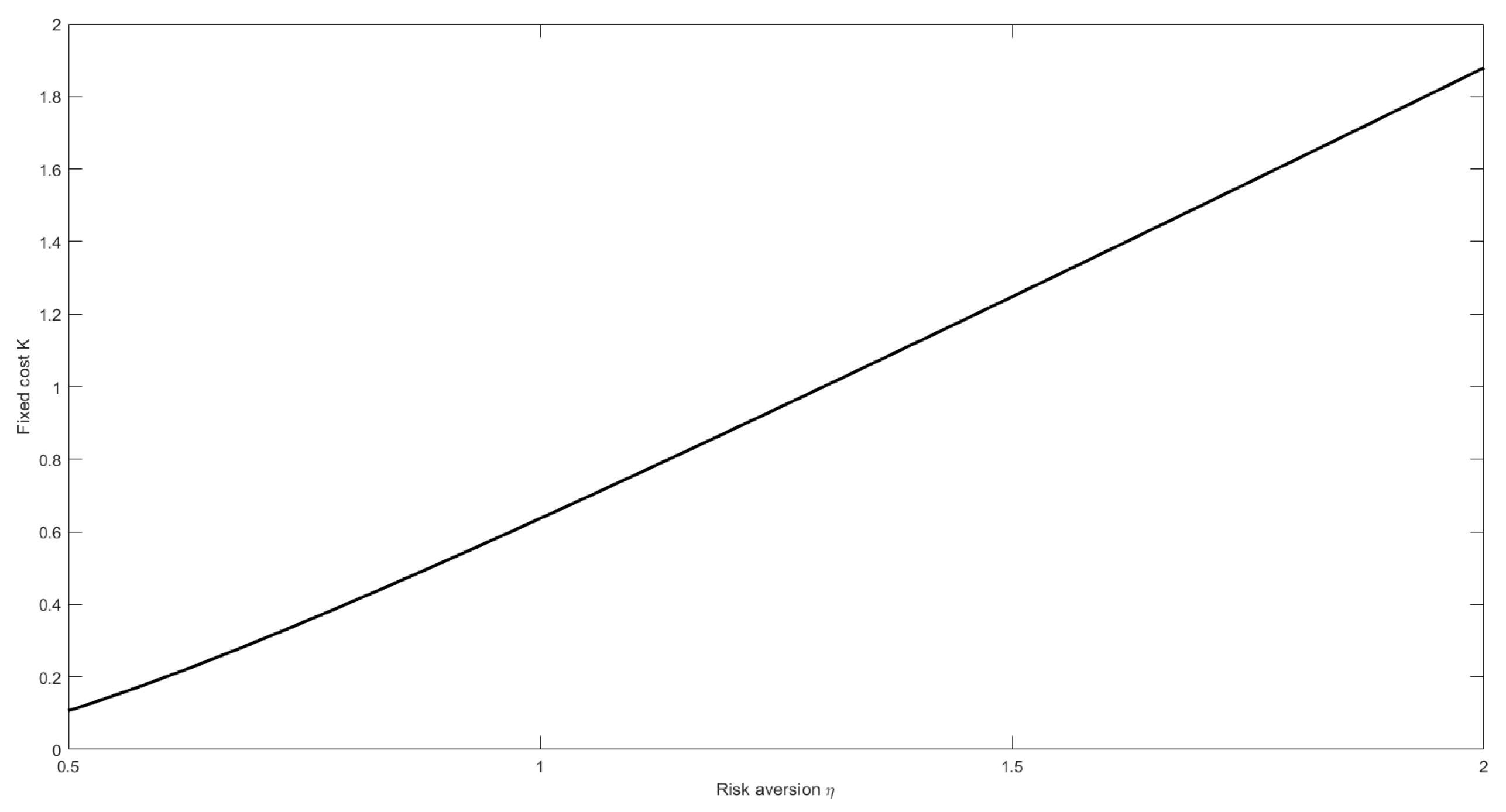

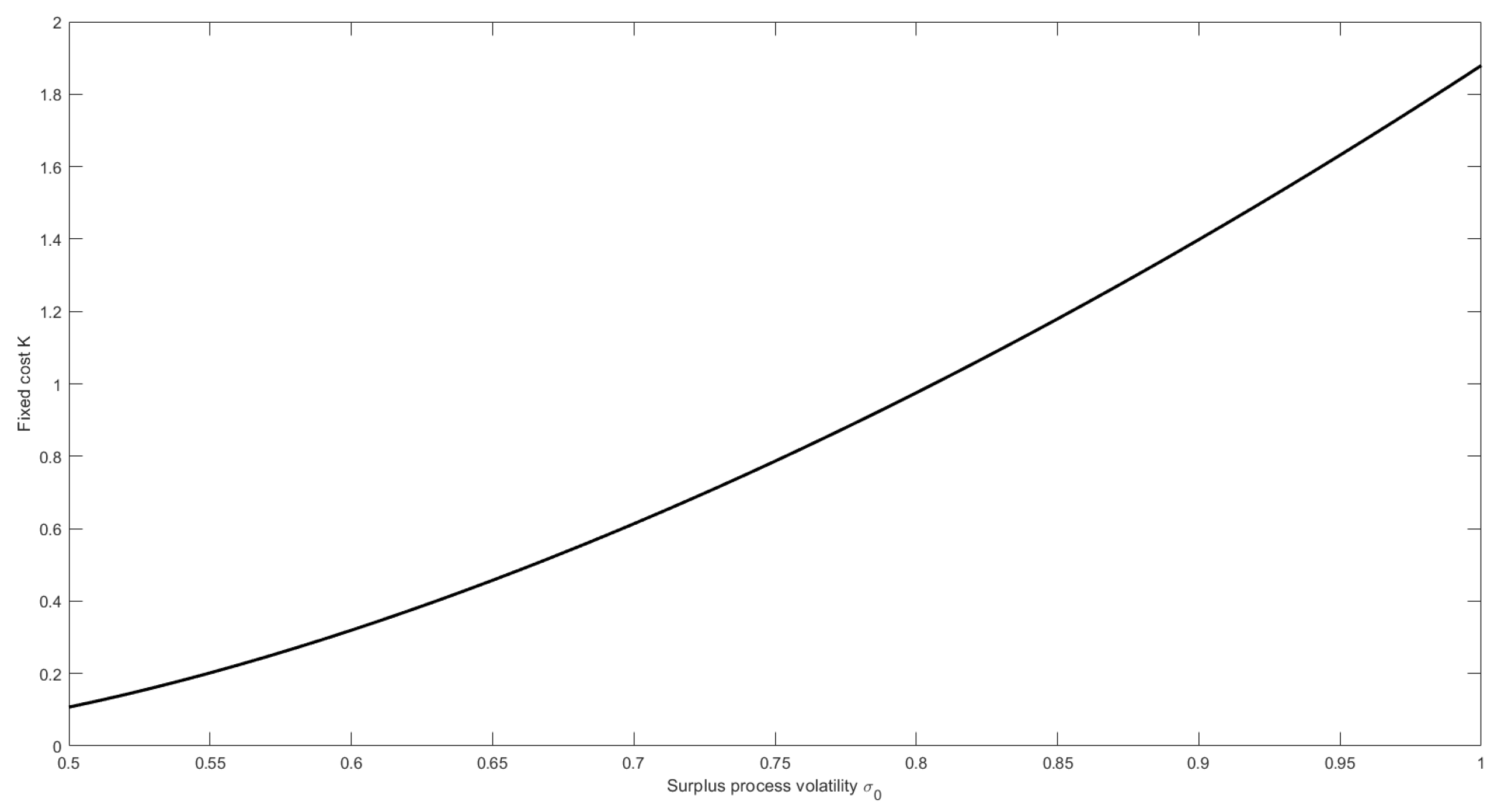

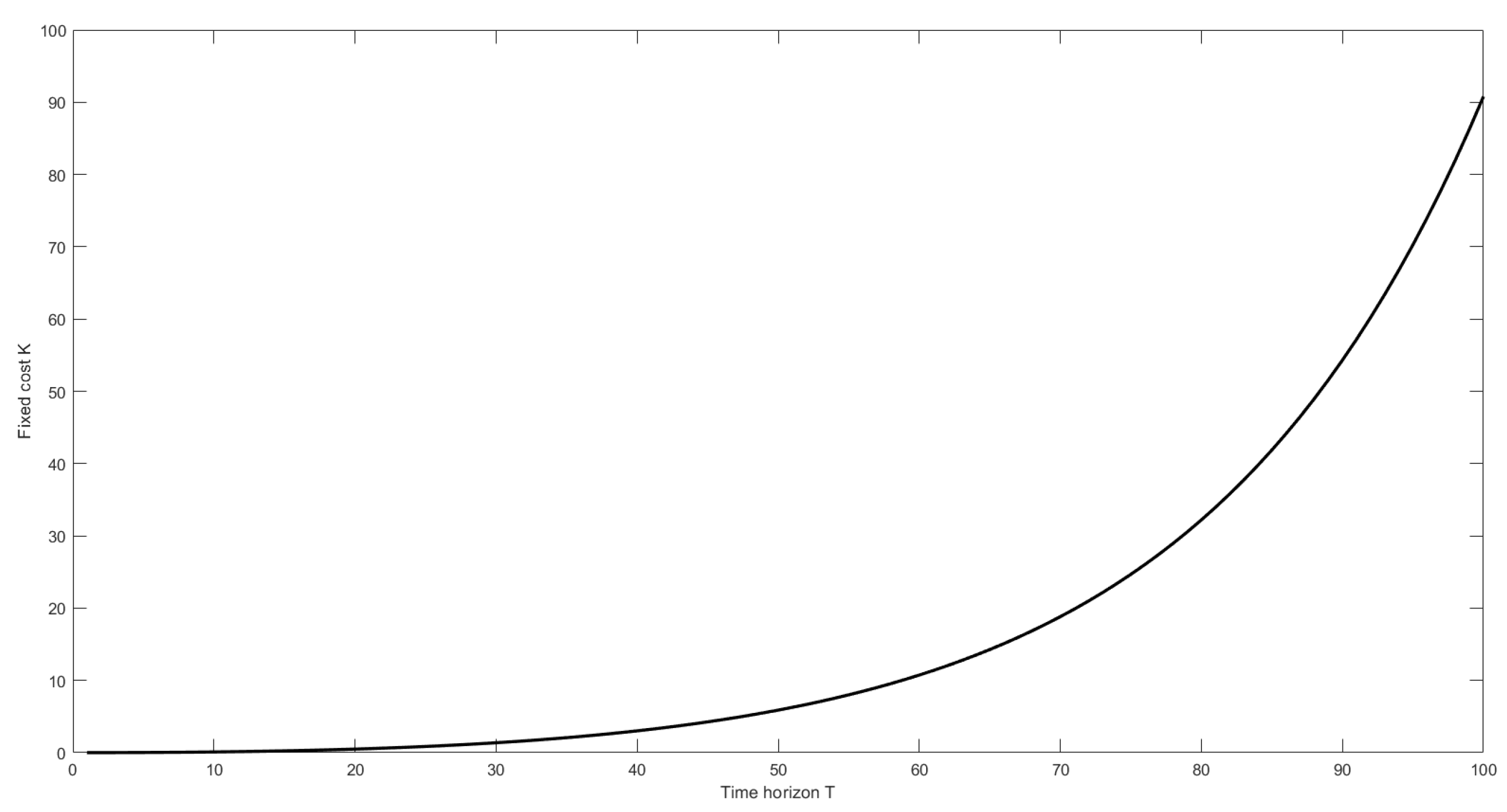

7. Numerical Simulations

8. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- De Finetti, B. Il problema dei “pieni”. G. Ist. Ital. Attuari 1940, 11, 1–88. [Google Scholar]

- Bühlmann, H. Mathematical Methods in Risk Theory; Springer: Berlin/Heidelberg, Germany, 1970. [Google Scholar]

- Gerber, H. Entscheidungskriterien für den zusammengesetzten Poisson-Prozess. Schweiz. Verein. Versicherungsmath. Mitt. 1969, 69, 185–228. [Google Scholar]

- Irgens, C.; Paulsen, J. Optimal control of risk exposure, reinsurance and investments for insurance portfolios. Insur. Math. Econ. 2004, 35, 21–51. [Google Scholar] [CrossRef]

- Brachetta, M.; Ceci, C. Optimal proportional reinsurance and investment for stochastic factor models. Insur. Math. Econ. 2019, 87, 15–33. [Google Scholar] [CrossRef] [Green Version]

- Brachetta, M.; Ceci, C. Optimal Excess-of-Loss Reinsurance for Stochastic Factor Risk Models. Risks 2019, 7, 48. [Google Scholar] [CrossRef] [Green Version]

- Skogh, G. The Transactions Cost Theory of Insurance: Contracting Impediments and Costs. J. Risk Insur. 1989, 56, 726–732. [Google Scholar] [CrossRef]

- Braouezec, Y. Public versus private insurance system with (and without) transaction costs: Optimal segmentation policy of an informed monopolist. Appl. Econ. 2019, 51, 1907–1928. [Google Scholar] [CrossRef]

- Egami, M.; Young, V.R. Optimal reinsurance strategy under fixed cost and delay. Stoch. Process. Their Appl. 2009, 119, 1015–1034. [Google Scholar] [CrossRef] [Green Version]

- Li, P.; Zhou, M.; Yin, C. Optimal reinsurance with both proportional and fixed costs. Stat. Probab. Lett. 2015, 106, 134–141. [Google Scholar] [CrossRef]

- Schmidli, H. Risk Theory; Springer Actuarial, Springer International Publishing: Berlin/Heidelberg, Germany, 2018. [Google Scholar]

- Karatzas, I.; Wang, H. Utility maximization with discretionary stopping. Siam J. Control. Optim. 2000, 39, 306–329. [Google Scholar] [CrossRef] [Green Version]

- Ceci, C.; Bassan, B. Mixed Optimal Stopping and Stochastic Control Problems with Semicontinuous Final Reward for Diffusion Processes. Stochastics Stoch. Rep. 2004, 76, 323–337. [Google Scholar] [CrossRef]

- Bouchard, B.; Touzi, N. Weak Dynamic Programming Principle for Viscosity Solutions. Siam J. Control. Optim. 2011, 49, 948–962. [Google Scholar] [CrossRef] [Green Version]

- Chen, M.; Yuen, K.C.; Wang, W. Optimal reinsurance and dividends with transaction costs and taxes under thinning structure. Scand. Actuar. J. 2020, 1–20. [Google Scholar] [CrossRef]

- Grandell, J. Aspects of Risk Theory; Springer: Berlin/Heidelberg, Germany, 1991. [Google Scholar]

- Eisenberg, J.; Schmidli, H. Optimal control of capital injections by reinsurance in a diffusion approximation. Blätter DGVFM 2009, 30, 1–13. [Google Scholar] [CrossRef]

- ∅ksendal, B. Stochastic Differential Equations; Springer: Berlin/Heidelberg, Germany, 2003. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Value |

|---|---|

| T | 10 |

| q | |

| R |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Brachetta, M.; Ceci, C. Optimal Reinsurance Problem under Fixed Cost and Exponential Preferences. Mathematics 2021, 9, 295. https://doi.org/10.3390/math9040295

Brachetta M, Ceci C. Optimal Reinsurance Problem under Fixed Cost and Exponential Preferences. Mathematics. 2021; 9(4):295. https://doi.org/10.3390/math9040295

Chicago/Turabian StyleBrachetta, Matteo, and Claudia Ceci. 2021. "Optimal Reinsurance Problem under Fixed Cost and Exponential Preferences" Mathematics 9, no. 4: 295. https://doi.org/10.3390/math9040295

APA StyleBrachetta, M., & Ceci, C. (2021). Optimal Reinsurance Problem under Fixed Cost and Exponential Preferences. Mathematics, 9(4), 295. https://doi.org/10.3390/math9040295