Testing the Resilience of CSR Stocks during the COVID-19 Crisis: A Transcontinental Analysis

Abstract

:1. Introduction

2. State of the Art

2.1. Wavelets Literature

2.2. Implementations of Wavelets in the Analysis of the Impact of COVID-19

3. Materials and Methods

3.1. Wavelets Methodology

3.2. Data Description

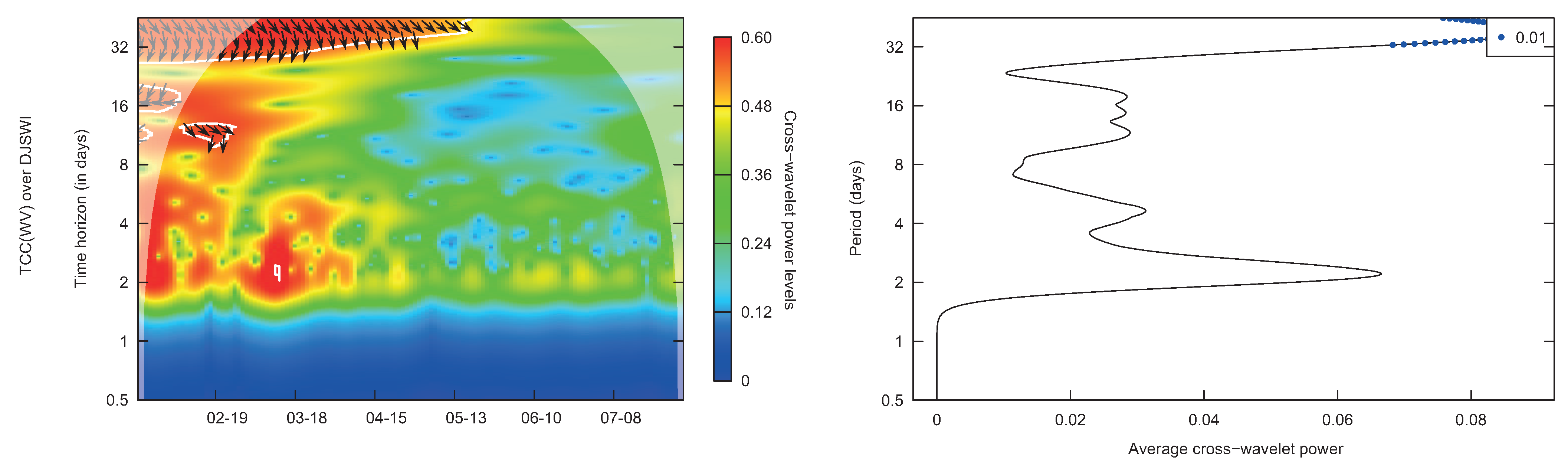

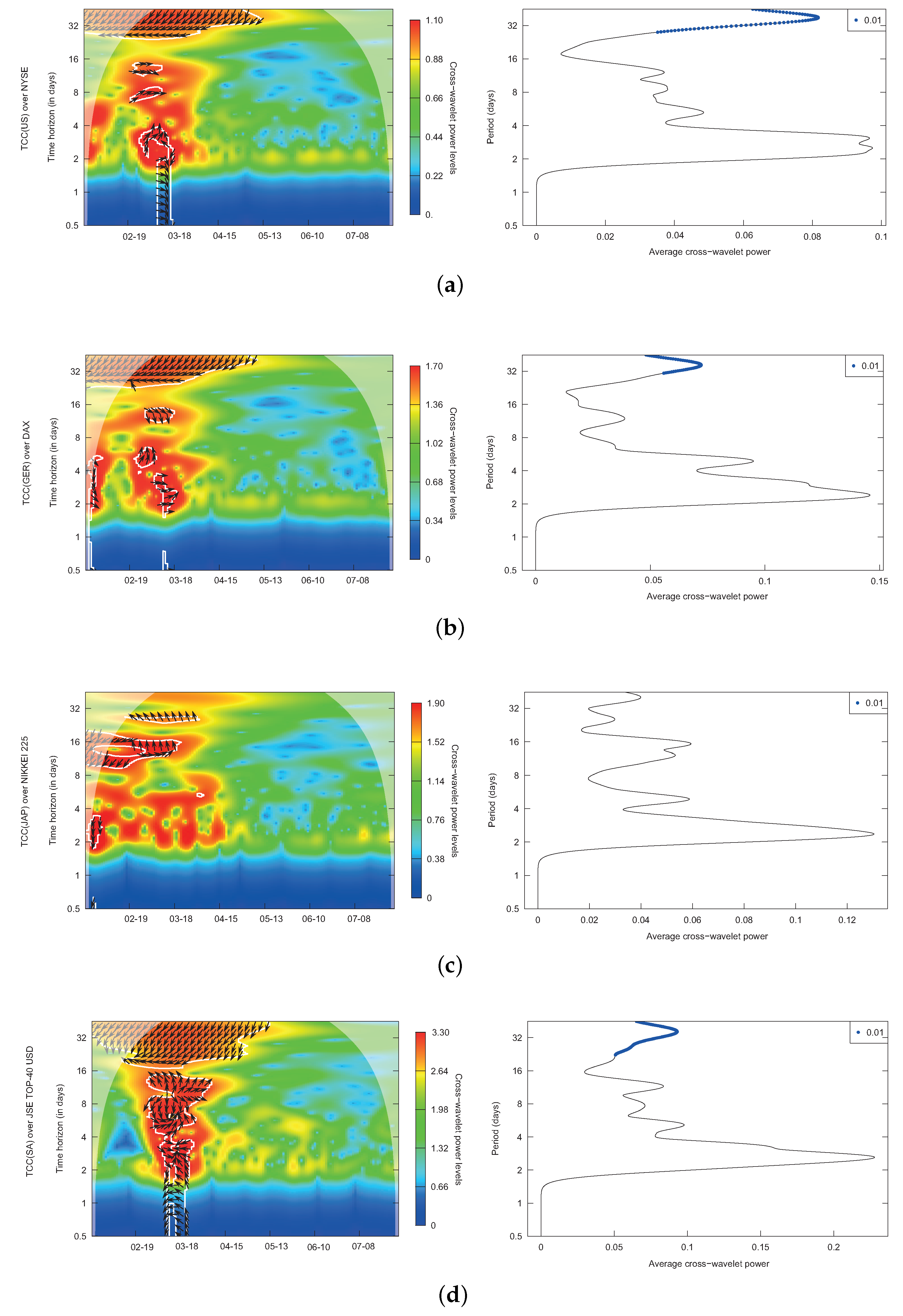

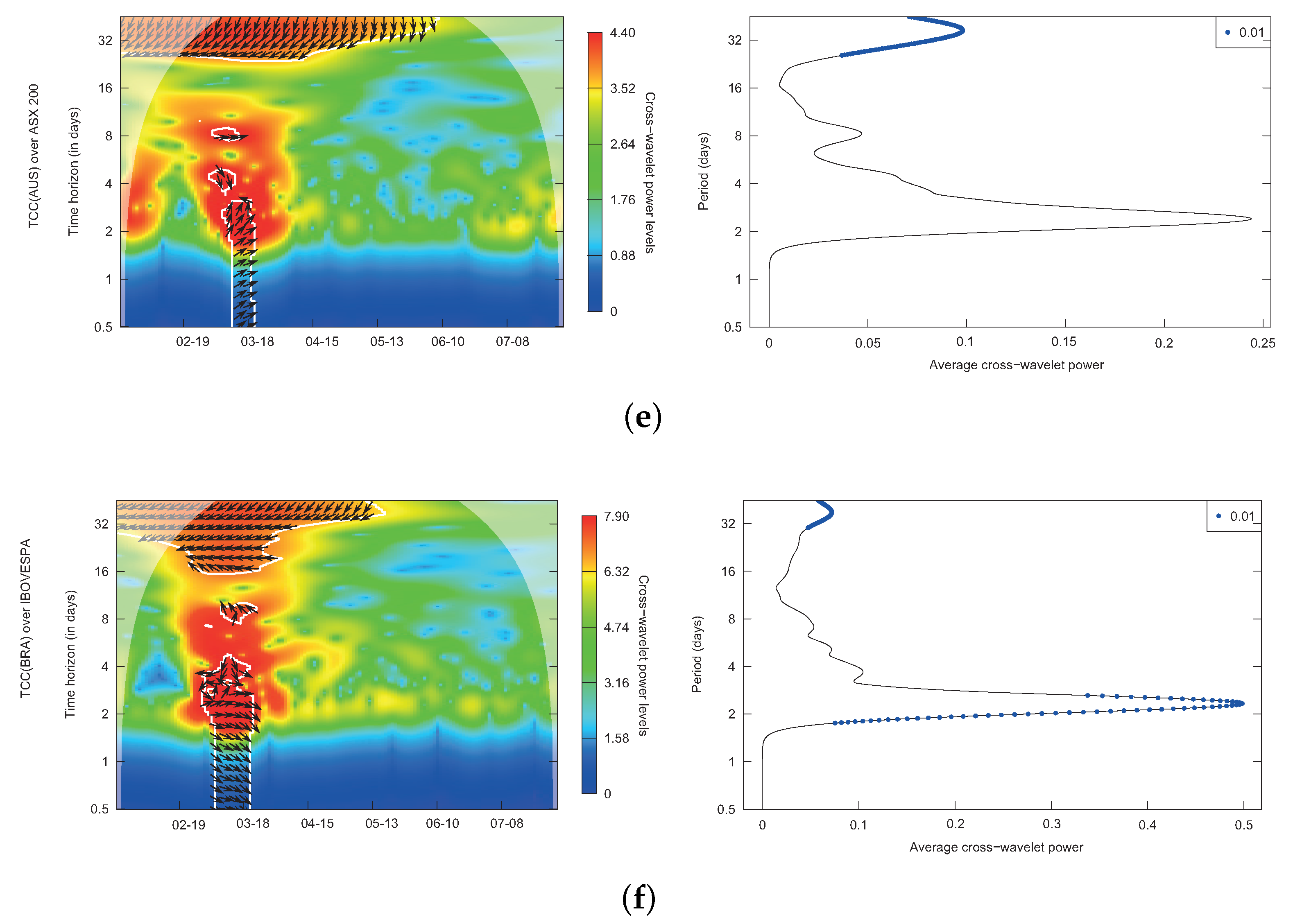

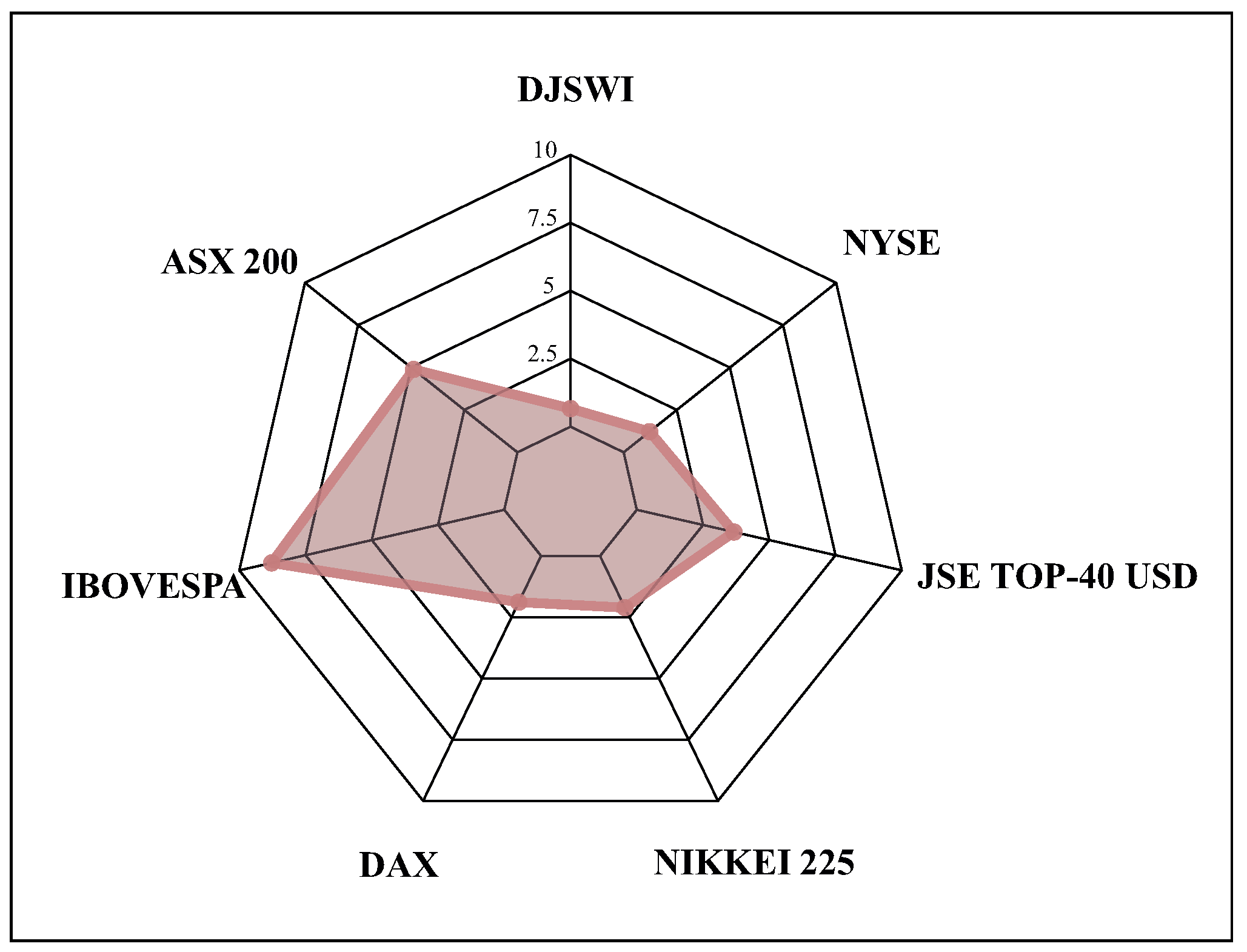

4. Empirical Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| ACPS | Average Cross-Wavelet Spectrum |

| CAPM | Capital Asset Pricing Model |

| COVID-19 | 2019-nCoV acute respiratory disease/Novel coronavirus pneumonia |

| CWT | Continuous Wavelet Transformation |

| DWT | Discrete Wavelet Transformation |

| EMH | Efficient-Markets Hypothesis |

| FMH | Fractal-Markets Hypothesis |

| GMWs | Generalized Morse Wavelets |

| MODWT | Maximum Overlap Discrete Wavelet Transform |

| SMIs | Stock market indices |

| WPS | Wavelets Power Spectrum |

| WC | Wavelet Coherency |

References

- Goodell, J.W. COVID-19 and finance: Agendas for future research. Financ. Res. Lett. 2020, 35, 101512. [Google Scholar] [CrossRef] [PubMed]

- Akhtaruzzaman, M.; Boubaker, S.; Sensoy, A. Financial contagion during COVID-19 crisis. Financ. Res. Lett. 2020, 38, 101604. [Google Scholar] [CrossRef]

- Gharib, C.; Mefteh-Wali, S.; Ben Jabeur, S. The bubble contagion effect of COVID-19 outbreak: Evidence from crude oil and gold markets. Financ. Res. Lett. 2020, 38, 101703. [Google Scholar] [CrossRef]

- Mazur, M.; Dang, M.; Vega, M. COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Financ. Res. Lett. 2020, 38, 101690. [Google Scholar] [PubMed]

- Aguiar-Conraria, L.F.; Magalhães, P.C.; Soares, M.J. Application of wavelets to the study of political history. In Encyclopedia of Complexity and Systems Science; Meyers, R.A., Ed.; Springer: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- Ramsey, J.B. The contribution of wavelets to the analysis of economic and financial data. Philos. Trans. Math. Phys. Eng. Sci. 1999, 357, 2593–2606. [Google Scholar] [CrossRef]

- Ramsey, J.B. Wavelets in Economics and Finance: Past and Future. Stud. Nonlinear Dyn. Econom. 2002, 6, 1. [Google Scholar] [CrossRef] [Green Version]

- Schleicher, C. An Introduction to Wavelets for Economists; Technical Report 2002-32, Working Papers; Monetary and Financial Analysis Department, Bank of Canada: Ottawa, ON, Canada, 2002. [Google Scholar]

- Fernández, V. The international CAPM and a wavelet-based decomposition of value at risk. Stud. Nonlinear Dyn. Econom. 2005, 9, 1328. [Google Scholar]

- Crowley, P.M. A guide to wavelets for economists. J. Econ. Surv. 2008, 21, 207–267. [Google Scholar] [CrossRef]

- Gallegati, M.; Gallegati, M.; Rammsey, J.B.; Semmler, W. Does productivity affect unemployment? A time-frequency analysis for the US. In Wavelet Applications in Economics and Finance; Dynamic Modeling and Econometrics in Economics and Finance; Gallegati, M., Semmler, W., Eds.; Springer International Publishing: Cham, Switzerland, 2014; Volume 20, pp. 23–46. [Google Scholar]

- Kumar, A.S.; Jayakumar, C.; Kamaiah, B. Fractal market hypothesis: Evidence for nine Asian forex markets. Indian Econ. Rev. 2017, 52, 181–192. [Google Scholar] [CrossRef]

- Tiwari, A.; Cunado, J.; Gupta, R.; Wohar, M. Are stock returns an inflation hedge for the UK? Evidence from a wavelet analysis using over three centuries of data. Stud. Nonlinear Dyn. Econom. 2018, 23, 20170049. [Google Scholar] [CrossRef] [Green Version]

- Owusu Junior, P.; Kwaku Boafo, B.; Awuye, B.K.; Bonsu, K.; Obeng-Tawiah, H. Co-movement of stock exchange indices and exchange rates in Ghana: A wavelet coherence analysis. Cogent Bus. Manag. 2018, 5, 1481559. [Google Scholar] [CrossRef]

- Tenreiro Machado, J.A.; Costa, A.C.; Quelhas, M.D. Wavelet analysis of human DNA. Genomics 2011, 98, 155–163. [Google Scholar] [CrossRef] [Green Version]

- Daubechies, I. The wavelet transform, time-frequency localization and signal analysis. IEEE Trans. Inf. Theory 1990, 36, 961–1005. [Google Scholar] [CrossRef] [Green Version]

- Ferrer, R.; Jammazi, R.; Bolós, V.J.; Benítez, R. Interactions between financial stress and economic activity for the U.S.: A time- and frequency-varying analysis using wavelets. Phys. A Stat. Mech. Appl. 2018, 492, 446–462. [Google Scholar] [CrossRef]

- Schmidbauer, H.; Röosch, A.; Uluceviz, E.; Erkol, N. Are American and European equity markets in phase?—Frequency aspects of return and volatility spillovers. In Proceedings of the Conference EcoMod 2016, Lisbon, Portugal, 6–8 July 2016. [Google Scholar]

- Crowley, P.M. Long cycles in growth: Explorations using new frequency domain techniques with US data. In Bank of Finland Research Discussion Papers; Bank of Finland: Helsinki, Finland, 2010. [Google Scholar]

- Aguiar-Conraria, L.F.; Soares, M.J. The Continuous Wavelet Transform: A Primer; NIPE Working Papers; Universidade de Minho, Núcleo de Investigação em Políticas Económica: Braga, Portugal, 2011. [Google Scholar]

- Addo, P.M.; Billio, M.; Guégan, D. Nonlinear dynamics and wavelets for business cycle analysis. In Wavelet Applications in Economics and Finance; Dynamic Modeling and Econometrics in Economics and Finance; Gallegati, M., Semmler, W., Eds.; Springer International Publishing: Cham, Switzerland, 2014; Volume 20, pp. 73–100. [Google Scholar]

- Priestley, M. Spectral Analysis and Time Series, 7th ed.; Academic Press: San Diego, CA, USA, 1992. [Google Scholar]

- Ramsey, J.B.; Lampart, C. The Decomposition of Economic Relationships by Time Scale Using Wavelets: Expenditure and Income. Stud. Nonlinear Dyn. Econom. 1998, 3, 23–42. [Google Scholar] [CrossRef]

- Ramsey, J.B.; Lampart, C. Decomposition of economic relationships by time scale using wavelets: Money and income. Macroecon. Dyn. 1998, 2, 49–71. [Google Scholar] [CrossRef]

- Baruník, J.; Vácha, L. Contagion among Central and Eastern European Stock Markets during the Financial Crisis. Czech J. Econ. Financ. Aúvěr 2013, 63, 443–453. [Google Scholar]

- Reboredo, J.C.; Rivera-Castro, M.A. Wavelet-based evidence of the impact of oil prices on stock returns. Int. Rev. Econ. Financ. 2014, 29, 145–176. [Google Scholar] [CrossRef]

- Ivanov, I.; Kabaivanov, S.; Bogdanova, B. Stock market recovery from the 2008 financial crisis: The differences across Europe. Res. Int. Bus. Financ. 2016, 37, 360–374. [Google Scholar] [CrossRef]

- Poměnková, J.; Klejmová, E.; Kučerová, Z. Cyclicality in lending activity of Euro area in pre- and post- 2008 crisis: A local-adaptive-based testing of wavelets. Balt. J. Econ. 2019, 19, 155–175. [Google Scholar] [CrossRef]

- Polanco-Martínez, J.; Fernández-Macho, J.; Neumann, M.; Faria, S. A pre-crisis vs. crisis analysis of peripheral EU stock markets by means of wavelet transform and a nonlinear causality test. Phys. A Stat. Mech. Appl. 2018, 490, 1211–1227. [Google Scholar] [CrossRef]

- Samadi, A.; Owjimehr, S.; Nezhad Halafi, Z. The cross-impact between financial markets, Covid-19 pandemic, and economic sanctions: The case of Iran. J. Policy Model. 2020. [Google Scholar] [CrossRef]

- Sadefo Kamdem, J.; Bandolo Essomba, R.; Njong Berinyuy, J. Deep learning models for forecasting and analyzing the implications of COVID-19 spread on some commodities markets volatilities. Chaos Solitons Fractals 2020, 140, 110215. [Google Scholar] [CrossRef] [PubMed]

- Iqbal, N.; Fareed, Z.; Shahzad, F.; He, X.; Shahzad, U.; Lina, M. The nexus between COVID-19, temperature and exchange rate in Wuhan city: New findings from partial and multiple wavelet coherence. Sci. Total Environ. 2020, 729, 138916. [Google Scholar] [CrossRef] [PubMed]

- Mustafa, S.; Ayaz Ahmad, M.; Baranova, V.; Deineko, Z.; Lyashenko, V.; Oyouni, A. Using wavelet analysis to assess the impact of COVID-19 on changes in the price of basic energy resources. Int. J. Emerg. Trends Eng. Res. 2020, 8, 2907–2912. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Štifanić, D.; Musulin, J.; Miočević, A.; Baressi Šegota, S.; Šubić, R.; Car, Z. Impact of COVID-19 on Forecasting Stock Prices: An Integration of Stationary Wavelet Transform and Bidirectional Long Short-Term Memory. Complexity 2020, 2020, 1–12. [Google Scholar] [CrossRef]

- Habib, Y.; Xia, E.; Fareed, Z.; Hashmi, S. Time-frequency co-movement between COVID-19, crude oil prices, and atmospheric CO2 emissions: Fresh global insights from partial and multiple coherence approach. Environ. Dev. Sustain. 2020. [Google Scholar] [CrossRef]

- Demir, E.; Bilgin, M.; Karabulut, G.; Doker, A. The relationship between cryptocurrencies and COVID-19 pandemic. Eurasian Econ. Rev. 2020, 10, 349–360. [Google Scholar] [CrossRef]

- Dynkin, A.; Telegina, E. Pandemic shock and the world after crisis. World Econ. Int. Relat. 2020, 64, 5–16. [Google Scholar] [CrossRef]

- Kuzemko, C.; Bradshaw, M.; Bridge, G.; Goldthau, A.; Jewell, J.; Overland, I.; Scholten, D.; Van de Graaf, T.; Westphal, K. Covid-19 and the politics of sustainable energy transitions. Energy Res. Soc. Sci. 2020, 68, 101685. [Google Scholar] [CrossRef]

- Albuquerque, R.A.; Koskinen, Y.J.; Yang, S.; Zhang, C. Resiliency of Environmental and Social Stocks: An Analysis of the Exogenous COVID-19 Market Crash, 2020; Finance Working Paper No. 676/2020; European Corporate Governance Institute: mboxBrussels, Belgium, 2020; Available online: https://ssrn.com/abstract=3583611 (accessed on 29 September 2020).

- Haar, A. Zur Theorie der orthogonalen Funktionensysteme. Math. Ann. 1910, 69, 331–371. [Google Scholar] [CrossRef]

- Meyer, Y. Principe d’incertitude, bases hilbertiennes et algèbres d’opérateurs. In Séminaire Bourbaki; Astérisque; Société Mathématique de France: Paris, France, 1987; Volume 1985–1986, pp. 651–668. [Google Scholar]

- Ricker, N.H. Wavelet Contraction, Wavelet Expansion, and the Control of Seismic Resolution. Geophysics 1953, 18, 769–792. [Google Scholar] [CrossRef]

- Gasquet, C.; Witomski, P. Fourier analysis and applications: Filtering, numerical computation, wavelets. In Texts in Applied Mathematics; Springer Science & Business Media: New York, NY, USA, 1998; Volume 30. [Google Scholar]

- Grossmann, A.; Morlet, J. Decomposition of Hardy functions into square integrable wavelets of constant shape. SIAM J. Math. Anal. 1984, 15, 723–736. [Google Scholar] [CrossRef]

- Morlet, J.; Arens, G.; Fourgeau, E.; Giard, D. Wave Propagation and Sampling Theory (Parts I and II). Geophysics 1982, 47, 203–236. [Google Scholar] [CrossRef] [Green Version]

- Morlet, J. Sampling theory and wave propagation. In Issues in Acoustic Signal—Image Processing and Recognition. NATO ASI Series; Chen, C., Ed.; Series F: Computer and System Sciences; Springer: Berlin/Heidelberg, Germany, 1983; Volume 1, pp. 233–261. [Google Scholar]

- Dong, X.; Nyren, P.; Patton, B.; Nyren, A.; Richardson, J.; Maresca, T. Wavelets for Agriculture and Biology: A Tutorial with Applications and Outlook. BioScience 2008, 58, 445–453. [Google Scholar] [CrossRef] [Green Version]

- Singh, C.B.; Choudhary, R.; Jayas, D.S.; Paliwal, J. Wavelet Analysis of Signals in Agriculture and Food Quality Inspection. Food Bioprocess Technol. 2010, 3, 2–12. [Google Scholar] [CrossRef]

- Scargle, J.D. Astronomical time series analysis. In Astronomical Time Series; Astrophysics and Space Science Library; Maoz, D., Sternberg, A., Leibowitz, E.M., Eds.; Springer: Dordrecht, The Netherlands, 1997; Volume 28. [Google Scholar]

- Unser, M.; Aldroubi, A. A review of wavelets in biomedical applications. Proc. IEEE 1996, 84, 626–638. [Google Scholar] [CrossRef]

- Aldroubi, A.; Unser, M. Wavelets in Medicine and Biology; CRC Press: Boca Ratón, FL, USA, 1996. [Google Scholar]

- Liò, P. Wavelets in bioinformatics and computational biology: State of art and perspectives. Bioinformatics 2003, 19, 2–9. [Google Scholar] [CrossRef] [PubMed]

- Rickard, Y. An efficient wavelet-based solution of electromagnetic field problems. Appl. Numer. Math. 1996, 58, 472–485. [Google Scholar] [CrossRef]

- Pan, G.W. Wavelets in electromagnetics and device modeling. In Wiley Series in Microwave and Optical Engineering; John Wiley & Sons: Hoboken, NJ, USA, 2003; Volume 159. [Google Scholar]

- Yuanhu, D. Wavelet analysis and its application in forestry. J. Northeast For. Univ. 1996, 7, 81–84. [Google Scholar]

- James, P.M.A.; Sturtevant, B.R.; Townsend, P.; Wolter, P.; Fortin, M.J. Two-dimensional wavelet analysis of spruce budworm host basal area in the Border Lakes landscape. Ecol. Appl. 2011, 21, 2197–2209. [Google Scholar] [CrossRef]

- Foufoula-Georgiou, E.; Kumar, P. Wavelet analysis in geophysics: An introduction. In Wavelet Analysis and Its Applications; Foufoula-Georgiou, E., Kumar, P., Eds.; Academic Press: London, UK, 1994; Volume 4, pp. 1–43. [Google Scholar]

- Grinsted, A.; Moore, J.C.; Jevrejeva, S. Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Process. Geophys. 2004, 11, 561–566. [Google Scholar] [CrossRef]

- Brillinger, D.R. Some uses if cumulants in wavelet analysis. J. Nonparametr. Stat. 1996, 6, 93–114. [Google Scholar] [CrossRef]

- Brillinger, D.R. A note on river wavelets. Environmetrics 1994, 5, 211–220. [Google Scholar] [CrossRef]

- Hudgins, L.; Friehe, C.A.; Mayer, M.E. Wavelet transforms and atmopsheric turbulence. Phys. Rev. Lett. 1993, 71, 3279–3282. [Google Scholar] [CrossRef] [PubMed]

- Meyers, S.D.; Kelly, B.G.; O’Brien, J.J. An Introduction to Wavelet Analysis in Oceanography and Meteorology: With Application to the Dispersion of Yanai Waves. Mon. Weather Rev. 1993, 121, 2858–2866. [Google Scholar] [CrossRef] [Green Version]

- Torrence, C.; Compo, G.P. A Practical Guide to Wavelet Analysis. Bull. Am. Meteorol. Soc. 1998, 79, 61–78. [Google Scholar] [CrossRef] [Green Version]

- Torrence, C.; Webster, P.J. Interdecadal Changes in the ENSO-Monsoon System. J. Clim. 1999, 12, 2679–2690. [Google Scholar] [CrossRef] [Green Version]

- Nazari-Sharabian, M.; Karakouzian, M. Relationship between Sunspot Numbers and Mean Annual Precipitation: Application of Cross-Wavelet Transform—A Case Study. J. Multidiscip. Sci. J. 2020, 3, 67–78. [Google Scholar] [CrossRef] [Green Version]

- Whitney, R. Quantifying near fault pulses using generalized Morse wavelets. J. Seismol. 2019, 23, 1115–1140. [Google Scholar] [CrossRef]

- Daubechies, I. Orthonormal bases of compactly supported wavelets. Commun. Pure Appl. Math. 1988, 41, 909–996. [Google Scholar] [CrossRef] [Green Version]

- Mallat, S.G. A theory for multiresolution signal decomposition: The wavelet representation. IEEE Trans. Pattern Anal. Mach. Intell. 1989, 7, 674–693. [Google Scholar] [CrossRef] [Green Version]

- Daubechies, I. Ten Lectures on Wavelets; SIAM Press: Philadelphia, PA, USA, 1992. [Google Scholar]

- Farge, M. Wavelet transforms and their applications to turbulence. Annu. Rev. Fluid Mech. 1992, 24, 395–457. [Google Scholar] [CrossRef]

- Jagrič, T.; Ovin, R. Method of analyzing business cycles in a transition economy: The case of Slovenia. Dev. Econ. 2004, 42, 42–62. [Google Scholar] [CrossRef]

- Crowley, P.M.; Mayes, D.G. How fused is the Euro area core?: An evaluation of growth cycle co-movement and synchronization using wavelet analysis. J. Bus. Cycle Meas. Anal. 2008, 4, 63–95. [Google Scholar] [CrossRef]

- Aguiar-Conraria, L.F.; Azevedo, N.; Soares, M.J. Using wavelets to decompose the time-frequency effects of monetary policy. Phys. A Stat. Mech. Appl. 2008, 387, 2863–2878. [Google Scholar] [CrossRef] [Green Version]

- Baubeau, P.; Cazelles, B. French Economic Cycles: A Wavelet Analysis of French Retrospective GNP Series. Cliometrica 2009, 3, 275–300. [Google Scholar] [CrossRef]

- Aguiar-Conraria, L.F.; Soares, M.J. Oil and the macroeconomy: Using wavelets to analyze old issues. Empir. Econ. 2011, 40, 645–655. [Google Scholar] [CrossRef]

- Aguiar-Conraria, L.F.; Soares, M.J. Business cycle synchronization and the Euro: A wavelet analysis. J. Macroecon. 2011, 33, 477–489. [Google Scholar] [CrossRef]

- Gençay, R.; Selçuk, F.; Whitcher, B. An Introduction to Wavelets and Other Filtering Methods in Finance and Economics; Academic Press: San Diego, CA, USA, 2002. [Google Scholar]

- Tenreiro Machado, J.A.; Duarte, F.B.; Monteiro Duarte, G. Analysis of Stock Market Indices with Multidimensional Scaling and Wavelets. Math. Probl. Eng. 2012, 2012, 1–14. [Google Scholar] [CrossRef]

- Goupillaud, P.; Grossmann, A.; Morlet, J. Cycle-octave and related transforms in seismic signal analysis. Geoexploration 1984, 23, 85–102. [Google Scholar] [CrossRef]

- Lilly, J.M.; Olhede, S.C. Generalized Morse Wavelets as a Superfamily of Analytic Wavelets. IEEE Trans. Signal Process. 2012, 60, 6036–6041. [Google Scholar] [CrossRef] [Green Version]

- Martín Cervantes, P.A.; Cruz Rambaud, S. An empirical approach to the “Trump Effect” on US financial markets with causal-impact Bayesian analysis. Heliyon 2020, 6, e04760. [Google Scholar] [CrossRef] [PubMed]

- Moller, N.; Zilca, S. The evolution of the January effect. J. Bank. Financ. 2008, 32, 447–457. [Google Scholar] [CrossRef]

- Jacobsen, B.; Nuttawat, V. The Halloween Effect in U.S. Sectors. Financ. Rev. 2009, 44, 437–459. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient Capital Markets: A Review of Theory and Empirical Work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Peters, E.E. Fractal Market Analysis: Applying Chaos Theory to Investment and Economics; Wiley Finance; John Wiley & Sons: New York, NY, USA, 1994; Volume 24. [Google Scholar]

- Kristoufek, L. Fractal Markets Hypothesis and the Global Financial Crisis: Wavelet Power Evidence. Sci. Rep. 2013, 3, 2857. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Forbes, K.J.; Rigobon, R. No contagion, only interdependence: Measuring stock market co-movements. J. Financ. 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Baruník, J.; Vácha, L.; Krištoufek, L. Comovement of Central European Stock Markets Using Wavelet Coherence: Evidence from High-Frequency Data; IES Working Papers; Charles University, Institute of Economic Studies (IES): Prague, Czech Republic, 2011. [Google Scholar]

- Sharpe, W.F. Capital asset prices: A theory of market equilibrium under conditions of risk. J. Financ. 1964, 19, 425–442. [Google Scholar]

- Stubbs, T.; Kring, W.; Laskaridis, C.; Kentikelenis, A.; Gallagher, K. Whatever it takes? The global financial safety net, Covid-19, and developing countries. World Dev. 2021, 137, 105171. [Google Scholar] [CrossRef] [PubMed]

- Merkl, C.; Weber, E. End the Recruitment Crisis! [Raus aus der Neueinstellungskrise!]. Wirtschaftsdienst 2020, 100, 507–509. [Google Scholar] [CrossRef] [PubMed]

- Pak, A.; Adegboye, O.; Adekunle, A.; Rahman, K.; McBryde, E.; Eisen, D. Economic Consequences of the COVID-19 Outbreak: The Need for Epidemic Preparedness. Front. Public Health 2020, 8, 241. [Google Scholar] [CrossRef]

- Richter, A.; Wilson, T. Covid-19: Implications for insurer risk management and the insurability of pandemic risk. Geneva Risk Insur. Rev. 2020, 45, 171–199. [Google Scholar] [CrossRef]

- Esin, P. World market development scenario in the context of the coronavirus crisis. Izv. Vyss. Uchebnykh Zavedeniy. Prikl. Nelineynaya Din. 2020, 28, 158–167. [Google Scholar]

- Kermack, W.O.; McKendrick, A.G. Contributions to the mathematical theory of epidemics I. Bull. Math. Biol. 1991, 53, 33–55. [Google Scholar] [PubMed]

- Kermack, W.O.; McKendrick, A.G. Contributions to the mathematical theory of epidemics II–The problem of endemicity. Bull. Math. Biol. 1991, 53, 57–87. [Google Scholar] [PubMed]

- Kermack, W.O.; McKendrick, A.G. Contributions to the mathematical theory of epidemics III–Further studies of the problem of endemicity. Bull. Math. Biol. 1991, 53, 89–118. [Google Scholar]

- Burri, M.; Kaufmann, D. A daily fever curve for the Swiss economy. Swiss J. Econ. Stat. 2020, 156, 6. [Google Scholar] [CrossRef]

- Grigoryev, L.; Pavlyushina, V.; Muzychenko, E. The fall into 2020 recession. Vopr. Ekon. 2020, 2020, 5–24. [Google Scholar] [CrossRef]

- Joshi, A.; Bhaskar, P.; Gupta, P. Indian economy amid COVID-19 lockdown: A prespective. J. Pure Appl. Microbiol. 2020, 14, 957–961. [Google Scholar] [CrossRef]

- Salamzadeh, A.; Dana, L. The coronavirus (COVID-19) pandemic: Challenges among Iranian startups. J. Small Bus. Entrep. 2020. [Google Scholar] [CrossRef]

- Connolly, R.; Hanson, P.; Bradshaw, M. It’s déjà vu all over again: COVID-19, the global energy market, and the Russian economy. Eurasian Geogr. Econ. 2020, 61, 511–531. [Google Scholar] [CrossRef]

- Gherghina, S.C.; Armeanu, D.S.; Joldeş, C.C. Stock market reactions to COVID-19 pandemic outbreak: Quantitative evidence from ARDL bounds tests and granger causality analysis. Int. J. Environ. Res. Public Health 2020, 17, 6729. [Google Scholar] [CrossRef] [PubMed]

- Chakraborty, T.; Ghosh, I. Real-time forecasts and risk assessment of novel coronavirus (COVID-19) cases: A data-driven analysis. Chaos Solitons Fractals 2020, 135, 109850. [Google Scholar] [CrossRef] [PubMed]

- Hazarika, B.; Gupta, D. Modelling and forecasting of COVID-19 spread using wavelet-coupled random vector functional link networks. Appl. Soft Comput. J. 2020, 96, 106626. [Google Scholar] [CrossRef] [PubMed]

- Singh, S.; Parmar, K.; Kumar, J.; Makkhan, S. Development of new hybrid model of discrete wavelet decomposition and autoregressive integrated moving average (ARIMA) models in application to one month forecast the casualties cases of COVID-19. Chaos Solitons Fractals 2020, 135, 109866. [Google Scholar] [CrossRef] [PubMed]

- Shah, K.; Khan, Z.; Ali, A.; Amin, R.; Khan, H.; Khan, A. Haar wavelet collocation approach for the solution of fractional order COVID-19 model using Caputo derivative. Alex. Eng. J. 2020, 59, 3221–3231. [Google Scholar] [CrossRef]

- Fareed, Z.; Iqbal, N.; Shahzad, F.; Shah, S.; Zulfiqar, B.; Shahzad, K.; Hashmi, S.; Shahzad, U. Co-variance nexus between COVID-19 mortality, humidity, and air quality index in Wuhan, China: New insights from partial and multiple wavelet coherence. Air Qual. Atmos. Health 2020, 13, 673–682. [Google Scholar] [CrossRef]

- Bilal; Bashir, M.F.; Benghoul, M.; Numan, U.; Shakoor, A.; Komal, B.; Bashir, M.A.; Bashir, M.; Tan, D. Environmental pollution and COVID-19 outbreak: Insights from Germany. Air Qual. Atmos. Health 2020, 13, 1385–1394. [Google Scholar] [CrossRef]

- Dong, E.; Du, H.; Gardner, L. An interactive web-based dashboard to track COVID-19 in real time. Lancet Infect. Dis. 2020, 5, 533–534. [Google Scholar] [CrossRef]

- Bloomberg. Bloomberg Professional Services. 2020. Available online: https://www.bloomberg.com/professional/solution/financial-data-management/ (accessed on 29 September 2020).

- S&P Global. Dow Jones Sustainability World Enlarged Index ex Alcohol, Tobacco, Gambling, Armaments & Firearms and Adult Entertainment. 2020. Available online: https://www.spglobal.com/spdji/en/indices/esg/dow-jones-sustainability-world-enlarged-index-ex-alcohol-tobacco-gambling-armaments-firearms-and-adult-entertainment/#overview (accessed on 29 September 2020).

- Tyszkiewicz, J. The Power of Spreadsheet Computations. In Fields of Logic and Computation III Essays: Dedicated to Yuri Gurevich on the Occasion of His 80th Birthday; Blass, A., Cégielski, P., Dershowitz, N., Droste, M., Finkbeiner, B., Eds.; Lecture Notes in Computer Science; Springer Nature: Cham, Switzerland, 2020; Volume 12180, pp. 305–323. [Google Scholar]

- Makhortykh, M.; Urman, A.; Ulloa, R. How search engines disseminate information about COVID19 and why they should do better. Special Issue on COVID-19 and Misinformation. Harv. Kennedy Sch. Misinf. Rev. 2020, 1. [Google Scholar] [CrossRef]

- Hintze, J.L.; Nelson, R.D. Violin Plots: A Box Plot-Density Trace Synergism. Am. Stat. 1998, 52, 181–184. [Google Scholar]

- WHO. Novel Coronavirus (2019-nCoV) Situation Report—1. 21 January 2020. World Health Organization. Available online: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200121-sitrep-1-2019-ncov.pdf?sfvrsn=20a99c10_4 (accessed on 29 September 2020).

- Imbert, F. Dow Falls More Than 100 Points after Suffering a Sudden Midday Sell-Off That Confused Traders. 2020. CNBC. Available online: https://www.cnbc.com/2020/02/20/us-futures-point-to-slightly-lower-open-after-new-highs-on-wall-street.html (accessed on 29 September 2020).

- von Mayr, G. Die gesetzmäßigkeit im gesellschaftsleben. In Die Naturkräfte. Eine Naturwissenschaftliche Volksbibliothek; Walter de Gruyter GmbH: Berlin, Germany, 1877; Volume 23. [Google Scholar]

- WHO. WHO Director-General’s Opening Remarks at the Media Briefing on COVID-19. 11 March 2020. World Health Organization. Available online: https://www.who.int/director-general/speeches/detail/who-director-general-s-opening-remarks-at-the-media-briefing-on-covid-19---11-march-2020 (accessed on 29 September 2020).

- Ceylan, R.F.; Ozkan, B.; Mulazimogullari, E. Historical evidence for economic effects of COVID-19. Eur. J. Health Econ. 2020, 21, 817–823. [Google Scholar] [CrossRef] [PubMed]

- Martín Cervantes, P.A.; Cruz Rambaud, S. Date-stamping the Tadawul bubble through the SADF and GSADF econometric approaches. Econ. Bull. 2020, 40, 1475–1485. [Google Scholar]

- Thai, M.; Wu, W.; Xiong, H. Big Data in Complex and Social Networks; Chapman & Hall/CRC Big Data Series; CRC Press: Boca Raton, FL, USA, 2016. [Google Scholar]

- Stone, P.J.; Dunphy, D.C.S.; Smith, M. The General Inquirer: A Computer Approach to Content Analysis; MIT Press: Cambridge, MA, USA, 1966. [Google Scholar]

- Vázquez Lázara, A. Homogenisation of COVID-19-Related Data, 2020. Parliamentary Questions: Question for Written Answer E-002553/2020 to the Commission, Rule 138. European Parliament Publising Services, Brussels. Available online: https://www.europarl.europa.eu/doceo/document/E-9-2020-002553_EN.html (accessed on 29 September 2020).

- Roberts, A. The Third and Fatal Shock: How Pandemic Killed the Millennial Paradigm. Public Adm. Rev. 2020, 80, 603–609. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Continent | Country | Variable I: Financial Markets | Variable II: COVID-19 Cases | |

|---|---|---|---|---|

| Stock Market Index | Abbreviation | Abbreviation | ||

| Americas | Brazil | Bovespa Index | IBOVESPA | TCC (BRA) |

| United States | NYSE Composite Index | NYSE | TCC (US) | |

| Africa | South Africa | JSE Top 40 Companies Index | JSE TOP-40 USD | TCC (SA) |

| Asia | Japan | Nikkei 225 Index | NIKKEI 225 | TCC (JAP) |

| Europe | Germany | DAX Xetra Index | DAX | TCC (GER) |

| Oceania | Australia | S&P/ASX 200 Index | ASX 200 | TCC (AUS) |

| Worldwide | Dow Jones Sustainability World Index | DJSWI | TCC (WV) | |

| Panel I: Descriptive Statistics. COVID-19 Cases *. | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Variable | N | Mean | SD | Variance | Min. | Q1 | Median | Q3 | Max. | Range |

| Total worldwide | 137 | 0.05327 | 0.07940 | 0.00630 | 0.00663 | 0.01759 | 0.02144 | 0.05605 | 0.64485 | 0.63822 |

| Australia | 137 | 0.04085 | 0.07867 | 0.00619 | 0 | 0.00105 | 0.00386 | 0.03548 | 0.44629 | 0.44629 |

| Brazil | 137 | 0.08220 | 0.15970 | 0.02550 | 0 | 0.01460 | 0.03860 | 0.07980 | 1.17870 | 1.17870 |

| Germany | 137 | 0.06520 | 0.16080 | 0.02590 | 0 | 0.00180 | 0.00380 | 0.04680 | 1.38630 | 1.38630 |

| Japan | 137 | 0.04891 | 0.07603 | 0.00578 | 0 | 0.00400 | 0.02495 | 0.07101 | 0.55962 | 0.55962 |

| South Africa | 137 | 0.06640 | 0.11890 | 0.01410 | 0 | 0.00790 | 0.04350 | 0.05550 | 0.84730 | 0.84730 |

| U.S. | 137 | 0.07960 | 0.13300 | 0.01770 | 0 | 0.01220 | 0.01920 | 0.07720 | 0.69310 | 0.69310 |

| Panel II: Descriptive Statistics. World Stock Indices *. | ||||||||||

| Variable | N | Mean | St. dev. | Variance | Min | Q1 | Median | Q3 | Max | Range |

| DJSWI | 137 | −0.00004 | 0.02176 | 0.00047 | −0.10602 | −0.00690 | 0.00159 | 0.00976 | 0.07695 | 0.18297 |

| ASX 200 | 137 | −0.00135 | 0.02400 | 0.00058 | −0.00958 | 0.00032 | 0.01034 | 0.06766 | 0.16970 | |

| IBOVESPA | 137 | −0.00102 | 0.03681 | 0.00136 | −0.15993 | −0.01253 | 0 | 0.01662 | 0.13022 | 0.29015 |

| DAX | 137 | −0.00068 | 0.02582 | 0.00067 | −0.13055 | −0.00933 | 0 | 0.01252 | 0.10414 | 0.23469 |

| NIKKEI 225 | 137 | −0.00074 | 0.01991 | 0.00040 | −0.06274 | −0.00935 | −0.00039 | 0.00845 | 0.07731 | 0.14005 |

| JSE TOP-40 USD | 137 | −0.00131 | 0.03106 | 0.00097 | −0.12801 | −0.01313 | 0.00059 | 0.01608 | 0.08502 | 0.21303 |

| NYSE | 137 | −0.00090 | 0.02864 | 0.00082 | −0.12595 | −0.01324 | 0 | 0.01223 | 0.09564 | 0.22159 |

| 02-19 | 03-18 | 04-15 | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | |||

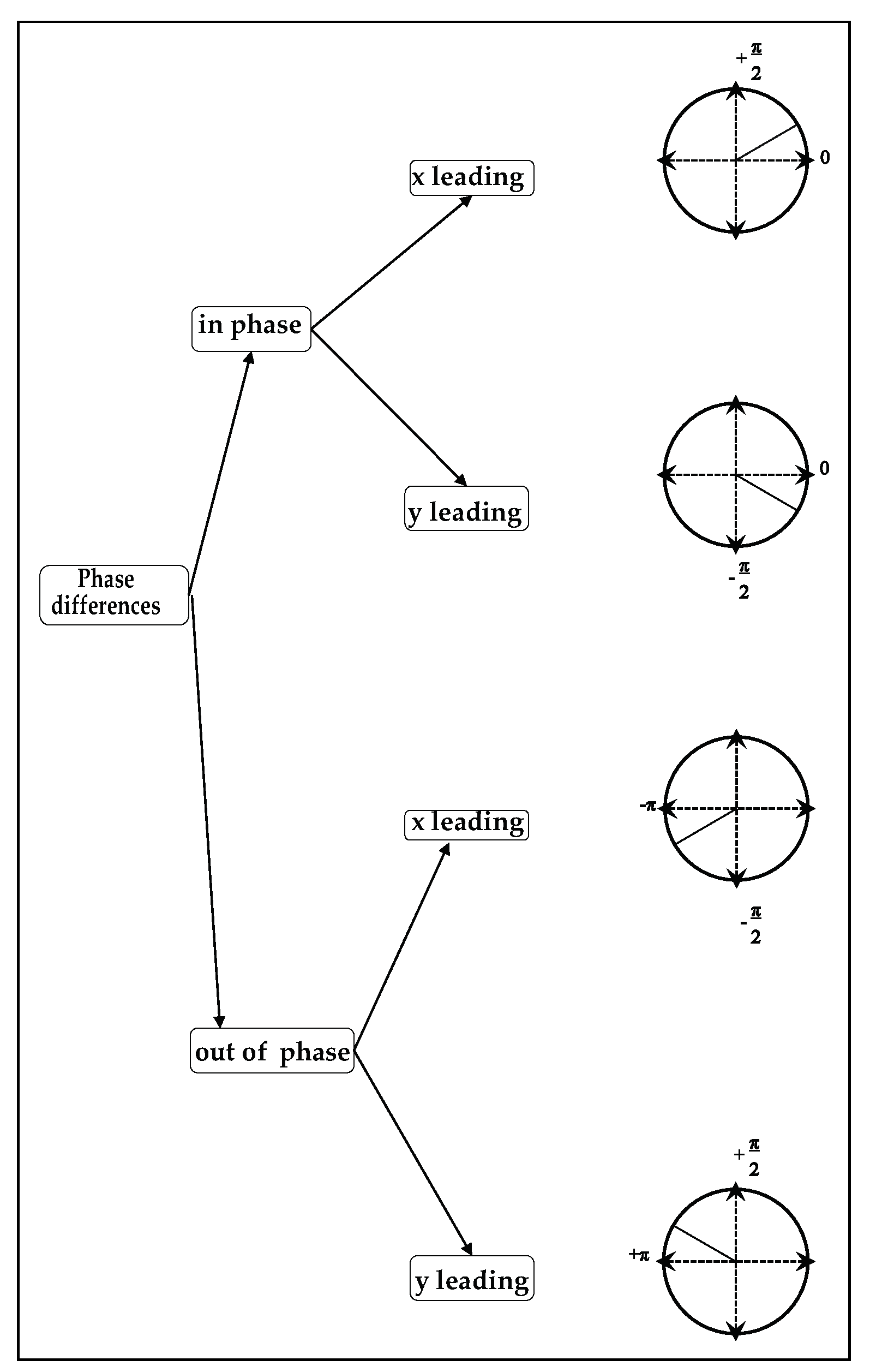

| TCC(WV) over DJSWI | — | — | — | — | — | In phase | — | — | — | — | — | In phase | — | — | — | — | — | In phase | ||

| TCC(US) over NYSE | — | — | — | — | — | Out of phase | In phase | In phase | In phase | In phase | In phase | Out of phase | — | — | — | — | — | Out of phase | ||

| TCC(GER) over DAX | — | — | — | — | — | Out of phase | In phase | In phase | In phase | In phase | In phase | Out of phase | — | — | — | — | — | Out of phase | ||

| TCC(JAP) over NIKKEI 225 | — | — | — | — | Out of phase | Out of phase | — | — | — | — | Out of phase | Out of phase | — | — | — | — | — | — | ||

| TCC(SA) over JSE TOP-40 USD | — | — | — | — | — | Out of phase | Out of phase | Out of phase | Out of phase | Out of phase | Out of phase | Out of phase | — | — | — | — | — | Out of phase | ||

| TCC(AUS) over ASX 200 | — | — | — | — | — | Out of phase | In phase | In phase | In phase | In phase | — | Out of phase | — | — | — | — | — | Out of phase | ||

| TCC(BRA) over IBOVESPA | — | — | — | — | — | Out of phase | In phase | In phase | In phase | Out of phase | Out of phase | Out of phase | — | — | — | — | — | Out of phase | ||

| 05-13 | 06-10 | 07-08 | ||||||||||||||||||

| 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | |||

| TCC(WV) over DJSWI | — | — | — | — | — | In phase | — | — | — | — | — | — | — | — | — | — | — | — | ||

| TCC(US) over NYSE | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | ||

| TCC(GER) over DAX | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | ||

| 02-19 | 03-18 | 04-15 | ||||||||||||||||||

| 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | 1 Day | 2 Days | 4 Days | 8 Days | 16 Days | 32 Days | |||

| TCC(JAP) over NIKKEI 225 | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | ||

| TCC(SA) over JSE TOP-40 USD | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | — | ||

| TCC(AUS) over ASX 200 | — | — | — | — | — | Out of phase | — | — | — | — | — | In phase | — | — | — | — | — | — | ||

| TCC(BRA) over IBOVESPA | — | — | — | — | — | Out of phase | — | — | — | — | — | — | — | — | — | — | — | — | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Valls Martínez, M.d.C.; Martín Cervantes, P.A. Testing the Resilience of CSR Stocks during the COVID-19 Crisis: A Transcontinental Analysis. Mathematics 2021, 9, 514. https://doi.org/10.3390/math9050514

Valls Martínez MdC, Martín Cervantes PA. Testing the Resilience of CSR Stocks during the COVID-19 Crisis: A Transcontinental Analysis. Mathematics. 2021; 9(5):514. https://doi.org/10.3390/math9050514

Chicago/Turabian StyleValls Martínez, María del Carmen, and Pedro Antonio Martín Cervantes. 2021. "Testing the Resilience of CSR Stocks during the COVID-19 Crisis: A Transcontinental Analysis" Mathematics 9, no. 5: 514. https://doi.org/10.3390/math9050514

APA StyleValls Martínez, M. d. C., & Martín Cervantes, P. A. (2021). Testing the Resilience of CSR Stocks during the COVID-19 Crisis: A Transcontinental Analysis. Mathematics, 9(5), 514. https://doi.org/10.3390/math9050514