1. Introduction

To implement the effective activities of organizations in the context of the transition to the digital economy, information systems and modern digital technologies are used, since, with their help, data on business processes are not only accumulated but also processed to obtain optimal management decisions. The principles of processing and accumulating data in various forms in information systems must comply with both national and international regulations, providing accounting and control of various types of accounting and financial assets. The digital technologies used in this case must take into account the industry specifics and features of the main business processes of the organization. Therefore, the main vendors supplying such systems to international markets provide the settings and configurations of their software products, allowing them to localize their systems to national requirements and regulations, taking into account the requirements of line ministries and departments.

The peculiarities of the creation of biological assets are that they are related to the land, as well as animals and plants, which act as means and subjects of labor in agriculture. They differ from other means and subjects of labor in their duration and cycle of life, and their cultivation depends on natural climatic conditions. Many studies around the world focus on the issues of assessing the fair value of biological assets, and special attention has been paid to these issues in countries in which the economy is based on agriculture and related industries [

1,

2,

3,

4,

5,

6,

7,

8,

9,

10,

11,

12,

13,

14,

15,

16,

17,

18,

19,

20,

21,

22,

23,

24,

25].

The authors’ theoretical studies are devoted to the research of the peculiarities of the application of accounting in agriculture in different countries of the world: C. Elad (2004) in Europe as a whole, M. Fischer (2013) in the USA, M. Lampe (2017) in Germany and Denmark, H. Bohušová (2018) in the Czech Republic, A. Vanova in Slovakia, S. Mili in Spain, L. Feleagă in Romania, V. Akasheva (2014) in Russia, N. Bayboltaeva (2018) in Kazakhstan, A. Khusainova in Tajikistan, R. Kurniawan (2014) in Indonesia, and S. Maruli and A. Farahmita (2011) in the Asia-Pacific region. The study of the application of the fair value and economic methods for assessing the assets of agricultural enterprises in terms of the impact on the financial reporting was carried out by A.A. Huffman (2013), R.L. Silva, P.C. Nardi, M. Ribeiro (2015), M. Fischer (2013), Feleagă and Răileanu (2012), etc.

Special attention in the above works is paid to the problems of profit volatility and subjective judgment when choosing a discount rate for the valuation of biological assets. We can state that there are virtually no satisfactory accounting models for assessing the fair value of biological assets in the practice of agricultural enterprises, considering the problem of accounting and valuation of biological assets in terms of Applied Mathematics. All existing models are based on expert assessment methods, market behavior of agents in the specified segment, and traditional principles of asset accounting (not necessarily biological). In the digital economy, issues of accounting and valuation of biological assets are becoming the most important for increasing the efficiency of a market sector, such as agriculture. Therefore, it is necessary to create a digital platform on which the accumulation and processing of data related to the accounting for biological assets would take place to implement the digital assessment methodology.

The purpose of the article is to develop principles of accounting for biological assets in financial reporting and the architecture description of the digital module of the information system, which allows to accumulate data and make management decisions through their processing, and to implement an assessment method based on fuzzy cognitive maps (using the example of agricultural enterprises of the Republic of Tajikistan).

2. The Essence of Accounting for Biological Assets from the Point of View of the International Financial Reporting Standard (IFRS)

One of the purposes of using IAS 41 Agriculture for agricultural enterprises is to evenly distribute revenue recognition across several periods [

26]. It should be noted that an agricultural enterprise, having a certain production season, generates proceeds from the sale of products precisely during the harvest (production) period. Without applying this standard, revenue would be recognized during the harvest period, i.e., in the third quarter of the reporting year. This leads to the fact that the agricultural producer faces difficulties in obtaining borrowed funds to ensure the proper level of working capital by providing a guarantee of borrowed funds’ repayment at the expense of future income from the harvest. It is in this situation that IAS 41 “Agriculture” comes to the rescue, allowing to recognize a part of future income from the process of “biological transformation” already at the moment of biological assets’ revaluation to their fair value” [

27,

28,

29,

30,

31].

This is the first industry standard adopted by the IASCF (International Accounting Standards Committee Foundation) that governs the treatment of biological assets in the financial statements of agricultural enterprises, i.e., performance.

The International Financial Reporting System (IFRS) having international significance and being developed by the decision of the Commission (committee) for the IFRS, which includes many states, i.e., professional organizations in many countries, in general, do not cover and are not tied to the legal and regulatory requirements of a particular state. It is this characteristic that makes its status international.

It should be noted that the regulatory framework of different countries is often different and, when preparing financial statements in accordance with the IFRS, it is necessary to disclose additional information related to the requirements of the national regulatory framework or other specific requirements [

7].

An agricultural enterprise in the general sense is an economic entity that, in addition to the production of agricultural products (biological assets), is also engaged in other activities, such as supply, sale, storage, processing, etc. To fulfill its statutory goals, an agricultural enterprise in its jurisdiction has property, equipment, and other assets and liabilities, the reflection of which, in the financial statements when using the IFRS, must be in accordance with the established requirements.

In agriculture, in addition to using IAS 41 “Agriculture”, other IFRSs are also used, which regulate the accounting and reflection of assets and liabilities in financial statements, which include such standards as IAS 1 “Presentation of Financial Statements”; IAS 2 Inventories; IAS 8 “Accounting Policies, Changes in Accounting Estimates and Errors”; IAS 16 Property, Plant, and Equipment; IAS 20 Accounting for Government Grants and Disclosure of Government Assistance; IAS 3b Impairment of Assets; IAS 37 “Provisions, Contingent Liabilities, and Contingent Assets”; IAS 38 Intangible Assets; and IAS 40 Investment Property. [

6,

27].

The use of international accounting and financial reporting standards related to an agricultural enterprise in the accounting and analytical system of the Republic of Tajikistan predetermines the need to clarify the conceptual apparatus represented by the basic definitions of international standards related to the specifics of agricultural production activities. For proper reflection on the financial statements of all assets and liabilities without exception, it is first of all necessary to comprehend the given definitions. IAS 41 “Agriculture” also defines basic terms such as “Biological Assets” and “Biotransformation”, etc.

IAS 41 “Agriculture” defines biological assets as follows: a biological asset is plants and animals controlled by an entity as a result of past events. This standard applies to accounting for biological assets and agricultural products, i.e., products obtained from biological assets at the time of collection [

29].

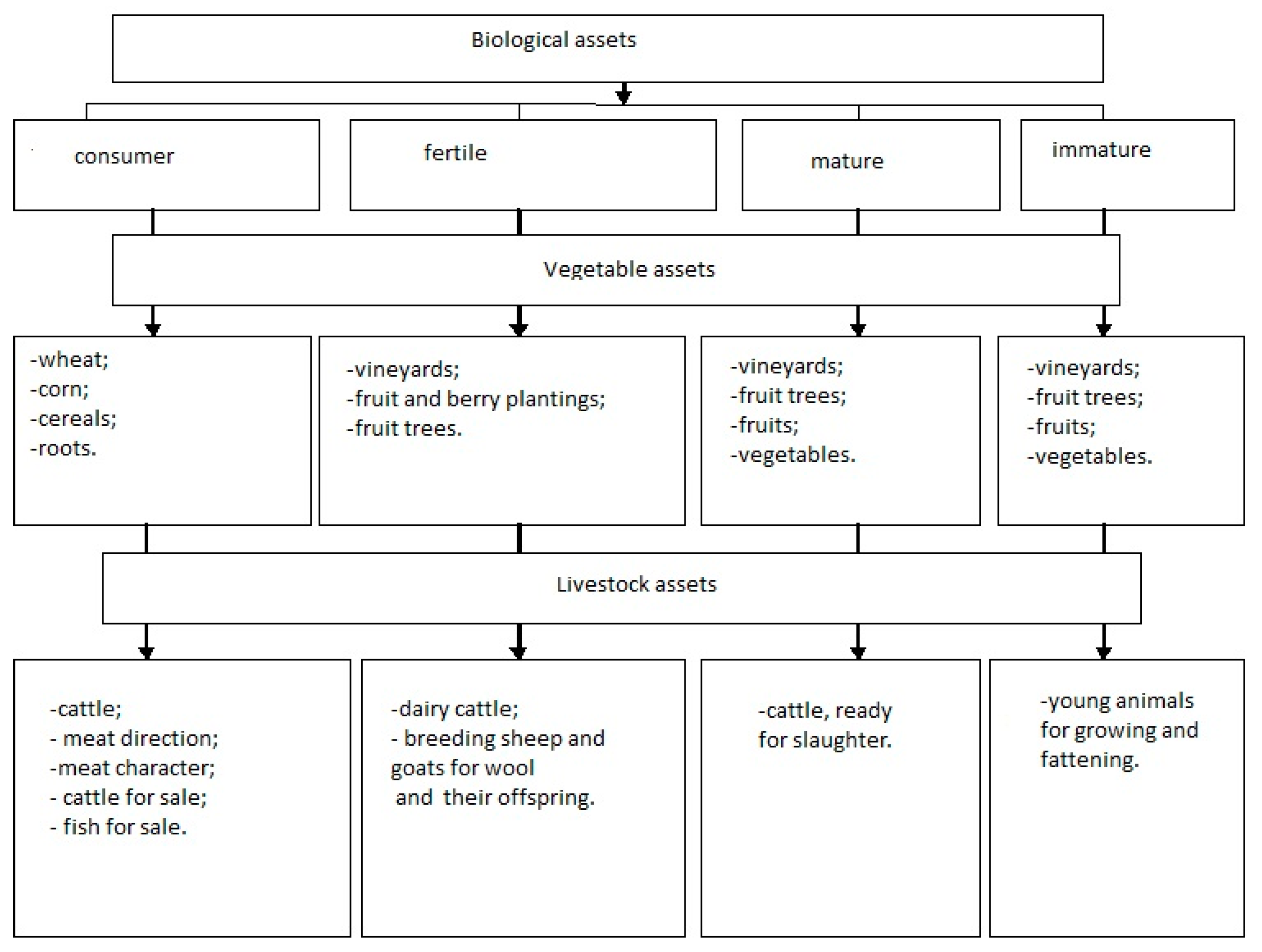

IAS 41 “Agriculture” allows biological assets to be grouped according to their purpose and the period of collection or use. The order of grouping biological assets is reflected in

Figure 1.

Along with the grouping typical for international practice, it is possible to divide biological assets into non-circulating (long-term) and circulating (short-term) assets. This is due to the structural content of the balance sheet used in practice at the enterprises of the Republic of Tajikistan and the peculiarities of marking in accounting and writing the value of property used in agricultural production.

Non-circulating (long-term) bio-assets create a separate group of biological assets that produce agricultural products or provide any other economic benefits for a period exceeding 12 months. In the crop production industry, non-circulating bio-assets include perennial plantations, and in livestock breeding, a food herd.

Circulating bio-assets are assets that produce products only for a short period within 12 months, after which they must be reproduced [

2].

Along with the grouping of biological assets, they can be subdivided by certain criteria. Based on the multiple receipts of agricultural products from a biological asset, they are divided into consumed and fertile (productive) assets. According to the degree of maturity as a sign of the grouping of biological assets, they are divided into mature and immature assets, and from the point of view of the terms of use, into circulating (short-term) and non-circulating (long-term) assets. In the regulatory legal documents governing the accounting of biological assets, it is also necessary to use grouping depending on their nature (biological assets of livestock, biological assets of crop production) and the degree of control. The classification of biological assets, according to the degree of their susceptibility to control, should cover and combine biological assets that are owned, leased, received on a lease, or that are on the right side of economic management, obtained for operational management. Practical use of the classification of biological assets makes it possible to form complete and reliable information related to their movement, as well as ensure proper control over the efficient use of biological assets at the disposal of an agricultural producer.

In accordance with the IFRS, a biological asset or agricultural products (products obtained from biological assets at the time of harvest) must be recognized in the financial statements of an enterprise in case:

Firstly, the entity controls the asset as a result of past events;

Secondly, these assets are likely to bring economic benefits in the future;

Thirdly, assets are preferably measured at fair value.

The future economic benefit, as a rule, is estimated based on the value of the main physical parameters of the biological asset being evaluated.

According to the IFRS 41 “Agriculture”, agricultural activities aim at managing the biotransformation of biological assets, which ultimately leads to the production of agricultural products or the production of additional biological assets. The process of biotransformation includes growth, degeneration, production, and reproduction, which forms the basis of changes in both quantitative and qualitative changes [

29].

Hence, depending on the type of agricultural activity, they still have certain common features: the ability to change; change of management; assessment of changes.

The main directions of the receipt of biological assets in the enterprise can be the purchase on the side, receiving, in the enterprise itself, contributions to the authorized capital of enterprises and receiving it free of charge under an agreement, providing for the fulfillment of obligations (payment) with no cash, etc.

The analysis of the accounting for biological assets showed the lack of specific assessment of biological assets of various types. The formulated general approaches to assessment do not take into account the economic features of countries, different economic models of behavior in agriculture, or cultural and national characteristics.

3. Accounting Principles for Biological Assets and Biotransformation Results for Agricultural Enterprises of the Republic of Tajikistan

According to the policy on food security of the Government of the Republic of Tajikistan, agriculture has an important role to play in providing the population with food, which also acts as a supplier of industrial raw materials and semi-finished products. In the context of digitalization, information and analytical support of accounting for agricultural enterprises allows to generate the necessary data for the management and other interested users of financial statements.

Since the Republic of Tajikistan is gradually integrating into the worldwide economic system, all reports accumulated and processed in information management systems of agricultural enterprises must contain reliable, useful, and objective accounting and reporting data and must be in accordance with the recommendations of the International Financial Reporting Standard (IFRS) and the regulatory framework, which is based on Law No. 702 of the Republic of Tajikistan “On accounting and financial reporting”, dated 25 March 2011.

At the same time, regarding the shortcomings of the accounting methodological basis, methodological guidelines reflecting the characteristics of agricultural production should be mentioned. In particular, this applies to one of the objects as biological assets, the specific weight of which is a significant proportion of agricultural enterprises.

The requirement of the current legislation of the Republic of Tajikistan, regarding the unity of methods and principles of accounting and financial reporting, is regulating it, as well as including the procedure for the development and adoption of state and industry standards, recommendations in the field of accounting, standards of an economic entity that apply to the valuation of property and obligations of agricultural enterprises, and the use of estimates at the actual cost of acquiring property in regulatory legal documents on accounting, which is an essential basis for assessing biological assets at actual costs in all directions of their receipt, except for receipt under a donation agreement (free of charge).

For the same reason, it is assumed that, not only biological assets, but all agricultural products obtained as a result of the assets’ biotransformation can be reflected in accounting, both at their actual cost and at fair value.

The value of the actual cost should be formed in the planned estimate at the time of receipt, with its subsequent bringing it to the actual cost at the end of the reporting year. A fair value measurement should be taken if the entity needs to present such data in the accounting (financial) statements. The information on the actual cost of biological assets obtained in accounting can then be transformed (converted, recalculated) into information on their fair value for the formation of accounting (financial) statements as of the date of their preparation. Recording biological assets using the fair value method increases the labor intensity of accounting work, which includes the assessment and bio-actives’ recording in the financial statements, but the feasibility of this process has a positive result. In our opinion, the key criterion when choosing a fair value measurement in accounting (financial) statements should be the fulfillment of the rationality’s requirement and compliance with the principles of the IFRS. The IFRS states that, when biological assets are recorded in the balance sheet at fair value, it is necessary to regularly check the value, both at the beginning of the reporting period and at the end, depending on changes in the composition and structure of assets that have occurred during the reporting period.

L.I. Khoruzhya and I.A. Sergeeva [

15] note that the IFRS provides the clearest and most complete definition of fair value, but, to be practically able to determine it in the accounting and financial reporting system, it is necessary to have information about a transaction with a similar asset. In this case, in their opinion, the transaction should be made between unrelated parties who have information about the conditions, which means the transaction is not forced.

The fair value of a biological asset can be more easily determined if the assets are pre-grouped, according to the main characteristics that the entity chooses from those used in the market as pricing (for example, age, product quality).

Many specialists in accounting for biological assets [

15,

16,

17,

18,

19,

20,

21,

22,

23,

24,

25,

26,

27,

28] reflect in the financial statements at a discounted value, which is calculated as the value of future cash flows at the date of the accounting (financial) statements at a discount rate. In the Republic of Tajikistan, the discount rate is proposed to determine the outcome in different ways:

- -

On the basis of the liquidation value of the biological asset;

- -

On the basis of the weighted average cost of the biological asset.

The calculation of the present value of a biological asset is made according to the formula, assuming that the agricultural enterprise will have a stable income from the sale in the future:

where Vt is the forecasted revenue from the sale of biological assets in the current period in monetary units:

K is the discount rate, %;

G is an average growth rate of proceeds from the sale of biological assets, %.

For the calculation in the conditions of the Republic of Tajikistan, the determination of the fair present value is practically impossible, and the increment of repeated use in the production process is more expedient than the accrual of depreciation from the amount of the initial cost. In this situation, the fair reporting (carrying) value of the bioactive is the difference between the initial cost and the accumulated depreciation.

Another issue of reflecting a biological asset in the financial statements is the order of its assessment associated with non-recurring assets. For this category, the fair value includes the actual costs incurred by the farm to acquire or build it.

Sometimes, the cost may approximate fair value if:

- -

From the moment the costs arise, there is no significant biotransformation (planting of seedlings);

- -

Biotransformation does not greatly affect the price

Since IAS 41 “Agriculture” does not contain and does not prescribe the depreciation of these types of biological assets, companies guided by the general principles of matching income and expenses can reduce the financial result of the reporting period in which the income is received. However, it is important that enterprises determine the useful life of a biological asset, that is, the period during which it will generate income for the company.

Analytical accounting of biological assets should cover quantitative and value terms. When quantitatively reflecting biological assets of an agricultural enterprise, the appropriate unit of physical measurement should be taken into account, which includes a piece, head, ton, kg., etc. Using units of bio-actives’ measurement in the crop production industry, taking into account the difficulties of quantitative determination, the use of the indicators of the cultivated areas that they occupy is allowed if an economic assessment is impractical. Among the main crops, for which it is more expedient to use the sown area indicator, are agricultural crops, such as cereals, sunflowers, and legumes [

7].

The introduction to the IFRS 41 Agriculture notes that, in agricultural activity, a change in the physical properties of an animal or plant immediately increases or decreases the economic benefits of the company. Using this model of accounting at initial cost, an agricultural enterprise engaged in horticulture will be able to reflect the profit no earlier than the first collection and sale of products from the biological assets reflected in the balance sheet, i.e., perhaps, only about 4 years after planting fruit trees, and in logging under the industry, even after 15–30 years, depending on the tree species. Under an accounting model, in which the biological growth of a biological asset is recognized and measured on the basis of current fair value, changes in fair value are recognized throughout the period from the moment of its establishment (tree planting) until its disposal (tree cutting). In modern conditions in the balance sheet, vineyards (mainly vineyard bushes) are accounted for at the end of the reporting period at their residual value as other fixed assets, i.e., the original cost of the garden minus the amount of accrued depreciation on it. At the same time, the amount of accrued depreciation for this garden for the period of fruiting and harvesting was displayed in the value of grapes sold during the corresponding period. This method of recording a biological asset in financial statements creates a distinctive feature of national accounting practices from others.

Each agricultural enterprise in the process of developing an accounting policy and its subsequent application can determine a specific procedure for organizing biological assets and the results of their biotransformation. According to A.S. Khusainova [

27], when determining the procedure for organizing accounting and reflecting biological assets in financial statements, an agricultural entity must be guided by the basic principles of accounting. The composition of the basic principles is shown in

Figure 2.

The specificity of agricultural production is characterized by the duration of the production and technological cycle, its seasonality, the discrepancy between the cost processes, and the receipt of finished products, the presence, and product use of our own production (seeds, feed), which leave an imprint on the mechanism for the formation of financial results from the activities of agricultural production.

A comparative analysis of the sources related to the valuation and accounting of biological assets in the Republic of Tajikistan showed that the problems in accounting for biological assets are identical to the world problems:

The fair value measurement of biological assets is difficult without a market for these assets in the country.

The fair value measurement of biological assets is related to unique characteristics, such as the increase in the value of assets in business processes (crops, livestock, etc.).

The increase in the value of assets on the sale makes it difficult to apply the method based on historical valuation.

The carrying value of the asset does not reflect its quality.

The cost allocation and accounting model does not distinguish between long-term assets (such as forest trees and oil palms) and short-term assets (such as poultry and rice crops).

4. A Fuzzy Model for Assessing the Value of Biological Assets, Taking into Account the Basic Principles of Accounting and the Results of Biotransformation and Risk

The present value of the cash-flows calculation, which includes the selection of the discount rate based on expert judgment, is used in most of the models in the assessment studies of the fair value of biological assets. The accuracy of the assessment determines the quality of financial information and the conditions of the profit management process [

21,

25,

31]. According to the study [

20], bio-assets for agricultural activities are measured at the beginning and end of the financial reporting period at the fair value and net of the sell costs. Gains or losses arising from changes in the fair value are recognized in profit or loss in the period in which they occur.

To build a fuzzy model for assessing biological assets, taking into account their biotransformation, we used the formalization associated with the investment processes’ description. Certainly, the purchase of a biological asset, such as fruit tree seedlings, can be viewed as an investment in the future. The biotransformation process is long and can be associated with risks, for example, some parts of the seedlings will die as a result and will not bring a return on investment.

The biotransformation process involves planning three main cash flows: the purchases’ flow of the initial biomaterial, the flow of current (operational) payments, and the flow of receipts after the end of the biotransformation process. All elements of this flow cannot be planned accurately because there is uncertainty associated with the future state of the market. The price and volumes of products sold (after the biotransformation process), the prices of initial biological assets, raw materials, and materials after a certain time may differ from the planned values.

Such unavoidable information uncertainty entails an unavoidable risk of decision-making in agricultural activities. Therefore, any agricultural enterprise is obliged to make efforts to raise its level of awareness and try to measure the riskiness of its decisions, both at the stage of purchasing biological assets and during the process of biotransformation.

Fuzzy set theory is a tool that allows you to measure opportunities (expectations). In the literature on investment analysis, the formula for the net present value (NPV) of investments is well known [

32,

33].

Let us take one important special case of NPV assessment, which we used as the basis for constructing a fuzzy model for assessing the value of biological assets, taking into account the following important conditions: all funds for the purchase of an initial type of biological asset fall on the beginning of the biological transformation process; the assessment of the residual value of biological assets is carried out after the end of the biotransformation process.

In view of the above, our formula takes the following form:

D—initial cash investment;

—the number of planned intervals in the k-th period of biotransformation;

p—the number of planned biotransformation periods;

—discount rate in the k-period of biotransformation,

—the receipts and payments circulating balance in the i-th interval of the k-th period of biotransformation;

—biological assets’ liquidation value of the k-period of biotransformation.

NPVBA biological asset valuation;

The discount rate is planned so that the period of interest accrual on the funds used coincides with the corresponding period of the biotransformation process; th interval does not refer to the k-th period of biotransformation but is allocated in the model to fix this moment so that the final financial result of the k-th period of biotransformation (transition of a biological asset from one species to another) is unambiguous.

All parameters in Formula (2) are fuzzy, i.e., their exact meaning is unknown but can be determined in a certain interval. The distribution within this interval is also an unknown function, then, as an estimate of the initial data, the theory of fuzzy sets recommendations using triangular fuzzy numbers with a standard membership function. Triangular numbers simulate the following natural language statements: “x is approximately equal to and is in the range ”. This approach makes it possible to formulate three types of the scenario for assessing the value of a biological asset: pessimistic, typical, optimistic.

In this case, Formula (2) takes the form:

Generally speaking, it is necessary to understand that, when multiplying and dividing triangular fuzzy numbers, the result is a number that does not have a clear triangular form [

33,

34]. In our particular case, at certain values of the discount rate

and

, the number of planned intervals in the k-th biotransformation period and the resulting number can be considered triangular. This can be shown with a specific example:

и

.

In this case, the number

has a triangular shape (see

Figure 3 and

Figure 4).

The rest of the operations in Formula (2) do not violate the triangular form of the result, i.e., the parameter for assessing the cost of a biological asset.

Violation of the usual properties of operations on numbers in the transition to fuzzy numbers with floating point makes performing arithmetic operations a rather difficult task. The literature [

33] describes in detail the rules for performing algebraic operations on the class of fuzzy numbers, which includes normal, unimodal fuzzy numbers, with convexity to the left and right from the maximum point of the membership function. In particular, in [

33,

34], rules are formulated for performing arithmetic operations on fuzzy numbers in the decomposition of the latter into the α-level sets of fuzzy numbers.

When expanding into the α-level sets of fuzzy numbers, the values of the inverse to the membership functions on the intervals of increasing and decreasing were calculated: . A single-valued inverse function f–1(y) exists on the interval [x1, x2] if the function f(x) is continuous and monotone on this interval. This is why, from the set of all fuzzy numbers, a class of normal, unimodal fuzzy numbers with convexity to the left and right form the maximum point of the membership function.

Let:

- (1).

,;

- (2).

μa(a0) = 1 (a0 ∈ Ua), μb(b0) = 1 (b0 ∈ Ub);

- (3).

μa(x) = μ↑a(x), x ∈ (–∞, a0], μb(x) = μ↑b(x), x ∈ (–∞, b0]; membership functions of numbers a and b increase (do not decrease) on intervals (–∞, a0] and (–∞, b0];

- (4).

μa(x) = μ↓a(x), x ∈ [a0, +∞), μb(x) = μ↓b(x), x ∈ [b0, +∞); membership functions of numbers a and b decrease (do not increase) on intervals [a0, +∞) and [b0, +∞).

The rules for performing arithmetic operations on fuzzy numbers are then determined by the following formulas:

where

.

Based on the proposed assessment model, all NPVBA implementations defined by the membership function in

Figure 5 at a given level of membership α are equally possible; therefore, the risk of investment inefficiency

is the geometric probability of an event of a point entering in the area

into the zone

, which is calculated by the following formula:

where

—values of

at which

—the membership function of the risk of inefficience using bio-assets in decomposition of fuzzy numbers into α-level sets.

However, in practice, the zero income is not acceptable for economic activities; therefore, when making decisions on the purchase of bio-assets with their subsequent transformation, the owner assesses the income in the future in percentage terms. If the given rate of return β is a percentage of investments D, then Formula (7) becomes:

—values of at which

—the maximum acceptable risk to make a decision on purchasing bio-assets.

This approach makes it possible to calculate all the key parameters in assessing the value of a biological asset, based on analytical ratios.

5. Application of the Fuzzy Model of Assessing the Value of Biological Assets at the Agricultural Enterprises of the Republic of Tajikistan

Some agricultural enterprises in the Republic of Tajikistan purchased vineyard seedlings for about 350 thousand somoni (1 somoni = 0.088 dollars).

In about 1 year, according to experts, it is possible to harvest the grapes. The number of transformation periods is 1, and the intervals in one period are 2. When calculating, we must keep in mind that the residual liquidation value of the asset is 0.

Let us apply the proposed formalization of calculating the biological asset cost with the following values:

,

. The rest of the values are shown in

Table 1.

Based on the data in

Table 1, and taking into account the assumption of the triangular form of the number that specifies the NPVBA value estimate, we obtain an explicit form of the NPVBA indicator’s membership function:

In our case, . This indicator allows not only to make a more effective decision on the purchase of bioactive assets but also to optimize the use of invested funds since the fuzzy valuation model can be reconfigured at any time. To achieve this effect, it is necessary to develop an information module for biological assets and the accounting of the biotransformation results.

6. Architecture of the Information Module for Accounting of Biological Assets and the Results of Biotransformation

Formalization of accounting standards in the field of assessing the fair value of biological assets will improve not only the quality of financial statements, but also the process of managing the profits of agricultural organizations. The digitalization of accounting mechanisms, which include the recognition, assessment, and disclosure of information on agricultural activities, will improve the quality of revenue management for companies in the agricultural sector and efficiently organize information flows. [

35,

36]. At the same time, useful information as a means of reducing uncertainty ensures an increase in the efficiency of the decision-making process, which, ultimately, is reflected in the results of economic activities of any business unit.

Functional information exchange, which implies the availability of accumulated information, explores its causality, provides effective modeling of the necessary knowledge based on intellectual models and high-quality circulation of information resources, and occurs using the digital platforms [

37,

38,

39,

40].

The architecture of the information system in the digital economy is modular and must support all management processes using appropriate technologies [

41,

42,

43].

The general architecture of the information module of accounting for biological assets and the results of biological transformation can be represented in the form of three main subsystems (see

Figure 6):

1. The mathematical subsystem includes the main calculating means of input data of the subject area in accordance with the models of assessing the factors of accounting for biological assets using data mining. This subsystem contains a set of programs that offer interaction with other subsystems in real time using standard interfaces that provide data processing and their transmission to the information system.

2. The instrumental graphical subsystem implements a graphical interface and provides visual preparation of the model’s object or economic process under consideration, the layout of the computational domain for convenient placement of elements in the workspace of the webserver, and interaction with the full set of scenarios and indicators used for modeling.

3. The database subsystem of the subject area contains a structured, replenished relational knowledge base about the simulated indicators of accounting for biological assets, as well as standards and principles of interaction between subsystems.

During the calculation, the user interacts with each of the subsystems through the standard web application interface. The implementation of a computational experiment for a specific mathematical model in the application is presented in the form of sequential work with input data, carried out within a single interface [

44].

We suggest using service-oriented architecture (SOA) for the successful integration of the information module because it allows implementation of the principles of its embeddedness into the appropriate IT (information technology) infrastructure of an organization, taking into account the big data processing technologies [

45,

46,

47,

48].

Web services technology allows applications to interact with each other regardless of the deployed platform and the programming language in which they are written. The web service has a programming interface that describes a set of operations (web methods) that are remotely invoked through standardized XML messages. This creates the basis for both the use of the developed services within the IT infrastructure of an enterprise and the automation of business processes, in the implementation of which several enterprises are involved.

The construction of information modules for the accounting of biological assets should be based on a web services architecture (WSA), a type of service-oriented architecture (SOA).

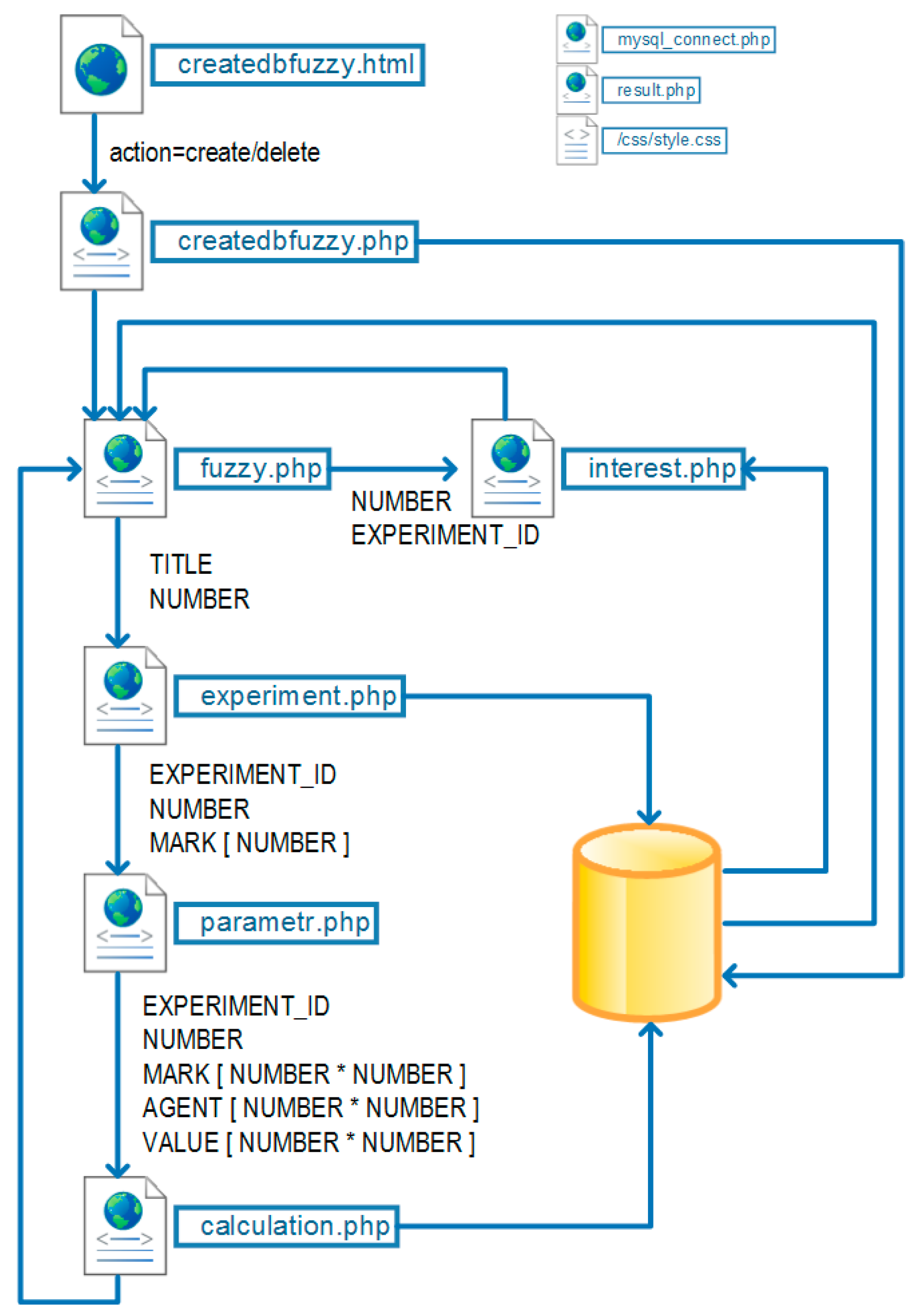

The main page of the web service is fuzzyuchet.php.

Figure 7 shows the interface of interaction between a web browser, a web server, and a database.

A user’s request to the web service initiates a request to a database, which entails the creation of an associative array, the elements of which are sequentially sent to the interest.php page. The script for this page prompts the user to perform data entry actions that are accumulated in the experiment.php page. The page parameter.php, without accessing the database, creates two arrays, MARK [NUMBER * NUMBER] and AGENT [NUMBER * NUMBER], with the name of the parameters and one array, VALUE [NUMBER * NUMBER], with values corresponding to the mutual influence of the parameters on each other, which are sent to the calculation.php page, where the necessary calculations are made.

The corresponding data is taken from the PrUchBA tuple, the elements of which were selected on the basis of the content analysis [

48,

49,

50,

51]:

where

I—identification of a biological asset (registration number);

T—time of recognition;

Period—interval of time before its transformation;

S—cost information of a biological asset;

Risk—risk of inefficient use of a biological asset;

U—fuzzy management function, taking into account the particular character of a biological asset;

Rez—set of the characteristics of the results of accounting for biological assets and the results of biological transformation.

This approach will allow one to fully take into account the result of the activity of an agricultural enterprise, which is determined by means of a monetary valuation of all business processes, since, according to the principles of the IFRS organization, it is possible to determine the financial result only through an assessment of the accounting objects that form it. The systematic use of the information module will allow to gather information and, using the accumulated data, clarify the intervals that formalize the initial data of the fuzzy model.

According to the current regulatory legal act in the Republic of Tajikistan governing accounting, the financial result is defined as the difference between the income and expenses of the enterprise. Based on the above requirements for assessing the financial result, one of the most important points in the organization of accounting for financial results is the correct determination of the amount of income and expenses during the reporting period, taking time costs into account.

7. Conclusions

Thus, the implementation and effective use of IAS 41 “Agriculture” in the activities of agricultural enterprises in the Republic of Tajikistan in the context of digitalization should be based on the improvement of the regulatory and legal framework, the use of modern information technologies, the formation, and development of an active agricultural market, which will contribute effective determination of the fair value of a bioactive asset.

The proposed architecture of the module for accounting for biological assets and the results of biotransformation, implemented as a web service, will allow, in full, correctly and comprehensively, to reflect and disclose the most significant information for an agricultural entity about accounting for biological assets in financial statements, which will lead to transparency and reliability of the submitted users of financial statements. The developed fuzzy model for assessing the cost of biological assets makes it possible to obtain an interval cost, taking into account the basic principles of accounting and the results of biotransformation. Based on this result, a specific agricultural enterprise can implement an economically sound forecast and form a development strategy for the medium period, assessing the risks of economic activity. Based on this result, a particular agricultural enterprise can implement an economically sound forecast, form a development strategy in the medium term, assess the risks of economic activities, and obtain the fair value of biological assets at any time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}