The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance

Abstract

:1. Introduction

2. Theoretical Background

2.1. CSR from a Diachronic Perspective

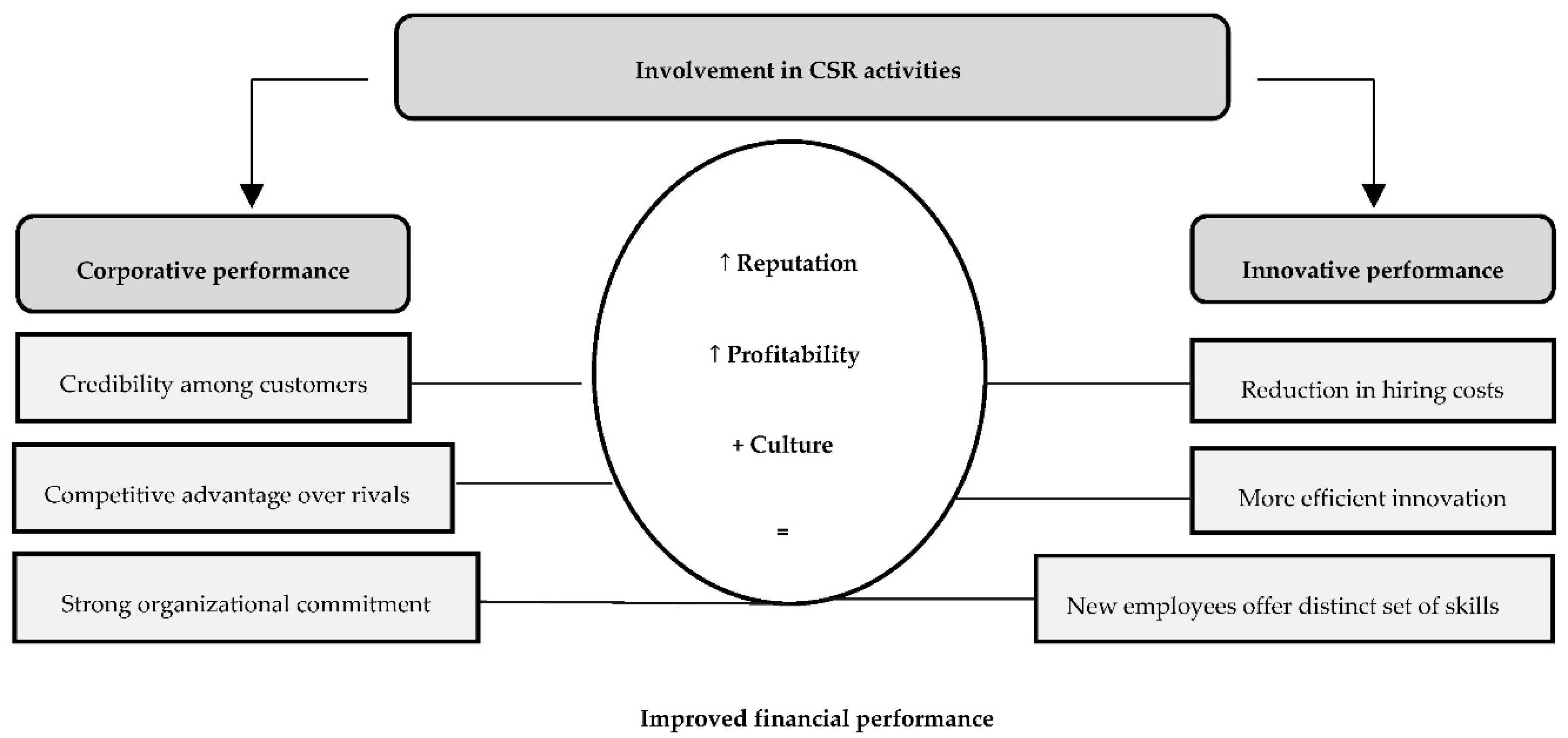

2.2. The Influence of CSR on Corporate Performance Perspectives

2.3. The Relationship between CSR and Innovation

2.4. Appraisal of the Most Cited Literature

2.5. The Emergence of Responsible Innovation

3. Methodology

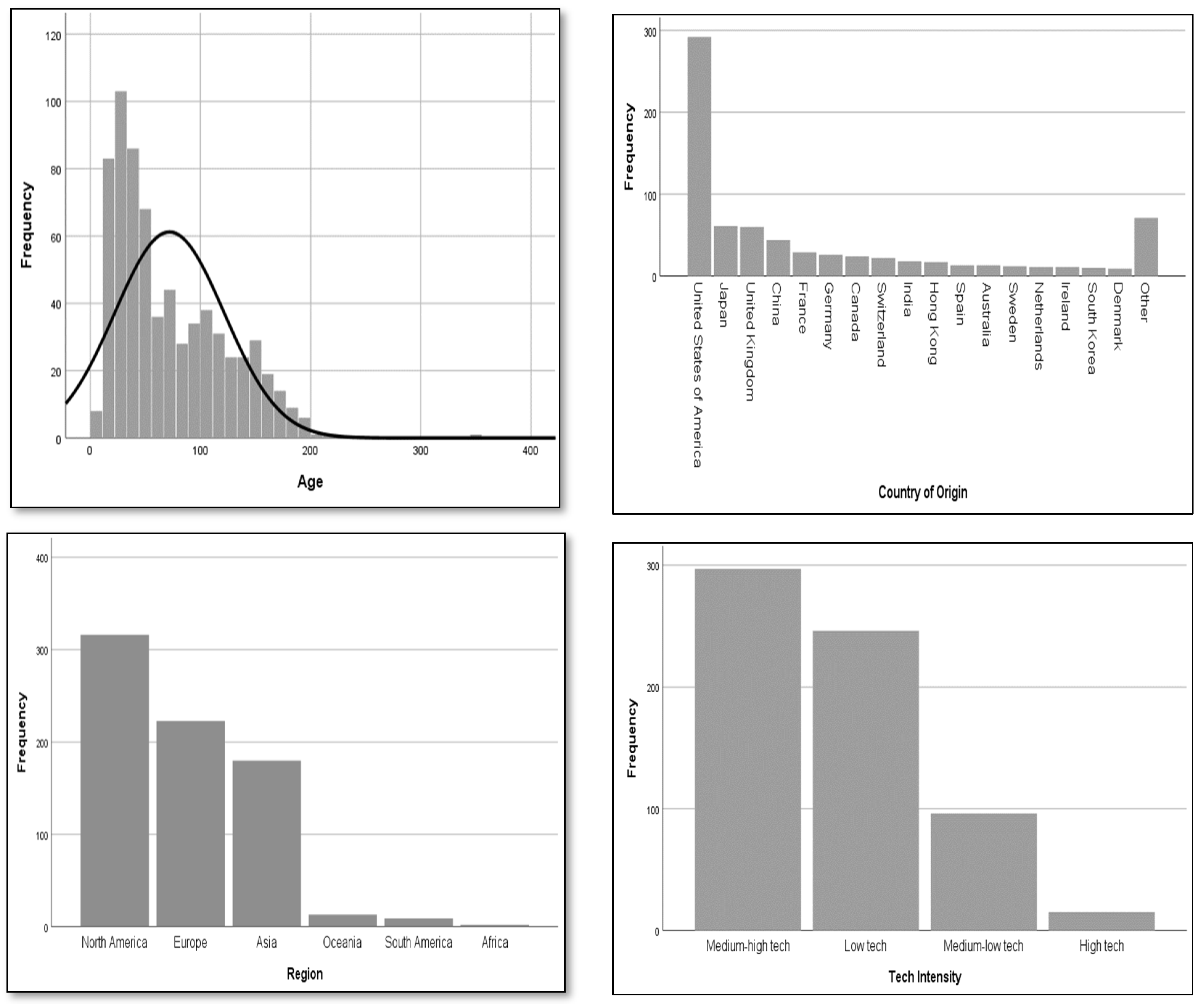

3.1. Sample Description

3.2. Proxying Corporate Social Responsibility

3.3. The Impact of CSR and Innovation on Financial Performance

3.4. Descriptive Statistics and Correlations

4. Econometric Analysis

4.1. Econometric Estimations

4.2. Results and Discussion

5. Conclusions

5.1. Theoretical and Empirical Findings

5.2. Limitations and Future Research

5.3. Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | |

| 2 | https://www.sustainalytics.com/esg-data (accessed on 15 February 2022). |

| 3 | Rating used to rank: Eurostat NACE Rev.2 3-digit level—Classification of manufacturing industries. |

References

- Ali, Rizwan, Muhammad S. Sial, Talles V. Brugni, Jinsoo Hwang, Nguyen V. Khuong, and Thai H. T. Khanh. 2019. Does CSR Moderate the Relationship between Corporate Governance and Chinese Firm’s Financial Performance? Evidence from the Shanghai Stock Exchange (SSE) Firms. Sustainability 12: 149. [Google Scholar] [CrossRef] [Green Version]

- Barrena Martínez, Jesus, Macarena López Fernández, and Pedro Miguel Romero Fernández. 2016. Corporate social responsibility: Evolution through institutional and stakeholder perspectives. European Journal of Management and Business Economics 25: 8–14. [Google Scholar] [CrossRef] [Green Version]

- Bennink, Hans. 2020. Understanding and Managing Responsible Innovation. Philosophy of Management 19: 317–48. [Google Scholar] [CrossRef]

- Bocquet, Rachel, Christian Le Bas, Caroline Mothe, and Nicolas Poussing. 2012. CSR Firm Profiles and Innovation: An Empirical Exploration with Survey Data. SSRN Electronic Journal. [Google Scholar] [CrossRef] [Green Version]

- Bocquet, Rachel, Christian Le Bas, Caroline Mothe, and Nicolas Poussing. 2013. Are firms with different CSR profiles equally innovative? Empirical analysis with survey data. European Management Journal 31: 642–54. [Google Scholar] [CrossRef] [Green Version]

- Branco, Manuel Castelo, and Lúcia Lima Rodrigues. 2006. Corporate social responsibility and resource-based perspectives. Journal of Business Ethics 69: 111–32. [Google Scholar] [CrossRef]

- Broadstock, David, Roman Matousek, Martin Meyer, and Nickolaus Tzeremes. 2019. Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental and social governance implementation and innovation performance. Journal of Business Research 119: 99–110. [Google Scholar] [CrossRef]

- Chapple, Wendy, and Jeremy Moon. 2005. Corporate social responsibility (CSR) in Asia a seven-country study of CSR Web site reporting. Business and Society 44: 415–41. [Google Scholar] [CrossRef] [Green Version]

- Chong, Wei, and Gilbert Tan. 2010. Obtaining Intangible and Tangible Benefits from Corporate Social Responsibility International Review of Business Research Papers Corporate Social Responsibility. Singapore: Institutional Knowledge at Singapore Management University, pp. 360–71. [Google Scholar]

- Cohen, Jacob. 1988. Statistical Power Analysis for the Behavioral Sciences, 2nd ed. London: Routledge. [Google Scholar]

- Commision of the European Communities. 2001. Green Paper—Promoting a European framework for Corporate Social Responsibility. Brussels: Commision of the European Communities. [Google Scholar]

- Cook, Kristen, Andrea Romi, Daniela Sánchez, and Juan Sánchez. 2019. The influence of corporate social responsibility on investment efficiency and innovation. Journal of Business Finance and Accounting 46: 494–537. [Google Scholar] [CrossRef]

- Costa, Cláudia, Luís Lages, and Paula Hortinha. 2015. The bright and dark side of CSR in export markets: Its impact on innovation and performance. International Business Review 24: 749–57. [Google Scholar] [CrossRef]

- Dahlsrud, Alexander. 2008. How corporate social responsibility is defined: An analysis of 37 definitions. Corporate Social Responsibility and Environmental Management 15: 1–13. [Google Scholar] [CrossRef]

- Davis, Keith. 1960. Can business afford to ignore social responsibilities? Corporate Social Responsibility 2: 23–29. [Google Scholar] [CrossRef]

- Duque-Grisales, Eduardo, and Javier Aguilera-Caracuel. 2019. Environmental, Social and Governance (ESG) scores and financial performance of multilatinas: Moderating effects of geographic international diversification and financial slack. Journal of Business Ethics 168: 315–34. [Google Scholar] [CrossRef]

- Fatma Mobin, Imran Khan, and Zillur Rahman. 2018. Striving for legitimacy through CSR: An exploration of employees responses in controversial industry sector. Social Responsibility Journal 15: 924–38. [Google Scholar] [CrossRef]

- Ferrell, Allen, Liang Hao, and Luc Renneboog. 2016. Socially responsible firms. Journal of Financial Economics 122: 585–606. [Google Scholar] [CrossRef] [Green Version]

- Freeman, Edward, and John McVea. 2001. A Stakeholder Approach to Strategic Management. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Friedman, Milton. 1970. The social responsibility of business is to increase its profits. Corporate Social Responsibility, 31–35. [Google Scholar]

- Gallego-Álvarez, Isabel, José Manuel Prado-Lorenzo, and Isabel Maria García-Sánchez. 2011. Corporate social responsibility and innovation: A resource-based theory. Management Decision 49: 1709–27. [Google Scholar] [CrossRef]

- Gil, Cohen. 2022. What can we learn from the financial market about sustainability? Environment Systems and Decisions 42: 1–7. [Google Scholar] [CrossRef]

- Hao, Jing, and Feng He. 2022. Corporate Social Responsibility (CSR) Performance and Green Innovation: Evidence from China. Finance Research Letters 48: 102889. [Google Scholar] [CrossRef]

- Ho, Virginia Harper. 2015. Corporate Social Responsibility in China: Law and the Business Case for Strategic CSR. SCJ Journal of International Business & Law. Available online: https://heinonline.org/hol-cgi-bin/get_pdf.cgi?handle=hein.journals/scjilb12andsection=5 (accessed on 22 March 2022).

- Im, Hyun, Roy Song, and Meng Zhao. 2020. CSR Performance and the Economic Value of Innovation. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Javed, Muhzar, Muhammad Rashid, Ghulam Hussain, and Hafiz Ali. 2020. The effects of corporate social responsibility on corporate reputation and firm financial performance: Moderating role of responsible leadership. Corporate Social Responsibility and Environmental Management 27: 1395–409. [Google Scholar] [CrossRef]

- Ji, Huanyong, Guannan Xu, Yuan Zhou, and Zhongzhen Miao. 2019. The impact of Corporate Social Responsibility on firms’ innovation in China: The role of institutional support. Sustainability 11: 6369. [Google Scholar] [CrossRef] [Green Version]

- Lahouel, Béchir, Younes Zaied, Yaoyao Song, and Guao-Liang Yang. 2020. Corporate social performance and financial performance relationship: A data envelopment analysis approach without explicit input. Finance Research Letters 69: 101656. [Google Scholar] [CrossRef]

- Lee, Jegoo, Samuel Graves, and Sandra Waddock. 2018. Doing good does not preclude doing well: Corporate responsibility and financial performance. Social Responsibility Journal 14: 764–81. [Google Scholar] [CrossRef]

- Liao, Yu, Xiadong Qiu, Anni Wu, Qian Sun, Haomin Shen, and Peyiang Li. 2022. Assessing the Impact of Green Innovation on Corporate Sustainable Development. Frontiers in Energy Research 9: 800848. [Google Scholar] [CrossRef]

- Lin, Lin, Pi-Hsia Hung, De-Way Chou, and Christine Lai. 2019. Financial performance and corporate social responsibility: Empirical evidence from Taiwan. Asia Pacific Management Review 24: 61–71. [Google Scholar] [CrossRef]

- Lu, Jintao, Licheng Ren, Chong Zhang, Chunyan Wang, Zahra Shahid, and Justas Streimikis. 2020. The Influence of a Firm’s CSR Initiatives on Brand Loyalty and Brand Image. Journal of Competitiveness 12: 106–124. [Google Scholar] [CrossRef]

- Luo, Xueming, and Shuili Du. 2015. Exploring the relationship between corporate social responsibility and firm innovation. Marketing Letters 26: 703–14. [Google Scholar] [CrossRef]

- Macgregor, Steven, and Joan Fontrodona. 2008. Exploring the fit between CSR and innovation. Business 3: 23. [Google Scholar] [CrossRef] [Green Version]

- Maqbool, Shafat, and Nasir Zameer. 2018. Corporate social responsibility and financial performance: An empirical analysis of Indian banks. Future Business Journal 4: 84–93. [Google Scholar] [CrossRef]

- Martinez-Conesa, Isabel, Pedro Soto-Acosta, and Mercedes Palacios-Manzano. 2017. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. Journal of Cleaner Production 142: 2374–83. [Google Scholar] [CrossRef]

- Mc Williams, Abagail, and Donald Siegel. 2018. Corporate social responsibility: A theory of the firm perspective. Business Ethics and Strategy 26: 137–47. [Google Scholar] [CrossRef]

- Mishra, Dev. 2017. Post-innovation CSR Performance and Firm Value. Journal of Business Ethics 140: 285–306. [Google Scholar] [CrossRef]

- Nidumolu, Ram, C. K. Prahalad, and M. R. Rangaswami. 2009. Why sustainability is now the key driver of innovation. Harvard Business Review 87: 9. [Google Scholar]

- Orlitzky, Marc, Frank Schmidt, and Sara Rynes. 2003. Corporate Social and Financial Performance: A meta-analysis. Organization Studies 24: 403–41. [Google Scholar] [CrossRef]

- Quazi, Ali, and Dennis O’Brien. 2000. An Empirical Corporate Test of a Model of Social Responsibility. Journal of Business Ethics 25: 33–51. [Google Scholar] [CrossRef]

- Refinitiv. 2021. Refinitiv ESG Company Scores. Refinitiv. Available online: https://www.refinitiv.com/en/sustainable-finance/esg-scores (accessed on 8 November 2021).

- Russo, Michael, and Paul Fouts. 1997. A resource-based perspective on corporate environmental performance and profitability. Academy of Management Journal 40: 534–59. [Google Scholar] [CrossRef]

- Sameer, Ibrahim. 2021. Impact of corporate social responsibility on organization’s financial performance: Evidence from Maldives public limited companies. Future Business Journal 7: 29. [Google Scholar] [CrossRef]

- Stilgoe, Jack, Richard Owen, and Phil Macnaghten. 2013. Developing a framework for responsible innovation. Research Policy 42: 1568–80. [Google Scholar] [CrossRef] [Green Version]

- Uyar, Ali, Abdullah Karaman, and Merve Kılıç. 2020. Is corporate social responsibility reporting a tool of signaling or greenwashing? Evidence from the worldwide logistics sector. Journal of Cleaner Production 253: 119997. [Google Scholar] [CrossRef]

- van Marrewijk, Marcel. 2013. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. Journal of Business Ethics 2: 95–105. [Google Scholar] [CrossRef]

- Visser, Wayne. 2009. Corporate Social Responsibility in Developing Countries. Oxford: The Oxford Handbook of Corporate Social Responsibility, pp. 1–28. [Google Scholar] [CrossRef] [Green Version]

- Von Schomberg, René. 2014. Prospects for Technology Assessment in a Framework of Responsible Research and Innovation. SSRN Electronic Journal, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Wang, Qian, Junsheng Dou, and Shenghua Jia. 2016. A Meta-Analytic Review of Corporate Social Responsibility and Corporate Financial Performance: The Moderating Effect of Contextual Factors. Business and Society 55: 8. [Google Scholar] [CrossRef]

- Wu, Liu, Zhen Shao, Changhui Yang, Tao Ding, and Wan Zhang. 2020. The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry. Sustainability 12: 6799. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Title | Authors | Journal | Objective | Methodology | Results | Citations |

|---|---|---|---|---|---|---|

| Social issues in supply chains: Capabilities link responsibility, risk (opportunity), and performance | Robert D. Klassen, Ann Vereecke | International Journal of Production Economics | Understand which social management capabilities contribute to competitiveness and how they can be linked to social responsibility, risk, opportunity, and performance in the supply chain. | Construction of a framework by joining information from various case studies along with interview responses. | Four links explain the existing relationship: exposure, audit, mitigation, and development. | 311 |

| Corporate social responsibility and its effect on innovation and firm performance: Empirical research in SMEs | Isabel Martinez-Conesa, Pedro Soto-Acosta, Mercedes Palacios-Manzano | Journal of Cleaner Production | Understand the relationship between CSR and organizational innovation and corporate performance in Spanish SMEs. | Construction of an equation model to evaluate data collected from a sample of 552 Spanish companies. | They proved the positive effect of CSR activities on companies’ innovation. | 137 |

| Exploring the Relationship Between Business Model Innovation, Corporate Sustainability and Organizational Values within the Fashion Industry | Esben Rahbek Gjerdrum Pedersen, Wencke Gwozdz, Kerli Kant Hvass | Journal of Business Ethics | Analyze the relationship between business model innovation, corporate sustainability, and underlying organizational values. | Interviews conducted with 492 managers in the Swedish fashion industry. | Fashion companies that exhibit high levels of business model innovation are more likely to be proactive on the sustainability agenda. | 95 |

| Who Needs CSR? The Impact of Corporate Social Responsibility on National Competitiveness | Ioanna Boulouta, Christos N. Pitelis | Journal of Business Ethics | Explore if and how CSR can impact the competitiveness of nations. | Analysis of data collected from a sample of 19 developed countries over a 6-year period. | CSR can make a significant positive contribution to national competitiveness, as measured by national standards of living. | 94 |

| The influence of corporate social responsibility practices on organizational performance: evidence from Eco-Responsible Spanish firms | Carmelo Reverte, Eduardo Gomez-Melero, Juan Gabriel Cegarra-Navarro | Journal of Cleaner Production | Analyze the impact of CSR practices on organizational performance, covering financial, and non-financial indicators, and study the potential mediating role of innovation in the CSR–performance relationship. | Construction of an equation model to evaluate data from a sample of 133 Spanish eco-responsible companies. | Positive and significant direct effects of CSR on innovation and organizational performance in all groups of companies. | 93 |

| N° of Companies | % | |

|---|---|---|

| N° Employees | ||

| Less than 1000 | 10 | 1.3 |

| Between 1000 and 100,000 | 106 | 14.2 |

| Between 100.000 and 500,000 | 282 | 37.9 |

| More than 500.000 | 297 | 39.9 |

| Age | ||

| Less than 50 years | 312 | 41.9 |

| Between 50 and 100 years | 182 | 24.5 |

| Between 100 and150 years | 135 | 18.1 |

| More than 150 years | 59 | 7.9 |

| Sector | ||

| Financial | 170 | 22.8 |

| Electronic | 95 | 12.8 |

| Utility Services | 62 | 8.4 |

| Drugs, Cosmetics, and Health Care | 52 | 6.9 |

| Remaining | 365 | 49.1 |

| Annual Turnover | ||

| Less than 5 million | 162 | 21.8 |

| Between 5 and 10 million | 125 | 16.8 |

| Between 10 and 20 million | 134 | 18 |

| More than 20 million | 320 | 43.2 |

| Variables | Abbrev | Description | Evaluation |

|---|---|---|---|

| ESG Score (1) | ESG | Overall score given to the company based on information reported by management on the environmental, social, and corporate governance pillars. | Percentage |

| CSR Strategy Score (2) | CSRStr | Reflects the company’s practices in communicating that it integrates the economic, social, and environmental dimensions in its decision-making processes. | Percentage |

| CSR Sustainability Committee (3) | CSRCom | Whether the company has a CSR committee or team. | 0 = No; 1 = Yes |

| CSR Sustainability Reporting (4) | CSRRep | Whether the company publishes a separate report or a section in its annual CSR/sustainability report. | 0 = No; 1 = Yes |

| North America | South America | Asia | Africa | Europe | Oceania | |

|---|---|---|---|---|---|---|

| ESG | 0.066 | −0.017 | 0.100 | 0.029 | 0.054 | 0.019 |

| CSRStr | 0.129 | 0.019 | 0.118 | 0.037 | 0.093 | 0.031 |

| CSRRep | 0.17 | 0.00 | 0.18 | 0.00 | 0.06 | 0.00 |

| CSRCom | 0.10 | 0.33 | 0.10 | 0.00 | 0.05 | 0.15 |

| Variables | Abbreviation | Description | Measurement |

|---|---|---|---|

| Research and Development (5) | R&D | Represents all direct and indirect costs related to the creation and development of new processes, techniques, applications, and products with commercial possibilities. | Absolute value |

| Eco-design Products (6) | EDPro | Whether the company reports specific products that aim to reuse, recycle, or reduce environmental impacts. | 0 = No; 1 = Yes |

| Brands and Patents (7) | B&P | Represents the net value of brands, patents, and registered trademarks. | Absolute value |

| ROA (8) | ROA | Financial indicator of how profitable a company’s assets are. | Percentage |

| ROE (9) | ROE | Financial indicator of a company’s ability to add value using its own resources. | Percentage |

| Tobin’s Q (10) | TsQ | Indicator with the objective of estimating whether a particular business or market is overvalued or undervalued. | Decimal |

| Sales Per Employee (11) | SPEmp | Ratio of a company’s annual sales and the total number of employees. | Ratio |

| Annual Turnover (12) | AT | Gross sales and other operating income less discounts, returns, and rebates. | Absolute value |

| Employees (13) | Emp | Represents the total number of employees in the company (company dimension). | Absolute value |

| Age (14) | Age | Number of years in operation. | Absolute value |

| Industry Tech Intensity (15) | ITI | Characterization of the technological intensity of the industrial sector. | 1 to 43 |

| Variables | North America | South America | Asia | Africa | Europe | Oceania |

|---|---|---|---|---|---|---|

| R&D (in millions) | 0.56 | 0.03 | 0.27 | −0.01 | 0.22 | 0.01 |

| EDPro (in p.p.) | 5.3 | 0.0 | 4.4 | 0.0 | 6.7 | 7.7 |

| B&P (in millions) | 0.36 | −0.24 | 0.02 | 0.23 | 0.90 | −0.28 |

| ROA (in p.p.) | 0.02 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 |

| ROE (in p.p.) | 1.11 | 0.12 | −0.01 | 0.34 | −0.08 | 0.05 |

| T’sQ (ratio) | 0.37 | 0.44 | 0.02 | 0.14 | 0.00 | 0.29 |

| SPEmp (in thousands) | 0.16 | 0.05 | 0.06 | 0.05 | 1.45 | −0.05 |

| AT (in millions) | 5.94 | 3.52 | 22.68 | 0.35 | 4.06 | −1.21 |

| Emp (absolute value) | 4236 | −11,922 | 17,825 | −12,092 | 5104 | −2395 |

| Variables | N | Min | Max | Mean | S D | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ESG (1) | 743 | 0 | 0.94 | 0.64 | 0.20 | 1 | |||||||||||||

| CSRStr (2) | 743 | 0 | 1.00 | 0.63 | 0.32 | 0.73 *** | 1 | ||||||||||||

| CSRCom (3) | 728 | 0 | 1.00 | 0.78 | 0.41 | 0.61 *** | 0.64 *** | 1 | |||||||||||

| CSRRep (4) | 728 | 0 | 1.00 | 0.88 | 0.33 | 0.62 *** | 0.73 *** | 0.58 *** | 1 | ||||||||||

| R&D (5) | 354 | 0.01 | 29.46 | 1.41 | 2.82 | 0.15 ** | 0.02 | 0.09 | −0.02 | 1 | |||||||||

| EDPro (6) | 710 | 0 | 1.00 | 0.21 | 0.40 | 0.26 *** | 0.16 *** | 0.17 *** | 0.17 *** | 0.13 ** | 1 | ||||||||

| B&P (7) | 269 | −0.01 | 63.58 | 2.35 | 6.27 | 0.14 ** | 0.10 | 0.12 ** | 0.06 | 0.14 * | 0.11 * | 1 | |||||||

| ROA (8) | 743 | −0.18 | 0.44 | 0.08 | 0.07 | 0.00 | −0.04 | 0.01 | −0.02 | 0.14 *** | 0.14 *** | −0.06 | 1 | ||||||

| ROE (9) | 738 | −0.48 | 1.81 | 0.18 | 0.21 | 0.01 | 0.06 | 0.05 | 0.06 | 0.11 ** | 0.04 | −0.01 | 0.46 *** | 1 | |||||

| TsQ (10) | 743 | 0.45 | 20.83 | 2.42 | 2.13 | −0.12 *** | −0.15 *** | −0.13 *** | −0.13 | 0.05 | 0.04 | −0.08 | 0.69 *** | 0.35 *** | 1 | ||||

| SPEmp (11) | 695 | 0.02 | 243.41 | 1.05 | 9.43 | 0.02 | 0.00 | 0.00 | −0.00 | 0.06 | −0.02 | 0.03 | −0.03 | 0.00 | −0.03 | 1 | |||

| AT (12) | 741 | 0.01 | 2297.15 | 53.73 | 146.80 | 0.06 * | 0.04 | 0.07 * | 0.03 | 0.24 *** | 0.03 | 0.14 ** | −0.05 | −0.04 | −0.09 ** | −0.01 | 1 | ||

| Emp (13) | 694 | 2 | 2,200,000 | 78,763 | 127,864 | 0.14 *** | 0.12 *** | 0.13 *** | 0.09 ** | 0.37 *** | 0.03 | 0.08 | −0.06 | 0.01 | −0.12 *** | −0.02 | 0.22 | 1 | |

| Age (14) | 687 | 8 | 353 | 72 | 50 | 0.25 *** | 0.21 *** | 0.18 *** | 0.12 *** | 0.00 | 0.16 *** | 0.12 * | −0.08 ** | 0.03 | −0.16 *** | 0.02 | −0.02 | 0.06 | 1 |

| ITI (15) | 654 | 1 | 4 | 2.12 | 0.95 | 0.07 * | 0.04 | 0.07 * | 0.10 ** | 0.06 | 0.18 *** | −0.13 * | 0.21 *** | 0.08 ** | 0.12 *** | −0.07 * | 0.03 | −0.08 * | −0.04 |

| Model | Predictors | ROA | ROE | Ts’Q | SPEmp | AT |

|---|---|---|---|---|---|---|

| 1 | ESG | 0.106 | −0.013 | 0.154 | 0.228 | 0.599 |

| (0.086) | (0.177) | (0.226) | (0.247) | (0.445) | ||

| CSRStr | −0.164 *** | −0.043 | −0.361 ** | 0.123 | 0.063 | |

| (0.056) | (0.113) | (0.147) | (0.160) | (0.288) | ||

| CSRCom | 0.009 | 0.094 | −0.039 | −0.158 | 0.041 | |

| (0.035) | (0.070) | (0.091) | (0.099) | (0.180) | ||

| CSRRep | 0.062 | 0.079 | 0.062 | −0.003 | −0.183 | |

| (0.053) | (0.111) | (0.139) | (0.151) | (0.273) | ||

| 2 | ESG | 0.031 | −0.296 | 0.001 | 0.135 | 0.084 |

| (0.089) | (0.180) | (0.236) | (0.261) | (0.441) | ||

| CSRStr | −0.155 *** | −0.021 | −0.337 ** | 0.119 | 0.040 | |

| (0.055) | (0.108) | (0.144) | (0.160) | (0.269) | ||

| CSRCom | 0.001 | 0.073 | −0.056 | −0.169 * | −0.012 | |

| (0.034) | (0.067) | (0.090) | (0.099) | (0.168) | ||

| CSRRep | 0.064 | 0.086 | 0.064 | 0.021 | −0.084 | |

| (0.052) | (0.024) | (0.136) | (0.151) | (0.255) | ||

| R&D | 0.006 | 0.024 *** | 0.017 | 0.025 ** | 0.082 *** | |

| (0.004) | (0.009) | (0.011) | (0.013) | (0.021) | ||

| EDPro | 0.050 ** | 0.083 * | 0.100 * | −0.022 | 0.051 | |

| (0.021) | (0.043) | (0.056) | (0.062) | (0.105) | ||

| B&P | −0.001 | −0.004 | −0.005 | 0.001 | 0.009 | |

| (0.001) | (0.002) | (0.003) | (0.003) | (0.006) | ||

| 3 | ESG | 0.006 | −0.321 * | −0.095 | 0.076 | 0.316 |

| (0.088) | (0.181) | (0.216) | (0.260) | (0.394) | ||

| CSRStr | −0.145 *** | −0.010 | −0.287 ** | 0.104 | −0.171 | |

| (0.054) | (0.110 | (0.133) | (0.161) | (0.243) | ||

| CSRCom | 0.011 | 0.088 | −0.016 | −0.144 | −0.017 | |

| (0.033) | (0.068) | (0.083) | (0.099) | (0.150) | ||

| CSRRep | 0.058 | 0.074 | 0.030 | 0.037 | 0.039 | |

| (0.051) | (0.107) | (0.125) | (0.150) | (0.228) | ||

| R&D | 0.010 ** | 0.029 *** | 0.031 *** | 0.036 *** | 0.073 *** | |

| (0.004) | (0.009) | (0.011) | (0.013) | (0.020) | ||

| EDPro | 0.058 *** | 0.093 ** | 0.138 ** | −0.013 | 0.018 | |

| (0.021) | (0.044) | (0.053) | (0.063) | (0.096) | ||

| B&P | −0.002 | −0.004 | −0.005 | −0.001 | 0.004 | |

| (0.001) | (0.002) | (0.003) | (0.004) | (0.005) | ||

| Emp | −0.000 *** | −0.000 | −0.000 *** | −0.000 * | 0.000 *** | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

| Age | −0.000 | 0.000 | −0.001 | 0.000 | 0.000 | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | ||

| ITI | −0.016 | −0.020 | −0.050 | −0.068 * | −0.094 | |

| (0.013) | (0.027) | (0.032) | (0.039) | (0.059) |

| Model | Test | ROA | ROE | T’sQ | SPEmp | AT |

|---|---|---|---|---|---|---|

| 1 | R2 | 0.071 | 0.027 | 0.084 | 0.031 | 0.029 |

| R2 change | 0.071 | 0.027 | 0.084 | 0.031 | 0.029 | |

| Sig F change | 0.064 | 0.533 | 0.031 | 0.438 | 0.476 | |

| 2 | R2 | 0.142 | 0.140 | 0.142 | 0.067 | 0.180 |

| R2 change | 0.071 | 0.113 | 0.058 | 0.011 | 0.151 | |

| Sig F change | 0.025 | 0.003 | 0.055 | 0.220 | 0.000 | |

| 3 | R2 | 0.210 | 0.169 | 0.308 | 0.113 | 0.373 |

| R2 change | 0.068 | 0.029 | 0.167 | 0.047 | 0.193 | |

| Sig F change | 0.024 | 0.292 | 0.000 | 0.122 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Costa, J.; Fonseca, J.P. The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance. Risks 2022, 10, 103. https://doi.org/10.3390/risks10050103

Costa J, Fonseca JP. The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance. Risks. 2022; 10(5):103. https://doi.org/10.3390/risks10050103

Chicago/Turabian StyleCosta, Joana, and José Pedro Fonseca. 2022. "The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance" Risks 10, no. 5: 103. https://doi.org/10.3390/risks10050103

APA StyleCosta, J., & Fonseca, J. P. (2022). The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance. Risks, 10(5), 103. https://doi.org/10.3390/risks10050103