Meta-Learning Approaches for Recovery Rate Prediction

Abstract

:1. Introduction

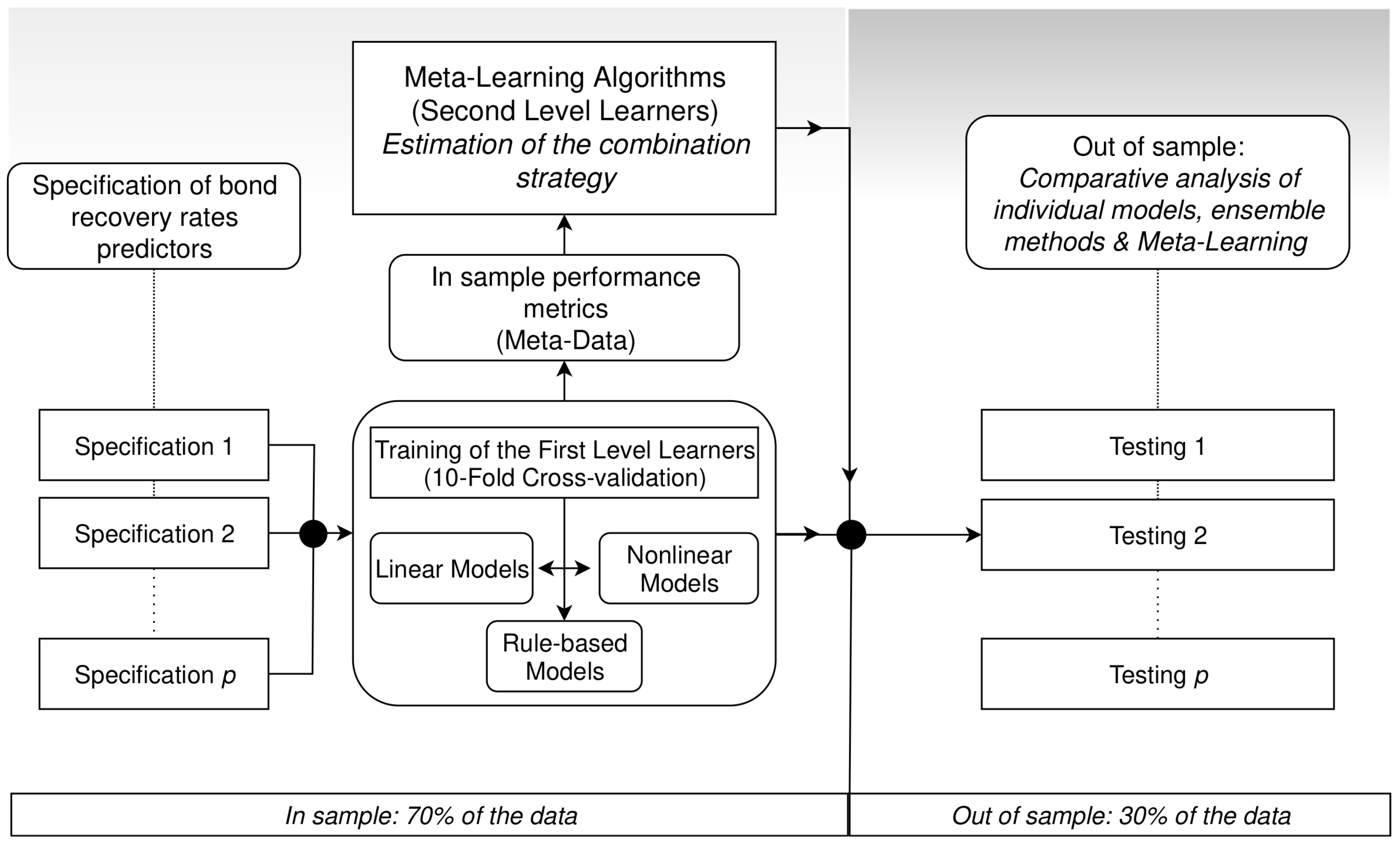

2. Methodology

2.1. First-Level Learners

2.1.1. Linear Models

2.1.2. Nonlinear Models

2.1.3. Rule-Based Models

2.2. Second-Level Learners

2.2.1. Linear Meta-Learners

2.2.2. Nonlinear Meta-Learners

3. Data

3.1. Recovery Rates and Security-Specific Characteristics

3.2. Systematic Factors

4. Results

- (a)

- Statistical approach: the algorithms can access either the full data set of systematic variables or a set created with variable selection techniques. For variable selection, we consider a model based on lasso-selected systematic variables and one based on lasso with stability selection (Meinshausen and Bühlmann 2010). While the latter has been used in Nazemi and Fabozzi (2018) to check the reliability of their lasso-selected macroeconomic variables, those retained by lasso with stability selection have never been used to feed predictive algorithms.11

- (b)

- Economic approach: we create models by relying exclusively on well-identified factors based on the results of Gambetti et al. (2019) and prior studies on recovery rate determinants. Table 10 includes a summary of the model specifications.

4.1. Predictive Models vs. Historical Averages

4.2. Models Based on Systematic Variables

4.3. First-Level Learners

4.4. Meta-Learning: Within and across Predictor Sets

5. Discussion and Practical Considerations

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Details on Nonlinear and Rule-Based Methods

Appendix A.1. Multivariate Adaptive Regression Splines (MARS)

Appendix A.2. K-Nearest Neighbors

Appendix A.3. Model-Averaged Neural Networks

Appendix A.4. Support Vector Regression, Relevance Vector Machine and Gaussian Processes

Appendix A.5. Regression Trees

Appendix A.6. Conditional Inference Trees

Appendix A.7. Bagged Trees and Random Forests

Appendix A.8. Boosted Trees

Appendix A.9. Cubist

Appendix B. A Closer Look at Uncertainty Measures

Appendix C. Economic Data

| Variable | Description | Tcode |

| COUP_RATE | Coupon Rate | 1 |

| BACK_F | Presence of additional backing guarantees | 1 |

| different from the issuer’s assets | ||

| DEF_DEBT_SENR.Senior.Subordinated | Seniority Status | 1 |

| DEF_DEBT_SENR.Senior.Unsecured | Seniority Status | 1 |

| DEF_DEBT_SENR.Subordinated | Seniority Status | 1 |

| MOODYS_11_CODE.Capital.Industries | Industry Code | 1 |

| MOODYS_11_CODE.Consumer.Industries | Industry Code | 1 |

| MOODYS_11_CODE.Energy...Environment | Industry Code | 1 |

| MOODYS_11_CODE.FIRE | Industry Code | 1 |

| MOODYS_11_CODE.Media...Publishing | Industry Code | 1 |

| MOODYS_11_CODE.Retail...Distribution | Industry Code | 1 |

| MOODYS_11_CODE.Technology | Industry Code | 1 |

| MOODYS_11_CODE.Transportation | Industry Code | 1 |

| MOODYS_11_CODE.Utilities | Industry Code | 1 |

| DEF_TYP_CD.Missed.interest.payment | Deafult Type | 1 |

| DEF_TYP_CD.Missed.principal.and.interest.payments | Deafult Type | 1 |

| DEF_TYP_CD.Missed.principal.payment | Deafult Type | 1 |

| DEF_TYP_CD.Others | Deafult Type | 1 |

| DEF_TYP_CD.Prepackaged.Chapter.11 | Deafult Type | 1 |

| DEF_TYP_CD.Receivership | Deafult Type | 1 |

| DEF_TYP_CD.Suspension.of.payments | Deafult Type | 1 |

| FinUnc_h.1 | Financial Uncertainty | 1 |

| Baseline_overall_index | Economic Policy Uncertainty index | 1 |

| News_Based_Policy_Uncert_Index | Newspaper-Based Policy Uncertainty | 1 |

| FedStateLocal_Ex_disagreement | Federal Tax Code Uncertainty | 1 |

| CPI_disagreement | CPI Survey Disagreement | 1 |

| X1..Economic.Policy.Uncertainty | 1. Economic Policy Uncertainty | 1 |

| X2..Monetary.policy | 2. Monetary Policy | 1 |

| Fiscal.Policy..Taxes.OR.Spending. | Fiscal Policy (Taxes OR Spending) | 1 |

| X4..Government.spending | 4. Government spending | 1 |

| X5..Health.care | 5. Healthcare | 1 |

| X6..National.security | 6. National Security | 1 |

| X7..Entitlement.programs | 7. Entitlement Programs | 1 |

| X8..Regulation | 8. Regulation | 1 |

| Financial.Regulation | Financial Regulation | 1 |

| X9..Trade.policy | 9. Trade Policy | 1 |

| X10..Sovereign.debt..currency.crises | 10. Sovereign Debt, Currency Crises | 1 |

| RPI | Real Personal Income | 5 |

| W875RX1 | Real Personal Income excluding | 5 |

| R current transfer receipts | ||

| DPCERA3M086SBEA | Real Personal Consumption Expenditures | 5 |

| CMRMTSPLx | Real Manu. and Trade Industries Sales | 5 |

| RETAILx | Retail and Food Services Sales | 5 |

| IPFINAL | IP: Final Products (Market Group) | 5 |

| IPCONGD | IP: Consumer Goods | 5 |

| IPDCONGD | IP: Durable Consumer Goods | 5 |

| IPNCONGD | IP: Nondurable Consumer Good | 5 |

| IPBUSEQ | IP: Business Equipment | 5 |

| IPMAT | IP: Materials | 5 |

| IPDMAT | IP: Durable Materials | 5 |

| IPNMAT | IP: Nondurable Materials | 5 |

| IPB51222S | IP: Residential Utilities | 5 |

| IPFUELS | IP: Fuels | 5 |

| CUMFNS | Capacity Utilization: Manufacturing | 2 |

| HWI | Help-Wanted Index for U.S. | 2 |

| HWIURATIO | Ratio of Help Wanted/No. Unemployed | 2 |

| CLF16OV | Civilian Labor Force | 5 |

| CE16OV | Civilian Employment | 5 |

| UNRATE | Civilian Unemployment Rate | 2 |

| UEMPMEAN | Average Duration of Unemployment (Weeks) | 2 |

| UEMPLT5 | Civilians Unemployed for Less Than 5 Weeks | 5 |

| UEMP5TO14 | Civilians Unemployed for 5-14 Weeks | 5 |

| UEMP15OV | Civilians Unemployed for 15 Weeks and Over | 5 |

| UEMP15T26 | Civilians Unemployed for 15-26 Weeks | 5 |

| UEMP27OV | Civilians Unemployed for 27 Weeks and Over | 5 |

| CLAIMSx | Initial Claims | 5 |

| PAYEMS | All Employees: Total Nonfarm | 5 |

| CES1021000001 | All Employees: Mining and Logging: Mining | 5 |

| USCONS | All Employees: Construction | 5 |

| DMANEMP | All Employees: Manufacturing | 5 |

| NDMANEMP | All Employees: Nondurable goods | 5 |

| USWTRADE | All Employees: Wholesale Trade | 5 |

| USTRADE | All Employees: Retail Trade | 5 |

| USFIRE | All Employees: Financial Activities | 5 |

| USGOVT | All Employees: Government | 5 |

| CES0600000007 | Avg Weekly Hours: Goods-Producing | 1 |

| AWOTMAN | Avg Weekly Overtime Hours: Manufacturing | 2 |

| M1SL | M1 Money Stock | 6 |

| M2REAL | Real M2 Money Stock | 5 |

| AMBSL | St. Louis Adjusted Monetary Base | 6 |

| TOTRESNS | Total Reserves of Depository Institutions | 6 |

| NONBORRES | Reserves Of Depository Institutions | 7 |

| BUSLOANS | Commercial and Industrial Loans | 6 |

| REALLN | Real Estate Loans at All Commercial Banks | 6 |

| NONREVSL | Total Nonrevolving Credit | 6 |

| CONSPI | Nonrevolving Consumer Credit to Personal Income | 2 |

| S.P..indust | S&P’s Common Stock Price Index: Industrials | 5 |

| S.P.div.yield | S&P’s Composite Common Stock: Dividend Yield | 5 |

| S.P.PE.ratio | S&P’s Composite Common Stock: Price–Earnings Ratio | 5 |

| FEDFUNDS | Effective Federal Funds Rate | 2 |

| CP3Mx | 3-Month AA Financial Commercial Paper Rate | 2 |

| TB3MS | 3-Month Treasury Bill | 2 |

| TB6MS | 6-Month Treasury Bill | 2 |

| GS1 | 1-Year Treasury Rate | 2 |

| GS5 | 5-Year Treasury Rate | 2 |

| AAA | Moody’s Seasoned Aaa Corporate Bond Yield | 2 |

| BAA | Moody’s Seasoned Baa Corporate Bond Yield | 2 |

| COMPAPFFx | 3-Month Commercial Paper Minus FEDFUNDS | 1 |

| TB3SMFFM | 3-Month Treasury C Minus FEDFUNDS | 1 |

| TB6SMFFM | 6-Month Treasury C Minus FEDFUNDS | 1 |

| T1YFFM | 1-Year Treasury C Minus FEDFUNDS | 1 |

| T10YFFM | 10-Year Treasury C Minus FEDFUNDS | 1 |

| AAAFFM | Moody’s Aaa Corporate Bond Minus FEDFUNDS | 1 |

| BAAFFM | Moody’s Baa Corporate Bond Minus FEDFUNDS | 1 |

| TWEXMMTH | Trade Weighted U.S. Dollar Index: Major Currencies, Goods | 5 |

| EXSZUSx | Switzerland/U.S. Foreign Exchange Rate | 5 |

| EXJPUSx | Japan/U.S. Foreign Exchange Rate | 5 |

| EXUSUKx | U.S./U.K. Foreign Exchange Rate | 5 |

| EXCAUSx | Canada/U.S. Foreign Exchange Rate | 5 |

| WPSFD49207 | PPI: Finished Goods | 6 |

| WPSID62 | PPI: Crude Materials | 6 |

| OILPRICEx | Crude Oil, Spliced WTI and Cushing | 6 |

| PPICMM | PPI: Metals and Metal Products | 6 |

| CPIAPPSL | CPI: Apparel | 6 |

| CPIMEDSL | CPI: Medical Care | 6 |

| CUSR0000SAD | CPI: Durables | 6 |

| CUSR0000SAS | CPI: Services | 6 |

| DDURRG3M086SBEA | Personal Cons. Exp: Durable Goods | 6 |

| DNDGRG3M086SBEA | Personal Cons. Exp: Nondurable Goods | 6 |

| DSERRG3M086SBEA | Personal Cons. Exp: Services | 6 |

| CES0600000008 | Avg Hourly Earnings: Goods-Producing | 6 |

| CES2000000008 | Avg Hourly Earnings: Construction | 6 |

| CES3000000008 | Avg Hourly Earnings: Manufacturing | 6 |

| UMCSENTx | Consumer Sentiment Index | 2 |

| MZMSL | MZM Money Stock | 6 |

| DTCOLNVHFNM | Consumer Motor Vehicle Loans Outstanding | 6 |

| DTCTHFNM | Total Consumer Loans and Leases Outstanding | 6 |

| INVEST | Securities in Bank Credit at All Commercial Banks | 6 |

| DelRate.ConsumerLoans | Delinquency Rates on Consumer Loans | 1 |

| DelRate.CreditCardLoans | Delinquency Rates on Credit Card Loans | 1 |

| DelRate.CommIndLoans | Delinquency Rates on Commercial and Industrial Loans | 1 |

| AMR.Def.Rate | American Default Rate | 1 |

| D_log.DIV. | CRSP - Dividends * | 5 |

| D_Preinvested | CRSP - Price Under Reinvestment * | 5 |

| d.p | CRSP - Dividend to Price * | 5 |

| R15.R11 | FF Factor (Small, High) Minus (Small, Low) | 1 |

| Sorted On (size, Book-to-Market) | ||

| CP.factor | FF Factor - Cash Profitability | 1 |

| SMB | FF Factor - Small - Big | 1 |

| UMD | FF Factor - Momentum | 1 |

| Agric | Portfolio Return | 1 |

| Food | Portfolio Return | 1 |

| Beer & Liquor | Portfolio Return | 1 |

| Smoke | Portfolio Return | 1 |

| Toys - Recreation | Portfolio Return | 1 |

| Fun - Entertaiment | Portfolio Return | 1 |

| Books - Printing and Publishing | Portfolio Return | 1 |

| Hshld - Consumer Goods | Portfolio Return | 1 |

| Clths - Apparel | Portfolio Return | 1 |

| MedEq - Medical Equipment | Portfolio Return | 1 |

| Drugs - Pharmaceutical Products | Portfolio Return | 1 |

| Chems - Chemicals | Portfolio Return | 1 |

| Rubbr - Rubber and Plastic Products | Portfolio Return | 1 |

| Txtls - Textiles | Portfolio Return | 1 |

| BldMt - Construction Materials | Portfolio Return | 1 |

| Construction | Portfolio Return | 1 |

| Steel | Portfolio Return | 1 |

| Machinery | Portfolio Return | 1 |

| Electrical Equipment | Portfolio Return | 1 |

| Autos - Automobiles and Trucks | Portfolio Return | 1 |

| Aero - Aircraft | Portfolio Return | 1 |

| Ships | Portfolio Return | 1 |

| Mines - Non-Metallic and Industrial Metal Mining | Portfolio Return | 1 |

| Coal | Portfolio Return | 1 |

| Oil | Portfolio Return | 1 |

| Util - Utilities | Portfolio Return | 1 |

| Telcm - Communication | Portfolio Return | 1 |

| PerSv - Personal Services | Portfolio Return | 1 |

| BusSv - Business Services | Portfolio Return | 1 |

| Hardw - Computers | Portfolio Return | 1 |

| Chips - Electronic Equipment | Portfolio Return | 1 |

| LabEq - Measuring and Control Equipment | Portfolio Return | 1 |

| Paper - Business Supplies | Portfolio Return | 1 |

| Boxes - Transportation | Portfolio Return | 1 |

| Trans - Transportation | Portfolio Return | 1 |

| Whlsl - Wholesale | Portfolio Return | 1 |

| Rtail - Retail | Portfolio Return | 1 |

| Meals - Restaurants, Hotels, Motels | Portfolio Return | 1 |

| Banks - Banking | Portfolio Return | 1 |

| Insur - Insurance | Portfolio Return | 1 |

| RlEst - Real Estate | Portfolio Return | 1 |

| Fin - Trading | Portfolio Return | 1 |

| Other | Portfolio Return | 1 |

| A032RC1A027NBEA | National Income | 5 |

| HOUSTNE | Housing Starts, Northeast | 4 |

| HOUSTW | Housing Starts, West | 4 |

| ACOGNO | New Orders for Consumer Goods | 5 |

| AMDMNOx | New Orders for Durable Goods | 5 |

| ANDENOx | New Orders for Nondefense Capital Goods | 5 |

| AMDMUOx | Unfilled Orders for Durable Goods | 5 |

| BUSINVx | Total Business Inventories | 5 |

| ISRATIOx | Total Business: Inventories to Sales Ratio | 2 |

| 1 | We define model risk from three perspectives: (i) maximum average loss across model specifications and model classes, (ii) average loss and (iii) its variability within each model class. |

| 2 | A weak learner is any machine learning algorithm that provides an accuracy slightly better than random guessing. |

| 3 | Models based on economic principles approximate the latter using industry default rates, loan delinquency rates, market and industrial production returns and recession indicators (Altman et al. 2005; Gambetti et al. 2019; Jankowitsch et al. 2014; Mora 2015). |

| 4 | Hyperparameters for first-level learners are tuned using 10-fold cross-validation in the training sample. Folds are created using stratified sampling based on seniority type, as in Nazemi et al. (2017), Nazemi and Fabozzi (2018) and Nazemi et al. (2018). The same applies for generating the training and test sets, with proportions of and . |

| 5 | Forecast selection outperforms the forecast combination only in very specific situations that are typically not encountered in practice: for instance, when the variance of the prediction errors of one model is lower than those of the others by several orders of magnitude, see, e.g., Roccazzella et al. (2021). |

| 6 | Another strategy consists of using an additional validation fold (Wolpert 1992). This has the drawback of extending the original data with potentially informative observations that would unevenly boost the performance of meta-learning techniques with respect to those of individual models and ensemble methods. In this paper, we empirically show that combining schemes that do not rely on additional sample splitting perform remarkably well compared to the a posterior best predictive framework. This is surprising especially for combination schemes whose weights are estimated using the same in sample information. |

| 7 | For further details on the COS methodology and for the explicit formula to estimate the optimal shrinkage intensity, we refer to Roccazzella et al. (2021). |

| 8 | For example, Dodge and Karam (2016) documents that deep learning methods are particularly sensitive to noise levels in image classification tasks. |

| 9 | We refer to Appendix C for the full list of the variables and the transformations performed on the raw data. |

| 10 | The reader can refer to Appendix B for more details and to Gambetti et al. (2019) for a detailed literature review on the topic. |

| 11 | We apply lasso with stability selection based on the R implementation stabs by Hofner and Hothorn (2017). We determine the dimension of bootstrapped lasso models using pointwise control (Meinshausen and Bühlmann 2010). Moreover, we specify a threshold of 0.6 for the selection probability as in Nazemi and Fabozzi (2018). |

| 12 | The MCS tests whether a subset of methods enters jointly in the superior set of models by repeatedly testing the null hypothesis of equal predictive performance with significance level . Let be the set of all forecasting models (both individual candidates and forecasts combinations), and let be the superior set of models. Formally, the MCS tests . If the null hypothesis is rejected, then the procedure eliminates the model with the greatest relative loss from the set . This procedure is sequentially repeated until the null hypothesis is not rejected at the chosen probability level . We compute the MCS p-values via bootstrapping (10,000 replications) and using the Oxford MFE Toolbox publicly available at https://www.kevinsheppard.com/code/matlab/mfe-toolbox/ (accessed on 28 April 2022). |

| 13 | We find our list of selected variables to be largely consistent with those highlighted in Nazemi and Fabozzi (2018). A table of predictor probabilities is included in the Appendix C. |

| 14 | We find this conclusion to be robust to different specifications of the nonlinear meta-learner’s architecture (i.e., the number of hidden units in the artificial neural networks). The results are available upon request. |

References

- Acharya, Viral V., Sreedhar T. Bharath, and Anand Srinivasan. 2007. Does industry-wide distress affect defaulted firms? Evidence from creditor recoveries. Journal of Financial Economics 85: 787–821. [Google Scholar] [CrossRef]

- Alexopoulos, Michelle, and Jon Cohen. 2015. The power of print: Uncertainty shocks, markets, and the economy. International Review of Economics & Finance 40: 8–28. [Google Scholar]

- Altman, Edward, Brooks Brady, Andrea Resti, and Andrea Sironi. 2005. The link between default and recovery rates: Theory, empirical evidence, and implications. The Journal of Business 78: 2203–27. [Google Scholar] [CrossRef]

- Altman, Edward I., and Egon A. Kalotay. 2014. Ultimate recovery mixtures. Journal of Banking & Finance 40: 116–129. [Google Scholar]

- Altman, Edward I., and Brenda Karlin. 2009. The re-emergence of distressed exchanges in corporate restructurings. Journal of Credit Risk 5: 43–56. [Google Scholar] [CrossRef]

- Altman, Edward I., and Vellore M. Kishore. 1996. Almost everything you wanted to know about recoveries on defaulted bonds. Financial Analysts Journal 52: 57–64. [Google Scholar] [CrossRef]

- Andersen, Leif, and Jakob Sidenius. 2004. Extensions to the Gaussian copula: Random recovery and random factor loadings. Journal of Credit Risk 1: 29–70. [Google Scholar] [CrossRef]

- Atiya, Amir F. 2020. Why does forecast combination work so well? International Journal of Forecasting 36: 197–200. [Google Scholar] [CrossRef]

- Bachmann, Rüdiger, Steffen Elstner, and Eric R. Sims. 2013. Uncertainty and economic activity: Evidence from business survey data. American Economic Journal: Macroeconomics 5: 217–49. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring Economic Policy Uncertainty. The Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision (BCBS). 2006. Basel II: International Convergence of Capital Measurement and Capital Standards: A Revised Framework—Comprehensive Version. Available online: https://www.bis.org/publ/bcbs128.pdf (accessed on 28 April 2022).

- Basel Committee on Banking Supervision (BCBS). 2011. Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems—Revised Version June 2011. Available online: https://www.bis.org/publ/bcbs189.pdf (accessed on 28 April 2022).

- Basel Committee on Banking Supervision (BCBS). 2017. Basel III: Finalising Post-Crisis Reforms. Available online: https://www.bis.org/bcbs/publ/d424.pdf (accessed on 28 April 2022).

- Bastos, João. 2014. Ensemble predictions of recovery rates. Journal of Financial Services Research 46: 177–93. [Google Scholar] [CrossRef]

- Bekaert, Geert, Marie Hoerova, and Marco Lo Duca. 2013. Risk, uncertainty and monetary policy. Journal of Monetary Economics 60: 771–88. [Google Scholar] [CrossRef]

- Bellotti, Anthony, Damiano Brigo, Paolo Gambetti, and Frédéric Vrins. 2021. Forecasting recovery rates on non-performing loans with machine learning. International Journal of Forecasting 37: 428–44. [Google Scholar] [CrossRef]

- Berd, Arthur. 2005. Recovery swaps. Journal of Credit Risk 1: 61–70. [Google Scholar] [CrossRef]

- Betz, Jennifer, Ralf Kellner, and Daniel Rösch. 2018. Systematic effects among loss given defaults and their implications on downturn estimation. European Journal of Operational Research 271: 1113–44. [Google Scholar] [CrossRef]

- Betz, Jennifer, Steffen Krüger, Ralf Kellner, and Daniel Rösch. 2020. Macroeconomic effects and frailties in the resolution of non-performing loans. Journal of Banking & Finance 112: 105212. [Google Scholar]

- Bloom, Nicholas. 2009. The impact of uncertainty shocks. Econometrica 77: 623–85. [Google Scholar]

- Breiman, Leo. 1996. Bagging predictors. Machine Learning 24: 123–40. [Google Scholar] [CrossRef]

- Breiman, Leo. 2001. Random forests. Machine Learning 45: 5–32. [Google Scholar] [CrossRef]

- Breiman, Leo, Jerome Friedman, Richard Olshen, and Charles Stone. 1984. Classification and Regression Trees. Monterey: Wadsworth and Brooks. [Google Scholar]

- Bris, Arturo, Ivo Welch, and Ning Zhu. 2006. The costs of bankruptcy: Chapter 7 liquidation versus chapter 11 reorganization. The Journal of Finance 61: 1253–303. [Google Scholar] [CrossRef]

- Bruche, Max, and Carlos González-Aguado. 2010. Recovery rates, default probabilities and the credit cycle. Journal of Banking & Finance 34: 754–64. [Google Scholar]

- Caputo, Barbara, Kim Lan Sim, Fredrik Furesjo, and Alexander J. Smola. 2002. Appearance-based object recognition using SVMs: Which kernel should I use? Paper presented at the NIPS Workshop on Statistical Methods for Computational Experiments in Visual Processing and Computer Vision, Vancouver, BC, Canada, 3–8 December 2001. [Google Scholar]

- Caruana, Rich, Alexandru Niculescu-Mizil, Geoff Crew, and Alex Ksikes. 2004. Ensemble selection from libraries of models. Paper presented at the Twenty-First International Conference on Machine Learning, ICML ’04, New York, NY, USA, July 4–8; New York: Association for Computing Machinery, p. 18. [Google Scholar]

- Claeskens, Gerda, Jan R. Magnus, Andrey L. Vasnev, and Wendun Wang. 2016. The forecast combination puzzle: A simple theoretical explanation. International Journal of Forecasting 32: 754–62. [Google Scholar] [CrossRef]

- Davydenko, Sergei A., and Julian R. Franks. 2008. Do bankruptcy codes matter? a study of defaults in france, germany, and the UK. Journal of Finance 63: 565–608. [Google Scholar] [CrossRef]

- Dodge, Samuel, and Lina Karam. 2016. Understanding how image quality affects deep neural networks. Paper presented at the 2016 Eighth International Conference on Quality of Multimedia Experience (QoMEX), Lisbon, Portugal, June 6–7; pp. 1–6. [Google Scholar]

- Dong, Xi, Li Yan, David E. Rapach, and Guofu Zhou. 2020. Anomalies and the expected market return. The Journal of Finance 77: 639–81. [Google Scholar] [CrossRef]

- ECB. 2009. Uncertainty and the economic prospects for the euro area. ECB Economic Bulletin, August. 58–61. [Google Scholar]

- ECB. 2016. The impact of uncertainty on activity in the euro area. ECB Economic Bulletin, August. 55–74. [Google Scholar]

- François, Pascal. 2019. The determinants of market-implied recovery rates. Risks 7: 57. [Google Scholar] [CrossRef]

- Franks, Julian R., and Walter N. Torous. 1994. A comparison of financial recontracting in distressed exchanges and Chapter 11 reorganizations. Journal of Financial Economics 35: 349–70. [Google Scholar] [CrossRef]

- Friedman, Jerome, Trevor Hastie, Rob Tibshirani, Narasimhan Balasubramanian, and Simon Noah. 2019. Glmnet: Lasso and Elastic-Net Regularized Generalized Linear Models. R Package Version 3.0-2. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Friedman, Jerome H. 1991. Multivariate adaptive regression splines. The Annals of Statistics 19: 1–67. [Google Scholar] [CrossRef]

- Gambetti, Paolo, Geneviève Gauthier, and Frédéric Vrins. 2018. Stochastic recovery rate: Impact of pricing measure’s choice and financial consequences on single-name products. In New Methods in Fixed Income Analysis. Edited by Mehdi Mili, Reyes Samaniego Medina and Filippo Di Pietro. Cham: Springer, pp. 181–203. [Google Scholar]

- Gambetti, Paolo, Geneviève Gauthier, and Frédéric Vrins. 2019. Recovery rates: Uncertainty certainly matters. Journal of Banking & Finance 106: 371–83. [Google Scholar]

- Gieseck, Arne, and Yannis Largent. 2016. The impact of macroeconomic uncertainty on activity in the euro area. Review of Economics 67: 25–52. [Google Scholar] [CrossRef]

- Granger, Clive W. J., and Ramu Ramanathan. 1984. Improved methods of combining forecasts. Journal of Forecasting 3: 197–204. [Google Scholar] [CrossRef]

- Greenwell, Brandon, Bradley Boehmke, Jay Cunningham, and Gbm Developers. 2018. GBM: Generalized Boosted Regression Models. R Package Version 2.1.4. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Gregory, Jon. 2012. Counterparty Credit Risk and Credit Value Adjustment: A Continuing Challenge for Global Financial Markets. Hoboken: Wiley. [Google Scholar]

- Hansen, Peter R., Asger Lunde, and James M. Nason. 2011. The model confidence set. Econometrica 79: 453–97. [Google Scholar] [CrossRef]

- Hartmann-Wendels, Thomas, Patrick Miller, and Eugen Töws. 2014. Loss given default for leasing: Parametric and nonparametric estimations. Journal of Banking & Finance 40: 364–375. [Google Scholar]

- Hastie, Trevor, Robert Tibshirani, and Jerome Friedman. 2009. The Elements of Statistical Learning. New York: Springer. [Google Scholar]

- Hofner, Benjamin, and Torsten Hothorn. 2017. Stabs: Stability Selection with Error Control. R Package Version 0.6-3. Vienna, Austria: R Foundation for Statistical Computing. [Google Scholar]

- Hornik, Kurt, Maxwell Stinchcombe, and Halbert White. 1989. Multilayer feedforward networks are universal approximators. Neural Networks 2: 359–366. [Google Scholar] [CrossRef]

- Hothorn, Torsten, Kurt Hornik, and Achim Zeileis. 2006. Unbiased recursive partitioning: A conditional inference framework. Journal of Computational and Graphical Statistics 15: 651–74. [Google Scholar] [CrossRef]

- Jankowitsch, Rainer, Florian Nagler, and Marti G. Subrahmanyam. 2014. The determinants of recovery rates in the US corporate bond market. Journal of Financial Economics 114: 155–77. [Google Scholar] [CrossRef]

- Jurado, Kyle, Sydney C. Ludvigson, and Serena Ng. 2015. Measuring uncertainty. American Economic Review 105: 1177–216. [Google Scholar] [CrossRef]

- Karatzoglou, Alexandros, Alex Smola, Kurt Hornik, and Achim Zeileis. 2004. Kernlab—An S4 package for kernel methods in R. Journal of Statistical Software 11: 1–20. [Google Scholar] [CrossRef]

- Koch, Gregory, Richard Zemel, and Ruslan Salakhutdinov. 2015. Siamese Neural Networks for One-Shot Image Recognition. Paper presented at the 32nd International Conference on Machine Learning, Lille, France, July 6–11; vol. 37. [Google Scholar]

- Kose, M. A., and M. Terrones. 2012. How does uncertainty affect economic performance? IMF World Economic Outlook, October. 49–53. [Google Scholar]

- Kuhn, Max, and Ross Quinlan. 2018. Cubist: Rule- And Instance-Based Regression Modeling. R Package Version 0.2.2. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Ledoit, Olivier, and Michael Wolf. 2004. Honey, i shrunk the sample covariance matrix. The Journal of Portfolio Management 30: 110–19. [Google Scholar] [CrossRef]

- Lessmann, Stefan, Bart Baesens, Hsin-Vonn Seow, and Lyn C. Thomas. 2015. Benchmarking state-of-the-art classification algorithms for credit scoring: An update of research. European Journal of Operational Research 247: 124–36. [Google Scholar] [CrossRef]

- Liaw, Andy, and Matthew Wiener. 2002. Classification and regression by randomforest. R News 2: 18–22. [Google Scholar]

- Liu, Jiaming, Sicheng Zhang, and Haoyue Fan. 2022. A two-stage hybrid credit risk prediction model based on xgboost and graph-based deep neural network. Expert Systems with Applications 195: 116624. [Google Scholar] [CrossRef]

- Loterman, Gert, Iain Brown, David Martens, Christophe Mues, and Bart Baesens. 2012. Benchmarking regression algorithms for loss given default modeling. International Journal of Forecasting 28: 161–70. [Google Scholar] [CrossRef]

- Ludvigson, Sydney C., Sai Ma, and Serena Ng. 2019. Uncertainty and business cycles: Exogenous impulse or endogenous response? American Economic Journal: Macroeconomics 13: 369–410. [Google Scholar]

- Lumley, Thomas. 2017. Leaps: Regression Subset Selection. R Package Version 3.0. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- McCracken, Michael W., and Serena Ng. 2015. FRED-MD: A Monthly Database for Macroeconomic Research. Working Paper 2015-12. St. Louis: Federal Reserve Bank of St. Louis. [Google Scholar]

- Meinshausen, Nicolai. 2017. quantregForest: Quantile Regression Forests. R Package Version 1.3-7. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Meinshausen, Nicolai, and Peter Bühlmann. 2010. Stability selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 72: 417–73. [Google Scholar] [CrossRef]

- Milborrow, Stephen. 2018. Earth: Multivariate Adaptive Regression Splines. R Package Version 4.6.3. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Mora, Nada. 2015. Creditor recovery: The macroeconomic dependence of industry equilibrium. Journal of Financial Stability 18: 172–86. [Google Scholar] [CrossRef]

- Nazemi, Abdolreza, and Frank J. Fabozzi. 2018. Macroeconomic variable selection for creditor recovery rates. Journal of Banking & Finance 89: 14–25. [Google Scholar]

- Nazemi, Abdolreza, Farnoosh Fatemi Pour, Konstantin Heidenreich, and Frank J. Fabozzi. 2017. Fuzzy decision fusion approach for loss-given-default modeling. European Journal of Operational Research 262: 780–91. [Google Scholar] [CrossRef]

- Nazemi, Abdolreza, Konstantin Heidenreich, and Frank J. Fabozzi. 2018. Improving corporate bond recovery rate prediction using multi-factor support vector regressions. European Journal of Operational Research 271: 664–75. [Google Scholar] [CrossRef]

- Pykthin, Michael. 2003. Unexpected recovery risk. Risk 16: 74–78. [Google Scholar]

- Qi, Min, and Xinlei Zhao. 2011. Comparison of modeling methods for loss given default. Journal of Banking & Finance 35: 2842–855. [Google Scholar]

- Quinlan, J. Ross. 1993. Combining instance-based and model-based learning. Paper presented at the Tenth International Conference on International Conference on Machine Learning, ICML’93, Amherst, MA, USA, July 27–29; San Francisco: Morgan Kaufmann Publishers Inc., pp. 236–43. [Google Scholar]

- Quinlan, Ross. 1992. Learning with continuous classes. Paper presented at the 5th Australian Joint Conference on Artificial Intelligence, Hobart, Tasmania, November 16–18. [Google Scholar]

- R Core Team. 2017. R: A Language and Environment for Statistical Computing. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Ravi, Sachin, and Hugo Larochelle. 2017. Optimization as a model for few-shot learning. Paper presented at 5th International Conference on Learning Representations, Toulon, France, April 24–26. [Google Scholar]

- Ripley, Brian D. 1996. Pattern Recognition and Neural Networks. Cambridge: Cambridge University Press. [Google Scholar]

- Ripley, Brian D., and William N. Venables. 2016. Nnet: Feed-Forward Neural Networks and Multinomial Log-Linear Models. R Package Version 7.3-12. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Roccazzella, Francesco, Paolo Gambetti, and Frédéric Vrins. 2021. Optimal and robust combination of forecasts via constrained optimization and shrinkage. International Journal of Forecasting 38: 97–116. [Google Scholar] [CrossRef]

- Santoro, Adam, Sergey Bartunov, Matthew Botvinick, Daan Wierstra, and Timothy Lillicrap. 2016. Meta-learning with memory-augmented neural networks. Paper presented at 33rd International Conference on Machine Learning, New York, NY, USA, June 19–24; vol. 48, pp. 1842–50. [Google Scholar]

- Santos, Andrey Bicalho, Arnaldo de Albuquerque Araújo, Jefersson A. dos Santos, William Robson Schwartz, and David Menotti. 2017. Combination techniques for hyperspectral image interpretation. Paper presented at the IEEE International Geoscience and Remote Sensing Symposium (IGARSS), Fort Worth, TX, USA, July 23–28; pp. 3648–51. [Google Scholar]

- Schuermann, Til. 2004. What do we know about loss given default? In Wharton Financial Institutions Center Working Paper. Working Paper No. 04-01. Philadelphia: The University of Pennsylvania’s Wharton Financial Institutions Center. [Google Scholar]

- Therneau, Terry, Beth Atkinson, and Brian Ripley. 2017. rpart: Recursive Partitioning and Regression Trees. R Package Version 4.1-11. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Tipping, Michael E. 2001. Sparse Bayesian learning and the relevance vector machine. Journal of Machine Learning Research 1: 211–44. [Google Scholar]

- Tobback, Ellen, David Martens, Tony Van Gestel, and Bart Baesens. 2014. Forecasting loss given default models: Impact of account characteristics and the macroeconomic state. Journal of the Operational Research Society 65: 376–92. [Google Scholar] [CrossRef]

- Vapnik, Vladimir N. 1995. The Nature of Statistical Learning Theory. New York: Springer. [Google Scholar]

- Wang, Tianhui, Renjing Liu, and Guohua Qi. 2022. Multi-classification assessment of bank personal credit risk based on multi-source information fusion. Expert Systems with Applications 191: 116236. [Google Scholar] [CrossRef]

- Wang, Zhu. 2018. bst: Gradient Boosting. R Package Version 0.3-15. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Westfall, Peter H., and S. Stanley Young. 1993. Resampling-Based Multiple Testing: Examples and Methods for p-Value Adjustment. Wiley Series in Probability and Statistics; Hoboken: Wiley. [Google Scholar]

- Williams, Christopher K. I., and Carl Edward Rasmussen. 1996. Gaussian processes for regression. In Advances in Neural Information Processing Systems 8. Cambridge: MIT Press, pp. 514–20. [Google Scholar]

- Wolpert, David H. 1992. Stacked generalization. Neural Networks 5: 241–59. [Google Scholar] [CrossRef]

- Yao, Xiao, Jonathan Crook, and Galina Andreeva. 2015. Support vector regression for loss given default modelling. European Journal of Operational Research 240: 528–38. [Google Scholar] [CrossRef]

- Zarnowitz, Victor, and Louis A. Lambros. 1987. Consensus and uncertainty in economic prediction. Journal of Political Economy 95: 591–621. [Google Scholar] [CrossRef]

- Zhang, Jie, and Lyn C. Thomas. 2012. Comparisons of linear regression and survival analysis using single and mixture distributions approaches in modelling LGD. International Journal of Forecasting 28: 204–15. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Acronym | R Algorithm | Reference |

|---|---|---|---|

| Linear regression | lm | lm | R Core Team (2017) |

| Backward step-wise selection | lm_bs | leaps | Lumley (2017) |

| Ridge regression | ridge | glmnet | Friedman et al. (2019) |

| Lasso regression | Lasso | glmnet | ″ |

| Elastic net regression | elnet | glmnet | ″ |

| MARS | mars | earth | Milborrow (2018) |

| Bagged MARS | bmars | earth | ″ |

| Model-averaged neural networks | avnnet | nnet | Ripley and Venables (2016) |

| Support vector regression | svr | ksvr | Karatzoglou et al. (2004) |

| Relevance vector regression | rvm | rvm | ″ |

| Gaussian processes | gauss | gausspr | ″ |

| Regression trees | cart | rpart | Therneau et al. (2017) |

| Conditional inference trees | cit | ctree | Hothorn et al. (2006) |

| Boosted tree | bst | bst | Wang (2018) |

| Stochastic gradient boosting | gbm | gbm | Greenwell et al. (2018) |

| Random forests | rf | randomForest | Liaw and Wiener (2002) |

| Quantile random forests | qrf | quantregForest | Meinshausen (2017) |

| Cubist | cubist | cubist | Kuhn and Quinlan (2018) |

| N | Min. | 1st Qu. | Median | Mean | 3rd Qu. | Max. | St. Dev. | |

|---|---|---|---|---|---|---|---|---|

| Recovery rate | 768 | 0.01% | 10.00% | 20.00% | 30.98% | 51.41% | 118.00% | 27.58% |

| Debt Seniority | N | Median | Mean | St. Dev. | Skewness |

|---|---|---|---|---|---|

| Senior Secured | 85 | 63.00% | 60.92% | 32.27% | |

| Senior Unsecured | 533 | 19.00% | 28.03% | 23.90% | |

| Senior Subordinated | 129 | 19.13% | 25.77% | 26.87% | |

| Subordinated | 21 | 9.13% | 16.71% | 23.37% |

| Industrial Sector | N | Median | Mean | St. Dev. | Skewness |

|---|---|---|---|---|---|

| Banking | 18 | 18.00% | 23.47% | 24.44% | |

| Capital Industries | 189 | 29.00% | 36.44% | 28.55% | |

| Consumer Industries | 88 | 30.25% | 39.86% | 28.68% | |

| Energy & Environment | 45 | 40.00% | 44.10% | 25.76% | |

| FIRE | 166 | 10.00% | 11.95% | 10.32% | |

| Media & Publishing | 90 | 43.62% | 40.72% | 31.45% | |

| Retail & Distribution | 32 | 36.25% | 34.92% | 25.89% | |

| Technology | 72 | 15.00% | 19.89% | 16.99% | |

| Transportation | 57 | 22.25% | 31.32% | 23.81% | |

| Utilities | 11 | 92.50% | 91.89% | 6.54% |

| Default Type | N | Median | Mean | St. Dev. | Skewness |

|---|---|---|---|---|---|

| Chapter 11 | 371 | 10.50% | 25.68% | 25.97% | |

| Missed interest payment | 281 | 28.50% | 37.55% | 26.76% | |

| Missed principal and interest payments | 14 | 58.12% | 56.14% | 18.85% | |

| Missed principal payment | 8 | 23.04% | 29.76% | 29.12% | |

| Others | 6 | 11.00% | 15.59% | 17.47% | |

| Prepackaged Chapter 11 | 71 | 12.00% | 31.95% | 33.01% | |

| Receivership | 7 | 0.50% | 4.57% | 9.70% | |

| Suspension of payments | 10 | 18.50% | 30.05% | 26.75% |

| Coupon | – | – | – | – | ≥ |

|---|---|---|---|---|---|

| Average RR | 14.82% | 24.22% | 23.01% | 33.11% | 36.95% |

| Maturity (Years) | – | – | – | – | ≥ |

|---|---|---|---|---|---|

| Average RR | 43.30% | 37.88% | 31.92% | 19.39% | 18.90% |

| Backing | Yes | No |

|---|---|---|

| Average RR | 40.02% | 29.33% |

| Name | Type | Methodology | References |

|---|---|---|---|

| Inflation uncertainty | Survey-based | Dispersion of forecasts from the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters. | Zarnowitz and Lambros (1987) Bachmann et al. (2013) Baker et al. (2016) |

| Federal/State/Local expenditures uncertainty | |||

| Economic policy uncertainty | News-based | Normalized volume of newspaper articles published in a given month containing expressions referring to specific types of economic uncertainty. | Baker et al. (2016) Alexopoulos and Cohen (2015) |

| Monetary policy uncertainty | |||

| Fiscal policy (taxes or spending) uncertainty | |||

| Tax uncertainty | |||

| Government spending uncertainty | |||

| Healthcare uncertainty | |||

| National security uncertainty | |||

| Entitlement programs uncertainty | |||

| Regulation uncertainty | |||

| Financial regulation uncertainty | |||

| Trade policy uncertainty | |||

| Sovereign debt, currency crises uncertainty | |||

| VIX | Volatility-based (Stock market) | Stock market implied volatility index from the Chicago Board Options Exchange. | Bloom (2009) Bekaert et al. (2013) |

| Financial uncertainty | Volatility-based (Forecast error) | Conditional volatility of the purely unforecastable prediction error of financial time series. | Jurado et al. (2015) Ludvigson et al. (2019) |

| Specification ID | Systematic Variables | Reference |

|---|---|---|

| 1 | Full data set | - |

| 2 | Lasso-selected macroeconomic variables | Nazemi and Fabozzi (2018) |

| 3 | Lasso-selected variables with stability control | - |

| 4 | Industry default rate, commercial and industrial loans delinquency rates, industrial production, market index returns, PMI | in Gambetti et al. (2019) |

| 5 | As in 4, with financial uncertainty substituted with industry default rates | in ″ |

| 6 | As in 4, with VIX substituted with industry default rates | in ″ |

| 7 | As in 4, plus financial uncertainty, news-based economic policy uncertainty, inflation uncertainty and federal/state/local expenditures uncertainty | in ″ |

| 8 | As in 4, plus all uncertainty measures of Table 9 | - |

| 9 | No systematic variables | in ″ Nazemi and Fabozzi (2018) Nazemi et al. (2018) |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | Mean | |

|---|---|---|---|---|---|---|---|---|---|---|

| Linear Models | 0.291 | 0.204 | 0.211 | 0.211 | 0.211 | 0.210 | 0.212 | 0.213 | 0.236 | 0.222 |

| Lin. regression | 0.774 | 0.206 | 0.205 | 0.206 | 0.206 | 0.206 | 0.206 | 0.209 | 0.233 | 0.272 |

| Lin. reg. back. sel. | 0.221 | 0.205 | 0.205 | 0.207 | 0.207 | 0.206 | 0.209 | 0.214 | 0.235 | 0.212 |

| Lasso 1 | 0.203 | 0.203 | 0.206 | 0.207 | 0.207 | 0.207 | 0.208 | 0.209 | 0.233 | 0.209 |

| Lasso 2 | 0.218 | 0.203 | 0.221 | 0.221 | 0.220 | 0.218 | 0.220 | 0.221 | 0.241 | 0.220 |

| Ridge 1 | 0.202 | 0.203 | 0.208 | 0.207 | 0.207 | 0.207 | 0.208 | 0.209 | 0.233 | 0.209 |

| Ridge 2 | 0.222 | 0.211 | 0.226 | 0.220 | 0.221 | 0.220 | 0.222 | 0.223 | 0.242 | 0.223 |

| Elastic net | 0.201 | 0.202 | 0.206 | 0.207 | 0.208 | 0.207 | 0.209 | 0.209 | 0.233 | 0.209 |

| Nonlinear Models | 0.211 | 0.203 | 0.207 | 0.206 | 0.211 | 0.208 | 0.207 | 0.213 | 0.237 | 0.211 |

| MARS | 0.207 | 0.199 | 0.214 | 0.197 | 0.202 | 0.198 | 0.194 | 0.216 | 0.237 | 0.207 |

| Gaussian processes | 0.211 | 0.204 | 0.205 | 0.207 | 0.207 | 0.208 | 0.207 | 0.211 | 0.234 | 0.210 |

| RVM | 0.236 | 0.212 | 0.200 | 0.207 | 0.223 | 0.214 | 0.216 | 0.212 | 0.230 | 0.217 |

| SVM | 0.191 | 0.197 | 0.212 | 0.212 | 0.212 | 0.212 | 0.211 | 0.213 | 0.245 | 0.212 |

| Rule-based Models | 0.232 | 0.225 | 0.233 | 0.216 | 0.217 | 0.213 | 0.221 | 0.216 | 0.240 | 0.224 |

| Regression tree | 0.230 | 0.223 | 0.244 | 0.218 | 0.215 | 0.215 | 0.222 | 0.211 | 0.256 | 0.226 |

| Conditional inference tree | 0.234 | 0.226 | 0.222 | 0.214 | 0.219 | 0.211 | 0.220 | 0.221 | 0.225 | 0.221 |

| Nonlinear Ensembles | 0.195 | 0.197 | 0.197 | 0.196 | 0.200 | 0.200 | 0.206 | 0.206 | 0.235 | 0.203 |

| Neural networks | 0.202 | 0.201 | 0.202 | 0.199 | 0.204 | 0.207 | 0.209 | 0.208 | 0.238 | 0.208 |

| Bagged MARS | 0.189 | 0.194 | 0.191 | 0.193 | 0.195 | 0.193 | 0.203 | 0.204 | 0.233 | 0.199 |

| Rule-based Ensembles | 0.189 | 0.191 | 0.186 | 0.186 | 0.187 | 0.185 | 0.183 | 0.185 | 0.229 | 0.191 |

| Cubist | 0.184 | 0.182 | 0.184 | 0.187 | 0.194 | 0.186 | 0.188 | 0.183 | 0.229 | 0.191 |

| Boosted trees s.g.b. | 0.194 | 0.198 | 0.195 | 0.189 | 0.187 | 0.188 | 0.189 | 0.187 | 0.238 | 0.196 |

| Boosted trees | 0.182 | 0.191 | 0.174 | 0.177 | 0.185 | 0.179 | 0.177 | 0.182 | 0.223 | 0.185 |

| Quantile random forests | 0.193 | 0.195 | 0.192 | 0.192 | 0.185 | 0.187 | 0.180 | 0.187 | 0.236 | 0.194 |

| Random forests | 0.190 | 0.187 | 0.187 | 0.185 | 0.185 | 0.187 | 0.182 | 0.184 | 0.220 | 0.190 |

| Linear Meta-Learning | 0.187 | 0.191 | 0.180 | 0.185 | 0.179 | 0.184 | 0.179 | 0.179 | 0.228 | 0.188 |

| Opt | 0.188 | 0.193 | 0.181 | 0.183 | 0.180 | 0.182 | 0.177 | 0.181 | 0.227 | 0.188 |

| Opt+ | 0.187 | 0.191 | 0.180 | 0.186 | 0.179 | 0.184 | 0.180 | 0.178 | 0.228 | 0.188 |

| COS-E | 0.187 | 0.191 | 0.180 | 0.186 | 0.179 | 0.184 | 0.180 | 0.178 | 0.228 | 0.188 |

| COS-IL | 0.187 | 0.191 | 0.180 | 0.186 | 0.179 | 0.184 | 0.180 | 0.178 | 0.228 | 0.188 |

| Equally weighted for. | 0.186 | 0.187 | 0.188 | 0.187 | 0.188 | 0.188 | 0.187 | 0.188 | 0.224 | 0.192 |

| Hill climbing | 0.193 | 0.195 | 0.180 | 0.189 | 0.178 | 0.188 | 0.189 | 0.187 | 0.225 | 0.192 |

| NonLinear Meta-Learning | 0.224 | 0.200 | 0.194 | 0.194 | 0.192 | 0.191 | 0.195 | 0.213 | 0.247 | 0.205 |

| NN - 1 | 0.241 | 0.198 | 0.193 | 0.187 | 0.187 | 0.180 | 0.189 | 0.234 | 0.241 | 0.205 |

| NN - 2 | 0.208 | 0.203 | 0.195 | 0.201 | 0.196 | 0.201 | 0.201 | 0.192 | 0.253 | 0.206 |

| Variable | Selection Probability |

|---|---|

| Financial Uncertainty | |

| Consumer Price Index for All Urban Consumers: Apparel | |

| New One-Family Houses Sold: United States | |

| Industrial Production: Fuels | |

| Number Unemployed for 5–14 Weeks | |

| Continued Claims (Insured Unemployment) | |

| ISM Manufacturing: Supplier Deliveries Index | |

| Securities in Bank Credit, All Commercial Banks | |

| Industry Returns: Agricultural | |

| Money Zero Maturity: Money Stock | |

| Total Consumer Loans and Leases Owned and Securitized by Finance Companies | |

| Industrial Production: Residential Utilities | |

| Employment Cost Index: Benefits: Private Industry Workers | |

| Reserves of Depository Institutions, Nonborrowed | |

| Number Unemployed for Less than 5 Weeks | |

| Total Borrowings of Depository Institutions from the Federal Reserve | |

| Gross Saving | |

| Economic Policy Uncertainty: Government Spending | |

| M1 Money Stock | |

| Light Weight Vehicle Sales: Autos and Light Trucks | |

| Industry Portfolio Returns: Other | |

| Economic Policy Uncertainty: Sovereign Debt Currency Crises | |

| Fama-French Factor: Momentum | |

| All Employees, Government | |

| Civilian Employment Level | |

| Change in Private Inventories | |

| Industry Portfolio Returns: Drugs | |

| Nonperforming Commercial Loans | |

| Industry Portfolio Returns: Smoke | |

| CBOE NASDAQ 100 Volatility Index | |

| Consumer Sentiment Index | |

| Economic Policy Uncertainty: Trade policy | |

| Consumer Price Index for All Urban Consumers: Medical Care | |

| Industrial Production: Nondurable Consumer Goods | |

| National Income | |

| Number Unemployed for 15–26 Weeks | |

| Civilian Labor Force Level | |

| University of Michigan: Inflation Expectation | |

| Corporate Profits after Tax with IVA and CCAdj: Net Dividends | |

| Industrial Production: Materials | |

| Excess Reserves of Depository Institutions |

| Model | Specification | RMSE | MAE | MCS | |

|---|---|---|---|---|---|

| Boosted trees | 7 | 0.1735 | 0.1076 | 0.6298 | *** |

| Opt+ | . | 0.1752 | 0.1041 | 0.6175 | *** |

| COS-E | . | 0.1752 | 0.1041 | 0.6175 | *** |

| COS-IL | . | 0.1752 | 0.1041 | 0.6175 | *** |

| Boosted trees | 3 | 0.1765 | 0.1123 | 0.6142 | *** |

| Boosted trees | 6 | 0.1771 | 0.1140 | 0.6115 | *** |

| Boosted trees | 4 | 0.1789 | 0.1118 | 0.6048 | *** |

| Quantile random forests | 3 | 0.1796 | 0.0963 | 0.6080 | *** |

| Boosted trees | 2 | 0.1819 | 0.1117 | 0.5920 | *** |

| Random forests | 3 | 0.1820 | 0.1140 | 0.5927 | *** |

| Boosted trees | 9 | 0.1823 | 0.1140 | 0.5886 | |

| Cubist | 8 | 0.1824 | 0.1053 | 0.5878 | |

| Cubist | 2 | 0.1831 | 0.1053 | 0.5858 | |

| Cubist | 7 | 0.1836 | 0.1076 | 0.5841 | |

| Cubist | 9 | 0.1836 | 0.1029 | 0.5843 | |

| Random forests | 2 | 0.1842 | 0.1136 | 0.5818 | |

| Opt | . | 0.1843 | 0.1078 | 0.5852 | |

| Boosted trees | 5 | 0.1845 | 0.1205 | 0.5781 | |

| Random forests | 6 | 0.1849 | 0.1164 | 0.5869 | |

| Quantile random forests | 5 | 0.1853 | 0.0964 | 0.5887 | |

| Equally weighted for. | . | 0.1862 | 0.1289 | 0.5962 | |

| Hill climbing | . | 0.1890 | 0.1213 | 0.5622 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gambetti, P.; Roccazzella, F.; Vrins, F. Meta-Learning Approaches for Recovery Rate Prediction. Risks 2022, 10, 124. https://doi.org/10.3390/risks10060124

Gambetti P, Roccazzella F, Vrins F. Meta-Learning Approaches for Recovery Rate Prediction. Risks. 2022; 10(6):124. https://doi.org/10.3390/risks10060124

Chicago/Turabian StyleGambetti, Paolo, Francesco Roccazzella, and Frédéric Vrins. 2022. "Meta-Learning Approaches for Recovery Rate Prediction" Risks 10, no. 6: 124. https://doi.org/10.3390/risks10060124

APA StyleGambetti, P., Roccazzella, F., & Vrins, F. (2022). Meta-Learning Approaches for Recovery Rate Prediction. Risks, 10(6), 124. https://doi.org/10.3390/risks10060124