Overview of Some Recent Results of Energy Market Modeling and Clean Energy Vision in Canada

Abstract

:1. A Brief Introduction

Literature Review

2. Closed-Form Option Pricing Formula for a Mean-Reverting Asset on the Energy Market (Swishchuk 2008)

Numerical Example (AECO Natural GAS Index (1 May 1998–30 April 1999))

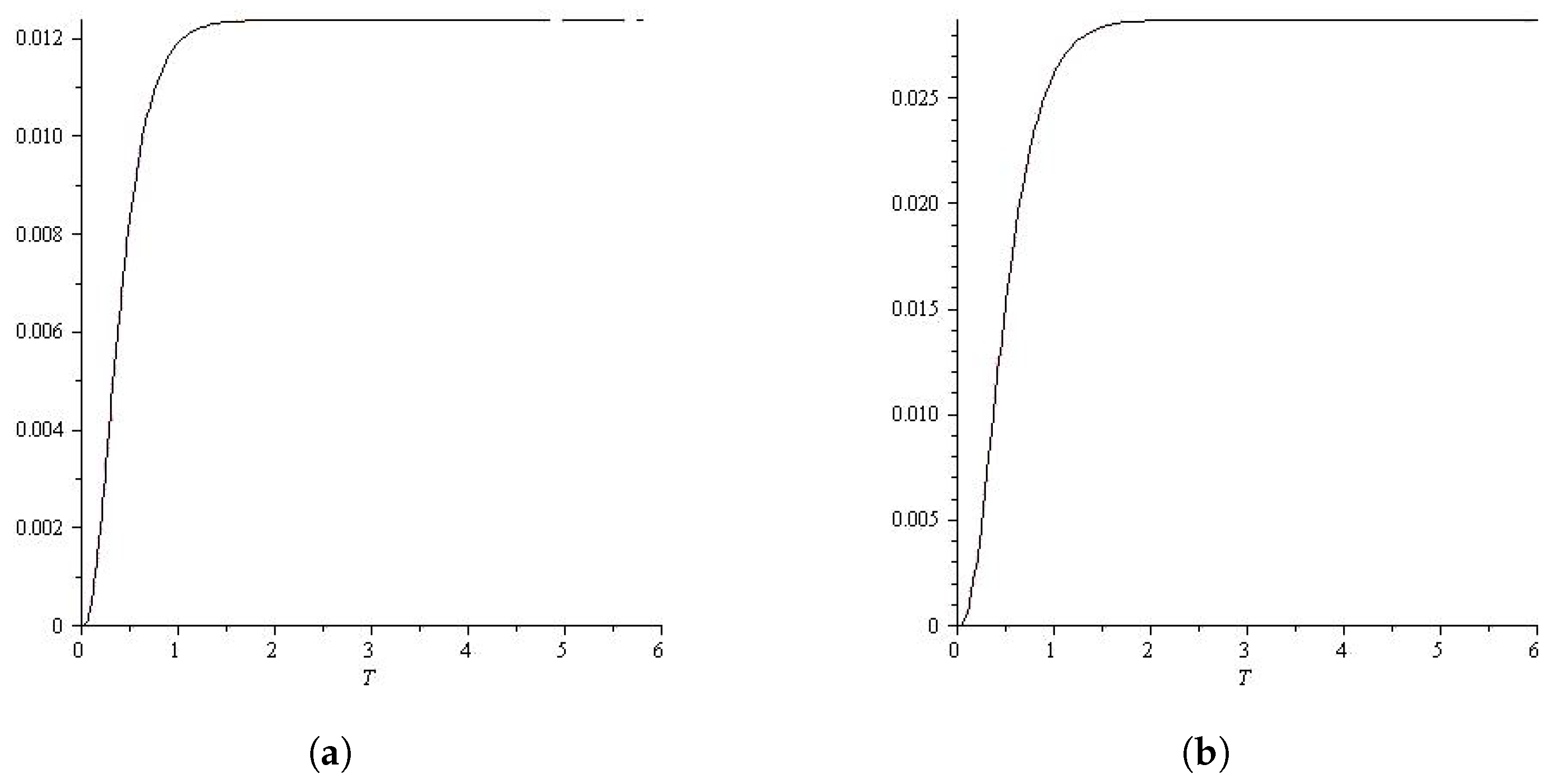

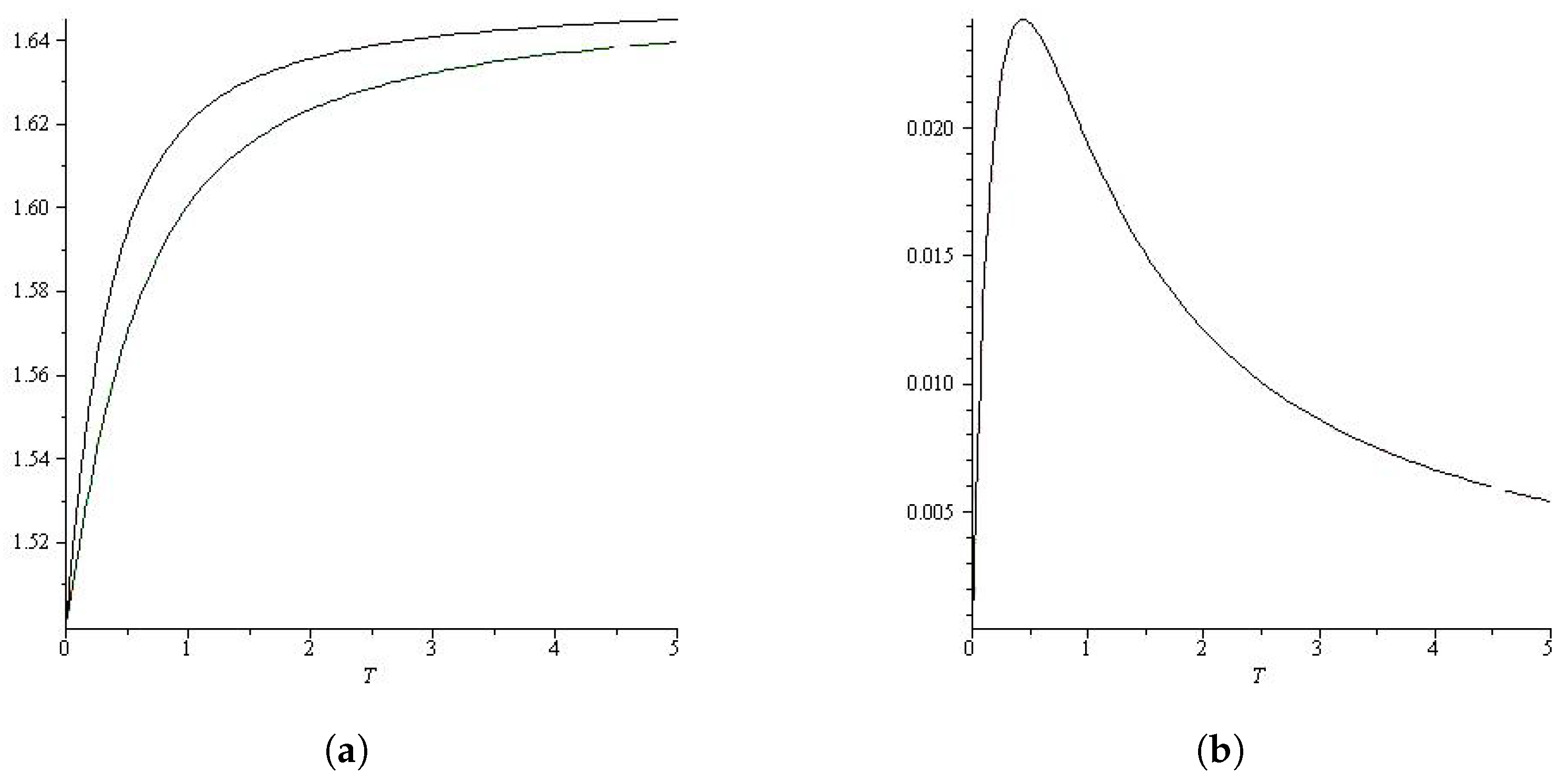

3. Variance and Volatility Swaps on Energy Markets (Swishchuk 2013a, 2013b)

Numerical Example (AECO Natural Gas Index for the Period 1 May 1998 to 30 April 1999)

4. Weather Derivatives on Energy Markets (Swishchuk and Cui 2013 and Cui and Swishchuk 2015)

- (a)

- In a static hedge, the number of hedging contracts is not changed over the course of the hedge in response to any movement in the values of the hedging instrument or the hedged asset.

- (b)

- In a dynamic hedge, on the other hand, more hedging contracts are bought or sold to bring back the hedge ratio to the target hedge ratio.

- and annual seasonal volatility;

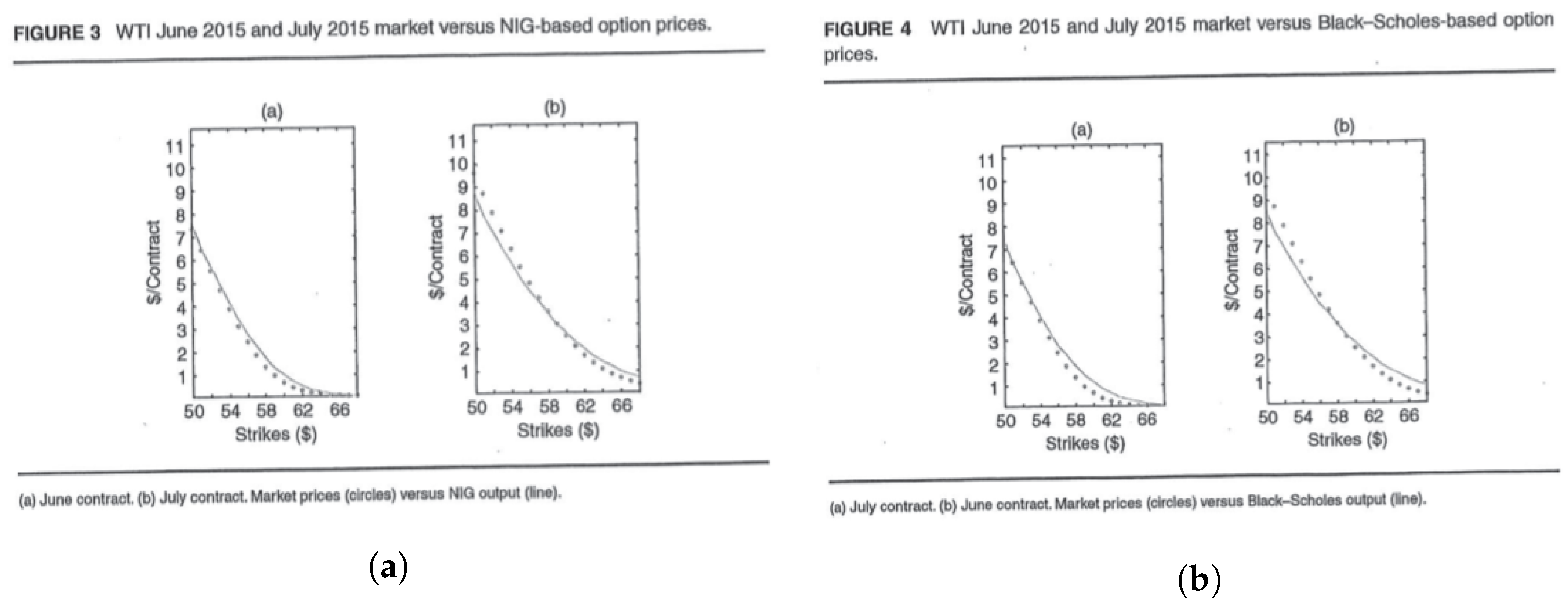

5. Pricing Crude Oil Options Using Lévy Processes (Shahmoradi and Swishchuk 2016)

- Merton’s Jump diffusion model (JDM) (see Merton 1976):where Brownian motion and Poisson process are independent, .

- Normal inverse Gaussian (NIG) model:where is the drift under Q measure,is an NIG process, and is the inverse Gaussian process. The NIG process has three parameters, tail-heaviness skewness , and scale .

- Variance gamma (VG) model:where is a VG process such that:and is a gamma process with parameter

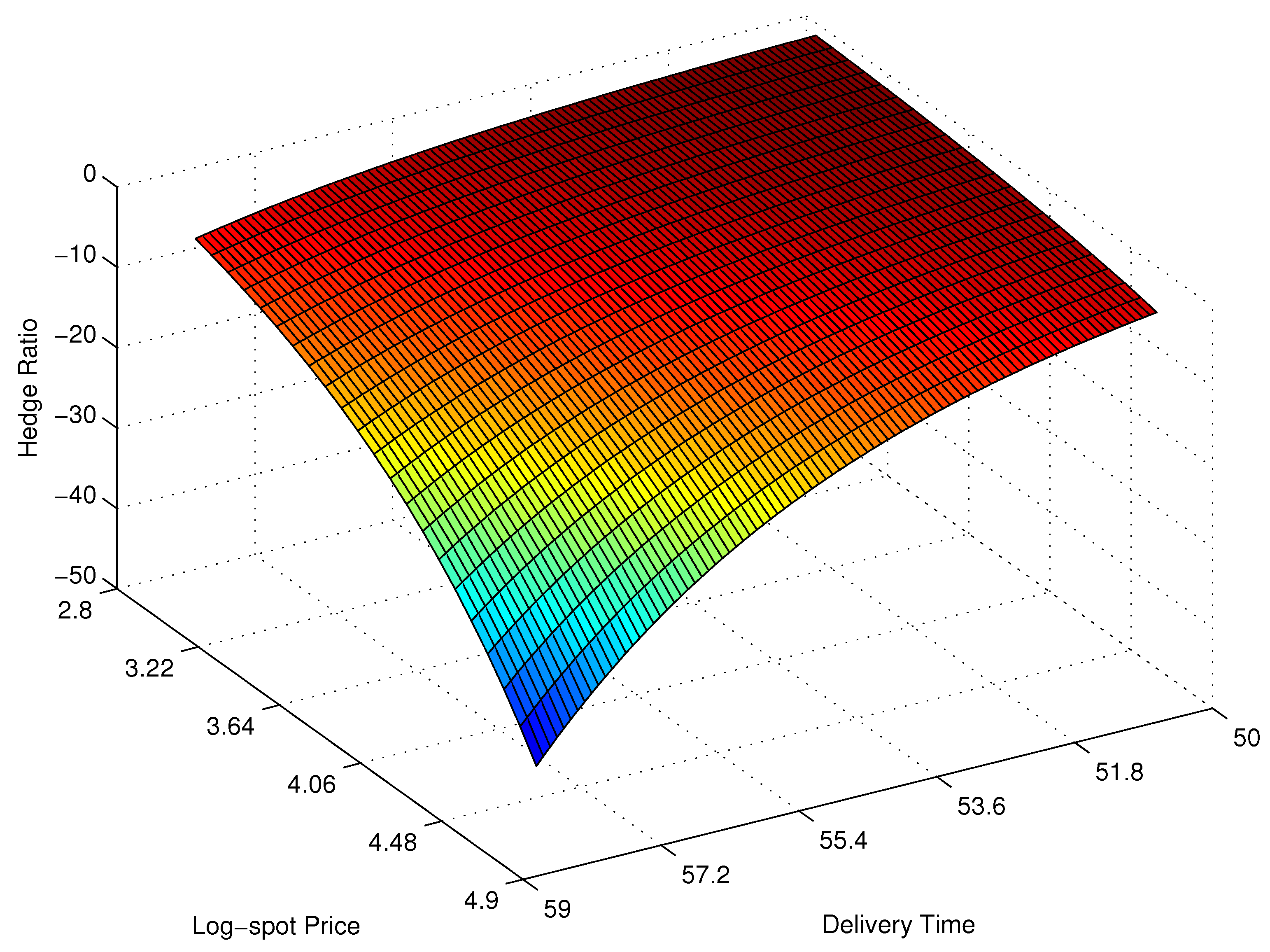

6. Energy Market Contracts with Delayed and Jumped Volatilities (Swishchuk 2020b)

- The increments are independent r.v. for any partition and ;

- It is continuous in probability, that is, for every and :

Numerical Example: Henry Hub Natural Gas Daily Spot Prices (1997–2011)

7. Mean-Reverting Processes in Alberta Energy Markets Modeling (Lu et al. 2021)

- Introduced a fuel-switching price to the Alberta market, which is designed for encouraging power plant companies to switch from coal to natural gas when they produce electricity, which has been successfully applied to the European market;

- Considered an energy-switching price which considers power switch from natural gas to wind;

- Modeled these two prices using five mean reverting processes including a regime-switching processes, Lévy-driven Ornstein–Uhlenbeck process, and inhomogeneous geometric Brownian motion, and estimate them based on multiple procedures such as the maximum likelihood estimation and expectation–maximization algorithm;

- Proved previous results applied to the Albertan market, where the jump modeling technique is needed when modeling fuel-switching data;

- Explained the necessity of introducing regime-switching models to the fuel-switching data by showing that the regime-switching model is better fitted to the data.

- Inhomogeneous geometric Brownian motion (IGBM):where is a standard Brownian motion.

- OU process (OU):where is a standard Brownian motion.

- Lévy-driven OU process (LDOU):where is a Lévy process.

- Regime-switching OU process (RSOU)where is a continuous-time finite-state Markov chain, and is a bounded function of z.

- Regime-switching Lévy-driven OU process (RSLDOU):

- (1)

- Conclude that the RSOU process and OU process are the best models for fuel-switching price and energy-switching price, respectively;

- (2)

- See that for the fuel-switching price, the regime-switching model largely increases the goodness of fit compared to other models, which indicates the important property of regime-switching for this price.

- (3)

- Conclude that jump modeling techniques are also important, as they increase the performance of the OU process, and this finding is similar to the previous results from North American and European markets.

8. Alternatives to Black-76 Model for Options Valuations of Futures Contracts (Swishchuk et al. 2021; Swishchuk 2020a)

- Take data (prices) and sketch their behavior, i.e., their evolution in time;

9. A Vision to Transition to 100% Wind, Water, and Solar Energy in Canada (TheSolutionsProject 2023)

- –

- Onshore wind: ;

- –

- Offshore wind: ;

- –

- Hydroelectric: ;

- –

- Concentrated solar plants: ;

- –

- Commercial & government rooftop solar: ;

- –

- Solar plants: ;

- –

- Residential rooftop solar: ;

- –

- Wave devices: ;

- –

- Geothermal: ;

- –

- Tidal turbines: .

- –

- Construction jobs: 315,138

- –

- Operation jobs: 367,889

- –

- Avoided health costs per year: B CAD (3.94% of the country’s GDP);

- –

- Lives lost to air pollution that could be saved each year: 9884.

- –

- Footprint Area:

- –

- Spacing Area:

- –

- Fossil Fuels & Nuclear Energy:

- –

- Wind, Water & Solar:

- –

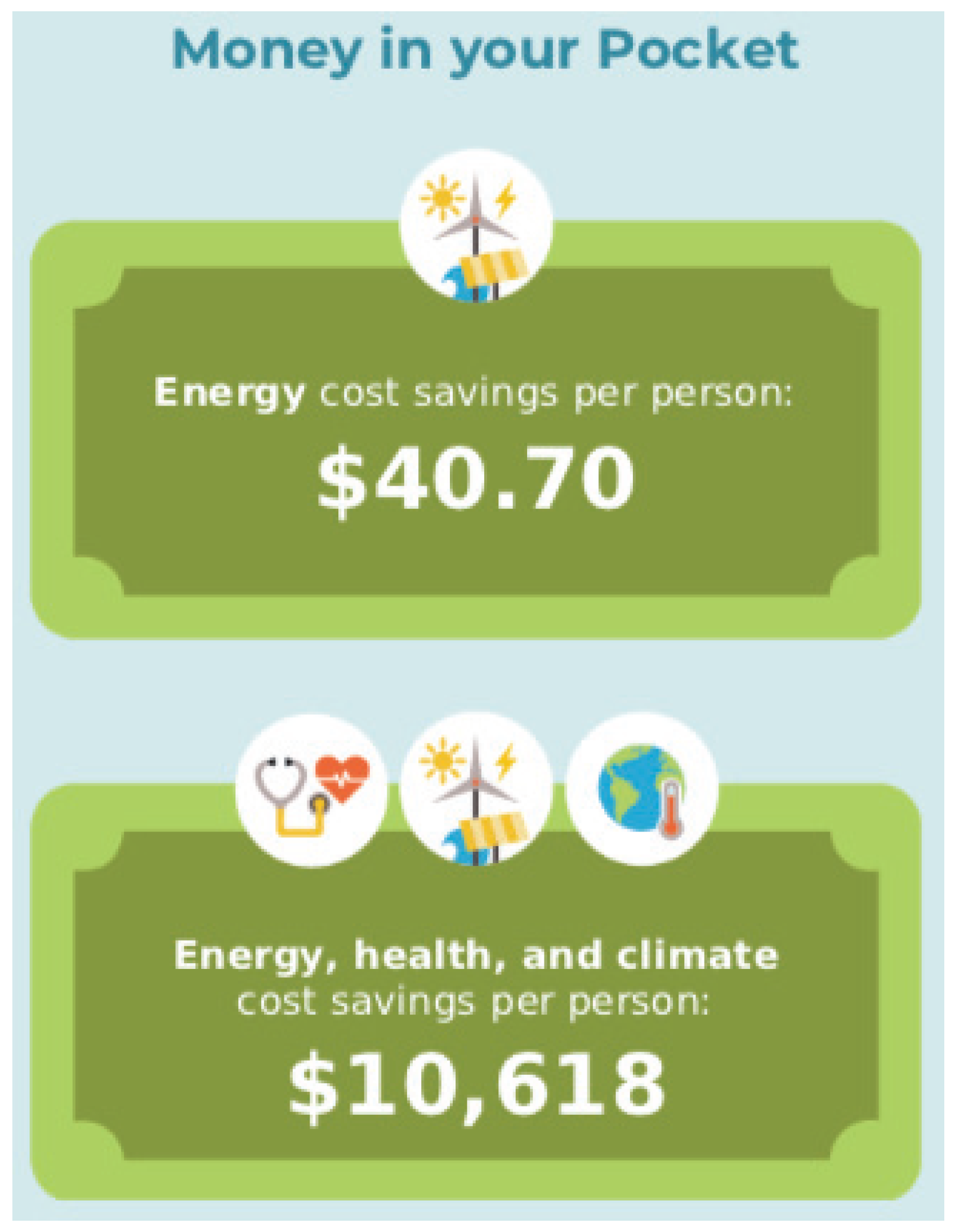

- Energy cost savings per person: CAD;

- –

- Energy, health, and climate cost savings per person: CAD

10. Wind and Solar Energy in Alberta (Dunn 2021)

11. Energy Transition Center in Calgary, AB, Canada (Witzel 2022)

12. Conclusions and Future Work

13. Discussion

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| MDPI | Multidisciplinary Digital Publishing Institute |

| DOAJ | Directory of open access journals |

| TLA | Three-letter acronym |

| LD | Linear dichroism |

References

- Anderson, Drew. 2022. The Narwhal: Guess What? Alberta Is on Track to Meet Its 2030 Renewable Energy Goal Ahead of Schedule. December. Available online: https://thenarwhal.ca/alberta-renewable-energy-2030/ (accessed on 23 May 2023).

- Askari, Hossein, and Noureddine Krichene. 2008. Oil Price Dynamics. Energy Economics 30: 2134–53. [Google Scholar] [CrossRef]

- Bachelier, L. 1900. Theorie de la Speculation. Ph.D. thesis, Sorbonne University, Paris, France. [Google Scholar]

- Benth, Fred Espen, and Jūratė Šaltytė-Benth. 2005. Stochastic Modelling of Temperature Variations with a View Towards Weather Derivatives. Applied Mathematical Finance 12: 53–85. [Google Scholar] [CrossRef]

- Benth, Fred Espen, Jūratė Šaltytė Benth, and Steen Koekebakker. 2008a. Stochastic Modelling of Electricity and Related Markets. Singapore: World Scientific. [Google Scholar]

- Benth, Fred Espen, Jūratė Šaltytė Benth, and Steen Koekebakker. 2008b. Stochastic Modelling of Electricity and Related Markets. Number 11 in Advanced Series on Statistical Science & Applied Probability. Singapore: World Scientific. [Google Scholar]

- Black, Fischer. 1976. The pricing of commodity contracts. Journal of Financial Economics 3: 167–79. [Google Scholar] [CrossRef]

- Black, Fischer, and Myron Scholes. 1973. The Pricing of Options and Corporate Liabilities. The Journal of Political Economy 81: 637–57. [Google Scholar]

- Borowski, Piotr F. 2020. Zonal and Nodal Models of Energy Market in European Union. Energies 13: 4182. [Google Scholar] [CrossRef]

- Bos, Len, Antony Ware, and Boris Pavlov. 2002. On a semi-spectral method for pricing an option on a mean-reverting asset. Quantitative Finance 2: 337–45. [Google Scholar] [CrossRef]

- Broadie, Mark, and Ashish Jain. 2008. Pricing and Hedging Volatility Derivatives. The Journal of Derivatives 15: 7–24. [Google Scholar] [CrossRef] [Green Version]

- Brockhaus, Oliver, and Douglas Long. 2000. Volatility swaps made simple. Risk-London Magazine Limited 13: 92–95. [Google Scholar]

- Carr, Peter, and Dilip Madan. 1998. Towards a Theory of Volatility Trading. In Volatility: New Estimation Techniques for Pricing Derivatives, 7th ed. Edited by Robert A. Jarrow. London: Risk Books. [Google Scholar]

- Considine, Geoffrey. 2000. Introduction to Weather Derivaties. Aquila Energy, 1–10. [Google Scholar]

- Crosby, John. 2008. A multi-factor jump-diffusion model for commodities. Quantitative Finance 8: 181–200. [Google Scholar] [CrossRef] [Green Version]

- Cui, Kaijie, and Anatoliy Swishchuk. 2015. Applications of weather derivatives in the energy market. The Journal of Energy Markets 8: 59–76. [Google Scholar] [CrossRef]

- De Brito, Marcelle Caroline Thimotheo, Amaro O. Pereira Junior, Mario Veiga Ferraz Pereira, Julio César Cahuano Simba, and Sergio Granville. 2022. Competitive Behavior of Hydroelectric Power Plants under Uncertainty in Spot Market. Energies 15: 7336. [Google Scholar] [CrossRef]

- Diewvilai, Radhanon, and Kulyos Audomvongseree. 2022. Possible Pathways toward Carbon Neutrality in Thailand’s Electricity Sector by 2050 through the Introduction of H2 Blending in Natural Gas and Solar PV with BESS. Energies 15: 3979. [Google Scholar] [CrossRef]

- Dornier, Fred, and Mark Queruel. 2000. Caution to the Wind. Energy and Power Risk Management 13: 30–32. [Google Scholar]

- Dunn, Carolyn. 2021. CBC News: How Canada’s Largest Solar Farm is Changing Alberta’s Landscape. November. Available online: https://www.cbc.ca/news/canada/calgary/travers-solar-project-vulcan-1.6233629 (accessed on 23 May 2023).

- Ellen, Jovin. 1998. Advances on the Weather Front (An Overview of the U.S. Weather Derivatives Market, Global Energy Risk). Electrical World 212: S6. [Google Scholar]

- Hamisultane, Hélène. 2006. Extracting Information from the Market to Price the Weather Derivatives. Available online: https://shs.hal.science/halshs-00079192/document (accessed on 23 June 2023).

- Hull, John C. 1997. Option, Futures, and Other Derivatives. Hoboken: Prentice Hall. [Google Scholar]

- Ikeda, Nobuyuki, and Shinzo Watanabe. 1981. Stochastic Differential Equations and Diffusion Processes. Tokyo: Kodansha Ltd. [Google Scholar]

- Ismail, Firas B., Maisarah Mazwan, Hussein Al-Faiz, Marayati Marsadek, Hasril Hasini, Ammar Al-Bazi, and Young Zaidey Yang Ghazali. 2022. An Offline and Online Approach to the OLTC Condition Monitoring: A Review. Energies 15: 6435. [Google Scholar] [CrossRef]

- Kaminski, Vincent. 1998. Pricing Weather Derivatives (Global Energy Risk). Electrical World 212: S6. [Google Scholar]

- Kazmerchuk, Yuriy, Anatoliy Swishchuk, and Jianhong Wu. 2005. A Continuous-time GARCH model for stochastic volatility with delay. The Canadian Applied Mathematics Quarterly 13: 123–49. [Google Scholar]

- Lu, Weiliang, Alexis Arrigoni, Anatoliy Swishchuk, and Stéphane Goutte. 2021. Modelling of Fuel- and Energy-Switching Prices by Mean-Reverting Processes and Their Applications to Alberta Energy Markets. Mathematics 9: 709. [Google Scholar] [CrossRef]

- Madan, Dilip, and Eugene Seneta. 1990. The Variance Gamma (V.G.) Model for Share Market Returns. The Journal of Business 63: 511–24. [Google Scholar] [CrossRef]

- Mallala, Balasubbareddy, Venkata Prasad Papana, Ravindra Sangu, Kowstubha Palle, and Venkata Krishna Reddy Chinthalacheruvu. 2022. Multi-Objective Optimal Power Flow Solution Using a Non-Dominated Sorting Hybrid Fruit Fly-Based Artificial Bee Colony. Energies 15: 4063. [Google Scholar] [CrossRef]

- Merton, Robert C. 1976. Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics 3: 125–44. [Google Scholar] [CrossRef] [Green Version]

- Navarro, Ramon, H. Rojas, Izabelly S. De Oliveira, J. E. Luyo, and Y. P. Molina. 2022. Optimization Model for the Integration of the Electric System and Gas Network: Peruvian Case. Energies 15: 3847. [Google Scholar] [CrossRef]

- Otunuga, Olusegun Michael, and Gangaram S. Ladde. 2014. Stochastic Modeling of Energy Commodity Spot Price Processes with Delay in Volatility. American International Journal of Contemporary Research 4: 1–19. [Google Scholar]

- Pilipović, Dragana. 1998. Energy Risk: Valuing and Managing Energy Derivatives. New York: McGraw-Hill. [Google Scholar]

- Podkovalnikov, Sergei, Lyudmila Chudinova, Ivan L. Trofimov, and Leonid Trofimov. 2022. Structural and Operating Features of the Creation of an Interstate Electric Power Interconnection in North-East Asia with Large-Scale Penetration of Renewables. Energies 15: 3647. [Google Scholar] [CrossRef]

- Sato, Ken-iti. 1999. Lévy Processes and Infinitely Divisible Distributions. Number 68 in Cambridge Studies in Advanced Mathematics. Cambridge and New York: Cambridge University Press. [Google Scholar]

- Schoutens, Wim. 2003. Lévy Processes in Finance: Pricing Financial Derivatives. Wiley Series in Probability and Statistics; Chichester, West Sussex and New York: J. Wiley. [Google Scholar]

- Schwartz, Eduardo S. 1997. The Stochastic Behavior of Commodity Prices: Implications for Valuation and Hedging. The Journal of Finance 52: 923–73. [Google Scholar] [CrossRef]

- Shahmoradi, Akbar, and Anatoliy Swishchuk. 2016. Pricing crude oil options using Lévy processes. The Journal of Energy Markets 9: 47–63. [Google Scholar] [CrossRef]

- Shobeiri, Elaheh, Huan Shen, Filippo Genco, and Akira Tokuhiro. 2022. Investigating Long-Term Commitments to Replace Electricity Generation with SMRs and Estimates of Climate Change Impact Costs Using a Modified VENSIM Dynamic Integrated Climate Economy (DICE) Model. Energies 15: 3613. [Google Scholar] [CrossRef]

- Skorokhod, Anatoliĭ Vladimirovich. 1991. Random Processes with Independent Increment. Dordrecht: Springer Science+Business Media. [Google Scholar]

- Sun, Bo, Siyuan Cheng, Jingdong Xie, and Xin Sun. 2022. Identification of Generators’ Economic Withholding Behavior Based on a SCAD-Logit Model in Electricity Spot Market. Energies 15: 4135. [Google Scholar] [CrossRef]

- Swishchuk, Anatoliy. 2008. Explicit Option Pricing Formula for a Mean-Reverting Asset in Energy Market. Journal of Numerical and Applied Mathematics 1: 216–33. [Google Scholar]

- Swishchuk, Anatoliy. 2013a. Modeling and Pricing of Swaps for Financial and Energy Markets with Stochastic Volatilities. Singapore: World Scientific. [Google Scholar] [CrossRef] [Green Version]

- Swishchuk, Anatoliy. 2013b. Variance and volatility swaps in energy markets. The Journal of Energy Markets 6: 33–49. [Google Scholar] [CrossRef]

- Swishchuk, Anatoliy. 2020a. Alternatives to Black-76 Model for Options Valuation of Futures Contracts (Lectures’ Notes). Unpublished manuscript. [Google Scholar] [CrossRef]

- Swishchuk, Anatoliy. 2020b. Stochastic Modeling and Pricing of Energy Markets’ Contracts with Local Stochastic Delayed and Jumped Volatilities. In Handbook of Energy Finance: Theories, Practices and Simulations. Edited by Stéphane Goutte and Duc Khuong Nguyen. Singapore: World Scientific Publishing Co. Pte. Ltd., pp. 247–66. [Google Scholar]

- Swishchuk, Anatoliy, Ana Roldan-Contreras, Elham Soufiani, Guillermo Martinez, Mohsen Selfi, Nishant Agrawal, and Yao Yao. 2021. Alternatives to Black-76 Model for Options Valuations of Futures Contracts. Wilmott 2021: 40–49. [Google Scholar] [CrossRef]

- Swishchuk, Anatoliy, and Kaijie Cui. 2013. Weather Derivatives with Applications to Canadian Data. Journal of Mathematical Finance 3: 81–95. [Google Scholar] [CrossRef] [Green Version]

- TheSolutionsProject. 2023. Available online: https://thesolutionsproject.org/ (accessed on 23 May 2023).

- Ullah, Zahid, Arshad, and Hany Hassanin. 2022. Modeling, Optimization, and Analysis of a Virtual Power Plant Demand Response Mechanism for the Internal Electricity Market Considering the Uncertainty of Renewable Energy Sources. Energies 15: 5296. [Google Scholar] [CrossRef]

- Wang, Jidong, Jiahui Wu, and Yingchen Shi. 2022. A Novel Energy Management Optimization Method for Commercial Users Based on Hybrid Simulation of Electricity Market Bidding. Energies 15: 4207. [Google Scholar] [CrossRef]

- Witzel, Jordan. 2022. University of Calgary: $2.14M Investment Announced to Support Energy Transition Collaboration between UCalgary Ecosystem and Energy Industry. January. Available online: https://ucalgary.ca/news/214m-investment-announced-support-energy-transition-collaboration-between-ucalgary-ecosystem-and (accessed on 23 May 2023).

- Yor, Marc. 1992. On some exponential functionals of Brownian motion. Advances in Applied Probability 24: 509–31. [Google Scholar] [CrossRef] [Green Version]

- Yor, Marc, and Hiroyuki Matsumoto. 2005. Exponential functionals of Brownian motion, I: Probability laws at fixed time. Probability Surveys 2: 312–47. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Bidan, Yang Du, Xiaoyang Chen, Eng Gee Lim, Lin Jiang, and Ke Yan. 2022. Potential Benefits for Residential Building with Photovoltaic Battery System Participation in Peer-to-Peer Energy Trading. Energies 15: 3913. [Google Scholar] [CrossRef]

- Zhao, Jun, Xiaonan Wang, and Jinsheng Chu. 2022. The Strategies for Increasing Grid-Integrated Share of Renewable Energy with Energy Storage and Existing Coal Fired Power Generation in China. Energies 15: 4699. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Price and Option Process Parameters | ||||||

|---|---|---|---|---|---|---|

| T | a | L | r | K | ||

| 6 months | 4.6488 | 1.5116 | 2.7264 | 0.1885 | 0.05 | 3 |

| Parameters | |||

|---|---|---|---|

| a | L | ||

| 4.6488 | 1.5116 | 2.7264 | 0.18 |

| Parameter | ||||||

|---|---|---|---|---|---|---|

| Estimation |

| Days to Expriy after Market Close on April 24, 2015 | ||||||||

|---|---|---|---|---|---|---|---|---|

| 18 | 52 | 113 | 205 | 297 | 387 | 417 | ||

| Settlements of Each Contracts | ||||||||

| WTI Crude Futures Options | 50.00 | 7.36 | 9.60 | 11.78 | 13.86 | 14.94 | 15.61 | 15.61 |

| 51.00 | 6.43 | 8.73 | 10.96 | 13.06 | 14.31 | 15.04 | 15.04 | |

| 52.00 | 5.53 | 7.89 | 10.15 | 12.28 | 13.38 | 14.29 | 14.29 | |

| 53.00 | 4.68 | 7.08 | 9.37 | 11.52 | 12.80 | 13.55 | 13.55 | |

| 54.00 | 3.87 | 6.30 | 8.62 | 10.78 | 11.88 | 12.83 | 12.83 | |

| 55.00 | 3.11 | 5.54 | 7.89 | 10.07 | 11.16 | 11.88 | 11.88 | |

| 56.00 | 2.44 | 4.84 | 7.19 | 9.37 | 10.65 | 11.19 | 11.19 | |

| 57.00 | 1.86 | 4.19 | 6.52 | 8.70 | 9.77 | 10.52 | 10.52 | |

| 58.00 | 1.35 | 3.58 | 5.88 | 8.05 | 9.11 | 9.87 | 9.87 | |

| 59.00 | 0.96 | 3.01 | 5.27 | 7.42 | 8.48 | 9.24 | 9.24 | |

| 60.00 | 0.67 | 2.51 | 4.69 | 6.81 | 7.87 | 8.63 | 8.63 | |

| 61.00 | 0.45 | 2.07 | 4.15 | 6.23 | 7.29 | 8.05 | 8.05 | |

| 62.00 | 0.31 | 1.67 | 3.66 | 5.67 | 6.73 | 7.48 | 7.48 | |

| 63.00 | 0.21 | 1.35 | 3.21 | 5.16 | 6.19 | 6.94 | 6.94 | |

| 64.00 | 0.15 | 1.08 | 2.79 | 4.67 | 6.00 | 6.43 | 6.43 | |

| 65.00 | 0.11 | 0.85 | 2.40 | 4.22 | 5.24 | 5.95 | 5.95 | |

| 66.00 | 0.09 | 0.68 | 2.07 | 3.79 | 5.10 | 5.80 | 5.80 | |

| 67.00 | 0.07 | 0.53 | 1.78 | 3.40 | 4.39 | 5.05 | 5.05 | |

| 68.00 | 0.06 | 0.42 | 1.53 | 3.05 | 4.00 | 4.64 | 4.64 | |

| Futures | 57.15 | 58.90 | 60.50 | 62.03 | 62.98 | 63.57 | 63.68 | |

| Days to Expriy after Market Close on April 24, 2015 | ||||||||

|---|---|---|---|---|---|---|---|---|

| 18 | 52 | 113 | 205 | 297 | 387 | 417 | ||

| At the Moneyness of Option Contracts | ||||||||

| WTI Crude Futures Options | ||||||||

| Futures | ||||||||

| Parameters | JDM | VG | NIG |

|---|---|---|---|

| St | ||||||

| St+1 − St | ||||||

| ln(St) | ||||||

| ln[St+1/St] |

| Parameter | k | c | ||||

|---|---|---|---|---|---|---|

| Estimation |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Swishchuk, A. Overview of Some Recent Results of Energy Market Modeling and Clean Energy Vision in Canada. Risks 2023, 11, 150. https://doi.org/10.3390/risks11080150

Swishchuk A. Overview of Some Recent Results of Energy Market Modeling and Clean Energy Vision in Canada. Risks. 2023; 11(8):150. https://doi.org/10.3390/risks11080150

Chicago/Turabian StyleSwishchuk, Anatoliy. 2023. "Overview of Some Recent Results of Energy Market Modeling and Clean Energy Vision in Canada" Risks 11, no. 8: 150. https://doi.org/10.3390/risks11080150

APA StyleSwishchuk, A. (2023). Overview of Some Recent Results of Energy Market Modeling and Clean Energy Vision in Canada. Risks, 11(8), 150. https://doi.org/10.3390/risks11080150