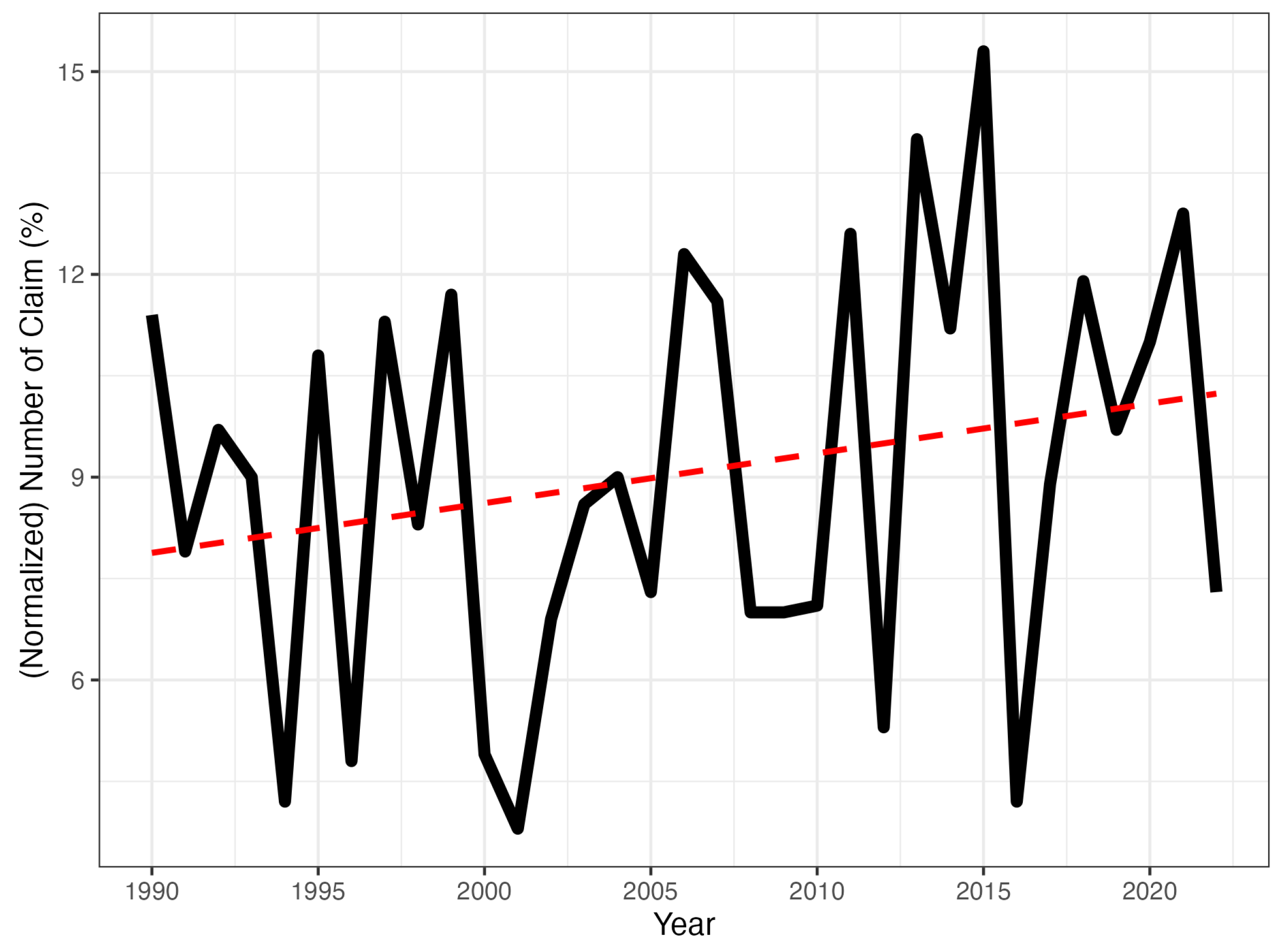

3.1. Monthly Normalized Number of Claims, N

In

Table 3, we present the results of three linear regression models designed to explore the relationship between climate variables, such as the SACI and its components, and the mean of

N.

In

model 1

we explore the influence of the monthly SACI on the mean of

N and find it to be significant at a

level. This suggests a certain influence on the number of hail claims. However, the deficient

indicates that the SACI alone does not explain the variations well in the mean of

N.

In

model 2,

we introduce the components of the SACI to discern their impact on the mean of

N. Notably, high-temperature days (

) and sea level (

) are significant, suggesting a potential link between these two SACI components and the mean. However, despite their significance, the overall explanatory power of the model, as indicated by

, remains low. While extreme heat and sea level contribute to the predictive model, additional variables are needed to enhance the accuracy of the analysis.

In

model 3, we test the formula

which incorporates the months from April to September, covering the high-incidence season of hailstorms. Despite the statistical significance observed for precipitation (

) and wind (

) with coefficients of opposite signs, the overall explanatory power of the model, indicated by the R-squared value

= 0.5, remains moderate, though it is significantly improved from the preceding case. Notably, the month variables attain statistical significance at the 1% level, except for April, which is significant at the 10% level. This affirms the seasonal pattern in the occurrence of hail events.

In summary, while the relationship between the mean of

N and the SACI appears fragile in model 1 (Equation (

9)), evidence from models 2 (Equation (

10)) and 3 (Equation (

11)) suggests that components such as high-temperature days (

), precipitation (

), wind (

), and sea level (

) explain the variation of the mean of

N up to a certain point. Notably, the wind component is significant in model 3 (Equation (

11)), with a negative

, indicating a potential opposite effect on

N from the other significant components. Additionally, the season variables from April to September are also significant, as expected.

Table 3.

Linear regression results for

N, models 1, 2, and 3 (see Equations (

9)–(

11)). For each independent variable, we show the

value, the

p-value (*, **, ***), and the standard deviation in parenthesis.

Table 3.

Linear regression results for

N, models 1, 2, and 3 (see Equations (

9)–(

11)). For each independent variable, we show the

value, the

p-value (*, **, ***), and the standard deviation in parenthesis.

| | Dependent Variable: |

|---|

| | Number of Claim |

|---|

| | Model 1 | Model 2 | Model 3 |

|---|

| SACI | 0.008 *** | | |

| | (0.001) | | |

| T90std | | 0.002 *** | 0.001 |

| | | (0.001) | (0.001) |

| T10std | | 0.002 | 0.0005 |

| | | (0.001) | (0.001) |

| Pstd | | −0.002 | 0.003 *** |

| | | (0.001) | (0.001) |

| Dstd | | −0.001 | −0.0001 |

| | | (0.001) | (0.001) |

| Wstd | | −0.001 | −0.003 *** |

| | | (0.001) | (0.001) |

| Sstd | | 0.002 *** | 0.0004 |

| | | (0.0004) | (0.0004) |

| April | | | 0.003 * |

| | | | (0.002) |

| May | | | 0.017 *** |

| | | | (0.002) |

| June | | | 0.017 *** |

| | | | (0.002) |

| July | | | 0.023 *** |

| | | | (0.002) |

| August | | | 0.020 *** |

| | | | (0.002) |

| September | | | 0.013 *** |

| | | | (0.002) |

| Constant | 0.004 *** | 0.003 *** | −0.0002 |

| | (0.001) | (0.001) | (0.001) |

| Observations | 396 | 396 | 396 |

| R2 | 0.081 | 0.138 | 0.502 |

| Adjusted R2 | 0.079 | 0.125 | 0.487 |

| Residual Std. Error | 0.012 (df = 394) | 0.012 (df = 389) | 0.009 (df = 383) |

| F Statistic | 34.868 *** (df = 1; 394) | 10.398 *** (df = 6; 389) | 32.197 *** (df = 12; 383) |

Next, we move to the study of the influence of the SACI and its components on the quantiles of

N. For this, we begin with

model 4:

The results are reported in

Table 4. At the 90th percentile, the SACI exhibits a statistically significant positive association with the number of claims (coefficient = 0.018,

p < 0.01). For the 95th percentile, although positive, the association is not significant (coefficient = 0.014,

p > 0.1); the confidence interval at 95% spans both negative and positive halves of the real line. At the 99th percentile, the positive relationship is marginally significant (coefficient = 0.005,

p < 0.1), but the confidence interval is similarly inconclusive. The confidence intervals for the 99th and 95th percentiles include both positive and negative values, suggesting a degree of uncertainty regarding the precise impact of the SACI. The two marginally significant positive coefficients, along with confidence intervals spanning from slightly negative to positive values, indicate that the relationships between the SACI and

N at those percentiles are not as conclusively positive as observed at the lower 90th percentile. The inclusion of zero in the intervals suggests the possibility of a null effect or a very modest effect that is not statistically distinguishable from zero. In

Table 4, we observe that the pseudo-R-squared decreases as the quantile increases in quantile regression. This decrease in pseudo-R-squared at higher quantiles suggests that the model’s explanatory power diminishes for extreme observations. It indicates the presence of additional factors or complexities contributing to the variability in the upper tail of the distribution.

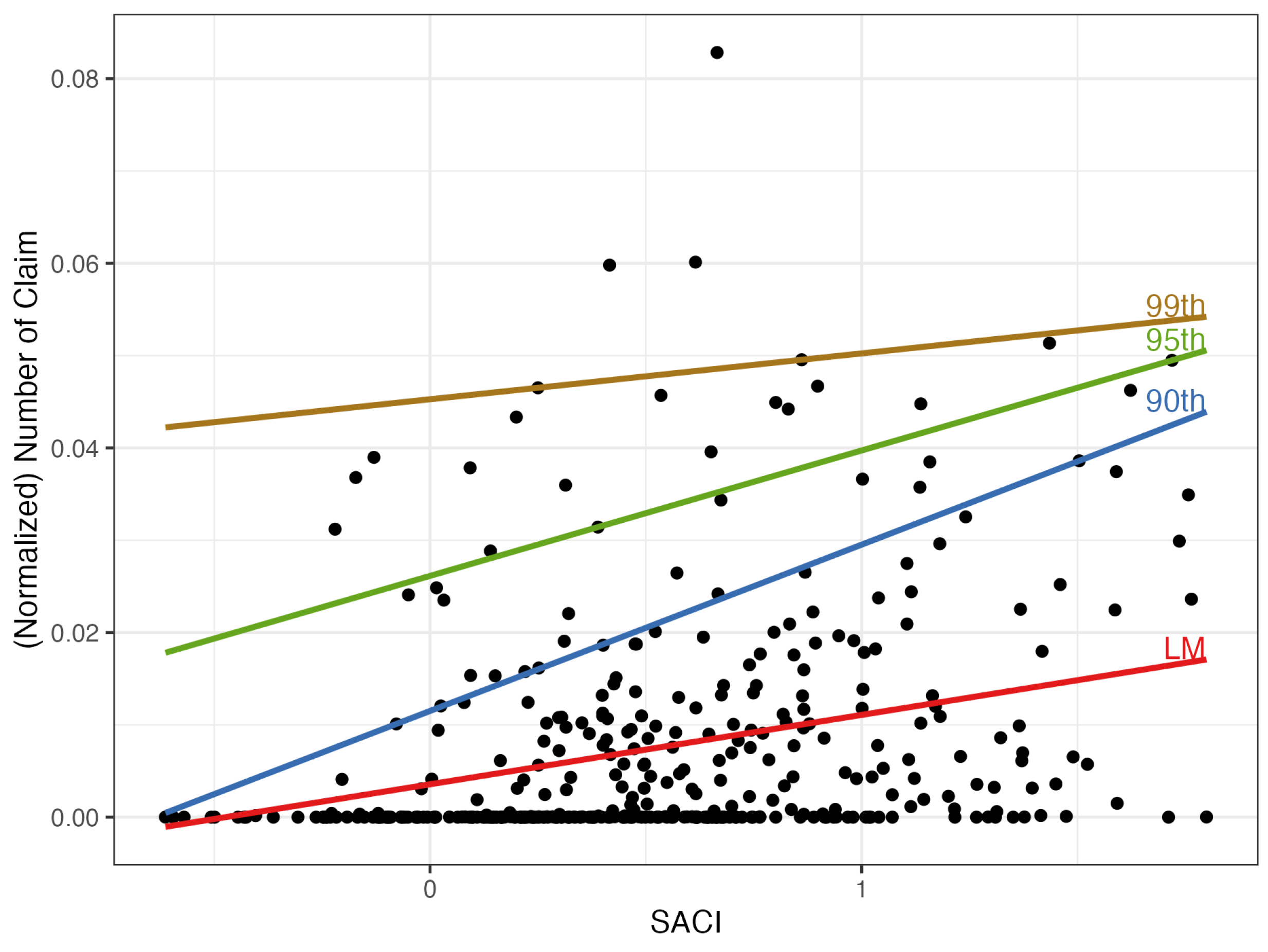

The scatter plot in

Figure 8 illustrates the influence of the SACI on the quantiles of

N, based on the information in

Table 4. The quantile lines correspond to model 4 (Equation (

12). With caution, we observe that an increase in the SACI leads to an increase in all three levels of

. Additionally, it appears that the higher the probability level, the less steep the quantile line.

In

model 5, we introduce the months relevant to hail risk:

while in

model 6 we introduce the SACI components together with the months as independent variables:

In

Table 5, the results for these two quantile regression models show that both the SACI and its components, except for drought (

), significantly impact the normalized number of claims across different quantiles. For the significant variables, confidence intervals lie on either side of the origin. In the cases of

, they are on the positive side, indicating an increasing influence on

. For

, this happens on the negative side, indicating that an increase in the wind component results in a decrease in the corresponding quantile of

N (similar to what was observed in the mean of

N; see model 3, Equation (

11)). These results suggest that the SACI, as a comprehensive climate index, has a substantial impact on the extremes of the number of claims,

N. The months constituting the hailstorm season are all significant, as expected. As explained in the previous section, pseudo-R-squared values are calculated following

Koenker and Machado (

1999). The values obtained for these six models all exceed 0.5, indicating a not negligible fitting score for all these models.

Figure 8.

Scatter plot of the monthly normalized number of claims,

N, versus the SACI. Regression and quantile regression (probabilities

) lines corresponding to model 1 (Equation (

9),

Table 3) and model 4 (Equation (

12),

Table 4).

Figure 8.

Scatter plot of the monthly normalized number of claims,

N, versus the SACI. Regression and quantile regression (probabilities

) lines corresponding to model 1 (Equation (

9),

Table 3) and model 4 (Equation (

12),

Table 4).

Table 5.

Results for quantile regression for the normalized number of claims, N.

Table 5.

Results for quantile regression for the normalized number of claims, N.

| | Dependent Variable: |

|---|

| | Number of Claims (Normalized) |

|---|

| | Model 5_0.9 | Model 5_0.95 | Model 5_0.99 | Model 6_0.9 | Model 6_0.95 | Model 6_0.99 |

|---|

| SACI | 0.0001 *** | 0.0001 *** | 0.0008 *** | | | |

| | (0.00003, 0.0001) | (0.0001, 0.0002) | (0.0007, 0.0010) | | | |

| T90std | | | | 0.00003 *** | 0.0002 *** | 0.0017 *** |

| | | | | (0.00002, 0.00005) | (0.0001, 0.0002) | (0.0015, 0.0019) |

| T10std | | | | 0.0001 *** | 0.0001 ** | 0.0009 *** |

| | | | | (0.00003, 0.0001) | (0.000003, 0.0002) | (0.0006, 0.0013) |

| Pstd | | | | 0.0001 *** | 0.0003 *** | 0.0019 *** |

| | | | | (0.00005, 0.0001) | (0.0002, 0.0004) | (0.0015, 0.0022) |

| Dstd | | | | −0.00002 | 0.0001 | 0.0003 |

| | | | | (−0.0001, 0.00001) | (−0.00002, 0.0002) | (−0.0001, 0.0007) |

| Wstd | | | | −0.00005 *** | −0.0001 *** | −0.0017 *** |

| | | | | (−0.0001, −0.00003) | (−0.0002, −0.0001) | (−0.0020, −0.0015) |

| Sstd | | | | 0.00002 *** | 0.0001 *** | 0.0008 *** |

| | | | | (0.00002, 0.00003) | (0.00002, 0.0001) | (0.0007, 0.0010) |

| April | 0.0101 *** | 0.0111 *** | 0.0153 *** | 0.0099 *** | 0.0105 *** | 0.0163 *** |

| | (0.0100, 0.0101) | (0.0110, 0.0112) | (0.0150, 0.0156) | (0.0099, 0.0100) | (0.0104, 0.0107) | (0.0157, 0.0169) |

| May | 0.0264 *** | 0.0600 *** | 0.0817 *** | 0.0265 *** | 0.0596 *** | 0.0798 *** |

| | (0.0264, 0.0265) | (0.0599, 0.0601) | (0.0814, 0.0819) | (0.0264, 0.0265) | (0.0594, 0.0598) | (0.0792, 0.0804) |

| June | 0.0348 *** | 0.0465 *** | 0.0495 *** | 0.0347 *** | 0.0461 *** | 0.0422 *** |

| | (0.0347, 0.0348) | (0.0464, 0.0466) | (0.0493, 0.0498) | (0.0346, 0.0347) | (0.0459, 0.0463) | (0.0415, 0.0428) |

| July | 0.0448 *** | 0.0492 *** | 0.0482 *** | 0.0448 *** | 0.0483 *** | 0.0432 *** |

| | (0.0448, 0.0449) | (0.0491, 0.0493) | (0.0480, 0.0485) | (0.0447, 0.0448) | (0.0481, 0.0484) | (0.0426, 0.0439) |

| August | 0.0373 *** | 0.0455 *** | 0.0589 *** | 0.0372 *** | 0.0449 *** | 0.0572 *** |

| | (0.0373, 0.0374) | (0.0454, 0.0456) | (0.0586, 0.0591) | (0.0371, 0.0372) | (0.0448, 0.0451) | (0.0566, 0.0579) |

| September | 0.0356 *** | 0.0394 *** | 0.0457 *** | 0.0355 *** | 0.0392 *** | 0.0423 *** |

| | (0.0356, 0.0357) | (0.0393, 0.0395) | (0.0454, 0.0460) | (0.0355, 0.0356) | (0.0390, 0.0394) | (0.0416, 0.0429) |

| Constant | 0.00003 *** | 0.0001 *** | 0.0006 *** | 0.0001 *** | 0.0003 *** | 0.0020 *** |

| | (0.00001, 0.0001) | (0.00004, 0.0001) | (0.0005, 0.0007) | (0.0001, 0.0001) | (0.0002, 0.0004) | (0.0017, 0.0023) |

| Observations | 396 | 396 | 396 | 396 | 396 | 396 |

| Pseudo | 0.5607 | 0.5771 | 0.5780 | 0.5609 | 0.5780 | 0.6475 |

3.2. Monthly Normalized Number of Loss Costs Equal to One,

Next, we explore the relationship between as the dependent variable and the SACI and its components as independent variables. It is important to note that a claim with a loss cost equal to 1 implies that the loss equals the value of the insured capital, indicating the full scale of damage for that claim.

In

model 7, we investigate the linear regression with the SACI alone as an independent variable:

while

model 8 also includes the months composing hailstorms season:

Results for both models are presented in

Table 6. Model 7 (Equation (

15)) indicates that the SACI is statistically significant at the 1% level, with a

coefficient of 0.0003. However, the R-squared value is extremely low,

, suggesting a very weak explanatory power of the model.

In model 8 (Equation (

16)), with the introduction of the months as independent variables (April to September), we observe that only May, July, and August are statistically significant among the month variables. This is a notable difference compared to the case of the number of claims,

N, suggesting that not every month in the hailstorm season is relevant to the loss costs being equal to one—only May, July, and August. Overall, the R-squared value of the model increases to 0.146, indicating an improvement in its ability to explain the mean of

. In summary, through model 8 (Equation (

16)), we have found that the SACI influences, to a certain extent, the mean of

. An increase of one unit in the SACI would result in an extremely slight increase in this mean by a factor of 0.0003. Additionally, during the hailstorm season, only May, July, and August are significant for the mean

.

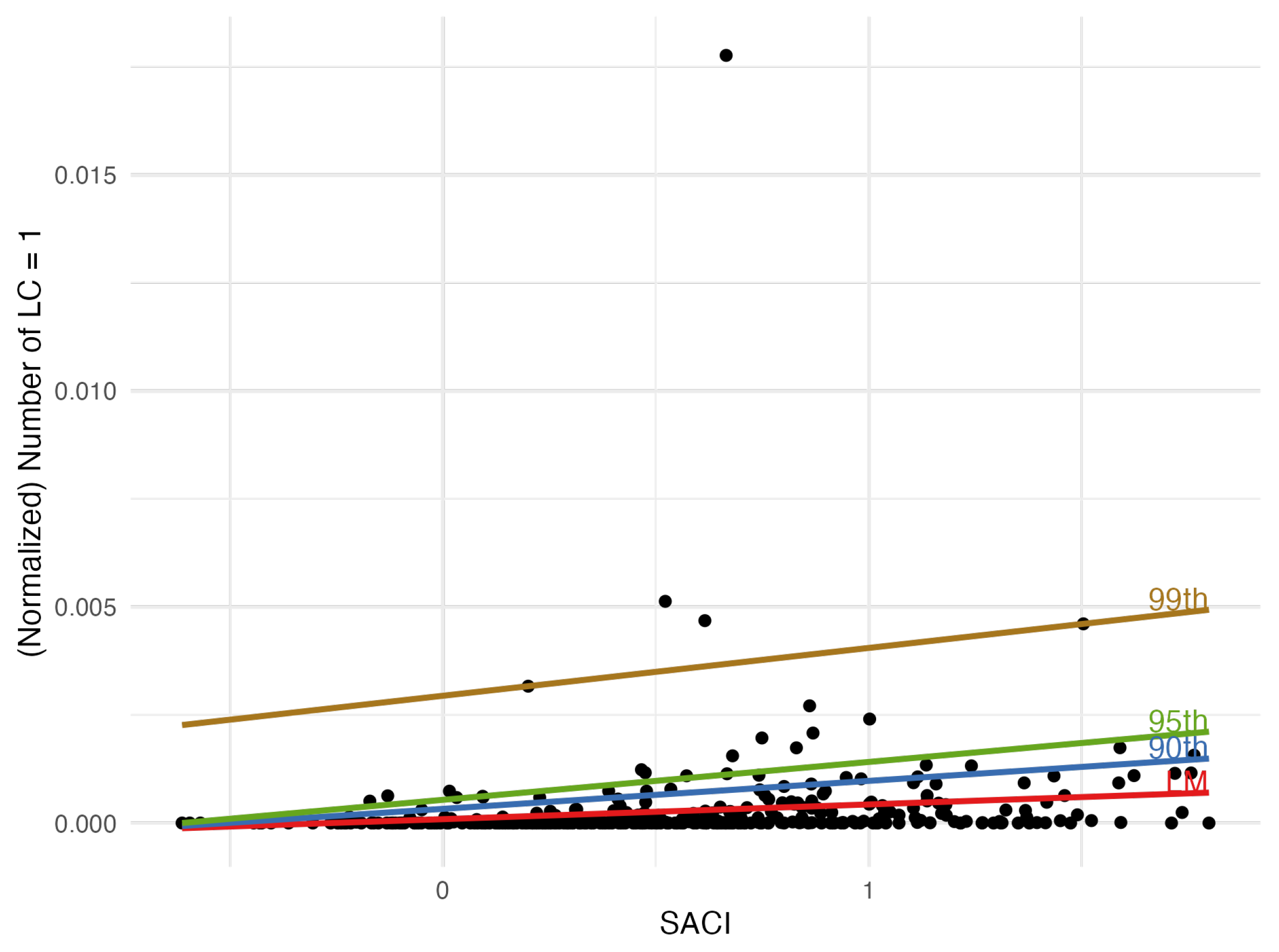

In

Figure 9, we observe the increasing line given by model 7 (Equation (

15) predicting the mean

based on the values of the SACI. Additionally, we find quantile regression lines corresponding to probability levels

. In all three cases, we have an increasing line. The three lines correspond to the quantile regression defined by

model 9:

In

Table 7, the coefficient for the variable SACI is statistically significant at the 1% level for both the 90th and 95th percentiles. This signifies a discernible positive relationship between the SACI and

at these percentiles, underscoring its role in influencing

. However, at the 99th percentile, there is no significance, and the confidence interval contains zero. This model is relatively weak, as indicated by the very low values of the pseudo-

.

Next, in

model 10 we introduce the months in the quantile regression using

We have finally decomposed the index into its components, adding the months in the quantile regression

model 11 for the same three

-values:

Table 7.

Quantile regression results for model 9 (Equation (

17).

Table 7.

Quantile regression results for model 9 (Equation (

17).

| | Dependent Variable: |

|---|

| | |

|---|

| | 90th | 95th | 99th |

|---|

| SACI | 0.001 *** | 0.001 *** | 0.001 |

| | (0.0004, 0.001) | (0.001, 0.001) | (−0.008, 0.010) |

| Constant | 0.0003 *** | 0.001 *** | 0.003 |

| | (0.0001, 0.001) | (0.0003, 0.001) | (−0.003, 0.009) |

| Observations | 396 | 396 | 396 |

| Pseudo | 0.0967 | 0.0742 | 0.0411 |

Figure 9.

Scatter plot of versus the SACI. The lines represent linear regression and quantile regressions for three different quantiles (0.9, 0.95, and 0.99) corresponding to models 6 and 8.

Figure 9.

Scatter plot of versus the SACI. The lines represent linear regression and quantile regressions for three different quantiles (0.9, 0.95, and 0.99) corresponding to models 6 and 8.

In

Table 8, we summarize the results corresponding to models 10 (Equation (

18)) and 11 (Equation (

19)). In model 10 (Equation (

18), the SACI variable has a significant impact on the 95th and 99th quantile levels. All months are significant except April in the 90th and 99th quantiles. In model 11 (

19), precipitation,

, and drought,

, are not significant at any of the three quantile levels, suggesting a weak association between extreme precipitation and drought with

extremes. On the other hand, high and low temperatures (

) are significant variables in all three quantiles, while wind,

, and sea level,

, are only significant for quantiles

and 0.95. Wind coefficients are negative, as observed in previous models. All months from April to September are significant across the three probability levels, and their inclusion has enhanced the models, as indicated by the increase in pseudo-

from model 10 to model 11 in

Table 7 and

Table 8. In this last case, the pseudo-

coefficients are all above 0.35, and they increase across higher quantiles, suggesting an improved ability of predictors to capture variability in the number of

LC1 at extreme percentiles.

3.3. Monthly Homogenized Losses, L

In the first stage, we will investigate the climate-change effect on L through four linear regression models, examining the impact of the SACI and its components on monthly total hailstorm losses.

The results are presented in

Table 9. In models 12 (Equation (

20)) and 13 (Equation (

21)), the SACI is significant at the 1% confidence level with a positive coefficient, indicating an increase in the mean of

L with an increase in the SACI. The

for model 12 is not negligible (0.159). Notably, in model 13 we achieve a high

value of 0.809, likely attributed to the inclusion of months in this model.

In models 14 (Equation (

22)) and 15 (Equation (

23)), we explore the significance of SACI components, revealing different levels of significance. In model 14 (without months), hot and cool temperatures, precipitation, and sea level (

) are significant, while drought and wind (

and

) are not. It is worth noting that the significance of

indicates a negative correlation with

L. In model 15 (including the months), cool temperatures, wind, and sea level (

) are significant, while the rest are not. Again, when wind is significant, it is negatively correlated with

L. Regarding the

scores, it is not negligible for model 14, and in model 15 it achieves a remarkably high value of 0.814. Given the complexity of the models, model 13 provides a more concise explanation of the mean monthly total hailstorm loss than model 15. This is because model 13 consolidates all climate-change effects into one measure, the SACI, simplifying interpretation and understanding.

In the context of model 13, interpreting the SACI coefficient (

) suggests that an increase of

c units in the SACI leads to an increase in the mean of

L by

. For example, assuming a monthly the SACI increase of 0.1, we would observe an approximate increase in the mean total loss by

, equivalent to approximately 9.1%. This interpretation helps estimate the potential cost of future climate change as measured by the SACI. In model 13 (Equation (

21)), we calculated the predicted

for different SACI values. Choosing the months with the maximum and minimum SACI values among April to September 2022, specifically July 2022 (SACI = 1.764) and May 2022 (SACI = 1.050), the model predicted values were approximately EUR 3,327,700 for July and EUR 2,433,643 for May. These cases can be used to establish upper and lower bounds for the increase in

corresponding to a hypothetical future increase in the SACI by 0.1 units. The increase can be estimated by multiplying these values by 0.091:

Change in losses from May to July is not solely attributable to the change in SACI values, as suggested by

. Instead, it resulted from a combination of the SACI’s effect and the specific monthly effect encoded by each month’s coefficient, highlighting the model’s complexity. The percentage change in losses due to the month shift, calculated as

which is approximately 36.74%, is approximately 36.74%, demonstrating the significant influence of monthly coefficients on

predictions.

Therefore, this interpretation is a key factor for sustainability management because it provides a concrete way to quantify the impact of an increment in the SACI on . In summary, this direct percentage relationship makes the SACI an effective tool for assessing future increases in the mean monthly total loss due to a growing climate-change scenario.

Finally, we note that models 13 and 15 (Equations (

21) and (

23)), which include the months, demonstrate stronger explanatory power compared to the other two models, as seen from their R-squared values of approximately 0.81.

Next, we move on to the quantile regression models with

as the dependent variable. It is relevant to outline here the well-known quantile property (see

Koenker 2005, p. 48):

for any monotone transformation,

. In our case,

.

Model 16 only includes the SACI as an independent variable:

Figure 10 illustrates the relationship between monthly

and the SACI. It contains four fitted lines. The upward red line, representing the linear regression, indicates that as the SACI increases,

tends to rise also, supporting the conclusion that there is a positive correlation between the SACI and hailstorm losses. In addition, three colored lines correspond to quantile regressions for the 90th, 95th, and 99th percentiles. These lines demonstrate the variation in higher losses associated with SACI values, illustrating the behavior of the tail of the monthly total loss distribution concerning SACI variations.

Table 10 presents the results of quantile regression for model 16 (Equation (

26), with the dependent variable being

and the independent one being the monthly SACI. For the 90th and 95th quantiles, the SACI coefficients are significant at the 1% level. On practical grounds, this implies that a one percentage point of 0.01 increase in the SACI is associated with a 1.141% increase in hail

L at the 90th quantile. A similar calculation could be carried out in the 95th quantile. Unfortunately, this is not extensible to the 99th quantile because the coefficient is no longer credible (see its confidence interval and

p-value). The pseudo-R-squared values are quite low, implying that the model explains only a small proportion of the variability in hailstorm losses. These values suggest that the SACI independent variable contributes modestly to explaining the variability in hailstorm losses at these quantiles.

In

model 17, we include the months of April to September as independent binary variables:

In

model 18, we decompose the monthly SACI into its components while still including the months:

Table 11 presents the results of an analysis using quantile regression to investigate the relationship between hailstorm total losses and the SACI or its components. The analysis is conducted separately for the 90th, 95th, and 99th percentiles, taking into account monthly variables from April to September. Concerning model 17 (Equation (

27)), the SACI exhibits statistical significance at the three percentiles, even though the confidence interval in the first case contains negative and positive values, a fact that devaluates the quality of this estimate. This indicates (with due caution for the 90th case) a significant positive correlation between the SACI and hailstorm losses across these percentiles. The SACI’s influence becomes more pronounced with increasing percentiles, highlighting its heightened importance in extreme loss events. The observed trend in SACI coefficient values, rising from 0.541 to 0.619, emphasizes its non-uniform impact across quantiles of the monthly total loss distribution. This underscores the SACI’s important role in assessing the severity and potential risk of the most damaging hailstorm events represented in the upper quantiles of the distribution. Note that all the months are significant.

Figure 10.

Scatter plot of monthly

versus the SACI. Note: The straight lines are linear regression (see

Table 9) and quantile regression (

) (see

Table 10).

Figure 10.

Scatter plot of monthly

versus the SACI. Note: The straight lines are linear regression (see

Table 9) and quantile regression (

) (see

Table 10).

Table 10.

Results of quantile regression for model 16 (Equation (

26).

Table 10.

Results of quantile regression for model 16 (Equation (

26).

| | Dependent Variable: |

|---|

| | |

|---|

| | 90th | 95th | 99th |

|---|

| SACI | 1.141 *** | 0.963 *** | 0.591 |

| | (0.480, 1.802) | (0.467, 1.458) | (−0.274, 1.455) |

| Constant | 14.031 *** | 14.536 *** | 15.256 *** |

| | (13.561, 14.501) | (14.183, 14.888) | (14.641, 15.871) |

| Observations | 396 | 396 | 396 |

| Pseudo | 0.0319 | 0.0304 | 0.0292 |

In model 18 (Equation (

28)),

(days of extremely hot temperature) is statistically significant at the 95th and 99th percentiles, indicating a positive correlation with losses at higher levels.

(days of extremely cold temperature) is only significant at the 95th percentile.

(days of heavy rainfall) is significant at the 95th and 99th percentiles. Conversely,

(wind speed) has a negative and statistically significant coefficient across all three percentiles, suggesting that higher wind speeds are associated with loss decrease. Remember that a similar behavior was observed for models related to the variables

N and

.

The variable representing sea level, , is significant at the 90th and 95th quantiles, but not at the 99th one. On the other hand, drought days, , are only significant at the 99th quantile. Note that all the months are significant at all the percentiles.

Table 11.

Results of quantile regression for .

Table 11.

Results of quantile regression for .

| | Dependent Variable: |

|---|

| | |

|---|

| | Model 17_ = 0.9 | Model 17_ = 0.95 | Model 17_ = 0.99 | Model 18_ = 0.9 | Model 18_ = 0.95 | Model 18_ = 0.99 |

|---|

| SACI | 0.541 * | 0.578 ** | 0.619 *** | | | |

| | (−0.059, 1.141) | (0.002, 1.153) | (0.257, 0.981) | | | |

| T90std | | | | 0.085 | 0.218 ** | 0.332 *** |

| | | | | (−0.128, 0.299) | (0.032, 0.404) | (0.183, 0.481) |

| T10std | | | | 0.121 | 0.422 ** | 0.143 |

| | | | | (−0.268, 0.510) | (0.083, 0.760) | (−0.128, 0.415) |

| Pstd | | | | 0.277 | 0.528 *** | 1.101 *** |

| | | | | (−0.065, 0.619) | (0.231, 0.826) | (0.863, 1.340) |

| Dstd | | | | 0.169 | 0.066 | 0.876 *** |

| | | | | (−0.248, 0.587) | (−0.297, 0.429) | (0.585, 1.167) |

| Wstd | | | | −0.338 ** | −0.268 ** | −0.484 *** |

| | | | | (−0.609, −0.067) | (−0.504, −0.032) | (−0.673, −0.295) |

| Sstd | | | | 0.168 ** | 0.148 ** | 0.020 |

| | | | | (0.036, 0.300) | (0.033, 0.264) | (−0.073, 0.112) |

| April | 5.331 *** | 4.495 *** | 3.203 *** | 5.165 *** | 4.703 *** | 3.826 *** |

| | (4.338, 6.324) | (3.543, 5.447) | (2.604, 3.802) | (4.522, 5.808) | (4.144, 5.263) | (3.378, 4.275) |

| May | 6.994 *** | 5.857 *** | 4.934 *** | 7.084 *** | 6.077 *** | 5.233 *** |

| | (6.015, 7.974) | (4.917, 6.796) | (4.343, 5.525) | (6.453, 7.716) | (5.528, 6.627) | (4.792, 5.673) |

| June | 6.717 *** | 5.249 *** | 3.911 *** | 6.594 *** | 5.672 *** | 4.694 *** |

| | (5.702, 7.732) | (4.275, 6.222) | (3.299, 4.523) | (5.889, 7.299) | (5.059, 6.285) | (4.202, 5.185) |

| July | 7.003 *** | 5.715 *** | 3.955 *** | 6.657 *** | 5.707 *** | 4.560 *** |

| | (5.998, 8.008) | (4.750, 6.679) | (3.348, 4.561) | (5.970, 7.344) | (5.109, 6.305) | (4.081, 5.039) |

| August | 6.767 *** | 5.388 *** | 3.625 *** | 6.387 *** | 5.317 *** | 3.719 *** |

| | (5.759, 7.776) | (4.420, 6.355) | (3.017, 4.234) | (5.720, 7.054) | (4.737, 5.897) | (3.253, 4.184) |

| September | 6.687 *** | 5.420 *** | 3.639 *** | 6.622 *** | 5.624 *** | 4.528 *** |

| | (5.700, 7.675) | (4.473, 6.367) | (3.043, 4.235) | (5.940, 7.303) | (5.032, 6.217) | (4.052, 5.003) |

| Constant | 7.992 *** | 9.540 *** | 11.305 *** | 8.142 *** | 9.439 *** | 11.018 *** |

| | (7.570, 8.414) | (9.135, 9.945) | (11.050, 11.560) | (7.854, 8.430) | (9.189, 9.690) | (10.817, 11.219) |

| Observations | 396 | 396 | 396 | 396 | 396 | 396 |

| Pseudo | 0.3711 | 0.3192 | 0.2531 | 0.38 | 0.3354 | 0.2857 |

Let us consider model 17 in the case of

(Equation (

27). Let us also consider again the maximum and minimum SACI monthly values for 2022, which are 1.764 (July) and 1.050 (May). We aim to build two bounds (relatives to the year 2022) for the

L-99th quantile variation corresponding to an SACI variation of 0.1, as was done for its mean in (

24). Model 17 predictions for the

L-99th quantiles corresponding to those SACI values are, respectively:

The two 2022-bounds for the

L-99th quantile variation corresponding to a 0.1 increase in the SACI are:

Observe that, when increasing the SACI by 0.1, the adjustment in the 99th quantile of

L can be computed by simply multiplying the loss by

, which is approximately 1.0639. Again, as in (

24), this interpretation is a key factor for sustainability management because it potentially provides a concrete way to quantify the impact of an increment in the SACI into any

-quantile of the monthly total loss,

L. This direct percentage relationship makes the SACI an effective tool for assessing future increases in any quantile of

L caused by an increasing climate-change scenario.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}