Capital Structure Models and Contingent Convertible Securities

Abstract

:1. Introduction

1.1. Structural Models

1.2. Contingent Convertible Securities

1.3. Brief Summary

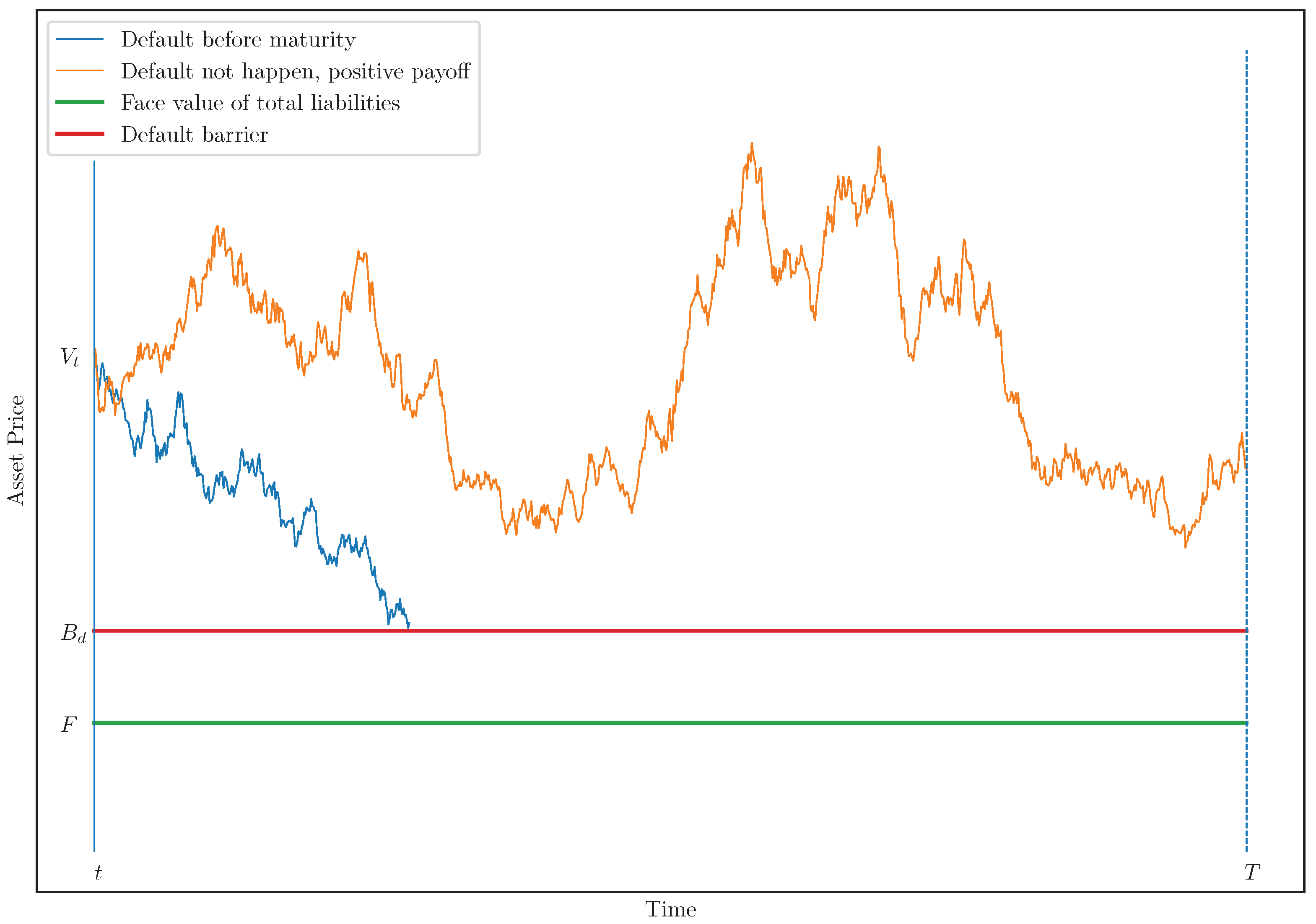

2. Capital Structure without Contingent Capital

2.1. Firm–Value Model

2.2. Capital Structure Assumptions

- The depositors are always paid fully, i.e., the recovery rate of deposits is . It is worth noting that deposits are normally fully insured by government agencies under a certain amount, such as the Federal Deposit Insurance Corporation (FDIC) in the United States and the Canada Deposit Insurance Corporation (CDIC) in Canada.6

- Both senior and junior debts are partially recovered, where the recovery rate of senior debt is higher than that of junior debt. We denote and as the recovery rate for senior and junior debt, respectively, and assume that . The recovery rates are treated as unknown constants to be calibrated.

- We assume that the residual value at liquidation, , is split equally between equity holders and bankruptcy costs. is defined as the difference between the bank’s asset value at default and the total amount paid to creditors:

2.3. Valuation

2.3.1. Debt Valuation

2.3.2. Bankruptcy Costs

2.3.3. Equity Valuation

2.3.4. Model-Implied Equity Volatility

2.3.5. CDS Spread

2.3.6. Equity Option Valuation

2.3.7. Debt Yield

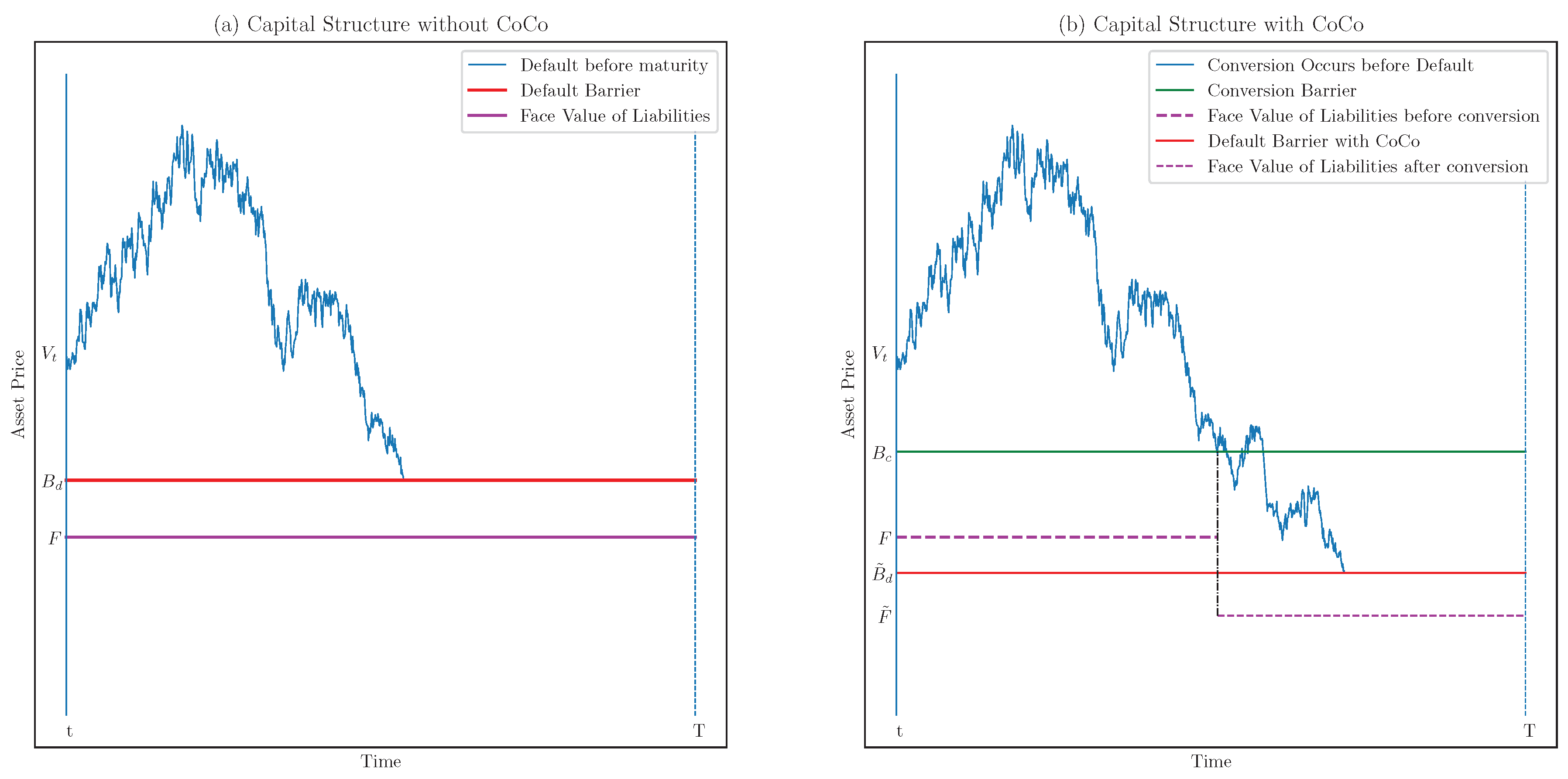

3. Capital Structure with Contingent Capital

3.1. Assumptions

- We assume that conversion is triggered when the bank’s asset–liability ratio falls below a pre-specified level c, defined as , where is the conversion barrier, assumed to be constant over time, and the conversion threshold c is expressed as a percentage of the face value of total liabilities F.

- A main goal of this paper is to use market-observed data to infer the exogenous conversion threshold c.

- Upon conversion, the bank’s liabilities are reduced from F to , and we assume that default occurs upon the first passage of asset value to the level and , or .

3.2. Valuation

4. Data

5. Calibration and Results

- Capital structure without CoCo: The parameters to be calibrated include the default threshold d, asset volatility , recovery rates for senior debt and junior debt , and the average jump size and jump frequency under the jump-diffusion model. The reasons we start with no CoCos in capital structure are as follows:

- (1)

- To provide insights for the banks that only have regular debts in their capital structure.

- (2)

- Chen et al. (2013) showed that as long as conversion precedes default, the optimal default threshold remains unaffected by the conversion trigger. This forms the basis for incorporating these calibrated parameters when introducing CoCo instruments into the capital structure.

- Capital structure with CoCo: using the parameter values from Step 1, we then calibrate the conversion threshold, which is the only unknown parameter.

5.1. Non-Contingent Capital Structure

5.1.1. Calibration

5.1.2. Results

- When the asset value process follows GBM, and we restrict our calibration to just four instruments, the optimal selections among these instruments (i.e., the set of instruments that are priced with minimum error) are typically the stock price and equity volatility, while CDS spreads and option prices may be considered as secondary options. Bond yields, in contrast, prove challenging to calibrate. It is important to note that there is no single, universally applicable set of instruments suitable for calibrating parameters across all banks.

- When jumps are considered in the model:

- −

- The asset volatility falls within the range of 1% to 2% for all banks. This range is consistent with the asset volatility calculated based on the book value of assets for each respective bank. Including jumps produces more realistic values for , compared with those obtained from the GBM model, which are unrealistically low.20

- −

- The recovery rates tend to be lower when compared to the (best-case) GBM model, implying that debtholders would incur greater losses in the event of a default under the jump-diffusion model. This results in a total amount of debtholder losses that are more in line with realism, as supported by prior research (see Altman (2014)).

- −

- The jump frequency represents, on average, the number of jumps occurring in a year. As an illustration, CIBC has a jump frequency of 0.10, indicating that, on average, 0.421 jumps are expected to occur during CIBC’s time-to-maturity of liability of 4.21 years. Across all banks, the jump frequencies are relatively low, with the highest frequency being 0.10, and considering that the average liability maturity time for all banks is 5.2 years, the frequency of jumps is not significant.

- −

- The calibrated average jump size, denoted as , exhibits a maximum average size of . Much like the jump frequency , the average jump size is also relatively modest in magnitude.

- −

- Compared to the outcomes obtained under the GBM model, the default threshold is extended even further below the current asset–liability ratio, experiencing an average reduction of 2%.

5.2. Default Threshold and Capital Requirement

- Common Equity Tier 1 (CET1) ratio;

- Tier 1 capital ratio;

- total capital ratio.

5.3. Capital Structure with Contingent Capital

5.3.1. Calibration

5.3.2. Results

- Under both types of default thresholds, the model-implied conversion would occur prior to the minimum CET1 ratio being breached (i.e., calibrated parameters are consistent with regulatory mandates).

- Except in the case of BMO, all results indicate that conversion should occur when the capital ratio exceeds the OSFI-required minimum total capital ratio.

- In summary, the model’s implied conversion thresholds indicate that conversion occurs at a capital level situated between the OSFI-required minimum total capital ratio and the bank’s actual total capital ratio at time zero, which suggests that the market expects the regulators will enforce conversion while the issuing bank is a going concern, as opposed to a gone concern.

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Expressions in Leland and Toft (1996)

Appendix B. Derivation of Model-Implied Equity Volatility under GBM

Appendix C. Jump-Diffusion Algorithm without Contingent Capital

- Simulate the number of jumps between time zero and T, the jump sizes (), and the jump times (, …, ), following Metzler and Reesor (2015).

- If , simulateand apply the Beskos and Roberts (2005) algothrim to determine the default time. We fixed a stopping time , taking values in . We said that default occurs or does not occur according to or , and is the asset value when default happens.

- If , for , simulate and , where , then computewhere , andFinally, simulate and computeThe default time is determined by two parts:

- −

- : the first time at which the asset value “diffuses” to the default barrier. For , simulatewith the convention that , and we defined and . Setting , we obtained the first time at which the asset value “diffuses” to the default barrier.

- −

- : the first time that the asset value jumps over the default barrier. Determineif , and if , with the convention that .

Thus, the default time, i.e., the first hitting time, isIf and , , and if , then . - The stock price, equity volatility, CDS spread, and senior and junior debt yields can be obtained based on , , and under the equations below. First, the time-t stock price can be estimated as follows:where , is the number of simulated sample paths, and represents the shares outstanding for common shares. For each sample path k, where , and denote the time-t stock price per share and equity value, is the time-t value of debt j, is the time-t bankruptcy cost, and are the asset value at maturity T and default time , respectively, and and are the recovery rate and face value of debt j, respectively.The sample path-k simulated terminal stock price iswhere the residual value along a path that defaults isThe simulated path-k return and the average return across all paths arerespectively. The estimated equity volatility isLet be the time-t fair CDS spread, which for the jump–diffusion model is approximated byThe approximated yields for senior and junior debt can be expressed as follows:

- Since the option maturity, , is shorter than that for long-term debts, an additional simulation is required to determine the option price:

- −

- Simulate the number of jumps between time zero and , the jump sizes (), and the jump times (,…,).

- −

- Determine if default happens between time zero and . If default happens before time , the option value is zero; otherwise, move to the next step.

- −

- If default does not happen before , perform an additional simulation for each sample path between time and T, where the bank’s asset value is . Repeat Steps 1 to 4 with the additional simulation parameters and determine the stock price at time .

- −

- The payoff of the option at time is thus , and the option price at time zero is .

Appendix D. Jump-Diffusion Algorithm for Time-t Stock Price with Contingent Capital

- For each sample path k, where and , simulate the number of jumps between time t and T, the jump sizes (), and the jump times (, …, ), following Metzler and Reesor (2015).

- Determine the conversion time and asset value at conversion:

- (a)

- If , simulate the time-T asset value following Equation (A33) and apply the Beskos and Roberts (2005) algorithm to determine the conversion time. We fixed a stopping time , taking values in for path k. We said that conversion occurs or does not occur according to or , and is the asset value when the conversion happens.

- (b)

- If , follow Step 3 of Appendix C to determine the conversion time and asset value at conversion .

- If conversion does not occur, i.e., , default does not occur either since default cannot precede conversion; thus, the CoCo does not convert to equity, and the stock price at time-t is the same as in the model of non-contingent when default does not happen.

- Determine whether conversion and default happen at the same time. If , upon default, the CoCo is treated as junior debt, and the time-t stock price is estimated as in the model of non-contingent when default happens. Otherwise, move to the next step.

- If conversion precedes default, perform an additional simulation for each sample path k between time and T with the additional paths. Apply Steps 1 to 3 of Appendix C to determine the default time between time- and T for each additional sample path m, where and the asset value process starts at . Denote and as the default time and asset value at default, respectively, and represents the asset value at maturity if default does not occur.

Appendix E. Simulation Steps for Yield, Spread, and Par Yield

- For each sample path , where , simulate the number of jumps between time zero and T, the jump sizes (), and the jump times (, …, ), following Metzler and Reesor (2015).

- Determine whether conversion happens following Step 2 of Appendix D.

- If conversion does not occur, then .

- If conversion occurs, i.e., , determine whether default occurs between and T and the corresponding default time , following the first three steps of Appendix C. Thus, the senior debt yield and CDS spread can be estimated following Equations (37) and (26):

- To estimate the par yield of CoCos, we first estimated the time-t CoCo value under Equation (A58), following the steps in Appendix D. We then equated and the face value of CoCo, , such that , and numerically evaluated the par yield.

| 1 | Data source: Bank of Canada historical bank assets database. |

| 2 | It is worth noting that the National Bank of Canada (NB) is typically grouped with the Big Five, constituting the Big Six. We excluded NB in this study due to the lack of data. |

| 3 | See https://www.bis.org/fsi/fsisummaries/defcap_b3.pdf (accessed on 2 September 2023) for the discussion of going concern and gone concern capital. |

| 4 | In some cases, CoCos are issued originally as preferred stocks. For simplicity, in this paper, we assume CoCos are coupon bonds at issuance. |

| 5 | Some contingent capital can be written down, rather than converting to equity, upon the trigger event, as in the case of the Credit Suisse issuance. |

| 6 | In principle, it is impossible to ensure is when jumps are allowed, as the asset value at default may jump far enough below the barrier to be less than . However, under realistic parameter values, this will happen quite rarely. |

| 7 | See Remark 1 for the situation when the bank’s asset value at default falls below the sum of the recovered values. |

| 8 | Due to the short-term nature of option contracts, the option maturity is generally shorter than the liability maturity T. Thus, if equity can be considered as a European call option written on the firm’s assets, the equity option is essentially an option-on-option on the firm’s assets, i.e., a compound option, where the strike price and maturity time of the inner option are the option strike price and maturity, respectively, and the strike price and maturity time of the outer option is the firm’s face value of liability (on a per share basis), and the liability maturity, respectively. |

| 9 | and is a monotonic function of . |

| 10 | For realistic parameter values, we calculated debt yields in two scenarios, both simplified by assuming constant values for all the other parameters: (1) with a coupon, and (2) without a coupon. Our findings indicate that the disparity between the two computed yields is minimal, with a maximum difference of only 5 to 8 basis points. |

| 11 | We denote as a representation when the asset value process breaches the conversion and default barriers simultaneously. In this case, CoCos do not convert to equity but enter default as junior debt. |

| 12 | Similar to Remark 1, in our simulation, the scenario where the bank’s asset value jumps below the sum of the recovered values and bankruptcy costs at the conversion time never occurred. |

| 13 | For simplicity, we use the name “CoCo” after conversion to distinguish it from the original equity. |

| 14 | We verify the unique equilibrium of price restriction in Theorem 1 of Sundaresan and Wang (2015) using our notations. The equity value at time t is a function of time and asset value: . Let be the conversion barrier such that when the equity value falls to the conversion barrier, the CoCos convert to equity. When , conversion occurs, the CoCo investors receive of the bank’s equity, and . Thus, . Multiplying on both sides gives , which satisfies Theorem 1 of Sundaresan and Wang (2015). |

| 15 | For all five banks, the senior debt accounts for more than 90% of non-deposit debts. |

| 16 | The selected call options for each bank are (a) BMO—strike price of CAD 90 and expiry date 20 October 2020; (b) CIBC—strike price of CAD 100 and expiry date 20 May 2020; (c) RBC—strike price of CAD 96 and expiry date 20 May 2020; (d) BNS—strike price of CAD 58 and expiry date 20 May 2020; and (e) TD—strike price of CAD 66 and expiry date 20 May 2020. |

| 17 | We used the Scipy package of Python to calibrate all parameters; specifically, under Scipy-Optimize-Minimize, the conjugate gradient algorithm is applied. |

| 18 | In Table 2, we report the value of , ℓ can be computed as the . |

| 19 | In the GBM model, a second approach is employed, wherein we do not initially compute the sum of squared errors. Instead, we use each of the 625 parameter groups as individual initial inputs and calibrate them one by one, resulting in 625 calibration outcomes. This approach is feasible in the GBM model as analytical functions are utilized. The two methods yield comparable results. However, in the context of jump-diffusion, where all equations are evaluated through simulation, we cannot employ the same methodology due to the considerable time required for the calibration of one parameter group, typically spanning two to three days. |

| 20 | To validate the calibrated asset volatility, one method is to compute the volatility of the book values of assets from the bank’s quarterly balance sheet. Using 10-year balance sheet data, the computed asset volatilities are between 1% and 2% for all banks. |

| 21 | https://www.bis.org/fsi/fsisummaries/defcap_b3.pdf (accessed on 2 September 2023). |

| 22 | Data sources: annual reports of BMO, CIBC, RBC, BNS, and TD from 2010 to 2019, https://www.sedarplus.ca/ (accessed on 15 July 2023). |

| 23 | To distinguish between the CoCo and the original common equity, we still refer to it as CoCo after conversion. |

References

- Albul, Boris, Dwight M. Jaffee, and Alexei Tchistyi. 2015. Contingent Convertible Bonds and Capital Structure Decisions. Berkeley: Center for Risk Management Research. [Google Scholar]

- Altman, Edward I. 2014. The Role of Distressed Debt Markets, Hedge Funds, and Recent Trends in Bankruptcy on the Outcomes of Chapter 11 Reorganizations. The American Bankruptcy Institute Law Review 22: 75. [Google Scholar]

- Amato, Jeffery D., and Jacob Gyntelberg. 2005. CDS Index Tranches and the Pricing of Credit Risk Correlations. BIS Quarterly Review, March. Amsterdam: Elsevier. [Google Scholar]

- Anderson, Ronald W., Suresh Sundaresan, and Pierre Tychon. 1996. Strategic analysis of contingent claims. European Economic Review 40: 871–81. [Google Scholar] [CrossRef]

- Avdjiev, Stefan, Bilyana Bogdanova, Patrick Bolton, Wei Jiang, and Anastasia Kartasheva. 2020. Coco issuance and bank fragility. Journal of Financial Economics 138: 593–613. [Google Scholar] [CrossRef]

- Avdjiev, Stefan, Anastasia V. Kartasheva, and Bilyana Bogdanova. 2013. Cocos: A primer. BIS Quarterly Review 2013: 43–56. [Google Scholar] [CrossRef]

- Beskos, Alexandros, and Gareth Roberts. 2005. Exact simulation of diffusions. The Annals of Applied Probability 15: 2422–44. [Google Scholar] [CrossRef]

- Beyhaghi, Mehdi, Chris D’Souza, and Gordon S. Roberts. 2014. Funding advantage and market discipline in the Canadian banking sector. Journal of Banking & Finance 48: 396–410. [Google Scholar]

- Bharath, Sreedhar T., and Tyler Shumway. 2008. Forecasting default with the Merton distance to default model. The Review of Financial Studies 21: 1339–69. [Google Scholar] [CrossRef]

- Black, Fischer, and John C. Cox. 1976. Valuing corporate securities: Some effects of bond indenture provisions. The Journal of Finance 31: 351–67. [Google Scholar] [CrossRef]

- Black, Fischer, and Myron Scholes. 1973. The pricing of options and corporate liabilities. Journal of Political Economy 81: 637–54. [Google Scholar] [CrossRef]

- Bolton, Patrick, Anastasia V. Kartasheva, and Wei Jiang. 2023. The credit suisse coco wipeout: Facts, misperceptions, and lessons for financial regulation. Journal of Applied Corporate Finance 35: 66–74. [Google Scholar] [CrossRef]

- Bolton, Patrick, and Frédéric Samama. 2012. Capital access bonds: Contingent capital with an option to convert. Economic Policy 27: 275–317. [Google Scholar] [CrossRef]

- Campolieti, Giuseppe, and Roman N. Makarov. 2018. Financial Mathematics: A Comprehensive Treatment. Boca Raton: CRC Press. [Google Scholar]

- Chen, Nan, Paul Glasserman, Behzad Nouri, and Markus Pelger. 2013. Cocos, Bail-In, and Tail Risk. Working Paper (0004). Washington, DC: Office of Financial Research. [Google Scholar]

- Collin-Dufresne, Pierre, and Robert S. Goldstein. 2001. Do credit spreads reflect stationary leverage ratios? The Journal of Finance 56: 1929–57. [Google Scholar] [CrossRef]

- Consiglio, Andrea, and Stavros A. Zenios. 2015. The case for contingent convertible debt for sovereigns. The Wharton Financial Institutions Center 15-13: 1–29. [Google Scholar] [CrossRef]

- Crosbie, Peter, and Jeffrey Bohn. 2019. Modeling Default Risk. World Scientific Reference on Contingent Claims Analysis in Corporate Finance: Volume 2: Corporate Debt Valuation with CCA. Singapore: World Scientific, pp. 471–506. [Google Scholar]

- Duan, Jin-Chuan. 1994. Maximum likelihood estimation using price data of the derivative contract. Mathematical Finance 4: 155–67. [Google Scholar] [CrossRef]

- Flannery, Mark J. 2017. Stabilizing large financial institutions with contingent capital certificates. In The Most Important Concepts in Finance. Cheltenham: Edward Elgar Publishing, pp. 277–300. [Google Scholar]

- Forte, Santiago. 2011. Calibrating structural models: A new methodology based on stock and credit default swap data. Quantitative Finance 11: 1745–59. [Google Scholar] [CrossRef]

- Geske, Robert. 1979. The valuation of compound options. Journal of Financial Economics 7: 63–81. [Google Scholar] [CrossRef]

- Geske, Robert, Avanidhar Subrahmanyam, and Yi Zhou. 2016. Capital structure effects on the prices of equity call options. Journal of Financial Economics 121: 231–53. [Google Scholar] [CrossRef]

- Huang, Jing-Zhi, and Ming Huang. 2012. How much of the corporate-treasury yield spread is due to credit risk? The Review of Asset Pricing Studies 2: 153–202. [Google Scholar] [CrossRef]

- Hull, John C. 2018. Options, Futures and Other Derivatives. New York: Pearson. [Google Scholar]

- Hull, John C., and Alan D. White. 2000. Valuing credit default swaps I: No counterparty default risk. The Journal of Derivatives 8: 29–40. [Google Scholar] [CrossRef]

- Javadi, Siamak, Weiping Li, and Ali Nejadmalayeri. 2023. Contingent capital conversion under dual asset and equity jump–diffusions. International Review of Financial Analysis 89: 102798. [Google Scholar] [CrossRef]

- Lando, David. 2009. Credit Risk Modeling: Theory and Applications. Princeton: Princeton University Press. [Google Scholar]

- Leland, Hayne E. 1994. Corporate debt value, bond covenants, and optimal capital structure. The Journal of Finance 49: 1213–52. [Google Scholar] [CrossRef]

- Leland, Hayne E., and Klaus Bjerre Toft. 1996. Optimal capital structure, endogenous bankruptcy, and the term structure of credit spreads. The Journal of Finance 51: 987–1019. [Google Scholar] [CrossRef]

- Li, Jingya. 2015. Studies of Contingent Capital Bonds. Ph.D. thesis, University of Western Ontario, Princeton, NJ, USA. [Google Scholar]

- Longstaff, Francis A., and Eduardo S. Schwartz. 1995. A simple approach to valuing risky fixed and floating rate debt. The Journal of Finance 50: 789–819. [Google Scholar] [CrossRef]

- McDonald, Robert L. 2013. Contingent capital with a dual price trigger. Journal of Financial Stability 9: 230–41. [Google Scholar] [CrossRef]

- Merton, Robert C. 1973. Theory of rational option pricing. The Bell Journal of Economics and Management Science 4: 141–83. [Google Scholar] [CrossRef]

- Merton, Robert C. 1974. On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance 29: 449–70. [Google Scholar]

- Metzler, Adam. 2008. Multivariate First-Passage Models in Credit Risk. Ph.D. thesis, University of Waterloo, Waterloo, ON, Canada. [Google Scholar]

- Metzler, Adam, and R. Mark Reesor. 2015. Valuation and analysis of zero-coupon contingent capital bonds. Mathematics and Financial Economics 9: 85–109. [Google Scholar] [CrossRef]

- Oster, Philippe. 2020. Contingent convertible bond literature review: Making everything and nothing possible? Journal of Banking Regulation 21: 343–81. [Google Scholar] [CrossRef]

- Sundaresan, Suresh. 2013. A review of Merton’s model of the firm’s capital structure with its wide applications. Annual Review of Financial Economics 5: 21–41. [Google Scholar] [CrossRef]

- Sundaresan, Suresh, and Zhenyu Wang. 2015. On the design of contingent capital with a market trigger. The Journal of Finance 70: 881–920. [Google Scholar] [CrossRef]

- Sundaresan, Suresh, and Zhenyu Wang. 2023. Strategic Bank Liability Structure Under Capital Requirements. Management Science 69: 6349–68. [Google Scholar] [CrossRef]

- Tarashev, Nikola A. 2008. An empirical evaluation of structural credit-risk models. International Journal of Central Banking 4: 1–53. [Google Scholar] [CrossRef]

- Weiss, Lawrence A. 1990. Bankruptcy resolution: Direct costs and violation of priority of claims. Journal of Financial Economics 27: 285–314. [Google Scholar] [CrossRef]

- Zhou, Xinghua. 2018. Three Essays on Structural Models. Ph.D. thesis, University of Western Ontario, London, ON, Canada. [Google Scholar]

{kind=link}

{kind=link}

| Panel A: Capital Structure (in millions) | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| Deposits | 568,143 | 485,712 | 886,005 | 733,390 | 913,862 |

| Senior Debt | 221,338 | 122,563 | 439,064 | 263,546 | 383,741 |

| Junior Debt | 16,328 | 7574 | 25,948 | 22,917 | 35,786 |

| Total Debt (Senior + Junior) | 237,666 | 130,137 | 465,012 | 286,463 | 419,527 |

| Total Liabilities | 805,809 | 615,849 | 1,351,017 | 1,019,853 | 1,333,389 |

| Equity (Market Cap) | 61,363 | 47,175 | 145,741 | 83,658 | 129,521 |

| Total Assets | 867,172 | 663,024 | 1,496,758 | 1,103,511 | 1,462,910 |

| Panel B: Capital Structure by Proportion | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| Deposits/Total Assets | 65.52% | 73.26% | 59.19% | 66.46% | 62.47% |

| Senior Debt/Total Assets | 25.52% | 18.49% | 29.33% | 23.88% | 26.23% |

| Junior Debt/Total Assets | 1.88% | 1.14% | 1.73% | 2.08% | 2.45% |

| Equity/Total Assets | 7.08% | 7.12% | 9.74% | 7.58% | 8.85% |

| Panel C: Payout Ratios | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| Interest Rate of Deposits | 1.52% | 1.73% | 1.47% | 1.89% | 1.50% |

| Coupon Rate of Debts | 3.90% | 2.45% | 3.20% | 1.16% | 2.70% |

| Dividend Yield | 0.30% | 0.38% | 0.39% | 0.39% | 0.36% |

| Total Payout Ratio | 1.85% | 1.92% | 1.85% | 1.82% | 1.61% |

| Panel D: Volatility, Yield, Spread, Stock, and Option | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| Equity Volatility | 16.35% | 17.06% | 16.58% | 17.47% | 16.14% |

| Time-to-maturity of Liabilities (year) | 5.63 | 4.21 | 6.03 | 6.47 | 3.68 |

| Senior Debt Yield | 2.17% | 2.08% | 2.26% | 2.25% | 2.15% |

| Junior Debt Yield | 2.37% | 2.28% | 2.46% | 2.45% | 2.35% |

| CDS Spread | 0.56% | 0.47% | 0.60% | 0.73% | 0.33% |

| Stock Price (CAD) | 97.50 | 112.31 | 106.24 | 75.54 | 75.21 |

| Option Price (CAD) | 9.7 | 12.95 | 11.3 | 17.75 | 9.6 |

| Option Strike Price (CAD) | 90 | 100 | 96 | 58 | 66 |

| Option Maturity (year) | 0.96 | 0.55 | 0.55 | 0.55 | 0.55 |

| Panel A (Part I): Calibration Results for GBM (4 Equations)—Best Case | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| A–L ratio | 1.0762 | 1.0766 | 1.1079 | 1.0820 | 1.0971 |

| d | 1.0548 | 1.0257 | 1.0831 | 1.0514 | 1.0928 |

| 0.82% | 1.10% | 1.05% | 1.13% | 0.31% | |

| 93.43% | 98.70% | 93.56% | 89.74% | 95.78% | |

| 92.76% | 96.57% | 69.01% | 88.79% | 57.44% | |

| RSS (Error) | 1.73% | 1.00% | 3.61% | 0.00% | 2.00% |

| Equation (1) | Stock Price | Stock Price | Stock Price | Stock Price | Stock Price |

| Equation (2) | Equity Vol | Equity Vol | Equity Vol | Equity Vol | Equity Vol |

| Equation (3) | CDS Spread | Option Price | CDS Spread | CDS Spread | CDS Spread |

| Equation (4) | Option Price | Junior Yield | Option Price | Option Price | Senior Yield |

| Panel A (Part II): Calibration Results for GBM (4 Equations)—Worst Case | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| A–L ratio | 1.0762 | 1.0766 | 1.1079 | 1.0820 | 1.0971 |

| d | 1.0387 | 1.0683 | 1.0838 | 1.0653 | 1.0603 |

| 0.60% | 0.03% | 0.08% | 0.29% | 0.62% | |

| 60.06% | 71.44% | 73.40% | 60.09% | 60.00% | |

| 59.47% | 71.27% | 63.12% | 59.65% | 36.00% | |

| RSS (Error) | 51.52% | 40.32% | 51.28% | 17.29% | 32.54% |

| Equation (1) | CDS Spread | Stock Price | Equity Vol | CDS Spread | Stock Price |

| Equation (2) | Option Price | CDS Spread | CDS Spread | Option Price | Equity Vol |

| Equation (3) | Senior Yield | Senior Yield | Option Price | Senior Yield | Option Price |

| Equation (4) | Junior Yield | Junior Yield | Senior Yield | Junior Yield | Junior Yield |

| Panel B: Calibration Results for Jump-Diffusion | |||||

| Bank | BMO | CIBC | RBC | BNS | TD |

| A–L Ratio | 1.0762 | 1.0766 | 1.1079 | 1.0820 | 1.0971 |

| d | 1.0200 | 1.0100 | 1.0716 | 1.0403 | 1.0606 |

| 1.25% | 1.50% | 1.25% | 1.52% | 1.26% | |

| 86.67% | 78.33% | 86.67% | 86.63% | 90.00% | |

| 77.50% | 77.50% | 77.50% | 77.46% | 85.00% | |

| 0.01 | 0.10 | 0.10 | 0.10 | 0.0275 | |

| −1.00% | −1.00% | −1.00% | −0.99% | −0.10% | |

| 0.27% | 0.27% | 0.27% | 0.27% | 0.03% | |

| RSS (Error) | 30.9% | 24.31% | 5.20% | 6.93% | 18.92% |

| Panel A: OSFI Requirement | ||||||||||

| Ratio | BMO | CIBC | RBC | BNS | TD | |||||

| (1) * | (2) ** | (1) | (2) | (1) | (2) | (1) | (2) | (1) | (2) | |

| CET1 | 4.5% | 1.8% | 4.5% | 1.8% | 4.5% | 1.7% | 4.5% | 1.9% | 4.5% | 1.5% |

| Tier 1 | 6.0% | 2.4% | 6.0% | 2.3% | 6.0% | 2.3% | 6.0% | 2.5% | 6.0% | 2.1% |

| Total Capital | 8.0% | 3.1% | 8.0% | 3.1% | 8.0% | 3.0% | 8.0% | 3.3% | 8.0% | 2.7% |

| Ratio | BMO | CIBC | RBC | BNS | TD | |||||

| (1) | (2) | (1) | (2) | (1) | (2) | (1) | (2) | (1) | (2) | |

| CET1 | 11.4% | 4.5% | 11.6% | 4.5% | 12.1% | 4.6% | 11.1% | 4.6% | 12.1% | 4.1% |

| Tier 1 | 13.0% | 5.1% | 12.9% | 5.0% | 13.2% | 5.0% | 12.2% | 5.0% | 13.5% | 4.6% |

| Total Capital | 15.2% | 6.0% | 15.0% | 5.8% | 15.2% | 5.8% | 14.2% | 5.9% | 16.3% | 5.6% |

| Panel A: Calibration Results as Default Thresholds | |||||

| BMO | CIBC | RBC | BNS | TD | |

| Multiplier | 1.3044 | 1.2930 | 1.3132 | 1.3419 | 1.3224 |

| CoCo Loss at Conversion | 0.2334 | 0.2266 | 0.2385 | 0.2548 | 0.2438 |

| A–L Ratio | 1.0762 | 1.0766 | 1.1079 | 1.0820 | 1.0971 |

| Adjusted Default Threshold | 0.9993 | 0.9976 | 1.0510 | 1.0169 | 1.0321 |

| Conversion Threshold | 1.0316 | 1.0312 | 1.0520 | 1.0400 | 1.0383 |

| Adjusted Total Capital Ratio | 1.0598 | 1.0584 | 1.0577 | 1.0586 | 1.0557 |

| RSS (Error) | 6.3% | 0.00% | 5.66% | 10.49% | 8.54% |

| Panel B: CET1 Ratio as Default Thresholds | |||||

| BMO | CIBC | RBC | BNS | TD | |

| Multiplier | 1.3044 | 1.2930 | 1.3132 | 1.3419 | 1.3224 |

| CoCo Loss at Conversion | 0.2334 | 0.2266 | 0.2385 | 0.2548 | 0.2438 |

| A–L Ratio | 1.0762 | 1.0766 | 1.1079 | 1.0820 | 1.0971 |

| Adjusted CET1 Ratio (Default Threshold) | 1.0177 | 1.0175 | 1.0171 | 1.0186 | 1.0154 |

| Conversion Threshold | 1.0189 | 1.0287 | 1.0423 | 1.0401 | 1.0383 |

| Adjusted Total Capital Ratio | 1.0598 | 1.0584 | 1.0577 | 1.0586 | 1.0557 |

| RSS (Error) | 5.39% | 1.41% | 3.16% | 8.19% | 8.43% |

| Ratios | BMO | CIBC | RBC | BNS | TD |

|---|---|---|---|---|---|

| Minimum Required CET1 Ratio | 4.50% | 4.50% | 4.50% | 4.50% | 4.50% |

| Minimum Required Total Capital Ratio | 8.00% | 8.00% | 8.00% | 8.00% | 8.00% |

| Actual CET1 Ratio at Time Zero | 11.4% | 11.6% | 12.1% | 11.1% | 12.1% |

| Actual Total Capital Ratio at Time Zero | 15.2% | 15.0% | 15.2% | 14.2% | 16.3% |

| Conv. Threshold (1) | 7.90% | 8.90% | 13.40% | 9.60% | 11.20% |

| Conv. Threshold (2) | 4.80% | 8.20% | 11.00% | 9.60% | 11.20% |

| Panel A: Calibration Results as Default Thresholds | |||||

| BMO | CIBC | RBC | BNS | TD | |

| Senior debt yield (without CoCo) | 2.17% | 2.08% | 2.26% | 2.25% | 2.15% |

| Senior debt yield (with CoCo) | 1.81% | 1.87% | 1.96% | 1.99% | 1.78% |

| CDS spread (without CoCo) | 0.56% | 0.47% | 0.60% | 0.73% | 0.33% |

| CDS spread (with CoCo) | 0.04% | 0.10% | 0.19% | 0.22% | 0.02% |

| Junior debt yield (without CoCo) | 2.37% | 2.28% | 2.46% | 2.45% | 2.35% |

| CoCo par yield (with CoCo) | 2.62% | 2.90% | 2.12% | 3.09% | 1.85% |

| Cost of debt (without CoCo) | 1.88% | 1.83% | 1.94% | 1.90% | 1.89% |

| Cost of debt (with CoCo) | 1.79% | 1.80% | 1.83% | 1.85% | 1.77% |

| BMO | CIBC | RBC | BNS | TD | |

| Senior debt yield (without CoCo) | 2.17% | 2.08% | 2.26% | 2.25% | 2.15% |

| Senior debt yield (with CoCo) | 1.80% | 1.97% | 1.76% | 1.83% | 1.76% |

| CDS spread (without CoCo) | 0.56% | 0.47% | 0.60% | 0.73% | 0.33% |

| CDS spread (with CoCo) | 0.03% | 0.18% | 0.00% | 0.06% | 0.00% |

| Junior debt yield (without CoCo) | 2.37% | 2.28% | 2.46% | 2.45% | 2.35% |

| CoCo par yield (with CoCo) | 2.12% | 2.73% | 1.95% | 3.13% | 1.86% |

| Cost of debt (without CoCo) | 1.88% | 1.83% | 1.94% | 1.90% | 1.89% |

| Cost of debt (with CoCo) | 1.78% | 1.81% | 1.76% | 1.81% | 1.76% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Meng, D.; Metzler, A.; Reesor, R.M. Capital Structure Models and Contingent Convertible Securities. Risks 2024, 12, 55. https://doi.org/10.3390/risks12030055

Meng D, Metzler A, Reesor RM. Capital Structure Models and Contingent Convertible Securities. Risks. 2024; 12(3):55. https://doi.org/10.3390/risks12030055

Chicago/Turabian StyleMeng, Di, Adam Metzler, and R. Mark Reesor. 2024. "Capital Structure Models and Contingent Convertible Securities" Risks 12, no. 3: 55. https://doi.org/10.3390/risks12030055

APA StyleMeng, D., Metzler, A., & Reesor, R. M. (2024). Capital Structure Models and Contingent Convertible Securities. Risks, 12(3), 55. https://doi.org/10.3390/risks12030055