The Sustainability Factor: How Much Do Pension Expenditures Improve in Spain?

,

,  and

and

Abstract

:1. Introduction

- (a)

- Those that have adopted a rigid system, since they have changed the starting parameters to other fixed values, although these changes happen over long transitional periods.

- (b)

- Those that have adopted a flexible system, since the values of the parameters depend on some reference or variable external to the system. These are called automatic resetting mechanisms.

2. Automatic Adjustment Mechanisms

3. The Sustainability Factor of the Spanish Pension System

- (a)

- The sustainability factor (SF) modifies the starting amount of the retirement pension benefit as life expectancy changes5.

- (b)

- The pension revaluation index adjusts the revaluation of all pensions based on the financial health of the system.

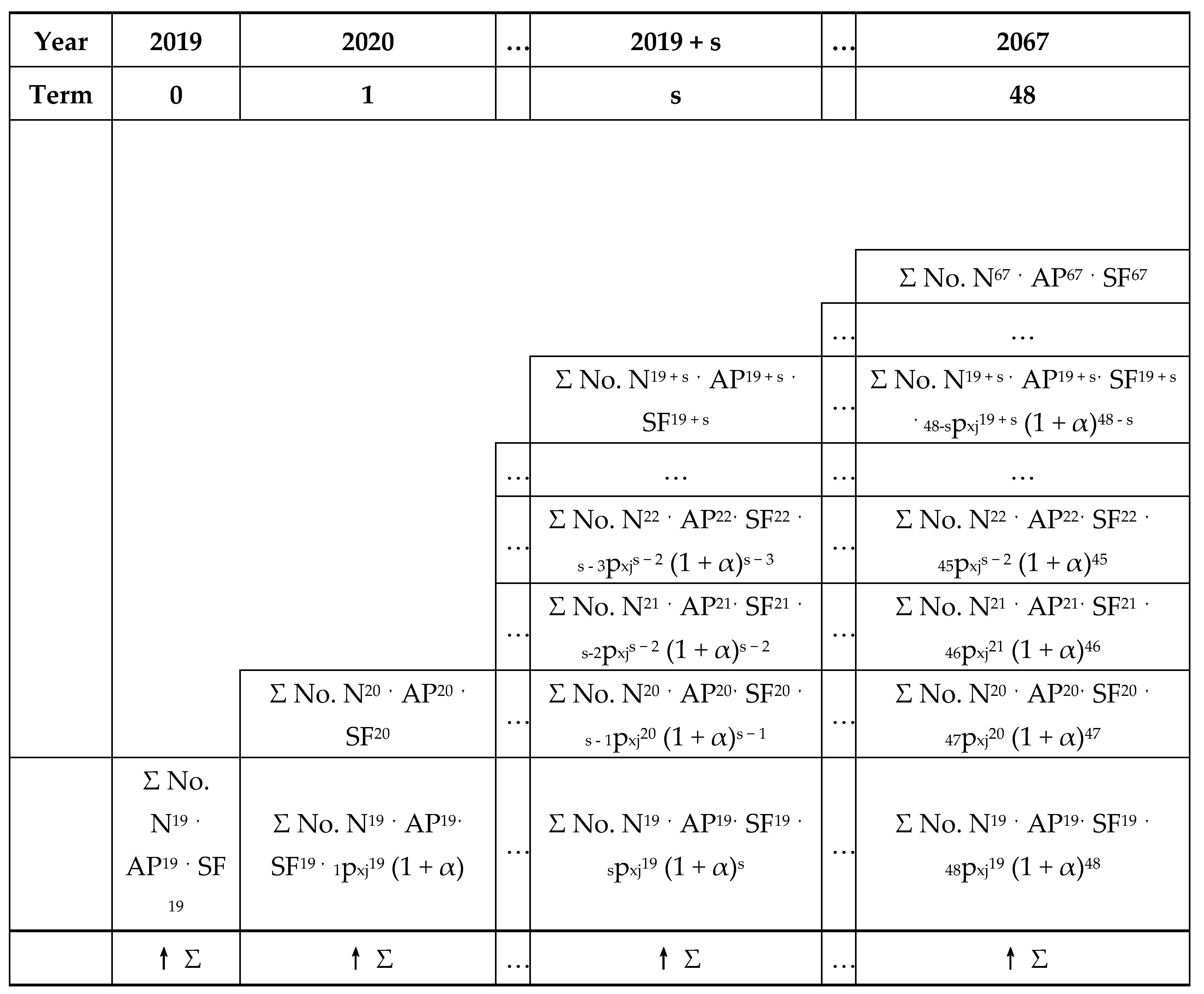

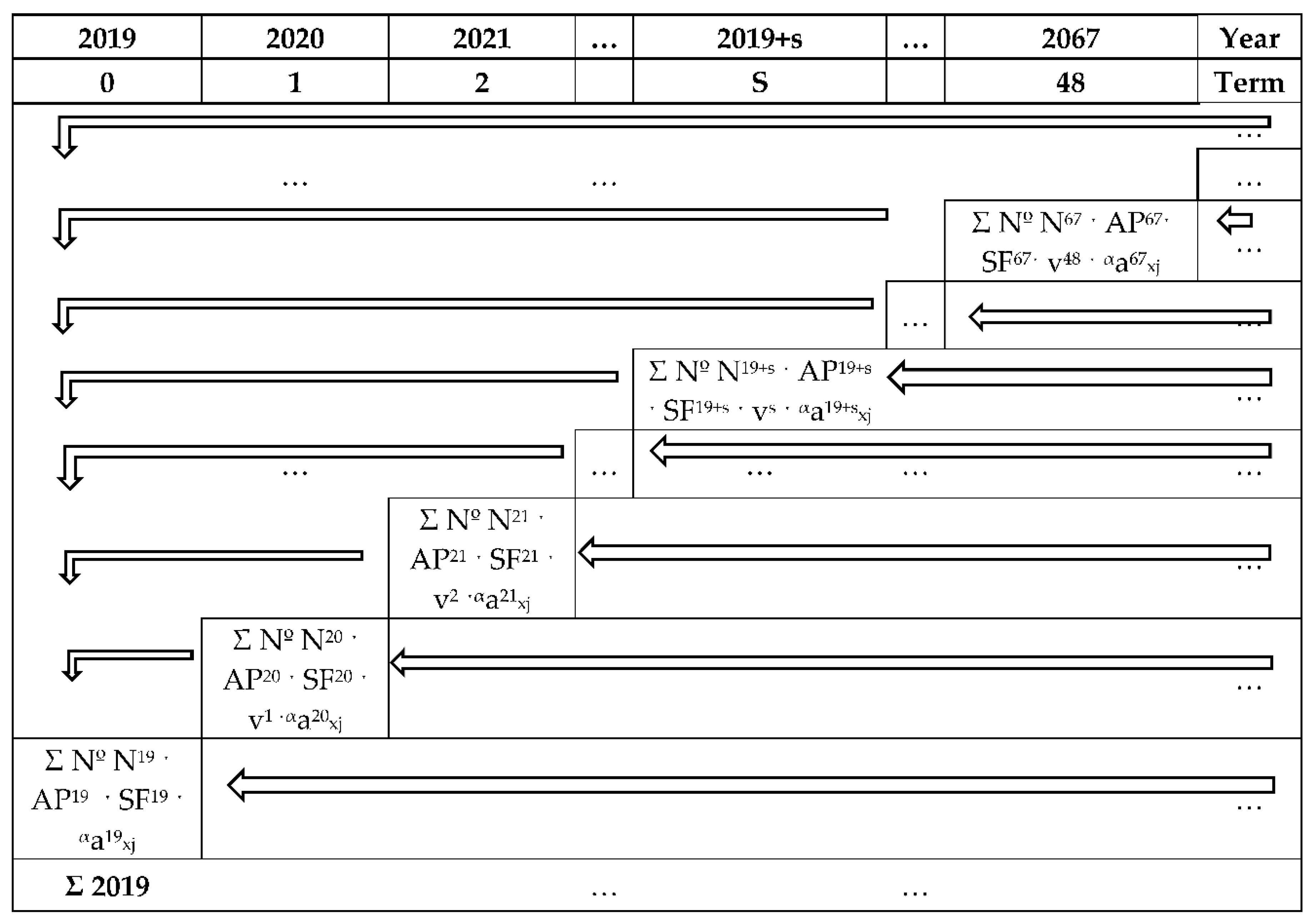

4. Financial-Actuarial Model with Microdata to Simulate Retirement Pension Expenditures

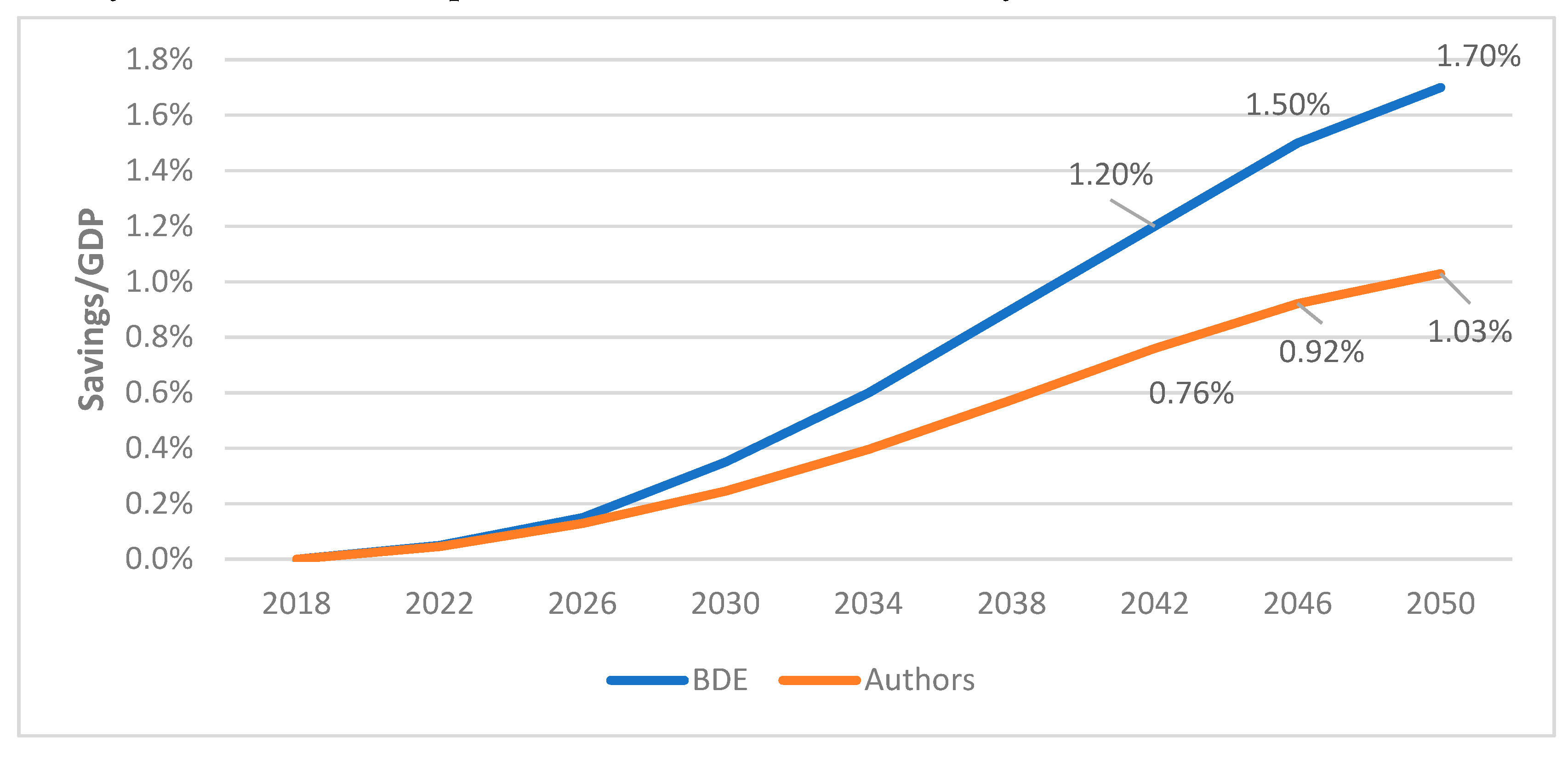

+...+ Σ No. N20 · AP20 · SF20 · s−1pxj20 · (1 + α)s − 1 + Σ No. N19 · AP19 · SF19 · spxj19 · (1 + α)s.

- -

- In terms of cash, although this is the model that has been used by multiple researchers10, we intended to improve upon it by introducing both aggregate and microdata information. We did this because of the different levels of information that we can extract from each of these bases.

- -

- The accrual model, which requires the calculation of the present actuarial value of pension expenditure, gives us a complementary view of the information on the cash balance. The box model does not collect information on everything that will happen with each cohort but rather what happens each year. Analyzing expenditure from the actuarial point of view involves

- Having a global perspective of what happens with a cohort or group of individuals during the entire contributory period.

- Knowing the effect on the increase in the implicit debt of the pension system due to not applying the SF.

- Knowing the amount that would have to be allocated annually to meet the new commitments arising from not applying the SF.

5. Working Hypothesis for the Application of the Financial-Actuarial Model, with Microdata, to Generate Pension Expenditure

- ✓

- Instrument 1. Microdata: Microdata were used, obtained from the MCVL2018, with which it was possible to generate information on the distribution of both the new retirement pensions and the total number of retirement pensions. This allows us to know, for each age and gender, the number of pensions and amount of their benefits, which is essential to apply the actuarial methods.

- ✓

- Instrument 2. Aggregate data: Real aggregate data on the total number and average amount of retirement pensions have also been used. This information obtained from Social Security, and the data from the MCVL2018 allow us to obtain the results for the population.

- ✓

- Instrument 3. Actuarial method. An actuarial method has been used, employing financial factors, survival probabilities, and annuities, which are necessary to adequately project the evolution of the different cohorts of retirees, as well as to correctly quantify them.

- ✓

- Instrument 4. Financial method. A financial or arithmetic projection method has been applied, complementing all the information obtained from the previous instruments.

5.1. Projection of the Number of New Retirement Pensions in the Period 2018–2067

- 1st

- The number is based on the variation of the number of pensions provided by the Social Security estimates until 2050. For the years 2051 to 2067, it has been assumed that the average variation will stay between the 2045 value and the 2050 value. These data were adjusted according to the growth in the number of retirement pensions between 2016 and 2019, which is 50% higher than the total pensions: 1.76% for retirement compared to 1.17%. In addition, within retirement, they were adjusted again by gender to keep growth between the 2016 and 2019 levels, which is 1.08% for men and 3.01% for women.

- 2nd

- The distribution by age and gender of the total existing retirement pensions in the year 2018 was obtained from the MCVL2018 regarding the total pensions of the system (Table 3).

- 3rd

- The next step is to apply the survival probabilities by age and gender to the previous distribution. The difference between the number of pensions of survivors from the previous year and the number of pensions estimated in sub–paragraph 1 will give us the number of new pensions that year.

- 4th

- Next, assuming that all the retirement pension withdrawals come from death14, the number of new pensions calculated in sub-paragraph 3 is added to the pensioner group, always maintaining the same age and gender distribution as for the new pensions for 2018. This process is repeated for the next few years.

5.2. Projection of the Starting Retirement Pension Benefit in the Period 2018–2067

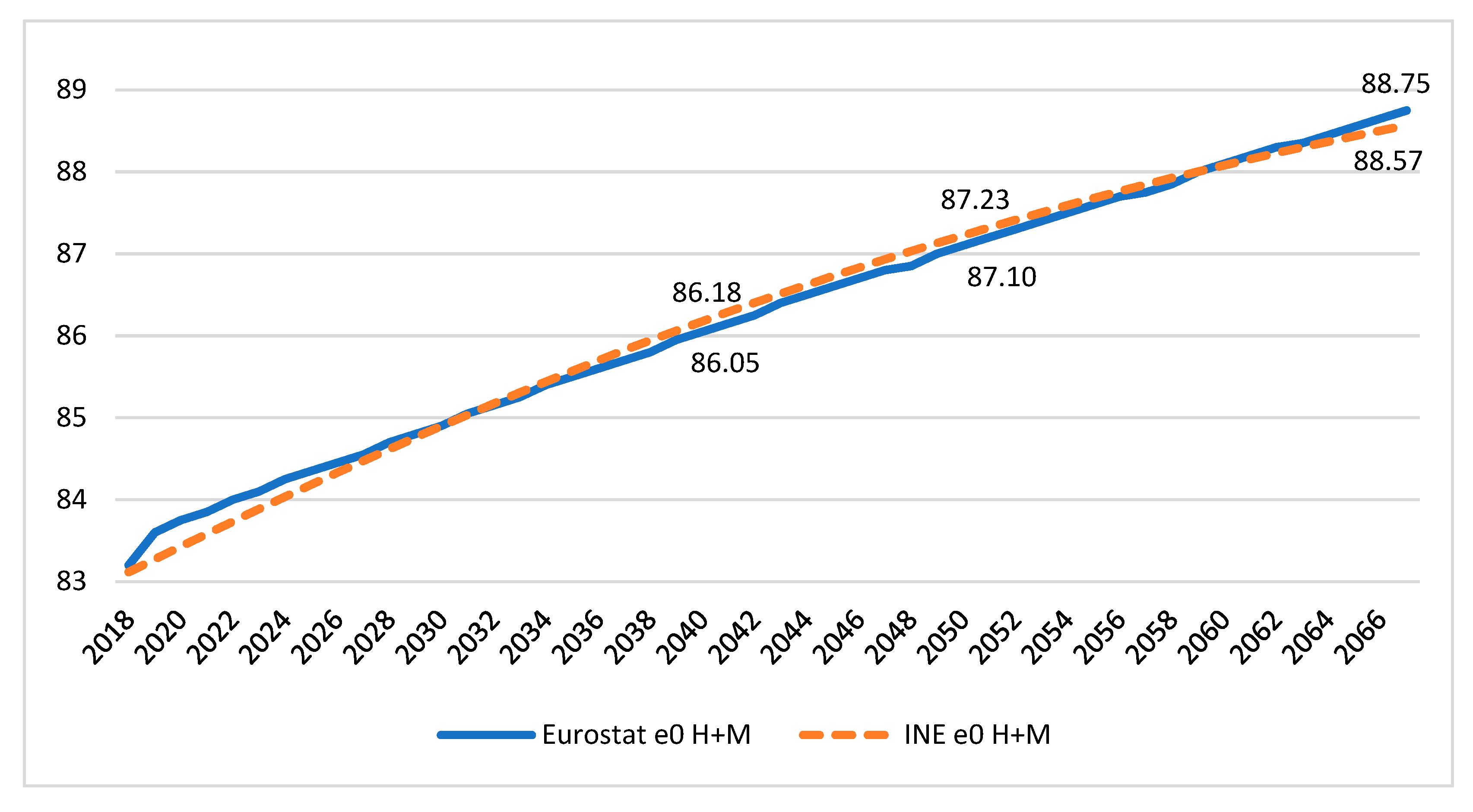

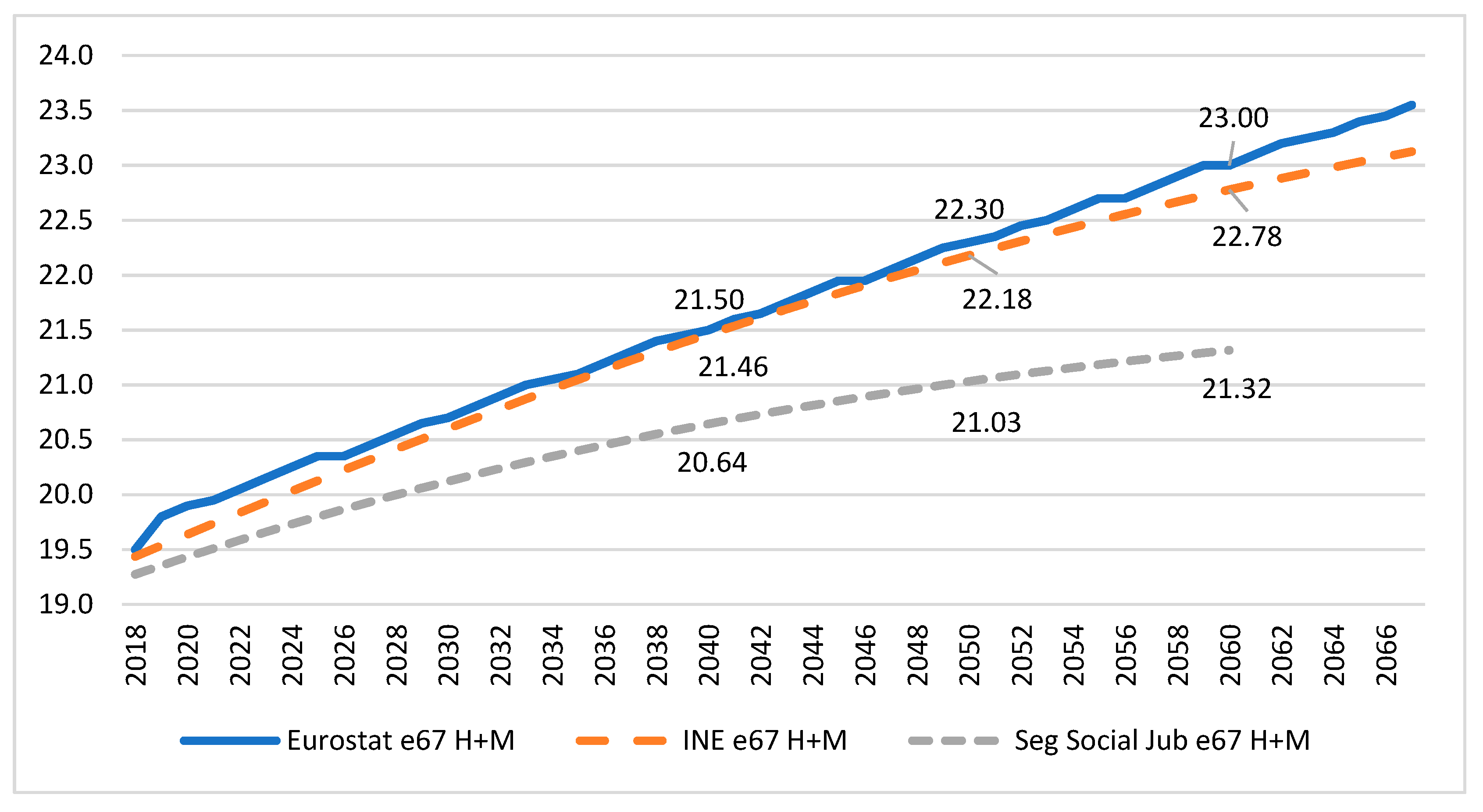

5.3. Mortality Tables

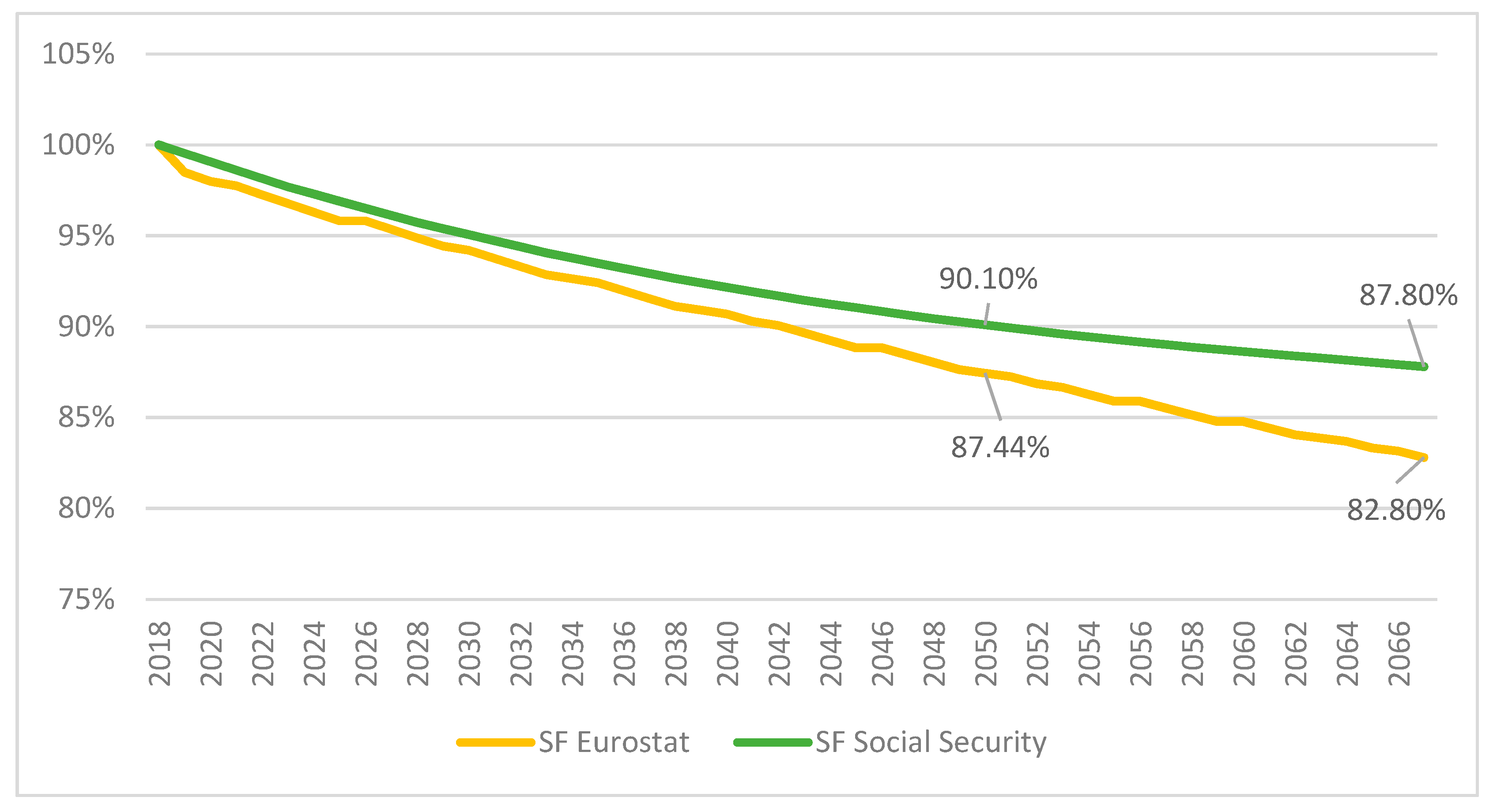

5.4. Sustainability Factor

5.5. Other Working Hypotheses

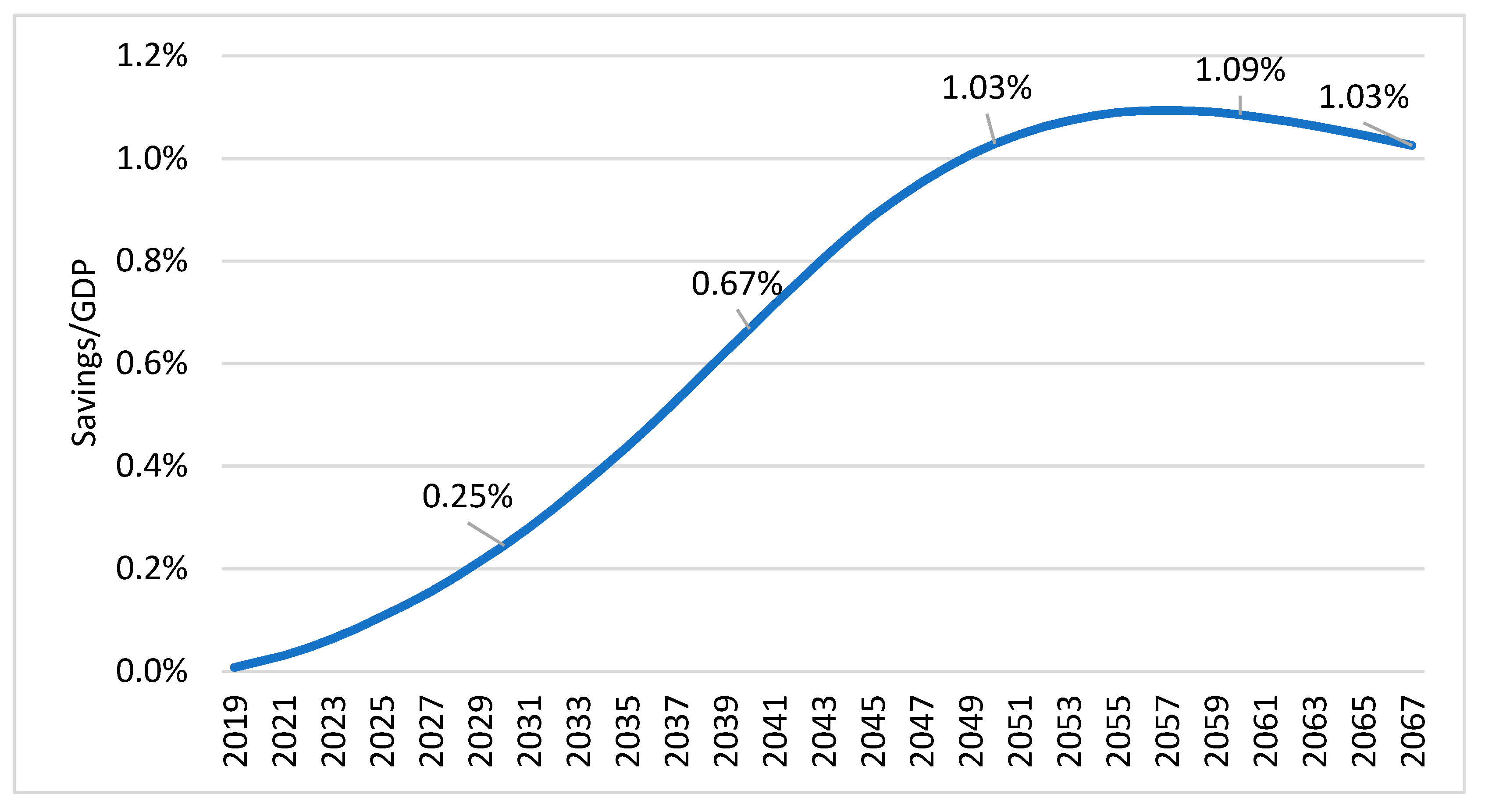

6. Savings in the Annual Expenditure on Retirement Pensions with the Application of the Sustainability Factor

6.1. Estimation of Savings in Annual Retirement Pension Expenditure in Cash Terms

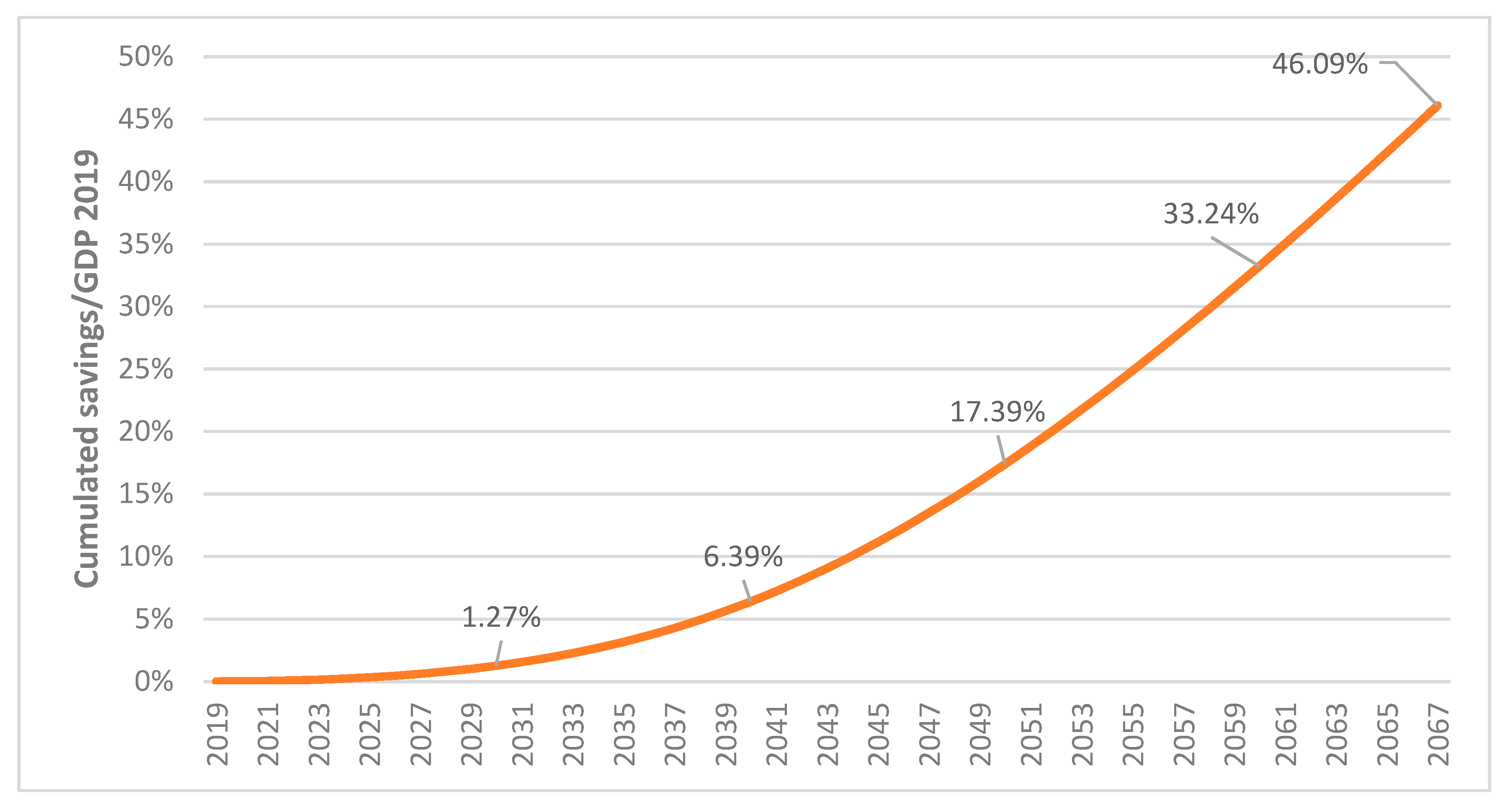

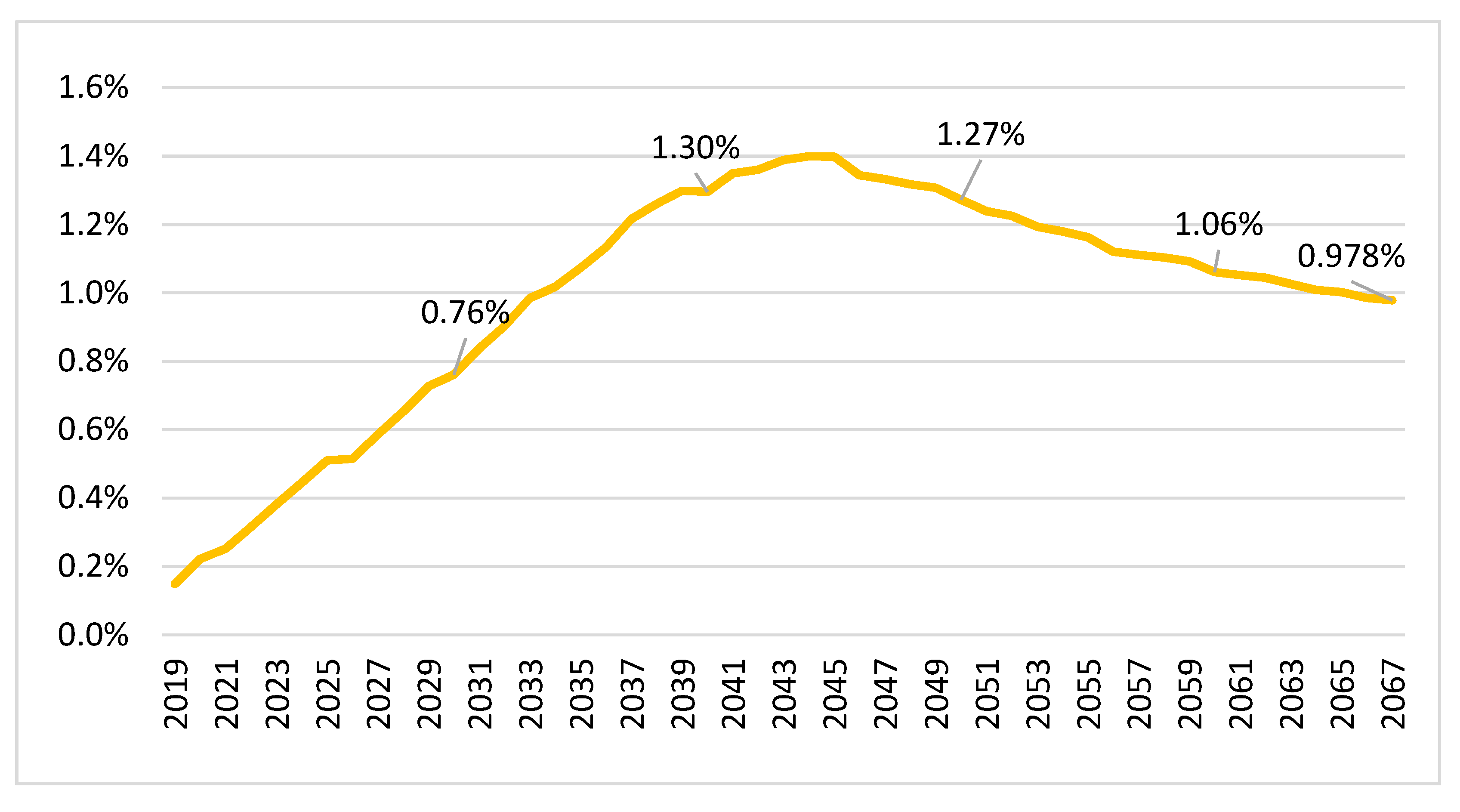

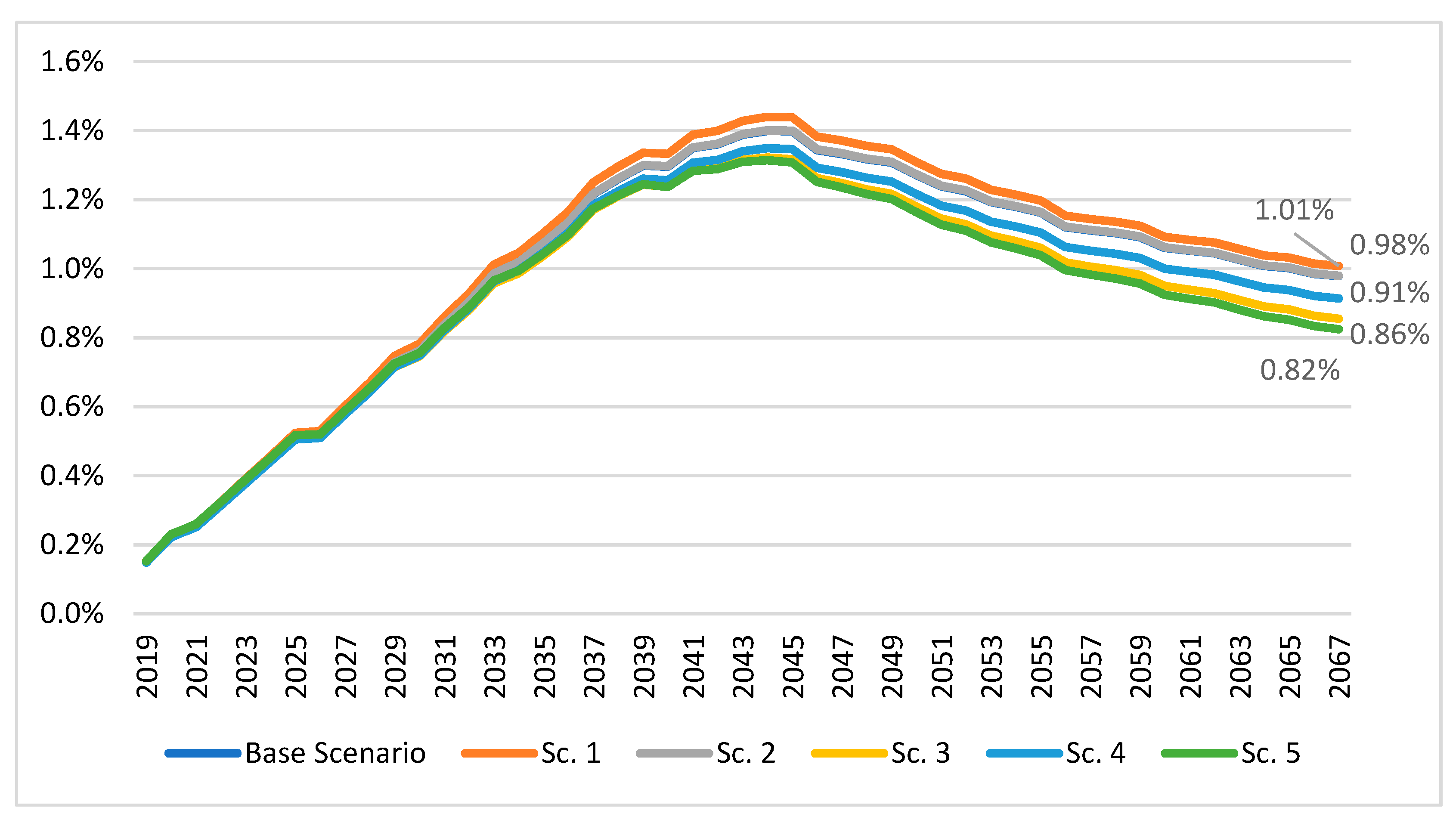

6.2. Estimation of Savings in Expenditures on Retirement Pensions in Terms of Accrual

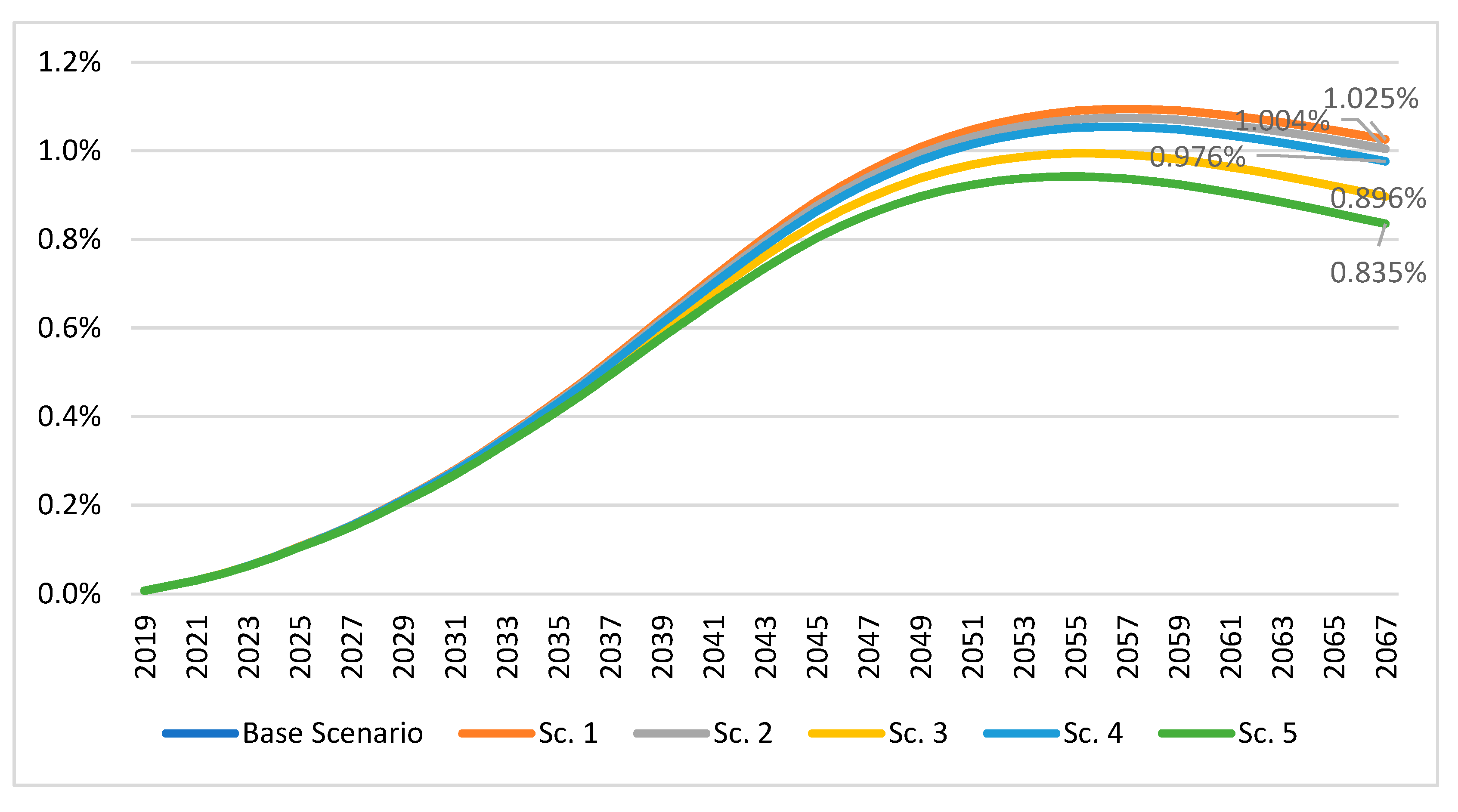

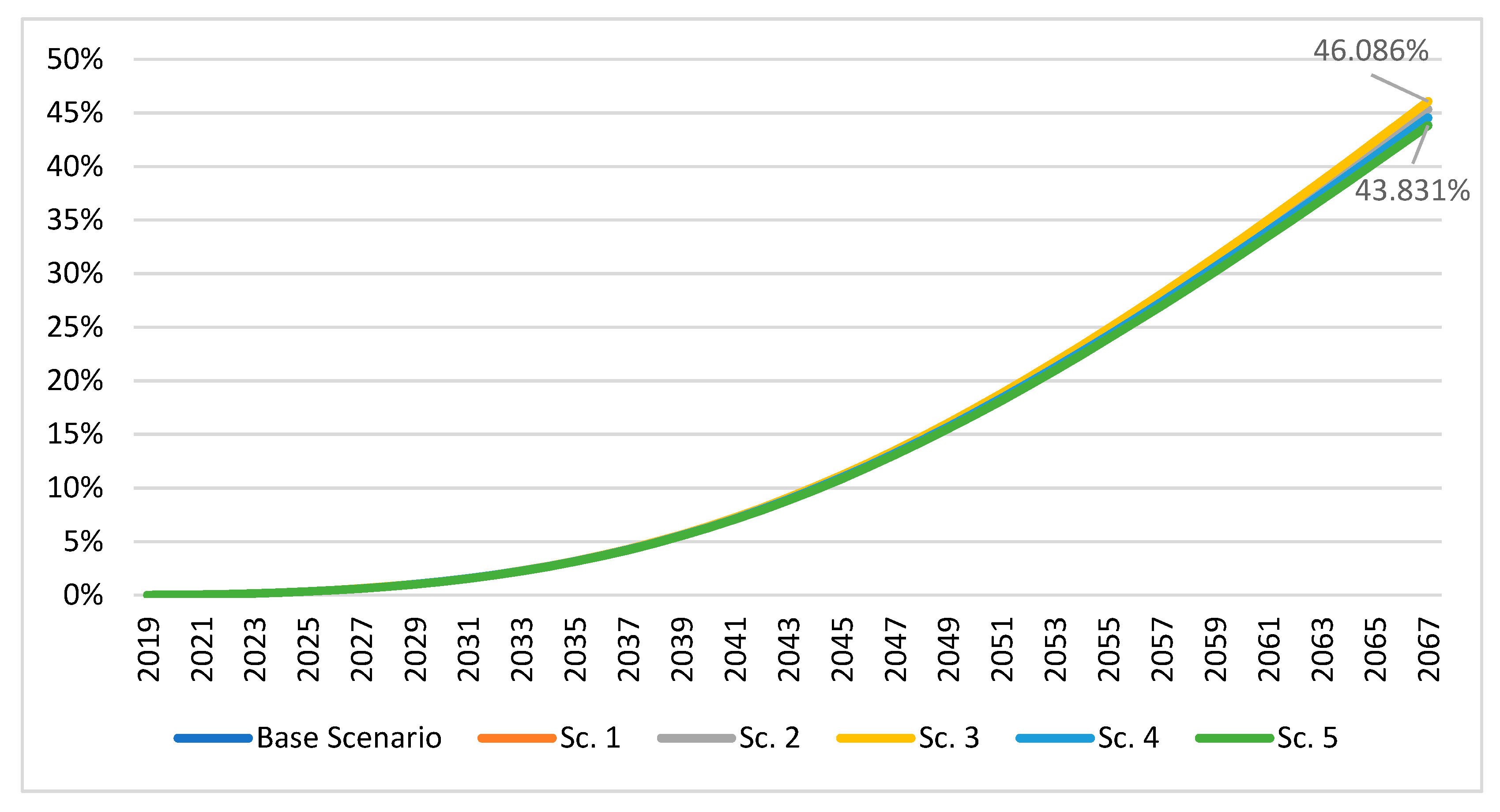

7. Sensitivity Analysis of the Working Hypotheses and the Effect of Delaying the Application of the Sustainability Factor

7.1. Modification of the Baseline Scenario

7.2. Delay in Applying the Sustainability Factor

8. Conclusions

- (a)

- Microdata were used, obtained from the MCVL2018, with which we generated information on both new registrations of retirement pensions (new pensions) and on the total retirement pensions, by age and by gender.

- (b)

- Real aggregate data from the pension system on the total number of retirement pensions and their average benefit amount were used, which allowed complete extraction of the data without loss of information.

- (c)

- An actuarial method was used, with financial factors, survival probabilities, and annuities, which are essential to adequately project the evolution of the different cohorts of retirees, as well as to correctly value them quantitative terms.

- (d)

- A projection using financial methods was applied, complementing all the information with that obtained from the previous instruments.

- (a)

- One, a significant savings in spending, which would either increase the sustainability of the system or allow the savings to be allocated to improve the situation of those receiving the fewest benefits.

- (b)

- Two, an increase in the intergenerational equity of the pension system by assigning individuals with the same work careers the same total sum in pensions, regardless of their year of retirement.

Author Contributions

Funding

Conflicts of Interest

References

- AIReF. 2019. Spanish Independent Authority for Fiscal Responsibility. Opinión Sobre la Sostenibilidad del Sistema de Seguridad Social. Opinión 1/19. Available online: https://www.airef.es/wp-content/uploads/2019/OPINIONES/190109_Opinion_Seguridad-Social.pdf (accessed on 29 November 2020).

- Alda, Mercedes, Isabel Marco, and Adrián Marzo. 2018. La reforma del sistema público de pensiones español: El factor de sostenibilidad. Revista de Finanzas y Política Económica 10: 25–43. [Google Scholar] [CrossRef] [Green Version]

- Antn, Sorin Gabriel, Elena Toader, and Bogdan Firtescu. 2016. Does Risk Management with Derivatives Improve the Financial Performance of Pension Funds? Empirical Evidence from Romania. Transformations in Business & Economics 15: 565–79. [Google Scholar]

- Barea, José, Maximino Carpio, and Eugenio Domingo. 1996. Escenarios de Evolución del Gasto Público en Pensiones y Desempleo en el Horizonte 2020. Bilbao: Fundación BBV Documenta. [Google Scholar]

- Carone, Giuseppe, Per Eckefeldt, Luigi Giamboni, Veli Laine, and Stephanie Pamies. 2016. Pension Reforms in the EU since the Early 2000’s: Achievements and Challenges Ahead. European Economy Discussion Paper, 42. Available online: http://ec.europa.eu/economy_finance/publications/eedp/pdf/dp042_en.pdf (accessed on 29 November 2020).

- Committee of Experts. 2013. Informe del Comite de Expertos Sobre el Factor de Sostenibilidad del Sistema Público de Pensiones. Available online: http://www1.seg-social.es/ActivaInternet/groups/public/documents/rev_anexo/rev_032187.pdf (accessed on 29 November 2020).

- Da-Rocha, José-Marıa, and Francisco Xavier Lores. 2005. ¿Es Urgente Reformar la Seguridad Social. RGEA Research Group in Economic Analisis, Working Paper Series; Vigo: Vigo University. [Google Scholar]

- Devesa-Carpio, José-Enrique, and Mar Devesa-Carpio. 2010. The cost and actuarial imbalance of pay-as-you-go systems: The case of Spain. Journal of Economic Policy Reform 13: 259–76. [Google Scholar] [CrossRef]

- Devesa, José Enrique, Mar Devesa, Robert Meneu, Juan José Alonso, Inmaculada Domínguez, Borja Encinas, Francisco Escribano, Pablo Moya, Isabel Pardo, and Raúl del Pozo. 2016. La Revolución de la Longevidad y su Influencia en las Necesidades de Financiación de los Mayores. Madrid: Fundación Edad & Vida, Available online: https://www.vidacaixa.es/documents/51066/91055/estudio.pdf/4247f979-a9ac-05a9-ac42-3d319ea8ada7 (accessed on 29 November 2020).

- Díaz-Giménez, Javier. 2014. Las Pensiones Europeas y sus Reformas Recientes. Documento de Trabajo nº 7. In Instituto BBVA de Pensiones. Madrid. Available online: https://www.jubilaciondefuturo.es/recursos/doc/pensiones/20131003/posts/2015-7-las-pensiones-europeas-y-sus-reformas-recientes-esp.pdf (accessed on 29 November 2020).

- Díaz-Giménez, Javier, and Julián Díaz-Saavedra. 2017. The future of spanish pensions. Journal of Pension Economics & Finance 16: 233–65. [Google Scholar]

- Duran, Almudena. 2007. La Muestra Continua de Vidas Laborales de la Seguridad Social. Revista del Ministerio de Trabajo y Asuntos Sociales 1: 231–240. [Google Scholar]

- Economic Policy Committee, and Social Protection Committee from the European Commission. 2020. Joint Paper on Pensions 2019. Available online: https://europa.eu/epc/system/files/2020-01/Joint-Paper-on-Pensions-2019.pdf (accessed on 29 November 2020).

- Encinas-Goenechea, Borja, Robert Meneu-Gaya, and María de la Cruz del Río. 2020. The Public Pension Systems and the Economic Crisis. In Economic Challenges of Pension Systems. A Sustainability and International Management Perspective. Edited by Marta Peris-Ortiz, José Alvarez-Garcia, Inmaculada Dominguez-Fabian and Pierre Devolder. Cham: Springer, pp. 57–80. [Google Scholar] [CrossRef]

- European Commission. 2012. Libro Blanco, Agenda Para una Pensiones Adecuadas, Seguras y Sostenibles. Bruselas, COM (2012) 55 Final, February 16. Available online: http://eurlex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2012:0055:FIN:ES:PDF (accessed on 29 November 2020).

- European Commission. 2018. The 2018 Ageing Report. Economic and Budgetary Projections for the 28 EU Member States (2016–2070). European Economy, Institutional Paper 079. Available online: https://ec.europa.eu/info/sites/info/files/economy-finance/ip079_en.pdf (accessed on 29 November 2020).

- Eurostat Database. 2020. Available online: https://ec.europa.eu/eurostat/data/database (accessed on 29 November 2020).

- Herce, José Antonio A., and Víctor Perez-Diaz, eds. 1995. La Reforma del Sistema Público de Pensiones en España. Servicio de Estudios de La Caixa, Colección Estudios e Informes, nº 4. Available online: https://www.caixabankresearch.com/sites/default/files/content/file/2016/09/ee04_esp.pdf (accessed on 29 November 2020).

- Hernandez de Cos, Pablo. 2020. Retos del Envejecimiento de la Población. Desayuno de Trabajo con la Junta de Gobierno del Instituto de Actuarios Españoles. Madrid. Available online: https://www.bde.es/f/webbde/GAP/Secciones/SalaPrensa/IntervencionesPublicas/Gobernador/Arc/Fic/hdc270120.pdf (accessed on 29 November 2020).

- Hernández de Cos, Pablo, Juan F. Jimeno Serrano, and Roberto Ramos. 2017. El sistema público de pensiones en España: Situación actual, retos y alternativas de reforma. In Documentos Ocasionales. Banco de España. Nº 1701. Available online: https://www.bde.es/f/webbde/SES/Secciones/Publicaciones/PublicacionesSeriadas/DocumentosOcasionales/17/Fich/do1701.pdf (accessed on 29 November 2020).

- Hoyo, Lao. 2014. El factor de sostenibilidad el sistema público de pensiones y su entrada en vigor. El factor de equidad intergeneracional ajustado a la edad de acceso a la jubilación. Economía Española y Protección Social, 75–117. Available online: file:///C:/Users/USUARIO/Downloads/EEYPS%20VI%20-%202014%20-%203.pdf (accessed on 29 November 2020).

- Lapuerta, Irene. 2010. Claves para el trabajo con la Muestra Continua de Vidas Laborales. In DemoSoc Working Paper. nº 2010-37. Barcelona: Universidad Pompeu Fabra. [Google Scholar]

- Law 27. 2011. de 1 de Agosto, Sobre Actualización, Adecuación y Modernización del Sistema de Seguridad Socia. Published in BOE Num. 184 of August, 2. Available online: https://www.boe.es/eli/es/l/2011/08/01/27 (accessed on 29 November 2020).

- Law 23. 2013. de 23 de Diciembre, Reguladora del Factor de Sostenibilidad y del Índice de Revalorización del Sistema de Pensiones de la Seguridad Social. Published in BOE Num. 309 of December, 26. Available online: https://www.boe.es/eli/es/l/2013/12/23/23 (accessed on 29 November 2020).

- Spanish Continuous Sample of Working Lives. 2018. Available online: http://www.seg-social.es/wps/portal/wss/internet/EstadisticasPresupuestosEstudios/Estadisticas/EST211 (accessed on 29 November 2020).

- Gaya, Robert Meneu, José Enrique Devesa Carpio, Mar Devesa Carpio, Amparo Nagore García, Inmaculada Domínguez Fabián, and Borja Encinas Goenechea. 2013. El factor de sostenibilidad: Diseños alternativos y valoración financiero-actuarial de sus efectos sobre los parámetros del sistema. Economía Española y Protección Social 63–96. Available online: file:///C:/Users/USUARIO/Downloads/EEYPS%20V%20-%202013%20-%203.pdf (accessed on 29 November 2020).

- Pérez Alonso, María Antonia. 2016. El Factor de Sostenibilidad en España. Lex Social 6: 145–74. [Google Scholar]

- Real Decreto-Law 5. 2013. de 15 de marzo, de Medidas Para Favorecer la Continuidad de la vida Laboral de los Trabajadores de Mayor edad y Promover el Envejecimiento Activo. Published in BOE Num. de 16/03/2013. Available online: https://www.boe.es/eli/es/rdl/2013/03/15/5/con (accessed on 29 November 2020).

- Sanchez Martin, Alfonso. 2014. The automatic adjustment of pension expenditures in Spain: An evaluation of the 2013 pension reform. In Banco de España. Documento de Trabajo nº 1420. Available online: https://www.bde.es/f/webbde/SES/Secciones/Publicaciones/PublicacionesSeriadas/DocumentosTrabajo/14/Fich/dt1420e.pdf (accessed on 29 November 2020).

- Serrano, Felipe, Miguel A. García, and Carlos Bravo. 2004. El Sistema Español de Pensiones. Un Proyecto viable Desde un Enfoque Economico. Barcelona: Ariel. [Google Scholar]

- Social Protection Comitee from the European Commision. 2016. Review of Recent Social Policy Reforms: 2015 Report of the Social Protection Committee. Available online: https://op.europa.eu/en/publication-detail/-/publication/3aff6199-ca44-11e5-a4b5-01aa75ed71a1/language-en (accessed on 29 November 2020).

| 1 | According to the most recent Eurostat data (Eurostat Database 2020), from years 2002 to 2018, the life expectancy at 65 years of age in the EU increased by 2.2 years and in Spain, one of the longest-living countries, by 2.5 years. This means that with each passing year, life expectancy grew by 1.65 and 1.88 months, respectively. In addition, according to the European Commission (2018), this increase in longevity will continue in the coming decades from 18 years for the EU as a whole in 2016 to 23.4 years in 2070. |

| 2 | Another type of reforms of the three-pillar system would be reforms focused on an additional private pillar and the different structure of the pension funds in Central and Eastern Europe (Anton et al. 2016). |

| 3 | A more in-depth study on these reforms can be found in Díaz-Giménez (2014), Social Protection Comitee from the European Commission (2016), Carone et al. (2016), European Commission (2018) and Encinas et al. (2020). |

| 4 | For more details on the characteristics of these automatic resetting mechanisms, see Gaya et al. (2013), Carone et al. (2016), European Commission (2018), and Economic Policy Committee and Social Protection Committee from the European Commission (2020). |

| 5 | In fact, this automatic mechanism was introduced in the reform approved in 2011 (Law 27 2011), but it did not specify which parameter of the system would be affected by changes in life expectancy. |

| 6 | Later, we will present the valuation data of Hernández de Cos et al. (2017) and AIReF (2019), although both have some drawbacks. |

| 7 | The Continuous Work Lives Sample (MCVL) is a random, non-stratified sample with information from more than 1.2 million individuals, representing 4% of all those who were associated with Social Security during a given year. This database is published annually by Social Security. For more information on MCVL, please refer to: Duran (2007), Lapuerta (2010) and Pérez Alonso (2016). |

| 8 | See Gaya et al. (2013) for more on this topic. |

| 9 | Although the current legislation includes the name sustainability factor, in the work (Committee of Experts 2013) that gave rise to regulatory development, the name used was intergenerational equity factor. |

| 10 | Among other authors they can be read Herce and Perez-Diaz (1995), Barea et al. (1996), Serrano et al. (2004), Da-Rocha and Lores (2005), Devesa-Carpio and Devesa-Carpio (2010). |

| 11 | It was not updated actuarially because we have been able to generate the data on new retirement rates, that is, how many individuals are retiring in 2020. |

| 12 | The rest of the benefits are not taken into account because, according to regulations in effect, the SF only applies to retirement pensions. |

| 13 | Calculations until 2067 are done because this spans a broad period of time that includes the end of the impact of the Baby Boom generation. |

| 14 | Actually, pension withdrawals can occur, according to Social Security data itself, for three reasons: “death”, “age or term”, and “other causes”. In the case of retirement, in March 2020, only 6.87% of total withdrawals were not death-related. This rate in July 2020 is 15.7%, which suggests that these variations are due to the effect of COVID-19. |

| 15 | Instead of the annualized five-year data set by the regulations. |

| 16 | For GDP growth in the base scenario, data from the Ageing Report (European Commission 2018) have been used. |

| 17 | On 28 September 2020, AIReF modified its demographic projections and updated its estimate of the sustainability factor, indicating that its 2023 application will mean an additional saving of 0.9 points of GDP in 2050, a figure somewhat higher than the result that we obtained. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Automatic Balancing Mechanism | Pension Amount Linked to Life Expectancy | Legal Retirement Age Linked to Life Expectancy | Introduction Year of the Automatic Resetting Mechanism |

|---|---|---|---|---|

| Italy | X | X | 1995 and 2010 | |

| Latvia | X | 1996 | ||

| Sweden | X | X | 1998 and 2001 | |

| Poland | X | 1999 | ||

| France | X | 2003 | ||

| Germany | X | 2004 | ||

| Finland | X | X | 2005 and 2015 | |

| Portugal | X | X | 2007 and 2013 | |

| Greece | X | 2010 | ||

| Denmark | X | 2011 | ||

| Spain | X | X | 2011 and 2013 | |

| The Netherlands | X | 2012 | ||

| Cyprus | X | 2012 | ||

| Slovakia | X | 2012 | ||

| Lithuania | X | 2016 | ||

| Estonia | X | 2018 |

| Variable | All | Men | Women | % Men | % Women | Men/Women |

|---|---|---|---|---|---|---|

| Number | 12,245 | 7014 | 5231 | 57.28% | 42.72% | 1.341 |

| Average retirement age | 64.44 | 64.24 | 64.80 | 99.69% | 100.56% | 0.991 |

| Average annual amount | 18,562 | 20,491 | 15,976 | 110.39% | 86.07% | 1.283 |

| Variable | All | Men | Women | % Men | % Women | Men/Women |

|---|---|---|---|---|---|---|

| Number | 240,215 | 148,599 | 91,616 | 61.86% | 38.14% | 1.62 |

| Average retirement age | 73.86 | 73.89 | 73.78 | 100.04% | 99.89% | 1.002 |

| Average annual amount | 15,485 | 17,858 | 11,636 | 115.32% | 75.14% | 1.53 |

| Parameter | Baseline Scenario |

|---|---|

| Interest rate | 2% |

| Inflation | 1.6% |

| α = Pension revaluation | 1.6% |

| GDP growth since 202116 | Ageing Report |

| β = Variation in the average benefit of new retirement pensions | 1.411% |

| Mortality tables | Eurostat |

| Parameter | Baseline Scenario | Scenario 1 | Scenario 2 | Scenario 3 | Scenario 4 | Scenario 5 |

|---|---|---|---|---|---|---|

| Interest rate | 2% | 1.8% | 2% | 2% | 2% | 1.8% |

| Inflation | 1.6% | 1.6% | 1.6% | 1.6% | 1.6% | 1.6% |

| α = Pension revaluation | 1.6% | 1.6% | 1.44% | 1.6% | 1.6% | 1.44% |

| GDP growth since 2021 | Ageing Report | Ageing Report | Ageing Report | 110% Ageing Report | Ageing Report | 110% Ageing Report |

| β = Variation in the average pension benefit of new retirement registrations | 1.411% | 1.411% | 1.411% | 1.411% | 1.27% | 1.27% |

| Mortality tables | Eurostat | Eurostat | Eurostat | Eurostat | Eurostat | Eurostat |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Devesa, E.; Devesa, M.; Dominguez-Fabián, I.; Encinas, B.; Meneu, R. The Sustainability Factor: How Much Do Pension Expenditures Improve in Spain? Risks 2020, 8, 134. https://doi.org/10.3390/risks8040134

Devesa E, Devesa M, Dominguez-Fabián I, Encinas B, Meneu R. The Sustainability Factor: How Much Do Pension Expenditures Improve in Spain? Risks. 2020; 8(4):134. https://doi.org/10.3390/risks8040134

Chicago/Turabian StyleDevesa, Enrique, Mar Devesa, Inmaculada Dominguez-Fabián, Borja Encinas, and Robert Meneu. 2020. "The Sustainability Factor: How Much Do Pension Expenditures Improve in Spain?" Risks 8, no. 4: 134. https://doi.org/10.3390/risks8040134

APA StyleDevesa, E., Devesa, M., Dominguez-Fabián, I., Encinas, B., & Meneu, R. (2020). The Sustainability Factor: How Much Do Pension Expenditures Improve in Spain? Risks, 8(4), 134. https://doi.org/10.3390/risks8040134