1. Introduction

In the last several decades, various stochastic volatility models have been developed in the literature to explain the volatility smile and heavy tails of return distribution as widely observed in the financial market; see, for example,

Heston (

1993);

Hull and White (

1987);

Lewis (

2000); and

Stein and Stein (

1991). Among them, a non-affine model with a mean reverting structure called the 3/2 stochastic volatility model

Lewis (

2000) enjoys empirical support in the bond and stock market by previous works, such as

Ahn and Gao (

1999);

Bakshi et al. (

2006); and

Jones (

2003). Effort has been made under the 3/2 stochastic volatility in derivative pricing problems such as

Carr and Sun (

2007);

Drimus (

2012); and

Yuen et al. (

2015). It seems, however, that little attention has been paid to portfolio selection problems under

Markowitz (

1952) mean-variance criterion.

The single-period asset allocation theory under the mean-variance criterion is first introduced by the seminal paper

Markowitz (

1952). Thereafter, there has been increasing attention on extensions and applications of Markowitz’s work. Two milestones are the work of

Li and Ng (

2000) and

Zhou and Li (

2000) that generalize Markowitz’s work to a multi-period and continuous-time setting by using embedding techniques. In

Zhou and Li (

2000), they assume that all the market parameters are deterministic functions or constants. To extend the results to more realistic models with random parameters, on the assumption that the return rate, volatility, and risk premium are all bounded stochastic processes, the backward stochastic differential equation (BSDE) approach is introduced by

Lim and Zhou (

2002) to solve a mean-variance problem in a complete market. From then on, many papers work on the mean-variance portfolio selection problem under various financial models by using the BSDE approach.

Chiu and Wong (

2011) consider the problem where asset prices are cointegrated.

Shen et al. (

2014) investigate the same problem under a constant elasticity of variance model by assuming that the risk premium process satisfies an exponential integrability.

Zhang and Chen (

2016) extend the results in

Shen et al. (

2014) by further incorporating a liability process.

Shen and Zeng (

2015) study the optimal investment-reinsurance problem for a mean-variance insurer in an incomplete market where the risk premium process is proportional to a Markovian, affine-form, and square-root process, and a modified locally square-integrable optimal strategy is derived by imposing an exponential integrability of order 2 on the risk premium process. Under similar conditions considered in

Shen and Zeng (

2015), a mean-variance problem under the Heston model with a liability process and a financial derivative is considered in

Li et al. (

2018). Other relevant works on mean-variance portfolio selection problems by applying not only the BSDE approach, but also other approaches (for example, the dynamic programming approach and the martingale approach

Pliska (

1986)) include

Bielecki et al. (

2005);

Chang (

2015);

Ferland and Watier (

2010);

Han and Wong (

2020);

Lv et al. (

2016);

Pan and Xiao (

2017);

Pan et al. (

2018);

Peng and Chen (

2020a,

2020b);

Shen (

2015,

2020);

Shen et al. (

2020);

Tian et al. (

2021); and

Yu (

2013).

The literature mentioned above under Markowitz’s paradigm, however, shares one characteristic, that is, all deals with pre-committed strategies

Strotz (

1956). The resulting optimal strategy always depends on the initial wealth level, and thus is called time-inconsistent. Recently, the time-consistent mean-variance portfolio selection problem has received considerable attention. To tackle the time-inconsistency,

Basak and Chabakauri (

2010) derive a time-consistent strategy which is determined by applying a backward recursion starting from the terminal date.

Björk et al. (

2017) develop a game theoretical approach under Markovian settings which essentially studies the subgame-perfect Nash equilibrium, and they derive the equilibrium strategy and equilibrium value function by solving an extended Hamilton–Jacobi–Bellman (HJB) equation. Along this approach, previous works include

Li et al. (

2012,

2015);

Lin and Qian (

2016); and

Zhu and Li (

2020), to name but only a few. Alternatively,

Pedersen and Peskir (

2017) introduce the dynamically optimal approach to investigate the time-inconsistency of mean-variance problems. They overcome the time-inconsistency by recomputing the statically optimal (pre-committed) strategy during the investment period, and they can therefore obtain dynamically optimal (time-consistent) strategies by solving infinitely many optimization problems.

Motivated by these aspects, we consider a dynamic mean-variance portfolio selection problem within the framework developed in

Pedersen and Peskir (

2017) in a complete market with two primitive assets: a risk-free asset and a stock with 3/2 stochastic volatility. In particular, the market is completed by fixing a perfectly negative correlation between the stock price and the volatility. To make the problem analytically tractable, the return rate of the stock is a constant so that the risk premium process is linear in the reciprocal of volatility process. We adopt the BSDE approach to solve this problem. The Lagrange multiplier is first applied to transform the mean-variance problem into an unconstrained optimization problem. By making an assumption on model parameters, the uniqueness and existence of solution to a special type BSDE

Bender and Kohlmann (

2000) is established. We then solve the BSDE explicitly and obtain the optimal strategy in a closed-form for the unconstrained optimization problem. Furthermore, we derive the analytic expression of the statically optimal strategy of the mean-variance portfolio selection problem by the Lagrange duality theorem. Finally, by solving the statically optimal strategy at each time, we obtain the dynamically optimal strategy which is shown to keep the corresponding wealth process strictly below the target (expected terminal wealth) before the terminal time. To summarize, this paper has main contributions in three aspects: (1) We make an assumption on the model parameters instead of on the risk premium process. This assumption guarantees the existence and uniqueness of solutions to the BSDEs. (2) We manage to derive the square-integrable optimal strategy instead of the locally square-integrable optimal strategy and verify the admissibility. (3) We provide both the static and dynamic optimality.

The rest of this paper is organized as follows.

Section 2 formulates the financial market and the portfolio selection problem. In

Section 3, we derive the explicit solutions to the BSDEs as well as the closed-from expression of the optimal investment strategy of the unconstrained problem.

Section 4 presents the static and dynamic optimality of the mean-variance portfolio selection problem. In

Section 5, we provide numerical examples to present the efficient frontier under the statically optimal strategy and illustrate the differences between the two optimal controlled wealth processes.

Section 6 concludes the paper.

2. Formulation of the Problem

Let be a finite horizon and be a complete probability space which carries a one-dimensional standard Brownian motion . The right-continuous, -complete filtration is generated by the Brownian motion W.

We consider a market where two primitive assets—one risk-free asset and one stock—are available to the investor. The price of the risk-free asset

B solves

with

at time

fixed and given, where

stands for the interest rate. The price of the stock follows

with

at time

. The return rate of the stock price

is a constant and

is the stochastic variance of the stock price described by a 3/2 model (see, for example,

Lewis (

2000)):

with the initial value of

at time

, where three parameters,

, and

, are all assumed to be positive. We hereby put the minus sign in front of

in (

2) to emphasize the assumption that the dynamics of the stock price

and the volatility

are perfectly negative correlated.

We shall consider Markov controls

denoting the wealth invested in the stock at time

, and such a deterministic function

is called a feedback control law. We assume that there are no transaction costs in the trading as well as other restrictions. The investor wishes to create a self-financing portfolio of the risk-free asset

B and the stock

S dynamically. Thus, the controlled wealth process

of the investor can be described by the system of SDEs below.

with

at time

. We let

denote the probability measure with initial value

at time

.

Definition 1. Given any fixed , if for any , it holds that

- 1.

,

- 2.

,

then the (Markovian) strategy u is called admissible. We denote by the set of admissible portfolio strategies.

We are first interested in determining an admissible strategy that solves the following portfolio problem:

Definition 2. The mean-variance portfolio problem is an optimization problem denoted bywhere ξ is a fixed and given constant playing the financial role of a target. The corresponding value function is denoted by . Remark 1. Here, we impose , in line with previous studies such as Lim and Zhou (2002); Shen and Zeng (2015), and Shen et al. (2014). Otherwise, the investor can simply take the risk-free strategy over which dominates any other admissible strategy. As a result of the quadratic nonlinearity of the variance operator, problem (

4) falls outside of Bellman’s principle. Denote by

the optimal strategy in problem (

4) which refers to the

static optimality (refer to Definition 1 in

Pedersen and Peskir (

2017)) and is relative to the initial position

. The investor might not be committed to the statically optimal strategy

chosen at the very initial position

during the following investment period

. Therefore, we shall also consider a dynamic formulation of problem (

4). Here, we opt for the framework developed in

Pedersen and Peskir (

2017). We now review the definition of

dynamic optimality in problem (

4) for the readers’ convenience.

Definition 3. For a triple fixed and given, we call a Makrov strategy dynamically optimal in problem (4), if for every and every strategy with and , there is a Markov strategy w satisfying and such that The dynamically optimal strategy

is essentially derived by solving the statically optimal strategy

at each time and implementing it in an infinitesimally small period of time, which in turn implies that we shall first address problem (

4) in the sense of static optimality so as to derive the dynamic optimality.

We observe that problem (

4) is, in fact, a convex optimization problem with linear constraint

. Thus, we can handle the constraint by introducing a Lagrange multiplier

, and define the following Lagrangian:

Then, the Lagrangian duality theorem (see, for example,

Luenberger (

1968)) indicates that we can derive the static optimality

in problem (

4) by solving the following equivalent min-max stochastic control problem:

This shows that we can solve problem (

6) with two steps, of which the first step is to solve the unconstrained stochastic optimization problem with respect to

given a fixed

and the second step is to solve the static optimization problem with respect to the Lagrange multiplier

. Therefore, we can first address the following unconstrained quadratic-loss minimization problem:

with

fixed and given.

3. Solution to the Unconstrained Problem

In this section, we opt for the BSDE approach so as to solve problem (

7) above. Before formulating the main results in this section, we make the following notations to facilitate the discussions below. For any

-valued,

-adapted stochastic process

, a continuous process

associated with

is defined by

. Let

be a generic constant, we denote by

: the space of

-adapted,

-valued stochastic processes

f satisfying

: the space of

-adapted,

-valued stochastic processes

f satisfying

the space of

-adapted,

-valued stochastic processes

f satisfying

Therefore, we have the following Banach space:

with the norm

.

In addition, we introduce

It can be easily checked that due to . The following standing assumption is imposed on the model parameters throughout the paper:

Assumption 1. .

Remark 2. It follows from Lemma 5 below that is strictly increasing in T. In particular, when , . This indicates the feasibility of Assumption 1. Moreover, Assumption 1 is crucial to guarantee that three BSDEs—(9), (12), and (17)—admit unique solutions and the statically optimal strategy (30) is admissible. The following linear BSDE of

is considered so as to solve problem (

7):

Clearly, due to the randomness and unboundedness of the driver of (

9), this linear BSDE is without the uniform Lipschitz continuity with respect to both

and

. Thus, BSDE (

9) is out of scope of

EI Karoui et al. (

1997). Nevertheless, we observe that BSDE (

9) follows a stochastic Lipschitz continuity which is first proposed in

Bender and Kohlmann (

2000). To proceed, some useful results on the BSDE with the stochastic Lipschitz continuity adapted from Definition 2 and Theorem 3 in

Bender and Kohlmann (

2000) are presented below.

Definition 4. We call a pair standard data for the BSDE of :if the following four conditions hold: - 1.

There exist two -valued, -adapted stochastic processes and such that We refer to this inequality as the stochastic Lipschitz continuity.

- 2.

There exists a positive constant satisfying .

- 3.

The terminal condition ζ satisfies in which β is a positive constant.

- 4.

.

Lemma 1. The BSDE of admits a unique solution if is standard data for a sufficiently large β, in particular, for . Before adapting the above results to establish the uniqueness and existence of the solution to BSDE (

9), we recall the following useful result from Theorem 5.1 in

Zeng and Taksar (

2013).

Lemma 2. Suppose the process follows the Cox–Ingersoll–Ross (CIR) model:where and σ are positive constants. Then, we have Lemma 3. Assume Assumption 1 holds, then there is a constant such that the unique solution with to BSDE (9) exists. Proof. Let

and

. Denote in this case the non-negative

-adapted process

by

and accordingly, define the increasing process

by

We then have

where the positive constant

is independent of

. By Itô’s lemma, we then have the following dynamics of the reciprocal of the variance process (

2):

which is a CIR process. It follows from Lemma 2 that if

then we have

Indeed, when Assumption 1 holds, there exists a constant

such that

, and the driver and the terminal condition of BSDE (

9) then constitute standard data. Finally, by Lemma 1 above, we see that a unique solution

to BSDE (

9) with

and

exists. □

In what follows, we shall give the explicit expression of the unique solution

of BSDE (

9).

Lemma 4. Assume Assumption 1 holds, then the unique solution of BSDE (9) has the following explicit expression:for , where , and and are solutions to the following system of ODEs: Proof. We first introduce the likelihood process

from the dynamics

Similar to the reasoning in Lemma 3, it can be easily verified from Assumption 1 above that

That is, the Novikov’s condition is satisfied for

. Thus,

is a uniformly integrable martingale under

measure and we can define an equivalent probability measure

on

through the Radon–Nikodym derivative

From the Girsanov’s theorem, Brownian motions under

and

are related to each other through

and we can rewrite (

9) under the

-measure as follows:

We see that the driver of BSDE (

12) again satisfies the stochastic Lipschitz continuity with, in this case,

for any

fixed and given and

such that using Hölder’s inequality we have for some

where

is constant-independent of

, the second equality follows from the fact that

is a

martingale due to Assumption 1, and the last strict inequality is due to Assumption 1. This shows that the terminal condition and the driver of BSDE (

12) constitute standard data. Then, by Lemma 1 above, the BSDE (

12) admits a unique solution

satisfying

with some

and

. Moreover, we see that under

measure

This shows that

is a local martingale under measure

. By the Burkholder–Davis–Gundy inequality and Hölder’s inequality, we then find that

where the positive constant

might vary between lines; the equality follows from the fact that

is a

martingale due to Assumption 1, and the last strict inequality is due to Assumption 1 and

. This shows that

is, in fact, a uniformly integrable martingale under

measure (refer to Corollary 5.17 in

Le Gall (

2016)). Upon noticing the boundary condition that

, we have the expectational form for

below.

Denote by

where

is the expectation at time

such that

under

-measure. Due to the Markovian structure of the variance process

with respect to

, we can obviously rewrite

as follows:

Note that the variance process

has

-dynamics:

Suppose the deterministic function

, then applying the Feynman–Kac theorem yields the following PDE governing function

g:

We conjecture that

g admits the following exponential expression:

with boundary condition

. Its derivatives are given by

Substituting (

14) into (

13) yields

The arbitrariness of

in turn leads to the system of ODEs (

11) as claimed above. Applying Itô’s lemma to

, we obtain

by the uniqueness result of BSDE (

9). □

Lemma 5. Assume Assumption 1 holds, then the explicit solutions of the ODE system (11) arewhere and Δ are given in (8). Moreover, function is strictly decreasing in t. Proof. By reformulating the Riccati ODE of

, we have

where

and

are given in (

8) above. After some tedious calculations upon considering

, we obtain (

15). Integrating both sides of ODE of

from

t to

T upon considering the boundary condition

gives (16). Furthermore, differentiating (

15) with respect to

t yields

□

Denote by

the reciprocal process of

. Then, a direct application of Itô’s lemma to

yields the backward stochastic Riccati equation (BSRE) of

below.

where

. As

given in (

10) is the unique solution of BSDE (

9), from the relationship of

and

, we see that BSRE (

17) admits a unique solution as well.

Lemma 6. Assume Assumption 1 holds, then the unique solution of BSRE (17) iswith and given in (15) and (16), respectively. Proof. The Equation (

18) can be directly derived from the relationship of

and

above. □

We now define a Doléans-Dade exponential

of

by

In the next lemma, we shall study the integrablity of

which will be useful when we verify the admissibility of optimal strategy (

20) below.

Lemma 7. Assume Assumption 1 holds, then the Doléans–Dade exponential (19) satisfies Proof. We know that the following equation of

k

admits two positive solutions

for any given constant

, where the first solution satisfies

. In particular, when

, we have

. Using Assumption 1, Lemma 5, and the reasoning given in the proof of Lemma 3 above, we see that

This completes the proof. □

To end this section, we shall relate the optimal Markovian strategy and the corresponding value function of problem (

7) to the solution

of BSRE (

17).

Proposition 1. Assume Assumption 1 holds, then for fixed and given, the optimal (Markovian) strategy of problem (7) isfor . The corresponding value function is The controlled wealth process evolves aswhere is given in (19). Moreover, the optimal strategy belongs to . Proof. Using Itô’s lemma to

, we obtain

Furthermore, applying Itô’s lemma to

yields

We observe that the stochastic integral on the right-hand side of (

23) is a local martingale, and thus we can define stopping times

as follows:

such that

,

almost surely as

. We integrate (

23) from

to

and take expectations on both sides of (

23):

where

. From the definition of function

in Lemma 4 above, we see that

for any

,

-a.s. Moreover, in view of Definition 1, we have

for

. As a result of the Lebesgue’s dominated convergence theorem and the monotone convergence theorem working on (

24), then we have

Upon considering explicit expressions of

and

(

18), we obtain the optimal Markov strategy (

20) and the value function (

21) for problem (

7).

Substituting

(

20) into the wealth process (

3), we obtain

A direction application of Itô’s lemma to

then yields the controlled wealth process

(

22).

In the following, we show that the optimal strategy

(

20) is admissible. For this, we first show that

Indeed, from Assumption 1 and Lemma 7 above we find that

where

is a constant that differs between lines and

. This shows that the second condition in Definition 1 that

is satisfied by Jensen’s inequality. In view of (

26), we further find that the first condition in Definition 1 that

holds as well as

where

is a constant that differs between lines and last strict inequality comes from (

26) and the fact that

is a CIR process (see the proof of Lemma 3 above) with finite second moment

at time

which is continuous in

t (see, for example,

Cox et al. (

1985)). These results show that the optimal strategy

(

20) is admissible. □

4. Static and Dynamic Optimality of the Problem

In this section, we derive the static and dynamic optimality of problem (

4) by exploiting the results above. In regard to the static optimality of problem (

4), it now suffices to maximize the following optimization problem with respect to the Lagrange multiplier

in view of (

5) and (

6) above:

Reformulating (

27) in terms of a quadratic functional over

, we find that the value function of problem (

4) can be obtained from

Upon considering the exponential expression of function

given in Lemma 4 above, the right-hand side of (

28) is then a quadratic function of

with strictly negative leading coefficient. Therefore, to the right-hand side of (

28) the maximum is uniquely attained at

Theorem 1. Assume Assumption 1 holds, then for given and fixed such that , the statically optimal (Makrovian) strategy of problem (4) isfor , where functions and are given in (15) and (16). The corresponding value function is The controlled wealth process is given bywhere is given in (19). Moreover, the statically optimal strategy belongs to . Proof. Substituting (

29) into (

28) gives the value function (

31). Replacing the constant

in (

20) and (

22) with

yields the statically optimal strategy (

30) and the wealth process (

32), respectively. In view of the proof in Proposition 1 above, it is obvious that the statically optimal strategy

(

30) is admissible. □

As discussed in

Section 2, the statically optimal strategy

(

30) derived in Theorem 1 relies on the initial value

. This implies that once the investor arrives at a new position

at later times, the statically optimal strategy

determined at the initial position would be sub-optimal. Now, we give the dynamically optimal strategy

of problem (

4) within the framework developed in

Pedersen and Peskir (

2017).

Theorem 2. Assume Assumption 1 holds, then for given and fixed such that , the dynamically optimal (Markovian) strategy of problem (4) for is The corresponding controlled wealth process issatisfying for . Proof. To derive a candidate for the dynamic optimality

over

, we identify

with

t,

with

x, and

with

v in the statically optimal strategy given in (

30). We then immediately find a candidate of the dynamically optimal strategy

In what follows, we show that this candidate (

35) is indeed dynamically optimal in problem (

4). To see this, we take any other admissible control

such that

and

, and we set

under the measure

. We note from (

30) with

replaced by

that

, and thus we have

for any

. Then, by continuity of

and

w, there exists a ball

such that

for any

when

is small enough and satisfies

. We observe from (

25) that

is, in fact, the unique continuous function such that the minimum within the expectation on the right-hand side of (

25) (with

and

in place of

and

, respectively) is attained up to probability one. Therefore, we can set exiting time

, and we see that for

where

is a fixed positive constant. Now, from (

25) with

and

in place of

and

, respectively, we find that

where

is a constant at position

, and the strict inequality makes use of the fact that

as the pair

has continuous sample paths with probability one under

measure. From (

36) we see that

This shows that for any

, the candidate

(

35) is the dynamically optimal (Markovian) strategy for problem (

4).

We substitute

(

35) into the controlled wealth process (

3) and denote the corresponding wealth process by

. Using Itô’s lemma to

yields

We then obtain the closed-form expression of

by solving the linear SDE (

37):

where

. From the definition of

and (

38), we conclude that

for

. Finally, the corresponding wealth process

(

34) follows from (

38). □

5. Numerical Examples

In this section, numerical examples are provided to analyze the impact of different parameters on the efficient frontier when the wealth process is controlled by the statically optimal strategy as well as to illustrate the differences between the dynamically optimal wealth and the statically optimal wealth derived in

Section 4. Unless otherwise stated, we consider the following model parameters adapted from previous empirical studies (see, for example,

Drimus (

2012)):

.

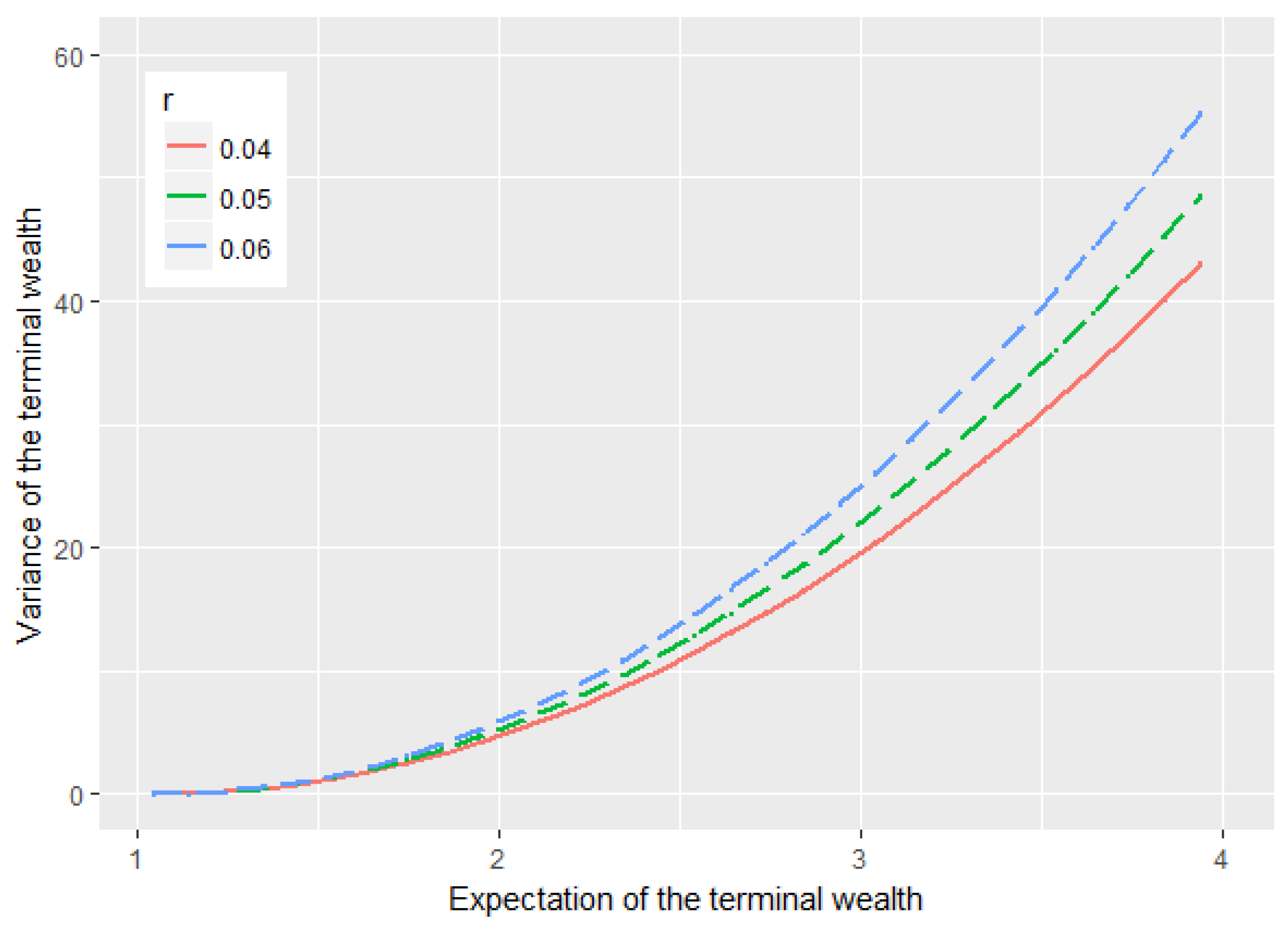

Figure 1 shows us how the interest rate

r affects the efficient frontier. We find that higher interest rate

r results in larger

with the same

. One of the possible reasons is that although the investor can get higher return by investing in the risk-free asset, the risk premium

decreases as

r increases so that the investor indeed derives less expected return from the stock, and thus undertakes more risk. In summary, the impact of

r on the stock is more significant than that on the risk-free asset.

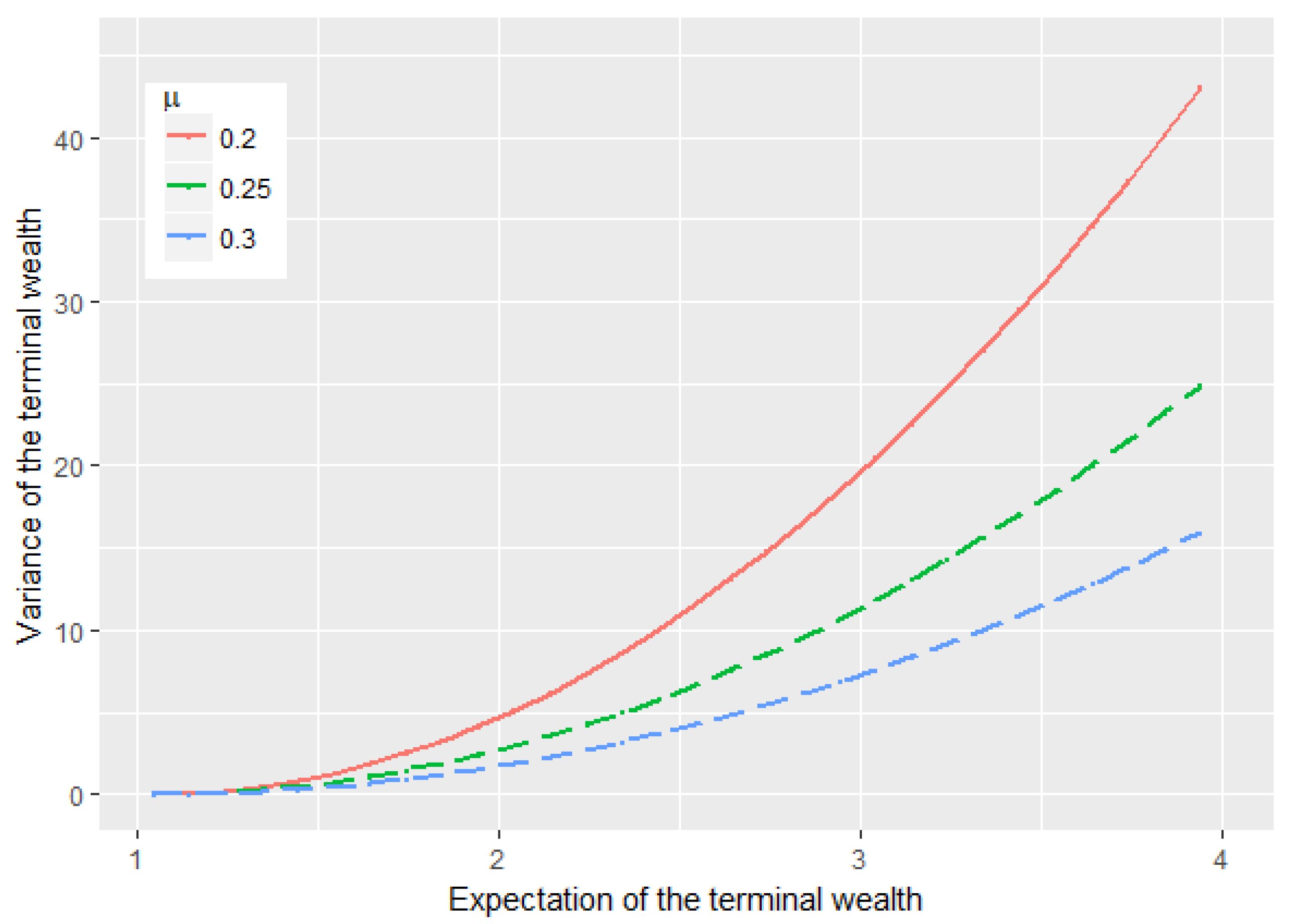

Figure 2 shows how the return rate of the stock

influences the efficient frontier. Higher level of the return rate of the stock price

lowers the variance of terminal wealth

with the same

, which is quite clear due to the fact that the investor receives more risk premium as

increases and the investor can therefore undertake less risk by investing less into the stock and more into the risk-free asset so as to have the same expected terminal wealth.

The impact of the parameter

on the efficient frontier is presented in

Figure 3 below. We see that larger

results in larger

with the same

. One possible reason is that as

partly stands for the mean-reversion speed of the reciprocal of the stochastic volatility

(recall the proof of Lemma 3 above), a larger

results in a faster speed of

towards the long-term level

. Meanwhile, we see that the long-term level is, in fact, decreasing in

. These two aspects in turn make the volatility of the stock

stays longer around the relatively higher level

. Therefore, the investor has to undertake more risk.

The effect of the parameter

on the efficient frontier is given in

Figure 4, which shows that

decreases with the same

as

increases. Again, from the proof of Lemma 3 above, we see that

plays a role as the volatility of the reciprocal of volatility process

, and a larger

results in milder movements of the volatility process

. In addition, we see that the long-run level of volatility

decreases as

increases. Therefore, these two factors help the investor bear less risk.

To end this section, we show the dynamics of wealth processes controlled by the statically optimal strategy

(

30) and the dynamically optimal strategy

(

33), respectively. By setting 500 equidistant time points over

, we simulate two paths of optimal wealth processes

and

.

Figure 5 illustrates the significant difference between the dynamically optimal wealth process

and the statically optimal wealth process

. In particular, we see that the result supports the conclusion of Theorem 2 above: the dynamically optimal wealth

is strictly smaller than the expected terminal wealth

when

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}