A Study on Balanced Scorecard and Its Impact on Sustainable Development of Renewable Energy Organizations; A Mediating Role of Political and Regulatory Institutions

,

,  , , , and

, , , and

Abstract

:1. Introduction

2. Literature

2.1. Using the Balanced Scorecard

2.2. Balanced Scorecard and Political and Regulatory Influence

2.3. Balanced Scorecard and Environmentally Sustainable Development

2.4. Political and Regulatory Influence and Sustainable Development

2.5. Benefits of Using Balance Scorecard in Strategy Implementation

3. Research Methodology

Sampling

4. Research Results and Findings

Demographics of the Study

5. Discussion

6. Conclusions

7. Limitations and Future Work

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ahmad, Syed Touseef, and Syed Amjad Farid Hasnu. 2013. Balanced Scorecard Implementation: Case Study of COMSATS. Researcher 5: 88–109. Available online: https://www.researchgate.net/publication/279182285_Balanced_Scorecard_Implementation_Case_Study_of_COMSATS_Abbottabad_Pakistan (accessed on 3 June 2021).

- Alani, Farooq Salman, M. Firdouse Rahman Khan, and Diana F. Manuel. 2018. University performance evaluation and strategic mapping using balanced scorecard (BSC) case study–Sohar University, Oman. International Journal of Educational Management 32: 689–700. [Google Scholar]

- Al-Najjar, Sabah M., and Khawla H. Kalaf. 2012. Designing a balanced scorecard to measure a bank’s performance: A case study. International Journal of Business Administration 3: 44. [Google Scholar] [CrossRef]

- Araújo, Maria, and Paulo Sampaio. 2014. The path to excellence of the Portuguese organisations recognised by the EFQM model. Total Quality Management & Business Excellence 25: 427–38. [Google Scholar]

- Ardito, Lorenzo, and Rosa Maria Dangelico. 2018. Firm environmental performance under scrutiny: The role of strategic and organizational orientations. Corporate Social Responsibility and Environmental Management 25: 426–40. [Google Scholar] [CrossRef]

- Baumgartner, Rupert J., and Romana Rauter. 2017. Strategic perspectives of corporate sustainability management to develop a sustainable organization. Journal of Cleaner Production 140: 81–92. [Google Scholar] [CrossRef]

- Bontis, Nick, Christopher K. Bart, Sanjoy Bose, and Keith Thomas. 2007. Applying the balanced scorecard for better performance of intellectual capital. Journal of Intellectual Capital. [Google Scholar] [CrossRef] [Green Version]

- Braam, Geert J. M., and Edwin J. Nijssen. 2004. Performance effects of using the balanced scorecard: A note on the Dutch experience. Long Range Planning 37: 335–49. [Google Scholar] [CrossRef]

- Cierna, Helena, and Erika Sujova. 2015. Parallels between corporate social responsibility and the EFQM excellence model. MM Science Journal 10: 670–76. [Google Scholar] [CrossRef]

- Creswell, John W. 1998. Qualitative Inquiry and Research Design: Choosing among Five Traditions. Thousand Oaks: Sage. [Google Scholar]

- Creswell, John W., V. L. Plano Clark, and A. L. Garrett. 2003. Advanced mixed methods research. In Handbook of Mixed Methods in Social and Behavioural Research. Thousand Oaks: Sage, pp. 209–40. [Google Scholar]

- Davis, Stan, and Tom Albright. 2004. An investigation of the effect of balanced scorecard implementation on financial performance. Management Accounting Research 15: 135–53. [Google Scholar] [CrossRef]

- Dias-Sardinha, Idalina, Lucas Reijnders, and Paula Antunes. 2002. From environmental performance evaluation to eco-efficiency and sustainability balanced scorecards. Environmental Quality Management 12: 51–51. [Google Scholar] [CrossRef]

- Duman, Gazi Murat, Murat Taskaynatan, Elif Kongar, and Kurt A. Rosentrater. 2018. Integrating environmental and social sustainability into performance evaluation: A Balanced Scorecard-based Grey-DANP approach for the food industry. Frontiers in Nutrition 5: 65. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Epstein, Marc J., and Peter Wisner. 2001. Good neighbours: Implementing social and environmental strategies with the BSC. Balanced Scorecard Report 3: 8–11. [Google Scholar]

- Falle, Susanna, Romana Rauter, Sabrina Engert, and Rupert Baumgartner. 2016. Sustainability management with the sustainability balanced scorecard in SMEs: Findings from an Austrian case study. Sustainability 8: 545. [Google Scholar] [CrossRef] [Green Version]

- Farid, Daryush, and Heydar Mirfakhredini. 2008. Balanced scorecard application in universities and higher education institutes: Implementation guide in an Iranian context. Universitatii Bucuresti Analele Seria Stiinte Economice Si Administrative 2: 29. [Google Scholar]

- Fernandez-Feijoo, Belen, Silvia Romero, and Silvia Ruiz. 2014. Effect of stakeholders’ pressure on transparency of sustainability reports within the GRI framework. Journal of Business Ethics 122: 53–63. [Google Scholar] [CrossRef]

- Ferreira, Aldónio, and David Otley. 2009. The design and use of performance management systems: An extended framework for analysis. Management Accounting Research 20: 263–82. [Google Scholar] [CrossRef]

- Figge, Frank, Tobias Hahn, Stefan Schaltegger, and Marcus Wagner. 2002. The sustainability balanced scorecard–linking sustainability management to business strategy. Business Strategy and the Environment 11: 269–84. [Google Scholar] [CrossRef]

- Fornell, Claes. 1981. A Comparative Analysis of Two Structural Equation Models: LISREL and PLS Applied to Market Data. New York: Sage. [Google Scholar]

- Fraenkel, Jack R. 2000. Research design and implentation. How to Design and Evaluate Research in Education 104. [Google Scholar] [CrossRef]

- Free, Clinton, and Sandy Q. Qu. 2011. The use of graphics in promoting management ideas: An analysis of the Balanced Scorecard, 1992–2010. Journal of Accounting & Organizational Change 7: 158–89. [Google Scholar]

- Furrer, Olivier, Howard Thomas, and Anna Goussevskaia. 2008. The structure and evolution of the strategic management field: A content analysis of 26 years of strategic management research. International Journal of Management Reviews 10: 1–23. [Google Scholar] [CrossRef]

- Grant, Robert M. 2016. Contemporary Strategy Analysis: Text and Cases Edition. Hoboken: John Wiley & Sons. [Google Scholar]

- Guerci, Marco, Annachiara Longoni, and Davide Luzzini. 2016. Translating stakeholder pressures into environmental performance–the mediating role of green HRM practices. The International Journal of Human Resource Management 27: 262–89. [Google Scholar] [CrossRef]

- Guerras-Martin, Luis Ángel, Anoop Madhok, and Ángeles Montoro-Sánchez. 2014. The evolution of strategic management research: Recent trends and current directions. BRQ Business Research Quarterly 17: 69–76. [Google Scholar] [CrossRef] [Green Version]

- Hair, Anderson. 1998. Multivariate Analysis. New York: Prentice Hall College Div. [Google Scholar]

- Hansen, Erik G., and Stefan Schaltegger. 2016. The sustainability balanced scorecard: A systematic review of architectures. Journal of Business Ethics 133: 193–221. [Google Scholar] [CrossRef]

- Hayes, Andrew F. 2009. Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Communication Monographs 76: 408–20. [Google Scholar] [CrossRef]

- Henrique da Rocha Vencato, Carlos, Clandia Maffini Gomes, Flavia Luciane Scherer, Jordana Marques Kneipp, and Roberto Schoproni Bichueti. 2014. Strategic sustainability management and export performance. Management of Environmental Quality: An International Journal 25: 431–45. [Google Scholar] [CrossRef]

- Hoque, Zahirul. 2014. 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps and opportunities for future research. The British Accounting Review 46: 33–59. [Google Scholar] [CrossRef]

- Hoskisson, Robert E., Wei Shi, Xiwei Yi, and Jing Jin. 2013. The evolution and strategic positioning of private equity firms. Academy of Management Perspectives 27: 22–38. [Google Scholar] [CrossRef]

- Hristov, Ivo, Antonio Chirico, and Andrea Appolloni. 2019. Sustainability Value Creation, Survival, and Growth of the Company: A Critical Perspective in the Sustainability Balanced Scorecard (SBSC). Sustainability 11: 2119. [Google Scholar] [CrossRef] [Green Version]

- Kaplan, Robert S., and David P. Norton. 1992. The balanced scorecard: Measures that drive performance. Available online: https://pubmed.ncbi.nlm.nih.gov/10119714/ (accessed on 3 June 2021).

- Kaplan, Robert S., and David P. Norton. 2000. Having trouble with your strategy? Then map it. Focusing Your Organization on Strategy—with the Balanced Scorecard, 167–76. Available online: https://hbr.org/2000/09/having-trouble-with-your-strategy-then-map-it (accessed on 3 June 2021).

- Kaplan, Robert S., Thomas H. Davenport, Norton P. David Kaplan S. Robert, Robert Steven Kaplan, and David P. Norton. 2001. The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment. Cambridge: Harvard Business Press. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 2001. Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part I. Accounting Horizons 15: 1. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 2004. The strategy map: Guide to aligning intangible assets. Strategy & Leadership 32: 10–17. [Google Scholar]

- Kenworthy, Thomas P., and Alain Verbeke. 2015. The future of strategic management research: Assessing the quality of theory borrowing. European Management Journal 33: 179–90. [Google Scholar] [CrossRef]

- Kramer, Sebastian. 2009. Strategic Sustainability: The case of the New Zealand Energy Sector. Wellington: Victoria University. [Google Scholar]

- Krasniqi, Besnik A, and Malush Tullumi. 2013. What perceived success factors are important for smalll business owners in a transition economy? International Journal of Business and Management Studies 5: 21–32. [Google Scholar]

- Lincoln, Yvonna S., and Egon G. Guba. 2000. The only generalization is: There is no generalization. Case Study Method, 27–44. [Google Scholar]

- Lucianetti, Lorenzo. 2010. The impact of the strategy maps on balanced scorecard performance. International Journal of Business Performance Management 12: 21–36. [Google Scholar] [CrossRef] [Green Version]

- M’Maiti, Hellen Igoki. 2014. Balanced Score Card as a Strategic Management Tool in the Kenyan Commercial State Corporations. Nairobi: University of Nairobi. [Google Scholar]

- Madriz, Esther, N. K. Denzin, and Y. S. Lincoln. 2000. Handbook of Qualitative Research. Thousand Oaks: Denzin & Lincoln, SAGE Publications, Inc. [Google Scholar]

- Meadowcroft, James. 2009. What about the politics? Sustainable development, transition management, and long term energy transitions. Policy Sciences 42: 323. [Google Scholar] [CrossRef]

- Modell, Sven. 2012. The politics of the balanced scorecard. Journal of Accounting & Organizational Change 8: 475–89. [Google Scholar]

- Molina-Azorín, José F. 2014. Microfoundations of strategic management: Toward micro–macro research in the resource-based theory. BRQ Business Research Quarterly 17: 102–14. [Google Scholar] [CrossRef]

- Nathan, Maria L. 2010. ‘Lighting tomorrow with today’: Towards a (strategic) sustainability revolution. International Journal of Sustainable Strategic Management 2: 29–40. [Google Scholar] [CrossRef]

- Punniyamoorthy, M., and R. Murali. 2008. Balanced score for the balanced scorecard: A benchmarking tool. Benchmarking: An International Journal 15: 420–43. [Google Scholar] [CrossRef]

- Rabbani, Fauziah, Sabrina N. H. Lalji, Farhat Abbas, S. M. Wasim Jafri, Junaid A. Razzak, Naheed Nabi, Firdous Jahan, Agha Ajmal, Max Petzold, and Mats Brommels. 2011. Understanding the context of balanced scorecard implementation: A hospital-based case study in Pakistan. Implementation Science 6: 31. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Radomska, Joanna. 2015. The concept of sustainable strategy implementation. Sustainability 7: 15847–56. [Google Scholar] [CrossRef] [Green Version]

- Rafiq, Muhammad, XingPing Zhang, Jiahai Yuan, Shumaila Naz, and Saif Maqbool. 2020. Impact of a balanced scorecard as a strategic management system tool to improve sustainable development: Measuring the mediation of organizational performance through PLS-smart. Sustainability 12: 1365. [Google Scholar] [CrossRef] [Green Version]

- Ronda-Pupo, Guillermo, and Luis Guerras-Martín. 2010. Dynamics of the scientific community network within the strategic management field through the Strategic Management Journal 1980–2009: The role of cooperation. Scientometrics 85: 821–48. [Google Scholar] [CrossRef]

- Ronda-Pupo, Guillermo Armando. 2015. Growth and consolidation of strategic management research: Insights for the future development of strategic management. Academy of Strategic Management Journal 14: 155. [Google Scholar]

- Ronda-Pupo, Guillermo Armando, Carlos Díaz-Contreras, Guillermo Ronda-Velázquez, and Jorge Carlos Ronda-Pupo. 2015. The role of academic collaboration in the impact of Latin-American research on management. Scientometrics 102: 1435–54. [Google Scholar] [CrossRef]

- Singh, Reetesh K., and Simple Sethi Arora. 2018. The adoption of balanced scorecard: An exploration of its antecedents and consequences. Benchmarking: An International Journal 25: 874–92. [Google Scholar] [CrossRef]

- Siva, Vanajah, Ida Gremyr, Bjarne Bergquist, Rickard Garvare, Thomas Zobel, and Raine Isaksson. 2016. The support of Quality Management to sustainable development: A literature review. Journal of Cleaner Production 138: 148–57. [Google Scholar] [CrossRef] [Green Version]

- Soderberg, Marvin, Suresh Kalagnanam, Norman T. Sheehan, and Ganesh Vaidyanathan. 2011. When is a balanced scorecard a balanced scorecard? International Journal of Productivity and Performance Management 60: 688–708. [Google Scholar] [CrossRef]

- Stead, Jean Garner, and W. Edward Stead. 2013. The coevolution of sustainable strategic management in the global marketplace. Organization & Environment 26: 162–83. [Google Scholar]

- Tabachnick, Barbara G., and Linda S. Fidell. 1996. Using Multivariate Statistics. Northridge: Harper Collins. [Google Scholar]

- Tariq, Muhammad, Arslan Ahmed, Shuaib Ahmed, and Syed Kashif Rafi. 2013. Investigating the Impact of Balanced Scorecard on Performance of Business: A study based on the Banking Sector of Pakistan. IBT Journal of Business Studies (JBS) 9. [Google Scholar] [CrossRef]

- Testa, Francesco, Francesco Rizzi, Tiberio Daddi, Natalia Marzia Gusmerotti, Marco Frey, and Fabio Iraldo. 2014. EMAS and ISO 14001: The differences in effectively improving environmental performance. Journal of Cleaner Production 68: 165–73. [Google Scholar] [CrossRef]

- Tingley, Dustin, Teppei Yamamoto, Kentaro Hirose, Luke Keele, and Kosuke Imai. 2014. Mediation: R package for causal mediation analysis. Journal of Statistical Software 59. [Google Scholar] [CrossRef] [Green Version]

- Ullah, Kafait, Maarten J. Arentsen, and Jon C. Lovett. 2017. Institutional determinants of power sector reform in Pakistan. Energy Policy 102: 332–39. [Google Scholar] [CrossRef]

- Walls, Judith L., Pascual Berrone, and Phillip H. Phan. 2012. Corporate governance and environmental performance: Is there really a link? Strategic Management Journal 33: 885–913. [Google Scholar] [CrossRef]

- Wang, Manyi. 2016. Issues of Balanced Scorecard and Its Implication for Chinese Companies. Auckland: Auckland University of Technology. [Google Scholar]

- Williams, Simon. 2001. Drive your business forward with the Balanced Scorecard. Management Services 45: 28–30. [Google Scholar]

- Williamson, Oliver E. 2000. The new institutional economics: Taking stock, looking ahead. Journal of Economic Literature 38: 595–613. [Google Scholar] [CrossRef] [Green Version]

- Wright, Mike, and Ileana Stigliani. 2013. Entrepreneurship and growth. International Small Business Journal 31: 3–22. [Google Scholar] [CrossRef]

- Yang, Baiyin. 2005. Factor analysis methods. Research in Organizations: Foundations and Methods of Inquiry, 181–99. [Google Scholar] [CrossRef]

- Yilmaz, Ayse Kucuk, and Triant Flouris. 2010. Managing corporate sustainability: Risk management process based perspective. African Journal of Business Management 4: 162–71. [Google Scholar]

- Zuhair, Mohamed Hamdhaan, and Priya A. Kurian. 2016. Socio-economic and political barriers to public participation in EIA: Implications for sustainable development in the Maldives. Impact Assessment and Project Appraisal 34: 129–42. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Constructs | Variables | Frequencies | Percentages (%) |

|---|---|---|---|

| Gender | Male | 213 | 75% |

| Female | 72 | 25% | |

| Age-groups (years) | 25 years | 25 | 9% |

| 26–35 years | 191 | 67% | |

| 36–45 years | 53 | 19% | |

| 46–55 years | 13 | 5% | |

| 56–above years | 3 | 1% | |

| Designation | Operation personnel | 11 | 4% |

| Lower management | 79 | 28% | |

| Middle management | 170 | 60% | |

| Top management | 25 | 8% | |

| Experience | Less than 2 years | 98 | 34% |

| between 2–4 years | 168 | 59% | |

| between 5–7 years | 19 | 7% |

| Variables | Minimum | Maximum | Mean | Std. Deviation |

|---|---|---|---|---|

| Financial Perspective | 1.17 | 4.83 | 3.4924 | 0.90439 |

| Customer Perspective | 1.50 | 5.00 | 3.9825 | 0.82109 |

| Internal Business Perspective | 1.00 | 5.00 | 3.9853 | 0.88600 |

| Learning and Growth Perspective | 1.40 | 5.00 | 3.5235 | 0.83035 |

| Political and Regulatory Influence | 1.17 | 5.00 | 3.6538 | 0.91289 |

| Sustainable Development | 1.33 | 5.00 | 3.6433 | 0.79059 |

| Variables | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted (AVE) |

|---|---|---|---|

| SD | 0.818 | 0.879 | 0.646 |

| LGP | 0.833 | 0.899 | 0.749 |

| IBP | 0.875 | 0.909 | 0.668 |

| CP | 0.882 | 0.911 | 0.634 |

| PRI | 0.918 | 0.938 | 0.753 |

| FP | 0.921 | 0.942 | 0.760 |

| Variables | Constructs | Factors Loading |

|---|---|---|

| Customer’s Perspective | cp1 | 0.830 |

| cp2 | 0.804 | |

| cp3 | 0.794 | |

| cp4 | 0.788 | |

| cp5 | 0.788 | |

| cp6 | 0.756 | |

| Financial Perspective | fp2 | 0.901 |

| fp3 | 0.911 | |

| fp4 | 0.881 | |

| fp5 | 0.854 | |

| fp6 | 0.808 | |

| Internal Business Perspective | ibp1 | 0.743 |

| ibp2 | 0.856 | |

| ibp3 | 0.886 | |

| ibp4 | 0.795 | |

| ibp5 | 0.798 | |

| Learning and Growth Perspective | lgp1 | 0.888 |

| lgp2 | 0.901 | |

| lgp3 | 0.804 | |

| Political and Regulatory Influence | pltclrgltryinfl2 | 0.896 |

| pltclrgltryinfl3 | 0.907 | |

| pltclrgltryinfl4 | 0.825 | |

| pltclrgltryinfl5 | 0.876 | |

| pltclrgltryinfl6 | 0.832 | |

| Sustainable Development | sd2 | 0.819 |

| sd3 | 0.833 | |

| sd4 | 0.774 | |

| sd5 | 0.787 |

| Variable | FP | CP | IBP | LGP | PRI | SD |

|---|---|---|---|---|---|---|

| Financial Perspective | 1 | |||||

| Customer Perspective | 0.809 ** | 1 | ||||

| Internal Business Perspective | 0.686 ** | 0.696 ** | 1 | |||

| Learning & Growth Perspective | 0.495 ** | 0.517 ** | 0.403 ** | 1 | ||

| Political & Regulatory Influence | 0.698 ** | 0.631 ** | 0.543 ** | 0.598 ** | 1 | |

| Sustainable Development | 0.557 ** | 0.528 ** | 0.509 ** | 0.811 ** | 0.628 ** | 1 |

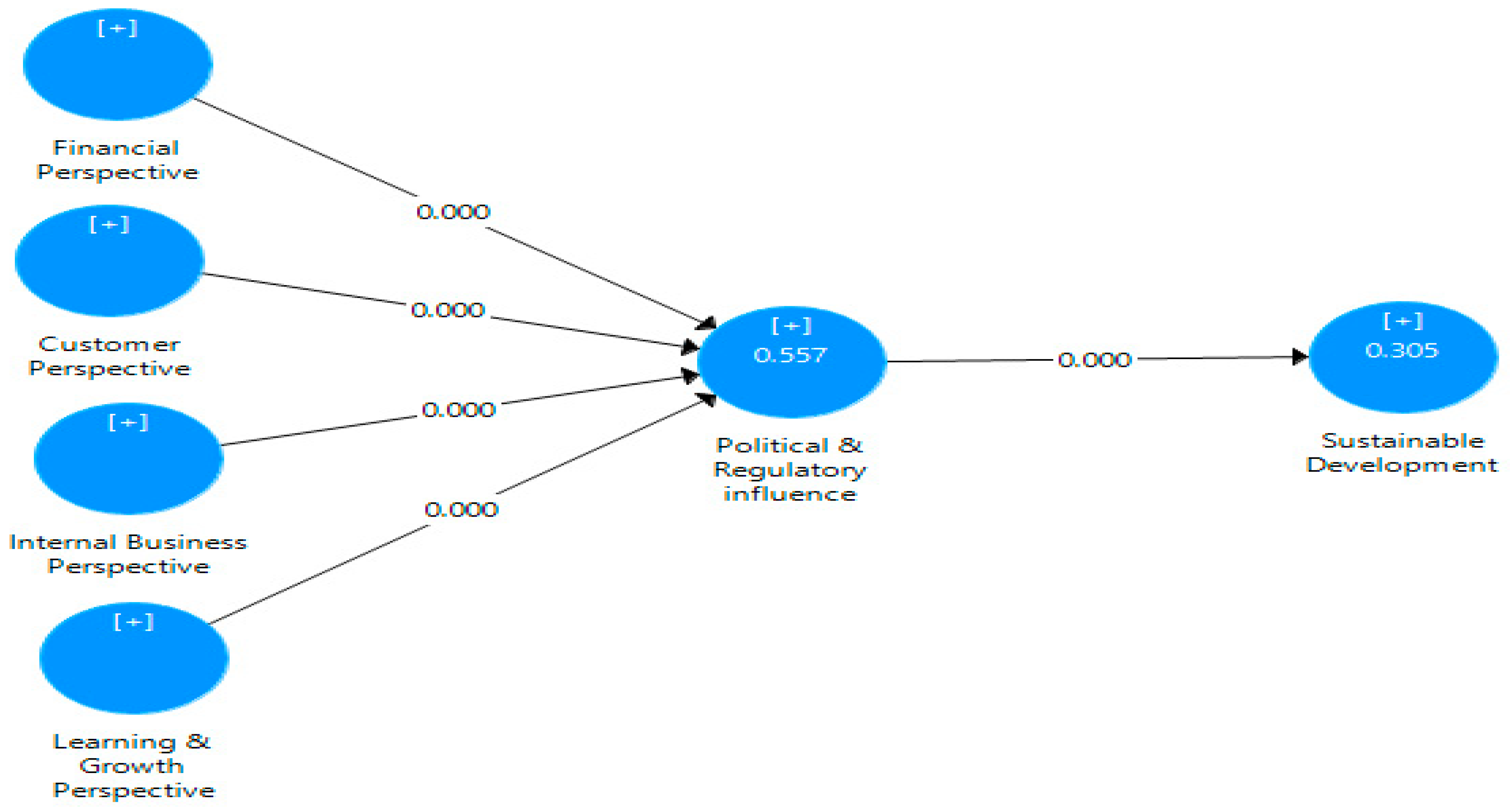

| Hypotheses | Relationship | R2 | Adj. R2 | F Statistics | Sig./p Value |

|---|---|---|---|---|---|

| H1 | FP-PRI | 0.488 | 0.486 | 269.266 | 0.000 |

| H2 | CP-PRI | 0.398 | 0.396 | 187.357 | 0.000 |

| H3 | IBP-PRI | 0.295 | 0.293 | 118.557 | 0.000 |

| H4 | LGP-PRI | 0.357 | 0.355 | 157.225 | 0.000 |

| H5 | FP-SD | 0.311 | 0.308 | 127.510 | 0.000 |

| H6 | CP-SD | 0.279 | 0.276 | 109.265 | 0.000 |

| H7 | IBP-SD | 0.259 | 0.256 | 98.726 | 0.000 |

| H8 | LGP-SD | 0.659 | 0.657 | 545.697 | 0.000 |

| H9 | PRI-SD | 0.394 | 0.392 | 184.289 | 0.000 |

| Relationship | R2 | Adj. R2 | F Statistics | Sig./p Value |

|---|---|---|---|---|

| FP-PRI-SD | 0.422 | 0.418 | 102.916 | 0.000 |

| CP-PRI-SD | 0.423 | 0.419 | 103.405 | 0.000 |

| IBP-PRI-SD | 0.434 | 0.430 | 108.164 | 0.000 |

| LGP-PRI-SD | 0.690 | 0.688 | 314.321 | 0.000 |

| No | Hypothesis | Status |

|---|---|---|

| H1 | Financial Perspective has an impact on Political and Regulatory Influence. | Supported |

| H2 | Customer Perspective has an impact on Political and Regulatory Influence. | Supported |

| H3 | Internal Business Perspective has an impact on Political and Regulatory Influence. | Supported |

| H4 | Learning and Growth Perspective has an impact on Political and Regulatory Influence. | Supported |

| H5 | Financial Perspective has an impact on Sustainable Development. | Supported |

| H6 | Customer Perspective has an impact on Sustainable Development. | Supported |

| H7 | Internal Business Perspective has an impact on Sustainable Development. | Supported |

| H8 | Learning and Growth Perspective has an impact on Sustainable Development. | Supported |

| H9 | Political and Regulatory Influence has an impact on Sustainable Development. | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rafiq, M.; Maqbool, S.; Martins, J.M.; Mata, M.N.; Dantas, R.M.; Naz, S.; Correia, A.B. A Study on Balanced Scorecard and Its Impact on Sustainable Development of Renewable Energy Organizations; A Mediating Role of Political and Regulatory Institutions. Risks 2021, 9, 110. https://doi.org/10.3390/risks9060110

Rafiq M, Maqbool S, Martins JM, Mata MN, Dantas RM, Naz S, Correia AB. A Study on Balanced Scorecard and Its Impact on Sustainable Development of Renewable Energy Organizations; A Mediating Role of Political and Regulatory Institutions. Risks. 2021; 9(6):110. https://doi.org/10.3390/risks9060110

Chicago/Turabian StyleRafiq, Muhammad, Saif Maqbool, José Moleiro Martins, Mário Nuno Mata, Rui Miguel Dantas, Shumaila Naz, and Anabela Batista Correia. 2021. "A Study on Balanced Scorecard and Its Impact on Sustainable Development of Renewable Energy Organizations; A Mediating Role of Political and Regulatory Institutions" Risks 9, no. 6: 110. https://doi.org/10.3390/risks9060110

APA StyleRafiq, M., Maqbool, S., Martins, J. M., Mata, M. N., Dantas, R. M., Naz, S., & Correia, A. B. (2021). A Study on Balanced Scorecard and Its Impact on Sustainable Development of Renewable Energy Organizations; A Mediating Role of Political and Regulatory Institutions. Risks, 9(6), 110. https://doi.org/10.3390/risks9060110