The Efficiency of the Polish Zloty Exchange Rate Market: The Uncovered Interest Parity and Fractal Analysis Approaches

Abstract

:1. Introduction

2. Methodology

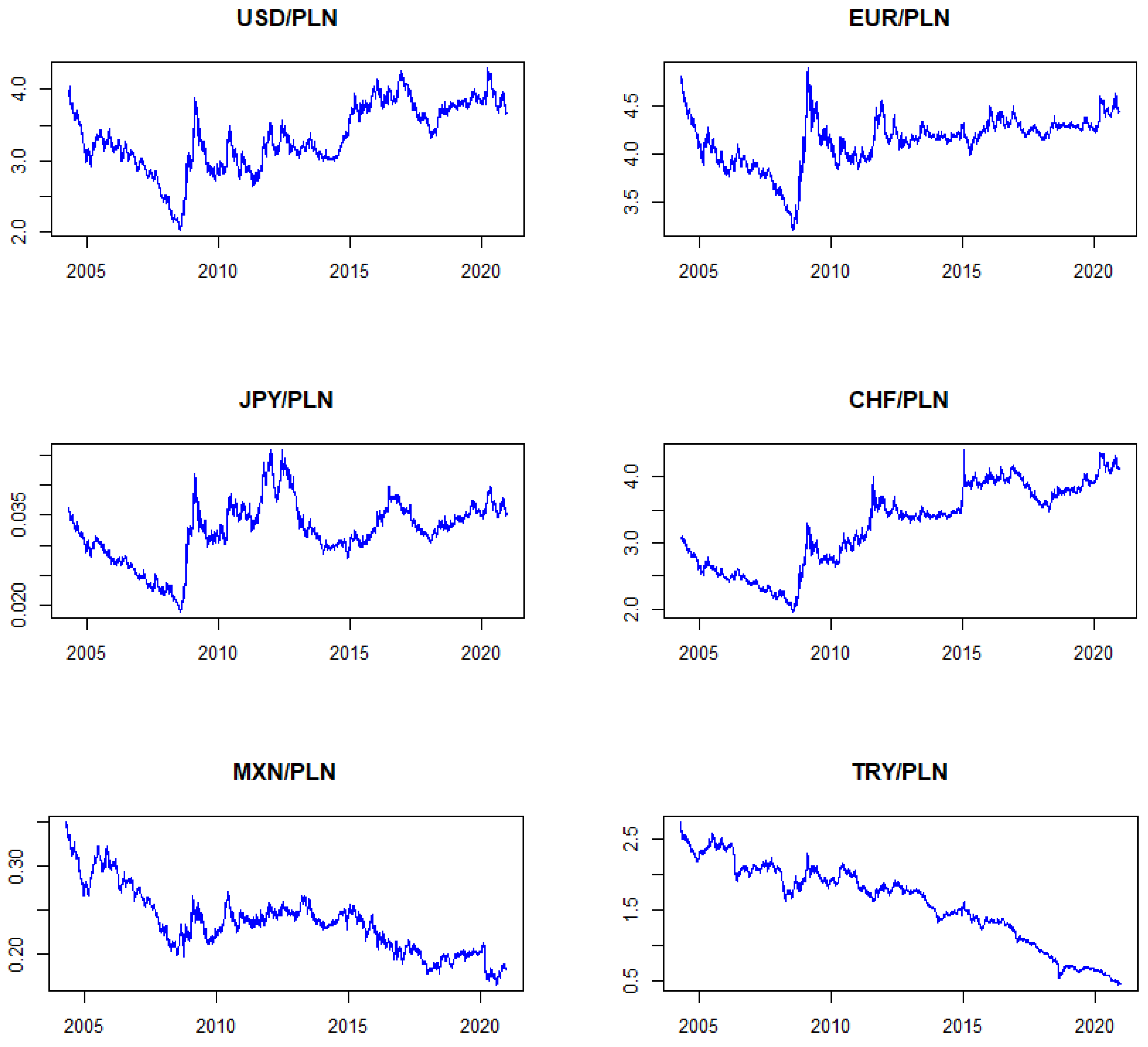

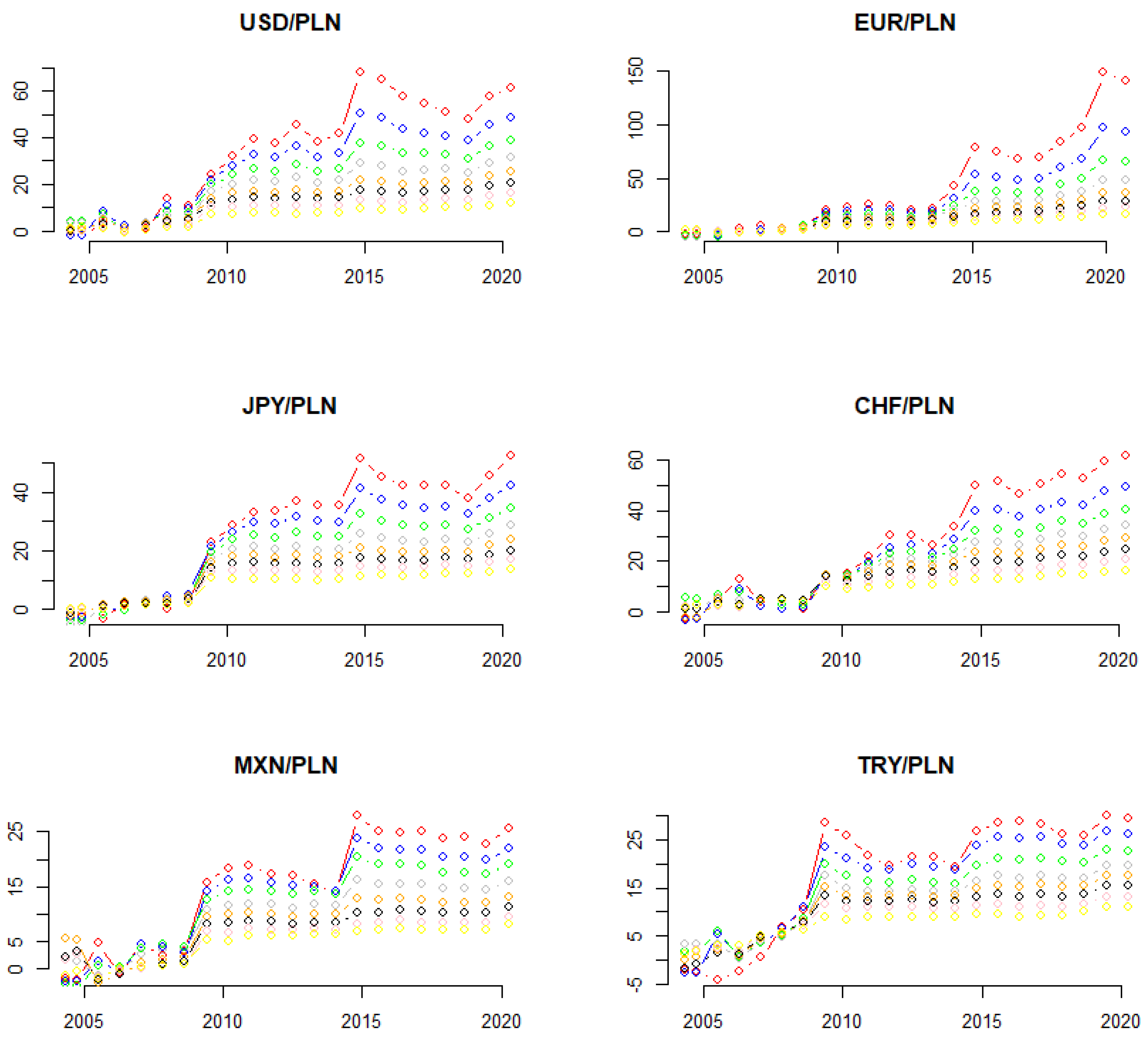

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B

References

- Akaike, Hirotugu. 1976. Canonical Correlation Analysis of Time Series and the Use of an Information Criterio. In Mathematics in Science and Engineering. Amsterdam: Elsevier, pp. 27–96. [Google Scholar] [CrossRef]

- Aslam, Faheem, Saqib Aziz, Duc Khuong Nguyen, Khurrum Mughal, and Maaz Khan. 2020. On the efficiency of foreign exchange markets in times of the COVID-19 pandemic. Technological Forecasting and Social Change 161: 120261. [Google Scholar] [CrossRef] [PubMed]

- Baillie, Richard, and Sanders Chang. 2011. Carry trades, momentum trading and the forward premium anomaly. Journal of Financial Markets 14: 441–64. [Google Scholar] [CrossRef]

- Baillie, Richard, and Rehim Kiliç. 2006. Do asymmetric and nonlinear adjustments explain the forward premium anomaly? Journal of International Money and Finance 25: 22–47. [Google Scholar] [CrossRef] [Green Version]

- Beyaert, Arielle, Jose García-Solanes, and Juan Pérez-Castejón. 2007. Uncovered interest parity with switching regimes. Economic Modelling 24: 189–202. [Google Scholar] [CrossRef]

- BIS. 2019. FX and OTC Derivatives Markets through the Lens of the Triennial Survey. BIS Quarterly Review. International Banking and Financial Market Developments. Basel: BIS. [Google Scholar]

- Bollerslev, Tim. 1990. Modelling the Coherence in Short-Run Nominal Exchange Rates: A Multivariate Generalized Arch Model. The Review of Economics and Statistics 72: 498. [Google Scholar] [CrossRef]

- Broock, William, Jose Scheinkman, Davis Dechert, and Blake LeBaron. 1996. A test for independence based on the correlation dimension. Econometric Reviews 15: 197–235. [Google Scholar] [CrossRef]

- Cerrato, Mario, Hyusok Kim, and Ronald MacDonald. 2013. Nominal interest rates and stationarity. Review of Quantitative Finance and Accounting 40: 741–45. [Google Scholar] [CrossRef] [Green Version]

- Chaboud, Alain, and Jonathan Wright. 2005. Uncovered interest parity: It works, but not for long. Journal of International Economics 66: 349–62. [Google Scholar] [CrossRef] [Green Version]

- Chiarella, Carl, Maurice Peat, and Max Stevenson. 1994. Detecting and modelling nonlinearity in flexible exchange rate time series. Asia Pacific Journal of Management 11: 159–86. [Google Scholar] [CrossRef]

- Cho, Dooyeon. 2018. On the persistence of the forward premium in the joint presence of nonlinearity, asymmetry, and structural changes. Economic Modelling 70: 310–19. [Google Scholar] [CrossRef]

- Cho, Dooyeon, and Sungju Chun. 2019. Can structural changes in the persistence of the forward premium explain the forward premium anomaly? Journal of International Financial Markets, Institutions and Money 58: 225–35. [Google Scholar] [CrossRef]

- Cho, Dooyeon, Heejoon Han, and Na Kyeong Lee. 2019. Carry trades and endogenous regime switches in exchange rate volatility. Journal of International Financial Markets, Institutions and Money 58: 255–68. [Google Scholar] [CrossRef]

- Clarida, Richard, Josh Davis, and Niels Pedersen. 2009. Currency carry trade regimes: Beyond the Fama regression. Journal of International Money and Finance 28: 1375–89. [Google Scholar] [CrossRef] [Green Version]

- Cleveland, Robert, William Cleveland, and Irma Terpenning. 1990. STL: A seasonal-trend decomposition procedure based on loess. Journal of Official Statistics 6: 3–73. [Google Scholar]

- Corazza, Marco, and Tassos Malliaris. 2002. Multi-Fractality in Foreign Currency Markets. Multinational Finance Journal 6: 65–98. [Google Scholar] [CrossRef]

- Czech, Katarzyna. 2020. Speculative trading and its effect on the forward premium puzzle: New evidence from Japanese yen market. Bank i Kredyt 51: 167–88. [Google Scholar]

- Díaz, Andres Fernandez, Pilar Grau-Carles, and Lorenzo Escot Mangas. 2002. Nonlinearities in the exchange rates returns and volatility. Physica A: Statistical Mechanics and its Applications 316: 469–82. [Google Scholar] [CrossRef]

- Dickey, David, and Wayne Fuller. 1979. Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association 74: 427–31. [Google Scholar] [CrossRef]

- Engle, Robert. 1982. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 50: 987. [Google Scholar] [CrossRef]

- Evertsz, Carl. 1995. Self-Similarity of high-frequency USD-DEM exchange rates. Paper Presented at the First International Conference on High Frequency Data in Finance, Zurich, Switzerland, March. [Google Scholar]

- Fama, Eugene. 1965. The Behavior of Stock-Market Prices. The Journal of Business 38: 34–105. [Google Scholar] [CrossRef]

- Fama, Eugene. 1970. Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance 25: 383–417. [Google Scholar] [CrossRef]

- Fama, Eugene. 1984. Forward and spot exchange rates. Journal of Monetary Economics 14: 319–38. [Google Scholar] [CrossRef]

- Fang, Hsing, Kon Lai, and Michael Lai. 1994. Fractal structure in currency futures price dynamics. The Journal of Futures Markets 14: 169–81. [Google Scholar] [CrossRef]

- Flood, Robert, and Andrew Rose. 2002. Uncovered Interest Parity in Crisis. IMF Staff Papers 49: 252–66. [Google Scholar] [CrossRef]

- Froot, Kenneth, and Jeffrey Frankel. 1989. Forward Discount Bias: Is it an Exchange Risk Premium? The Quarterly Journal of Economics 104: 139. [Google Scholar] [CrossRef] [Green Version]

- Galluccio, Stefano, Guido Caldarelli, Matteo Marsili, and Yicheng Zhang. 1997. Scaling in currency exchange. Physica A: Statistical Mechanics and its Applications 245: 423–36. [Google Scholar] [CrossRef] [Green Version]

- Glosten, Lawrence, Ravi Jagannathan, and David Runkle. 1993. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. The Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Goh, Soo Khoon, Guay Lim, and Nills Olekalns. 2006. Deviations from uncovered interest parity in Malaysia. Applied Financial Economics 16: 745–59. [Google Scholar] [CrossRef]

- Gould, Martin, Mason Porter, and Sam Howison. 2015. The Long Memory of Order Flow in the Foreign Exchange Spot Market. SSRN Journal. [Google Scholar] [CrossRef] [Green Version]

- Hamilton, James. 1994. Time Series Econometrics. Princeton: Princeton Unviersity Press. [Google Scholar]

- Han, Chenyu, Yiming Wang, and Ye Ning. 2019. Comparative analysis of the multifractality and efficiency of exchange markets: Evidence from exchange rates dynamics of major world currencies. Physica A: Statistical Mechanics and Its Applications 535: 122365. [Google Scholar] [CrossRef]

- Han, Chenyu, Yiming Wang, and Yingying Xu. 2020. Nonlinearity and efficiency dynamics of foreign exchange markets: Evidence from multifractality and volatility of major exchange rates. Economic Research-Ekonomska Istraživanja 33: 731–51. [Google Scholar] [CrossRef] [Green Version]

- Hsieh, David. 1989. Testing for Nonlinear Dependence in Daily Foreign Exchange Rates. The Journal of Business 62: 339–68. [Google Scholar] [CrossRef]

- Ichiue, Hibiki, and Kentaro Koyama. 2011. Regime switches in exchange rate volatility and uncovered interest parity. Journal of International Money and Finance 30: 1436–50. [Google Scholar] [CrossRef]

- Isard, Peter. 2006. Uncovered Interest Parity. IMF Working Papers. International Monetary Fund WP/06/96. pp. 1–12. Available online: https://ssrn.com/abstract=901883 (accessed on 20 May 2021).

- Kantelhardt, Jan, Stephan Zschiegner, Eva Koscielny-Bunde, Shlomo Havlin, Armin Bunde, and Eugene Stanley. 2002. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A: Statistical Mechanics and Its Applications 316: 87–114. [Google Scholar] [CrossRef] [Green Version]

- Karahan, Özcan, and Olcay Çolak. 2012. Does Uncovered Interest Rate Parity Hold in Turkey? International Journal of Economics and Financial Issues 2: 386–94. [Google Scholar]

- Kitamura, Yoshihiro. 2017. Simple measures of market efficiency: A study in foreign exchange markets. Japan and the World Economy 41: 1–16. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav, and Miloslav Vosvrda. 2016. Gold, currencies and market efficiency. Physica A: Statistical Mechanics and Its Applications 449: 27–34. [Google Scholar] [CrossRef] [Green Version]

- Kwiatkowski, Denis, Peter Phillips, Peter Schmidt, and Yongcheol Shin. 1992. Testing the null hypothesis of stationarity against the alternative of a unit root. Journal of Econometrics 54: 159–78. [Google Scholar] [CrossRef]

- Laib, Mohamed, Luciano Telesca, and Mikhail Kanevski. 2017. MFDFA: MultiFractal Detrended Fluctuation Analysis. Available online: https://mlaib.github.io/MFDFA/ (accessed on 20 May 2021).

- Laib, Mohamed, Jean Golay, Luciano Telesca, and Mikhail Kanevski. 2018. Multifractal analysis of the time series of daily means of wind speed in complex regions. Chaos, Solitons & Fractals 109: 118–27. [Google Scholar] [CrossRef] [Green Version]

- Lean, Hooi Hooi, and Russell Smyth. 2015. Testing for weak-form efficiency of crude palm oil spot and future markets: New evidence from a GARCH unit root test with multiple structural breaks. Applied Economics 47: 1710–21. [Google Scholar] [CrossRef]

- Lei, Qiang, and Ying-li Pan. 2012. Nonlinear analyses of exchange rates of six emerging markets. Journal of Shanghai Jiaotong University (Science) 17: 108–13. [Google Scholar] [CrossRef]

- Li, Dandan, Atanu Ghoshray, and Bruce Morley. 2012. Measuring the risk premium in uncovered interest parity using the component GARCH-M model. International Review of Economics & Finance 24: 167–76. [Google Scholar] [CrossRef] [Green Version]

- Liu, Angela, Ming-Shiun Pan, and Paul Hsueh. 1994. A Modified R/S Analysis of Long-Term Dependence in Currency Futures Prices. Journal of International Financial Markets, Institutions & Money 3: 97–113. [Google Scholar] [CrossRef]

- Lothian, James, and Liuren Wu. 2011. Uncovered interest-rate parity over the past two centuries. Journal of International Money and Finance 30: 448–73. [Google Scholar] [CrossRef] [Green Version]

- Malliaropulos, Dimitrios. 1997. A multivariate GARCH model of risk premia in foreign exchange markets. Economic Modelling 14: 61–79. [Google Scholar] [CrossRef]

- Mammadli, Sadig. 2017. Analysis of chaos and nonlinearities in a foreign exchange market. Procedia Computer Science 120: 901–7. [Google Scholar] [CrossRef]

- Marquardt, Donald. 1963. An Algorithm for Least-Squares Estimation of Nonlinear Parameters. Journal of the Society for Industrial and Applied Mathematics 11: 431–41. [Google Scholar] [CrossRef]

- McCallum, Bennett. 1994. A reconsideration of the uncovered interest parity relationship. Journal of Monetary Economics 33: 105–32. [Google Scholar] [CrossRef] [Green Version]

- Miloş, Laura Raisa, Cornel Haţiegan, Marius Cristian Miloş, Flavia Mirela Barna, and Claudiu Boțoc. 2020. Multifractal Detrended Fluctuation Analysis (MF-DFA) of Stock Market Indexes. Empirical Evidence from Seven Central and Eastern European Markets. Sustainability 12: 535. [Google Scholar] [CrossRef] [Green Version]

- Narayan, Paresh Kumar, Ruipeng Liu, and Joakim Westerlund. 2016. A GARCH model for testing market efficiency. Journal of International Financial Markets, Institutions and Money 41: 121–38. [Google Scholar] [CrossRef]

- Nguyen, Tin. 2000. Foreign Exchange Market Efficiency, Speculators, Arbitrageurs and International Capital Flows. CIES Working Paper 0033. pp. 1–47. Available online: https://ssrn.com/abstract=239452 (accessed on 15 May 2021).

- Olmo, Jose, and Keith Pilbeam. 2011. Uncovered interest parity and the efficiency of the foreign exchange market: A re-examination of the evidence. International Journal of Finance & Economics 16: 189–204. [Google Scholar] [CrossRef]

- Peters, Edgar. 1994. Fractal Market Analysis. Applying Chaos Theory to Investment and Economics. New York: John Wiley & Sons, Inc. [Google Scholar]

- Pietrych, Łukasz, Julio Sandubete, and Lorenzo Escot. 2021. Solving the chaos model-data paradox in the cryptocurrency market. Communications in Nonlinear Science and Numerical Simulation 102: 105901. [Google Scholar] [CrossRef]

- Sarno, Lucio. 2005. Viewpoint: Towards a solution to the puzzles in exchange rate economics: Where do we stand? Canadian Journal of Economics/Revue canadienne d’économique 38: 673–708. [Google Scholar] [CrossRef]

- Serletis, Apostolos, and Periklis Gogas. 1997. Chaos in East European black market exchange rates. Research in Economics 51: 359–85. [Google Scholar] [CrossRef] [Green Version]

- Shahzad, Syed Jawad, Jose Areola Hernandez, Waqas Hanif, and Ghulam Mujtaba Kayani. 2018. Intraday return inefficiency and long memory in the volatilities of forex markets and the role of trading volume. Physica A: Statistical Mechanics and its Applications 506: 433–50. [Google Scholar] [CrossRef]

- Šonje, Velimir, Denis Alajbeg, and Zoran Bubaš. 2011. Efficient market hypothesis: Is the Croatian stock market as (in)efficient as the U.S. market. Financial Theory and Practice 35: 301–26. [Google Scholar] [CrossRef]

- Tabasi, Hamed, Vahidreza Yousefi, Jolanta Tamošaitienė, and Foroogh Ghasemi. 2019. Estimating Conditional Value at Risk in the Tehran Stock Exchange Based on the Extreme Value Theory Using GARCH Models. Administrative Sciences 9: 40. [Google Scholar] [CrossRef] [Green Version]

- Tai, Chu-Sheng. 2001. A multivariate GARCH in mean approach to testing uncovered interest parity: Evidence from Asia-Pacific foreign exchange markets. The Quarterly Review of Economics and Finance 41: 441–60. [Google Scholar] [CrossRef]

- Theiler, James, Stephen Eubank, Andre Longtin, Bryan Galdrikian, and Doyne Farmer. 1992. Testing for nonlinearity in time series: The method of surrogate data. Physica D: Nonlinear Phenomena 58: 77–94. [Google Scholar] [CrossRef] [Green Version]

- van de Gucht, Linda, Marnik Dekimpe, and Chuck Kwok. 1996. Persistence in foreign exchange rates. Journal of International Money and Finance 15: 191–220. [Google Scholar] [CrossRef]

- Xiao, Ling, Gurjeet Dhesi, Eduard Gabriel Ceptureanu, Kevin Lin, Claudiu Herteliu, Babar Syed, and Sebastian Ion Ceptureanu. 2020. Liquidity transmission and the subprime mortgage crisis: A multivariate GARCH approach. Soft Comput 24: 13871–78. [Google Scholar] [CrossRef]

- Zakoian, Jean-Michel. 1994. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18: 931–55. [Google Scholar] [CrossRef]

- Zhou, Su, and Ali Kutan. 2005. Does the forward premium anomaly depend on the sample period used or on the sign of the premium? International Review of Economics & Finance 14: 17–25. [Google Scholar] [CrossRef]

- Zivot, Eric, and Donald Andrews. 2002. Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. Journal of Business & Economic Statistics 20: 25–44. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| USD | EUR | JPY | CHF | MXN | TRY | |

|---|---|---|---|---|---|---|

| ) | ||||||

| Augmented Dickey–Fuller test (ADF) | ||||||

| 5% Critical Value: Test statistic: | −1.94 −12.90 | −1.94 −12.22 | −1.94 −12.41 | −1.94 −12.96 | −1.94 −14.22 | −1.94 −13.10 |

| Kwiatkowski, Phillips, Schmidt and Shin test (KPSS) | ||||||

| 5% Critical Value: Test statistic: | 0.463 0.127 | 0.463 0.154 | 0.463 0.079 | 0.463 0.136 | 0.463 0.088 | 0.463 0.214 |

| ) | ||||||

| Augmented Dickey–Fuller test (ADF) | ||||||

| 5% Critical Value: Test statistic: | −1.94 −1.88 | −1.94 −2.28 | −1.94 −1.58 | −1.94 −1.60 | −1.94 −0.36 | −1.94 −0.72 |

| Kwiatkowski, Phillips, Schmidt and Shin test (KPSS) | ||||||

| 5% Critical Value: Test statistic: | 0.463 0.459 | 0.463 0.232 | 0.463 1.510 | 0.463 0.851 | 0.463 0.644 | 0.463 0.484 |

| Zivot–Andrew test | ||||||

| Test statistic: p-value: | −5.12 <0.001 | −3.43 <0.001 | −3.75 0.017 | −3.14 0.032 | −4.06 0.003 | −4.90 0.001 |

| Coefficients | USD | EUR | JPY | CHF | MXN | TRY |

|---|---|---|---|---|---|---|

| mean equation | ||||||

| 0.001 | −0.001 | 0.005 | 0.009 * | −0.008 *** | −0.013 ** | |

| 0.055 | −0.187 | −3.993 ** | −3.667 ** | −0.997 ** | −0.692 | |

| variance equation | ||||||

| 0.001 | 0.001 * | 0.001 ** | 0.001 ** | 0.002 *** | 0.001 *** | |

| 0.065 * | 0.237 ** | 0.406 *** | 0.573 ** | 0.043 *** | 0.291 *** | |

| 0.075** | - | - | - | 0.051*** | - | |

| - | - | - | −0.583 ** | - | - | |

| 0.135 * | 0.637 *** | 0.418 ** | 0.412 *** | 0.552 *** | - | |

| 0.890 *** | - | - | - | 0.048 *** | - | |

| 1.426 *** | 1.728*** | 1.504*** | 1.494*** | 1.948 *** | - | |

| Wald test () | ||||||

| F test statistic: | 0.207 | 2.335 * | 8.999 *** | 4.299 ** | 19.448 *** | 3.410 ** |

| USD | EUR | JPY | CHF | MXN | TRY | |

|---|---|---|---|---|---|---|

| Time series stationarity tests | ||||||

| ADF test | ||||||

| 5% Critical Value: Test Statistic: | −1.94 −3.821 | −1.94 −2.067 | −1.94 −3.868 | −1.94 −2.831 | −1.94 −2.725 | −1.94 −0.740 |

| KPSS test | ||||||

| 5% Critical Value: Test Statistic: | 0.463 0.169 | 0.463 0.227 | 0.463 0.104 | 0.463 0.157 | 0.463 0.094 | 0.463 0.270 |

| Ljung–Box Q test for autocorrelation (21 retards ~ 1 month) | ||||||

| p-value: | 0.006 | 0.007 | 0.057 | 0.000 | 0.000 | 0.067 |

| Nonlinearity tests: | ||||||

| Surrogate Test (p-value): | <0.05 | <0.05 | <0.05 | <0.05 | <0.05 | <0.05 |

| Terasvirta Test (p-value): | 0.386 | 0.000 | 0.681 | 0.067 | 0.000 | 0.000 |

| White Test (p-value): | 0.671 | 0.028 | 0.611 | 0.024 | 0.066 | 0.214 |

| BDS Test (ARMA fit, p-value): | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| BDS Test (shuffled data): | >0.1 | >0.1 | >0.1 | >0.1 | >0.1 | >0.1 |

| USD | EUR | JPY | CHF | MXN | TRY | |

|---|---|---|---|---|---|---|

| Heteroscedasticity tests | ||||||

| McLeod–Li (p-value): | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Engle ARCH (p-value:) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Variance nonlinearity tests | ||||||

| Surrogate Test (p-value): | <0.05 | <0.05 | <0.05 | <0.05 | <0.05 | <0.05 |

| Terasvirta Test (p-value): | 0.004 | 0.000 | 0.024 | 0.000 | 0.276 | 0.000 |

| White Test (p-value): | 0.004 | 0.001 | 0.032 | 0.000 | 0.000 | 0.000 |

| BDS Test (ARMA fit, p-value): | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| BDS Test (shuffled data, p-value): | >0.1 | >0.1 | >0.1 | >0.1 | >0.1 | >0.1 |

| The Period from Access to the E.U. (3 May 2004, n = 4336) | Periods Since the End of the Crisis (1 January 2010, n = 2857) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Returns | Variance | Returns | Variance | |||||||||

| Hurst DFA | Hurst DFA_SHUFF | BDS | BDS SHUFF | Hurst DFA | Hurst DFA_SHUFF | Hurst DFA | Hurst DFA_SHUFF | BDS | BDS SHUFF | Hurst DFA | Hurst DFA_SHUFF | |

| USD | 0.4944 | 0.4968 | <0.05 | >0.05 | 0.6520 | 0.4814 | 0.5039 | 0.5147 | <0.05 | >0.05 | 0.7168 | 0.5117 |

| EUR | 0.4750 | 0.5206 | <0.05 | >0.05 | 0.6511 | 0.5023 | 0.4851 | 0.4713 | <0.05 | >0.05 | 0.6954 | 0.4855 |

| JPY | 0.5382 | 0.5003 | <0.05 | >0.05 | 0.7222 | 0.4958 | 0.5233 | 0.4826 | <0.05 | >0.05 | 0.7172 | 0.5273 |

| CHF | 0.5419 | 0.5027 | <0.05 | >0.05 | 0.6174 | 0.5291 | 0.5543 | 0.5005 | <0.05 | >0.05 | 0.7633 | 0.5146 |

| MXN | 0.4242 | 0.5272 | <0.05 | >0.05 | 0.6249 | 0.4996 | 0.4339 | 0.4964 | <0.05 | >0.05 | 0.6533 | 0.4871 |

| TRY | 0.4593 | 0.5020 | <0.05 | >0.05 | 0.6157 | 0.5015 | 0.4832 | 0.4962 | <0.05 | >0.05 | 0.7303 | 0.4952 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Czech, K.; Pietrych, Ł. The Efficiency of the Polish Zloty Exchange Rate Market: The Uncovered Interest Parity and Fractal Analysis Approaches. Risks 2021, 9, 142. https://doi.org/10.3390/risks9080142

Czech K, Pietrych Ł. The Efficiency of the Polish Zloty Exchange Rate Market: The Uncovered Interest Parity and Fractal Analysis Approaches. Risks. 2021; 9(8):142. https://doi.org/10.3390/risks9080142

Chicago/Turabian StyleCzech, Katarzyna, and Łukasz Pietrych. 2021. "The Efficiency of the Polish Zloty Exchange Rate Market: The Uncovered Interest Parity and Fractal Analysis Approaches" Risks 9, no. 8: 142. https://doi.org/10.3390/risks9080142

APA StyleCzech, K., & Pietrych, Ł. (2021). The Efficiency of the Polish Zloty Exchange Rate Market: The Uncovered Interest Parity and Fractal Analysis Approaches. Risks, 9(8), 142. https://doi.org/10.3390/risks9080142