1. Introduction

The Maxwell (M) distribution, also called Maxwell–Boltzmann distribution, is a classical one-parameter distribution, finding numerous applications in engineering, physics, chemistry and reliability. Formerly, it appears in statistical mechanics, corresponding to the distribution of the speed of molecules in a gas. Mathematically, the M distribution with parameter

is specified by the following cumulative distribution function (cdf):

and

for

, where

is the standard error function. The corresponding probability density function (pdf) is obtained as

and

for

. Historically, the parameter

connected with the Boltzmann constant (

k), the temperature of the gas (

T) and the mass of a molecule

through the following formula:

. Beyond the previous use, many studies have shown the interest of the M distribution, both from a theoretical and statistical point of view. We refer the reader to [

1,

2,

3,

4,

5,

6,

7,

8].

However, like most one-parameter distributions, the M distribution is not suitable to model certain lifetime phenomena. This is especially true for those with highly biased right distributed values or any other type of left skewed distributed values. For this reason, some extensions were developed by applying diverse notorious schemes. We may refer to those presented in [

9,

10,

11,

12]. In particular, Modi [

11] and Saghir [

12] proposed to extend the M distribution through the use of the length-biased scheme, introducing the length-biased Maxwell (LBM) distribution with parameter

. The corresponding cdf is

and

for

, and the pdf is expressed as

and

for

. This pdf is defined such that

, where

. It is proven that the LBM model offers an interesting alternative to the M model on certain aspects, while keeping the simplicity of one-parameter adjustment. The merits of the LBM distribution are discussed in more detail in [

11,

12,

13,

14]. For these reasons, the LBM distribution is a candidate to be at the top of the list of useful one-parameter lifetime distributions, alongside the exponential distribution, Rayleigh distribution, Maxwell distribution, Lindley distribution by [

15], Shanker distribution by [

16], length-biased exponential (LBE) distribution introduced by [

17] and the distribution for instantaneous failures proposed by [

18], to name a few.

As a new remark, the LBM distribution can be viewed as a special power version of the LBE distribution, the LBE distribution being defined by the following cdf:

and

for

, where

denotes the related parameter. More precisely, if

X denotes a random variable following the LBE distribution with parameter

, then

follows the LBM distribution with parameter

. This remark combined with recent developments on the LBE distribution inspired this study. In particular, Haq [

19] proposed to extend the LBE distribution through the famous Marshall–Olkin scheme established by [

20]. Then, it is proven that the ratio transform and the additional tuning parameter of the Marshall–Olkin scheme extend the perspectives of applications of the former LBE distribution. More precisely, Haq [

19] introduced the Marshall–Olkin length-biased exponential (MOLBE) distribution defined by following cdf:

where

is an additional parameter. In some senses, the MOLBE corrects the lack of flexibility in skewness and kurtosis of the LBE distribution. As a consequence, it demonstrates a more adequate fit to the LBE distribution for various data sets.

In this study, based on the link between the LBE and LBM distributions and the successful strategy of [

19], we seek to apply the Marshall–Olkin scheme for the LBM distribution. We thus introduce the Marshall–Olkin LBM (MOLBM) distribution, defined with the following cdf:

where

. Explicitly, for

, we have

We investigate the basics of the MOLBM distribution, defining the corresponding pdf, survival function (sf), hazard rate function (hrf) and quantile function (qf). Then, we analyze the shape properties of the pdf and hrf, showing that they are more pliant than the corresponding pdf and hrf of the LBM distribution. In particular, we show that the pdf can be skewed to the right or to the left, with wide variations on the kurtosis. Strong compounding and stochastic dominance results are proven, revealing some hierarchy between the pdfs and hrfs of the MOLBM and LBM distributions, mainly depending on . We perform a moment analysis of the new distribution by providing theoretical and numerical results. The versatility of the skewness and kurtosis is emphasized. We define the incomplete moments and some related functions having possible applications in lifetime analysis. Then, the statistical side of the MOLBM distribution is explored through the use of the maximum likelihood method. A simulation work provides some guarantee of convergence of the related estimates. Then, the new model is applied to fit five practical data sets. As a notable result, it outperforms the fit behavior of five well-referenced models based on the following reputed criteria: Akaike information criterion (AIC), consistent Akaike information criterion (CAIC), Bayesian information criterion (BIC) and Hannan–Quinn information criterion (HQIC), and based on the following well-known goodness of fit measures as well: Anderson–Darling (), Cramer-von Mises (), Kolmogorov–Smirnov (KS) and its p-value.

The structure of the paper is as follows.

Section 2 is devoted to the fundamental functions of the MOLBM distribution. The stochastic and moments properties are examined in

Section 3. Estimation of the model parameters is discussed in

Section 4.

Section 5 contains our data analyzes. The paper ends with concluding notes in

Section 6.

3. Compounding, Dominance and Moments

We now put the light on some interesting results involving the MOLBM distribution.

3.1. Compounding

The following theorem is about a compounding characterization of the MOLBM distribution.

Theorem 1. Let X and Y be two random variables such that has the following conditional sf: and for , with and , and Y follows the exponential distribution with parameter , i.e., with pdf for and for . Then, X follows the MOLBM distribution with parameters α and β.

Proof. By the definition, the sf of

X is obtained as

We recognize , ending the proof of Theorem 1. □

3.2. Stochastic Dominance

The following first-order stochastic dominance result holds.

Proposition 1. For any , , and , we have Proof. This inequality is clear for

, the both cdfs being equal to 0. For

, we have

and

Therefore, is a decreasing function with respect to and , proving the desired result. □

In particular, since , Proposition 1 implies the following first-order stochastic dominance related to the MOLBM and LBM distributions: For , we have , and for , .

The MOLBM distribution also enjoys a strong hazard rate dominance, formulated in the next result.

Proposition 2. For any and , we have Proof. This inequality is clear for

, the both hrfs being equal to 0. For

, we have

Therefore, is a decreasing function with respect to , proving the desired result. □

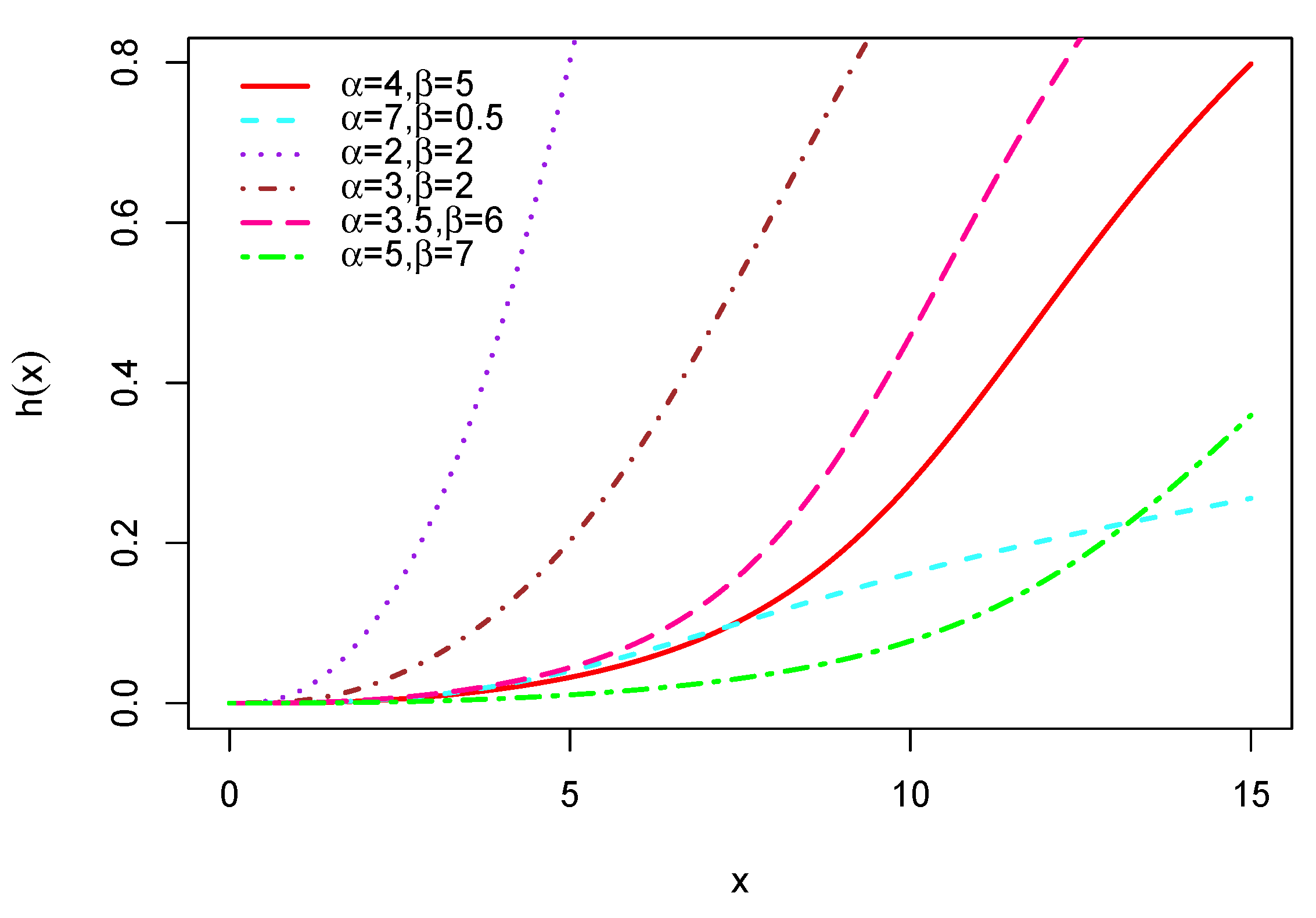

In particular, since corresponds to the hazard rate function of the LBM distribution denoted by , the following hazard rate dominance result holds: For , we have , and for , .

All the above results demonstrate the power of

in the pliancy of the MOLBM distribution in comparison to the classic LBM distribution. For further results about the first-order stochastic dominance, we refer the reader to [

22].

3.3. Moments

Hereafter, we work with a random variable

X following the MOLBM distribution with parameters

and

. Then, for any integer

s, the

moment of

X is obtained as

where

denotes the expectation. Thanks to the obtained equivalences functions of

at

and

, owing to the Riemann integral criteria,

exists in the integral convergence sense.

However, in view of the complexity of , there is no simple analytical expression for . From a computational point of view, numerical integration techniques can be employed to evaluate it through the use of mathematical software. A more transparency, direct and analytical approach consists in providing series expansion for . A such expansion is given in the following result for the case through the use of the gamma function defined by with .

Proposition 3. For , we have Proof. In the case

, we have

. By applying the geometric series formula, followed by the classic binomial formula, a series expansion of

is given as

Now, by the dominated convergence theorem, we get

By applying the change of variable

and introducing the well-known gamma function, we can express

as

Therefore, by putting the previous equalities together, we get

This ends the proof of Proposition 3. □

From Proposition 3, it is clear that is an increasing function with respect to .

The case

, corresponding to the classic LBM distribution, can be found in [

12]. From this reference, the following formula is reported:

The next result discusses a series expansion for in the case , demanding another strategy of proof.

Proof. In the case

, in view of using some generic formula, we need to re-express

. In this regard, for

, we have

Now, let us notice that

. By applying the geometric series formula, followed by the classic binomial formula two times in a row, the following series expansion of

holds:

where

Now, by the dominated convergence theorem, we get

By proceeding as in (

5), we arrive at

Therefore, by putting the previous equalities together, we get

This ends the proof of Proposition 4. □

From Proposition 4, as for the case , we can notice is an increasing function with respect to . By combining Propositions 3 and 4, we can derive a manageable approximation finite sum expression of by substituting the infinite limits by large integers. From the computational point of view, such series approximation can be more precise than direct integral approximation techniques from the initial definition of .

Remark 1. One can show that exists provided , allowing the consideration of some negative moments for X. The negative moment being defined by Therefore, for , 2 and 3, can be expressed as in Propositions 3 and 4 by putting instead of s in the series expansions.

The moments of

X include the mean of

X corresponding to

. The variance of

X is obtained by the standard Koenig–Huygens formula:

. In addition, the

central moment of

X is obtained as

From this central moment, we can define the general coefficient of X by . The coefficients of asymmetry and kurtosis of X are given as and , respectively.

Table 1 indicates numerical values for moments (standard and negative), asymmetry and kurtosis of the MOLBM distribution for selected values of parameters

and

.

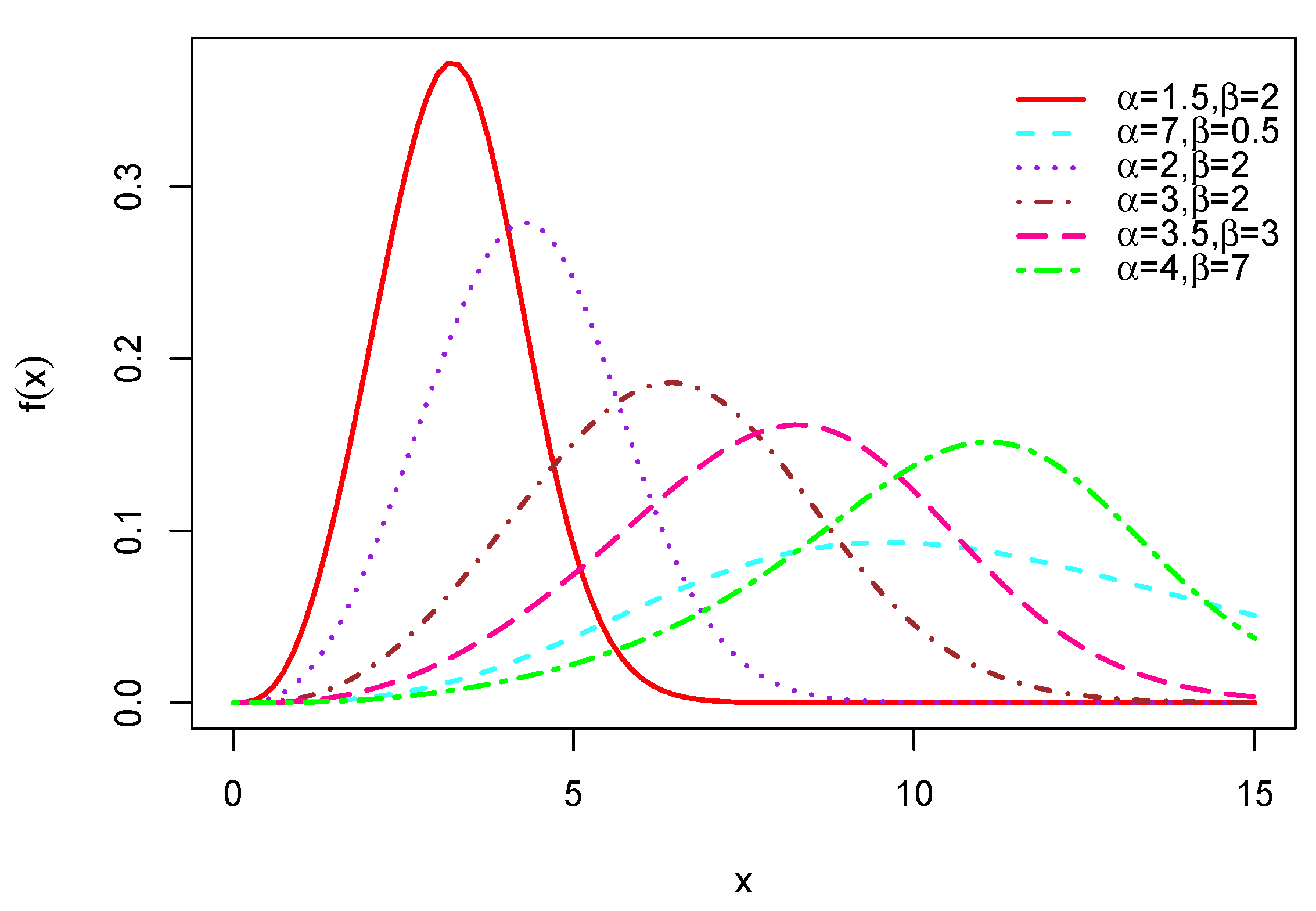

From this table, we see wide variations in the values of the mean, the other moments and negatives moments. The variance can be small or large. In addition, the MOLBM distribution can have or , revealing the versatile nature of its skewness. The same remark holds for the kurtosis; we have , or , showing that the MOLBM distribution can be platykurtic, mesokurtic or leptokurtic, respectively.

3.4. Incomplete Moments

Let

and

be the indicator random variable over the event

, that is

if

realized, and 0 otherwise. Then, for any integer

s, the

incomplete moment of

X at

t exists and it is obtained as

An analytical expression for is not expected, but numerical integration techniques can be considered. Alternatively, we can express it as in Propositions 3 and 4 through the use of the lower incomplete gamma function defined by with and . The proposition below formalizes this expression, according to , and .

Proposition 5. The following expansions for hold:

For , we have

The proof of Proposition 5 follows the lines of Propositions 3 and 4, just an adjustment of the upper bound in the integral needs special treatment according to the respective changes of variables. For this reason, the detailed proof is omitted.

By applying

, we rediscover the

moment of

X. Several related quantities can be derived from

, such as the mean deviation about the mean defined by

where

denotes the first incomplete moment of

X taken at

. As a second famous example, one can discuss the reversed residual life of

X defined by

where, by the classic binomial formula, the integral term can be developed as

We thus have a generic expression for

according to the incomplete moments, from which we can deduce the mean waiting time of

X by taking

. Similarly, the variance and coefficient of variation of the reversed residual life of

X can be defined from

and

. More details are provided in [

23].

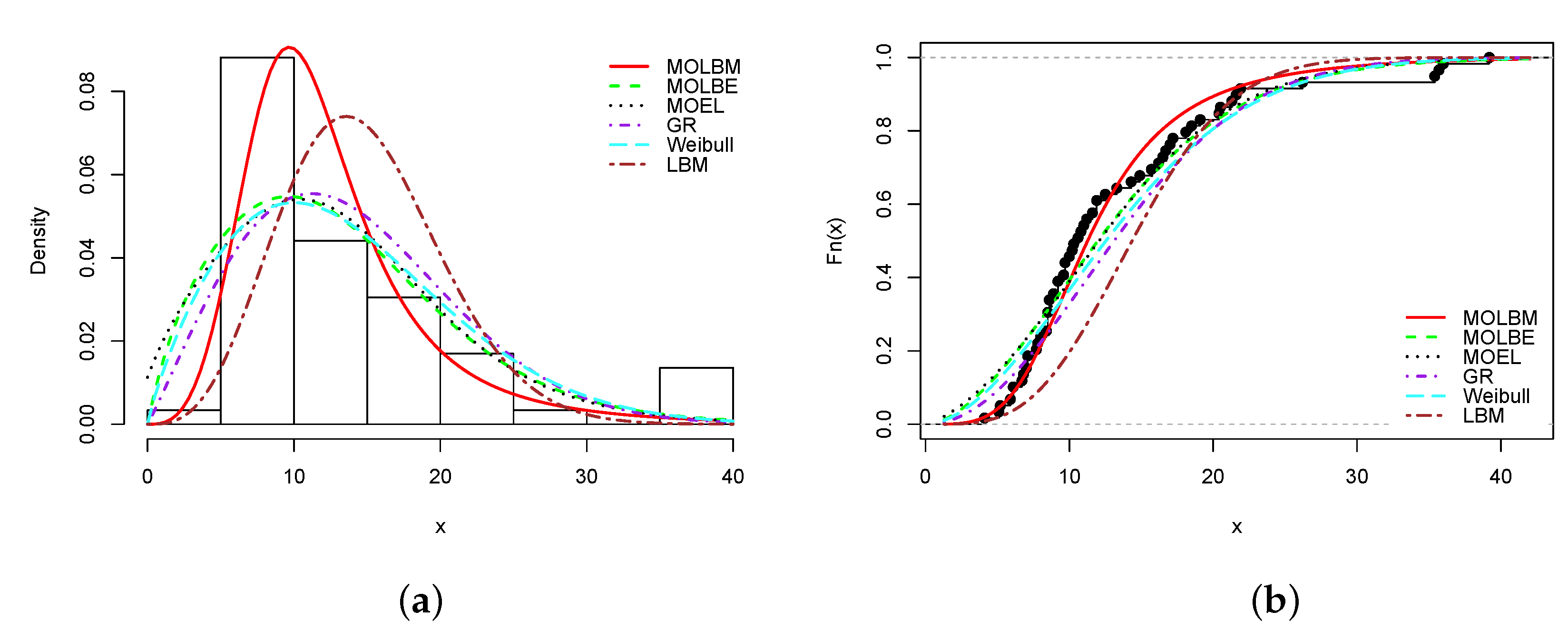

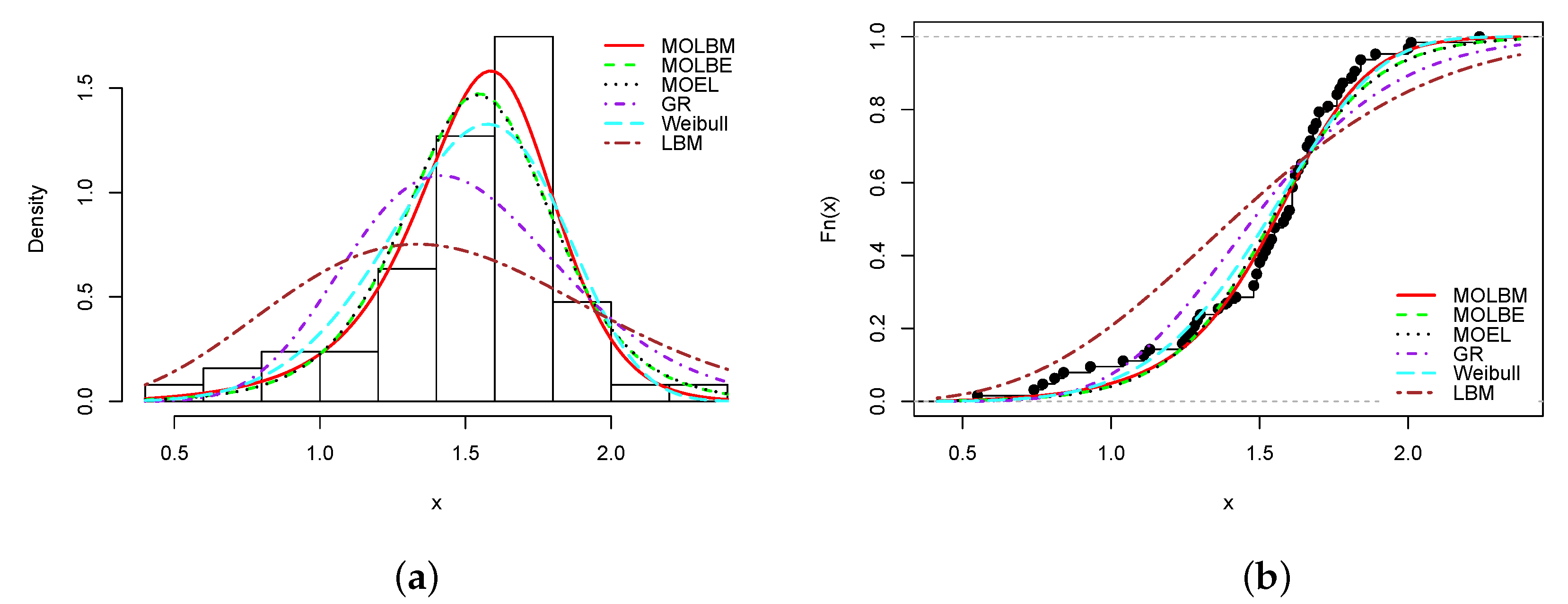

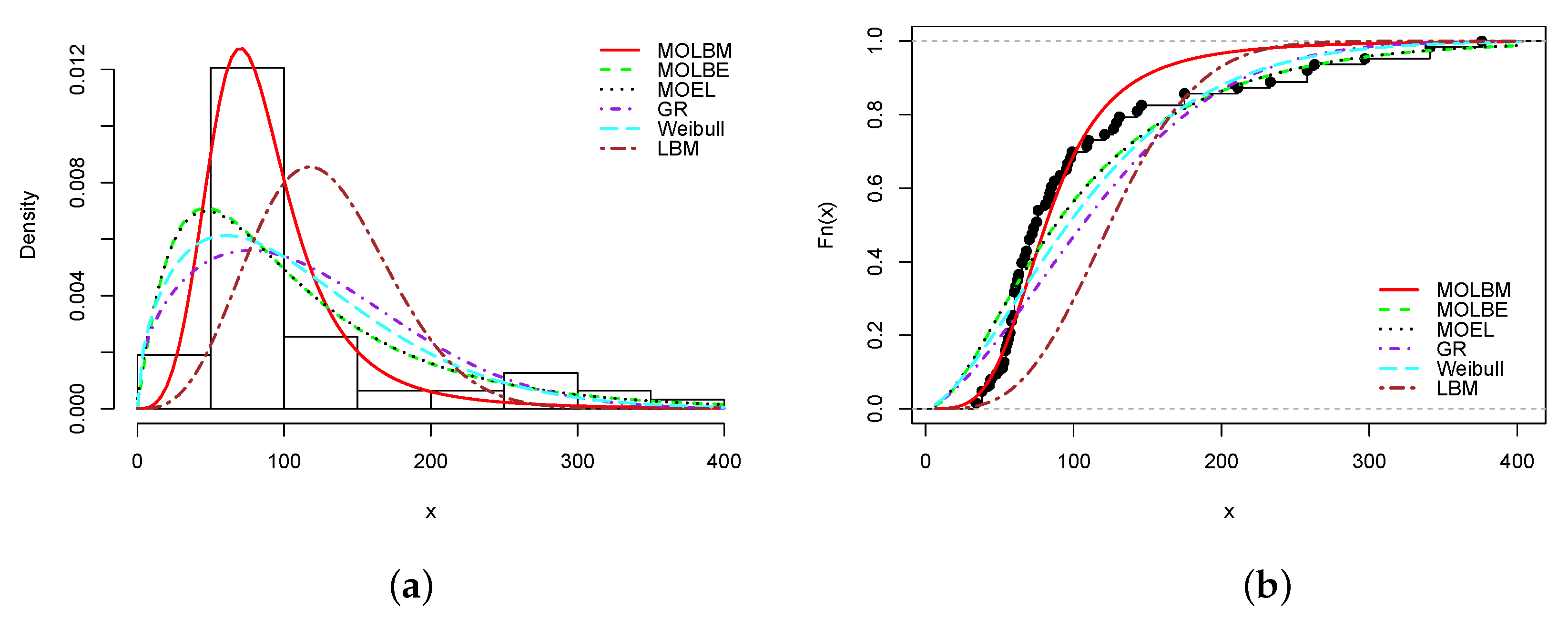

5. Applications

In this section, we explore the potentiality of the new model with other five well known competitive models which are the Marshall–Olkin length-biased exponential (MOLBE), Marshall–Olkin extended Lindley (MOEL) (see [

25]), generalized Rayleigh (GR) (see [

26]), Weibull and length-biased Maxwell (LBM) models. For the sake of transparency, the pdfs of these competitive models are expressed below.

The pdf of the MOLBE model is

and

for

.

The pdf of the MOEL model is

and

for

.

The pdf of the GR model is

and

for

.

The pdf of the Weibull model is

and

for

.

The pdf of the LBM model is

and

for

.

All the involved parameters and are supposed to be strictly positive.

The five data sets considered are given below, along with the estimated model parameters, the values of the following models comparison criteria: AIC, CAIC, BIC and HQIC, and the following goodness-of-fit statistics values: , and KS, as well as the p-value of the KS test. We recall that a lower AIC, BIC, CAIC, BIC, HQIC, , or KS value indicates a better fit for the corresponding model. Moreover, the larger the p-value of the KS test, the less we can reject the suitability of the model to fit the data.

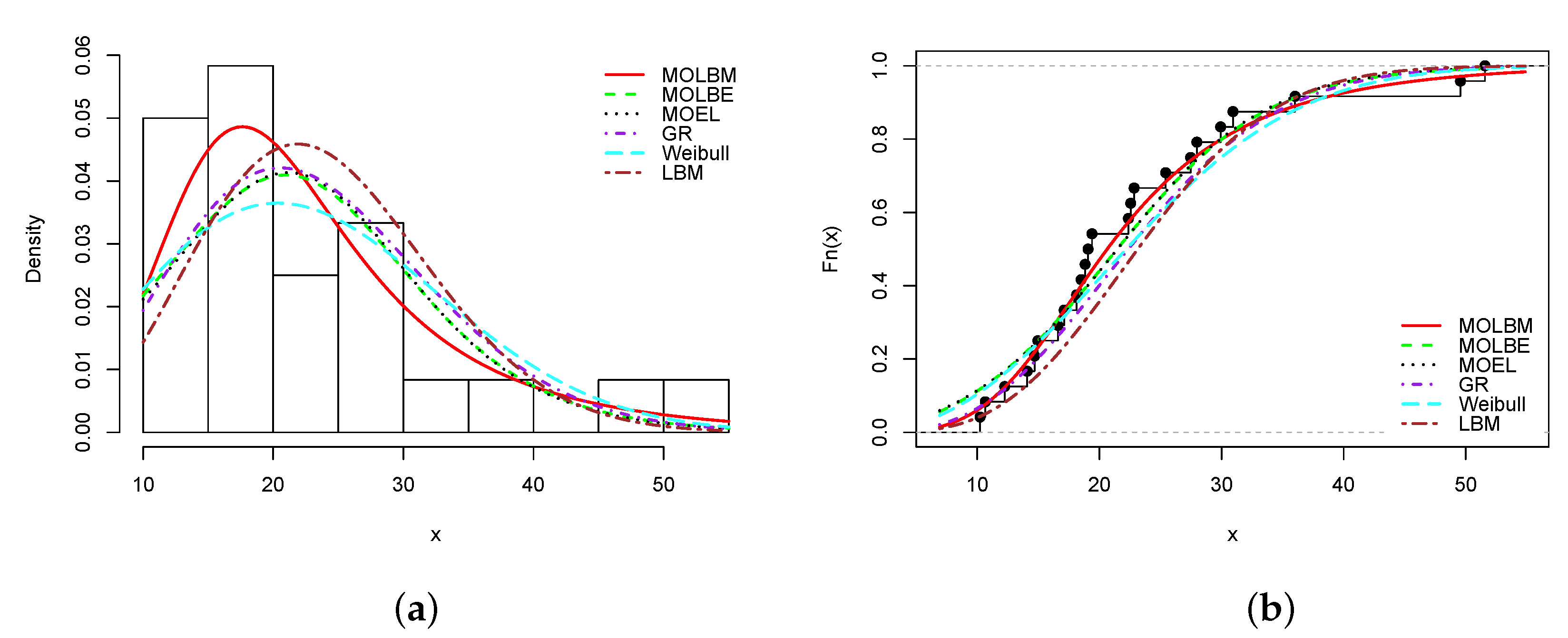

Data set 1: The data are extracted from [

27]. They represent the failure times of mechanical components. They are given as follows: 30.94, 18.51, 16.62, 51.56, 22.85, 22.38, 19.08, 49.56, 17.12, 10.67, 25.43, 10.24, 27.47, 14.70, 14.10, 29.93, 27.98, 36.02, 19.40, 14.97, 22.57, 12.26, 18.14, 18.84.

Table 7 shows the MLEs of the parameters of the considered models, with their standard errors.

Table 8 indicates the −

, AIC, CAIC, BIC, HQIC,

,

, KS and

p-value of the considered models.

A global conclusion on the fit behavior of the MOLBM model for the five data sets will be formulated later.

Data set 2: The data are taken from [

28]. They represent fracture toughness MPa

data from the Alumina

material. They are given as follows: 5.5, 5, 4.9, 6.4, 5.1, 5.2, 5.2, 5, 4.7, 4, 4.5, 4.2, 4.1, 4.56, 5.01, 4.7, 3.13, 3.12, 2.68, 2.77, 2.7, 2.36, 4.38, 5.73, 4.35, 6.81, 1.91, 2.66, 2.61, 1.68, 2.04, 2.08, 2.13, 3.8, 3.73, 3.71, 3.28, 3.9, 4, 3.8, 4.1, 3.9, 4.05, 4, 3.95, 4, 4.5, 4.5, 4.2, 4.55, 4.65, 4.1, 4.25, 4.3, 4.5, 4.7, 5.15, 4.3, 4.5, 4.9, 5, 5.35, 5.15, 5.25, 5.8, 5.85, 5.9, 5.75, 6.25, 6.05, 5.9, 3.6, 4.1, 4.5, 5.3, 4.85, 5.3, 5.45, 5.1, 5.3, 5.2, 5.3, 5.25, 4.75, 4.5, 4.2, 4, 4.15, 4.25, 4.3, 3.75, 3.95, 3.51, 4.13, 5.4, 5, 2.1, 4.6, 3.2, 2.5, 4.1, 3.5, 3.2, 3.3, 4.6, 4.3, 4.3, 4.5, 5.5, 4.6, 4.9, 4.3, 3, 3.4, 3.7, 4.4, 4.9, 4.9, 5.

Table 9 shows the MLEs of the parameters of the considered models, with their standard errors.

Table 10 indicates the −

, AIC, CAIC, BIC, HQIC,

,

, KS and

p-value of the considered models.

Data set 3: The data are taken from [

29]. These data represent the monthly taxes revenue in Egypt. They are given as follows: 5.9, 20.4, 14.9, 16.2, 17.2, 7.8, 6.1, 9.2, 10.2, 9.6, 13.3, 8.5, 21.6, 18.5, 5.1, 6.7, 17, 8.6, 9.7, 39.2, 35.7, 15.7, 9.7, 10, 4.1, 36, 8.5, 8, 9.2, 26.2, 21.9, 16.7, 21.3, 35.4, 14.3, 8.5, 10.6, 19.1, 20.5, 7.1, 7.7, 18.1, 16.5, 11.9, 7, 8.6, 12.5, 10.3, 11.2, 6.1, 8.4, 11, 11.6, 11.9, 5.2, 6.8, 8.9, 7.1, 10.8.

Table 11 shows the MLEs of the parameters of the considered models, with their standard errors.

Table 12 indicates the −

, AIC, CAIC, BIC, HQIC,

,

, KS and

p-value of the considered models.

Data set 4: The data are taken from [

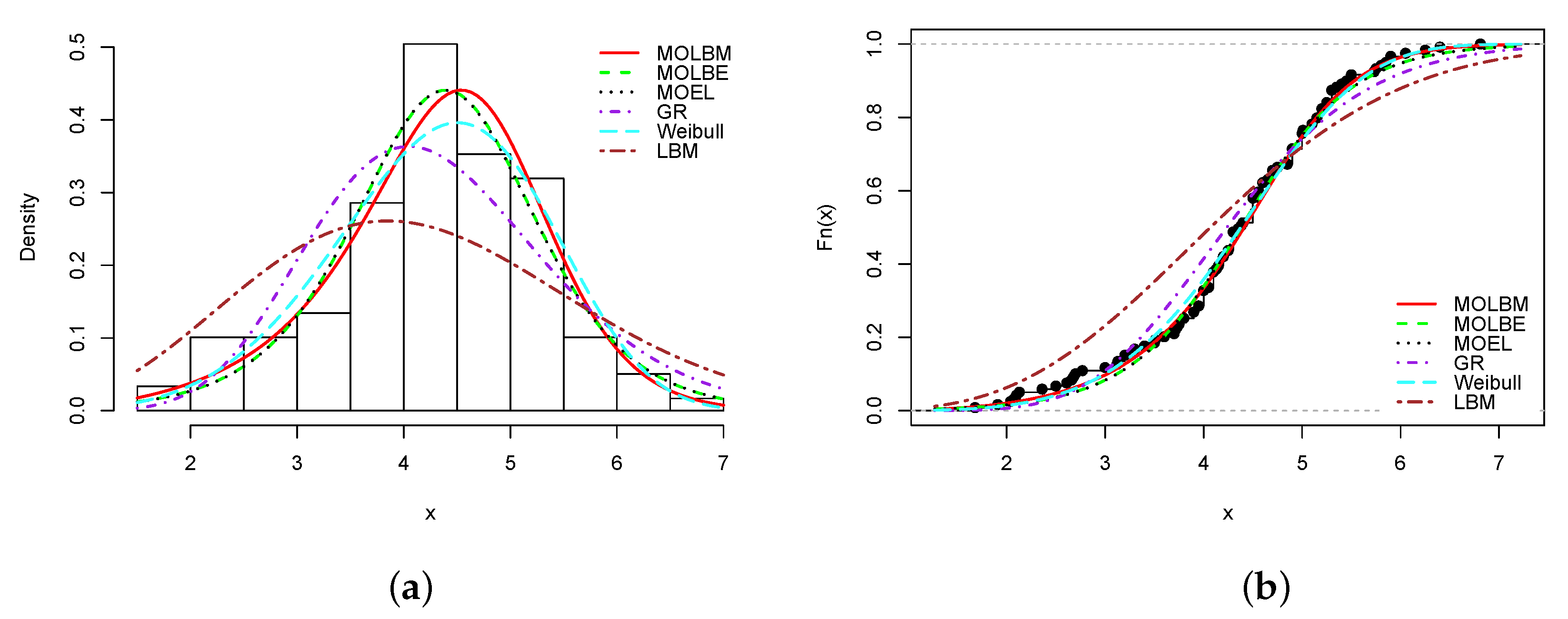

30]. They represent the strengths of 1.5 cm glass fibers. They are given as follows: 0.55, 0.74, 0.77, 0.81, 0.84, 1.24, 0.93, 1.04, 1.11, 1.13, 1.30, 1.25, 1.27, 1.28, 1.29, 1.48, 1.36, 1.39, 1.42, 1.48, 1.51, 1.49, 1.49, 1.50, 1.50, 1.55, 1.52, 1.53, 1.54, 1.55, 1.61, 1.58, 1.59, 1.60, 1.61, 1.63, 1.61, 1.61, 1.62, 1.62, 1.67, 1.64, 1.66, 1.66, 1.66, 1.70, 1.68, 1.68, 1.69, 1.70, 1.78, 1.73, 1.76, 1.76, 1.77, 1.89, 1.81, 1.82, 1.84, 1.84, 2.00, 2.01, 2.24.

Table 13 shows the MLEs of the parameters of the considered models, with their standard errors.

Table 14 indicates the −

, AIC, CAIC, BIC, HQIC,

,

, KS and

p-value of the considered models.

Data set 5: The data are taken from [

31]. These data represent the survival times of injected guinea pigs with different doses of tubercle bacilli. They are given as follows: 34, 38, 38, 43, 44, 48, 52, 53, 54, 54, 55, 56, 57, 58, 58, 59, 60, 60, 60, 60, 61, 62, 63, 65, 65, 67, 68, 70, 70, 72, 73, 75, 76, 76, 81, 83, 84, 85, 87, 91, 95, 96, 98, 99, 109, 110, 121, 127, 129, 131, 143, 146, 175, 175, 211, 233, 258, 258, 263, 297, 341, 341, 376.

Table 15 gives the MLEs of the parameters of the considered models, with their standard errors.

Table 16 presents the −

, AIC, CAIC, BIC, HQIC,

,

, KS and

p-value of the considered models.

From

Table 8,

Table 10,

Table 12,

Table 14 and

Table 16, it is clear that the smallest AIC, CAIC, BIC, HQIC,

,

and KS statistics, and largest KS

p-value are obtained for the MOLBM model; it is the best model. As the main illustrations, the plots of the estimated pdfs over the histograms and cdfs over the empirical cdfs are presented in

Figure 3,

Figure 4,

Figure 5,

Figure 6 and

Figure 7 for Data sets 1, 2, 3, 4 and 5, respectively.

In all the graphs, we see that the red curves fit the empirical objects better than the other colored curves. From these numerical and visual evidences, we can conclude that the MOLBM model can be adequate for modeling these data.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}