1. Introduction

The role of gold as a traditional “safe haven” historically is well-established, as recently highlighted by Boubaker et al. [

1], based on the entire available history of gold prices available from 1258 until recent years. This role of gold implies that investors recurrently are attracted to gold due to its ability to offer portfolio-diversification and/or hedging benefits during periods of heightened economic and financial uncertainty, geopolitical risks, high degree of risk aversion, and/or low investor sentiment. In the wake of a series of crises over the last decade and half, such as the global financial crisis (GFC), the European sovereign debt crisis, “Brexit”, and the ongoing COVID-19 pandemic, there has been a sharp rise in the number of studies (see, for example, Fang et al. [

2], Demirer et al. [

3,

4], Asai et al. [

5], Gkillas et al. [

6], Bouri et al. [

7]) analyzing the role of various proxies of uncertainty in modeling and forecasting gold-market volatility. The reader is referred to the references cited in these papers for earlier studies in this area. The interest of researchers in inspecting the link between uncertainty and gold-market volatility is understandable because, during episodes of recurring crises and associated heightened uncertainties across various dimensions, accurate forecasts of gold-market volatility are of paramount importance to investors in the pricing of related derivative securities and for devising portfolio-allocation strategies [

8,

9].

Turning back now to the existing literature on proxies of uncertainty and gold-market volatility, Demirer et al. [

3], studied the in- and out-of-sample predictive value of time-varying risk aversion of the United States (U.S.) for daily volatility of gold returns via an extended version of the heterogeneous autoregressive (realized) volatility (HAR-RV) model. They showed that time-varying risk aversion often captures information useful for out-of-sample prediction of realized volatility not already contained in other predictors, namely higher-moments, jumps, gold returns, and a leverage effect, as well as a newspapers-based index of economic policy uncertainty of the U.S. Along similar lines, Demirer et al. [

4] pointed out that a U.S. financial risk shock derived from the Chicago Board Options Exchange (CBOE)’s Volatility Index (VIX), incorporated into a high-frequency (daily) data structural model of the oil market, is important in forecasting gold (realized) volatility on its own (though including oil price shocks in the model provides additional forecasting power). The VIX, often called a fear index or fear gauge, is a popular measure of the stock market’s expectation of volatility based on the S&P 500 index options, and often is considered a very good proxy of (financial) uncertainty prevailing in the U.S. Gkillas et al. [

6], in turn, using a quantiles-dependent version of the HAR-RV model, show that U.S. newpapers-based measure of geopolitical risks can forecast daily volatility of the gold market, especially at longer horizons, beyond the information contained in policy-related uncertainty of the U.S. In this regard, it should be noted that Asai et al. [

5] were more interested in modeling and forecasting the covariance matrix of the returns of crude oil and gold futures, and, in the process, depict the role of the geopolitical risks indicator in forecasting covolatilities of these two commodities. Finally, Bouri et al. [

7] analyzed the predictive power of a daily newspaper-based index of U.S. uncertainty associated with infectious diseases (EMVID) for gold-market volatility. These authors documented that incorporating EMVID into a forecasting setting significantly improves the forecast accuracy of the volatility of gold-returns at short-, medium-, and long-run horizons, based on the HAR-RV model.

As can be seen, a general tendency of the above studies is to primarily incorporate the role of U.S.-based measures of uncertainty in predicting movements of gold-market volatility, barring Fang et al. [

2]. These authors highlighted the importance of a newspapers-based measure of global economic policy-related uncertainty derived from 22 countries, using the mixed data sampling generalized autoregressive conditional heteroskedasticity (MIDAS-GARCH) model, in forecasting gold-returns volatility. The focus on U.S. uncertainty certainly reflects to some extent the dominance of the U.S. as a major player in the gold market, and global assets market in general, besides the fact that the GFC originated in the U.S. Based on 2019 data on production volumes derived from the Metals Focus of the World Gold Council, the U.S. is the fourth largest gold producer. However, as has been pointed out by Jones and Sackley [

10], Raza et al. [

11], and Beckmann et al. [

12], uncertainties associated with other economies within the G7 (comprising of Canada, France, Germany, Italy, Japan, the United Kingdom (UK), and the U.S.), and China, also tend to drive gold-market volatility as many of the recent major crises (for example, the European sovereign debt crisis, “Brexit”, COVID-19) originated in these economies, and also due to the importance of their position as producers, exporters, and importers in the gold market. For further details, see

https://www.gold.org/goldhub/data/historical-mine-production,

https://www.worldstopexports.com/gold-exports-country/, and

https://www.worldstopexports.com/international-markets-for-imported-gold-by-country/ (accessed on 2 July 2021). Against this backdrop, in this paper, we forecast the quarterly realized variance (RV) of gold-price returns, and, in the process of doing so, we consider not only the role of uncertainties of all the G7 countries and China but also the respective international spillovers of uncertainty to the rest of the world, over the period from 1996Q1 to 2020Q4. Accounting for the total amount of international uncertainty spillovers of these major economies onto other countries, evidence of which is widespread (see, for example, Klössner and Sekkel [

13], Yin and Han [

14], Antonakakis et al. [

15], Kang and Yoon [

16]), renders it possible to better model worldwide uncertainty and its influence on global gold demand in a parsimonious manner, i.e., without incorporating the information from uncertainties of multiple other (135 to be exact, based on our data source, which we shall discuss later in detail) countries in the world. This approach is further vindicated by the fact that the network of international spillovers is so detailed that it has led to global convergence in terms of uncertainty (Christou et al. [

17]). The motivation to look at the need to consider uncertainty at the global level, rather than just the U.S., also emanates from the work of Fang et al. [

2] discussed above.

We measure RV in terms of the sum of squared daily returns over a quarter, which provides an observable (unconditional) metric of volatility, which is otherwise a latent process, and, hence, follow the existing literature discussed above in terms of the measure of volatility. To the best of our knowledge, this is the first paper that evaluates the out-of-sample forecasting power of uncertainties of the G7 and China and its international spillovers for gold returns variance. Further, since market agents care not only about the nature of variance, but also about its level, with traders making distinctions between upside (“good”) and downside (“bad”) variance (Giot et al. [

18]), we also forecast good RV (the sum of squared daily positive returns only over a quarter) and bad RV (the sum of squared daily negative returns only over a quarter), besides overall RV. Given that our data sample spans a 25-year period (1996–2020) of 100 quarterly observations, and we have 16 predictors, besides one lag of RV that captures the well-known persistence of RV associated with the gold market (Asai et al. [

19]), as our econometric approach, we use a machine-learning technique known as least absolute shrinkage and selection operator (Lasso), proposed by Tibshirani [

20]. The Lasso estimator is a well-established regression technique that aims at both predictor selection and model regularization (that is, the process of limiting the dimension of a forecasting model so as to prevent overfitting) in order to enhance the prediction accuracy and interpretability of the resulting forecasting model. Our paper, thus, adds to the already existing large literature on the predictability of gold-returns volatility based on a wide array of models and macroeconomic, financial, and behavioral predictors (see, for example, Pierdzioch et al. [

21], Fang et al. [

22], Nguyen and Walther [

23], Salisu et al. [

24], Bonato et al. [

25]) by considering the role of uncertainties of major economies of the world and the associated international spillovers. We also would like to emphasize that our aim was not to introduce new econometric or forecasting methods in this paper but to provide a novel and important application of forecasting RV of the gold market, based on the informational content of uncertainty of major economies, and also the corresponding international spillovers to the rest of the world.

The remainder of the paper is organized as follows: In

Section 2, we describe our data. In

Section 3, we briefly discuss the forecasting models, along with the Lasso approach used to estimate these models. In

Section 4, we present the results from our forecasting experiment. In

Section 5, we conclude.

2. Data

As far as the gold price is concerned, we use daily data of the U.S. dollar-based (per troy ounce) gold-fixing price (at 3:00 P.M. London time) in the London Bullion Market. The data is downloadable from the FRED database of the Federal Reserve Bank of St. Louis at:

https://fred.stlouisfed.org/series/GOLDPMGBD228NLBM (accessed on 2 July 2021). After transforming the data to daily log-returns, we compute quarterly overall, upside (“good”), and downside (“bad”) realized variances by summing up the daily squared returns, positive returns only, and negative returns only over a specific quarter, and

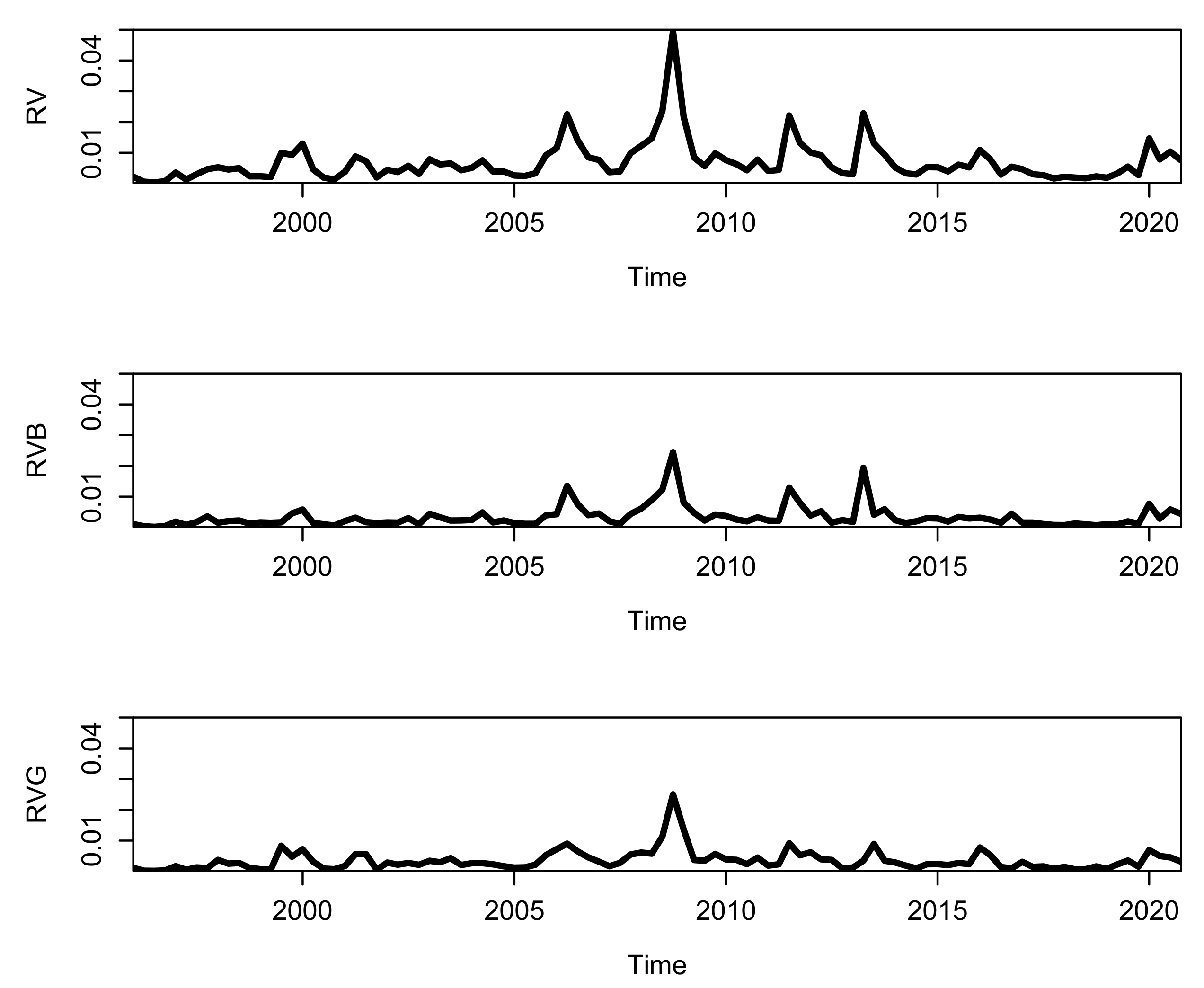

Figure 1 plots the realized variance along with its “good” and “bad” counterparts. The peak in the realized variance in the final quarter of the year 2008 witnesses the impact of the Global Financial Crisis on gold-price dynamics.

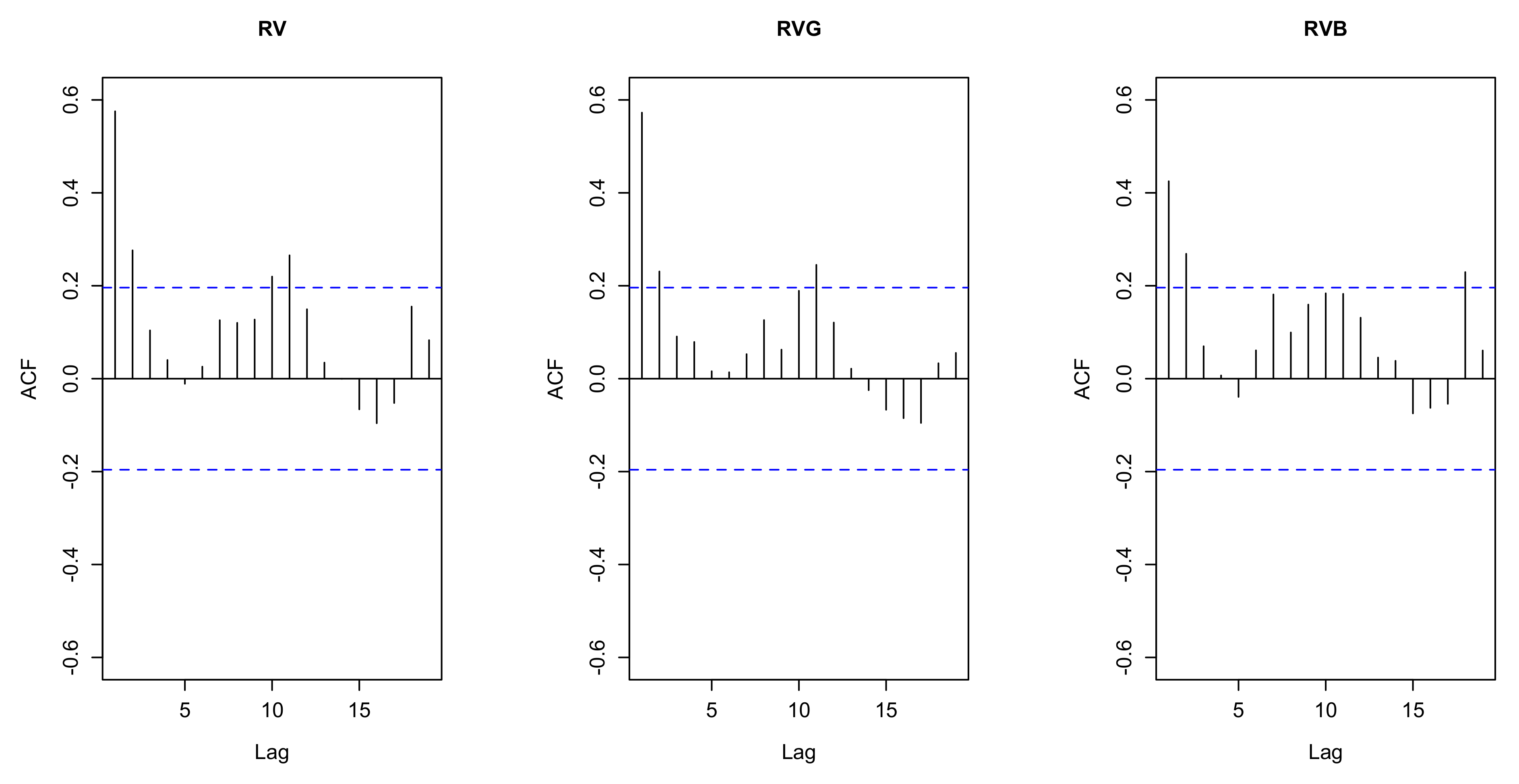

Figure 2 plots the corresponding autocorrelation functions. The autocorrelation functions show that using a first-order autocorrelated process as our benchmark model should suffice to capture the persistence of realized variance.

One must realize that uncertainty is a latent variable, and, hence, researchers need to find ways to measure it. In this regard, besides the widely-studied metrics of uncertainty associated with financial markets (such as implied-volatility indices, like the popular VIX, realized volatility, idiosyncratic volatility of equity returns, corporate spreads), there are primarily three approaches to quantify uncertainty (Gupta et al. [

26]): (1) A text-based approach builds on the idea that uncertainty can be measured by searching major newspapers or country reports for terms related to (economic and policy) uncertainty, and then to use the results to construct indices of uncertainty; (2) another approach is to measure uncertainty by estimating stochastic volatility extracted from various types of small and large-scale structural models related to macroeconomics and finance; and (3) yet another approach is to compute uncertainty based on the dispersion of professional forecaster disagreement. In our empirical research, we use the first approach outlined by Ahir et al. [

27]. Our decision to use the first approach reflects that it does not require any complicated estimation of a large-scale model and, hence, is not model-specific. Besides, the uncertainty data, and the associated spillover of the G7 economies and China on to other economies in the world, are available publicly for download (

https://worlduncertaintyindex.com/data/ (accessed on 2 July 2021)).

Ahir et al. [

27] construct quarterly indices of economic uncertainty for 143 countries (37 countries in Africa, 22 in Asia and the Pacific, 35 in Europe, 27 in the Middle East and Central Asia, and 22 in the Western Hemisphere, of which we use 8 for the G7 and China), from 1996 onwards using frequency counts of “uncertainty” (and variants thereof) in the quarterly Economist Intelligence Unit (EIU) country reports. The EIU reports discuss significant political and economic developments in a country, and also lay out analyses and forecasts of political, policy, and economic conditions. The analyses are undertaken by country-specific teams of analysts and a central EIU editorial team. In order to make the uncertainty indexes comparable across the large number of countries, the raw counts are scaled by the total number of words in each report. In addition to the uncertainty indexes of each of the 143 countries, the dataset of Ahir et al. [

27] also comprises the uncertainty spillover metrics for the G7 and China, which, in turn, determines the choice of the countries that we analyze in our empirical study, and the quarterly sample period of 1996Q1 to 2020Q4, which is the latest available data at the time of writing this paper. Specifically, the eight (G7 plus China) uncertainty spillover indexes of one of these particular countries to the remaining 142 countries is computed by counting the percent of word “uncertain” (or its variant) which is mentioned within a proximity to a word related to a particular G7 country or China in the EIU country reports. The spillover index is then rescaled by multiplying with 1,000,000, with a higher number, suggesting higher uncertainty related to the specific country involving the G7 or China, and vice versa. For further details regarding the words related to the G7 and China that are used, the reader is referred to Ahir et al. [

27]. We use the cross-sectional sum over time to obtain the total uncertainty spillover (on to the remaining 142 economies) indexes of each of these 8 countries.

We would like to point out that the data frequency we use for our analysis, i.e., quarterly, and the sample period, i.e., 1996Q1 to 2020Q4, is purely driven by the availability of data of the metrics of uncertainty of the G7 countries and China, and its associated spillovers to the rest of the world.

3. Methodologies

For the forecasting analysis, we use a parsimonious autoregressive model as our benchmark model. The benchmark model uses an intercept and the contemporaneous (that is, period-

t) realized variance as predictors. In order to study the predictive value of uncertainty,

U, and international spillovers,

S, we then enlarge the benchmark model as specified in the following equations:

The index h denotes the forecast horizon, denotes an error term, and and denote the number of uncertainties and international spillovers. For longer-term forecasts (that is, for ), we use, as in a long-horizon regression, the average realized variance over the forecast horizon as our dependent variable. We set ,2, and 4 and, thereby, study the predictive value of uncertainty and spillovers over a short term, a medium-term, and a long term-forecast horizon. In this process, we structure the data matrix such that the total number of forecasts is the same across all three forecast horizons.

In order to measure the realized variance of gold returns, we use the sum of squared daily returns per quarter. In other words, we use the following widely-studied classical estimator of

(see, e.g., Andersen and Bollerslev [

28]):

where

denotes the daily return (computed as the log-difference in consecutive daily prices), and

denotes the number of trading days per quarter. In one of our robustness analyses, we shall also use

as our dependent variable. In empirical applications, researchers often use the term “volatility” to refer to the square root of

. Finally, we also consider upward (“good”,

) and downward (“bad”,

) realized variance as dependent variables in our forecasting models. Like Barndorff-Nielsen et al. [

29], we compute bad and good realized variance as follows (

indicator function):

Given that the dimension of our forecasting models becomes relatively large (relative to the length of the sample period) once we add the numerous uncertainties and international spillovers to the benchmark forecasting model, we estimate the core model by the standard ordinary-least-squares technique and the extended models by means of the least absolute shrinkage and selection operator (Lasso) estimator. The Lasso estimates of the coefficients,

minimize the following expression (

the number of observations; for a textbook exposition of the Lasso, see, for example, Hastie et al. [

30]):

The minimization problem specified in Equation (

8) shows that the Lasso estimator shrinks the magnitude of the coefficient vectors toward zero, where shrinkage takes place under the

norm. When the shrinkage parameter,

, is sufficiently large, the Lasso estimator shrinks and even sets to zero some of the coefficients. In other words, the Lasso estimator can be interpreted as a predictor-selection technique. Because the choice of a “good” value of the shrinkage parameter is crucial, we use 10-fold cross validation to identify the value of the shrinkage parameter,

, that minimizes the minimum mean cross-validated error (using instead 5-fold cross-validation as a robustness check gave results, available from the authors upon request) that are qualitatively similar to those we shall report in

Table 1 and, thus, corroborated our main finding that uncertainty tends to play a more prominent role than international spillovers for out-of-sample forecasting of gold RV.). All estimations are carried out in the R environment for statistical computing (R Core Team [

31]), and the R add-on package “glmnet” (Friedman et al. [

32]) is used for estimation of the Lasso.

We use a a recursively expanding estimation window to compute out-of-sample forecasts, where we use data for a training period of 10 years to start the estimations. In order to test for significant differences in forecasting performance across our four different forecasting models, we use the Clark and West test [

33]. The test is implemented by estimating a regression of the quantity

on a constant. A hat above a variable denotes a forecast of

, and the subindices

A and

B refer to the two models being studied. Model

A denotes the benchmark model with an intercept and the period-

t realized variance as predictors, while

B denotes the larger model that features, in addition, uncertainty and/or international spillovers. The null hypothesis of the CW test is that the models under scrutiny produce an equal out-of-sample mean-squared prediction error (MSPE), the alternative hypothesis is that Model B produces a smaller MSPE than Model A. The CW test, hence, is a one-sided test, which is standard when comparing forecasts from nested forecasting models. The null hypothesis can be rejected if the t-statistic of the constant in this regression model is significantly positive. We use Newey-West robust standard errors to assess the significance of the t-statistic.

4. Empirical Results

The forecasting results (

p-values of the CW test) that we report in Panel A of

Table 1 show that, at the medium and especially at the long forecasting horizon, uncertainty does have predictive value for subsequent realized variance. The test results for international spillovers are only weakly significant at the short forecast horizon. The significance of the test results for uncertainty strengthens when we use a somewhat longer training period in Panel B. The test results for international spillovers also strengthen, especially at the medium forecasting horizon, but overall remain weak. We report in Panel C results for a shorter out-of-sample period, where we drop some forecasts at the end of the sample period in order to control for the potential exceptional impact of the recent COVID-19 pandemic. The results show that uncertainty has predictive value mainly at the long forecasting horizon, while test results for international spillovers, in turn, are significant at the short horizon. We conclude that the recent COVID-19 pandemic has strengthened the predictive value of uncertainty for realized variance. Finally, we observe that adding simultaneously both uncertainty and international spillovers as predictors to the forecasting model (column “All”, which is this forecasting model, features both uncertainty and international spillovers as predictors; the benchmark model still uses an intercept and the contemporaneous realized variance as predictors) does not improve forecasting performance in a systematic way. Only the test results for the medium and long forecasting horizon are significant, and only when we study the longer training period. To sum up, the test results support the view that uncertainty has predictive value for realized variance, mainly at the medium and long forecasting horizon, while the evidence of an effect of spillovers on subsequent realized variance mainly is centered at the short forecasting horizon.

Table 2 summarizes, as a robustness check, root-mean-squared-forecasting error (RMSFE) ratios and mean-absolute-forecasting error (MAFE) ratios. The ratios are defined as the RMSFE (MAFE) of the benchmark model (that is, the model that features an intercept and the period-

t realized variance as predictors) and the extended model (the model that features also uncertainty and/or international spillovers). With one exception, the ratios exceed unity and, thus, indicate a superior forecasting performance of the extended model. Moreover, the ratios are (again with one exception) larger for the models that feature uncertainty than for the models that feature international spillovers as additional predictors. Combining uncertainty and international spillovers in a unified model (that is, using “All” predictors) yields better results than the benchmark model, but using the “All” predictors model rather than focusing on uncertainty alone is advantageous in terms of forecasting performance only for the short forecasting horizon.

Table 3 summarizes the test results for good and bad realized variance. In terms of bad variance, we again observe significant test results for uncertainty at the medium and long forecast horizons in Panels A to C (and in Panel B, where we use a longer training period, also at the short forecast horizon). Further, the test results for international spillovers are significant at the short and the medium forecast horizons in Panel A and for all three forecast horizons in Panel C (where we delete some forecasts computed at the end of the sample period). In addition, the test results are significant when we add both uncertainty and international spillovers at the same time to the forecasting model. Turning to the test results for good variance, we find that uncertainty has significant predictive value for realized variance mainly at the long forecast horizon (Panels D to F), while the test results for international spillovers are statistically insignificant (with one exception, but only at the 10% level of significance). There is also some evidence, mainly concentrated at the long forecasting horizon, that the combined use of uncertainty and international spillovers in a unified forecasting model has predictive value.

Table 4 summarizes the results for

. Again, we find evidence that uncertainty has predictive value for

at the medium and, especially, the long forecast horizon. The test results for international spillovers, in contrast, are insignificant. On balance, thus, our empirical findings suggest that the predictive value of uncertainty for realized variance is more robust to the specific details a researcher uses to develop a forecasting model than the predictive value of international spillovers.

As yet another robustness check, we report in

Table 5 the results we obtain when we forecast the natural logarithm of

, as one often encounters such a specification in earlier literature. The test results lend further support to the notion that uncertainty adds to predictive value of the forecasting model at the medium and long forecast horizon. The test results for international spillovers, in turn, are not significant, corroborating that the predictive value of international spillovers is more sensitive to the details of the forecasting model than the predictive value of uncertainties.

Where does the predictive value of uncertainty come from? In order to shed light on this question, we report in

Table 6 the inclusion of the various predictors (in percent) in the Lasso models. The results show that, at the medium and long forecasting horizons, uncertainties originating in China and the U.S. are important sources of predictive value. In addition, Italy and, to a lesser extent, France, appear to be important sources of uncertainty, which is likely to reflect the impact of the European sovereign debt crisis. The international spillover predictors, in turn, are less often included in the forecasting models, as one would have expected given the results of the CW tests. Interestingly, the Lasso estimator selects at the short forecasting horizon relatively often the international spillovers from Italy and, at the medium forecasting horizon, from Germany and France.

5. Conclusions

Being based on a dataset for the group of G7 countries and China, our results show that uncertainty and international spillovers have predictive value in an out-of-sample forecasting exercise for the realized variance of gold returns. The predictive value of uncertainty is mainly concentrated at the medium and long forecasting horizons, while the predictive value of international spillovers is concentrated at the short and medium forecasting horizons. Moreover, our results show that the predictive value of uncertainty is more robust across the various model specifications that we have studied than the corresponding role of international spillovers, which is likely due to the fact that, besides being major players on the demand- and supply-side of the gold market, the central banks of the G7 and China features prominently in the Top 10 countries in terms of holding of gold reserves, according to the recent figures from the World Gold Council. China, Italy, and the U.S. appear to be important sources of uncertainty that help to predict the realized variance of gold returns.

With volatility being a key input in investment decisions (Poon and Granger [

34]), the predictive value of uncertainties emanating in the G7 and China for gold-returns variance should be of paramount importance to traders in the gold market in gauging accurately the risks of investing in this precious metal, and, in the process, construct optimal portfolios. As discussed in the introductory section of this paper, higher uncertainty is a key determinant of gold-market volatility due to more trading in this precious metal, and since uncertainty is a latent variable, gold-price movements can be used as a metric of global uncertainty by policymakers (Piffer and Podstawski [

35]), and design in a timely way appropriately tailored fiscal and monetary policy responses to shelter economies from the well-established recessionary impact of uncertainty (Gupta et al. [

36]). Having pointed out the important implications of our results, it is also necessary to acknowledge one limitation of our study in terms of the low-frequency of our data. Ideally, we would have preferred to conducted the forecasting exercise of realized variance of gold at a higher frequency (as done in the existing literature using primarily U.S.-based proxies of uncertainties), as this would be of greater importance to investors and policymakers in making timely portfolio and policy decisions, but the uncertainty spillover indexes are available only quarterly and, hence, constrain us in our ability to provide higher-frequency (say, for example, daily or monthly) results. In addition, we could have utilized a MIDAS-GARCH framework, too, for providing gold volatility forecasts at a daily frequency, but then this framework would not have been able to handle as many as 16 of the uncertainty indexes simultaneously as used by us in this paper.

As part of future research, it is interesting to go beyond our analysis and to study other prominent precious metals, like platinum, palladium, rhodium, and silver, which, too, have been known to have safe-haven characteristics (Baur and Smales [

37]), based on updated data that stretches into 2021, if and when available, for our uncertainty-based predictors, to better capture the role of heightened global uncertainty due to the ongoing impact of the COVID-19 pandemic.

{kind=link}

{kind=link}