Stochastic Capital–Labor Lévy Jump Model with the Precariat Labor Force

Abstract

:1. Introduction

2. Properties of the Solution

2.1. The Global Positive Solution Existence and Uniqueness

2.2. Stochastic Ultimately Boundedness

3. Stochastic Extinction of Free Jobs and the Labor Force

4. Stochastic Extinction of Capital Labor

5. Stochastic Persistence

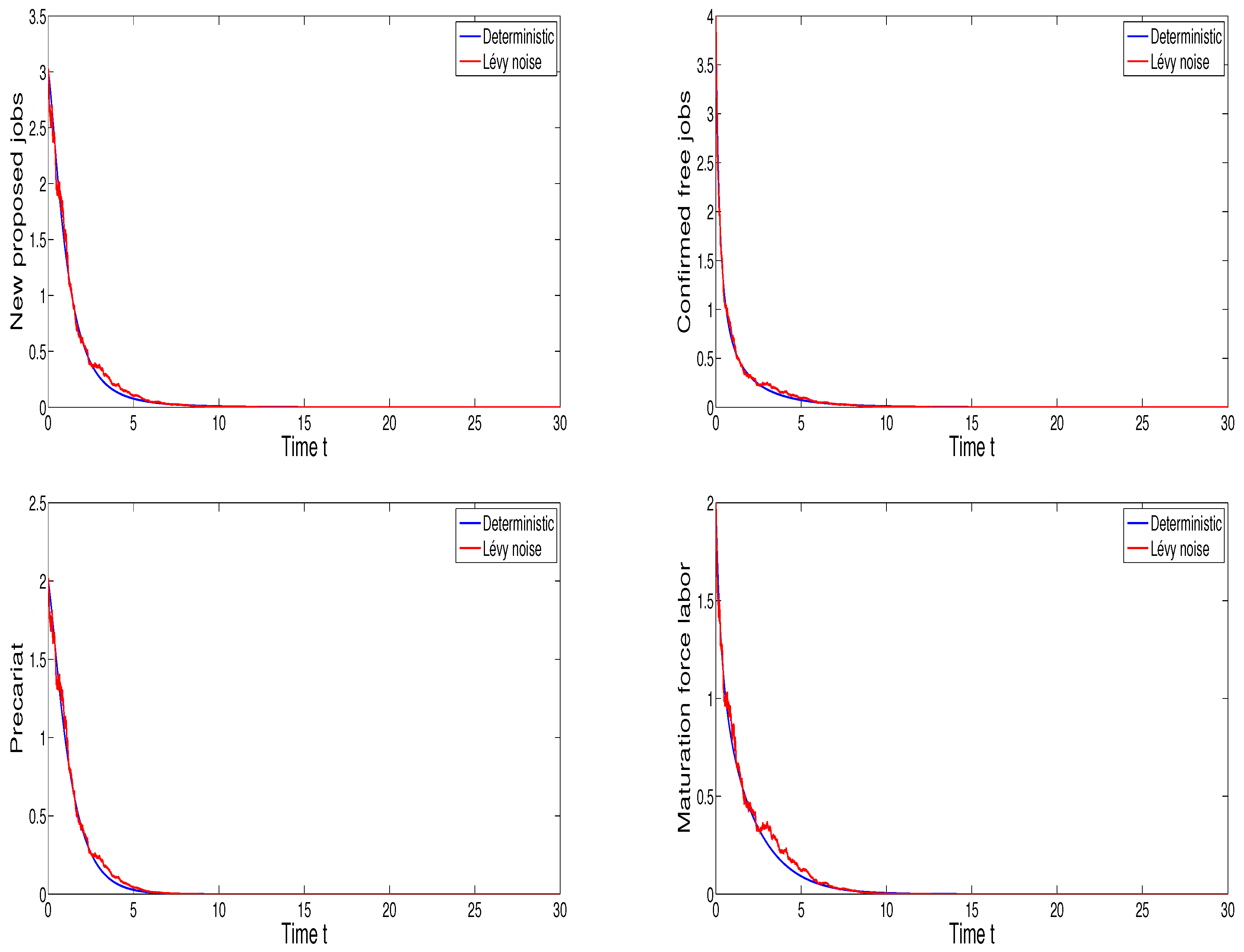

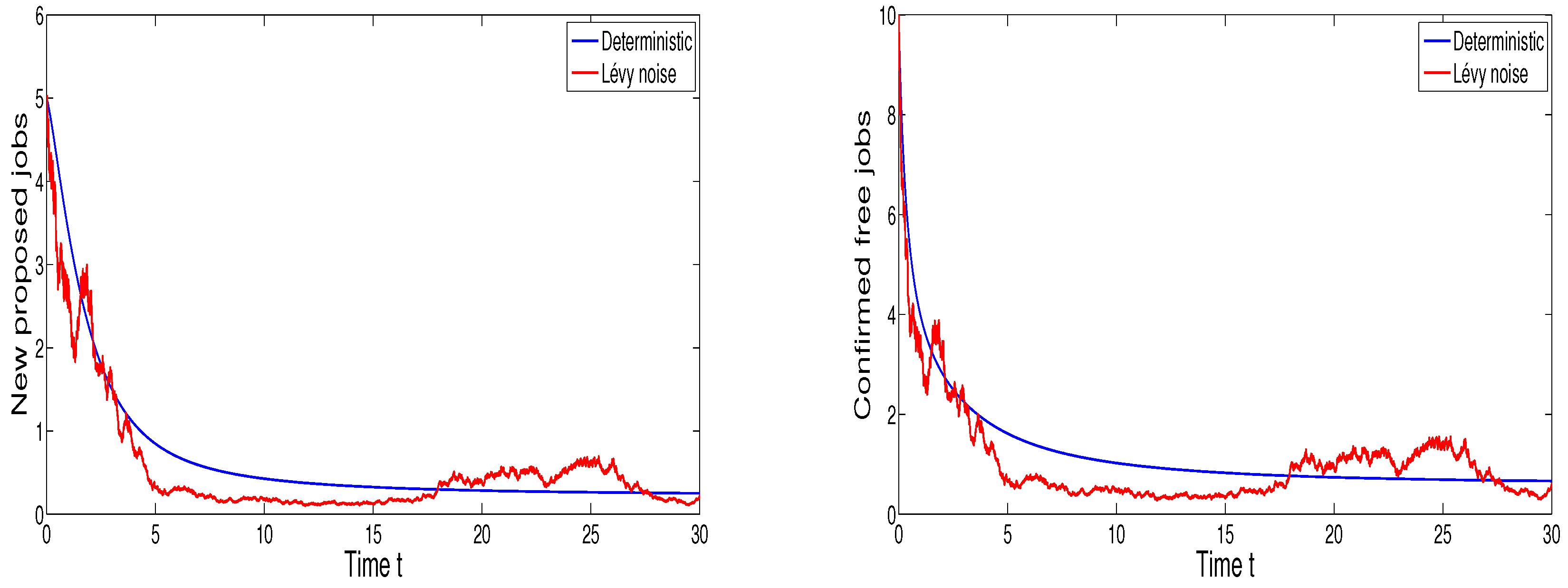

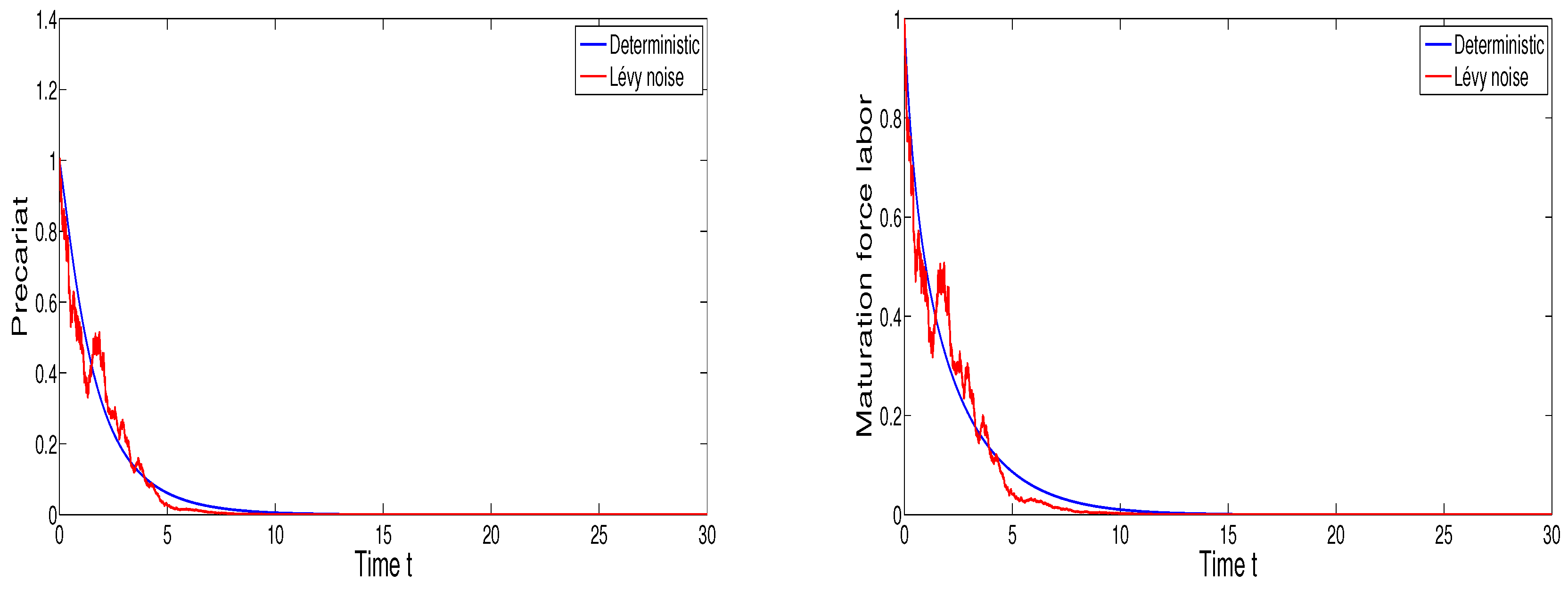

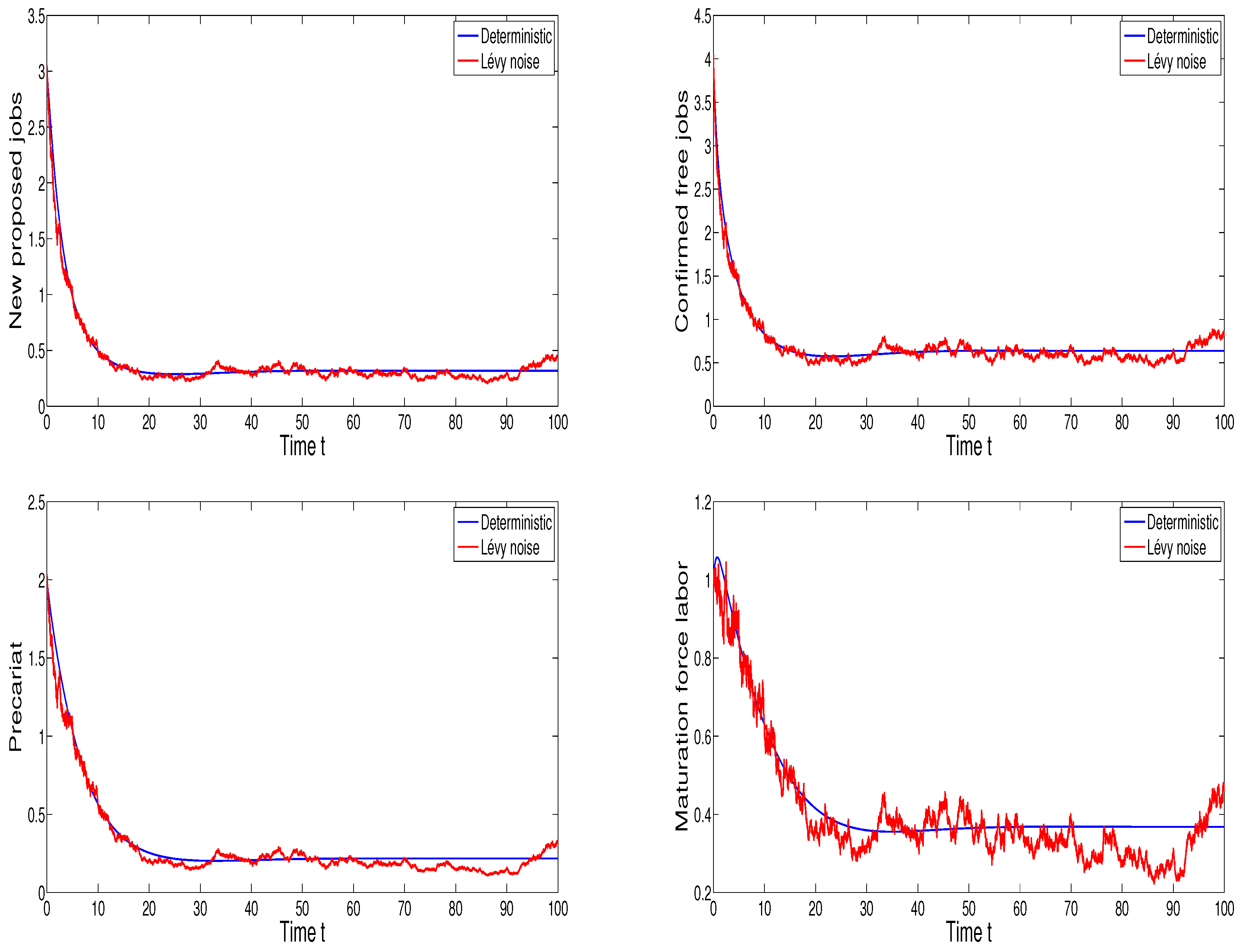

6. Numerical Simulations

7. Conclusions and Discussion

Funding

Conflicts of Interest

References

- Tcherneva, R.P. When a rising tide sinks most boats: Trends in US income inequality. Real World Econ. Rev. 2015, 71, 64–74. [Google Scholar]

- Piketty, T.; Saez, E.; Zucman, G. Distributional National Accounts: Methods and Estimates for the United States. Q. J. Econ. 2018, 133, 553–609. [Google Scholar] [CrossRef] [Green Version]

- Piketty, T. Capital in the Twenty-First Century; Harvard University Press: Cambridge, MA, USA, 2013. [Google Scholar]

- David, A.; Katz, L.F.; Kearney, M.S. The Polarization of the US Labor Market; NBER Working Paper; National Bureau of Economic Research: Cambridge, MA, USA, 2006. [Google Scholar]

- Kaplan, N.S.; Rau, J. It’s the Market: The Broad-Based Rise in the Return to Top Talent. J. Econ. Perspect. 2013, 27, 35–56. [Google Scholar] [CrossRef] [Green Version]

- Acemoglu, D.; Pascual, R. Robots and Jobs: Evidence from US Labor Market; NBER Working Paper; National Bureau of Economic Research: Cambridge, MA, USA, 2017. [Google Scholar]

- David, A.; Salomons, A. Is Automation Labor-Displacing? Productivity Growth, Employment, and the Labor Share; Brookings Papers on Economic Activity; Brookings Institution: Washington, DC, USA, 2018. [Google Scholar]

- Bloom, N. Corporations in the Age of Inequality; Harvard Business Review; 2017. Available online: https://hbr.org/cover-story/2017/03/corporations-in-the-age-of-inequality (accessed on 1 August 2017).

- Dorn, D.; Katz, L.F.; Patterson, C.; Van Reenen, J. Concentrating on the Fall of the Labor Share. Am. Econ. Rev. 2017, 107, 180–185. [Google Scholar]

- Baker, D. The Upward Redistribution of Income: Are Rents the Story? CEPR Working Paper; Center for Economic and Policy Research: Washington, DC, USA, 2015. [Google Scholar]

- Howell, D.R.; Arne, L.K. Declining Job Quality in the United States: Explanations and Evidence; Washington Center for Equitable Growth: Washington, DC, USA, 2019. [Google Scholar]

- Stiglitz, J.E. The Price of Inequality; W.W. Norton: New York, NY, USA, 2013. [Google Scholar]

- Weil, D. The Fissured Workplace; Harvard University Press: Cambridge, MA, USA, 2014. [Google Scholar]

- Naidu, S. A Political Economy Take on W/Y. In After Piketty; Boushey, H., DeLong, J.B., Steinbaum, M., Eds.; Harvard University Press: Cambridge, MA, USA, 2017; pp. 99–125. [Google Scholar]

- Standing, G. Work after Globalization: Building Occupational Citizenship; Edwin Elgar: Northhampton, MA, USA, 2009. [Google Scholar]

- Wolff, N.E.; Zacharias, A. Class structure and economic inequality. Camb. J. Econ. 2013, 37, 1381–1406. [Google Scholar] [CrossRef] [Green Version]

- Standing, G. The Precariat; Bloomsbury: New York, NY, USA, 2014. [Google Scholar]

- Standing, G. The Precariat and Class Struggle. RCCS Annu. Rev. 2015, 7, 3–16. [Google Scholar] [CrossRef] [Green Version]

- Greenstein, J. The Precariat class structure and income inequality among US workers: 1980–2018. Rev. Radic. Political Econ. 2020, 52, 447–469. [Google Scholar] [CrossRef]

- International Labor Organization (ILO). Work Employment and Social Outlook: The Changing Nature of Jobs; International Labor Organization: Geneva, Switzerland, 2015. [Google Scholar]

- Breman, J.; van der Linden, M. Informalizing the Economy: The Return of the Social Question at a Global Level. Dev. Chang. 2014, 45, 920–940. [Google Scholar] [CrossRef]

- Riad, D.; Hattaf, K.; Yousfi, N. Dynamics of capital-labour model with Hattaf-Yousfi functional response. Br. J. Math. Comput. Sci. 2016, 18, 1–7. [Google Scholar] [CrossRef]

- Zine, H.; Danane, J.; Torres, D.F. A Stochastic Capital-Labour Model with Logistic Growth Function. arXiv 2022, arXiv:2202.05348. [Google Scholar]

- Danane, J.; Allali, K.; Hammouch, Z. Mathematical analysis of a fractional differential model of HBV infection with antibody immune response. Chaos Solitons Fractals 2020, 136, 109787. [Google Scholar] [CrossRef]

- Danane, J.; Hammouch, Z.; Allali, K.; Rashid, S.; Singh, J. A fractional-order model of coronavirus disease 2019 (COVID-19) with governmental action and individual reaction. Math. Methods Appl. Sci. 2021. [Google Scholar] [CrossRef] [PubMed]

- Zhang, T.-W.; Zhou, J.-W.; Liao, Y.-Z. Exponentially stable periodic oscillation and Mittag-Leffler stabilization for fractional-order impulsive control neural networks with piecewise Caputo derivatives. IEEE Trans. Cybernet. 2021, 52, 9670–9683. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Danane, J. Stochastic Capital–Labor Lévy Jump Model with the Precariat Labor Force. Math. Comput. Appl. 2022, 27, 93. https://doi.org/10.3390/mca27060093

Danane J. Stochastic Capital–Labor Lévy Jump Model with the Precariat Labor Force. Mathematical and Computational Applications. 2022; 27(6):93. https://doi.org/10.3390/mca27060093

Chicago/Turabian StyleDanane, Jaouad. 2022. "Stochastic Capital–Labor Lévy Jump Model with the Precariat Labor Force" Mathematical and Computational Applications 27, no. 6: 93. https://doi.org/10.3390/mca27060093

APA StyleDanane, J. (2022). Stochastic Capital–Labor Lévy Jump Model with the Precariat Labor Force. Mathematical and Computational Applications, 27(6), 93. https://doi.org/10.3390/mca27060093