1. Introduction

Cryptocurrencies serve as a peer-to-peer digital currency where every detailed transaction occurs in a secured way. The transactions are further stored in a block, known as Blockchain. The security features made cryptocurrency a popular and well-known trading platform for investors. Cryptocurrencies have been growing dramatically, gaining popularity and capitalization. Bitcoin is the first decentralized cryptocurrency developed by Satoshi Nakamoto [

1], and it has become the world’s most valuable cryptocurrency. With the vast transaction volume of cryptocurrencies, many types of currencies were introduced into the cryptography world. Some well-known cryptocurrencies are Ethereum and Ripple, among others.

This study focuses on cryptocurrency price prediction. The cryptocurrency price prediction is a time series problem that can be solved by using deep learning regression techniques. Although price prediction of cryptocurrency is challenging, developing cryptocurrency price prediction algorithms is worthwhile because it plays a vital role for cryptocurrency traders. Inspired by the success of deep learning regression models in a wide spectrum of applications, this paper proposes a hybrid regression model that amalgamates a 1-dimensional convolutional neural network (1DCNN) and a stacked gated recurrent unit (GRU), into the 1DCNN-GRU model for cryptocurrency price prediction. Three cryptocurrency historical price datasets are first collected from the cryptocurrency exchange website. Subsequently, the datasets are subjected to some data pre-processing, including normalization and missing value removal before passing into the 1DCNN-GRU model for representation learning and price prediction. The 1DCNN layer plays the role of extracting the salient features in the historical price data. The extracted features are then passed into the stacked GRU for temporal encoding where the long-range dependencies are captured. The temporal encoding is then leveraged for the cryptocurrency price prediction. The predicted price is compared against the real price and the root mean square error is computed. The main contributions of this paper are as follows.

The cryptocurrency historical price data are acquired from the cryptocurrency exchange website. As the daily or hourly interval data are susceptible to information loss, this study leverages the one-minute interval data for more accurate price prediction.

The feature scaling is performed on the cryptocurrency historical price data by normalization. In addition, the data is further pre-processed to remove the missing values that might affect model learning. The clean data are then partitioned into the training set and testing set for model learning and price prediction.

A hybrid 1DCNN-GRU model is proposed for representation learning and cryptocurrency price prediction. The 1DCNN model encodes the prominent patterns in the historical price data, hence producing discriminative features to represent the historical price data. Thereafter, the stacked GRU model captures the long-range dependencies in the features, thus alleviating the gradient vanishing problems.

2. Related Works

This section describes some existing works in cryptocurrency price prediction. There are many deep learning models that are adopted for price prediction [

2,

3,

4,

5,

6,

7,

8,

9,

10,

11,

12,

13,

14].

In early work, Sin et al. (2017) [

15] proposed a forecasting algorithm that can be applied to different financial, engineering, and medical tasks. The algorithm integrated an artificial neural network (ANN) and a multilayer perceptron (MLP). From the experiments, the incorporation of MLP into ANN increased the Bitcoin price prediction accuracy from about 58% to 63%.

A deep learning algorithm, known as the Facebook Prophet for Bitcoin price prediction was adopted by Yenidogan et al. (2018) [

16]. A three-fold splitting technique was conducted to provide optimum ratios for training, testing, and validation sets. The experimental results showed that the PROPHET algorithm outperformed the ARIMA algorithm, in which Prophet obtained a lower root mean square error (RMSE) of 652.18 compared to 817.01.

McNally et al. (2018) [

17] leveraged several deep learning algorithms to predict the price of Bitcoin. In the early process, functional patterns were extracted from the data by feature engineering. The experimental results demonstrated that the long short-term memory (LSTM) model achieved the highest accuracy of 52.78% while recurrent neural networks (RNN) achieved the lowest accuracy of 5.45%.

Various regression techniques were presented by Phaladisailoed et al. (2018) [

18] to predict Bitcoin prices by using Keras libraries and scikit-learn. The dataset was taken from Kaggle where it consists of one-minute interval data on the Bitcoin exchange website Bitstamp. The best results showed that R-Square of 99.2% was obtained by the LSTM and GRU models.

Jiang (2020) [

19] proposed deep learning methods to forecast Bitcoin prices by gathering and reorganizing data on the Bitcoin price per minute to hours. The dataset was pre-processed, followed by mini-batch and min-max normalization before feeding it into the regression models. The work proposed a few deep learning networks such as MLP, RNN with the extension of LSTM, and GRU to predict future Bitcoin price. The experimental results showed that the MLP model, with the involvement of two layers of GRU achieved the best result, which had the minimal RMSE of 19.020.

Politis et al. (2021) [

20] leveraged multiple deep learning models for predicting the price of Ethereum. Feature selection was performed to reduce the dataset complexity and anomalies. The ensemble model was implemented with the combination of LSTM, GRU and/or temporal convolutional networks (TCN). In the daily forecast experimental result, the ensemble model with LSTM, GRU, and Hybrid GRU-TCN had the best performance of 84.2% accuracy, whereas the LSTM-GRU model achieved the lowest RMSE of 8.6.

Another LSTM-GRU hybrid model was put forth by Tanwar et al. (2021) [

21] for cryptocurrency price prediction. The work considered Bitcoin as the parent currency and captured the movement direction of Bitcoin price. Subsequently, the movement direction was utilized to predict the price of Litecoin and Zcash with the inter-dependency assumptions between Bitcoin-Litecoin and Bitcoin-Zcash. With a one-day window size, the LSTM-GRU model recorded a mean squared error (MSE) of 0.02038 for Litecoin and 0.00461 for Zcash.

Livieris et al. (2021) [

22] proposed a multiple-input cryptocurrency deep learning model, also known as MICDL. The proposed approach utilized each cryptocurrency data as input in a convolutional layer, followed by a pooling layer and an LSTM layer. The classical structure of a deep learning neural network, such as a dense layer, batch normalization layer, dropout layer, and output layer were leveraged. The proposed CNN with an LSTM layer achieved 55.03% accuracy on the Bitcoin data, whereas accuracy of 51.51% was obtained for Ethereum data and 49.61% for Ripple data.

Zhang et al. (2021) [

23] presented a weighted and attentive memory convolutional neural network (WAMC) for cryptocurrency price prediction. The model consists of a GRU to establish the attentive memory for each input sequence, a channel-wise weighting module to learn the interdependencies among several cryptocurrencies, and a CNN to extract local temporal features of the historical price data. The proposed WAMC recorded an RMSE of 9.70 for Ethereum and 1.37 for Bitcoin.

Jay et al. (2020) [

24] devised stochastic neural networks for the price prediction of Bitcoin, Ethereum, and Litecoin. The work considered three factors, namely cryptocurrency exchange market statistics, blockchain data, and social sentiment as the neural networks’ input. In order to address the randomness in the factors, the stochastic layers were incorporated into the MLP and LSTM model. In comparison to the deterministic MLP and LSTM, the stochastic neural networks (MLP and LSTM) showed an average improvement of 4.84833% for Bitcoin, 4.15640% for Ethereum, and 4.74619% for Litecoin.

The price prediction of the same cryptocurrencies were performed by Sebastiao et al. (2021) [

25]. The authors devised a few machine learning models, including linear models, random forest, and support vector machine to examine the predictability of the cryptocurrencies. The experimental results showed that the best results were achieved by the ensemble of linear models, random forest, and support vector machine on Ethereum prices, which was at 63.33% of win rates of the strategies. In another way, linear models achieved optimal RMSEs on forecasting Ethereum and Litecoin prices, which were only 6.85 and 8.14, whereas random forest achieved an RMSE of 5.77 on forecasting Bitcoin prices.

Saadah et al. (2020) [

26] applied several machine learning and deep learning methods for predicting the price of Bitcoin, Ethereum, and Ripple. The methods include k-nearest neighbors, support vector machine, and LSTM. The experimental results demonstrated that the LSTM achieved the optimal RMSE for all three cryptocurrencies, with RMSE of 928.62 on Bitcoin, 11.69 on Ethereum, and 0.16 on Ripple.

Derbentsev et al. (2020) [

27] implemented machine learning approaches, namely random forest and gradient boosting machine to forecast cryptocurrency prices. Three cryptocurrencies were used, i.e., Bitcoin, Ethereum, and Ripple. The experiments showed that gradient boosting machine is able to better forecast the price compared to random forest, in which RMSE of 263.34 was obtained on Bitcoin, 5.02 on Ethereum, and 0.92 on Ripple.

The summary of the existing works is presented in

Table 1. Many existing works leveraged LSTM for price prediction, attributable to its gating mechanism that is able to capture the sequential and temporal information in the data. However, there might be noise or outliers in the raw historical price data; thus, this work first performs feature extraction by using 1DCNN to capture the salient features and suppress the noise in the data. Subsequently, GRU is leveraged to encode the long-range temporal information in the features. The details of the proposed hybrid model with 1DCNN and GRU are discussed in the next section.

3. Cryptocurrency Price Prediction with 1-Dimensional Convolutional Neural Network and Stacked Gated Recurrent Unit (1DCNN-GRU)

This section details the proposed 1DCNN-GRU model for cryptocurrency price prediction. The historical price data of three cryptocurrencies are first acquired, namely Bitcoin, Ethereum, and Ripple. Subsequently, the collected data are pre-processed to clean missing values. Thereafter, the cleaned data are fed into the hybrid 1DCNN-GRU model for model learning and price prediction.

Figure 1 illustrates the process flow of the cryptocurrency price prediction.

3.1. Data Acquisition

Three datasets were used for the cryptocurrency price prediction, namely Bitcoin, Ethereum, and Ripple.

The Bitcoin historical data [

28] were acquired from the Kaggle website. The provided one-minute interval data range from 1 January 2012 until 31 March 2021, which contain approximately 4.8 millions samples, including NaN values. Some columns in the data are open, high, low, close (OHLC) price, volume, and the weighted price. All the timestamps are in UNIX time. The NaN values indicate that no trade or activity happened at that time.

Figure 2 visualizes the Bitcoin closing price for the years 2012 to 2021.

The Ethereum historical data were collected from the Bitstamp exchange website. The data comprise around 396,403 samples at one-minute intervals. The Ethereum closing price of the year 2021 is shown in

Figure 3.

Ripple is another widely known cryptocurrency, which has slightly lower values compared to other cryptocurrencies. The Ripple historical data were also gathered from the Bitstamp exchange website. The historical data consist of around 396,403 samples, as displayed in

Figure 4.

3.2. Data Pre-Processing

Some pre-processing steps are performed to clean the cryptocurrency historical data, including feature selection, timestamp conversion, missing values removal, train-test split, and min-max scaling normalization.

As each dataset consists of many features, this work only utilizes three features for price prediction, namely timestamp, date, and closing price. Subsequently, timestamp conversion is carried out where the timestamp in UNIX is converted into the YY:MM:DD date format. The zeros and NaNs are filtered out by dropping the associated rows. To avoid huge data losses and to provide more timely and detailed prediction, the samples are taken at one-min intervals. Due to the inconsistency of historical data and high sampling rates, the historical data of one week are used. With these settings, the number of samples is 10,797 for Bitcoin and 10,834 for both Ethereum and Ripple. The samples are further partitioned into six days for the training set and one day for the testing set. Apart from that, the features are subjected to min-max scaling normalization that transforms each feature into the range [0, 1]. The min-max scaling suppresses the effects of outliers while preserving the relationships among the data values. The min-max scaling is computed as

3.3. 1-Dimensional Convolutional Neural Network and Gated Recurrent Unit

In this work, a hybrid model that integrates 1DCNN and GRU is proposed for cryptocurrency price prediction. The architecture of the proposed 1DCNN-GRU model is depicted in

Figure 5. The proposed 1DCNN-GRU comprises a 1D convolutional layer and two GRU layers with 256 units each.

The cryptocurrency historical price is a kind of time series data that captures the closing price over the time. Using the raw price data as the input might introduce noise and outliers, causing the regression model to learn on the insignificant data. Therefore, a 1DCNN is leveraged to extract the prominent patterns from the historical price data. In the 1-dimensional convolutional layer (Conv1D), the kernel slides along the temporal axis and encodes the price data into representative features. The Conv1D layer in the proposed model sets both kernel size and stride to 1; hence the convolution window will read one time step at one time. The Conv1D layer consists of 256 output filters in the convolution, thus producing 256-dimensional output space. The output of the Conv1D layer is passed into the subsequent GRU layer.

Two GRU layers are leveraged to encode the long-term dependencies of the extracted features. The ability of capturing long-term dependencies in GRU is attributable to the gating mechanisms. There are two gates in the GRU, namely update gate and reset gate. The update gate

at time step

t determines the information from the previous time steps to be passed to the future, defined as

where the weights

and

are multiplied with the input

and hidden states

, respectively. The results of the multiplication are summed and passed into a sigmoid activation function to squash the values between 0 and 1.

The reset gate

determines the past information to forget, where the computation is defined as

where the input

and hidden states

are multiplied with their corresponding weights

and

. The sum of the results is likewise fed into a sigmoid activation function to limit the output to the range between 0 and 1.

A new memory content

is then leveraged to store past information, defined as

where ⊙ denotes the element-wise product. The new memory content is determined by first multiplying the input

and hidden states

with the corresponding weights

W and

U. Thereafter, the element-wise product of the reset gate

and

is calculated. The product operation diminishes the information from the previous time step when the values of

close to 0. Then, the sum of

and

is regulated by a tanh function to keep the output within −1 and 1.

Following that, the final memory at the current time step

that determines the information to be passed to the next time step is calculated as

Having values close to 1 will retain the majority of the previous information, whereas values close to 0 will keep the most part of the current information.

Lastly, the output from the GRU layers is passed into a dense layer with one hidden unit for price prediction. The layer-wise architecture of the proposed 1DCNN-GRU is presented in

Table 2.

4. Hyperparameter Tuning

A hyperparameter tuning by grid search is performed to determine the optimal settings of the 1DCNN-GRU model. The hyperparameters that are involved in the hyperparameter tuning are optimizer, activation function, and batch size. The optimizers play the role of optimizing the model learning process to ensure the model converges optimally. In this work, four optimizers are considered, namely Adam, SGD, Adamax, and RMSProp. The activation function is the function in the Conv1D layer and GRU layers that transforms the input, enabling the model to learn and perform more complex tasks. Five activation functions are explored, which are sigmoid, softmax, ReLU, tanh, and linear. The batch size defines the number of samples that is used for error gradient computation in each model weights update. The RMSE is adopted as the evaluation metric of the cryptocurrency price prediction models. The RMSE is the square root of the average squared distance between actual and predicted values, defined as

where

n is the total number of predictions,

y is the real price, and

denotes the predicted price. The optimal settings are set to the hyperparameter values with the lowest RMSE.

Table 3 shows the experimental results of different hyperparameter values on the Bitcoin dataset. The lowest RMSE of 43.933 is obtained on the Bitcoin dataset when SGD optimizer, sigmoid activation function, and batch size of 16 are used. The experimental results on the Ethereum dataset are presented in

Table 4. It is observed that the lowest RMSE of 3.511 is achieved with the Adamax optimizer, softmax activation function, and batch size of 32. As for the Ripple dataset, the lowest RMSE of 0.00128 is recorded when the Adam optimizer, softmax activation function, and batch size of 32 are set, as shown in

Table 5. The experimental settings are given in

Table 6.

5. Experimental Results and Analysis

In this section, the performance of the proposed 1DCNN-GRU model is compared with the existing prediction models. All models are trained on the same one-minute interval historical data.

Table 7 presents the comparison results of the methods on Bitcoin, Ethereum, and Ripple datasets. In general, the RMSE of all methods on the Bitcoin dataset is the highest, followed by the Ethereum dataset, and the Ripple dataset yields the lowest RMSE. This is due to the difference in the price where higher prices tend to result in higher RMSE.

The experimental results show that the proposed 1DCNN-GRU outshines the methods in comparison. The proposed 1DCNN-GRU model records an RMSE of 43.933 on the Bitcoin dataset, 3.511 on the Ethereum dataset, and 0.00128 on the Ripple dataset. Compared to the GRU model [

19] alone, adding 1DCNN has reduced the RMSE on all datasets. This is attributable to 1DCNN that is able to learn local relationships and encode the cryptocurrency historical data into discriminative features. In doing so, the noise, outliers and insignificant data in the input are suppressed.

Apart from that, the proposed 1DCNN-GRU also showed much improvement in relation to the CNN-LSTM model [

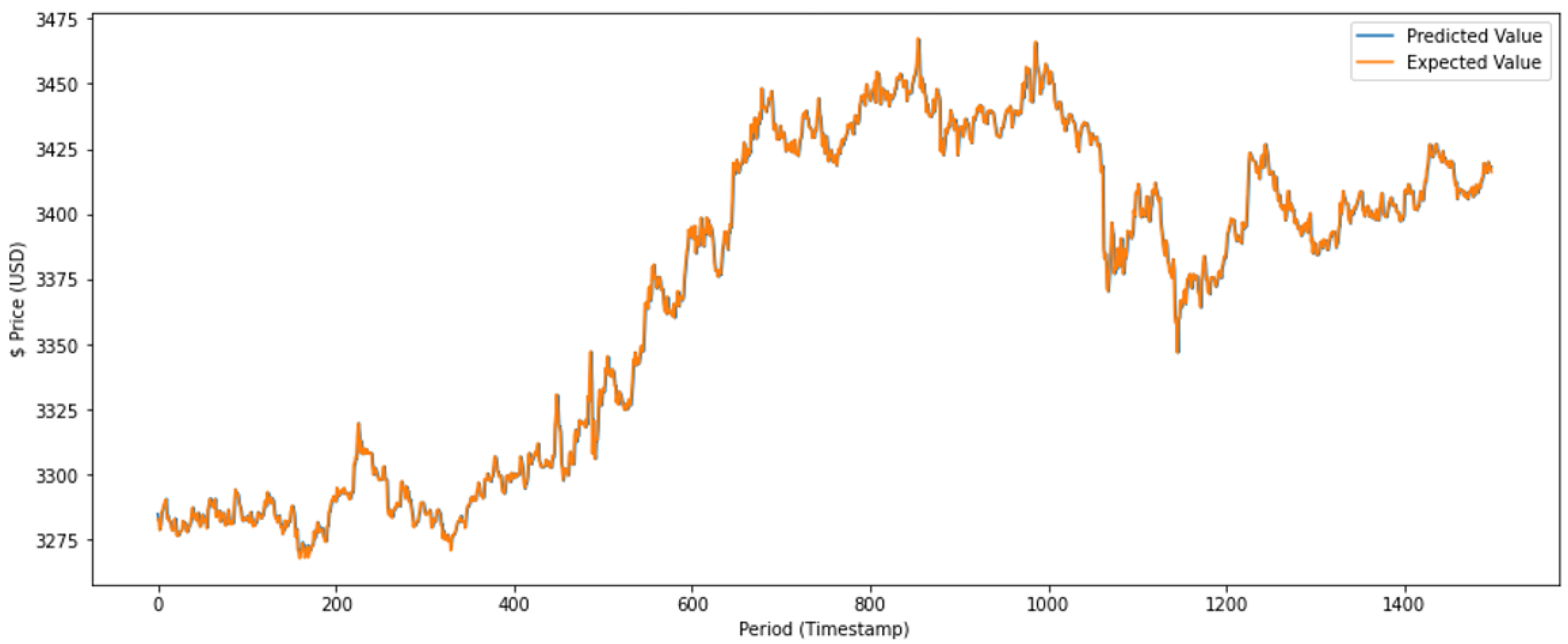

22]. The RMSE has reduced from 47.537 to 43.933 on the Bitcoin dataset, from 3.516 to 3.511 on the Ethereum dataset, and from 0.00135 to 0.00128 on the Ripple dataset. Both LSTM and GRU have their own strengths and perform well in different applications in which they utilize gating mechanisms to retain the historical information. In this application, the improvement corroborates the effectiveness of stacked GRU in capturing the long-range dependencies of the features, thus alleviating the vanishing gradient problems. The real and predicted prices of the Bitcoin, Ethereum, and Ripple are illustrated in

Figure 6,

Figure 7 and

Figure 8, respectively.

6. Conclusions

This paper presents a hybrid deep learning model that harnesses the strengths of 1DCNN and stacked GRU for cryptocurrency price prediction. The historical price of three cryptocurrencies are acquired, namely Bitcoin, Ethereum, and Ripple. The collected data are normalized and pre-processed to remove the missing values. Subsequently, the pre-processed data are passed into the hybrid 1DCNN-GRU model. The 1DCNN model transforms the price data into a discriminative representation that captures the significant patterns in the price data. Subsequently, the stacked GRU model encodes the long-range dependencies in the representation to mitigate past information loss problems. The gating mechanism of GRU determines the past and current information to be updated and reset, thus alleviating diminishing gradient problems. The experimental results demonstrate that the proposed 1DCNN-GRU outperforms the methods in comparison with the lowest RMSE values of 43.933 on the Bitcoin dataset, 3.511 on the Ethereum dataset, and 0.00128 on the Ripple dataset.

As a proof of concept and due to the limitations in computing resources, this study only utilizes the historical data for one week. Training the model on the cryptocurrency data for a longer time span should be able to further improve the generalization capability of the model. In addition to the closing price, other factors such as the seasonality trends, government policies and laws, social media, can also be considered as the input for price prediction model.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}