A Hybrid Stock Price Prediction Model Based on PRE and Deep Neural Network

Abstract

:1. Introduction

- (1)

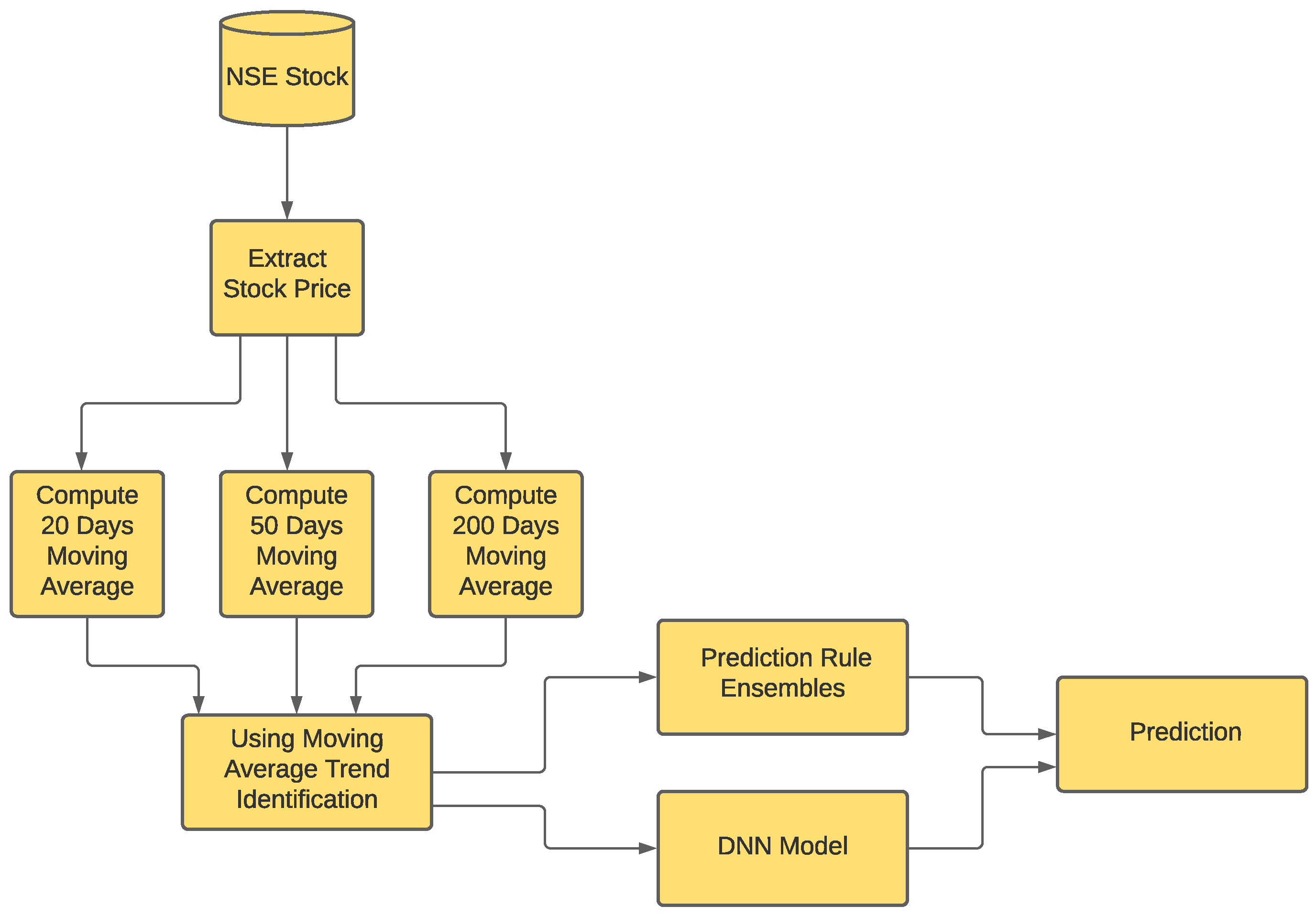

- First, stock technical indicators are considered to identify the uptrend in stock prices. We consider moving average technical indicators: moving average 20 days, moving average 50 days, and moving average 200 days.

- (2)

- We propose a hybrid stock prediction model using the PRE and DNN.

2. Literature Reviews

3. Data Specification

4. Stock Uptrend Identification Using Moving Average Technical Indicators

5. Hybrid Stock Prediction Model Using Prediction Rule Ensembles and Deep Neural Network

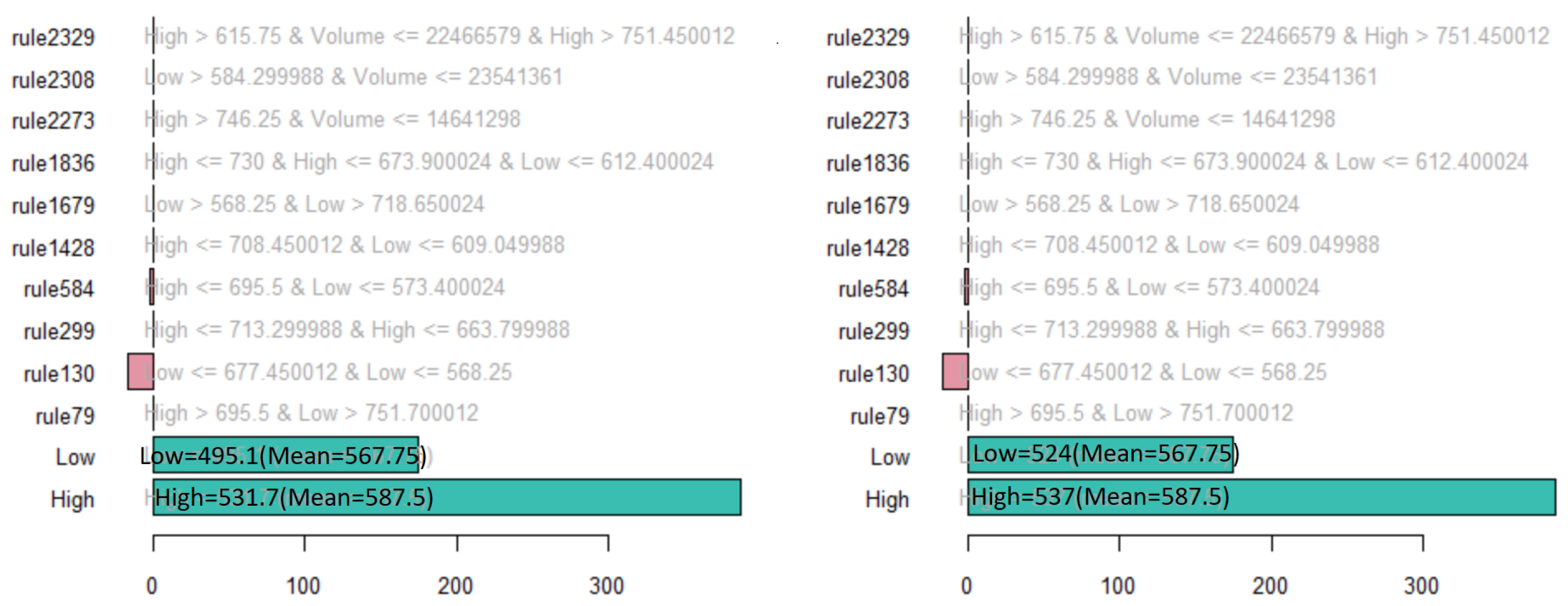

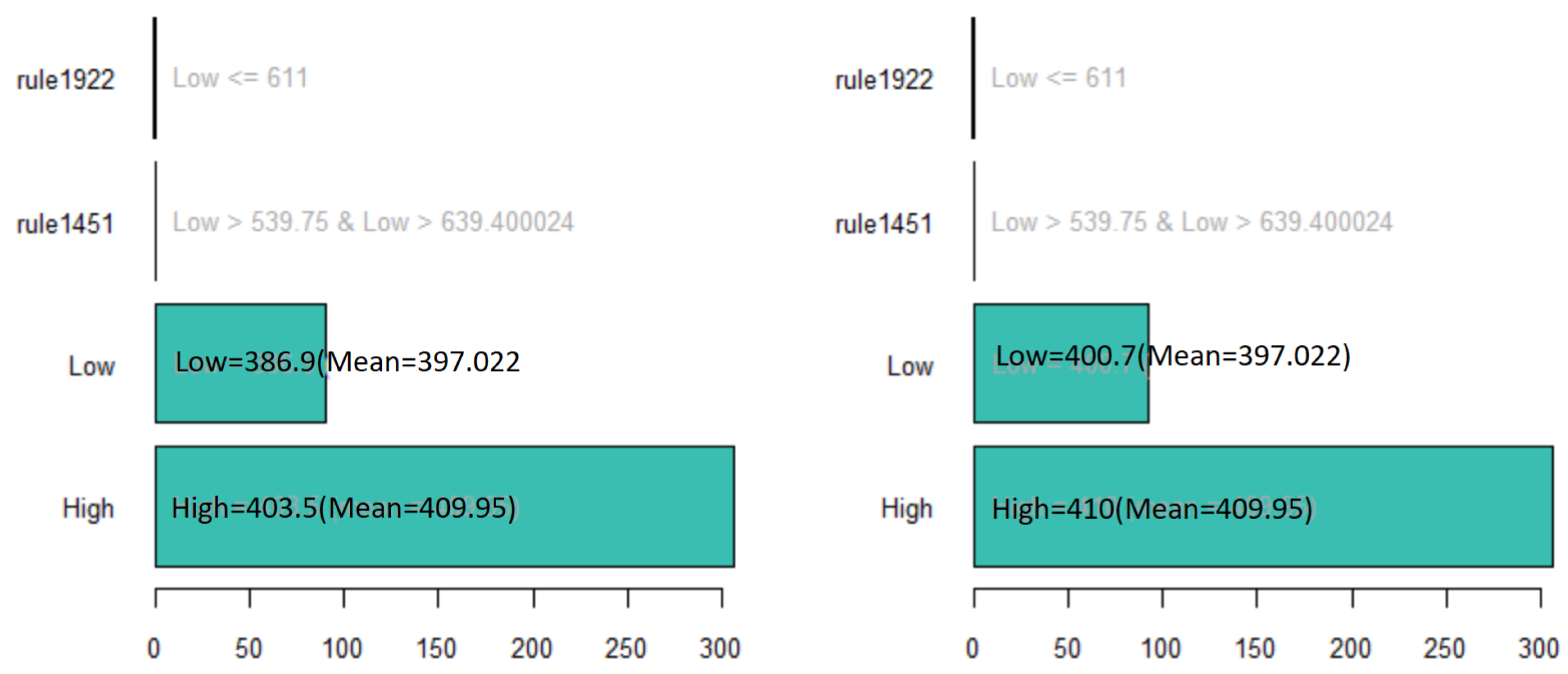

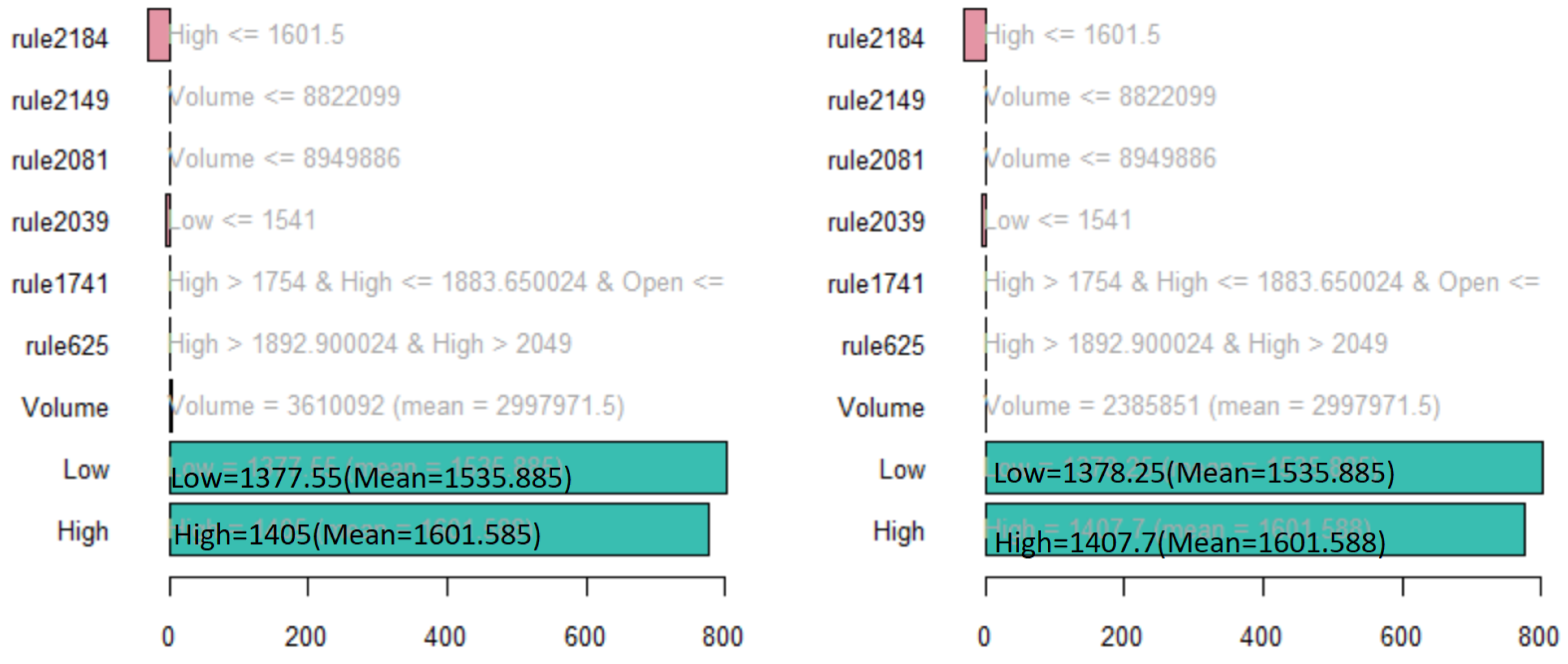

5.1. Prediction Rule Ensembles

5.2. DNN for Stock Price Prediction

| Algorithm 1 Hybrid stock prediction model using PRE and DNN. |

|

6. Results

7. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rai, K.; Garg, B. Dynamic correlations and volatility spillovers between stock price and exchange rate in BRIICS economies: Evidence from the COVID-19 outbreak period. Appl. Econ. Lett. 2021, 29, 1–8. [Google Scholar] [CrossRef]

- He, J.; Khushi, M.; Tran, N.H.; Liu, T. Robust Dual Recurrent Neural Networks for Financial Time Series Prediction. In Proceedings of the 2021 SIAM International Conference on Data Mining (SDM), virtually, 29 April–1 May 2021; pp. 747–755. [Google Scholar]

- Ribeiro, G.T.; Santos, A.A.P.; Mariani, V.C.; dos Santos Coelho, L. Novel hybrid model based on echo state neural network applied to the prediction of stock price return volatility. Expert Syst. Appl. 2021, 184, 115490. [Google Scholar] [CrossRef]

- Doong, S.C.; Doan, A.T. The influence of political uncertainty on commercial banks in emerging market countries. Int. J. Public Adm. 2021, 104, 1–17. [Google Scholar] [CrossRef]

- Avramov, D.; Kaplanski, G.; Subrahmanyam, A. Moving average distance as a predictor of equity returns. Rev. Financ. Econ. 2021, 39, 127–145. [Google Scholar] [CrossRef]

- Singh, J.; Khushi, M. Feature Learning for Stock Price Prediction Shows a Significant Role of Analyst Rating. Appl. Syst. Innov. 2021, 4, 17. [Google Scholar] [CrossRef]

- Thakkar, A.; Chaudhari, K. A comprehensive survey on deep neural networks for stock market: The need, challenges, and future directions. Expert Syst. Appl. 2021, 177, 114800. [Google Scholar] [CrossRef]

- Patel, J.; Shah, S.; Thakkar, P.; Kotecha, K. Predicting stock and stock price index movement using trend deterministic data preparation and machine learning techniques. Expert Syst. Appl. 2015, 42, 259–268. [Google Scholar] [CrossRef]

- Kong, A.; Zhu, H.; Azencott, R. Predicting intraday jumps in stock prices using liquidity measures and technical indicators. J. Forecast. 2021, 40, 416–438. [Google Scholar] [CrossRef]

- Ravichandra, T.; Thingom, C. Stock price forecasting using ANN method. In Information Systems Design and Intelligent Applications; Springer: New Delhi, India, 2016; pp. 599–605. [Google Scholar]

- Fenghua, W.; Jihong, X.; Zhifang, H.; Xu, G. Stock price prediction based on SSA and SVM. Procedia Comput. Sci. 2014, 31, 625–631. [Google Scholar] [CrossRef] [Green Version]

- Khaidem, L.; Saha, S.; Dey, S.R. Predicting the direction of stock market prices using random forest. arXiv 2016, arXiv:1605.00003. [Google Scholar]

- Niu, H.; Xu, K.; Wang, W. A hybrid stock price index forecasting model based on variational mode decomposition and LSTM network. Appl. Intell. 2020, 50, 4296–4309. [Google Scholar] [CrossRef]

- Jing, N.; Wu, Z.; Wang, H. A hybrid model integrating deep learning with investor sentiment analysis for stock price prediction. Expert Syst. Appl. 2021, 178, 115019. [Google Scholar] [CrossRef]

- Senapati, M.R.; Das, S.; Mishra, S. A novel model for stock price prediction using hybrid neural network. J. Inst. Eng. (India) Ser. B 2018, 99, 555–563. [Google Scholar] [CrossRef]

- Kim, H.Y.; Won, C.H. Forecasting the volatility of stock price index: A hybrid model integrating LSTM with multiple GARCH-type models. Expert Syst. Appl. 2018, 103, 25–37. [Google Scholar] [CrossRef]

- Yu, P.; Yan, X. Stock price prediction based on deep neural networks. Neural Comput. Appl. 2020, 32, 1609–1628. [Google Scholar] [CrossRef]

- Hu, Z.; Zhao, Y.; Khushi, M. A survey of forex and stock price prediction using deep learning. Appl. Syst. Innov. 2021, 4, 9. [Google Scholar] [CrossRef]

- Sedighi, M.; Jahangirnia, H.; Gharakhani, M.; Farahani Fard, S. A novel hybrid model for stock price forecasting based on metaheuristics and support vector machine. Data 2019, 4, 75. [Google Scholar] [CrossRef] [Green Version]

- Hu, Y.; Ni, J.; Wen, L. A hybrid deep learning approach by integrating LSTM-ANN networks with GARCH model for copper price volatility prediction. Phys. A Stat. Mech. Its Appl. 2020, 557, 124907. [Google Scholar] [CrossRef]

- Zhong, X.; Enke, D. Predicting the daily return direction of the stock market using hybrid machine learning algorithms. Financ. Innov. 2019, 5, 1–20. [Google Scholar] [CrossRef]

- Lu, W.; Li, J.; Wang, J.; Qin, L. A CNN-BiLSTM-AM method for stock price prediction. Neural Comput. Appl. 2021, 33, 4741–4753. [Google Scholar] [CrossRef]

- Vijh, M.; Chandola, D.; Tikkiwal, V.A.; Kumar, A. Stock closing price prediction using machine learning techniques. Procedia Comput. Sci. 2020, 167, 599–606. [Google Scholar] [CrossRef]

- Chandar, S.K. Grey Wolf optimization-Elman neural network model for stock price prediction. Soft Comput. 2021, 25, 649–658. [Google Scholar] [CrossRef]

- Xiao, C.; Xia, W.; Jiang, J. Stock price forecast based on combined model of ARI-MA-LS-SVM. Neural Comput. Appl. 2020, 32, 5379–5388. [Google Scholar] [CrossRef]

- Ananthi, M.; Vijayakumar, K. Stock market analysis using candlestick regression and market trend prediction (CKRM). J. Ambient Intell. Humaniz. Comput. 2021, 12, 4819–4826. [Google Scholar] [CrossRef]

- Zhang, J.; Li, L.; Chen, W. Predicting stock price using two-stage machine learning techniques. Comput. Econ. 2021, 57, 1237–1261. [Google Scholar] [CrossRef]

- Xu, Y.; Yang, C.; Peng, S.; Nojima, Y. A hybrid two-stage financial stock forecasting algorithm based on clustering and ensemble learning. Appl. Intell. 2020, 50, 3852–3867. [Google Scholar] [CrossRef]

- Li, Y.; Ni, P.; Chang, V. Application of deep reinforcement learning in stock trading strategies and stock forecasting. Computing 2020, 102, 1305–1322. [Google Scholar] [CrossRef]

- Yun, K.K.; Yoon, S.W.; Won, D. Prediction of stock price direction using a hybrid GA-XGBoost algorithm with a three-stage feature engineering process. Expert Syst. Appl. 2021, 186, 115716. [Google Scholar] [CrossRef]

- Jaggi, M.; Mandal, P.; Narang, S.; Naseem, U.; Khushi, M. Text mining of stocktwits data for predicting stock prices. Appl. Syst. Innov. 2021, 4, 13. [Google Scholar] [CrossRef]

- Zhang, Z.; Khushi, M. Ga-MSSR: Genetic algorithm maximizing sharpe and sterling ratio method for robotrading. In Proceedings of the 2020 International Joint Conference on Neural Networks (IJCNN), Glasgow, UK, 19–24 July 2020; pp. 1–8. [Google Scholar]

- Nayak, R.K.; Tripathy, R.; Mishra, D.; Burugari, V.K.; Selvaraj, P.; Sethy, A.; Jena, B. Indian Stock Market Prediction Based on Rough Set and Support Vector Machine Approach. In Intelligent and Cloud Computing; Springer: Singapore, 2021; pp. 345–355. [Google Scholar]

- Manickamahesh, N. A Study on Technical Indicators for Prediction of Select Indices Listed on NSE. Turk. J. Comput. Math. Educ. (TURCOMAT) 2021, 12, 5730–5736. [Google Scholar]

- Fifield, S.; Power, D.; Knipe, D. The performance of moving average rules in emerging stock markets. Appl. Financ. Econ. 2008, 18, 1515–1532. [Google Scholar] [CrossRef]

- Djemo, C.R.T.; Eita, J.H.; Mwamba, J.W.M. Predicting Foreign Exchange Rate Movements: An Application of the Ensemble Method. Rev. Dev. Financ. 2021, 11, 58–70. [Google Scholar]

- Dwivedi, V.K.; Gore, M.M. A historical data based ensemble system for efficient stock price prediction. Recent Adv. Comput. Sci. Commun. (Former. Recent Pat. Comput. Sci.) 2021, 14, 1182–1212. [Google Scholar] [CrossRef]

- Fokkema, M. Fitting prediction rule ensembles with R package pre. arXiv 2017, arXiv:1707.07149. [Google Scholar] [CrossRef] [Green Version]

- Friedman, J.H.; Popescu, B.E. Predictive learning via rule ensembles. Ann. Appl. Stat. 2008, 2, 916–954. [Google Scholar] [CrossRef]

- Fokkema, M.; Strobl, C. Fitting prediction rule ensembles to psychological research data: An introduction and tutorial. Psychol. Methods 2020, 25, 636. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors | Technique | Outcomes |

|---|---|---|

| Niu et al. [13] | Hybrid neural network VMD-LSTM | Stock price prediction |

| Jing et al. [14] | Hybrid model that combines deep learning and sentiment analysis | Stock price prediction |

| Senapati et al. [15] | Hybrid model for stock price prediction using ANN and PSO | Stock price prediction |

| Kim et al. [16] | Hybrid long short-term memory (LSTM) | Stock price forecasting |

| Sedighi et al. [19] | Hybrid stock prediction model by combining ABC, ANFIS, and SVM | Stock price forecasting |

| HyperParameters | Range |

|---|---|

| Number of layers | 2 to 3 |

| Number of neurons | 5 to 20 |

| Learning rate | 0.001 to 0.004 |

| Epochs | 300 to 600 |

| Stock | Prediction Technique | MAE | RMSE |

|---|---|---|---|

| Kotak Bank | Proposed Hybrid Model | 9.50 | 6.50 |

| ICICI Bank | Proposed Hybrid Model | 10.30 | 5.60 |

| Axis Bank | Proposed Hybrid Model | 9.90 | 7.10 |

| SBI Bank | Proposed Hybrid Model | 8.53 | 6.30 |

| Infosys | Proposed Hybrid Model | 9.30 | 7.20 |

| TCS | Proposed Hybrid Model | 8.55 | 6.75 |

| Kotak Bank | DNN Model | 13.50 | 11.50 |

| ICICI Bank | DNN Model | 14.50 | 13.60 |

| Axis Bank | DNN Model | 13.30 | 12.60 |

| SBI Bank | DNN Model | 13.50 | 11.20 |

| Infosys | DNN Model | 15.13 | 13.11 |

| TCS | DNN Model | 14.45 | 12.40 |

| ICICI Bank | ANN Model [10] | 15.1221 | 19.9444 |

| SBI BANK | ANN Model [10] | 17.4341 | 23.1585 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Srivinay; Manujakshi, B.C.; Kabadi, M.G.; Naik, N. A Hybrid Stock Price Prediction Model Based on PRE and Deep Neural Network. Data 2022, 7, 51. https://doi.org/10.3390/data7050051

Srivinay, Manujakshi BC, Kabadi MG, Naik N. A Hybrid Stock Price Prediction Model Based on PRE and Deep Neural Network. Data. 2022; 7(5):51. https://doi.org/10.3390/data7050051

Chicago/Turabian StyleSrivinay, B. C. Manujakshi, Mohan Govindsa Kabadi, and Nagaraj Naik. 2022. "A Hybrid Stock Price Prediction Model Based on PRE and Deep Neural Network" Data 7, no. 5: 51. https://doi.org/10.3390/data7050051

APA StyleSrivinay, Manujakshi, B. C., Kabadi, M. G., & Naik, N. (2022). A Hybrid Stock Price Prediction Model Based on PRE and Deep Neural Network. Data, 7(5), 51. https://doi.org/10.3390/data7050051