An Ensemble Model for Predicting Retail Banking Churn in the Youth Segment of Customers

Abstract

:1. Introduction

- To predict whether or not a young customer will discontinue his retail bank account;

- To analyse and discuss the features impacting churn using appropriate data science algorithms.

2. Literature Review

2.1. Need for Churn Prediction in the Industry

2.2. Churn Prediction Techniques

3. Method

3.1. Research Design

3.2. Setting

3.3. Sampling and Data Collection

3.4. Procedure

3.5. Instrument

3.6. Data Analysis

3.6.1. Demographic Profile

{kind=link}

| Frequency | % | ||

|---|---|---|---|

| Gender | Female | 214 | 36 |

| Male | 388 | 64 | |

| Opened any new savings Bank account in the past 1 year | Yes | 286 | 48 |

| No | 313 | 52 | |

| Closed an existing Savings Bank account in the past 1 year | Yes | 267 | 44 |

| No | 335 | 56 | |

| Type of city in which they are currently living | Metropolitan | 172 | 29 |

| Non-Metropolitan | 430 | 71 | |

| Industry | Information Technology and allied | 355 | 59 |

| Insurance | 126 | 21 | |

| Manufacturing | 66 | 11 | |

| Others (Retails, Logistics, Hospitality) | 55 | 9 | |

3.6.2. Machine Learning Models

- Data preparation: The collected data were pre-processed and checked for duplication, correctness, and missing data. Cleaning and transformation were done, and feature selection was carried out.

- Select Machine learning algorithms: 13 algorithms, including ensembles, were shortlisted for this study.

- Predictive modelling: In this step, we used a 70:30 ratio and cross-validation methods for building the models.

- Prediction and evaluation: The selected models were used to predict churn, and performances were compared. The performance matrix selected included accuracy, F1 score, sensitivity, specificity, AUC, and precision.

- Model selection: Based on the performance matrix above-mentioned, the model was finalized.

- nodej = importance of node j

- wj = weighted number of samples arriving at node j

- Ij = impurity of node j

- l(j) = child node on the left

- r(j) = child node on the right

- Feature importance of a node i

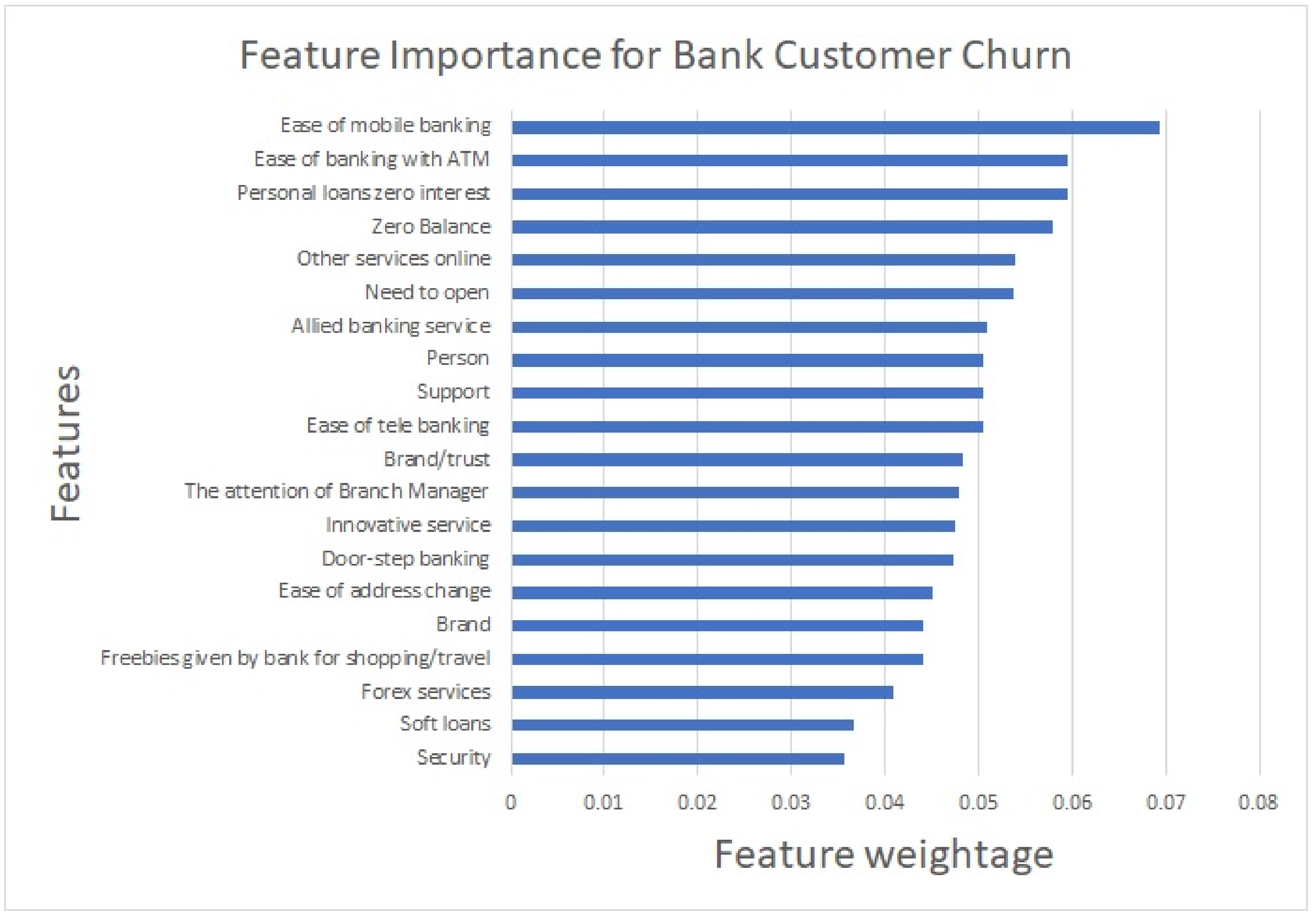

3.6.3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rughoo, A.; Sarantis, N. The global financial crisis and integration in European retail banking. J. Bank. Financ. 2014, 40, 28–41. [Google Scholar] [CrossRef] [Green Version]

- Ahmed, S.; Bangassa, K.; Akbar, S. A study on trust restoration efforts in the UK retail banking industry. Br. Account. Rev. 2019, 52, 100871. [Google Scholar] [CrossRef]

- Broby, D. Financial technology and the future of banking. Financ. Innov. 2021, 7, 47. [Google Scholar] [CrossRef]

- Amin, A.; Anwar, S.; Adnan, A.; Nawaz, M.; Alawfi, K.; Hussain, A.; Huang, K. Customer churn prediction in the telecommunication sector using a rough set approach. Neurocomputing 2017, 237, 242–254. [Google Scholar] [CrossRef]

- Colgate, M.; Stewart, K.; Kinsella, R. Customer defection: A study of the student market in Ireland. Int. J. Bank Mark. 1996, 14, 23–29. [Google Scholar] [CrossRef]

- Rust, R.T.; Zahorik, A.J. Customer satisfaction, customer retention, and market share. J. Retail. 1993, 69, 193–215. [Google Scholar] [CrossRef]

- Gupta, S.; Lehmann, D.R.; Stuart, J.A. Valuing Customers. J. Mark. Res. 2004, 41, 7–18. [Google Scholar] [CrossRef]

- Dahlman, C.; Mealy, S.; Wermelinger, M. Harnessing the Digital Economy for Developing Countries; OECD Development Centre Working Papers, No. 334; OECD Publishing: Paris, France, 2016. [Google Scholar]

- Abdulquadri, A.; Mogaji, E.; Kieu, T.A.; Nguyen, N.P. Digital transformation in financial services provision: A Nigerian perspective to the adoption of chatbot. JEC 2021, 15, 258–281. [Google Scholar] [CrossRef]

- Chayjan, M.R.; Bagheri, T.; Kianian, A.; Someh, N.G. Using data mining for prediction of retail banking customer’s churn behaviour. Int. J. Electron. Bank. 2020, 2, 303. [Google Scholar] [CrossRef]

- Libai, B.; Bart, Y.; Gensler, S.; Hofacker, C.F.; Kaplan, A.; Kötterheinrich, K.; Kroll, E.B. Brave New World? On AI and the Management of Customer Relationships. J. Interact. Mark. 2020, 51, 44–56. [Google Scholar] [CrossRef]

- Kumar, V. A theory of customer valuation: Concepts, metrics, strategy, and implementation. J. Mark. 2018, 82, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Yaseen, A. Next-wave of E-commerce: Mobile customers churn prediction using machine learning. Res. J. Comput. Sci. Inf. Technol. 2021, 5, 62–72. [Google Scholar] [CrossRef]

- Chauhan, S.; Akhtar, A.; Gupta, A. Customer experience in digital banking: A review and future research directions. IJQSS 2022, 14, 311–348. [Google Scholar] [CrossRef]

- Al Zadjali, M.; Al Busaidi, K.A. The values of BI-empowered customer service in telecom. IJECRM 2018, 11, 363. [Google Scholar] [CrossRef]

- Hassani, H.; Huang, X.; Silva, E.; Ghodsi, M. Deep Learning and Implementations in Banking. Ann. Data Sci. 2020, 7, 433–446. [Google Scholar] [CrossRef]

- Chen, P.-Y.; Hsieh, C.-J.; Li, B.; Liu, S. Third Workshop on Adversarial Learning Methods for Machine Learning and Data Mining (AdvML 2021). In Proceedings of the 27th ACM SIGKDD Conference on Knowledge Discovery & Data Mining, Virtual Event, Singapore, 14–18 August 2021; ACM: New York, NY, USA, 2021; pp. 4112–4113. [Google Scholar] [CrossRef]

- Ahn, J.; Hwang, J.; Kim, D.; Choi, H.; Kang, S. A Survey on Churn Analysis in Various Business Domains. IEEE Access 2020, 8, 220816–220839. [Google Scholar] [CrossRef]

- Borah, S.B.; Prakhya, S.; Sharma, A. Leveraging service recovery strategies to reduce customer churn in an emerging market. J. Acad. Mark. Sci. 2020, 48, 848–868. [Google Scholar] [CrossRef]

- Senanu, B.; Narteh, B. Banking sector reforms and customer switching intentions: Evidence from the Ghanaian banking industry. J. Financ. Serv. Mark. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Ajmal, M.M.; Khan, M.; Shad, M.K.; AlKatheeri, H.; Jabeen, F. Socio-economic and technological new normal in supply chain management: Lessons from COVID-19 pandemic. IJLM 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Caimi, G.; Anderson, J.; Hoppe, F. COVID-19: Building a Digital Bridge to the New Normal. 2020. Available online: https://bit.ly/39ImmDR (accessed on 2 April 2022).

- Diebner, R.; Silliman, E.; Ungerman, K.; Vancauwenberghe, M. Adapting Customer Experience in the Time of Coronavirus. 2020. Available online: https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/adapting-customer-experience-in-the-time-of-coronavirus (accessed on 22 April 2022).

- Bhalla, R.; Osta, E. Digital transformation and the COVID-19 challenge. J. Digit. Bank. 2021, 5, 291–304. [Google Scholar]

- Hussain, M.; Papastathopoulos, A. Organizational readiness for digital financial innovation and financial resilience. Int. J. Prod. Econ. 2021, 243, 108326. [Google Scholar] [CrossRef]

- Liyanaarachchi, G.; Deshpande, S.; Weaven, S. Online banking and privacy: Redesigning sales strategy through social exchange. IJBM 2021, 39, 955–983. [Google Scholar] [CrossRef]

- Velez-Calle, A.; Mariam, M.; Gonzalez-Perez, M.A.; Jimenez, A.; Eisenberg, J.; Santamaria-Alvarez, S.M. When technological savviness overcomes cultural differences: Millennials in global virtual teams. CPOIB 2020, 16, 279–303. [Google Scholar] [CrossRef]

- Gabbi, G.; Giammarino, M.; Matthias, M.; Monferrà, S.; Sampagnaro, G. Does face-to-face contact matter? Evidence on loan pricing. Eur. J. Financ. 2019, 26, 820–836. [Google Scholar] [CrossRef]

- Borg, K.; Smith, L. Digital inclusion and online behaviour: Five typologies of Australian internet users. Behav. Inf. Technol. 2018, 37, 367–380. [Google Scholar] [CrossRef]

- Valluri, C.; Raju, S.; Patil, V.H. Customer determinants of used auto loan churn: Comparing predictive performance using machine learning techniques. J. Mark. Anal. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Chen, X.; You, X.; Chang, V. FinTech and commercial banks’ performance in China: A leap forward or survival of the fittest? Technol. Forecast. Soc. Chang. 2021, 166, 120645. [Google Scholar] [CrossRef]

- Amankwah-Amoah, J.; Khan, Z.; Wood, G.; Knight, G. COVID-19 and digitalization: The great acceleration. J. Bus. Res. 2021, 136, 602–611. [Google Scholar] [CrossRef]

- Huang, B.; Kechadi, M.T.; Buckley, B. Customer churn prediction in telecommunications. Expert Syst. Appl. 2012, 39, 1414–1425. [Google Scholar] [CrossRef]

- Wei, C.-P.; Chiu, I.-T. Turning telecommunications call details to churn prediction: A data mining approach. Expert Syst. Appl. 2002, 23, 103–112. [Google Scholar] [CrossRef]

- Xie, Y.; Li, X.; Ngai, E.W.; Ying, W. Customer churn prediction using improved balanced random forests. Expert Syst. Appl. 2009, 36, 5445–5449. [Google Scholar] [CrossRef]

- Hadden, J.; Tiwari, A.; Roy, R.; Ruta, D. Churn prediction: Does technology matter. Int. J. Intell. Technol. 2006, 1, 104–110. [Google Scholar]

- Mutanen, T.; Nousiainen, S.; Ahola, J. Customer churn prediction—A case study in retail banking. In Data Mining for Business Applications; IOS Press: Amsterdam, The Netherlands, 2010; pp. 77–83. [Google Scholar]

- Veningston, K.; Rao, P.V.; Selvan, C.; Ronalda, M. Investigation on Customer Churn Prediction Using Machine Learning Techniques. In Proceedings of International Conference on Data Science and Applications; Springer: Singapore, 2022; pp. 109–119. [Google Scholar] [CrossRef]

- Van den Poel, D.; Larivière, B. Customer attrition analysis for financial services using proportional hazard models. Eur. J. Oper. Res. 2004, 157, 196–217. [Google Scholar] [CrossRef]

- Ahn, Y.; Kim, D.; Lee, D.-J. Customer attrition analysis in the securities industry: A large-scale field study in Korea. IJBM 2019, 38, 561–577. [Google Scholar] [CrossRef]

- Khan, Y.; Shafiq, S.; Naeem, A.; Ahmed, S.; Safwan, N.; Hussain, S. Customers Churn Prediction using Artificial Neural Networks (ANN) in Telecom Industry. IJACSA 2019, 10, 132–142. [Google Scholar] [CrossRef]

- Anjum, A.; Usman, S.; Zeb, A.; Uddin, I.; Masoom, P.; Anwar, Z.; Anjum, A.; Raza, B.; Kamran, A.; Ur, S. Optimizing Coverage of Churn Prediction in Telecommunication Industry. IJACSA 2017, 8, 179–188. [Google Scholar] [CrossRef] [Green Version]

- Vo, N.N.Y.; Liu, S.; Li, X.; Xu, G. Leveraging unstructured call log data for customer churn prediction. Knowl. Based Syst. 2020, 212, 106586. [Google Scholar] [CrossRef]

- Charandabi, S.; Ghanadiof, O. Evaluation of Online Markets Considering Trust and Resilience: A Framework for Predicting Customer Behavior in E-Commerce. J. Bus. Manag. Stud. 2022, 4, 23–33. [Google Scholar] [CrossRef]

- Abou el Kassem, E.; Ali, S.; Mostafa, A.; Kamal, F. Customer Churn Prediction Model and Identifying Features to Increase Customer Retention based on User Generated Content. IJACSA 2020, 11, 522–531. [Google Scholar] [CrossRef]

- CustomerGauge. The 2018 NPS® & CX Benchmarks Report. Available online: https://customergauge.com/benchmarks-report (accessed on 2 February 2022).

- Shaaban, E.; Helmy, Y.; Khedr, A.; Nasr, M. A proposed churn prediction model. Int. J. Eng. Res. Appl. 2012, 2, 693–697. [Google Scholar]

- Ahmad, A.K.; Jafar, A.; Aljoumaa, K. Customer churn prediction in telecom using machine learning in big data platform. J. Big Data 2019, 6, 28. [Google Scholar] [CrossRef] [Green Version]

- Ullah, I.; Raza, B.; Malik, A.K.; Imran, M.; Islam, S.U.; Kim, S.W. A Churn Prediction Model Using Random Forest: Analysis of Machine Learning Techniques for Churn Prediction and Factor Identification in Telecom Sector. IEEE Access 2019, 7, 60134–60149. [Google Scholar] [CrossRef]

- Alboukaey, N.; Joukhadar, A.; Ghneim, N. Dynamic behavior based churn prediction in mobile telecom. Expert Syst. Appl. 2020, 162, 113779. [Google Scholar] [CrossRef]

- Idris, A.; Iftikhar, A.; Rehman, Z.U. Intelligent churn prediction for telecom using GP-AdaBoost learning and PSO undersampling. Clust. Comput. 2017, 22, 7241–7255. [Google Scholar] [CrossRef]

- Xu, T.; Ma, Y.; Kim, K. Telecom Churn Prediction System Based on Ensemble Learning Using Feature Grouping. Appl. Sci. 2021, 11, 4742. [Google Scholar] [CrossRef]

- Jaisakthi, S.M.; Gayathri, N.; Uma, K.; Vijayarajan, V. Customer Churn Prediction Using Stochastic Gradient Boosting Technique. J. Comput. Theor. Nanosci. 2018, 15, 2410–2414. [Google Scholar] [CrossRef]

- Mohammadzadeh, M.; Hoseini, Z.Z.; Derafshi, H. A data mining approach for modeling churn behavior via RFM model in specialized clinics Case study: A public sector hospital in Tehran. Procedia Comput. Sci. 2017, 120, 23–30. [Google Scholar] [CrossRef]

- Karvana, K.G.M.; Yazid, S.; Syalim, A.; Mursanto, P. Customer churn analysis and prediction using data mining models in banking industry. In Proceedings of the 2019 International Workshop on Big Data and Information Security (IWBIS), Bali, Indonesia, 11 October 2019; pp. 33–38. [Google Scholar] [CrossRef]

- Dingli, A.; Marmara, V.; Fournier, N.S. Comparison of Deep Learning Algorithms to Predict Customer Churn within a Local Retail Industry. IJMLC 2017, 7, 128–132. [Google Scholar] [CrossRef]

- He, Y.; Xiong, Y.; Tsai, Y. Machine Learning Based Approaches to Predict Customer Churn for an Insurance Company. In Proceedings of the 2020 Systems and Information Engineering Design Symposium (SIEDS), Charlottesville, VA, USA, 24 April 2020; pp. 1–6. [Google Scholar] [CrossRef]

- Mauritsius, T.; Kristianto; Sayoga, R.Y.; Alamas, N.; Anggraeni, M.; Binsar, F. Customer Churn Prediction Models for PT. XYZ Insurance. In Proceedings of the 2020 8th International Conference on Orange Technology (ICOT), Daegu, Korea, 18–21 December 2020; pp. 1–6. [Google Scholar] [CrossRef]

- Jain, H.; Yadav, G.; Manoov, R. Churn prediction and retention in banking, telecom and IT sectors using machine learning techniques. In Advances in Machine Learning and Computational Intelligence; Springer: Singapore, 2021; pp. 137–156. [Google Scholar] [CrossRef]

- Matuszelański, K.; Kopczewska, K. Customer Churn in Retail E-Commerce Business: Spatial and Machine Learning Approach. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 165–198. [Google Scholar] [CrossRef]

- Xiahou, X.; Harada, Y. B2C E-Commerce Customer Churn Prediction Based on K-Means and SVM. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 458–475. [Google Scholar] [CrossRef]

- Wright, K.B. Researching Internet-Based Populations: Advantages and Disadvantages of Online Survey Research, Online Questionnaire Authoring Software Packages, and Web Survey Services. J. Comput. Mediat. Commun. 2005, 10, JCMC1034. [Google Scholar] [CrossRef]

- Regmi, P.R.; Waithaka, E.; Paudyal, A.; Simkhada, P.; Van Teijlingen, E. Guide to the design and application of online questionnaire surveys. Nepal J. Epidemiol. 2017, 6, 640–644. [Google Scholar] [CrossRef]

- Ministry of External Affairs, GoI. One of The Youngest Populations in the World—India’s Most Valuable Asset. 2021. Available online: https://bit.ly/3L1qH2I (accessed on 22 April 2022).

- Statista. Smartphone Penetration Rate in India 2010–2040. 2021. Available online: https://bit.ly/3uY31GJ (accessed on 22 April 2022).

- Gui, M.; Argentin, G. Digital skills of internet natives: Different forms of digital literacy in a random sample of northern Italian high school students. New Media Soc. 2011, 13, 963–980. [Google Scholar] [CrossRef] [Green Version]

- Khazaal, Y.; Van Singer, M.; Chatton, A.; Achab, S.; Zullino, D.F.; Rothen, S.; Khan, R.A.; Billieux, J.; Thorens, G. Does Self-Selection Affect Samples’ Representativeness in Online Surveys? An Investigation in Online Video Game Research. J. Med. Internet Res. 2014, 16, e164. [Google Scholar] [CrossRef]

- Dewaele, J.M. Online questionnaires. In The Palgrave Handbook of Applied Linguistics Research Methodology; Palgrave Macmillan: London, UK, 2018; pp. 269–286. [Google Scholar]

- Porter, S.R.; Whitcomb, M.E. Non-response in student surveys: The Role of Demographics, Engagement and Personality. Res. High. Educ. 2005, 46, 127–152. [Google Scholar] [CrossRef]

- Chu, X.; Ilyas, I.F.; Krishnan, S.; Wang, J. Data Cleaning: Overview and Emerging Challenges. In Proceedings of the 2016 International Conference on Management of Data, San Francisco, CA, USA, 26 June–1 July 2016; ACM: New York, NY, USA, 2016; pp. 2201–2206. [Google Scholar] [CrossRef]

- Kumar, A.; Boehm, M.; Yang, J. Data Management in Machine Learning: Challenges, Techniques, and Systems. In Proceedings of the 2017 ACM International Conference on Management of Data, Chicago, IL, USA, 14–19 May 2017; ACM: New York, NY, USA, 2017; pp. 1717–1722. [Google Scholar] [CrossRef]

- Ilyas, I.F.; Rekatsinas, T. Machine Learning and Data Cleaning: Which Serves the Other? J. Data Inf. Qual. 2020; ahead-of-print. [Google Scholar] [CrossRef]

- Omar, A.; Sultan, N.; Zaman, K.; Bibi, N.; Wajid, A.; Khan, K. Customer Perception towards Online Banking Services: Empirical Evidence from Pakistan. J. Int. Bank. Commer. 2011, 16, 24. [Google Scholar]

- Jun, M.; Palacios, S. Examining the key dimensions of mobile banking service quality: An exploratory study. Int. J. Bank Mark. 2016, 34, 307–326. [Google Scholar] [CrossRef]

- Hossain, M.M.; Irin, D.; Islam, M.S.; Saha, S. Electronic-Banking Services: A Study on Selected Commercial Banks in Bangladesh. Asian Bus. Rev. 2015, 3, 53. [Google Scholar] [CrossRef] [Green Version]

- Chawla, D.; Joshi, H. Consumer attitude and intention to adopt mobile wallet in India—An empirical study. Int. J. Bank Mark. 2019, 37, 1590–1618. [Google Scholar] [CrossRef]

- Wijaya, A.F.B.; Surachman, S.; Mugiono, M. The Effect of Service Quality, Perceived Value and Mediating Effect of Brand Image on Brand Trust. J. Manaj. Kewirausahaan 2020, 22, 45–56. [Google Scholar] [CrossRef]

- Khan, I.; Hollebeek, L.D.; Fatma, M.; Islam, J.U.; Rahman, Z. Brand engagement and experience in online services. J. Serv. Mark. 2019, 34, 163–175. [Google Scholar] [CrossRef]

- Sahut, J.M. Advantages of E-Banking. J. Int. Bank. Commer. 2021, 26, 1. [Google Scholar]

- Hassan, M.K.; Rabbani, M.R.; Ali, M.A.M. Challenges for the Islamic Finance and Banking in Post COVID Era and the Role of Fintech. J. Econ. Coop. Dev. 2020, 41, 93–116. [Google Scholar]

- Kumari, P.B.; Madhumitha, L. Customer Preference in Availing New Generation Banking Facilities of ICICI (with Special Reference to Employees). Eurasian J. Anal. Chem. 2018, 13, 121–124. [Google Scholar]

- Raman, R.; Bhattacharya, S.; Pramod, D. Predict employee attrition by using predictive analytics. BIJ 2018, 26, 2–18. [Google Scholar] [CrossRef]

- Raman, R.; Pramod, D. The role of predictive analytics to explain the employability of management graduates. BIJ, 2021; ahead-of-print. [Google Scholar] [CrossRef]

- McDonald, G.C. Ridge regression. WIREs Comput. Stat. 2009, 1, 93–100. [Google Scholar] [CrossRef]

- Peng, C.-Y.J.; Lee, K.L.; Ingersoll, G.M. An Introduction to Logistic Regression Analysis and Reporting. J. Educ. Res. 2002, 96, 3–14. [Google Scholar] [CrossRef]

- Bansal, A.; Singhrova, A. Performance Analysis of Supervised Machine Learning Algorithms for Diabetes and Breast Cancer Dataset. In Proceedings of the 2021 International Conference on Artificial Intelligence and Smart Systems (ICAIS), Coimbatore, India, 25–27 March 2021; pp. 137–143. [Google Scholar] [CrossRef]

- Dong, X.; Yu, Z.; Cao, W.; Shi, Y.; Ma, Q. A survey on ensemble learning. Front. Comput. Sci. 2019, 14, 241–258. [Google Scholar] [CrossRef]

- Shtar, G.; Rokach, L.; Shapira, B.; Nissan, R.; Hershkovitz, A. Using Machine Learning to Predict Rehabilitation Outcomes in Postacute Hip Fracture Patients. Arch. Phys. Med. Rehabil. 2020, 102, 386–394. [Google Scholar] [CrossRef]

- Ampomah, E.K.; Qin, Z.; Nyame, G. Evaluation of Tree-Based Ensemble Machine Learning Models in Predicting Stock Price Direction of Movement. Information 2020, 11, 332. [Google Scholar] [CrossRef]

- Geurts, P.; Ernst, D.; Wehenkel, L. Extremely randomized trees. Mach. Learn. 2006, 63, 3–42. [Google Scholar] [CrossRef] [Green Version]

- John, V.; Liu, Z.; Guo, C.; Mita, S.; Kidono, K. Real-Time Lane Estimation Using Deep Features and Extra Trees Regression. In Image and Video Technology; Springer International Publishing: Cham, Switzerland, 2016; pp. 721–733. [Google Scholar]

- Grabmeier, J.L.; Lambe, L.A. Decision trees for binary classification variables grow equally with the Gini impurity measure and Pearson’s chi-square test. Int. J. Bus. Intell. Data Min. 2007, 2, 213. [Google Scholar] [CrossRef]

- Silveira, L.J.; Pinheiro, P.R.; Junior, L.S.D.M. A Novel Model Structured on Predictive Churn Methods in a Banking Organization. J. Risk Financ. Manag. 2021, 14, 481. [Google Scholar] [CrossRef]

| Industry | Data Science Technique(s) | Notable Contributors |

|---|---|---|

| Telecommunication | Artificial Neural Network | [41] |

| Deep Learning, Logistic Regression, and Naïve Bayes algorithms | [45] | |

| Logistic Regressions, Linear Classifications, Naive Bayes, Decision Trees, Multilayer Perceptron Neural Networks, Support Vector Machines, and the Evolutionary Data Mining Algorithm | [33] | |

| Linear regression, neural networks, decision trees, k- nearest neighbours, genetic algorithms, Naïve Bayes, Support Vector Machines (SVM), and Multilayer Perceptron Neural Networks | [47] | |

| Decision Tree, Random Forest, Gradient Boosted Machine Tree “GBM”, and Extreme Gradient Boosting “XGBOOST” | [48] | |

| Random Forest | [49] | |

| Long Short-term Memory (LSTM) and Convolutional Neural Networks (CNN) Models | [50] | |

| Genetic Programming-based AdaBoost (GP-based AdaBoost) | [51] | |

| Ensemble Learning with feature-grouping | [52] | |

| Healthcare | Stochastic Gradient Boosting Technique | [53] |

| Decision Trees, Naïve Bayes, and Neural Networks | [54] | |

| Banking | Artificial neural networks, decision trees, and class- weighted core support vector machines (CWC- SVM) and improved balanced random forests | [35] |

| Naïve Bayes model | [38] | |

| Artificial Neural Networks (ANN) and Random Forests | [44] | |

| Support Vector Machines | [55] | |

| Retail | Convolution Neural Networks and Restricted Boltzmann Machine | [56] |

| Insurance | Randomized Trees Classifier and Gradient Boosting Model | [57] |

| Decision Tree (DT), Naïve Bayes (NB), and ANN. | [58] | |

| IT Services | Logistic regression, random forest, SVM, and Extreme Gradient Boosting (XGBoost), on three different domains. | [59] |

| e-Commerce | Logistic regression, Extreme Gradient Boosting K-means, and SVM | [60] [61] |

| Feature | Instrument (Questions with Binary-Type Scale) | Source |

|---|---|---|

| Ease of banking with an ATM | I am not satisfied with the automated teller machine (ATM) location and access | [73,74] |

| The attention of the Branch Manager | I am not satisfied with the attention given by the Branch Manager | [74] |

| Allied banking service | The bank does not have allied banking services | [73,75] |

| Ease of address change | I cannot easily change my address via mobile or internet banking | [74] |

| Other services online | The bank does not have many essential online services | [76] |

| Ease of telebanking | I cannot do transactions via telebanking | [76,77] |

| Ease of mobile banking | I cannot do transactions very easily via mobile banking | [76,77] |

| Freebies are given by bank for shopping/travel | The bank does not provide any shopping/travel freebies | [76,77] |

| Security | The bank does not have adequate security features | [78] |

| Brand | The brand image of bank is not appealing | [77,78] |

| Zero Balance | Bank does not offer a zero-balance savings account | [79] |

| Personal loans zero interest | The bank charges interest on personal loans | [80] |

| Soft loans | The bank does not have a soft loan facility | [80] |

| Need to open | It was of NO NEED for me anymore | [79] |

| Brand/trust | The bank failed to build trust as its brand image is not good | [78] |

| Innovative service | The services provided by the bank are legacy | [74] |

| Door-step banking | The bank does not provide a door-step banking facility | [81] |

| Support | I am not satisfied with the support provided by bank | [81] |

| Person | The employees are not approachable and are unfriendly and not willing to help | [73] |

| Forex services | The Bank does not offer Forex Cards for a variety of currencies | [76] |

| Algorithm | Accuracy | Sensitivity | Specificity | Precision | AUC | F1 Score |

|---|---|---|---|---|---|---|

| ExtraTreesClassifier | 92.0 | 0.9286 | 0.9091 | 0.9286 | 0.9188 | 0.9286 |

| BaggingClassifier | 88.0 | 0.8571 | 0.9091 | 0.9231 | 0.8831 | 0.8889 |

| RandomForestClassifier | 88.0 | 1.0000 | 0.7272 | 0.8235 | 0.8636 | 0.9032 |

| GradientBoostingClassifier | 84.0 | 1.0000 | 0.6364 | 0.7778 | 0.8182 | 0.8750 |

| DecisionTreeClassifier | 80.0 | 0.7857 | 0.8182 | 0.8462 | 0.8019 | 0.8148 |

| SVC | 80.0 | 1.0000 | 0.5455 | 0.7368 | 0.7727 | 0.8485 |

| KNeighboursClassifier | 72.0 | 0.6429 | 0.8182 | 0.8182 | 0.7305 | 0.7200 |

| AdaBoostClassifier | 72.0 | 0.7857 | 0.6364 | 0.7333 | 0.7110 | 0.7586 |

| LogisticRegression | 72.0 | 0.7857 | 0.6364 | 0.7333 | 0.7110 | 0.7586 |

| LinearSVC | 72.0 | 0.7857 | 0.6364 | 0.7333 | 0.7110 | 0.7586 |

| RidgeClassifierCV | 72.0 | 0.7857 | 0.6364 | 0.7333 | 0.7110 | 0.7586 |

| BernoulliNB | 60.0 | 0.5000 | 0.7273 | 0.7000 | 0.6136 | 0.5833 |

| GaussianNB | 60.0 | 0.5000 | 0.7273 | 0.7000 | 0.6136 | 0.5833 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bharathi S, V.; Pramod, D.; Raman, R. An Ensemble Model for Predicting Retail Banking Churn in the Youth Segment of Customers. Data 2022, 7, 61. https://doi.org/10.3390/data7050061

Bharathi S V, Pramod D, Raman R. An Ensemble Model for Predicting Retail Banking Churn in the Youth Segment of Customers. Data. 2022; 7(5):61. https://doi.org/10.3390/data7050061

Chicago/Turabian StyleBharathi S, Vijayakumar, Dhanya Pramod, and Ramakrishnan Raman. 2022. "An Ensemble Model for Predicting Retail Banking Churn in the Youth Segment of Customers" Data 7, no. 5: 61. https://doi.org/10.3390/data7050061

APA StyleBharathi S, V., Pramod, D., & Raman, R. (2022). An Ensemble Model for Predicting Retail Banking Churn in the Youth Segment of Customers. Data, 7(5), 61. https://doi.org/10.3390/data7050061