Multitiered Fresh Produce Supply Chain: The Case of Tomatoes

and

and

Abstract

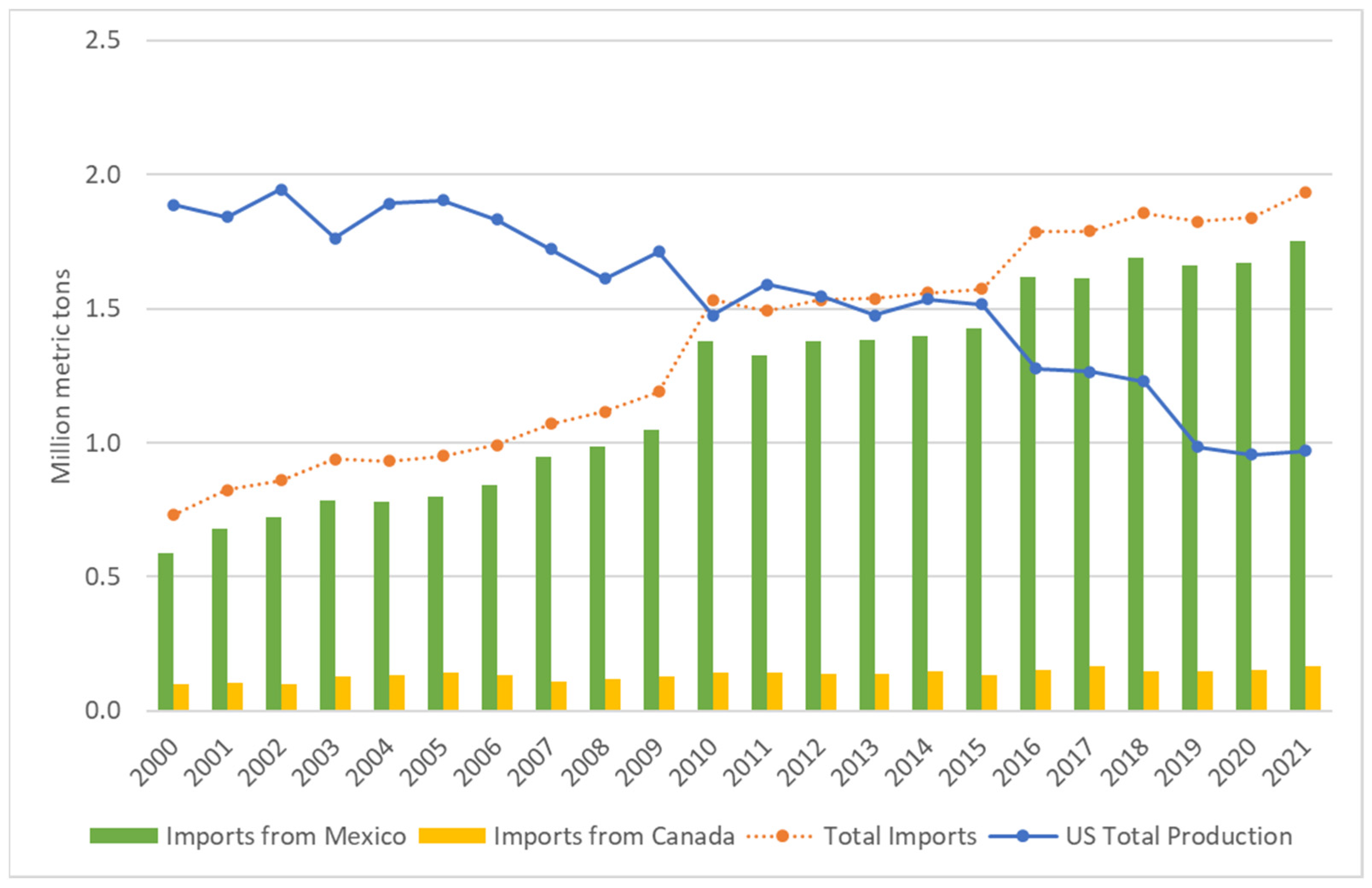

:1. Introduction

2. Methods

2.1. Supply Chain Modeling Theoretical Foundations

2.2. Supply Chain Research Questions

3. Supply Chain Structure of Fresh Market Tomatoes

3.1. Supply Chain Mapping

3.1.1. Growers

Production Systems

Varieties

Grading and Sizing

Seasonality

3.1.2. Grower-Shippers

3.1.3. Repackers

3.1.4. Distributors

3.1.5. Retailers and Foodservices

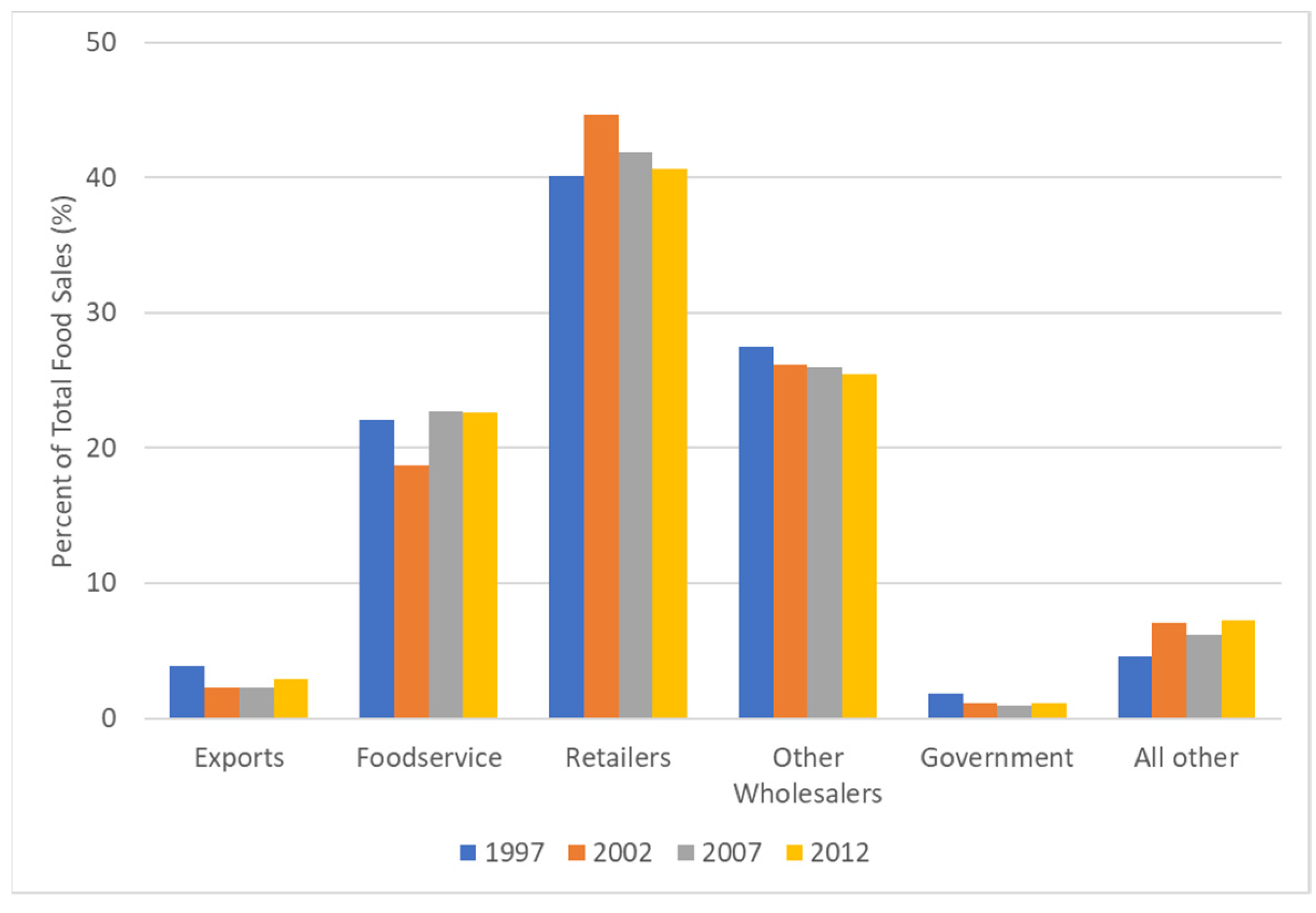

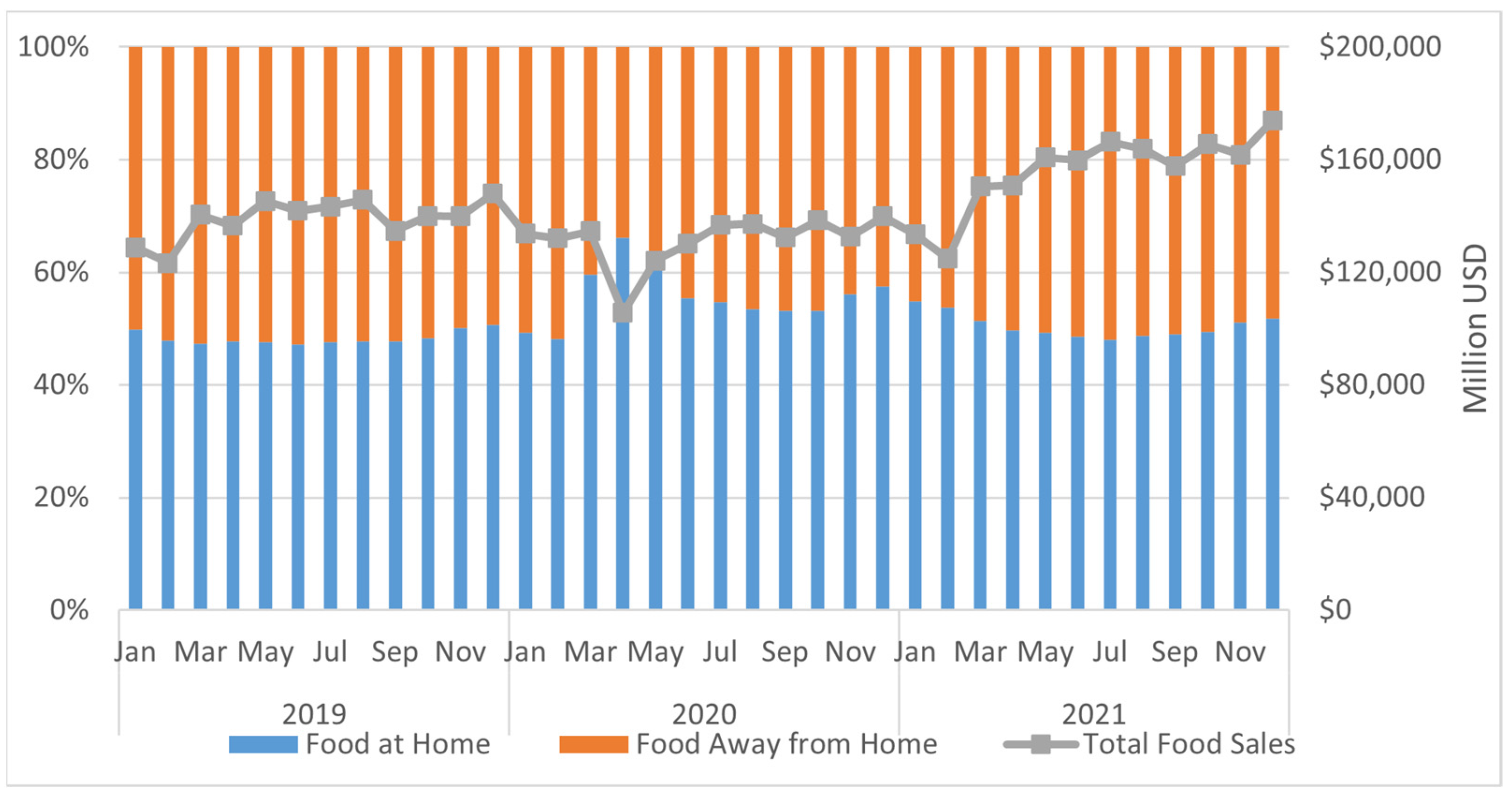

3.2. Price Trends along the Supply Chain

3.2.1. Shipping Point Price Trend

3.2.2. Terminal Market Price Trend

3.2.3. Retail Price Trend

4. Discussion

4.1. Seasonality

4.2. Perishability and Shelf Life

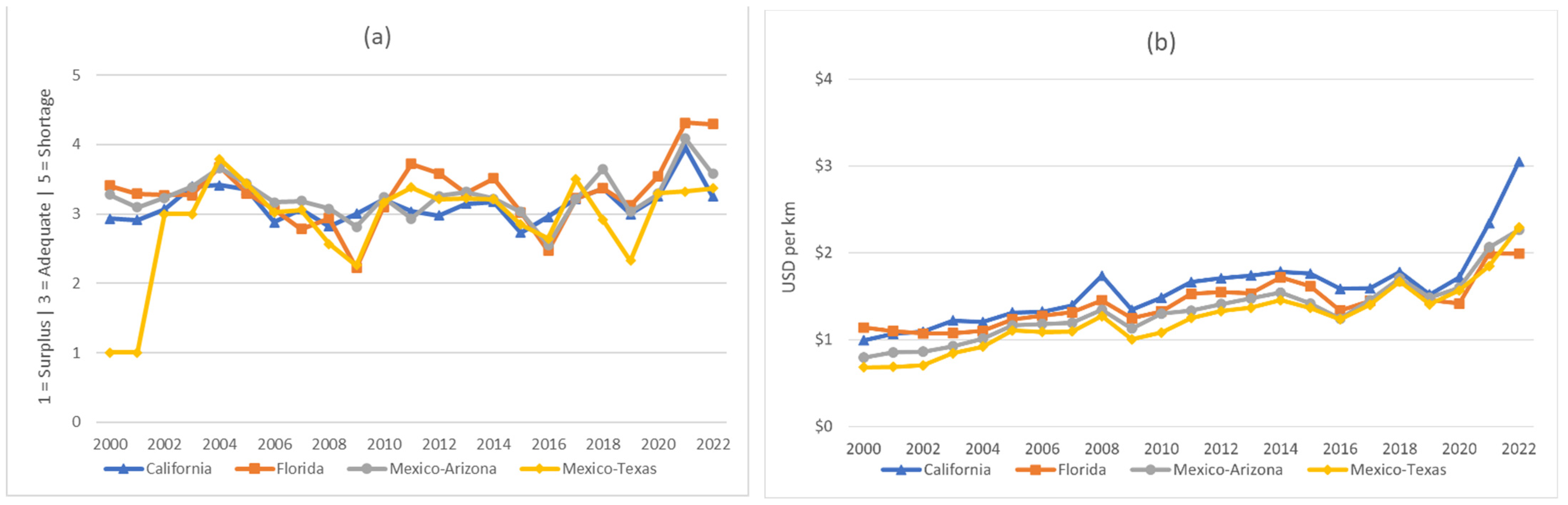

4.3. Transportation

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Anastasiadis, F.; Apostolidou, I.; Michailidis, A. Mapping Sustainable Tomato Supply Chain in Greece: A Framework for Research. Foods 2020, 9, 539. [Google Scholar] [CrossRef] [PubMed]

- United States Department of Agriculture, Economic Research Service (USDA-ERS). Vegetables and Pulses Data. Available online: https://www.ers.usda.gov/data-products/vegetables-and-pulses-data/ (accessed on 26 July 2022).

- Guan, Z.; Biswas, T.; Wu, F. The US Tomato Industry: An Overview of Production and Trade. Available online: https://edis.ifas.ufl.edu/publication/FE1027. (accessed on 10 January 2022).

- Wu, F.; Qushim, B.; Calle, M.; Guan, Z. Government Support in Mexican Agriculture. Choices 2018, 33, 1–11. [Google Scholar] [CrossRef]

- Calvin, L.; Cook, R.; Denbaly, M.; Dimitri, C.; Glaser, L.; Handy, C.; Jekanowski, M.; Kauf-man, P.; Krissoff, B.; Thompson, G.U.S. Fresh Fruit and Vegetable Marketing: Emerging Trade Practices, Trends, and Issues. Agric. Econ. Rep. 2001, AER-795, 60. [Google Scholar]

- Huang, K.-M.; Guan, Z.; Hammami, A. The U.S. Fresh Fruit and Vegetable Industry: An Overview of Production and Trade. Agriculture 2022, 12, 1719. [Google Scholar] [CrossRef]

- Food and Agriculture Organization of the United Nations (FAO). FAOSTAT. Available online: https://www.fao.org/faostat/en/#home (accessed on 27 November 2022).

- United States Department of Agriculture, Foreign Agricultural Service (USDA FAS). Mexico: Tomato Annual. Available online: https://www.fas.usda.gov/data/mexico-tomato-annual-4 (accessed on 26 July 2022).

- Canadian Tomatoes, from Farm to Fork. Available online: https://www150.statcan.gc.ca/n1/pub/11-627-m/11-627-m2021038-eng.htm (accessed on 16 March 2022).

- Roka, F.M.; Guan, Z. Farm Labor Management Trends in Florida, USA—Challenges and Opportunities. Int. J. Agric. Manag. 2018, 7, 79–87. [Google Scholar] [CrossRef]

- Florida’s Minimum Wage Changes Through 2026. Available online: https://hr.fsu.edu/article/floridas-minimum-wage-changes-through-2026 (accessed on 27 November 2022).

- United States Department of Agriculture, Foreign Agricultural Service (USDA FAS). Global Agricultural Trade System (GATS). Available online: https://apps.fas.usda.gov/GATS/default.aspx (accessed on 27 November 2022).

- Gereffi, G.; Lee, J.; Christian, M. US-Based Food and Agricultural Value Chains and Their Relevance to Healthy Diets. J. Hunger. Environ. Nutr. 2009, 4, 357–374. [Google Scholar] [CrossRef] [Green Version]

- Chanda, S.; Bhat, M.; Shetty, K.G.; Jayachandran, K. Technology, Policy, and Market Adaptation Mechanisms for Sustainable Fresh Produce Industry: The Case of Tomato Production in Florida, USA. Sustainability 2021, 13, 5933. [Google Scholar] [CrossRef]

- Parajuli, R.; Matlock, M.D.; Thoma, G. Cradle to Grave Environmental Impact Evaluation of the Consumption of Potato and Tomato Products. Sci. Total Environ. 2020, 758, 143662. [Google Scholar] [CrossRef]

- Winans, K.; Brodt, S.; Kendall, A. Life Cycle Assessment of California Processing Tomato: An Evaluation of the Effects of Evolving Practices and Technologies over a 10-Year (2005–2015) Timeframe. Int. J. Life Cycle Assess. 2019, 25, 538–547. [Google Scholar] [CrossRef] [Green Version]

- Heller, M.; Narayanan, T.; Meyer, R.; Koeleian, G. Category-Level Product Environmental Footprints of Foods: Food Life Cycle Assessment Literature Review. CSS Rep. Univ. Mich. Ann. Arbor 2016, 2, 1–14. [Google Scholar]

- Del Borghi, A.; Gallo, M.; Strazza, C.; Del Borghi, M. An Evaluation of Environmental Sustainability in the Food Industry through Life Cycle Assessment: The Case Study of Tomato Products Supply Chain. J. Clean. Prod. 2014, 78, 121–130. [Google Scholar] [CrossRef]

- Bernstad, A.K.; Cánovas, A.; Valle, R. Consideration of Food Wastage along the Supply Chain in Lifecycle Assessments: A Mini-Review Based on the Case of Tomatoes. Waste Manag. Res. 2017, 35, 29–39. [Google Scholar] [CrossRef] [PubMed]

- Van der Vorst, J.; Kooten, O.; Luning, P. Towards a Diagnostic Instrument to Identify Improvement Opportunities for Quality Controlled Logistics in Agrifood Supply Chain Networks. Int. J. Food Syst. Dyn. 2011, 2, 94–105. [Google Scholar] [CrossRef]

- Farris II, M.T. Solutions to Strategic Supply Chain Mapping Issues. Int. J. Phys. Distrib. Logist. Manag. 2010, 40, 164–180. [Google Scholar] [CrossRef]

- Hasibuan, A.; Arfah, M.; Parinduri, L.; Hernawati, T.; Suliawati; Harahap, B.; Sibuea, S.R.; Sulaiman, O.K.; Purwadi, A. Performance Analysis of Supply Chain Management with Supply Chain Operation Reference Model. J. Phys. Conf. Ser. 2018, 1007, 012029. [Google Scholar] [CrossRef]

- Hines, P.; Rich, N. The Seven Value Stream Mapping Tools. Int. J. Oper. Prod. Manag. 1997, 17, 46–64. [Google Scholar] [CrossRef] [Green Version]

- Gardner, J.T.; Cooper, M.C. Strategic Supply Chain Mapping Approaches. J. Bus. Logist. 2003, 24, 37–64. [Google Scholar] [CrossRef]

- Tummala, R.; Schoenherr, T. Assessing and Managing Risks Using the Supply Chain Risk Management Process (SCRMP). Supply Chain. Manag. Int. J. 2011, 16, 474–483. [Google Scholar] [CrossRef]

- Tagarakis, A.C.; Benos, L.; Kateris, D.; Tsotsolas, N.; Bochtis, D. Bridging the Gaps in Traceability Systems for Fresh Produce Supply Chains: Overview and Development of an Integrated IoT-Based System. Appl. Sci. 2021, 11, 7596. [Google Scholar] [CrossRef]

- Madevu, H.; Louw, A.; Ndanga, L.Z.B. Mapping the Competitive Food Chain for Fresh Produce Retailers in Tshwane, South Africa. In Proceedings of the International Association of Agricultural Economists Conference, Beijing, China, 16–22 August 2009. [Google Scholar]

- Norwood, F.B.; Peel, D. Supply Chain Mapping to Prepare for Future Pandemics. Appl. Econ. Perspect. Policy 2021, 43, 412–429. [Google Scholar] [CrossRef]

- Sultan, F.A.; Routroy, S.; Thakur, M. A Simulation-Based Performance Investigation of Downstream Operations in the Indian Surimi Supply Chain Using Environmental Value Stream Mapping. J. Clean. Prod. 2021, 286, 125389. [Google Scholar] [CrossRef]

- United States Department of Agriculture, National Agricultural Statistics Service (USDA-NASS). 2017 Census of Agriculture-State Data. Available online: https://www.nass.usda.gov/AgCensus/ (accessed on 7 February 2022).

- United States Department of Agriculture, National Agricultural Statistics Service (USDA-NASS). QuickStats Ad-Hoc Query Tool. Available online: https://quickstats.nass.usda.gov/ (accessed on 1 January 2022).

- Cao, X.; Guan, Z.; Vallad, G.E.; Wu, F. Economics of Fumigation in Tomato Production: The Impact of Methyl Bromide Phase-out on the Florida Tomato Industry. Int. Food Agribus. Manag. Rev. 2019, 22, 589–600. [Google Scholar] [CrossRef]

- Wu, F.; Qushim, B.; Guan, Z.; Boyd, N.S.; Vallad, G.E.; Macrae, A.; Jacoby, T. Weather Uncertainty and Efficacy of Fumigation in Tomato Production. Sustainability 2019, 12, 199. [Google Scholar] [CrossRef] [Green Version]

- United States Department of Agriculture, Economic Research Service (USDA-ERS). Methyl Bromide Phaseout Proceeds. Available online: https://www.ers.usda.gov/amber-waves/2003/april/methyl-bromide-phaseout-proceeds/ (accessed on 26 July 2022).

- Cook, R.; Calvin, L. Greenhouse Tomatoes Change the Dynamics of the North American Fresh Tomato Industry. Econ. Res. Rep. 2005, 2, 86. [Google Scholar]

- Wade, T.; Hyman, B.; McAvoy, E.; VanSickle, J. Constructing a Southwest Florida Tomato Enterprise Budget. Available online: https://edis.ifas.ufl.edu/publication/FE1087 (accessed on 12 January 2022).

- Cook, D.R. Fresh Tomato Production and Marketing Trends in the N. American Market. Available online: https://arefiles.ucdavis.edu/uploads/filer_public/fd/de/fddea761-ecf0-48c6-ac9a-223763d6ce23/cooknatomatoupdate150501.pdf (accessed on 10 January 2022).

- United States Department of Agriculture, Agricultural Marketing Service (USDA-AMS). Tomato Grades and Standards. Available online: https://www.ams.usda.gov/grades-standards/tomato-grades-and-standards (accessed on 26 July 2022).

- Lia, S.; Wu, F.; Guan, Z.; Luo, T. How Trade Affects the US Produce Industry: The Case of Fresh Tomatoes. Int. Food Agribus. Manag. Rev. 2022, 25, 121–133. [Google Scholar] [CrossRef]

- Wu, F.; Guan, Z.; Suh, D.H. The Effects of Tomato Suspension Agreements on Market Price Dynamics and Farm Revenue. Appl. Econ. Perspect. Policy 2018, 40, 316–332. [Google Scholar] [CrossRef]

- Guan, Z.; Wu, F.; Roka, F.; Whidden, A. Agricultural Labor and Immigration Reform. Choices 2015, 30, 61. [Google Scholar]

- Florida Tomato Committee. 2020–2021 Tomato Annual Report. Available online: https://www.floridatomatoes.org/ (accessed on 11 January 2022).

- United States Department of Agriculture, Agricultural Marketing Service (USDA-AMS). Market News—Fruit and Vegetable. Available online: https://www.marketnews.usda.gov/mnp/fv-home (accessed on 26 July 2022).

- Suslow, T.V.; Cantwell, M. Recommendations for Maintaining Postharvest Quality Produce Facts Tomato. Available online: https://postharvest.ucdavis.edu/files/259455.pdf (accessed on 16 March 2022).

- Sargent, S.A. Tomato Production Guide for Florida: Harvest and Handling 1 Maturity at Harvest. Available online: http://ufdcimages.uflib.ufl.edu/IR/00/00/46/81/00001/CV17400.pdf (accessed on 3 May 2022).

- United States Department of Agriculture, Economic Research Service (USDA-ERS). Retailing & Wholesaling. Available online: https://www.ers.usda.gov/topics/food-markets-prices/retailing-wholesaling/ (accessed on 26 July 2022).

- Capstone Partners. Food Distribution—June 2021. Available online: https://www.capstonepartners.com/insights/food-distribution-june-2021/ (accessed on 26 July 2022).

- United States Department of Agriculture, Agricultural Marketing Service (USDA-AMS). Refrigerated Truck Dashboard. Available online: https://internal.agtransport.usda.gov/stories/s/56s5-rpde (accessed on 26 July 2022).

- United Fresh Produce Association. FreshFacts on Retail Q1 2020. Available online: www.unitedfresh.org (accessed on 26 July 2022).

- United States Department of Agriculture, Economic Research Service (USDA-ERS). Food Expenditure Series. Available online: https://www.ers.usda.gov/data-products/food-expenditure-series/ (accessed on 26 July 2022).

- United States Census Bureau. Monthly Retail Trade—Time Series Data. Available online: https://www.census.gov/retail/marts/www/timeseries.html (accessed on 10 March 2022).

- Aradhyula, S.; Chin, E.; Duval, D.; Thompson, G.; Tronstad, R. Impact of COVID-19 Pandemic on Fresh Tomato Shipments and Prices. Available online: https://economics.arizona.edu/ImpactofCOVIDReport (accessed on 27 November 2022).

- Guan, Z.; Wu, F.; Sargent, S. FE1026: Labor Requirements and Costs for Harvesting Tomatoes. Available online: https://edis.ifas.ufl.edu/publication/FE1026 (accessed on 7 February 2022).

- Baskins, S.; Bond, J.; Minor, T. Unpacking the Growth in Per Capita Availability of Fresh Market Tomatoes. Veg. Pulses Outlook 2019, VGS-19C-01, 17. [Google Scholar]

- Ketzenberg, M.; Gaukler, G.; Salin, V. Expiration Dates and Order Quantities for Perishables. Eur. J. Oper. Res. 2018, 266, 569–584. [Google Scholar] [CrossRef]

- Trucking Workforce Issues Top the List of Industry Concerns. Available online: https://truckingresearch.org/2021/10/24/trucking-workforce-issues-top-the-list-of-industry-concerns/ (accessed on 27 November 2022).

- United States Bureau of Labor Statistics. Quarterly Census of Employment and Wages. Available online: https://www.bls.gov/CEW/ (accessed on 27 November 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| State | 2014 | 2019 |

|---|---|---|

| California | 8299 | 20,691 |

| Colorado | - | 7820 |

| Kentucky | 319 | 8073 |

| Tennessee | - | 23,202 |

| Texas | - | 19,927 |

| Utah | 53 | 8793 |

| Other States | 27,425 | 43,180 |

| U.S. Total | 36,095 | 131,685 |

| Tomato Varieties | Mature Stage | Production System & Characteristics |

|---|---|---|

| Round tomatoes | Mature green | Harvested from the open fields at stage 2 before changing color, then treated to induce ripening. Preferred by the foodservice sector for firmness and slicing characteristics. |

| Vine ripe | Harvested from the open fields at ripening stages. The main variety sold at retail. | |

| Tomatoes-on-the-vine (TOV) | TOVs are produced under protection and preferred by consumers. | |

| Roma/Plum | Mature Green/Vine ripe | Roma tomatoes can be produced in open fields and protected structures. These are traditionally used for canning or cooking. |

| Grape, cherry & other specialty tomatoes | N/A | These tomatoes can be produced in open fields and protected structure. Snacking varieties have gained popularity in all segments. |

| January | February | March | April | May | June | July | August | September | October | November | December | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Open Field | CA | √ | √ | √ | √ | √ | √ | √ | |||||

| FL | √ | √ | √ | √ | √ | √ | √ | √ | √ | ||||

| Rest of U.S. | √ | √ | √ | ||||||||||

| Sinaloa, MX | √ | √ | √ | √ | √ | ||||||||

| Greenhouse | U.S. | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ |

| Canada | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ | |||

| Mexico | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ | √ | |

| Maturity | Grade | Size | ||||||

|---|---|---|---|---|---|---|---|---|

| Season | Green | Ripe | 85% U.S. #1 | U.S. Combo | U.S. #2 | 5 × 6 | 6 × 6 | 6 × 7 |

| 2020/2021 | 85% | 15% | 66% | 16% | 18% | 50% | 33% | 17% |

| 2019/2020 | 85% | 15% | 65% | 15% | 20% | 50% | 32% | 18% |

| 2018/2019 | 88% | 12% | 63% | 19% | 18% | 49% | 33% | 18% |

| 2017/2018 | 87% | 13% | 59% | 24% | 17% | 51% | 32% | 17% |

| 2016/2017 | 87% | 13% | 52% | 33% | 15% | 52% | 33% | 15% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cui, X.; Guan, Z.; Morgan, K.L.; Huang, K.-M.; Hammami, A.M. Multitiered Fresh Produce Supply Chain: The Case of Tomatoes. Horticulturae 2022, 8, 1204. https://doi.org/10.3390/horticulturae8121204

Cui X, Guan Z, Morgan KL, Huang K-M, Hammami AM. Multitiered Fresh Produce Supply Chain: The Case of Tomatoes. Horticulturae. 2022; 8(12):1204. https://doi.org/10.3390/horticulturae8121204

Chicago/Turabian StyleCui, Xiurui, Zhengfei Guan, Kimberly L. Morgan, Kuan-Ming Huang, and A. Malek Hammami. 2022. "Multitiered Fresh Produce Supply Chain: The Case of Tomatoes" Horticulturae 8, no. 12: 1204. https://doi.org/10.3390/horticulturae8121204

APA StyleCui, X., Guan, Z., Morgan, K. L., Huang, K. -M., & Hammami, A. M. (2022). Multitiered Fresh Produce Supply Chain: The Case of Tomatoes. Horticulturae, 8(12), 1204. https://doi.org/10.3390/horticulturae8121204