Evolving Consumption Trends, Marketing Strategies, and Governance Settings in Ornamental Horticulture: A Grey Literature Review

Abstract

:1. Introduction

2. Methodology

3. The World and European Ornamental Sector

3.1. A Description of the Global Scenario

3.2. Relevant Insights from Europe

4. Ornamentals Consumption Trends in the European Context

4.1. The New Determinants of Consumption Trends: A Classification

4.2. Consumer Profiles and Dominant Consumption Trends

4.2.1. New High-Value Consumer Profiles

4.2.2. Dominant Trends in Flower and Plant Consumption Preferences and Behavior

- Consumers mostly prefer quality over priceConsumers ever more valuate and choose flowers and ornamental plants that are qualified as specialty goods and that offer multiple functional and emotional advantages [6,9,11,53,54].Specifically, they recognize and pay a premium for flowers and plants capable of symbolizing their identity values and tastes, and to provide them with specific benefits, not only in terms of aesthetics but also with reference to their personal realization and well-being. Accordingly, the European market registers an increase in the number and frequency of purchases of high value-added ornamental products.In line with this, refined bouquets and flower arrangements consolidate their positioning in both the segments of luxury gifts and events [4,11,49,81]. In these segments, main differentiation attributes become the following: rareness, creativity, branding, craftsmanship, and personalization. At the same time, flower and plant customized compositions acquire a growing market share in the segment of daily-use goods [5], as either decorations for homes and gardens or horti products [15,81].In particular, with reference to flower and plant material, consumers choose and remunerate the quality of specialty crops, i.e., using branded seeds, valorizing innovative and trendy species and varieties as well as traditional essences. In particular, good market performance is registered by seasonal off-the-cuff landraces and hardy and heat resistant crops [49,64,65,81].Besides that, high-value aesthetics and designs reinforce their role in winning the favor of consumers. To that regard, a new ethic-oriented canon is emerging in flower beauty: consumers request and value new organic and fresh-from-the-field styles of flowers and compositions, valorizing effortlessness and naturalness [97,98,99].

- Sustainability and transparency play as primary determinants of choiceAn increasing number of consumers, especially in the group of young educated people, make responsible consumption choices when purchasing flowers and plants. For example, in the representative German market, a share of about 20% of total consumers consider sustainability as a primary determinant of choice [21,22,23,49,65]. Furthermore, according to a survey carried out by Statista in June 2021, the ongoing pandemic furtherly focuses flowers and plants trade and consumption on the value of sustainability and regionality. In addition, it increases consumer willingness to pay for environmentally friendly and socially sustainable production and distribution processes [11].The growing consumer desire for sustainability is accompanied by a higher consideration for product transparency. As a consequence, flower and plant consumers are increasingly prepared to listen, learn and appreciate the value of product information [81].Accordingly, consumers appear to increase their desire and willingness to pay for new quality attributes intended to: disclose products origin; communicate their low environmental impact and high social fairness; promote their contribution to biodiversity preservation; highlight their functionality for a better quality of living [9,11,22,23,55].Therefore, higher price premiums are obtained by products that strategically use specific signaling tools. For example, a growing number of consumers perceive and remunerate the added value of quality and safety standards as well as origin marks and sustainability certifications schemes (e.g., fair trade, organic, GLOBAL GAP, etc.) [4,26,54,57,65,76,95,96,100].Likewise, consumers even consider the communicative value of packaging. In particular, they appreciate eco-friendly and plastic-free containers, vases, cartons, and wraps, either recycled or biodegradable [11,101], and appreciate their capacity to claim the product story, identity, and unique benefits.

- Consumers recognize and remunerate ornamental products for their socio-ecological and therapeutic functionalityEver more consumers are interested in discovering the unique and superior benefits flowers and plants can provide for multiple uses [6,102].Accordingly, especially in cities, both private ambiances and public spaces are changing their design, focusing on the valorization of the beneficial role of flowers and plants [11,64]. Indeed, in the consumers’ intention, the latter is used with multiple functions of: softening and beautifying urban landscapes, home, and commercial spaces; recalling a contact with nature; mitigating temperatures; purifying the air; treating stress disorders, concentration problems, and mental illnesses.In that regard, particular consideration should be given to the new role of plants in the transformation of home environments, such as livings, gardens, balconies, and workspaces. Specifically, concerning the indoor segment, consumers increase their spending on green plants, e.g., split-leaf species, scented, and air-cleaning, as well as on woody plants [49]. In addition, the gardening segment is characterized by an unprecedented positive trend in consumption. As a benchmark, in 2019, it registered a turnover of about EUR 4.4 billion in the representative German market [55]. Moreover, Messe Essen (2022) [11] reports recent estimations by Statista, evidencing that in 2021 around 15 million people aged over 14 spent time working in the garden several times per month, as far as around 9 million people doing it more times per week.Moreover, consumers increasingly perceive home gardens as unique places for happiness, absolving also to the purposes of recreation and food production [11,49]. Specifically, they find satisfaction in the creation and caring of near-natural spaces, providing them with joy and peace of mind, contributing to the surviving of insects and small animals, valorizing regional and native plants, and producing healthy zero-mile food.Consequently, a good market performance is registered by space-saving ornamentals (e.g., flowering perennials, beddings, and balcony plants), trees and shrubs as well as by fruit trees, cacti, vegetable crops, and herbs [11,49,55,65,81]. For example, a new trend for “nibbles gardens” is emerging [49,65]. In that regard, consumers research and pay for the specialty of snack and dwarf vegetable crops, fruit nibbles, aromatics, and officinal plants as well as easy-care and insect-friendly ornamental plants [11,49,55,64,81].Lastly, the expansion of the gardening segment boosts the growth of complementary markets, such as Do-It-Yourself (DIY) and hobby gardening, e.g., to buy integrated pests, near-natural fertilizers, recyclable materials, and innovative protection stuff [11,49,64]. At the same time, a fast-growing “smart gardening” segment is emerging, combining consumer interest in gardening with their desire to experiment with the high functionality of new smart devices and home automation technologies (e.g., robotic lawn mowers, digitally controlled irrigation systems, drones, etc.) [11,49,55,65].

- Consumers valuate ornamental products origin and show a preference for locally-grown and seasonal flowersConsumers appreciate the origin of ornamental products as a distinctive quality attribute, thus valuing their territorial linkage as a determinant of choice. In this sense, they consider not only the geographical provenance of the product but also the typicality of the used species and varieties and the adoption of traditional production and processing techniques [32].In light of that, a large part of consumers favors the purchase of both locally-and-nationally-grown flowers and plants. In addition, the market shows a new consumer interest in buying native species and varieties, even valorizing specialty crops and landraces that are typical of other countries [11].In light of the above, consumers are willing to pay a premium for ornamental products qualified by specific signs or storytelling, identifying their local or national provenance.

- Consumers attribute a growing added value to customized servicesIn line with the abovementioned trends, flower and plant consumers are changing their perception and remuneration of services (e.g., assistance, information, advice, composition, etc.). Accordingly, the flower market shows a shift in the composition of total consumer spending, characterized by a higher share for the remuneration of services, which become the main determinant of consumer choices and willingness to pay, while flowers and plants are considered components or “ingredients” [9,26,30,54,55,57,96].

- Consumers use alternative shopping channels and favor multi-channel experiencesSpecialized trade still maintains the largest share of the market. Nonetheless, consumers are increasingly hybrid in alternatively using specialized and non-specialized shopping channels [4,5,11].As a matter of fact, consumers increase channel switching frequency, on the basis of the purchase occasion and the wanted product category [49,54,63,66]. Accordingly, consumers are more likely to combine the use of specialized shops to purchase premium price products (e.g., rare essences, personalized compositions, or arrangements), with the use of non-specialized channels to buy standardized products (e.g., mono or mixed bouquets, ordinary houseplants, seeds, and gardening material) [9,54].Specifically, on the one hand, florists, kiosks, and street stalls still keep the highest share of the market, especially due to the expansion of luxury gifts and event segments. On the other hand, super-/hypermarkets and garden centers, followed by discounts and DIY, are rising their share, because of the higher sales of bouquets, houseplants (outdoor), and gardening products [4,5,49,50]. To illustrate, in the representative German market, in 2021, specialized trade accounted for a 60% share of private customers’ total expenditure for flowers and plants, covering 30% of the total purchased quantity, while large-scale retailers reached a share of 40% of total expenditure, and covered 70% of the total purchased quantity [11].Besides that, consumers are increasing their use and appreciation of online shopping channels. Remarkably, in consumer perception, online trade is complementing and integrating the role of stationary trade, but not replacing it. Indeed, while the market shows a swipe up of consumer spending on the online channel, the turnover of offline trade remains largely stable [9,65].In line with this, consumers–and particularly “Baby Boomers”-, show a preference for multi-channel shopping experiences [9,15,26,54,57,96]. In that regard, on the one hand, they choose and value the higher convenience, entertainment, and personalization of online searching and purchasing processes [9,11,65]. On the other hand, they still prefer to visit offline shops to experience and valuate products, picking up orders, enjoy moments of leisure, and relate with local growers and retailers [54,63].The positive trend in online sales started in the UK and Dutch markets, which represent the initiators of the trend in the European context, with a good performance in both the handicrafts and gardening segments [25,49]. Nowadays, online sales are experiencing a steady growth in major European markets (The Netherlands, France, Germany, and the UK), with the best performances of indoor and outdoor potted plants [4,11]. The good mood of online purchases in the gardening and DIY segments is flanked by the increase in online sales in the markets for flower and plant gifts and floral design arrangements [63].

4.2.3. A Focus on the Institutional Demand Segment

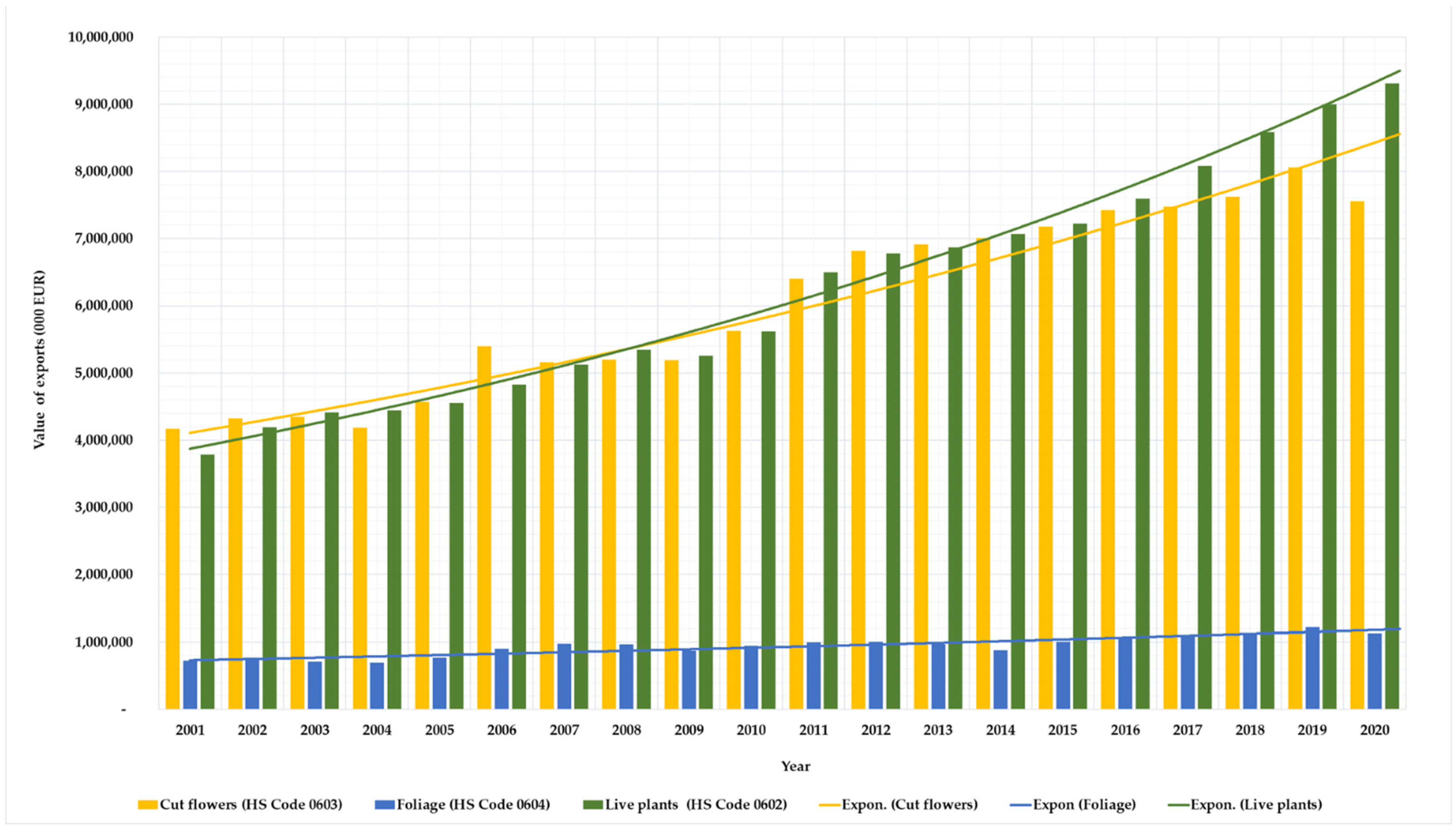

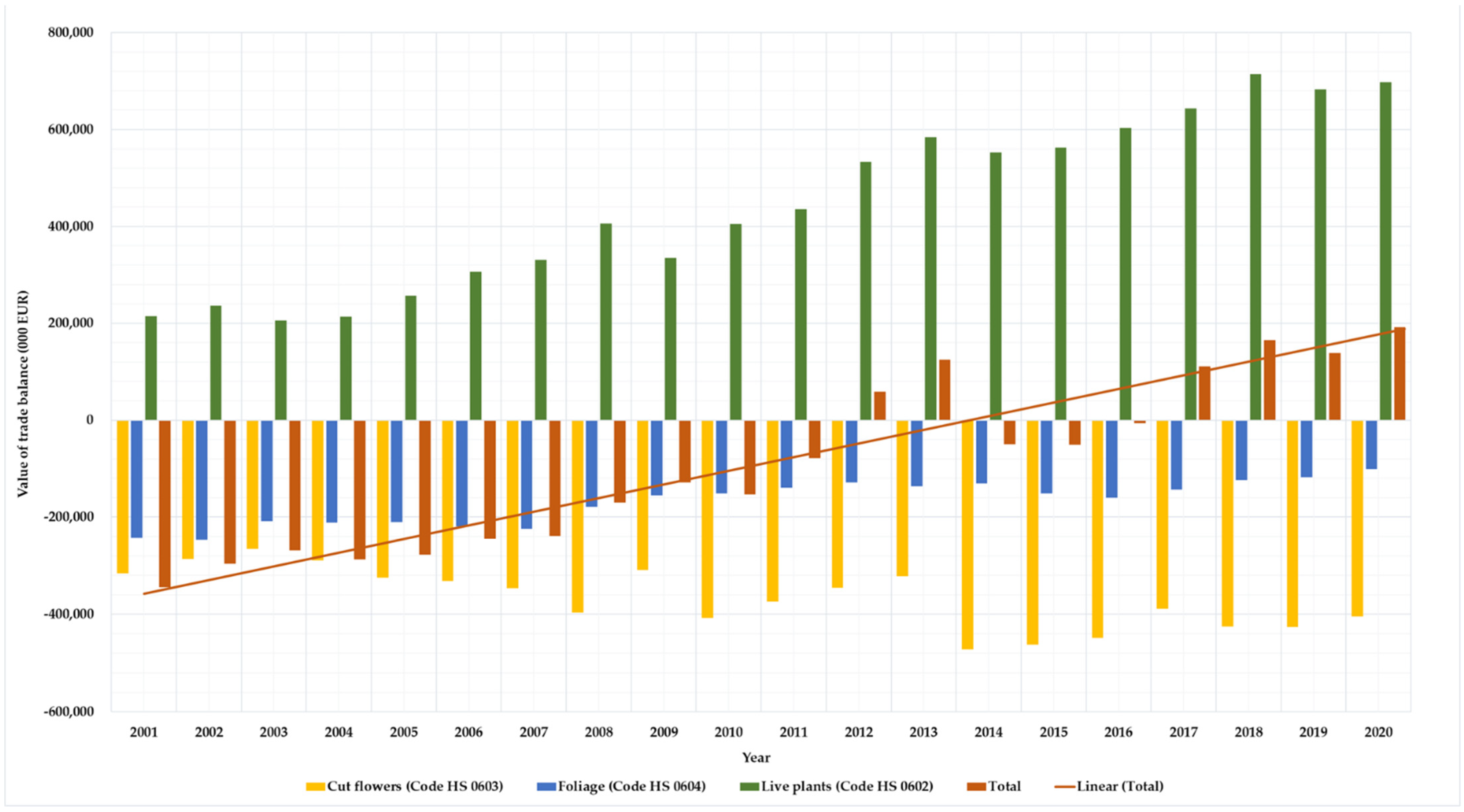

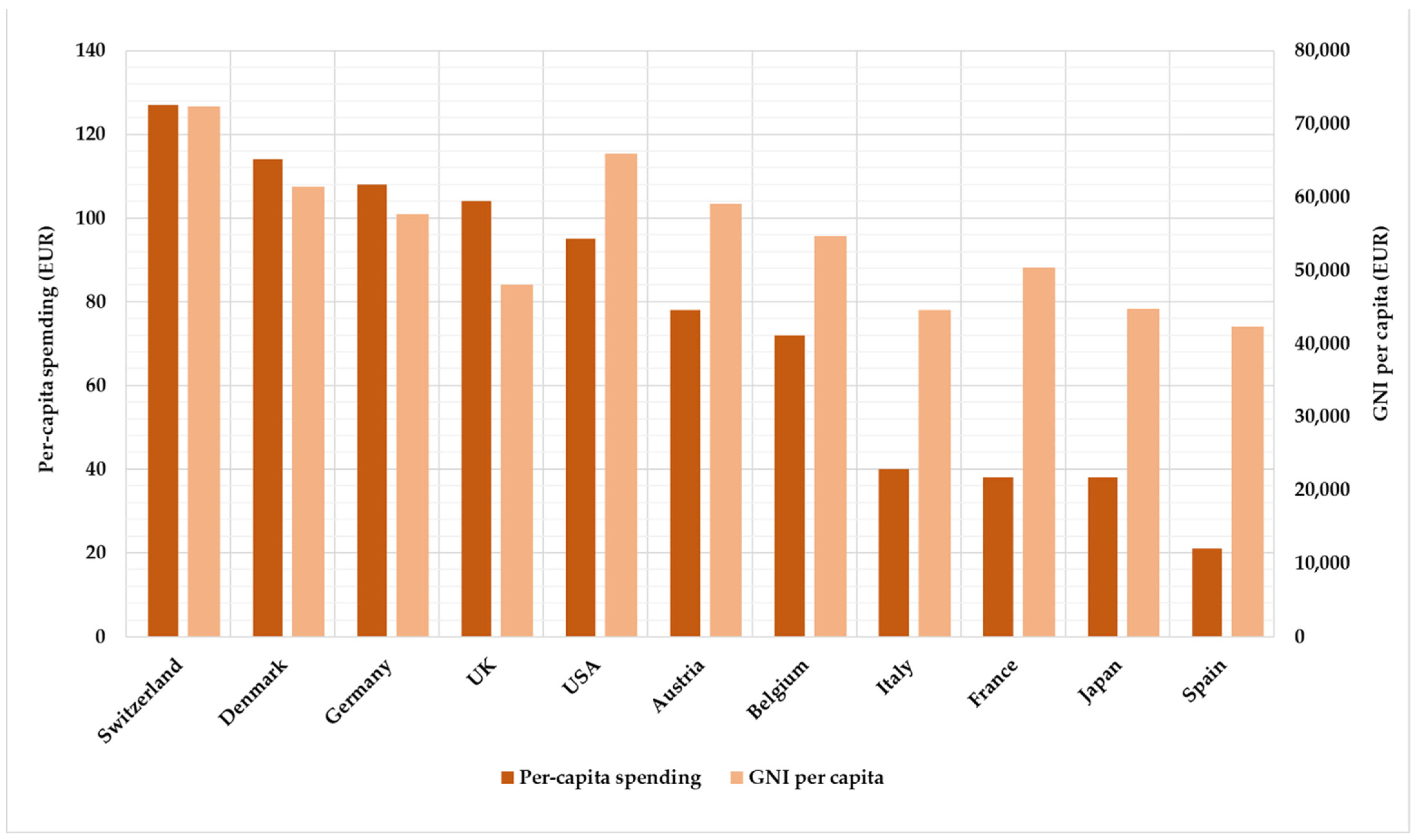

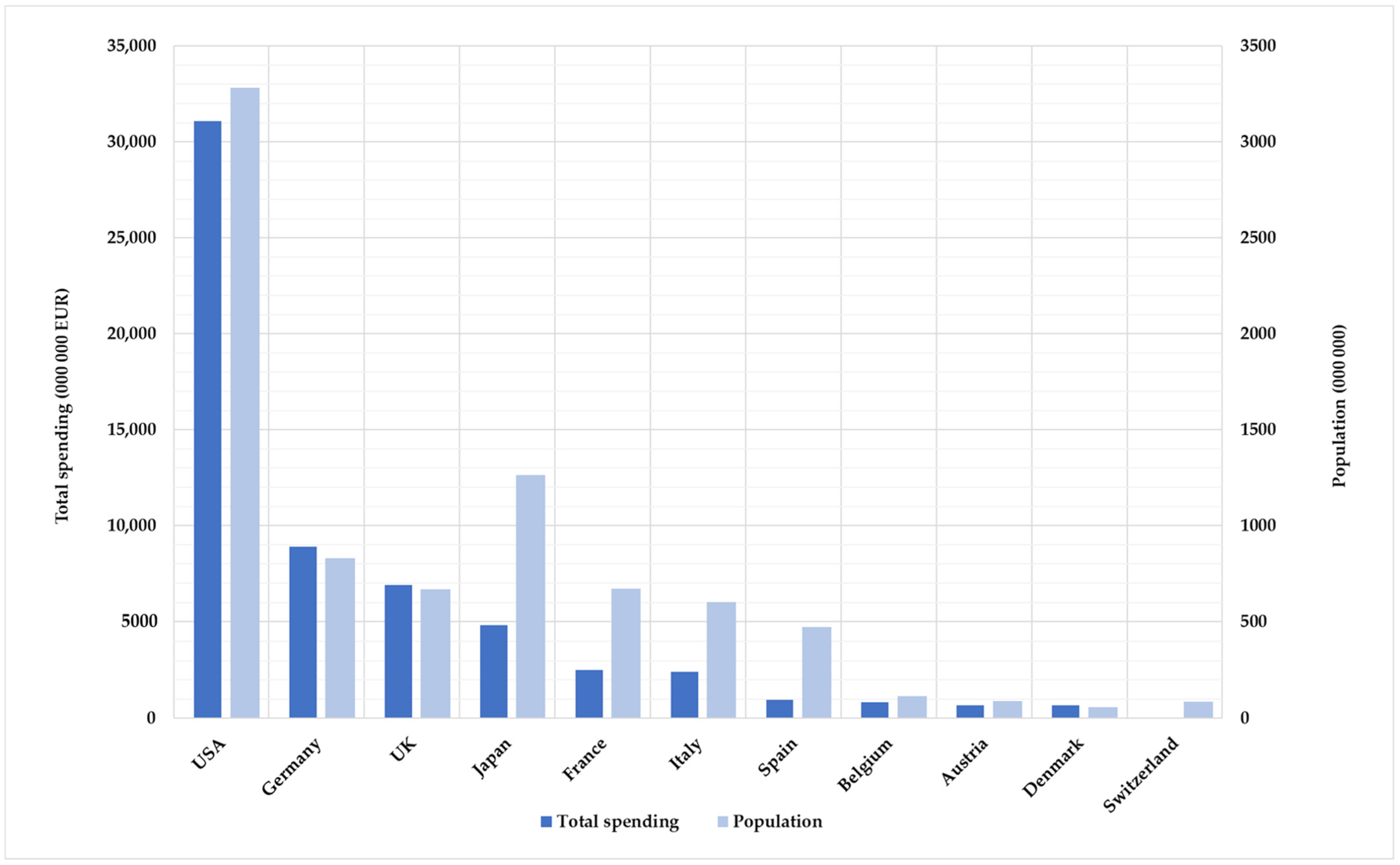

4.3. Consumer Spending and Consumption Value

5. Emerging Competitive Dynamics in the European Ornamental Sector

5.1. The European Competitive Environment and Evolving Marketing Strategies

5.2. The European Competitive Environment: The Role of Governance

- the specialist: targeting consumers who buy flowers and plants as a gift or for special occasions. It is centered on the role of specialist shops (florists, garden centers), auctions, wholesale markets, and growers, that are focused on the enhancement of specialty products and differential quality attributes;

- the big-box: specialized in serving large retailer outlets. This chain includes growers, indeed large growing companies and associations, service providers, that play a dominant role in dealing with sourcing, logistics, payments, and quality control, and large-scale retailers, as super/hypermarkets, DIY, and discount stores. The focus is on the realization of sustainable cost and operational advantages, valorizing responsive logistics and economies-of-scale;

- the e-commerce: targeting consumers buying flowers and plants online. It is characterized by short flexible connections between growers, digital marketplaces, and online retailers, committed to the pursuit of higher logistics efficiency, for assuring the satisfaction of a great number of small client-specific orders. Particular consideration should be also given to the entering into the market of new online retailers such as Amazon, or retailers with subscription models, such as Bloomon, or new logistical players, such as Post.nl.

6. A New Action-Research Agenda for the European Ornamental Horticulture Industry Development and Sustainability

- Product innovation and multifunctionalityAction research should favor the specification and implementation of new high-value quality and related product attributes capable of obtaining a price premium for the remuneration of producers and supply chains. In particular, the creation of innovative products with specific reference to the local provenance of flower and plant material, underutilized and neglected landraces, traditional crops, the sustainability of production methods, the socio-ecological functionality of varieties, and arrangement techniques should be further investigated.

- Consumer analysisAdvances in consumer analysis should sustain the action of high-cost producers and localized supply systems in identifying consumers’ attitudes and evaluating their willingness to pay in both private and institutional segments. In this regard, specific attention should be paid to the description analysis of new consumer profiles.

- Quality-oriented marketing strategiesAction research should sustain new valuable approaches to market segmentation and sustainable differentiation, favoring the identification and targeting of emerging niche markets, recognizing and remunerating specific quality attributes. Accordingly, future goals should evaluate the potential of creating product brands, adopting origin signs and certification schemes, enhancing products transparency, and consumer engagement.The institutional market segment should be also considered for the valorization of high-value products and services, with specific attention to floral design, landscaping, and urban greening.The pursuit of higher competitiveness of high-cost domestic producers and localized supply systems asks for in-depth research on the potential of direct or short distribution channels, also paying attention to the role of online trade and digitalization.

- Collaborative Governance settingsResearch advances are needed to favor the innovation and reinforcement of governance settings, both public and private. On the public side, research should support the improvement and harmonization of policies, standards, and legislations, at both the EU and national level. To that end, particular consideration should be given to foster the recognition and remuneration of the strategic role of the ornamental sector in sustaining the realization of the EU Green Deal strategy goals and of the related EU and national agricultural, social and environmental policies, programmes, and regulations.On the private side, new forms of coordination, cooperation, and collaboration, at both the horizontal and vertical level, should be studied, discussed, and validated, for the enhancement of supply chains competitiveness, guaranteeing not only a generation but also a fair distribution of benefits, towards higher social, economic, and environmental sustainability.

- Dedicated research observatoriesThe construction of dedicated research observatories at the national or European level, committed to improving the availability of harmonized, updated, and reliable quantitative and qualitative data, is fundamental to support the new positioning of the ornamental sector and the implementation of effective marketing strategies and multi-actor governance models and the realization of participatory action-research.This could support the development of academic and institutional research, according to the hypotheses identified by this work, and, on the other hand, promote a more widespread ability to forecast and strategic planning among the various actors for the realization of new competitive objectives.

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Volckaert, E.; Gobin, B. “Ornamental Plants and Floriculture” Soils, Plant Growth and Crop Production. Encyclopedia of Life Support System (EOLLSS). UNESCO-EOLSS Sample Chapters C 10. 2014. Available online: https://www.eolss.net/Sample-Chapters/C10/E1-05A-51.pdf (accessed on 2 February 2022).

- Yahia, E.M. Chapter 3—Classification of Horticultural Commodities. In Postharvest Technology of Perishable Horticultural Commodities; Yahia, E.M., Ed.; Woodhead Publishing: Cambridge, UK, 2019; pp. 71–97. ISBN 9780128132760. [Google Scholar]

- Oxford Economics. The Economic Impact of Ornamental Horticulture and Landscaping in the UK. A Report for the Ornamental Horticulture Round Table Group. October 2018. Available online: https://www.rhs.org.uk/science/pdf/The-economic-impact-of-ornamental-horticulture-and.pdf (accessed on 3 February 2022).

- Van Horen, L. A Mixed Bouquet of Development in Floriculture-World Floriculture Map 2021. RaboResearch Food&Agribusiness Rabobank, January 2022. Available online: https://research.rabobank.com/far/en/documents/179560_Rabobank_A-Mixed-Bouquet-of-Developments-World-Floriculture-Map-2021_vanHoren_January2022.pdf (accessed on 31 January 2022).

- RaboResearch Food&Agribusiness World Floriculture Map 2021. Rabobank: Utrecht, The Netherlands, January 2022. Available online: https://research.rabobank.com/far/en/documents/175926_Rabobank_Flower-Map-2021_20211230.pdf (accessed on 31 January 2022).

- Hendricks, J.; Briercliffe, T.; Oosterom, B.; Treer, A.; Kok, G.; Edwards, T.; Kong, H. Ornamental Horticulture, A Growing Industry? International Vision Project Reports. AIPH Horticulture House: Chilton Didcot, Oxfordshire, UK, September 2019. Available online: https://aiph.org/giic/international-vision-project-reports/ (accessed on 25 January 2022).

- Hendricks, J.; Briercliffe, T.; Oosterom, B.; Treer, A.; Kok, G.; Edwards, T.; Kong, H. Production and Markets, the Future of Ornamentals. International Vision Project Reports. AIPH Horticulture House: Chilton Didcot, Oxfordshire, UK, July 2019. Available online: https://aiph.org/giic/international-vision-project-reports/ (accessed on 25 January 2022).

- Coherent Market Insights (CMI) Floriculture Market. Global Industry Insights, Trends, Outlook, and Opportunity Analysis, 2019–2027. CMI Floriculture Market Report. August 2019. Available online: https://www.coherentmarketinsights.com/market-insight/floriculture-market-1586 (accessed on 4 February 2022).

- Van Horen, L. Flourishing Flowers, Promising Plants: Changes in Consumer Behaviour. RaboResearch Food&Agribusiness Rabobank, December 2017. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/flourishing_flowers_promising_plants_changes_in_consumer_behaviour.html (accessed on 5 June 2021).

- Centre for the Promotion of Imports from Developing Countries of The Netherlands Ministry of Foreign Affairs (CBI). What Competition Do You Face on the European Cut Flowers and Foliage Market? CBI Ministry of Foreing Affairs Market Information. 3 May 2017. Available online: https://www.cbi.eu/market-information/cut-flowers-foliage/competition (accessed on 3 February 2022).

- Löbke, A. Record Sales for the Flower and Plant Market. MESSE ESSEN Press Text. 25 January 2022. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 27 January 2022).

- Assembly of European Horticultural Regions (AREFLH). Position Paper on the European Ornamental Plant Sector. AREFLH Position Statements. April 2020. Available online: https://www.areflh.org/en/aboutus/positions/position-statement-plants (accessed on 25 January 2022).

- Mattia, G. Il Neo-Lusso. Marketing e Consumi di Qualità in Tempi di Crisi; FrancoAngeli: Milan, Italy, 2013; ISBN 8820451727. [Google Scholar]

- Borsellino, V.; Schimmenti, E.; El Bilali, H. Agri-food markets towards sustainable patterns. Sustainability 2020, 12, 2193. [Google Scholar] [CrossRef] [Green Version]

- MESSE ESSEN GmbH Press Media Center for IPM Essen. Green, Great, Gorgeous! Excellent Mood at IPM ESSEN 2020. IPM ESSEN 2020 Final Report. Essen, Germany, 31 January 2020. Available online: https://www.ipm-essen.de/news-en/ (accessed on 30 October 2021).

- Sharathkumar, M.; Peter, K.V.; Rajeevan, P.K. Ornamentals for greening. Acta Hortic. 2017, 1165, 45–56. [Google Scholar] [CrossRef]

- Yue, C.; Dennis, J.H.; Behe, B.K.; Hall, C.R.; Campbell, B.L.; Lopez, R.G. Investigating Consumer Preference for Organic, Local, or Sustainable Plants. HortScience 2011, 46, 610–615. [Google Scholar] [CrossRef] [Green Version]

- Isaak, M.; Wolfgang, L. Consumer Preferences for Sustainability in Food and Non-Food Horticulture Production. Sustainability 2020, 12, 7004. [Google Scholar] [CrossRef]

- Bulgari, R.; Petrini, A.; Cocetta, G.; Nicoletto, C.; Ertani, A.; Sambo, P.; Ferrante, A.; Nicola, S. The Impact of COVID-19 on Horticulture: Critical Issues and Opportunities Derived from an Unexpected Occurrence. Horticulturae 2021, 7, 124. [Google Scholar] [CrossRef]

- McBain, J. Post COVID-19 Consumer Landscape. Finding Opportunities Amid Upheaval. Lecture Presented at the Conference “AIPH Virtual International Conference. Recovery from Crisis—The Future for Ornamentals”. 15 September 2020. Available online: https://aiph.org/event/recovery-from-crisis/ (accessed on 4 February 2022).

- Hall, C.R.; Knuth, M.J. An Update of the Literature Supporting the Well-Being Benefits of Plants: Part 4—Available Resources and Usage of Plant Benefits Information. J. Environ. Hortic. 2020, 38, 68–72. [Google Scholar] [CrossRef]

- International Association of Horticultural Producers (AIPH). How Gardening Will Keep You Well during the Coronavirus Pandemic. Factsheets. March 2020. Available online: https://aiph.org/latest-news/gardening-will-keep-you-well-during-the-coronavirus-pandemic/ (accessed on 27 January 2022).

- International Association of Horticultural Producers (AIPH). How Flowers Can Help during the Coronavirus Pandemic. Factsheets. March 2020. Available online: https://aiph.org/latest-news/how-flowers-will-help-keep-you-well-during-quarantine/ (accessed on 27 January 2022).

- Havardi-Burger, N.; Mempel, H.; Bitsch, V. Sustainability Challenges and Innovations in the Value Chain of Flowering Potted Plants for the German Market. Sustainability 2020, 12, 1905. [Google Scholar] [CrossRef] [Green Version]

- Van Rijswick, C. World Floriculture Map 2016: Equator Countries Gathering Speed. RaboResearch Food&Agribusiness Rabobank, November 2016. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/world_floriculture_map_2016.html (accessed on 23 May 2021).

- van Horen, L. Towards Smarter Floriculture Chains. Lecture Presented at the Conference “CROP Innovation & Business”, Amsterdam, The Netherlands. 4 April 2017. Available online: https://www.cropib.com/storage/app/media/Programme_2017/Presentations/4b.%20Ornamentals%20-%20Lambert%20van%20Horen.pdf (accessed on 5 June 2021).

- Zarbà, A.S.; Di Vita, G.; Allegra, V. Strategy Development for Mediterranean Pot Plants: A Stakeholder Analysis. Qual.-Access Success 2013, 14, 52–58. [Google Scholar]

- Darras, A. Overview of the Dynamic Role of Specialty Cut Flowers in the International Cut Flower Market. Horticulturae 2021, 7, 51. [Google Scholar] [CrossRef]

- Karpun, O. Conceptual model of floriculture supply chain management. Intellect. Logist. Supply Chain Manag. 2020, 4, 41–52. [Google Scholar] [CrossRef]

- van Horen, L. Flourishing Flowers, Promising Plants: Internationalisation Strategy. RaboResearch Food&Agribusiness Rabobank, December 2017. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/Flourishing_flowers_promising_plants_Internationalisation_strategy.html (accessed on 6 June 2021).

- Lambrecht, E.; Taragola, N.; Kühne, B.; Crivits, M.; Gellynck, X. Networking and innovation within the ornamental plant sector. Agric. Food Econ. 2015, 3, 10. [Google Scholar] [CrossRef] [Green Version]

- Gabellini, S.; Scaramuzzi, S. Luxury strategies for agricultural products: A new sustainable governance model for the valorisation of the Tuscan flower supply chain. In Green Metamorphoses: Agriculture, Food, Ecology. Proceedings of the LV Conference of SIDEA Studies; Torquati, B., Marchini, A., Eds.; Wageningen Academic Publishers: Wageningen, The Netherlands, 2020; pp. 413–423. ISBN 978-90-8686-347-1. [Google Scholar]

- Hall, C.R. Business Decisions to Help Me Outshine the Competition. The Association of Horticulture Professionals (OFA) Bullettin No. 932 March/April 2012. Available online: https://cdn.coverstand.com/4456/102937/102937.1.pdf (accessed on 2 February 2022).

- Di Vita, G.; Allegra, V.; Zarbà, A.S. Building scenarios: A qualitative approach to forecasting market developments for ornamental plants. Int. J. Bus. Glob. 2015, 15, 130–151. [Google Scholar] [CrossRef]

- Owen, J.S., Jr.; LeBude, A.V.; Calabro, J.; Boldt, J.K.; Gray, J.; Altland, J.E. Research Priorities of the Environmental Horticultural Industry Founded through Consensus. J. Environ. Hortic. 2019, 37, 120–126. [Google Scholar] [CrossRef]

- Cardoso, B.F.; Rasetti, M.; Giampietri, E.; Finco, A.; Shikida, P.F.A. Trade Dynamics in the Italian Floriculture Sector within EU Borders: A Gravity Model Analysis. AGRIS-Line Pap. Econ. Inform. 2017, 9, 23–32. [Google Scholar] [CrossRef] [Green Version]

- Wani, M.A.; Nazki, I.T.; Din, A.; Iqbal, S.; Wani, S.A.; Khan, F.U. Floriculture Sustainability Initiative: The Dawn of New Era. In Sustainable Agriculture Reviews 27. Sustainable Agriculture Reviews; Lichtfouse, E., Ed.; Springer: Cham, Switzerland, 2018; Volume 27, pp. 91–127. ISBN 978-3-319-75190-0. [Google Scholar]

- Dominguez, G.B.; Mibus-Schoppe, H.; Sparke, K. Evaluation of Existing Research Concerning Sustainability in the Value Chain of Ornamental Plants. Eur. J. Sustain. Dev. 2017, 6, 11. [Google Scholar] [CrossRef]

- Floriculture Sustainability Initiative (FSI) 2025. FSI 2025 Strategy Summary for Approval by the FSI General Assembly. FSI 2025 Summary Strategy Paper. 2 February 2021. Available online: https://www.fsi2025.com/wp-content/uploads/2021/02/FSI-2025-SUMMARY.pdf (accessed on 3 February 2022).

- Snyder, H. Literature review as a research methodology: An overview and guidelines. J. Bus. Res. 2019, 104, 333–339. [Google Scholar] [CrossRef]

- Torraco, R.J. Writing Integrative Literature Reviews: Using the Past and Present to Explore the Future. Hum. Resour. Dev. Rev. 2016, 15, 404–428. [Google Scholar] [CrossRef]

- Farace, D.; Schöpfel, J. Grey Literature. In Encyclopedia of Library and Information Sciences; Bates, M.J., Maack, M.N., Eds.; CRC Press: Boca Raton, FL, USA, 2015; pp. 2029–2039. ISBN 9780203757635. [Google Scholar]

- Da Silva, R.N.; Brandão, M.A.G.; Ferreira, M.D.A. Integrative Review as a Method to Generate or to Test Nursing Theory. Nurs. Sci. Q. 2020, 33, 258–263. [Google Scholar] [CrossRef] [PubMed]

- Whittemore, R.; Knalf, K. The integrative review: Updated methodology. J. Adv. Nurs. 2005, 52, 546–553. [Google Scholar] [CrossRef] [PubMed]

- Bonato, S. Searching the Grey Literature. A Handbook for Searching Reports, Working Papers, and Other Unpublished Research; Rowman & Littlefield Publishers: Lanham, MD, USA, 2018; ISBN 978-1-5381-0063-9. [Google Scholar]

- Saunders, B.; Sim, J.; Kingstone, T.; Baker, S.; Waterfield, J.; Bartlam, B.; Burroughs, H.; Jinks, C. Saturation in qualitative research: Exploring its conceptualization and operationalization. Qual. Quant. 2018, 52, 1893–1907. [Google Scholar] [CrossRef] [PubMed]

- van Rijswick, C. World Floriculture Map 2015: Gearing Up For Stronger Competition. RaboResearch Food&Agribusiness Rabobank Industry Note #475. January 2015. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/world_floriculture_map_2015.html (accessed on 12 March 2021).

- Hübner, S. International Statistics Flowers and Plants 2021; International Association of Horticultural Producers (AIPH) and International Flower Trade Association (Union Fleurs); AIPH Horticulture House: Oxfordshire, UK, 2021; Volume 69, ISBN 978-1-9164807-9-7. [Google Scholar]

- Kirchhoff, A. BGI Markt + Trend. Ausbage IPM 2020. BGI Service UG: Straelen-Herongen, Germany, 2020. Available online: https://bgi-ev.de/data/2020/01/BGI_Folder_MarktTrend_A4_2020_WEB.pdf (accessed on 6 June 2021).

- Hübner, S. International Statistics Flowers and Plants 2020; International Association of Horticultural Producers (AIPH) and International Flower Trade Association (Union Fleurs); Horticulture House: Oxfordshire, UK, 2020; Volume 68. [Google Scholar]

- International Trade Center (ITC) Trade Map. Available online: https://www.trademap.org/Index.aspx (accessed on 31 January 2022).

- European Commission Taxation and Customs Union Harmonized System-General Information. Available online: https://ec.europa.eu/taxation_customs/business/calculation-customs-duties/customs-tariff/harmonized-system-general-information_en (accessed on 1 February 2022).

- Altmann, M. Developments and Trends in the Flower and Plant Market for 2015/2016, Stability Is Not Enough: New Markets Are Important-IPM ESSEN 2016. MESSE ESSEN Press Text. Essen, Germany, October 2015. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 27 May 2021).

- Kirchhoff, A. BGI Markt + Trend. Ausbage IPM 2019. BGI Service UG: Straelen-Herongen, Germany, 2019. Available online: https://bgi-ev.de/data/2019/01/BGI_Folder_MarktTrend_IPM19_WEB.pdf (accessed on 6 June 2021).

- MESSE ESSEN GmbH Press Media Center for IPM Essen. “We Gardeners Can Do Climate!”: Sustainability and Climate Change Were Defining Subjects at the World’s Leading Fair for Horticulture. IPM ESSEN 2019 Final Report. Essen, Germany, 25 January 2019. Available online: https://www.ipm-essen.de/news-en/ (accessed on 16 September 2021).

- Mamias, S. The Floriculture Supply-Chain: Characteristics & Prospects. Lecture Presented at the Seminar “Supply-Chains in the Agri-Food Sector as the UK Leaves the EU”, Amsterdam, The Netherlands. 8 February 2018. Available online: https://unionfleurs.org/industry/ (accessed on 25 January 2022).

- Mamias, S. Opportunities for Market Diversification. Lecture Presented at the “Kenya Flower Industry Sustainability Conference”, Nairobi, Kenya. 6 June 2017. Available online: https://unionfleurs.org/industry/ (accessed on 25 January 2022).

- RaboResearch Food&Agribusiness World Floriculture Map 2016. Rabobank: Utrecht, The Netherlands, November 2016. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/world_floriculture_map_2016.html (accessed on 23 May 2021).

- RaboResearch Food&Agribusiness World Floriculture Map 2015. Rabobank: Utrecht, The Netherlands, January 2015. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/world_floriculture_map_2015.html (accessed on 12 March 2021).

- European Commission Directorate-General for Agriculture and Rural Development (DG AGRI). Unit G.2—Wine, Spirits, and Horticultural Products Working Document. Horticultural Products. Flowers and Ornamental Plants-Production Statistics 2010–2019. DGAGRI-G2. 10 February 2020. Available online: https://ec.europa.eu/info/food-farming-fisheries/plants-and-plant-products/live-plants-and-flowers_en (accessed on 3 January 2022).

- European Commission Directorate-General for Agriculture and Rural Development (DG AGRI). Unit G.2—Wine, Spirits, and Horticultural Products Working Document. Horticultural Products. Flowers and Ornamental Plants Statistics 2006–2016. DGAGRI-G2. 23 November 2017. Available online: https://ec.europa.eu/info/food-farming-fisheries/plants-and-plant-products/live-plants-and-flowers_en (accessed on 28 October 2020).

- Lariviere, V. Live Plants and Products of Floriculture Sector in the EU. Lecture Presented at the Parliament’s Committee on Agriculture and Rural Development (AGRI Committee), Brussels, Belgium. 12 December 2017. Available online: https://ec.europa.eu/info/food-farming-fisheries/plants-and-plant-products/live-plants-and-flowers_en (accessed on 28 October 2020).

- Löbke, A. The Flower and Plant Market in 2019 (IPM Essen 2020). MESSE ESSEN Press Text. 30 October 2019. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 30 October 2021).

- Altmann, M.; Löbke, A. IPM Market Description of the Flower and Plant Markets, Part 1. Best Economic Prerequisites for IPM ESSEN 2018. MESSE ESSEN Press Text. Essen, Germany, 7 December 2017. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 12 June 2021).

- Altmann, M.; Löbke, A. IPM Market Description of the Flower and Plant Markets, Part 2. IPM ESSEN 2018 Focuses on Individualisation and Digitalisation. MESSE ESSEN Press Text. Essen, Germany, 14 December 2017. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 12 June 2021).

- MESSE ESSEN GmbH Press Media Center for IPM Essen. Heat, Water Shortage and Rising Ecological Awareness: IPM ESSEN 2020 Shows Trends and New Products. IPM ESSEN 2020 News. Essen, Germany, 27 January 2020. Available online: https://www.ipm-essen.de/news-en/ (accessed on 30 October 2021).

- Wakefield, R. Growers and Traders Discuss the Impacts of Brexit on the Global Ornamental Horticulture Industry. AIPH News. 3 December 2020. Available online: https://aiph.org/latest-news/growers-and-traders-discuss-the-impacts-of-brexit-on-the-global-ornamental-horticulture-industry/ (accessed on 27 January 2022).

- Altmann, M.; Löbke, A. The Climate Influences the Turnover in the International Green Sector-IPM ESSEN 2019. MESSE ESSEN Press Text. Essen, Germany, 21 November 2018. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 13 June 2021).

- International Flower Trade Association (UNION FLEURS). EU-Wide Survey Provides a First Estimate of the Brutal Impact of COVID-19 Pandemic on the European Flower & Live Plants Sector (March–April 2020). Union Fleurs News. 16 June 2020. Available online: https://unionfleurs.org/news_events/eu-wide-survey-provides-a-first-estimate-of-the-brutal-impact-of-covid-19-pandemic-on-the-european-flower-live-plants-sector-march-april-2020/ (accessed on 25 January 2022).

- FloraCulture International-International Association of Horticultural Producers (AIPH). Coronavirus Global Impact Survey-Datasheet Revised Part 1. March 2020. Available online: https://aiph.org/latest-news/horticultural-industry-looks-to-the-future-in-the-latest-covid-19-global-impact-survey/ (accessed on 26 January 2022).

- FloraCulture International-International Association of Horticultural Producers (AIPH). Coronavirus Global Impact Survey-Datasheet Revised Part 2. May 2020. Available online: https://aiph.org/latest-news/horticultural-industry-looks-to-the-future-in-the-latest-covid-19-global-impact-survey/ (accessed on 26 January 2022).

- Van Horen, L.; van Rijswick, C. Floriculture Demand Collapses Dramatically Under Coronavirus Pressure. RaboResearch Food&Agribusiness Rabobank, March 2020. Available online: https://research.rabobank.com/far/en/sectors/fresh-produce/floriculture-demand-collapses-under-coronavirus.html (accessed on 31 October 2021).

- Van Tol, F. FCI—Reflecting on the Long-Term Impact of COVID-19. FloraCulture International-AIPH Issue: July-August 2020. Available online: https://aiph.org/covid-19/long-term-impact/ (accessed on 26 January 2022).

- Wakefield, R. Resilience and Positivity in the Face of Adversity at the AIPH Recovery from Crisis Conference. AIPH News. 17 September 2020. Available online: https://aiph.org/latest-news/resilience-and-positivity-in-the-face-of-adversity-at-the-aiph-recovery-from-crisis-conference/ (accessed on 27 January 2022).

- International Association of Horticultural Producers (AIPH). Sustainability. The Growing Global Population Places Increasing Demands on Our Natural Resources. Available online: https://aiph.org/ornamentals-production/sustainability/ (accessed on 3 February 2022).

- Van Horen, L. Flourishing Flowers, Promising Plants: Embracing Sustainability. RaboResearch Food&Agribusiness Rabobank, December 2017. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/Flourishing_flowers_promising_plants_Embracing_sustainability.html (accessed on 5 June 2021).

- Van Horen, L. Flourishing Flowers, Promising Plants: Chain Organisation in European Floriculture. RaboResearch Food&Agribusiness Rabobank, November 2017. Available online: https://research.rabobank.com/far/en/sectors/regional-food-agri/flourishing_flowers_promising_plants_chain_organisation_in_european_floriculture.html (accessed on 5 June 2021).

- Corbellini, E.; Saviolo, S. L’Esperienza del Lusso. Mondo, Mercati, Marchi; Rizzoli: Milan, Italy, 2007; ISBN 8817095273. [Google Scholar]

- International Association of Horticultural Producers (AIPH). AIPH International Conference: The Path to Sustainability in Ornamental Horticulture. Available online: https://aiph.org/event/sustainability-conference-2021/ (accessed on 30 January 2022).

- Kirchhoff, A. BGI Trade Center IPM 2018. BGI Service UG: Straelen-Herongen, Germany, 2018. Available online: https://bgi-ev.de/data/2018/01/BGI_TradeCenter_2018_WEB-final.pdf (accessed on 5 June 2021).

- Altmann, M.; Löbke, A. The Green Sector is Characterised by these Currents-IPM ESSEN 2019. MESSE ESSEN Press Text. Essen, Germany, 21 November 2018. Available online: https://www.ipm-essen.de/press/press-texts/ (accessed on 13 June 2021).

- Wakefield, R. Horticultural Industry Looks to the Future in the Latest COVID-19 Global Impact Survey. FloraCulture International-AIPH Press Release. 29 May 2020. Available online: https://aiph.org/latest-news/horticultural-industry-looks-to-the-future-in-the-latest-covid-19-global-impact-survey/ (accessed on 26 January 2022).

- International Association of Horticultural Producers (AIPH). Global Impact of Coronavirus Pandemic on Garden Centres. April 2020. Available online: https://aiph.org/latest-news/global-impact-of-coronavirus-pandemic-on-garden-centres/ (accessed on 27 January 2022).

- Van Rijswick, C.; Fumasi, R.; van Horen, L.; Higgins, H.; Magaña, D. Coronavirus Concerns in the Global Fresh Produce Sector: Different Every Day. RaboResearch Food&Agribusiness Rabobank, March 2020. Available online: https://research.rabobank.com/far/en/sectors/fresh-produce/corona-concerns-in-the-global-fresh-produce-sector.html (accessed on 31 October 2021).

- International Association of Horticultural Producers (AIPH). Coronavirus Global Impact Survey on the Ornamental Horticultural Industry (Part 2). 2020. Available online: https://aiph.org/wp-content/uploads/2020/11/Coronavirus-Global-Impact-Survey-Particpant-Comments.pdf (accessed on 27 January 2022).

- European Commission. A European Green Deal. Striving to be the First Climate-Neutral Continent. EU Commission Strategy, Priorities 2019–2024. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en#thebenefitsoftheeuropeangreendeal (accessed on 21 February 2022).

- Moonen, G. (Ed.) The New CAP Creating New Horizons. Journal n. 2/2021; European Court of Auditors: Luxembourg, 2021; QJ-AD-21 002-2A-N. [Google Scholar]

- European Commission. The CAP Reform’s Compatibility with the Green Deal’s Ambition. EU Commission News. Agriculture and Rural Development: Brussels, Belgium, 20 May 2020. Available online: https://ec.europa.eu/info/news/cap-reforms-compatibility-green-deals-ambition-2020-may-20_it (accessed on 21 February 2022).

- Bruns, J.D. Let Us Plant and Tree Nurseries Be Part of the European Green Deal. FloraCulture International-AIPH EU, 31 May 2020. Available online: https://aiph.org/floraculture/news/let-us-plant-and-tree-nurseries-be-part-of-the-european-green-deal/ (accessed on 21 February 2022).

- International Flower Trade Association (UNION FLEURS). STATEMENT: Situation of the Ornamental Sector—COVID-19 Crisis. Union Fleurs News. 24 March 2020. Available online: https://unionfleurs.org/news_events/statement-situation-of-the-ornamental-sector-covid-19-crisis/ (accessed on 21 February 2022).

- European Commission. Biodiversity Strategy for 2030. EU Commission Strategy. Available online: https://ec.europa.eu/environment/strategy/biodiversity-strategy-2030_en (accessed on 21 February 2022).

- European Commission. 3 Billion Trees Pledge. EU Commission Environment. Available online: https://ec.europa.eu/environment/3-billion-trees_it (accessed on 21 February 2022).

- European Union Assembly of Regional and Local Representatives. Concerted Action Needed to Green the EU’s Communities. European Committee of the Regions Press Release. 27 January 2022. Available online: https://cor.europa.eu/en/news/Pages/concerted-action-needed-green-communities.aspx (accessed on 21 February 2022).

- Baccino, F. Le Affinità (elettive) tra New Green Deal e Florovivaismo. Terra e Vita, 15 September 2021. Available online: https://terraevita.edagricole.it/featured/le-affinita-elettive-tra-new-green-deal-e-florovivaismo/ (accessed on 21 February 2022).

- Centre for the Promotion of Imports from Developing Countries of The Netherlands Ministry of Foreign Affairs (CBI). Through What Channels Can You Get Cut Flowers or Foliage onto the European Market? CBI Ministry of Foreign Affairs Market Information. 9 May 2017. Available online: https://www.cbi.eu/market-information/cut-flowers-foliage/channels-segments (accessed on 3 February 2022).

- Betjes, J.; Vallen, J.; Luca, E.R.; Tufano, G. Con RoyalFloraHolland Verso il Futuro Grandi Opportunita’ di Sviluppo per I Produttori Agricoli. Lecture Presented at the RoyalFloraHolland and Veiling Rhein-Maas Meeting “I Fiori di Roma”, Oasi di Kufra, Sabaudia, Latina, Italy. 25 November 2017. Available online: https://www.royalfloraholland.com/en (accessed on 25 May 2021).

- Byczynski, L.; Benzakein, E. Fresh from the Field Wedding Flowers, 1st ed.; Fairplain Publications Incorporated: Lawrance, KS, USA, 2014; ISBN 0977978133. [Google Scholar]

- Needleman, D. What Happened to Traditional Floral Bouquets? The New York Times Style Magazine. 20 March 2017. Available online: https://www.nytimes.com/2017/03/20/t-magazine/traditional-floral-bouquets.html (accessed on 3 February 2022).

- Prinzing, D. Slow Flowers: Four Seasons of Locally Grown Bouquets from the Garden, Meadow and Farm, 1st ed.; St. Lynn’s Press: Pittsburgh, PA, USA, 2013; ISBN 0983272689. [Google Scholar]

- Centre for the Promotion of Imports from Developing Countries of The Netherlands Ministry of Foreign Affairs (CBI). What Requirements Should Your Cut Flowers and Foliage Comply with to Be Allowed on the European Market? CBI Ministry of Foreing Affairs Market Information. 4 May 2017. Available online: https://www.cbi.eu/market-information/cut-flowers-foliage/buyer-requirements (accessed on 3 February 2022).

- Hall, C.R.; Campbell, B.L.; Behe, B.K.; Yue, C.; Lopez, R.G.; Dennis, J.H. The appeal of biodegradable packaging to floral consumers. HortScience 2010, 45, 583–591. [Google Scholar] [CrossRef]

- Hall, C.R.; Dickson, M.W. Economic, Environmental, and Health/Well-Being Benefits Associated with Green Industry Products and Services: A Review. J. Environ. Hortic. 2011, 29, 96–103. [Google Scholar] [CrossRef]

- European Network for Rural Development (ENRD). Green Economy Opportunities for Rural Europe. EU Rural Review No. 23; Thorpe, E., Ed.; Publications Office of the European Union: Luxembourg, 2017. [Google Scholar]

- Schouten, M. EU Action Plan: Towards Zero Pollution for Air, Water and Soil. European Committee of the Regions, ENVE Commission, Opinion No. CDR 3178/2021, Adopted. 27 January 2022. Available online: https://cor.europa.eu/en/our-work/Pages/OpinionTimeline.aspx?opId=CDR-3178-2021 (accessed on 21 February 2022).

- Ronco, R. La Filiera Florovivaistica nel Veneto. Veneto Agricoltura: Legnaro, Padova, Italy, December 2002. Available online: https://www.venetoagricoltura.org/upload/pubblicazioni/PDF%20Economia/SC36.pdf (accessed on 3 February 2022).

- Lufkin, B. Why Are Flowers so Expensive? BBC Worklife Economics. 8 May 2019. Available online: https://www.bbc.com/worklife/article/20190507-why-are-flowers-so-expensive (accessed on 28 January 2022).

- Joyce, D.C.; Turner, C. Developing a Commercial Floriculture Activity in a Research Environment and a Supply Chain Context. Acta Hortic. 2007, 755, 45–54. [Google Scholar] [CrossRef]

- International Trade Center (ITC) Standards Map App. Available online: https://standardsmap.org/en/identify (accessed on 3 February 2022).

- Stebner, S.; Baker, L.M.; Peterson, H.H.; Boyer, C.R. Marketing with More: An In-depth Look at Relationship Marketing with New Media in the Green Industry. J. Appl. Commun. 2017, 101, 7–18. [Google Scholar] [CrossRef] [Green Version]

- Paniagua, J.; Sapena, J. Business performance and social media: Love or hate? Bus. Horiz. 2014, 57, 719–728. [Google Scholar] [CrossRef]

- Weinberg, B.D.; Pehlivan, E. Social spending: Managing the social media mix. Bus. Horiz. 2011, 54, 275–282. [Google Scholar] [CrossRef]

- Yao, B.; Shanoyan, A.; Peterson, H.H.; Boyer, C.; Baker, L. The use of new-media marketing in the green industry: Analysis of social media use and impact on sales. Agribusiness 2018, 35, 281–297. [Google Scholar] [CrossRef]

- Hall, C.R. How to Market Yourself in a Questionable Economy. The Association of Horticulture Professionals (OFA) Bullettin No. 929 September/October 2011. Available online: https://cdn.coverstand.com/4456/81472/81472.1.pdf (accessed on 2 February 2022).

- Malindretos, G.; Moschuris, S.; Folinas, D. Cut-Flowers Supply Chain and Logistics. The Case of Greece. Int. J. Res. Manag. Bus. Stud. 2015, 2, 15–25. [Google Scholar]

- Allegra, V.; Bellia, C.; Zarbà, A.S. Direct Sales as a Tool for Competitiveness for Smes in the EU. The Case of Farms “Ornamental Floriculture and Nursery Products”. Qual.-Access Success 2014, 15, 19–24. [Google Scholar]

- Serra, G. La Filiera Della Qualità nel Florovivaismo: Qualità-Valore-Servizio-Convenienza-Scelta. Lecture Presented at the Conference “La Qualità Totale nel Florovivaismo”. Baveno (Verbano-Cusio-Ossola), Italy. 2009; To be submitted. [Google Scholar]

- European Commission. Proposal for a Regulation of the European Parliament and of the Council COM(2018) 392 Final 2018/0216 (COD); European Commission: Brussels, Belgium, 1 June 2018; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM%3A2018%3A392%3AFIN (accessed on 21 February 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Definers | Key Terms |

|---|---|

| Market and Industry | Floriculture Flower industry Ornamental industry Nursery industry Flower market Ornamental plants market |

| Product Category | Flowers and ornamental plants Ornamentals Cut flowers and pot(ted) plants Cut flowers and indoor plants |

| Supply Chain Structure and Characterization | Supply chain structure and dynamics Production Trade Consumption Consumption patterns Sales and spending |

| Geographical Area | World/Global Europe European Union (EU), i.e., EU (28)/EU (27) + United Kingdom (UK) |

| Name of the Institution | Country | Official Websites 1 |

|---|---|---|

| International Association of Horticultural Producers (AIPH) | Belgium | http://aiph.org/ |

| International Flower Trade Association (Union Fleurs) | Belgium | https://unionfleurs.org/ |

| Messe Essen GmbH Press Media Centre for IPM Essen | Germany | https://www.ipm-essen.de/world-trade-fair/ |

| Royal Flora Holland (RFH) | The Netherlands | https://www.royalfloraholland.com/en |

| Association of the German Flower Wholesale and Import Trade (BGI) | Germany | https://bgi-ev.de/en/the-association/ |

| RaboResearch Food and AgriBusiness (Rabobank) | The Netherlands | https://research.rabobank.com/far/en/home/index.html |

| European Commission Directorate-General for Agriculture and Rural Development (DG AGRI) Unit G2-Wine, spirits, and horticultural products | Belgium | https://ec.europa.eu/info/food-farming-fisheries/plants-and-plant-products/live-plants-and-flowers_en |

| International Trade Centre (ITC)—Trade Map | n/a | https://www.trademap.org/Index.aspx |

| Centre for the Promotion of Imports from developing countries of the Netherlands Ministry of Foreign Affairs (CBI) | The Netherlands | https://www.cbi.eu/ |

| Assembly of European Regions producing Fruits, Vegetables and Ornamental Plants (AREFLH) | France | https://www.areflh.org/en/ |

| Inclusion Criteria | Description of the Included Grey Literature |

|---|---|

| Relevance and reliability |

|

| Document typology and accessibility |

|

| Year of publication |

|

| Scope |

|

| Language |

|

| Country Group | Included Country/Area 1 | Market Determinants | Characteristics of Demand and Supply | |

|---|---|---|---|---|

| Mature domestic producer countries | Europe Canada United States (US) China Japan |

| High-value domestic demand |

|

| Strong domestic production base |

| |||

| Emerging domestic producer countries | India Mexico Brazil |

| High-growth domestic demand |

|

| Expanding domestic production base |

| |||

| Mature exporting producer countries | Colombia Kenya Ecuador |

| Low-growth domestic demand |

|

| Strong domestic production base |

| |||

| Emerging exporting producer countries | Ethiopia Vietnam | Low-growth domestic demand |

| |

| Expanding domestic production base |

| |||

| Determinant | Drivers for Change of Consumption Trends |

|---|---|

| Globalization |

|

| Climate change |

|

| Urbanization and new city living |

|

| Evolution of the socio-demographic context |

|

| Neo-luxury and sustainability-oriented consumption patterns |

|

| Evolution and spreading of the Internet and ICT |

|

| COVID-19 Pandemic |

|

| Classification Criterion | Description of Consumer Profile | |||

|---|---|---|---|---|

| Cultivated Performers | Cosiness Seekers | Individualistic Performers | ||

| Psychographic |

|

|

| |

| Behavioral |

|

|

| |

| Market share | TOT | |||

| % total consumers | 14.6 | 8.5 | 14.7 | 37.7 |

| % total turnover | 38.2 | 15 | 15.5 | 68.7 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gabellini, S.; Scaramuzzi, S. Evolving Consumption Trends, Marketing Strategies, and Governance Settings in Ornamental Horticulture: A Grey Literature Review. Horticulturae 2022, 8, 234. https://doi.org/10.3390/horticulturae8030234

Gabellini S, Scaramuzzi S. Evolving Consumption Trends, Marketing Strategies, and Governance Settings in Ornamental Horticulture: A Grey Literature Review. Horticulturae. 2022; 8(3):234. https://doi.org/10.3390/horticulturae8030234

Chicago/Turabian StyleGabellini, Sara, and Silvia Scaramuzzi. 2022. "Evolving Consumption Trends, Marketing Strategies, and Governance Settings in Ornamental Horticulture: A Grey Literature Review" Horticulturae 8, no. 3: 234. https://doi.org/10.3390/horticulturae8030234

APA StyleGabellini, S., & Scaramuzzi, S. (2022). Evolving Consumption Trends, Marketing Strategies, and Governance Settings in Ornamental Horticulture: A Grey Literature Review. Horticulturae, 8(3), 234. https://doi.org/10.3390/horticulturae8030234