Stock Index Return Volatility Forecast via Excitatory and Inhibitory Neuronal Synapse Unit with Modified MF-ADCCA

Abstract

:1. Introduction

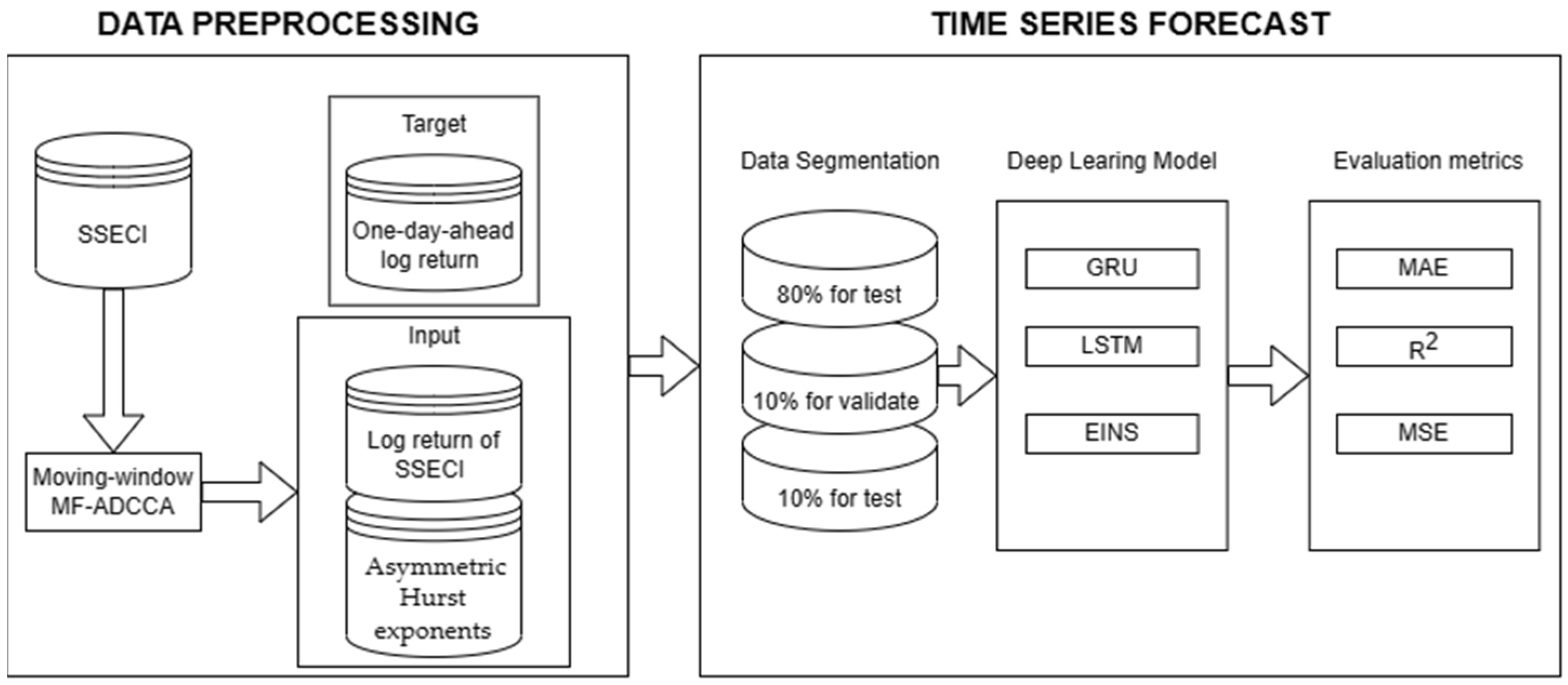

2. Materials and Methods

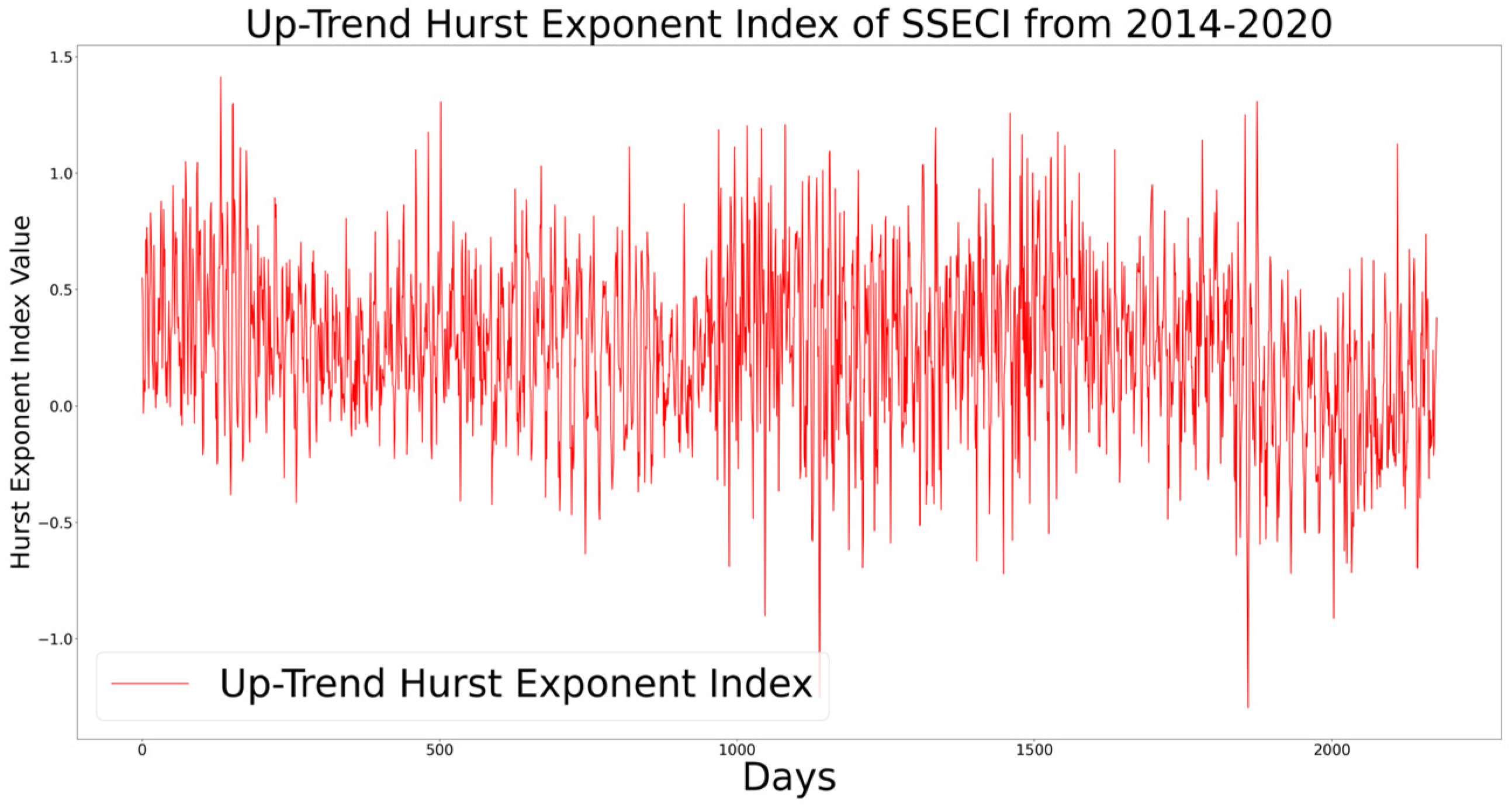

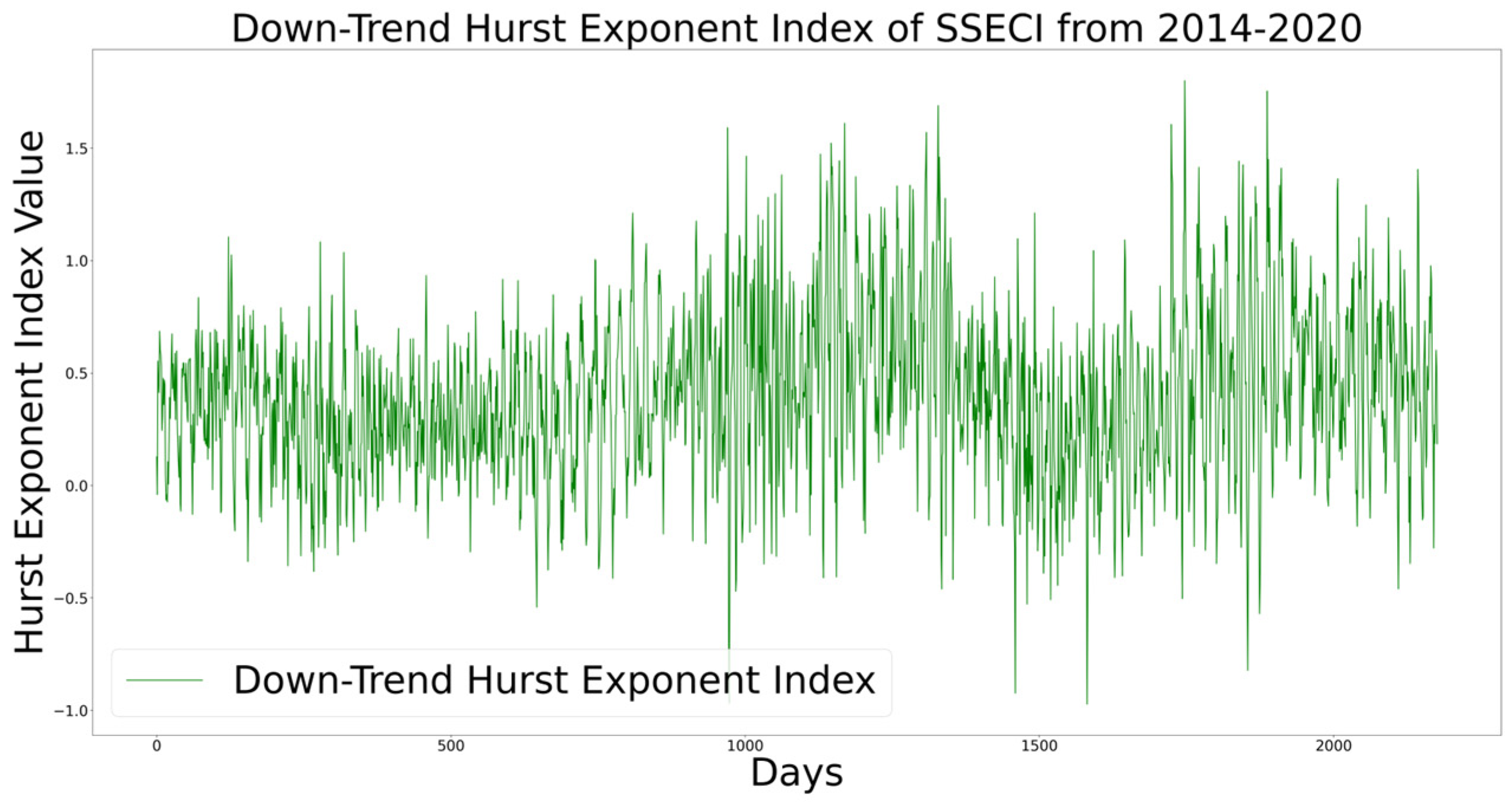

2.1. Multifractal Asymmetric Detrended Cross-Correlation Analysis (MF-ADCCA)

| Algorithm 1. Algorithm to Moving-window MF-ADCCA Method. | ||

| Input: Time Series: ; | < Size () > | |

| Time Series: ; | < Size () > | |

| Days Scaling: ; | ||

| Step: ; | ||

| Output: Asymmetric generalized Hurst exponents; | ||

| Function Moving-window MF-ADCCA () | ||

| Initialize rray[0,…]rray[0,…], rray[0,…] | ||

| for in range (0, , step) do | ||

| | ||

| return | ||

| End function | ||

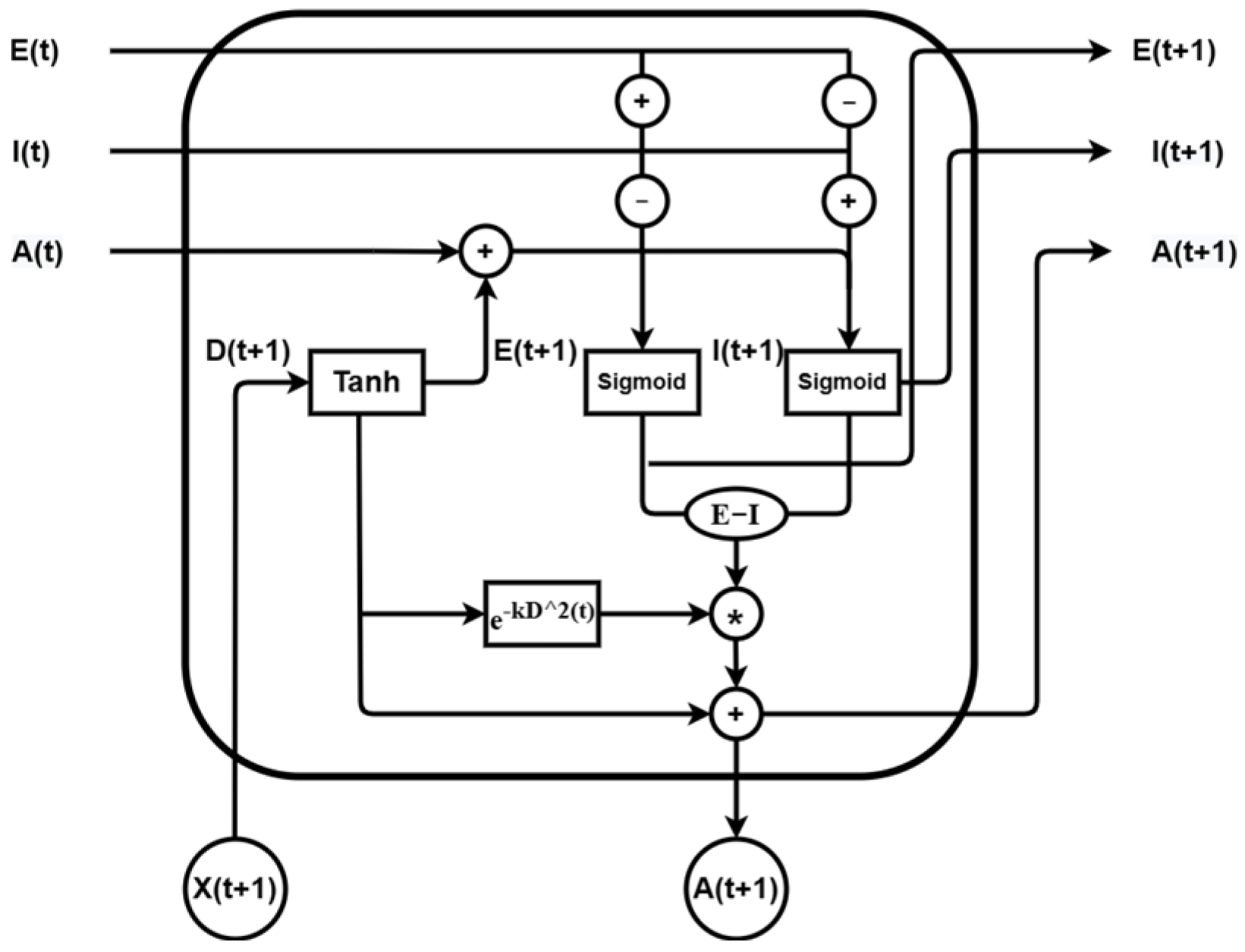

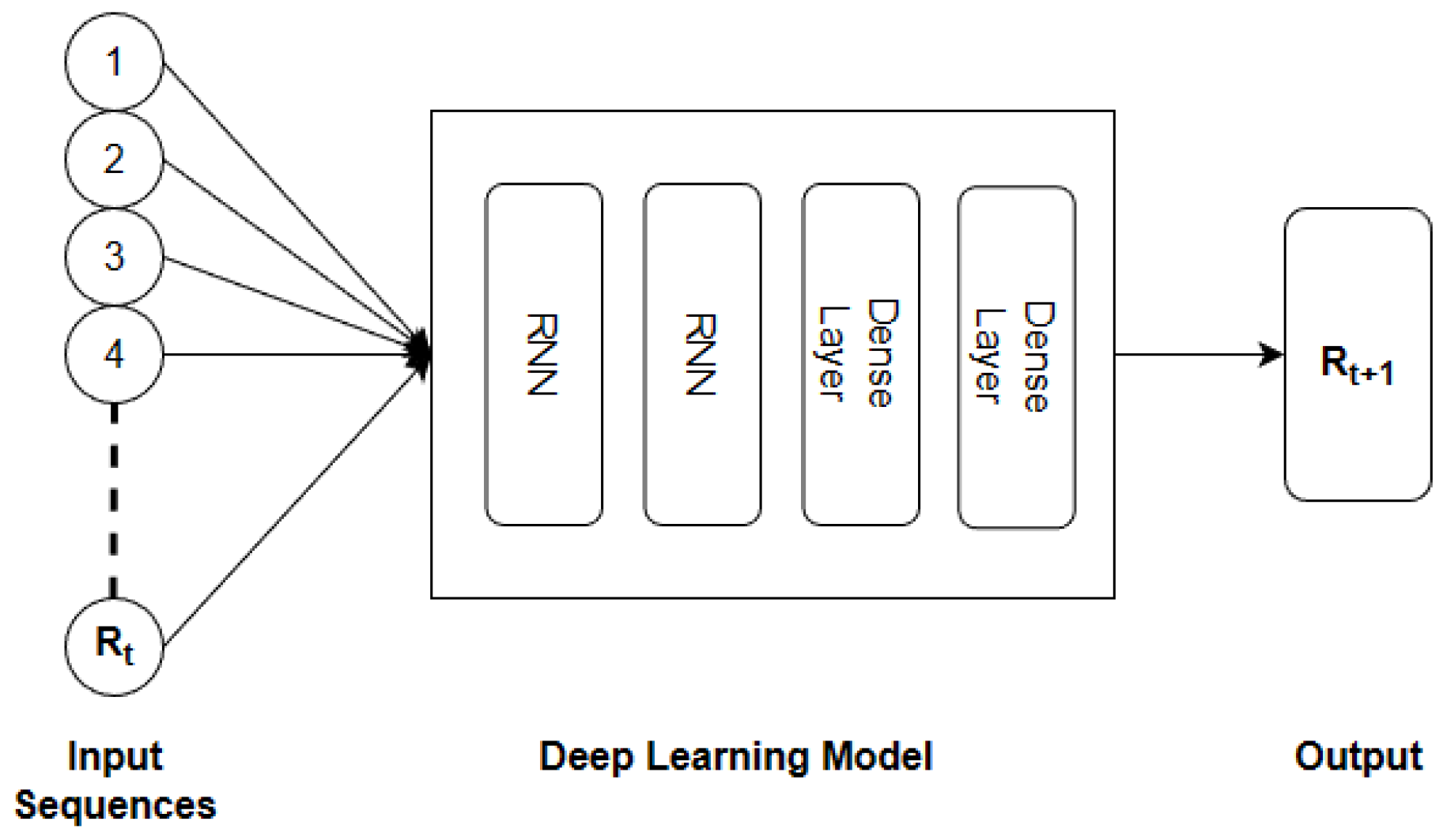

2.2. Excitatory and Inhibitory Neuronal Synapse Unit (EINS)

| Algorithm 2. Algorithm to Excitatory and Inhibitory Neural Synapse Model. | ||

| Input: Time Series: ; | < Size () > | |

| Input Size: ; Hidden Size: ; Output Size: ; | ||

| Step: ; | ||

| Output: Prediction Result: ; | ||

| Procedure EINS () | ||

| Initialize 0; ; ; ; ; . | ||

| for in do | ||

| | ||

| return | ||

| End for | ||

| While do | ||

| Update by running training algorithm for steps | ||

| if then | ||

| else | ||

| End if | ||

| End while | ||

| return and save the trained EINS model weights | ||

| End Procedure | ||

3. Data and Experiments

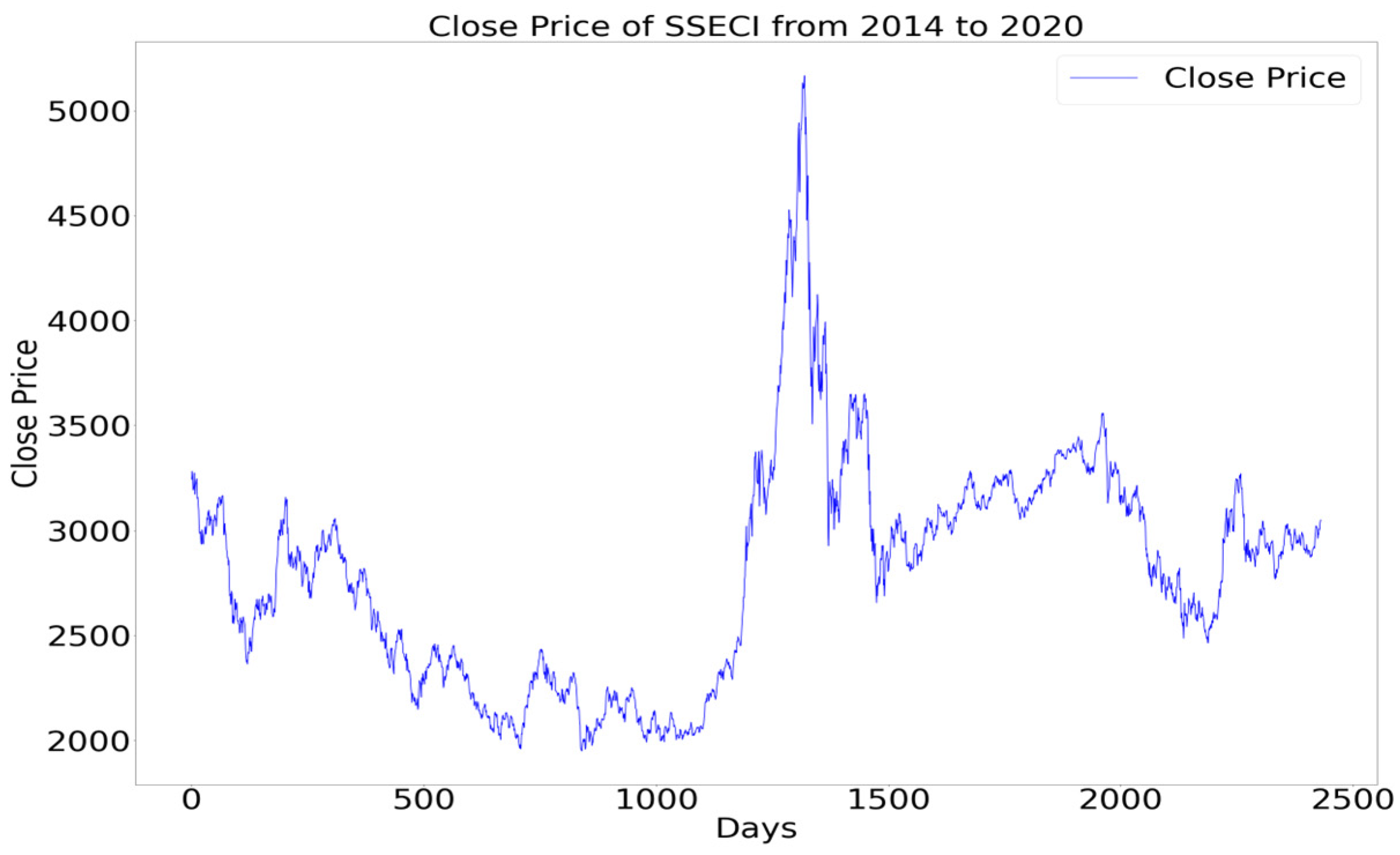

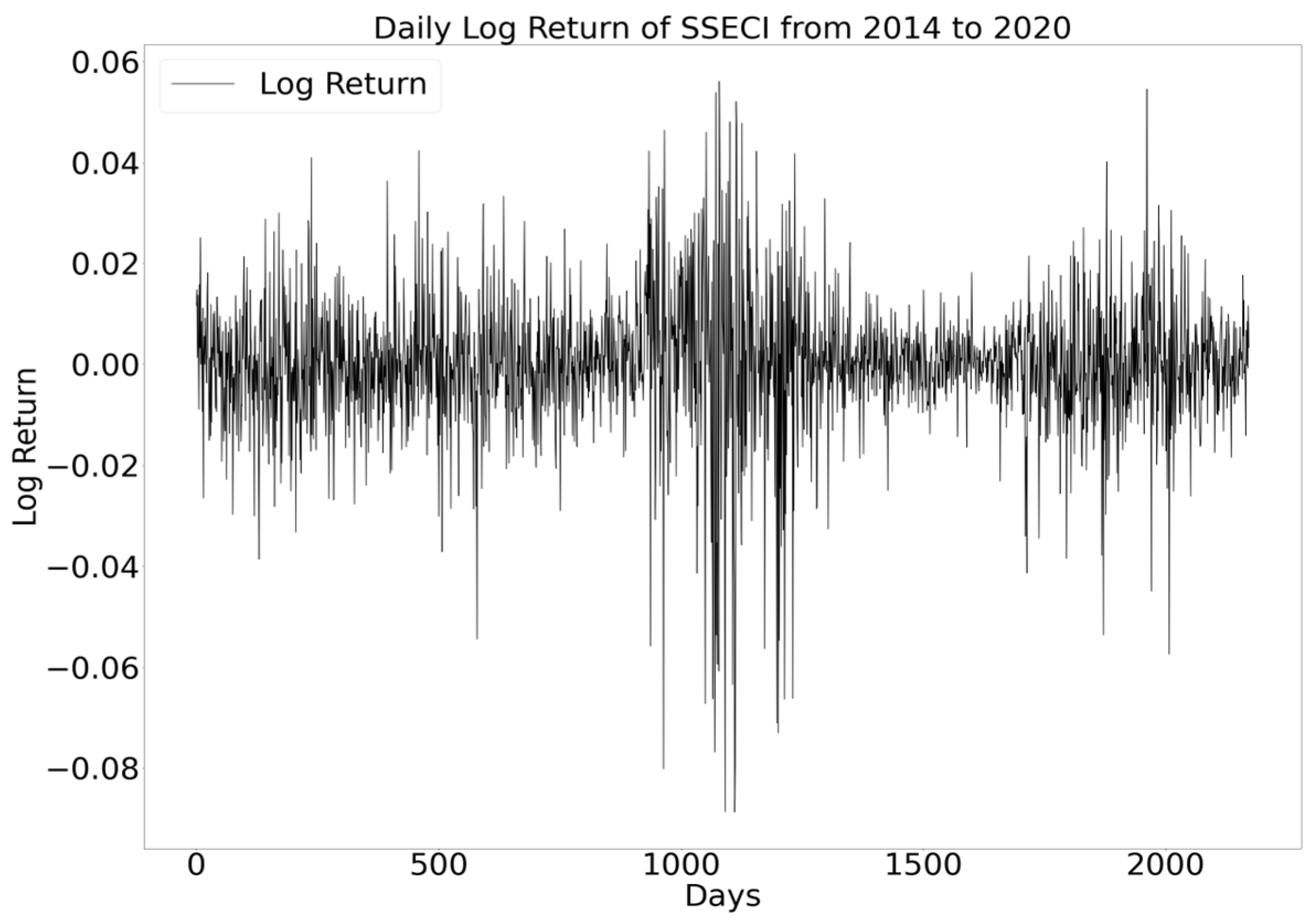

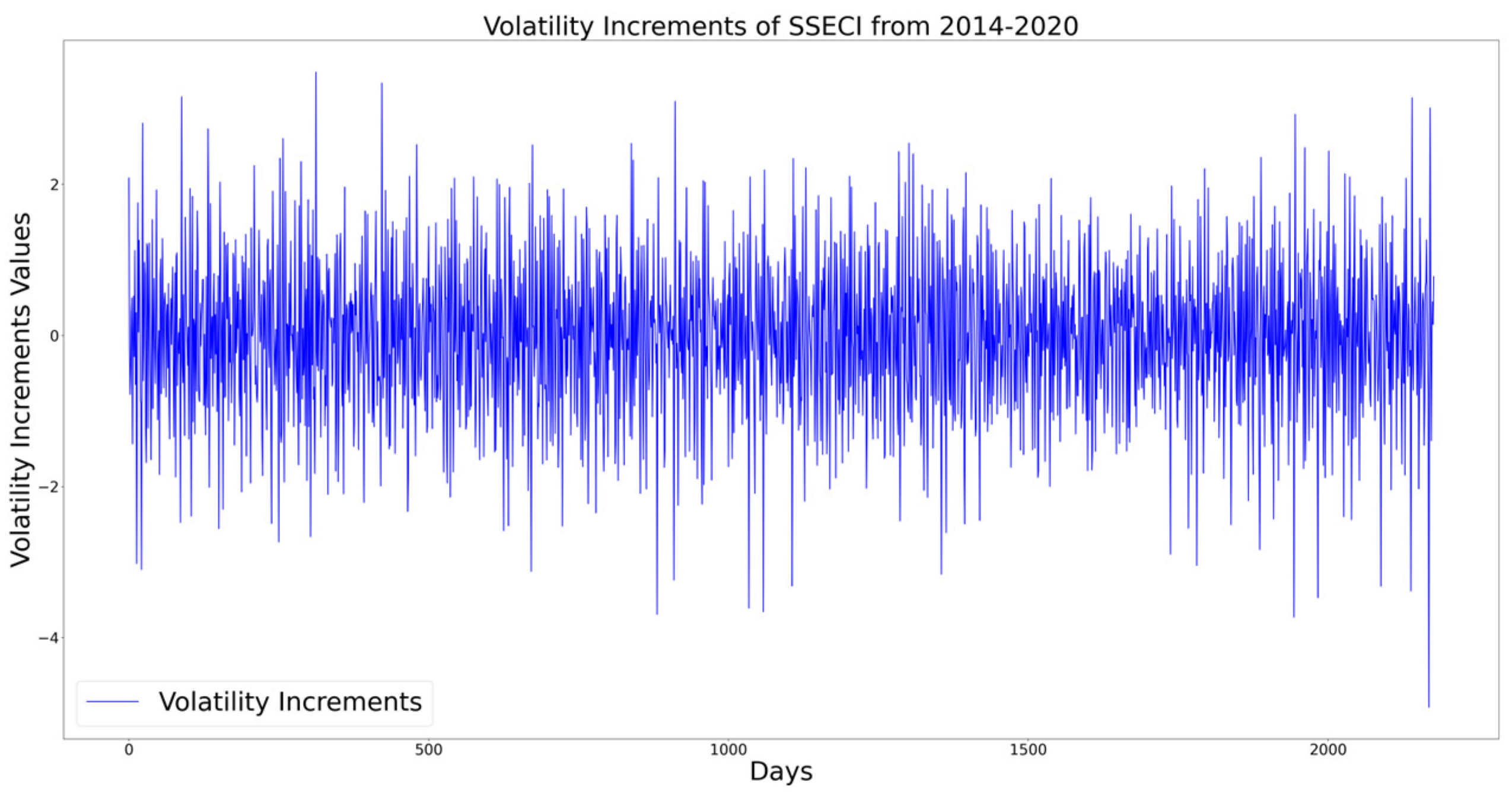

3.1. Data Description

3.2. Experiments

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Zhang, L.; Wang, F.; Xu, B.; Chi, W.; Wang, Q.; Sun, T. Prediction of stock prices based on LM-BP neural network and the estimation of overfitting point by RDCI. Neural Comput. Appl. 2018, 30, 1425–1444. [Google Scholar] [CrossRef]

- Liu, G.; Yu, C.P.; Shiu, S.N.; Shih, I.T. The Efficient Market Hypothesis and the Fractal Market Hypothesis: Interfluves, Fusions, and Evolutions. Sage Open 2022, 12, 21582440221082137. [Google Scholar] [CrossRef]

- Arashi, M.; Rounaghi, M.M. Analysis of market efficiency and fractal feature of NASDAQ stock exchange: Time series modeling and forecasting of stock index using ARMA-GARCH model. Futur. Bus. J. 2022, 8, 14. [Google Scholar] [CrossRef]

- Hurst, H.E. Long-term storage capacity of reservoirs. Trans. Am. Soc. Civ. Eng. 1951, 116, 770–799. [Google Scholar] [CrossRef]

- Peters, E.E. Fractal Market Analysis: Applying Chaos Theory to Investment and Economics; John Wiley & Sons: Hoboken, NJ, USA, 1994; Volume 24. [Google Scholar]

- Kantelhardt, J.W.; Zschiegner, S.A.; Koscielny-Bunde, E.; Havlin, S.; Bunde, A.; Stanley, H. Multifractal detrended fluctuation analysis of nonstationary time series. Phys. A Stat. Mech. Its Appl. 2002, 316, 87–114. [Google Scholar] [CrossRef] [Green Version]

- Zhou, W.-X. Multifractal detrended cross-correlation analysis for two nonstationary signals. Phys. Rev. E 2008, 77, 066211. [Google Scholar] [CrossRef] [Green Version]

- Podobnik, B.; Stanley, H.E. Detrended Cross-Correlation Analysis: A New Method for Analyzing Two Nonstationary Time Series. Phys. Rev. Lett. 2008, 100, 084102. [Google Scholar] [CrossRef] [Green Version]

- Cao, G.; Zhang, M.; Li, Q. Volatility-constrained multifractal detrended cross-correlation analysis: Cross-correlation among Mainland China, US, and Hong Kong stock markets. Phys. A Stat. Mech. Its Appl. 2017, 472, 67–76. [Google Scholar] [CrossRef]

- Yuan, X.; Sun, Y.; Lu, X. SHIBOR Fluctuations and Stock Market Liquidity: An MF-DCCA Approach. Emerg. Mark. Financ. Trade 2022, 58, 2050–2065. [Google Scholar] [CrossRef]

- Cao, G.; Cao, J.; Xu, L.; He, L. Detrended cross-correlation analysis approach for assessing asymmetric multifractal detrended cross-correlations and their application to the Chinese financial market. Phys. A Stat. Mech. Its Appl. 2014, 393, 460–469. [Google Scholar] [CrossRef]

- Alvarez-Ramirez, J.; Rodriguez, E.; Echeverria, J.C. A DFA approach for assessing asymmetric correlations. Phys. A Stat. Mech. Its Appl. 2009, 388, 2263–2270. [Google Scholar] [CrossRef]

- Liu, C.; Zheng, Y.; Zhao, Q.; Wang, C. Financial stability and real estate price fluctuation in China. Phys. A Stat. Mech. Its Appl. 2020, 540, 122980. [Google Scholar] [CrossRef]

- Kakinaka, S.; Umeno, K. Exploring asymmetric multifractal cross-correlations of price-volatility and asymmetric volatility dynamics in cryptocurrency markets. Phys. A Stat. Mech. its Appl. 2021, 581, 126237. [Google Scholar] [CrossRef]

- Guo, Y.; Yu, Z.; Yu, C.; Cheng, H.; Chen, W.; Zhang, H. Asymmetric multifractal features of the price–volume correlation in China’s gold futures market based on MF-ADCCA. Res. Int. Bus. Financ. 2021, 58, 101495. [Google Scholar] [CrossRef]

- Yuan, Y.; Zhang, T. Forecasting stock market in high and low volatility periods: A modified multifractal volatility approach. Chaos Solitons Fractals 2020, 140, 110252. [Google Scholar] [CrossRef]

- Hu, H.; Zhao, C.; Li, J.; Huang, Y. Stock Prediction Model Based on Mixed Fractional Brownian Motion and Improved Fractional-Order Particle Swarm Optimization Algorithm. Fractal Fract. 2022, 6, 560. [Google Scholar] [CrossRef]

- Cao, G.; Han, Y.; Li, Q.; Xu, W. Asymmetric MF-DCCA method based on risk conduction and its application in the Chinese and foreign stock markets. Phys. A Stat. Mech. Its Appl. 2017, 468, 119–130. [Google Scholar] [CrossRef]

- Jaiswal, R.; Jha, G.K.; Kumar, R.R.; Choudhary, K. Deep long short-term memory based model for agricultural price forecasting. Neural Comput. Appl. 2022, 34, 4661–4676. [Google Scholar] [CrossRef]

- Lee, M.-C.; Chang, J.-W.; Yeh, S.-C.; Chia, T.-L.; Liao, J.-S.; Chen, X.-M. Applying attention-based BiLSTM and technical indicators in the design and performance analysis of stock trading strategies. Neural Comput. Appl. 2022, 34, 13267–13279. [Google Scholar] [CrossRef] [PubMed]

- Chandar, S.; Sankar, C.; Vorontsov, E.; Kahou, S.E.; Bengio, Y. Towards non-saturating recurrent units for modelling long-term dependencies. Proc. AAAI Conf. Artif. Intell. 2019, 33, 3280–3287. [Google Scholar] [CrossRef] [Green Version]

- Cho, P.; Lee, M. Forecasting the Volatility of the Stock Index with Deep Learning Using Asymmetric Hurst Exponents. Fractal Fract. 2022, 6, 394. [Google Scholar] [CrossRef]

- Hochreiter, S.; Schmidhuber, J. Long short-term memory. Neural Comput. 1997, 9, 1735–1780. [Google Scholar] [CrossRef] [PubMed]

- Chung, J.; Gulcehre, C.; Cho, K.; Bengio, Y. Empirical evaluation of gated recurrent neural networks on sequence modeling. arXiv 2014, arXiv:1412.3555. [Google Scholar]

- Cifelli, P.; Ruffolo, G.; De Felice, E.; Alfano, V.; van Vliet, E.A.; Aronica, E.; Palma, E. Phytocannabinoids in Neurological Diseases: Could They Restore a Physiological GABAergic Transmission? Int. J. Mol. Sci. 2020, 21, 723. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Xu, Y.; Jia, Y.; Ma, J.; Alsaedi, A.; Ahmad, B. Synchronization between neurons coupled by memristor. Chaos Solitons Fractals 2017, 104, 435–442. [Google Scholar] [CrossRef]

- Zhang, J.; Liao, X. Synchronization and chaos in coupled memristor-based FitzHugh-Nagumo circuits with memristor synapse. Aeu-Int. J. Electron. Commun. 2017, 75, 82–90. [Google Scholar] [CrossRef]

- Lee, R.S.T. Chaotic Type-2 Transient-Fuzzy Deep Neuro-Oscillatory Network (CT2TFDNN) for Worldwide Financial Prediction. IEEE Trans. Fuzzy Syst. 2019, 28, 731–745. [Google Scholar] [CrossRef]

- Njitacke, Z.T.; Doubla, I.S.; Kengne, J.; Cheukem, A. Coexistence of firing patterns and its control in two neurons coupled through an asymmetric electrical synapse. Chaos: Interdiscip. J. Nonlinear Sci. 2020, 30, 023101. [Google Scholar] [CrossRef]

- Lee, R.S.T. Chaotic interval type-2 fuzzy neuro-oscillatory network (CIT2-FNON) for Worldwide 129 financial products prediction. Int. J. Fuzzy Syst. 2019, 21, 2223–2244. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E.; Shephard, N. Power and bipower variation with stochastic volatility and jumps. J. Financ. Econom. 2004, 2, 1–37. [Google Scholar] [CrossRef] [Green Version]

- Dickey, D.A.; Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar]

- Kwiatkowski, D.; Phillips, P.C.B.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J. Econom. 1992, 54, 159–178. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Max | Min | Std | Skew | Kurt | J-Bera 1 | ADF 2 | KPSS 3 | |

|---|---|---|---|---|---|---|---|---|---|

| −0.953 | 6.695 | 4372.8 * | −9.148 * | * | |||||

| 3.7987 | −3.7436 | 0.8384 | 1.0185 | 93.18 * | −15.769 * | * |

| Hyper-Parameters | Settings |

|---|---|

| Hidden neurons | 128,256 |

| Time Horizons | 32,128 |

| Learning rate | |

| Dropout rate | 0.2 |

| Epochs | 100 |

| Optimizer | Adam |

| Error function | Mean squared error |

| Multifractal | Model | MSE | MAE | |

|---|---|---|---|---|

| MF-DFA | EINS | 0.02584 | 0.11069 | −0.01746 |

| LSTM | 0.02704 | 0.11351 | −0.06485 | |

| GRU | 0.02769 | 0.11494 | −0.09042 | |

| MF-ADCCA | EINS | 0.02549 | 0.10999 | −0.00398 |

| LSTM | 0.02577 | 0.11091 | −0.01469 | |

| GRU | 0.02580 | 0.11130 | −0.01605 | |

| MF-DFA | EINS | 0.02324 | 0.10689 | −0.00691 |

| LSTM | 0.02337 | 0.10810 | −0.01262 | |

| GRU | 0.02354 | 0.10885 | −0.02011 | |

| MF-ADCCA | EINS | 0.02372 | 0.10770 | −0.02798 |

| LSTM | 0.02507 | 0.11252 | −0.08636 | |

| GRU | 0.02496 | 0.11118 | −0.08178 | |

| MF-DFA | EINS | 0.02582 | 0.11069 | −0.01666 |

| LSTM | 0.02727 | 0.11501 | −0.07390 | |

| GRU | 0.02699 | 0.11419 | −0.06298 | |

| MF-ADCCA | EINS | 0.02532 | 0.11003 | 0.00296 |

| LSTM | 0.02704 | 0.11489 | −0.06500 | |

| GRU | 0.02593 | 0.11145 | −0.02102 | |

| MF-DFA | EINS | 0.02366 | 0.10756 | −0.02516 |

| LSTM | 0.02467 | 0.11103 | −0.06923 | |

| GRU | 0.02774 | 0.11885 | −0.20226 | |

| MF-ADCCA | EINS | 0.02335 | 0.10705 | −0.01197 |

| LSTM | 0.02419 | 0.10989 | −0.04810 | |

| GRU | 0.02418 | 0.11025 | −0.04761 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, L.; Lee, R.S.T. Stock Index Return Volatility Forecast via Excitatory and Inhibitory Neuronal Synapse Unit with Modified MF-ADCCA. Fractal Fract. 2023, 7, 292. https://doi.org/10.3390/fractalfract7040292

Wang L, Lee RST. Stock Index Return Volatility Forecast via Excitatory and Inhibitory Neuronal Synapse Unit with Modified MF-ADCCA. Fractal and Fractional. 2023; 7(4):292. https://doi.org/10.3390/fractalfract7040292

Chicago/Turabian StyleWang, Luochao, and Raymond S. T. Lee. 2023. "Stock Index Return Volatility Forecast via Excitatory and Inhibitory Neuronal Synapse Unit with Modified MF-ADCCA" Fractal and Fractional 7, no. 4: 292. https://doi.org/10.3390/fractalfract7040292

APA StyleWang, L., & Lee, R. S. T. (2023). Stock Index Return Volatility Forecast via Excitatory and Inhibitory Neuronal Synapse Unit with Modified MF-ADCCA. Fractal and Fractional, 7(4), 292. https://doi.org/10.3390/fractalfract7040292