Provoking Actual Mobile Payment Use in the Middle East

Abstract

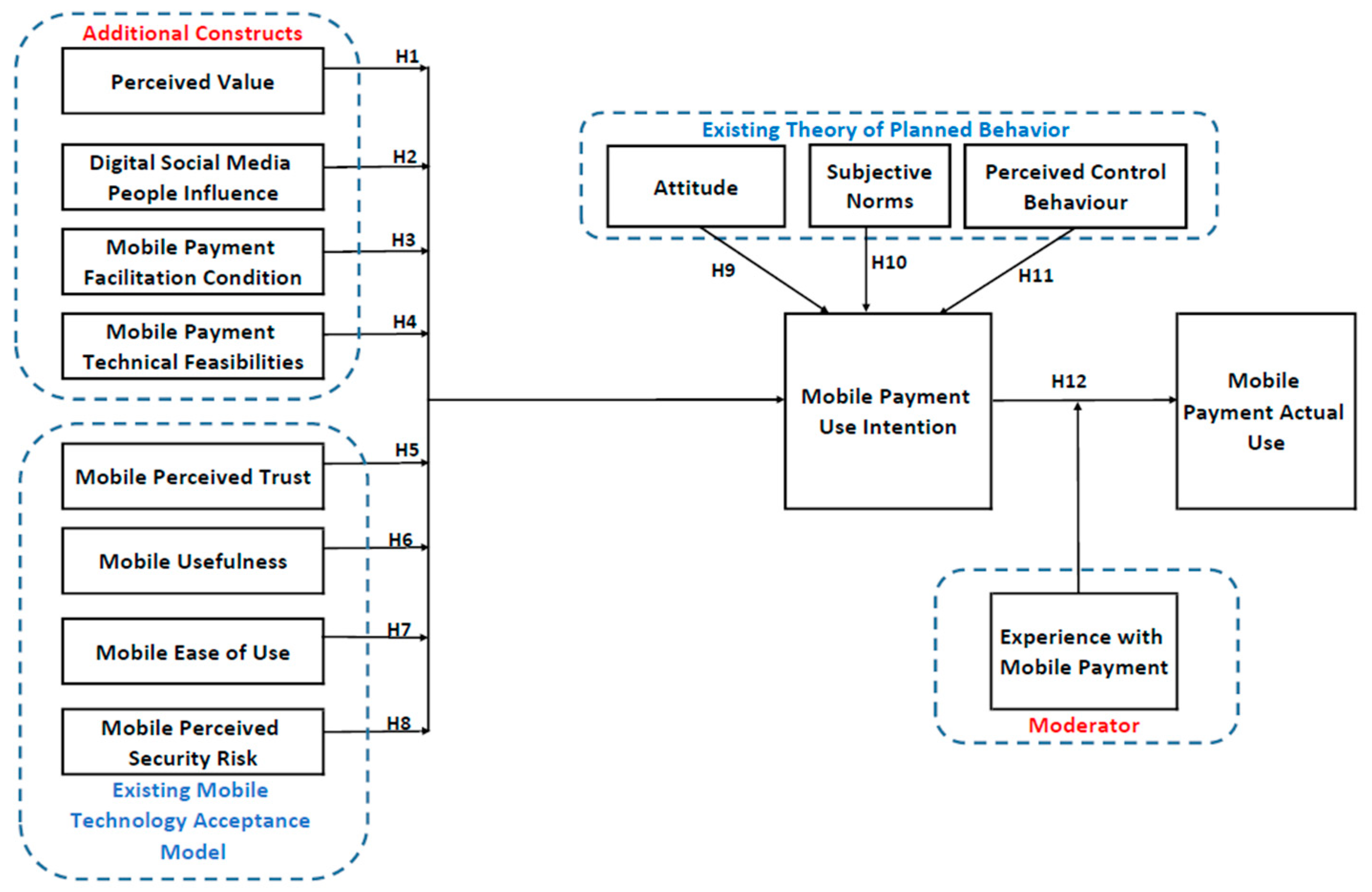

:1. Introduction

2. Literature Review

2.1. Mobile Payment

2.2. Why Do People Accept or Resist Adopting Mobile Payments?

2.3. Theoretical Framework

2.3.1. Mobile Technology Acceptance Model (MTAM)

2.3.2. The Theory of Planned Behaviour

2.4. Hypothesis Development

3. Research Methodology

3.1. Pre-Test

3.2. Data Collection and Respondent’s Demographic Profile

3.3. Outer Measurement Model Assessment

4. Finding and Discussion

5. Significance of the Study

5.1. Theoretical Contribution

5.2. Managerial Contribution

5.3. Methodological Contribution

5.4. Social Contribution

6. Conclusions and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Merhi, M.; Hone, K.; Tarhini, A.; Ameen, N. An empirical examination of the moderating role of age and gender in consumer mobile banking use: A cross-national, quantitative study. J. Enterp. Inf. Manag. 2020, 34, 1144–1168. [Google Scholar] [CrossRef]

- How Behavioural Science Can Unleash Digital Payments Adoption. Available online: https://www.simon-kucher.com/sites/default/files/2018-12/SimonKucher_Report_Payment%20Adoption_Final_0.pdf (accessed on 1 February 2022).

- Flavian, C.; Guinaliu, M.; Lu, Y. Mobile payments adoption—Introducing mindfulness to better understand consumer behaviour. Int. J. Bank Mark. 2020, 38, 1575–1599. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; García-Maroto, I.; Muñoz-Leiva, F.; Ramos-de-Luna, I. Mobile Payment Adoption in the Age of Digital Transformation: The Case of Apple Pay. Sustainability 2020, 12, 5443. [Google Scholar] [CrossRef]

- Kang, J. Mobile payment in Fintech environment: Trends, security challenges, and services. Hum. -Cent. Comput. Inf. Sci. 2018, 8, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Mouakket, S. Investigating the role of mobile payment quality characteristics in the United Arab Emirates: Implications for emerging economies. Int. J. Bank Mark. 2020, 38, 1465–1490. [Google Scholar] [CrossRef]

- Odoom, R.; Kosiba, J.P. Mobile money usage and continuance intention among micro-enterprises in an emerging market—The mediating role of agent credibility. J. Syst. Inf. Technol. 2020, 22, 97–117. [Google Scholar] [CrossRef]

- Kumar, V.; Lai, K.K.; Chang, Y.H.; Bhatt, P.C.; Su, F.P. A structural analysis approach to identify technology innovation and evolution path: A case of the m-payment technology ecosystem. J. Knowl. Manag. 2020, 34, 1144–1168. [Google Scholar] [CrossRef]

- Dimitriadis, S.; Kyrezis, N.; Chalaris, M. A comparison of two multivariate analysis methods for segmenting users of alternative payment means. Int. J. Bank Mark. 2018, 36, 322–335. [Google Scholar] [CrossRef]

- Kothari, S. 5 Reasons Why Consumers Still Don’t Use Digital Payments. Available online: https://economictimes.indiatimes.com/wealth/spend/5-reasons-why-consumers-still-dont-use-digital-payments/articleshow/64699938.cms?from=mdr (accessed on 26 November 2020).

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319–339. [Google Scholar] [CrossRef] [Green Version]

- Oertzen, A.-S.; Odekerken-Schröder, G. Achieving continued usage in online banking: A post-adoption study. Int. J. Bank Mark. 2019, 37, 1394–1418. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Y.; Miao, M.; Jalees, T.; Zaman, S.I. Analysis of the moral mechanism to purchase counterfeit luxury goods: Evidence from China. Asia Pac. J. Mark. Logist. 2019, 31, 647–669. [Google Scholar] [CrossRef]

- Ooi, K.-B.; Tan, G.W.-H. Mobile technology acceptance model: An investigation using mobile users to explore smartphone credit cards. Expert Syst. Appl. 2016, 59, 33–46. [Google Scholar] [CrossRef]

- Verma, S.; Chaurasia, S.S.; Bhattacharyya, S.S. The effect of government regulations on continuance intention of in-store proximity mobile payment services. Int. J. Bank Mark. 2020, 38, 34–62. [Google Scholar] [CrossRef]

- Khoi, N.H.; Tuu, H.H.; Olsen, S.O. The role of perceived values in explaining Vietnamese consumers’ attitude and intention to adopt mobile commerce. Asia Pac. J. Mark. Logist. 2018, 30, 1112–1134. [Google Scholar] [CrossRef] [Green Version]

- Ryu, H.-S. What makes users willing or hesitant to use Fintech?: The moderating effect of user type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Feng, Y.; Chen, X.; Lai, I. The effects of tourist experiential quality on perceived value and satisfaction with bed and breakfast stay in southwestern China. J. Hosp. Tour. Insights 2020, 25, 477–499. [Google Scholar] [CrossRef]

- Lin, K.-Y.; Wang, Y.-T.; Huang, T.K. Exploring the antecedents of mobile payment service usage: Perspectives based on cost-benefit theory, perceived value, and social influences. Online Inf. Rev. 2020, 44, 299–318. [Google Scholar] [CrossRef]

- Hew, J.-J.; Lee, V.-H.; Ooi, K.-B.; Lin, B. Mobile social commerce: The booster for brand loyalty? Comput. Hum. Behav. 2016, 59, 142–154. [Google Scholar] [CrossRef]

- Trinh, H.N.; Tran, H.H.; Vuong, D.H.Q. Determinants of consumers’ intention to use a credit card: A perspective of multifaceted perceived risk. Asian J. Econ. Bank. 2020, 4, 105–120. [Google Scholar] [CrossRef]

- Patten, E.; Ozuem, W.; Howell, K. Service quality in multichannel fashion retailing: An exploratory study. Inf. Technol. People 2020, 33, 1327–1356. [Google Scholar] [CrossRef]

- Islam, M.S.; Karia, N.; Khaleel, M.; Fauzi, F.B.A.; Soliman, M.S.M.; Khalid, J.; Bhuiyan, M.Y.A.; Mamun, M.A.A. Intention to adopt mobile banking in Bangladesh: An empirical study of emerging economy. Int. J. Bus. Inf. Syst. 2019, 31, 136–151. [Google Scholar] [CrossRef]

- Gupta, K.P.; Manrai, R.; Goel, U. Factors influencing adoption of payments banks by Indian customers: Extending UTAUT with perceived credibility. J. Asia Bus. Stud. 2019, 13, 173–195. [Google Scholar] [CrossRef]

- Leong, C.-M.; Tan, K.-L.; Puah, C.-H.; Chong, S.-M. Predicting mobile network operators users m-payment intention. Eur. Bus. Rev. 2021, 33, 104–126. [Google Scholar] [CrossRef]

- Danyali, A.A. Factors influencing customers’ change of behaviours from online banking to mobile banking in Tejarat Bank, Iran. J. Organ. Chang. Manag. 2018, 31, 1226–1233. [Google Scholar] [CrossRef]

- Cao, X.; Yu, L.; Liu, Z.; Gong, M.; Adeel, L. Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Res. 2018, 28, 456–476. [Google Scholar] [CrossRef]

- Chaouali, W.; Hedhli, K.E. Toward a contagion-based model of mobile banking adoption. Int. J. Bank Mark. 2019, 37, 69–96. [Google Scholar] [CrossRef] [Green Version]

- Mostafa, R.B. Mobile banking service quality: A new avenue for customer value co-creation. Int. J. Bank Mark. 2020, 38, 1107–1132. [Google Scholar] [CrossRef]

- Mazambani, L.; Mutambara, E. Predicting FinTech innovation adoption in South Africa: The case of cryptocurrency. Afr. J. Econ. Manag. Stud. 2019, 11, 30–50. [Google Scholar] [CrossRef]

- Harb, A.A.; Fowler, D.; Chang, H.J.J.; Blum, S.C.; Alakaleek, W. Social media as a marketing tool for events. J. Hosp. Tour. Technol. 2019, 10, 28–44. [Google Scholar] [CrossRef]

- Farah, M.F.; Hasni, M.J.S.; Abbas, A.K. Mobile-banking adoption: Empirical evidence from the banking sector in Pakistan. Int. J. Bank Mark. 2018, 36, 1386–1413. [Google Scholar] [CrossRef]

- Vashistha, A.; Anderson, R.; Mare, S. Examining the Use and Non-Use of Mobile Payment Systems for Merchant Payments in India. In Proceedings of the 2nd ACM SIGCAS Conference on Computing and Sustainable Societies, Accra, Ghana, 3 July 2019; pp. 1–12. [Google Scholar]

- JosephNg, P.S.; Eaw, H.C. Making Financial Sense from EaaS for MSE during Economic Uncertainty. In Advances in Information and Communication. FICC 2021. Advances in Intelligent Systems and Computing; Arai, K., Ed.; Springer: Cham, Switzerland, 2021; Volume 1363, pp. 976–989. [Google Scholar] [CrossRef]

- JosephNg, P.S. EaaS Optimization: Available yet hidden information technology infrastructure inside the medium-size enterprise. Technol. Forecast. Soc. Chang. 2018, 132, 165–173. [Google Scholar] [CrossRef]

- NCSI. National Centre for Statistics and Information. Popul. Stat. Bull. 2020, 12, 5443. [Google Scholar]

- Mohajan, H. Two Criteria for Good Measurements in Research: Validity and Reliability. Ann. Spiru Haret Univ. 2017, 3, 32. [Google Scholar] [CrossRef] [Green Version]

- See, S.; JosephNg, P.; Phan, K.; Lim, J. JomWowNFC: Why NFC must be used for Merchant & Consumer? In Proceedings of the 2021 Innovations in Power and Advanced Computing Technologies (i-PACT), Kuala Lumpur, Malaysia, 27–29 November 2021; pp. 1–6. [Google Scholar] [CrossRef]

- Al-Saedi, K.; Al-Emran, M.; Ramayah, T.; Abusham, E. Developing a general extended UTAUT model for M-payment adoption. Technol. Soc. 2020, 62, 101293. [Google Scholar] [CrossRef]

- Zhao, H.; Anong, S.T.; Zhang, L. Understanding the impact of financial incentives on NFC mobile payment adoption An experimental analysis. Int. J. Bank Mark. 2019, 37, 1296–1312. [Google Scholar] [CrossRef]

{kind=link}

| Characteristics | Answer | Number | Percentage (%) |

|---|---|---|---|

| Language | Arabic | 64 | 63.37 |

| English | 37 | 36.63 | |

| Age | Less than 15 | 0 | 0.00 |

| 15 to 25 | 20 | 19.80 | |

| 26 to 35 | 30 | 29.70 | |

| 36 to 45 | 31 | 30.69 | |

| 46 to 55 | 20 | 19.80 | |

| Above 55 | 0 | 0.00 | |

| Education Level | Secondary school or lower | 19 | 18.81 |

| Diploma | 14 | 13.86 | |

| Undergraduate (Bachelor’s) | 44 | 43.56 | |

| Postgraduate (Master’s and Above) | 24 | 23.76 | |

| Do you use a mobile payment application? | Yes | 6 | 5.94 |

| No | 95 | 94.06 | |

| If yes, since when did you start to use mobile payments? | Less than 1 Year | 4 | 3.96 |

| 1 to 2 years | 31 | 30.69 | |

| 3 to 4 Years | 30 | 29.70 | |

| More than 5 Years | 30 | 29.70 | |

| N/A | 6 | 5.94 | |

| Have you ever encountered or faced a problem or issue because of mobile payments? | Yes | 76 | 75.25 |

| No | 25 | 24.75 | |

| If yes, what was the nature of the problem you faced? | Network Issue | 4 | 3.96 |

| Login Issue | 31 | 30.69 | |

| Transaction Issue | 3 | 2.97 | |

| Unfamiliar with application | 8 | 7.92 | |

| Other | 55 | 54.46 |

| Construct | Item | Loading | Cronbach’s Alpha | Rho_A | Composite Reliability | Average Variance Extracted (AVE) |

|---|---|---|---|---|---|---|

| Attitude | AT1 | 0.958 | 0.979 | 0.980 | 0.985 | 0.941 |

| AT2 | 0.972 | |||||

| AT3 | 0.970 | |||||

| AT4 | 0.980 | |||||

| Actual Mobile Payment Use | AUB1 | 0.928 | 0.896 | 0.948 | 0.933 | 0.824 |

| AUB2 | 0.878 | |||||

| AUB3 | 0.917 | |||||

| Digital Social Media Influence | DSMPI1 | 0.916 | 0.856 | 0.903 | 0.932 | 0.873 |

| DSMPI2 | 0.952 | |||||

| Facilitating Condition | FC1 | 0.835 | 0.938 | 0.956 | 0.956 | 0.845 |

| FC2 | 0.929 | |||||

| FC3 | 0.955 | |||||

| FC4 | 0.952 | |||||

| Intention to Use Mobile Payments | IU1 | 0.952 | 0.974 | 0.975 | 0.981 | 0.928 |

| IU2 | 0.958 | |||||

| IU3 | 0.972 | |||||

| IU4 | 0.972 | |||||

| Perceived Behavioural Control | PBC1 | 0.961 | 0.960 | 0.960 | 0.974 | 0.926 |

| PBC2 | 0.963 | |||||

| PBC3 | 0.963 | |||||

| Perceived Ease of Use | PEoU1 | 0.922 | 0.958 | 0.963 | 0.969 | 0.888 |

| PEoU2 | 0.950 | |||||

| PEoU3 | 0.957 | |||||

| PEoU4 | 0.940 | |||||

| Perceived Security Risk | PSR1 | 0.869 | 0.772 | 0.822 | 0.896 | 0.811 |

| PSR2 | 0.931 | |||||

| Perceived Trust | PT1 | 0.836 | 0.894 | 0.894 | 0.927 | 0.760 |

| PT2 | 0.837 | |||||

| PT3 | 0.902 | |||||

| PT4 | 0.908 | |||||

| Perceived Usefulness | PU1 | 0.840 | 0.950 | 0.966 | 0.964 | 0.871 |

| PU2 | 0.967 | |||||

| PU3 | 0.969 | |||||

| PU4 | 0.950 | |||||

| Perceived Value | PV1 | 0.944 | 0.949 | 0.950 | 0.967 | 0.908 |

| PV2 | 0.967 | |||||

| PV3 | 0.948 | |||||

| Subjective Norms | SN1 | 0.884 | 0.847 | 0.849 | 0.908 | 0.767 |

| SN2 | 0.831 | |||||

| SN3 | 0.911 | |||||

| Technical Feasibilities | TF1 | 0.921 | 0.840 | 0.845 | 0.926 | 0.861 |

| TF2 | 0.935 |

| Item | AT | MPAUB | DSMPI | FC | MPIU | PCB | PEoU | PSR | PT | PU | PV | SN | TF |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AT1 | 0.958 | 0.667 | 0.738 | 0.775 | 0.786 | 0.834 | 0.804 | 0.631 | 0.731 | 0.730 | 0.786 | 0.726 | 0.836 |

| AT2 | 0.972 | 0.672 | 0.676 | 0.829 | 0.822 | 0.907 | 0.899 | 0.713 | 0.687 | 0.853 | 0.822 | 0.780 | 0.891 |

| AT3 | 0.970 | 0.746 | 0.791 | 0.872 | 0.789 | 0.876 | 0.838 | 0.695 | 0.715 | 0.789 | 0.794 | 0.745 | 0.859 |

| AT4 | 0.980 | 0.691 | 0.695 | 0.855 | 0.847 | 0.924 | 0.908 | 0.736 | 0.716 | 0.848 | 0.845 | 0.787 | 0.906 |

| AUB1 | 0.642 | 0.92 | 0.754 | 0.707 | 0.636 | 0.592 | 0.570 | 0.501 | 0.471 | 0.574 | 0.714 | 0.702 | 0.706 |

| AUB2 | 0.520 | 0.878 | 0.694 | 0.653 | 0.536 | 0.508 | 0.454 | 0.579 | 0.467 | 0.449 | 0.649 | 0.627 | 0.558 |

| AUB3 | 0.738 | 0.917 | 0.737 | 0.777 | 0.872 | 0.741 | 0.706 | 0.580 | 0.553 | 0.660 | 0.828 | 0.571 | 0.793 |

| DSMI1 | 0.564 | 0.625 | 0.916 | 0.716 | 0.553 | 0.562 | 0.556 | 0.542 | 0.461 | 0.549 | 0.668 | 0.451 | 0.672 |

| DSMPI2 | 0.801 | 0.849 | 0.952 | 0.870 | 0.727 | 0.789 | 0.713 | 0.634 | 0.567 | 0.712 | 0.859 | 0.636 | 0.846 |

| FC1 | 0.637 | 0.541 | 0.664 | 0.835 | 0.602 | 0.708 | 0.715 | 0.644 | 0.405 | 0.626 | 0.670 | 0.540 | 0.707 |

| FC2 | 0.778 | 0.701 | 0.840 | 0.929 | 0.700 | 0.840 | 0.784 | 0.585 | 0.576 | 0.769 | 0.807 | 0.622 | 0.818 |

| FC3 | 0.839 | 0.801 | 0.821 | 0.955 | 0.855 | 0.851 | 0.819 | 0.777 | 0.585 | 0.757 | 0.923 | 0.696 | 0.915 |

| FC4 | 0.875 | 0.835 | 0.816 | 0.952 | 0.798 | 0.877 | 0.830 | 0.669 | 0.623 | 0.817 | 0.852 | 0.735 | 0.887 |

| IU1 | 0.813 | 0.708 | 0.649 | 0.755 | 0.952 | 0.847 | 0.827 | 0.576 | 0.616 | 0.751 | 0.862 | 0.660 | 0.865 |

| IU2 | 0.756 | 0.771 | 0.630 | 0.761 | 0.958 | 0.802 | 0.790 | 0.775 | 0.610 | 0.714 | 0.834 | 0.656 | 0.798 |

| IU3 | 0.780 | 0.767 | 0.694 | 0.774 | 0.972 | 0.815 | 0.809 | 0.730 | 0.620 | 0.726 | 0.844 | 0.662 | 0.836 |

| IU4 | 0.873 | 0.757 | 0.708 | 0.843 | 0.972 | 0.919 | 0.909 | 0.700 | 0.674 | 0.859 | 0.889 | 0.711 | 0.903 |

| PBC1 | 0.896 | 0.644 | 0.710 | 0.872 | 0.857 | 0.961 | 0.915 | 0.655 | 0.676 | 0.867 | 0.879 | 0.744 | 0.903 |

| PBC2 | 0.846 | 0.681 | 0.736 | 0.851 | 0.829 | 0.963 | 0.881 | 0.686 | 0.684 | 0.864 | 0.823 | 0.701 | 0.847 |

| PBC3 | 0.893 | 0.684 | 0.685 | 0.859 | 0.849 | 0.963 | 0.937 | 0.752 | 0.650 | 0.881 | 0.837 | 0.749 | 0.877 |

| PEoU1 | 0.873 | 0.598 | 0.619 | 0.785 | 0.792 | 0.892 | 0.922 | 0.778 | 0.695 | 0.881 | 0.777 | 0.721 | 0.830 |

| PEoU2 | 0.852 | 0.701 | 0.692 | 0.848 | 0.909 | 0.932 | 0.950 | 0.663 | 0.678 | 0.828 | 0.850 | 0.684 | 0.873 |

| PEoU3 | 0.825 | 0.612 | 0.638 | 0.821 | 0.767 | 0.886 | 0.957 | 0.644 | 0.661 | 0.917 | 0.757 | 0.661 | 0.819 |

| PEoU4 | 0.801 | 0.549 | 0.640 | 0.774 | 0.779 | 0.856 | 0.940 | 0.570 | 0.731 | 0.849 | 0.741 | 0.624 | 0.781 |

| PSR1 | 0.477 | 0.549 | 0.561 | 0.584 | 0.543 | 0.489 | 0.468 | 0.869 | 0.433 | 0.463 | 0.538 | 0.544 | 0.498 |

| PSR2 | 0.774 | 0.554 | 0.584 | 0.719 | 0.736 | 0.779 | 0.763 | 0.931 | 0.752 | 0.688 | 0.693 | 0.647 | 0.719 |

| PT1 | 0.642 | 0.422 | 0.486 | 0.545 | 0.584 | 0.624 | 0.688 | 0.512 | 0.836 | 0.654 | 0.482 | 0.503 | 0.568 |

| PT2 | 0.593 | 0.344 | 0.415 | 0.419 | 0.560 | 0.562 | 0.601 | 0.550 | 0.837 | 0.513 | 0.449 | 0.413 | 0.443 |

| PT3 | 0.691 | 0.596 | 0.580 | 0.600 | 0.589 | 0.632 | 0.631 | 0.701 | 0.902 | 0.600 | 0.618 | 0.758 | 0.629 |

| PT4 | 0.627 | 0.570 | 0.453 | 0.531 | 0.545 | 0.605 | 0.632 | 0.609 | 0.908 | 0.617 | 0.540 | 0.702 | 0.533 |

| PU1 | 0.586 | 0.502 | 0.588 | 0.640 | 0.577 | 0.701 | 0.702 | 0.449 | 0.478 | 0.840 | 0.626 | 0.493 | 0.637 |

| PU2 | 0.793 | 0.634 | 0.674 | 0.776 | 0.759 | 0.882 | 0.893 | 0.632 | 0.676 | 0.967 | 0.771 | 0.612 | 0.799 |

| PU3 | 0.818 | 0.613 | 0.659 | 0.770 | 0.779 | 0.859 | 0.891 | 0.658 | 0.691 | 0.969 | 0.746 | 0.658 | 0.822 |

| PU4 | 0.867 | 0.610 | 0.636 | 0.825 | 0.813 | 0.912 | 0.924 | 0.673 | 0.682 | 0.950 | 0.791 | 0.695 | 0.836 |

| PV1 | 0.771 | 0.781 | 0.775 | 0.830 | 0.824 | 0.815 | 0.759 | 0.608 | 0.567 | 0.724 | 0.944 | 0.666 | 0.863 |

| PV2 | 0.845 | 0.812 | 0.851 | 0.872 | 0.838 | 0.852 | 0.799 | 0.613 | 0.595 | 0.756 | 0.967 | 0.668 | 0.919 |

| PV3 | 0.778 | 0.749 | 0.746 | 0.851 | 0.880 | 0.848 | 0.820 | 0.756 | 0.555 | 0.777 | 0.948 | 0.653 | 0.884 |

| SN1 | 0.688 | 0.568 | 0.477 | 0.600 | 0.643 | 0.690 | 0.655 | 0.466 | 0.577 | 0.608 | 0.602 | 0.884 | 0.637 |

| SN2 | 0.642 | 0.673 | 0.630 | 0.683 | 0.600 | 0.613 | 0.552 | 0.697 | 0.543 | 0.528 | 0.636 | 0.831 | 0.631 |

| SN3 | 0.728 | 0.571 | 0.454 | 0.587 | 0.588 | 0.691 | 0.668 | 0.596 | 0.675 | 0.608 | 0.587 | 0.911 | 0.627 |

| TF1 | 0.751 | 0.626 | 0.692 | 0.748 | 0.778 | 0.788 | 0.733 | 0.544 | 0.494 | 0.685 | 0.840 | 0.617 | 0.921 |

| TF2 | 0.914 | 0.802 | 0.830 | 0.935 | 0.858 | 0.898 | 0.891 | 0.730 | 0.659 | 0.858 | 0.889 | 0.719 | 0.935 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

JosephNg, P.S.; Al-Rawahi, M.M.K.; Eaw, H.C. Provoking Actual Mobile Payment Use in the Middle East. Appl. Syst. Innov. 2022, 5, 37. https://doi.org/10.3390/asi5020037

JosephNg PS, Al-Rawahi MMK, Eaw HC. Provoking Actual Mobile Payment Use in the Middle East. Applied System Innovation. 2022; 5(2):37. https://doi.org/10.3390/asi5020037

Chicago/Turabian StyleJosephNg, Poh Soon, Mohamed Musallam Khasib Al-Rawahi, and Hooi Cheng Eaw. 2022. "Provoking Actual Mobile Payment Use in the Middle East" Applied System Innovation 5, no. 2: 37. https://doi.org/10.3390/asi5020037

APA StyleJosephNg, P. S., Al-Rawahi, M. M. K., & Eaw, H. C. (2022). Provoking Actual Mobile Payment Use in the Middle East. Applied System Innovation, 5(2), 37. https://doi.org/10.3390/asi5020037