Exploring Transaction Security on Consumers’ Willingness to Use Mobile Payment by Using the Technology Acceptance Model

Abstract

:1. Introduction

2. Literature Review

2.1. Mobile Payment

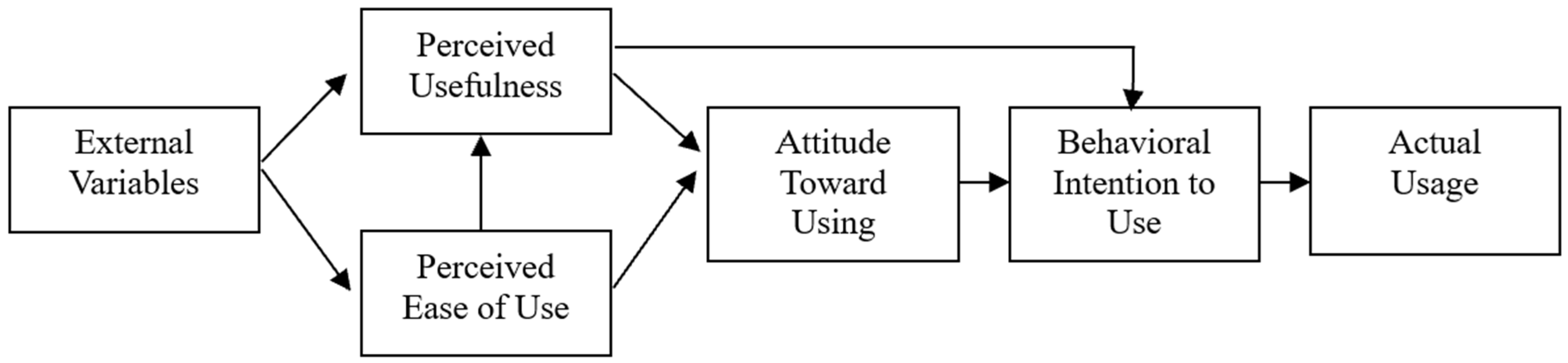

2.2. Technology Acceptance Model

2.3. Transaction Security

- Confidentiality: Transactions cannot be traced over public networks, and information about transactions cannot be obtained by unauthorized intermediaries. All information transacted in an e-commerce environment is kept confidential.

- Integrity: Transactions must not be disrupted or interfered with. It should be confirmed that the content of the electronic transaction has not been changed during the transmission between the client and the server—that is, the information cannot be arbitrarily added, deleted or modified during the transaction processing.

- Authentication: There needs to be assurance that the identity of a subject or resource is characteristic of the person it declares. Authentication applies to users, programs, systems, and information.

- Transaction non-repudiation: The sender of the transaction has its own unique electronic signature, making it impossible to deny the fact of sending this document.

- Privacy: Transactions should remain inviolable, and messages sent and received over the Internet cannot be read, modified or intercepted by any other parties.

3. Research Method and Design

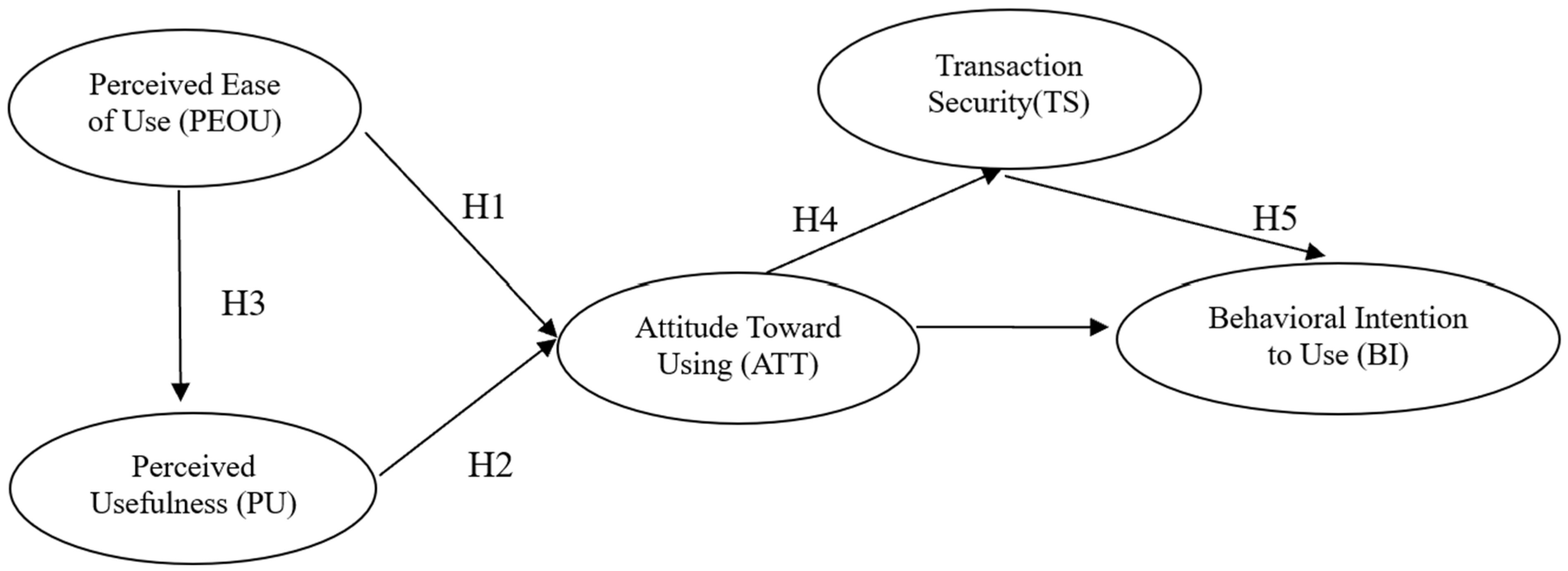

3.1. Conceptual Framework

3.2. Research Subjects

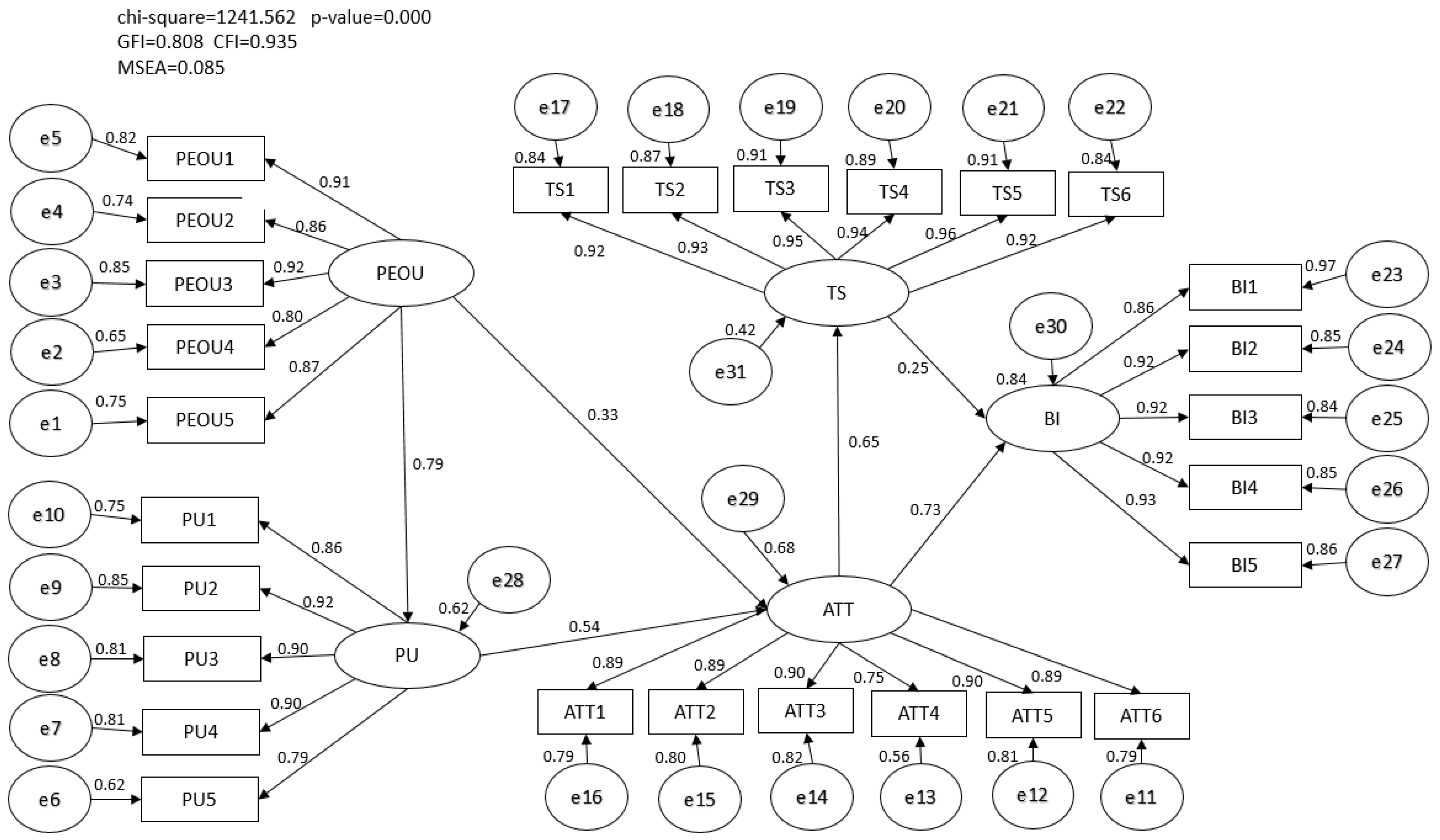

4. Analysis of Results

4.1. Confirmatory Factor Analysis

4.1.1. Perceived Ease of Use

4.1.2. Perceived Ease of Use

4.1.3. Attitude toward Using

4.1.4. Behavioral Intention to Use

4.1.5. Transaction Security

4.2. Reliability, Validity and Fit Analysis

4.2.1. Reliability

4.2.2. Validity

Convergent Validity

Discriminant Validity

4.2.3. Test of Goodness-of-Fit

4.3. Overall Model Analysis

Testing of Hypotheses

4.4. Analysis of Mediating Effect

4.5. Summary of Results

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Al Hogail, A.; Al Shahrani, M. Building Consumer Trust to Improve Internet of Things (IoT) Technology Adoption. In Proceedings of the International Conference on Applied Human Factors and Ergonomics, Orlando, FL, USA, 21–25 July 2018; pp. 325–334. [Google Scholar]

- Christensen, C.M.; Dillon, K.; Hall, T.; Duncan, D.S. Competing Against Luck: The Story of Innovation and Customer Choice, 1st ed.; Harper Business: Manhattan, NY, USA, 2016. [Google Scholar]

- Dunning, D.; Anderson, J.E.; Schlösser, T.; Ehlebracht, D.; Fetchenhauer, D. Trust at zero acquaintance: More a matter of respect than expectation of reward. J. Personal. Soc. Psychol. 2014, 107, 122–141. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chawla, M.; Aparajita, D.; Chakraborty, A. Exploring Factors Influencing Usage of E-Wallets in India. ANVESHAK Int. J. Manag. 2021, 10, 73–92. [Google Scholar] [CrossRef]

- Dhingra, M.; Sachdeva, K.; Machan, M. Factors Impacting the Usage of E-Wallets in National Capital Region. Turk. J. Comput. Math. Educ. 2020, 11, 675–686. [Google Scholar]

- Eriksson, N.; Gökhan, A.; Stenius, M. A qualitative study of consumer resistance to mobile payments for in-store purchases. Procedia Comput. Sci. 2021, 181, 634–641. [Google Scholar] [CrossRef]

- de Kerviler, G.; Demoulin, N.T.M.; Zidda, P. Adoption of in-store mobile payment: Are perceived risk and convenience the only drivers? J. Retail. Consum. Serv. 2016, 31, 334–344. [Google Scholar] [CrossRef]

- de Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Mallat, N. Exploring consumer adoption of mobile payments—A qualitative study. J. Strateg. Inf. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, Y.; Li, H.; Yu, B. Understanding perceived risks in mobile payment acceptance. Ind. Manag. Data Syst. 2015, 115, 253–269. [Google Scholar] [CrossRef]

- Chang, W.-L.; Lo, C.-Y. Exploring Trust Transfer in Mobile Payment Adoption. J. Technol. Manag. 2020, 25, 77–108. [Google Scholar]

- Rogers, E.M. Chapter 1 Elements of Diffusion. In Diffusion of Innovations, 5th ed.; The Free Press: New York, NY, USA, 2003; pp. 1–22. [Google Scholar]

- Moore, G.A.; McKenna, R. Chapter 1 High-Tech Marketing Illusion. In Crossing the Chasm: Marketing and Selling High-Tech Products to Mainstream Customers; HarperCollins Publishers: New York, NY, USA, 1999; pp. 7–19. [Google Scholar]

- Liébana-Cabanillas, F.; Ramos-de-Luna, I.; Montoro-Ríos, F.J. Intention to use new mobile payment systems: A comparative analysis of SMS and NFC payments. Econ. Res. Istraz. 2017, 30, 892–910. [Google Scholar] [CrossRef]

- Chiu, S.-C.; Jhang, S.-Y. Do You Use Mobile Payment while the Epidemic Coming? Manag. Inf. Comput. 2022, 11, 81–94. [Google Scholar]

- Daştan, I.; Gürler, C. Factors Affecting the Adoption of Mobile Payment Systems: An Empirical Analysis. Emerg. Mark. J. 2016, 6, 17–24. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; García-Maroto, I.; Muñoz-Leiva, F.; de Luna, I.R. Mobile Payment Adoption in the Age of Digital Transformation: The Case of Apple Pay. Sustainability 2020, 12, 5443. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q 1989, 13, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Ram, S.; Seth, J.N. Consumer Resistance to Innovations: The Marketing Problem and Its Solutions. J. Consum. Mark. 1989, 6, 5–14. [Google Scholar] [CrossRef]

- Laukkanen, T.; Lauronen, J. Consumer value creation in mobile banking services. Int. J. Mob. Commun. 2005, 3, 325–338. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Kim, B.G.; Park, S.C.; Lee, K.J. A structural equation modeling of the Internet acceptance in Korea. Electron. Commer. Res. Appl. 2008, 6, 425–432. [Google Scholar] [CrossRef]

- Chandra, S.; Srivastava, S.C.; Theng, Y.-L. Evaluating the Role of Trust in Consumer Adoption of Mobile Payment Systems: An Empirical Analysis. Commun. Assoc. Inf. Syst. 2010, 27, 561–588. [Google Scholar] [CrossRef] [Green Version]

- AL-Mamoorey, M.A.; Al-Rubaye, M.M.M. The role of electronic payment systems in Iraq in reducing banking risks: An empirical research on private banks. Pol. J. Manag. Stud. 2020, 21, 49–59. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research; Addison-Wesley: Boston, MA, USA, 1975. [Google Scholar]

- Deepak Chawla, D.; Joshi, H. Consumer attitude and intention to adopt mobile wallet in India—An empirical study. Int. J. Bank Mark. 2019, 37, 1590–1618. [Google Scholar] [CrossRef]

- Alswaigh, N.Y.; Aloud, M.E. Factors Affecting User Adoption of E-Payment Services Available in Mobile Wallets in Saudi Arabia. IJCSNS Int. J. Comput. Sci. Netw. Secur. 2021, 21, 222–230. [Google Scholar]

- Alkhowaiter, W.A. Digital payment and banking adoption research in Gulf countries: A systematic literature review. Int. J. Inf. Manag. 2020, 53, 102102. [Google Scholar] [CrossRef]

- Alabdan, R.; Sulphey, M.M. Understanding proximity mobile payment acceptance among Saudi individuals: An exploratory study. IJACSA Int. J. Adv. Comput. Sci. Appl. 2020, 11. [Google Scholar] [CrossRef]

- Lanford, D. Ethics and the internet: Appropriate behavior in electronic communication. Ethics Behav. 1996, 6, 91–106. [Google Scholar] [CrossRef]

- Taylor, S.; Todd, P. Decomposition and Crossover Effect in the Theory of Planned Behavior: A Study of Consumer Adoption Intentions. Int. J. Res. Mark. 1995, 12, 137–155. [Google Scholar] [CrossRef]

- Rong, T.-S. E-Marketing: Practical E-Commerce; Wunan Publishing Co.: Taipei, Taiwan, 2000. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Construct | Indicator | Standardized Factor Loading | Unstandardized Factor Loading | p Value | GFI | CFI | RMSEA |

|---|---|---|---|---|---|---|---|

| PEOU | PEOU1 | 0.916 | 1 | *** | 0.976 | 0.988 | 0.105 |

| PEOU2 | 0.856 | 1.004 | *** | ||||

| PEOU3 | 0.932 | 1.070 | *** | ||||

| PEOU4 | 0.786 | 0.889 | *** | ||||

| PEOU5 | 0.855 | 0.947 | *** |

| Construct | Indicator | Standardized Factor Loading | Unstandardized Factor Loading | p Value | GFI | CFI | RMSEA |

|---|---|---|---|---|---|---|---|

| PU | PU1 | 0.843 | 1 | *** | 0.957 | 0.979 | 0.141 |

| PU2 | 0.935 | 1.123 | *** | ||||

| PU3 | 0.902 | 1.065 | *** | ||||

| PU4 | 0.909 | 1.059 | *** | ||||

| PU5 | 0.766 | 1.021 | *** |

| Construct | Indicator | Standardized Factor Loading | Unstandardized Factor Loading | p Value | GFI | CFI | RMSEA |

|---|---|---|---|---|---|---|---|

| ATT | ATT1 | 0.890 | 1 | *** | 0.957 | 0.979 | 0.141 |

| ATT2 | 0.895 | 1.032 | *** | ||||

| ATT3 | 0.908 | 1.028 | *** | ||||

| ATT4 | 0.741 | 0.749 | *** | ||||

| ATT5 | 0.898 | 1.025 | *** | ||||

| ATT6 | 0.880 | 1.085 | *** |

| Construct | Indicator | Standardized Factor Loading | Unstandardized Factor Loading | p Value | GFI | CFI | RMSEA |

|---|---|---|---|---|---|---|---|

| BI | BI1 | 0.857 | 1 | *** | 0.902 | 0.958 | 0.222 |

| BI2 | 0.921 | 1.053 | *** | ||||

| BI3 | 0.912 | 1.035 | *** | ||||

| BI4 | 0.923 | 1.054 | *** | ||||

| BI5 | 0.932 | 1.050 | *** |

| Construct | Indicator | Standardized Factor Loading | Unstandardized Factor Loading | p Value | GFI | CFI | RMSEA |

|---|---|---|---|---|---|---|---|

| TS | TS1 | 0.924 | 1 | *** | 0.911 | 0.964 | 0.179 |

| TS2 | 0.933 | 1 | *** | ||||

| TS3 | 0.953 | 1.008 | *** | ||||

| TS4 | 0.940 | 1.008 | *** | ||||

| TS5 | 0.953 | 0.992 | *** | ||||

| TS6 | 0.608 | 0.602 | *** |

| Construct | Factor | Chronbach’s α |

|---|---|---|

| PEOU | PEOU1 I think it is easy to learn how to use proximity mobile payment. | 0.939 |

| PEOU 2 I think it is easy to use proximity mobile payment to complete my tasks. | ||

| PEOU 3 To me, proximity mobile payment is easy to understand. | ||

| PEOU 4 I think proximity mobile payment is flexible to use. | ||

| PEOU 5 It is easy for me to become familiar with using proximity mobile payment. | ||

| PU | PU1 The use of proximity mobile payment can improve the convenience of my life and work. | 0.939 |

| PU2 By using proximity mobile payment, I can complete payments faster. | ||

| PU3 Proximity mobile payment improves my efficiency when making payments. | ||

| PU4 Proximity mobile payment makes payments easier. | ||

| PU5 Proximity mobile payment can improve the quality of my life and work. | ||

| ATT | ATT1 I think it is a good idea to use proximity mobile payment. | 0.949 |

| ATT2 I think proximity mobile payment is a good payment tool. | ||

| ATT3 I think proximity mobile payment is an intelligent idea. | ||

| ATT4 I think proximity mobile payment is an advanced idea. | ||

| ATT5 I think proximity mobile payment is valuable to me. | ||

| ATT6 Overall, I’m willing to use proximity mobile payment. | ||

| BI | BI1 In the future, I will use proximity mobile payment instead of other payment methods. | 0.959 |

| BI2 In the future, I will use proximity mobile payment often. | ||

| BI3 In the future, proximity mobile payment will become part of my daily life. | ||

| BI4 In the future, I will recommend others to use proximity mobile payment. | ||

| BI5 In the future, I will encourage friends and family to use proximity mobile payment. | ||

| TS | TS1 I think customer data can securely transfer through proximity mobile payment. | 0.977 |

| TS2 I think proximity mobile payment has a good reputation for security. | ||

| TS3 I think proximity mobile payment has a good design for payment security protocols. | ||

| TS4 I think proximity mobile payment contains state-of-the-art technologies available to protect transactions. | ||

| TS5 I think proximity mobile payment provides security protection in the shopping process. | ||

| TS6 I think proximity mobile payment contains appropriate encryption and privacy protections are in place to ensure successful transactions. |

| Construct | Combined Reliability | Average Variance Extraction |

|---|---|---|

| PEOU | 0.9397 | 0.7578 |

| PU | 0.9410 | 0.7623 |

| ATT | 0.9492 | 0.7579 |

| BI | 0.9598 | 0.8270 |

| TS | 0.9590 | 0.7579 |

| Construct | PEOU | PU | ATT | BI | TS |

|---|---|---|---|---|---|

| PEOU | 0.7578 | ||||

| PU | 0.6209 | 0.7623 | |||

| ATT | 0.5670 | 0.6464 | 0.7579 | ||

| BI | 0.4475 | 0.4610 | 0.7046 | 0.827 | |

| TS | 0.3136 | 0.2470 | 0.4212 | 0.5256 | 0.799 |

| Goodness-of-Fit | Fit Model | Ideal Indicator | Fit Level |

|---|---|---|---|

| CMIN/DF | 2.904 | <3 | Good |

| GFI | 0.808 | >0.9 | Not Good |

| AGFI | 0.902 | >0.9 | Good |

| RMSEA | 0.085 | <0.07 | Not Good |

| PGFI | 0.680 | >0.5 | Good |

| PNFI | 0.828 | >0.5 | Good |

| NFI | 0.914 | Between 0 and 1 and closer to 1 | Good |

| RFI | 0.905 | Between 0 and 1 and closer to 1 | Good |

| IFI | 0.935 | Between 0 and 1 and closer to 1 | Good |

| CFI | 0.935 | Between 0 and 1 and closer to 1 | Good |

| Construct | Variable | Standardized Factor Loading | Unstandardized Factor Loading | SE | CR T-Value | p-Value |

|---|---|---|---|---|---|---|

| PEOU 🡒 PU | 0.789 | 0.751 | 0.049 | 15.354 | *** | |

| PEOU 🡒 ATT | 0.326 | 0.368 | 0.066 | 5.581 | *** | |

| PU 🡒 ATT | 0.541 | 0.642 | 0.073 | 8.817 | *** | |

| ATT 🡒 TS | 0.650 | 0.732 | 0.051 | 14.393 | *** | |

| TS 🡒 BI | 0.249 | 0.214 | 0.029 | 7.304 | *** | |

| ATT 🡒 BI | 0.732 | 0.709 | 0.041 | 17.112 | *** | |

| PEOU | PEOU1 | 0.908 | 1.034 | 0.040 | 25.940 | *** |

| PEOU2 | 0.858 | 1.049 | 0.046 | 23.017 | *** | |

| PEOU3 | 0.921 | 1.102 | 0.041 | 26.765 | *** | |

| PEOU4 | 0.805 | 0.949 | 0.046 | 20.715 | *** | |

| PEOU5 | 0.867 | 1.000 | ||||

| PU | PU1 | 0.864 | 0.976 | 0.049 | 19.827 | *** |

| PU2 | 0.920 | 1.052 | 0.049 | 21.497 | *** | |

| PU3 | 0.902 | 1.014 | 0.048 | 20.982 | *** | |

| PU4 | 0.899 | 0.999 | 0.048 | 20.911 | *** | |

| PU5 | 0.787 | 1.000 | ||||

| ATT | ATT1 | 0.886 | 0.907 | 0.034 | 26.523 | |

| ATT2 | 0.892 | 0.937 | 0.035 | 26.998 | *** | |

| ATT3 | 0.904 | 0.932 | 0.033 | 27.876 | *** | |

| ATT4 | 0.748 | 0.689 | 0.036 | 19.021 | *** | |

| ATT5 ATT6 | 0.899 0.890 | 0.933 1.000 | 0.074 | 27.493 | *** | |

| BI | BI1 | 0.857 | 1.000 | |||

| BI2 | 0.922 | 1.054 | 0.039 | 26.752 | *** | |

| BI3 | 0.918 | 1.041 | 0.039 | 26.379 | *** | |

| BI4 | 0.921 | 1.052 | 0.040 | 26.316 | *** | |

| BI5 | 0.927 | 1.045 | 0.039 | 26.727 | *** | |

| TS | TS1 | 0.918 | 1.000 | |||

| TS2 | 0.931 | 1.004 | 0.030 | 33.960 | *** | |

| TS3 | 0.951 | 1.013 | 0.028 | 36.435 | *** | |

| TS4 | 0.945 | 1.019 | 0.029 | 35.260 | *** | |

| TS5 TS6 | 0.956 0.917 | 1.001 0.980 | 0.027 0.031 | 36.847 32.010 | *** *** | |

| Constructs | Standardized Factor Loading | Unstandardized Factor Loading | SE | CR | Construct |

|---|---|---|---|---|---|

| ATT 🡒 TS | 0.650 | 0.732 | 0.650 | 14.393 | *** |

| TS 🡒 BI | 0.249 | 0.214 | 7.304 | *** | |

| ATT 🡒 BI | 0.732 | 0.709 | 0.041 | 17.112 | *** |

| Constructs | Direct Effect | Indirect Effect | Total Effect |

|---|---|---|---|

| ATT 🡒 BI | 0.732 | 0.162 | 0.894 |

| ATT 🡒 TS | 0.650 | ||

| TS 🡒 BI | 0.249 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tsai, S.-C.; Chen, C.-H.; Shih, K.-C. Exploring Transaction Security on Consumers’ Willingness to Use Mobile Payment by Using the Technology Acceptance Model. Appl. Syst. Innov. 2022, 5, 113. https://doi.org/10.3390/asi5060113

Tsai S-C, Chen C-H, Shih K-C. Exploring Transaction Security on Consumers’ Willingness to Use Mobile Payment by Using the Technology Acceptance Model. Applied System Innovation. 2022; 5(6):113. https://doi.org/10.3390/asi5060113

Chicago/Turabian StyleTsai, Shuo-Chang, Chih-Hsien Chen, and Keng-Chang Shih. 2022. "Exploring Transaction Security on Consumers’ Willingness to Use Mobile Payment by Using the Technology Acceptance Model" Applied System Innovation 5, no. 6: 113. https://doi.org/10.3390/asi5060113

APA StyleTsai, S. -C., Chen, C. -H., & Shih, K. -C. (2022). Exploring Transaction Security on Consumers’ Willingness to Use Mobile Payment by Using the Technology Acceptance Model. Applied System Innovation, 5(6), 113. https://doi.org/10.3390/asi5060113