The Key Techno-Economic and Manufacturing Drivers for Reducing the Cost of Power-to-Gas and a Hydrogen-Enabled Energy System

Abstract

:1. Introduction

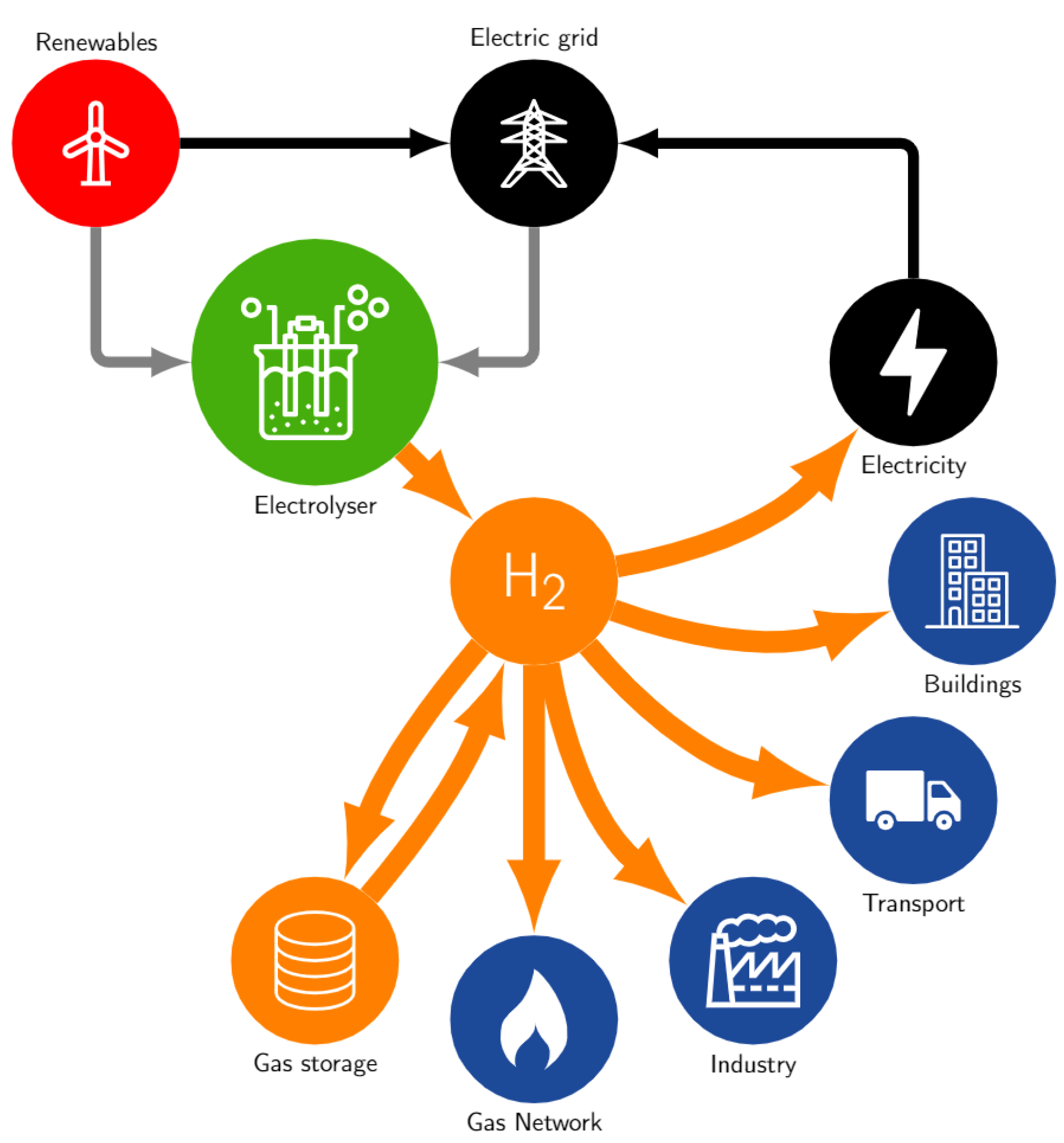

- Storage: Hydrogen can be stored readily as compressed gas, as a liquid, or absorbed into materials. The former has the most potential to bring resilience and scale to energy networks. At scale, geological hydrogen storage could potentially be deployed by utilising depleted gas fields [15];

- Gas network: There is an opportunity for hydrogen to be used for heating and power in buildings. Using the existing (and future) gas network infrastructure including blending with natural gas. This is a potential pathway to bringing forward a means for distribution;

- Industry—feedstocks: Hydrogen is a key feed stock for steel, ammonia, and methanol production, as well as for refineries offering a competitive alternative to natural gas and coal as the primary energy source. It can also offer mid- to high-grade thermal energy for industry, in competition with electrical heating and heat pumps;

- Transportation: There is scope for hydrogen to fuel trains, heavy and medium-duty trucks, vans for urban delivery, coaches, long and short distance urban buses, small and large ferries, taxis, large passenger vehicles, sports utility vehicles (SUVs), mid-size short and long range vehicles, small urban cars, syn-fuelled aviation and forklifts. All applications would be expected to have competition from battery vehicles, bio-fuels, and electric catenary systems. Nevertheless, some studies point to the fact that, on-balance, a typical driver would prefer hydrogen [14];

- Buildings: Buildings would benefit from using gas in boilers or in hydrogen fuelled combined heat and power systems. Renewable hydrogen potentially represents a cost competitive alternative to the use of biogas and in the long term natural gas with carbon capture;

- Electric power: Hydrogen offers the potential for utility scale electricity production via fuel cells, simple cycle and combined cycle turbines, as well as for back-up and remote generation;

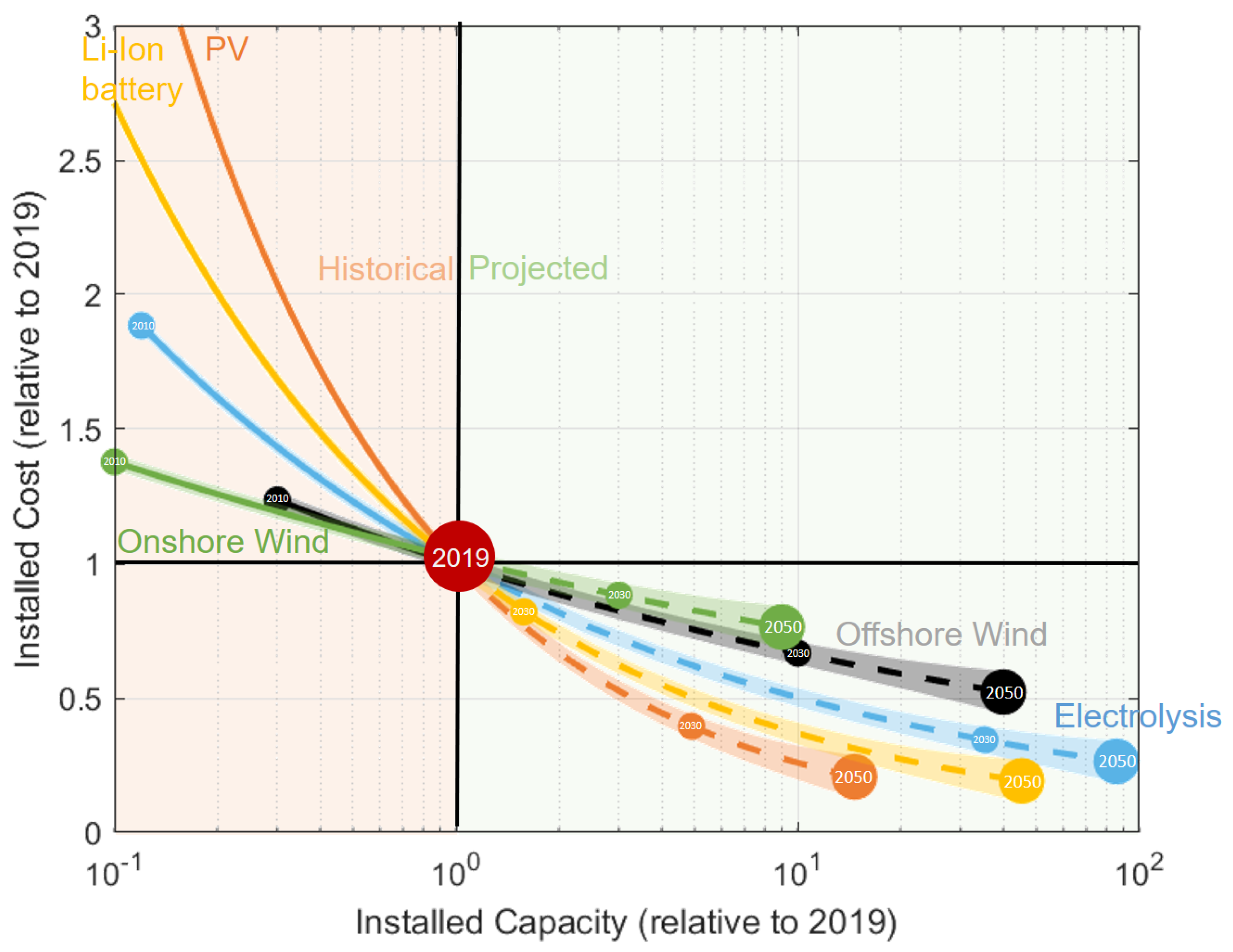

1.1. A Growing Opportunity for Renewable Hydrogen

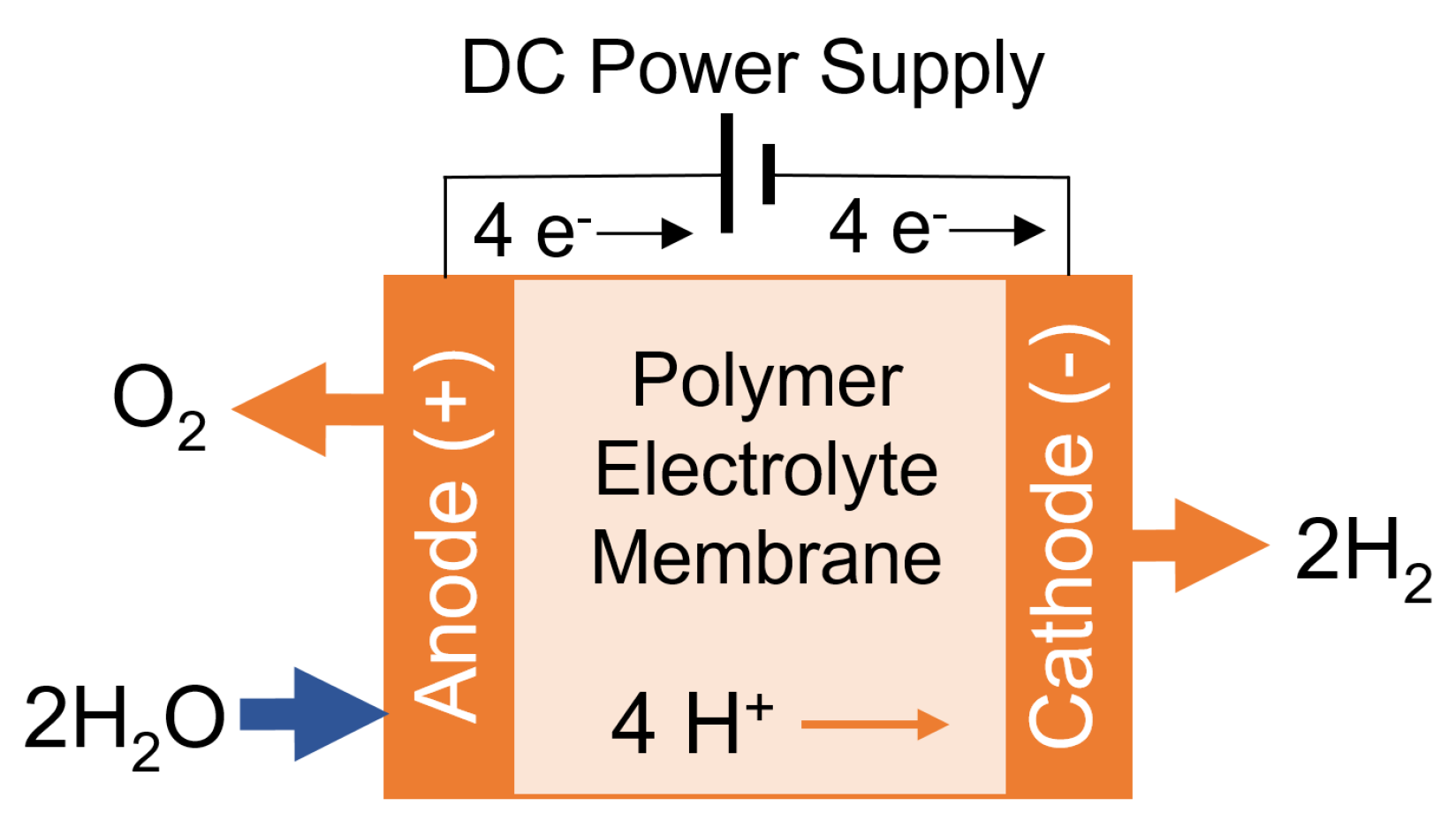

1.2. The Electrolysis of Water to Produce Hydrogen

1.2.1. Electrolysis Types

1.2.2. The Contribution of This Research

2. Methodology

2.1. Capital Cost of an Electrolyser System

2.1.1. Stack Cost

2.1.2. Balance of Plant Cost

2.2. Total System Costs

2.3. Life-Cycle Costing Analysis

3. Results

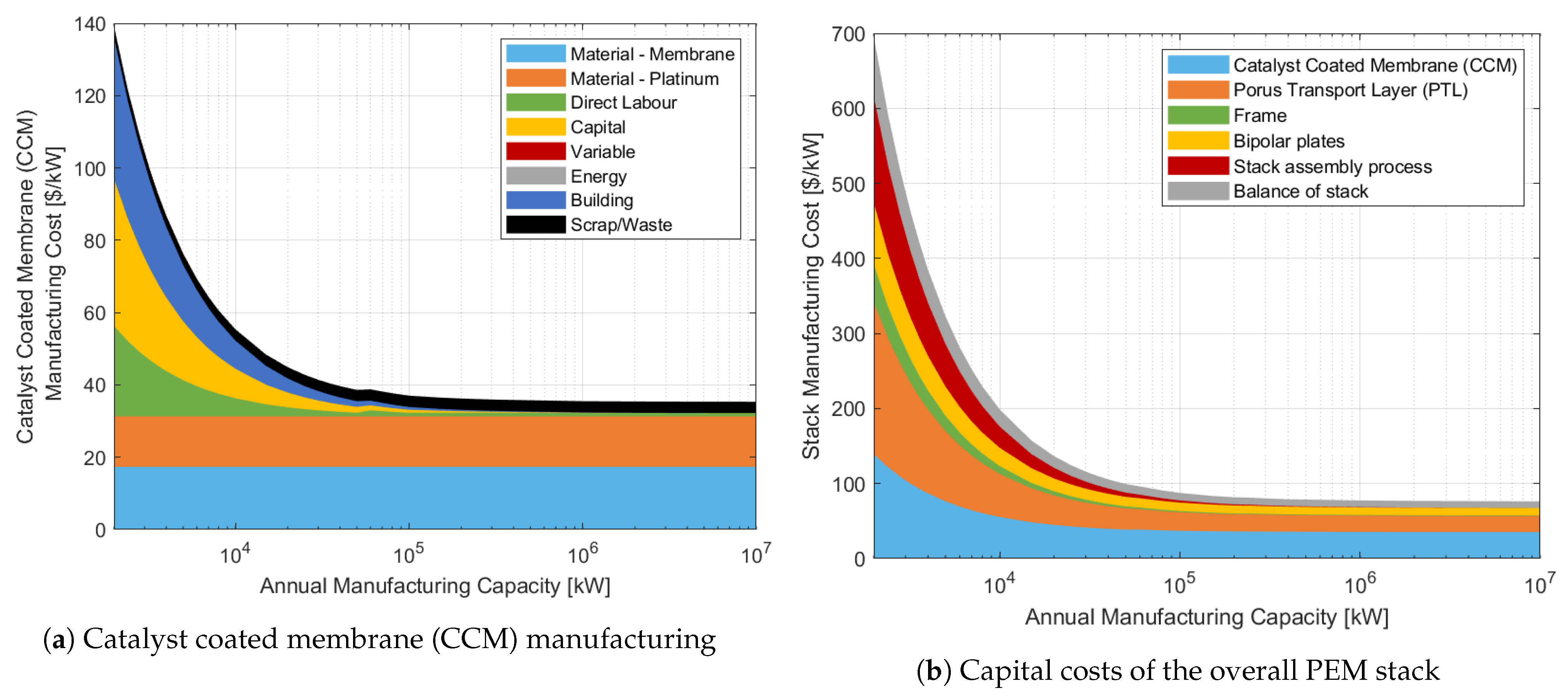

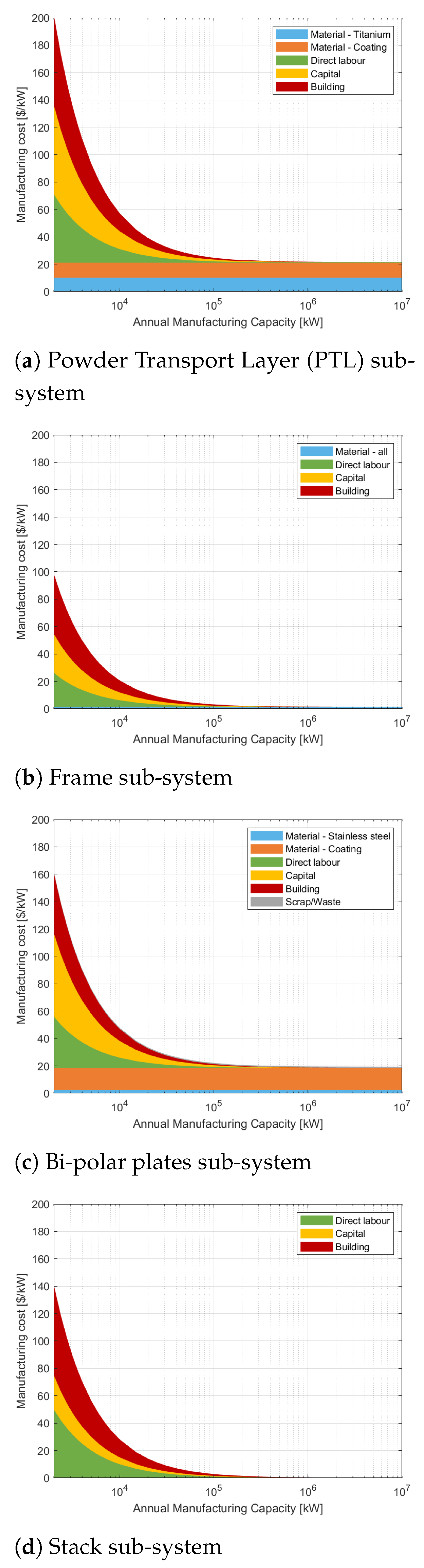

3.1. Capital Cost of PEM System

3.1.1. Individual Stack Process Costs

3.1.2. Overall Stack Process Costs

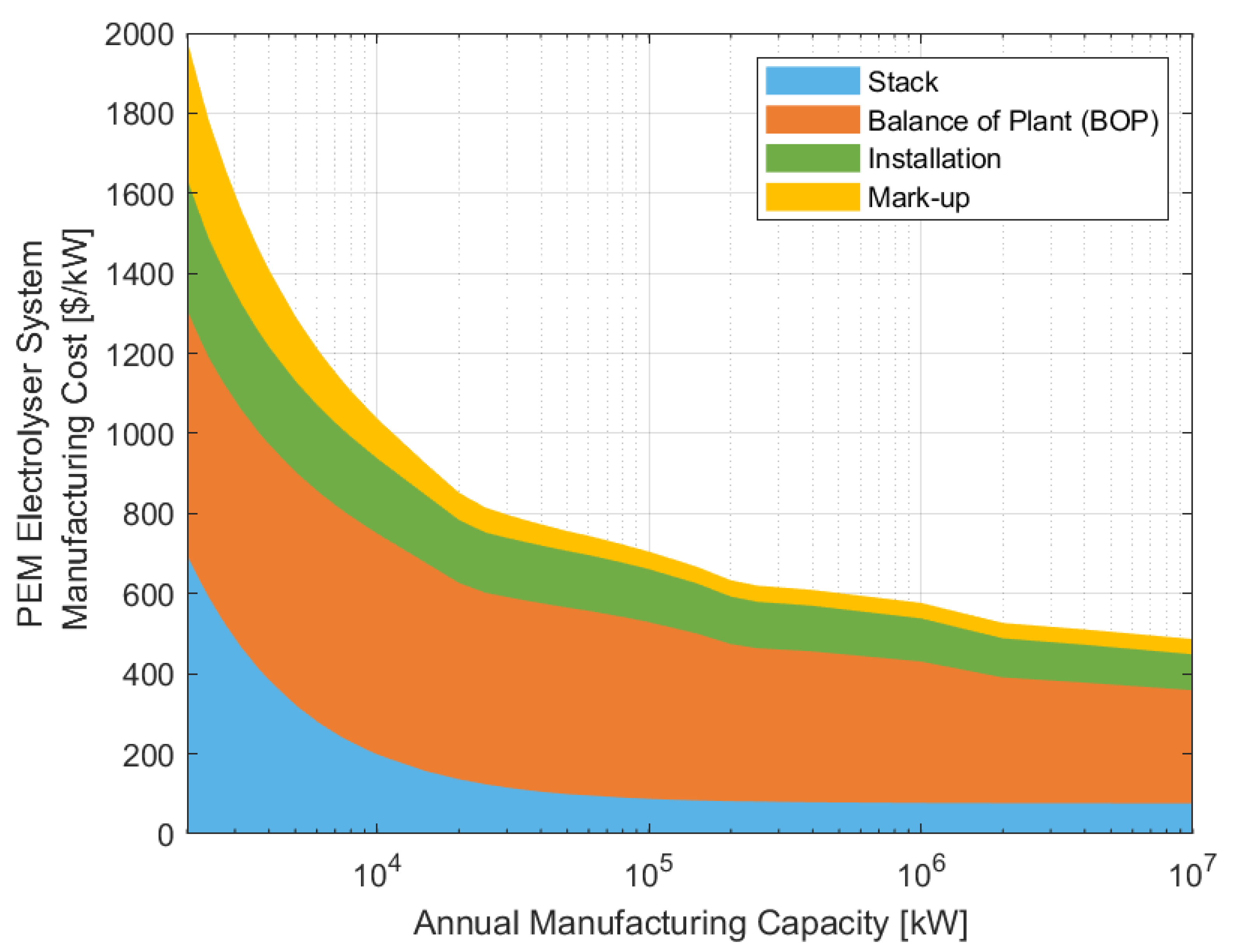

3.1.3. Overall System Cost

3.1.4. Comparison of Current and Future System Capital Costs

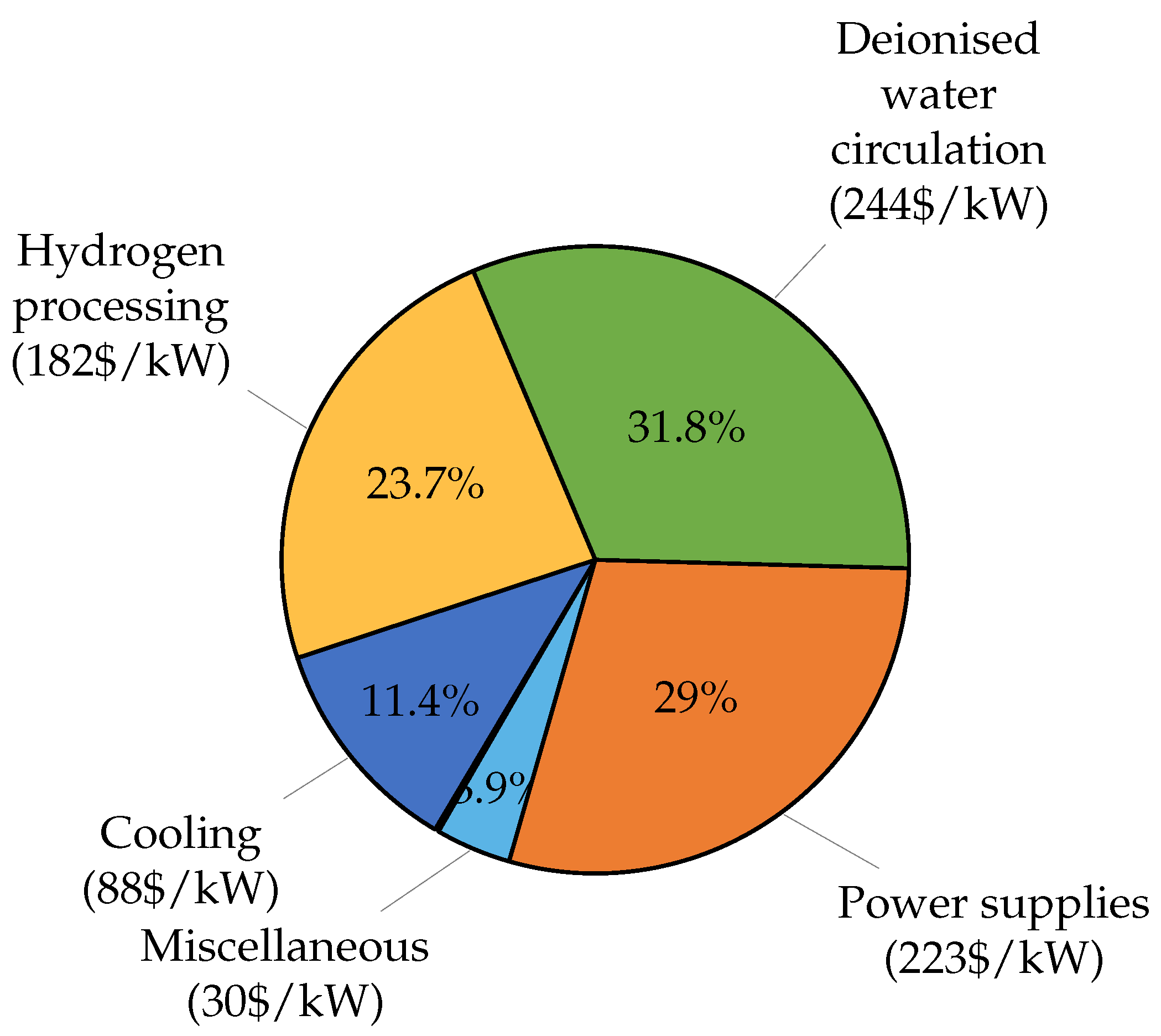

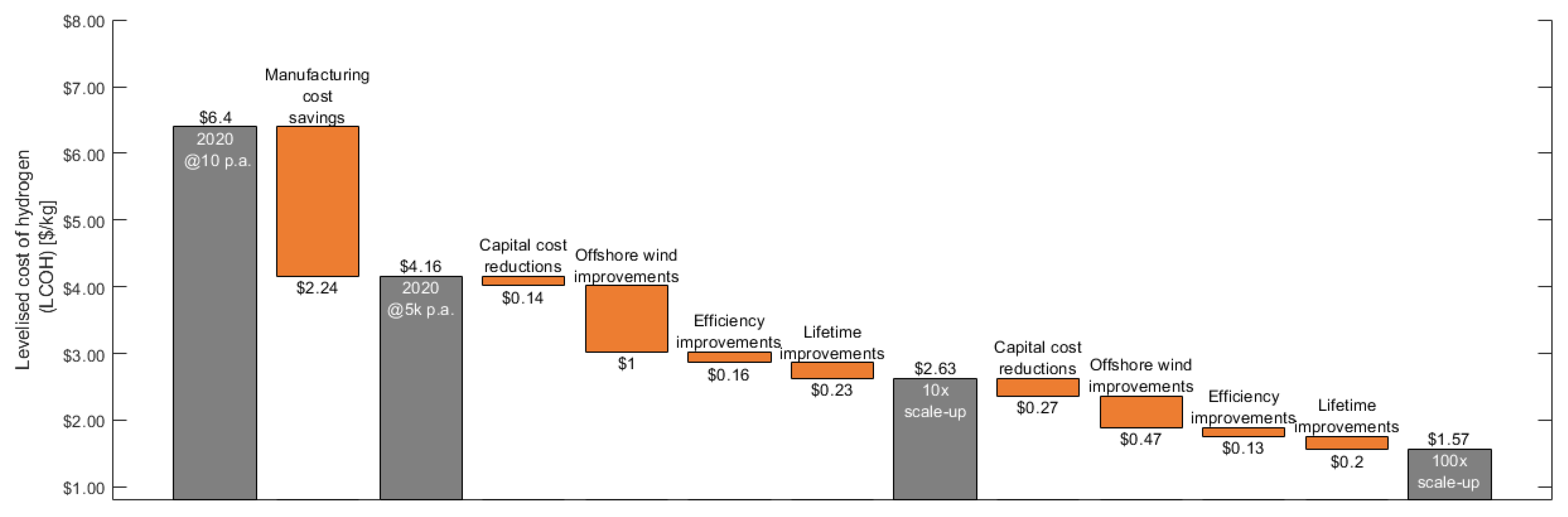

- Improved balance of plant (BOP) cost and efficiency: These benefits will come through a BOP capital and operational cost reduction. As presented in the breakdown presented in Figure 7, gas processing, cooling, power supplies, and water processing would all be considered to be well established in conventional industrial or power generation sectors and typically become more cost effective as they are scaled up. The ×10 scale-up in installed capacity case assumes that the BOP costs can be improved by 60 $/kW;

- Symbiosis and heat recovery: Additionally, as low-grade heat is the principle waste product, opportunities for heat recovery and utilisation can also be exploited [39]. Hydrogen compression via sorption technology also represents an opportunity for direct recovery and utilisation of heat from the PEM system [40]. The ×100 scale-up in installed capacity case assumes that the installation of symbiotic technology costs can be improved by 20 $/kW. The ×100 scale-up in installed capacity case assumes that further savings can be achieved through larger systems increasing by 30 $/kW;

- Advanced electrolysis system operational pressures: It is likely that improved PEM electrolysis systems could deliver a higher pressure hydrogen gas as an output, as such there is the potential to reduce the need to perform mechanical compression (in total or in stages) to achieve practical storage pressures (current included in BOP costs). This would improve the overall system energy consumption and reduced CAPEX for the hydrogen compressor. The ×10 scale-up in installed capacity case assumes that the BOP costs can be improved by 79 $/kW and a further 79 $/kW at ×100 installed capacity scale-up;

- Novel electrolysis system designs: Electrolysis systems based on the PEM stack arrangement presented in Figure 4 has been the focus of this article. Fundamentally, a stack arrangement for PEM stack systems have reached a sufficient level of maturity such that it can be scaled-up. However, the layout and its design is material intensive and it has the limitation that it typically scales-up in a modular and linear way;In the long term, there is the possibility that other electrolysis technologies and arrangements, such as those presented by Grader et al., [37] may well offer more potential for deployment at the 1MW+ scale. These designs perform water electrolysis process in two stages. By decoupling the two reactions, this could potentially offer a greater efficiency (95%), with the co-benefits of being more scaleable and operating at higher hydrogen production pressures (up to 100 bar). The ×100 scale-up in installed capacity case assumes that the stack and wider BOP costs can be improved by 80 $/kW.

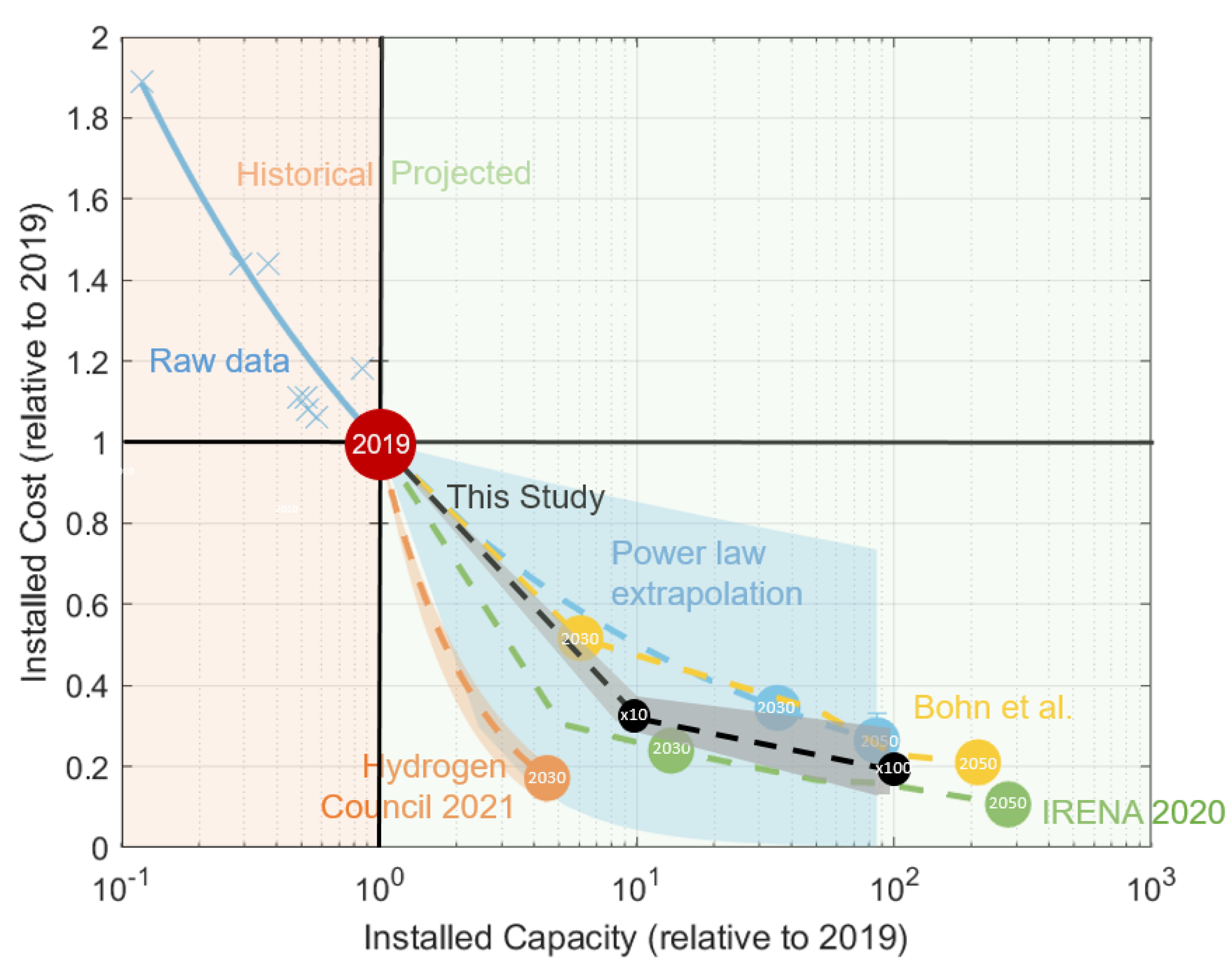

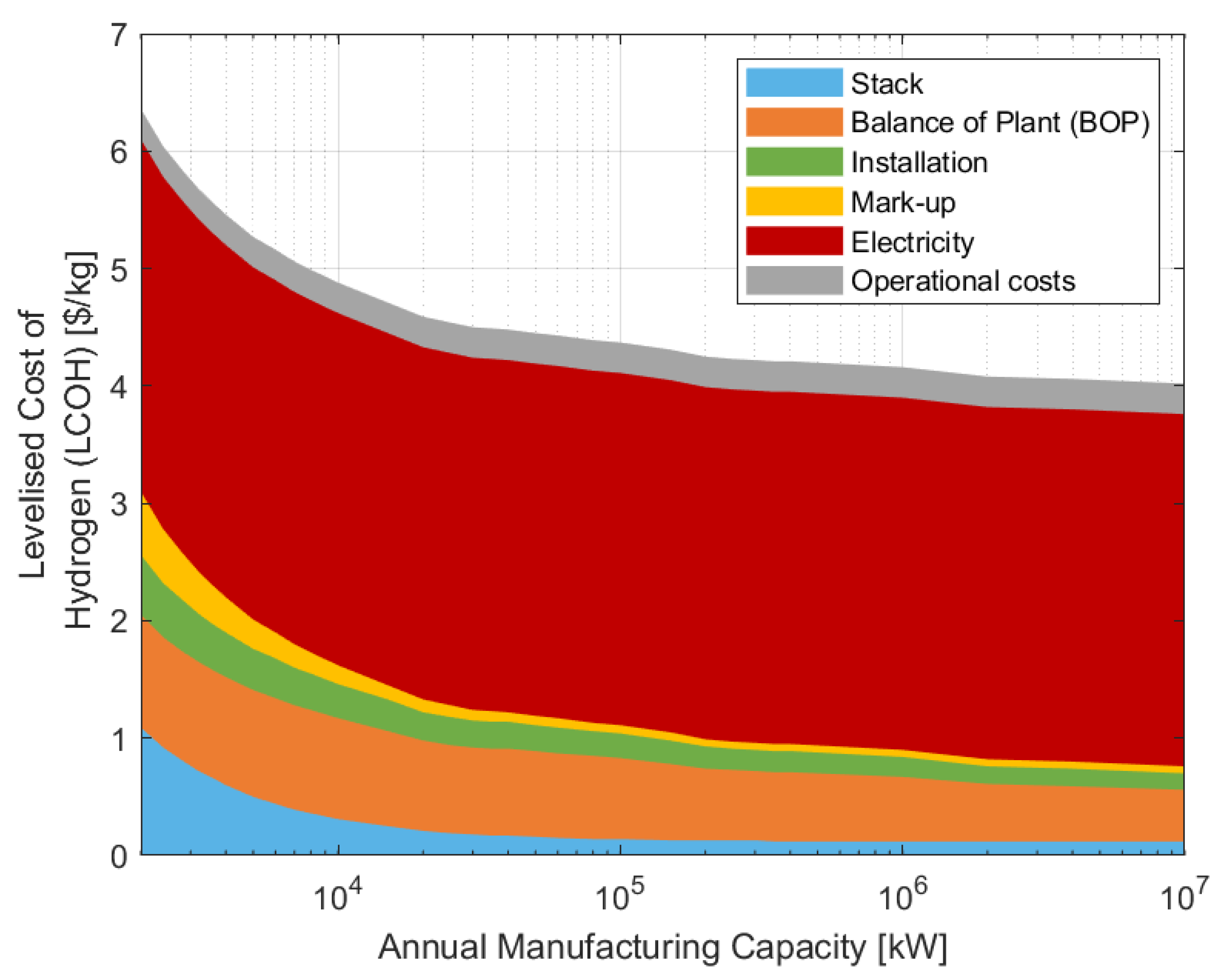

3.2. A Levelised Cost of Hydrogen Analysis

3.2.1. The Value of Increasing to Mass Manufacturing Scale

3.2.2. The Impact of a Ten-Fold Scale-Up of Installed Capacity

3.2.3. The Impact of a Hundred-Fold Scale-Up of Installed Capacity

4. Discussion

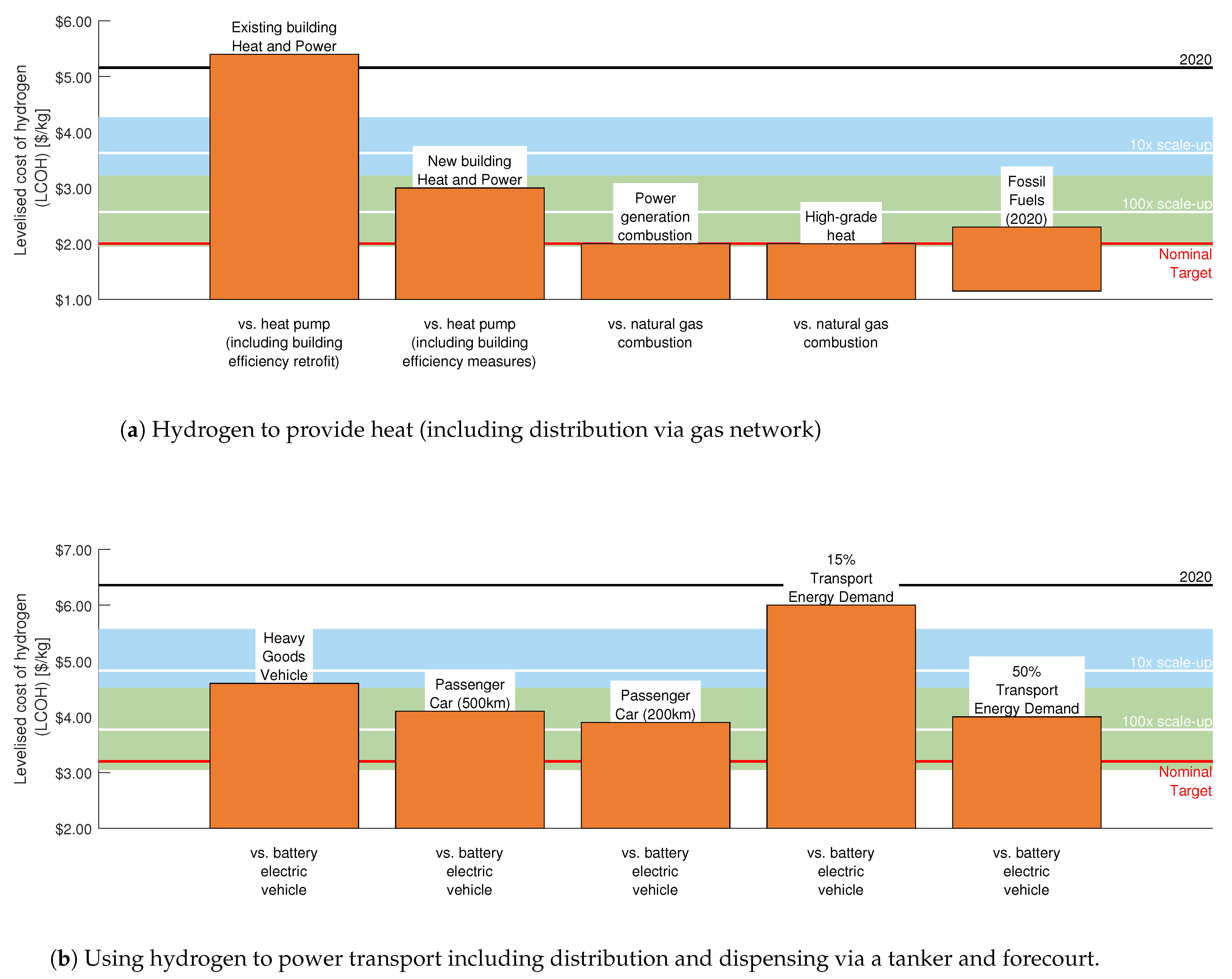

4.1. Implications on the Wider Energy System and Reaching Net-Zero

4.1.1. Residential Heating

4.1.2. Industrial Heating and Power Generation

4.1.3. Transport

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| A | PEM electrolysis cell active area |

| AEL | Alkaline water electrolysis |

| C | Cost |

| CAPEX | Capital expenditure |

| CCM | Catalyst coated membrane |

| CRF | Capital recovery factor |

| BEV | Battery electric vehicle |

| BOP | Balance of plant |

| BP | Bipolar plates |

| EV | Electric vehicle |

| F | Faraday’s constant |

| FCEV | Fuel cell electric vehicle |

| G | Gibbs free energy |

| H | Entropy |

| HGV | Heavy good vehicle |

| LCC | Life-cycle costing analysis |

| LCOH | Levelised cost of hydrogen |

| N | Number of cell in a PEM stack |

| OPEX | Operating expenditure |

| PEM | Proton exchange membrane |

| PtG | Power to gas |

| PTL | Porous transport layer |

| PV | Photovoltaic |

| RES | Renewable energy sources |

| S | Enthalpy |

| S | PEM electrolysis system size |

| SA | Stack assembly |

| SOEC | solid oxide electrolysis |

| SUV | Sports utility vehicle |

| T | Temperature |

| V | Voltage |

Appendix A. Manufacturing Cost Parameters

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Value | Unit | Comment |

|---|---|---|---|

| Operating hours | Variable | hours | 8-h shifts, 2 per day |

| Annual operating days | 250 | days | 5 working days per week and 10 public holidays |

| Inflation rate | 2.6 | % | Data from world bank |

| Discount rate | 10 | % | Similar to other literature [25] |

| Tool lifetime | 15 | Years | [25] |

| Floor space cost | 880 | $/m | [25] |

| Building recovery | 31 | years | U.S. bureau of Economic Analysis rates [25] |

| Building footprint | Variable | m | See Appendix B |

| Hourly labour cost | 23.63 | $/h | [25] |

Appendix B. Manufacturing Model Assumptions

| Parameter | Current | ×10 | Unit | Comment |

|---|---|---|---|---|

| System | Scale-Up | |||

| Nafion membrane cost | 500 | 50 | $/m | [47] |

| Coating line cost | 1,000,000 | 800,000 | $ | Similar spray coatings are used in the PV sector [25] |

| (Ultrasonic spray) | ||||

| Coating manufacturing | 90 | 95 | % | [25] |

| line footprint | ||||

| Manufacturing line speed | 0.5 | 1.0 | m/min | [48] |

| Web width | 1.09 | 1.09 | m | [25] |

| Platinum group metal | 7 | 0.4 | g/m | [47] |

| loading Pt only | ||||

| Platinum group metal | 4 | 0.3 | g/m | [47] |

| loading Pt and Ir (1:1) ratio | ||||

| Platinum price | 30.7 | 30.7 | $/g | 2019 Spot price [49] |

| Iridium price | 47.0 | 47.0 | $/g | 2019 Spot price [49] |

| Nafion ionomer | 1.53 | 1.0 | $/g | [25] |

| Solvents | 10 | 10 | $/gallon | [25] |

| Workers/line | 2 | 2 | workers | [25] |

| CCM area | 0.068 | 0.068 | m | [25] |

| Parameter | Current | ×10 | Unit | Comment |

|---|---|---|---|---|

| System | Scale-Up | |||

| Titanium powder cost | 35 | 35 | $/g | Average price of high purity titanium [25] |

| Powder metallurgy | 1,500,000 | 1,200,000 | $ | [25] |

| production line | ||||

| Gold coating layer | 100 | 50 | nm | 50% reduction in thickness of layer [50] |

| Gold price | 45 | 45 | $/g | 2019 spot price [51] |

| Carbon cloth cost | 400 | 50 | $/m | [52] |

| Physical Vapour | 400,000 | 320,000 | $ | A 20% learning rate curve applied [25] |

| deposition machine | ||||

| Production line | 150 | 150 | m | [25] |

| footprint | ||||

| Powder metallurgy | 99 | 99 | % | [25] |

| process yield | ||||

| Coating process | 99.9 | 99.9 | % | [25] |

| yield | ||||

| Line throughput | 2.0 | 2.0 | units/min | [25] |

| Workers/line | 4 | 4 | workers | [25] |

| Useful area | 0.068 | 0.068 | m | [25] |

| Mass of Titanium/unit | 29 | 23.2 | kg | A 20% reduction in material use via improved design [25] |

| Parameter | Current | Future | Unit | Comment |

|---|---|---|---|---|

| Value | Value | |||

| Distance of frame from | 0.625 | 0.625 | cm | Used for MEA frame bonding (injection moulding) [25] |

| edges of MEA | ||||

| Total frame width | 2.445 | 2.445 | cm | [25] |

| Polyphenylene mixed with | 5.95 | 5.95 | $/kg | [25] |

| 40% glass fibre resin | ||||

| Injection moulding | 700,000 | 560,000 | $ | [25] |

| production line | ||||

| Production line | 100 | 100 | /m | [25] |

| footprint | ||||

| Process yield | 99 | 99 | % | [25] |

| Production line | 2 | 3 | units/min | [25] |

| throughput | ||||

| Workers/line | 2 | 2 | workers | [25] |

| Parameter | Current | ×10 | Unit | Comment |

|---|---|---|---|---|

| System | Scale-Up | |||

| Stainless steel (316L) | 5.0 | 5.0 | $/unit | Based on plate area of 957.44 cm [25] |

| Gold coating layer size | 100 | 50 | nm | 50% reduction [50] |

| Gold coating layer cost | 41 | 41 | $/g | 2019 average price [51] |

| Consumables | 0.6 | 0.6 | $/unit | [25] |

| Production line | 1,500,000 | 1,200,000 | $ | [25] with 20% technological improvement |

| Footprint | 100 | 100 | m | [25] |

| Stamping process | 95 | 96 | % | [25] with 20% technological improvement |

| yield | ||||

| PVD coating process | 99.9 | 99.9 | % | [25] |

| yield | ||||

| Stamping line | 11 | 13 | % | [25] with 20% technological improvement |

| throughput | ||||

| Workers/line | 3 | 3 | workers | [25] |

| Plate area | 957.44 | 947.44 | cm | [25] |

| Parameter | Current | ×10 | Unit | Comment |

|---|---|---|---|---|

| System | Scale-Up | |||

| Assembly line type | ||||

| Manual | 500,000 | 400,000 | $ | [25] |

| Semi-automatic | 1,000,000 | 800,000 | $ | [25] |

| Automatic | 2,000,000 | 1,600,000 | $ | [25] |

| Production line | 150 | 150 | m | [25] |

| footprint | ||||

| Assembly yield | 99.5 | 99.5 | % | [25] |

| Line throughput | 11 | 11 | % | [25] |

| Assembly line staff | ||||

| Manual | 4 | 4 | workers | [25] |

| Semi-automatic | 3 | 3 | workers | [25] |

| Automatic | 2 | 2 | workers | [25] |

| Maximum throughput | ||||

| Manual | 100,000 | 100,000 | units | [25] |

| Semi-automatic | <700,000 | <700,000 | units | [25] |

| Automatic | >700,000 | >700,000 | units | [25] |

Appendix C. Manufacturing Model Results

Appendix D. Operating Parameters of PEM System

| Parameter | Current | ×10 | Unit |

|---|---|---|---|

| System | Scale-Up | ||

| Power | 200 | 200 | kW |

| Gross system power | 220 | 220 | kW |

| H production rate | 30 | 30 | Nm/h |

| H production rate | 80 | 80 | kg/day |

| Turndown ratio | 0–100 | 0–100 | % |

| Operating pressure | 0–30 | 0–30 | bar |

| Total plate area | 957 | 957 | cm |

| CCM coated area | 748 | 748 | cm |

| Single cell active area | 680 | 680 | cm |

| Gross cell inactive area | 9 | 9 | % |

| Single cell current | 1156 | 1156 | A |

| Current density | 1.7 | 2.1 | A/m |

| Reference voltage | V | ||

| Power density | 2.89 | 4.4 | W/m |

| Single cell power | 1956 | 1956 | W |

| Cells per system | 102 | 102 | - |

| Stacks per system | 1 | 1 | - |

| Water pump power | 5 | 5 | kW |

| Other parasitic power | 15 | 15 | kW |

Appendix E. Balance of Plant Capital Costs

| System | Sub-System | Cost |

|---|---|---|

| $ | ||

| Power supply | Power supply | 44,000 |

| DC voltage transducer | 225 | |

| DC current transducer | 340 | |

| Deionised water circulation | Oxygen separator tank | 20,000 |

| Circulation pump | 7053 | |

| Polishing pump | 2289 | |

| Piping | 10,000 | |

| Valves and instrumentation | 7500 | |

| Controls | 2000 | |

| $ | ||

| Hydrogen processing | Dryer bed | 13,860 |

| Water/hydrogen separator | 10,000 | |

| Piping | 5000 | |

| Valves and instrumentation | 5000 | |

| Controls | 2500 | |

| Cooling | Plate heat exchanger | 9000 |

| Cooling pump | 1500 | |

| Piping | 1000 | |

| Valves and instrumentation | 2000 | |

| Dry cooler | 4000 | |

| Miscellaneous | Valve air supply-nitrogen | 2000 |

| Ventilation and safety | 2000 | |

| Gas detectors | 2000 | |

| Exhaust ventilation | 2000 | |

| Total costs | BOP total capital cost for 200 kW system | 153,267 |

| BOP capital cost per kW | 766.34 |

References

- Committee on Climate Change. Net Zero—The UK’s Contribution to Stopping Global Warming. 2019. Available online: https://www.theccc.org.uk/publication/net-zero-the-uks-contribution-to-stopping-global-warming (accessed on 1 June 2021).

- International Renewable Energy Agency (IRENA). Future of Wind: Deployment, Investment, Technology, Grid Integration and Socio-Economic Aspects. 2019. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/Oct/IRENA_Future_of_wind_2019.pdf (accessed on 1 June 2021).

- International Renewable Energy Agency (IRENA). Future of Solar Photovoltaic: Deployment, Investment, Technology, Grid Integration and Socio-Economic Aspects. 2019. Available online: https://irena.org/-/media/Files/IRENA/Agency/Publication/2019/Nov/IRENA_Future_of_Solar_PV_2019.pdf (accessed on 1 June 2021).

- Tsiropoulos, I.; Tarvydas, D.; Lebedeva, N. Li-Ion Batteries for Mobility and Stationary Storage Applications: Scenarios for Costs and Market Growth. 2018. Available online: https://publications.jrc.ec.europa.eu/repository/bitstream/JRC113360/kjna29440enn.pdf (accessed on 1 June 2021).

- International Renewable Energy Agency (IRENA). Renewable Power Generation Costs in 2019. 2020. Available online: https://www.irena.org/publications/2020/Jun/Renewable-Power-Costs-in-2019 (accessed on 1 June 2021).

- International Renewable Energy Agency (IRENA). Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5 °C Climate Goal. 2020. Available online: https://irena.org/-/media/Files/IRENA/Agency/Publication/2020/Dec/IRENA_Green_hydrogen_cost_2020.pdf (accessed on 1 June 2021).

- Möst, D. Will the Experience Curve of PV Repeat for Batteries and Electrolysis? 2019. Available online: https://www.storeandgo.info/fileadmin/downloads/deliverables_2019/20190801-STOREandGO-D7.5-EIL-Report_on_experience_curves_and_economies_of_scale.pdf (accessed on 1 June 2021).

- Böhm, H.; Zauner, A.; Goers, S.; Tichler, R.; Kroon, P. Innovative Large-Scale Energy Storage Technologies and Power-to-Gas Concepts after Optimization. 2018. Available online: https://ec.europa.eu/research/participants/documents/downloadPublic?documentIds=080166e5beb60938&appId=PPGMS (accessed on 1 June 2021).

- Hydrogen Council in Collaboration with McKinsey & Company. Hydrogen Insights: A Perspective on Hydrogen Investment, Market Development and Cost Competitiveness. 2021. Available online: https://hydrogencouncil.com/wp-content/uploads/2021/02/Hydrogen-Insights-2021.pdf (accessed on 1 June 2021).

- International Energy Agency. World Energy Outlook; OECD Publishing: Paris, France, 2017. [Google Scholar] [CrossRef]

- International Energy Agency. World Energy Outlook; OECD Publishing: Paris, France, 2020. [Google Scholar] [CrossRef]

- EnAppSys. GB Electricity Market Summary. 2019. Available online: https://www.enappsys.com/wp-content/uploads/2020/12/gb-market-summary-2019.pdf (accessed on 1 June 2021).

- Shiva Kumar, S.; Himabindu, V. Hydrogen production by PEM water electrolysis—A review. Mater. Sci. Energy Technol. 2019, 2, 442–454. [Google Scholar] [CrossRef]

- Hydrogen Council. Path to Hydrogen Competitiveness: A Cost Perspective. 2020. Available online: https://hydrogencouncil.com/en/path-to-hydrogen-competitiveness-a-cost-perspective/ (accessed on 1 June 2021).

- Hassanpouryouzband, A.; Joonaki, E.; Edlmann, K.; Haszeldine, R.S. Offshore Geological Storage of Hydrogen: Is This Our Best Option to Achieve Net-Zero? ACS Energy Lett. 2021, 6, 2181–2186. [Google Scholar] [CrossRef]

- Lee, B.; Heo, J.; Kim, S.; Sung, C.; Moon, C.; Moon, S.; Lim, H. Economic feasibility studies of high pressure PEM water electrolysis for distributed H2 refueling stations. Energy Convers. Manag. 2018, 162, 139–144. [Google Scholar] [CrossRef]

- McDonald, A.; Schrattenholzer, L. Learning rates for energy technologies. Energy Policy 2001, 29, 255–261. [Google Scholar] [CrossRef] [Green Version]

- Colli, A.N.; Girault, H.H.; Battistel, A. Non-Precious Electrodes for Practical Alkaline Water Electrolysis. Materials 2019, 12, 1336. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- LeRoy, R.L.; Bowen, C.T.; LeRoy, D.J. The Thermodynamics of Aqueous Water Electrolysis. J. Electrochem. Soc. 1980, 127, 1954–1962. [Google Scholar] [CrossRef]

- Climate Change Committee. The Fifth Carbon Budget: The Next Step towards a Low- Carbon Economy. 2015. Available online: https://www.theccc.org.uk/publication/the-fifth-carbon-budget-the-next-step-towards-a-low-carbon-economy/ (accessed on 1 June 2021).

- Dönitz, W.; Erdle, E. High-temperature electrolysis of water vapor—status of development and perspectives for application. Int. J. Hydrog. Energy 1985, 10, 291–295. [Google Scholar] [CrossRef]

- Holladay, J.; Hu, J.; King, D.; Wang, Y. An overview of hydrogen production technologies. Catal. Today 2009, 139, 244–260, Hydrogen Production—Selected papers from the Hydrogen Production Symposium at the American Chemical Society 234th National Meeting & Exposition, Boston, MA, USA, 19–23 August 2007. [Google Scholar] [CrossRef]

- US Department of EnergyHydrogen and Fuel Cell Technologies Office. Hydrogen Production. 2020. Available online: https://www.energy.gov/eere/fuelcells/hydrogen-productionf (accessed on 1 June 2021).

- greencarcongress.com. UK Supports Gigastack Feasibility Study with ITM Power, Ørsted, Element Energy- Gigawatt-Scale PEM Electrolysis. 2020. Available online: https://www.greencarcongress.com/2019/08/20190830gstack.html (accessed on 1 June 2021).

- Colella, W.; James, B.; Moton, J.; Saur, G.; Ramsden, T. Techno-Economic Analysis of PEM Electrolysis for Hydrogen Production. Strategic Analysis Inc. Electrolytic Hydrogen Production Workshop. NREL, Golden, Colorado. February 2014. Available online: https://www.energy.gov/sites/prod/files/2014/08/f18/fcto_2014_electrolytic_h2_wkshp_colella1.pdf (accessed on 1 June 2021).

- Saggiorato, N.; Wei, M.; Lipman, T.; Chan, A.M.S.H.; Breunig, H.; McKone, T.; Beattie, P.; Chong, P.; Colella, W.G.; James, B.D. A Total Cost of Ownership Model for Low Temperature PEM Fuel Cells in Combined Heat and Power and Backup Power Applications. 2016. Available online: https://www.energy.gov/sites/prod/files/2017/02/f34/fcto_2016_tco_model_low_temp_pem_fc.pdf (accessed on 1 June 2021).

- Wei, M.; Lipman, T.E.; Mayyas, A.; Chien, J.; Chan, S.H.; Gosselin, D.; Breunig, H.; Stadler, M.; McKone, T.E.; Beattie, P.; et al. A Total Cost of Ownership Model for Low Temperature PEM Fuel Cells in Combined Heat and Power and Backup Power Applications; Technical report; Lawrence Berkeley National Laboratory: Berkeley, CA, USA, 2014. [Google Scholar]

- Öker, F.; Adigüzel, H. Time-driven activity-based costing: An implementation in a manufacturing company. J. Corp. Account. Financ. 2010, 22, 75–92. [Google Scholar] [CrossRef]

- Prince-Richard, S.; Whale, M.; Djilali, N. A techno-economic analysis of decentralized electrolytic hydrogen production for fuel cell vehicles. Int. J. Hydrog. Energy 2005, 30, 1159–1179. [Google Scholar] [CrossRef]

- Mergel, J.; Carmo, M.; Stolten, D.; Fritz, D.L. A comprehensive review on PEM water electrolysis, International Journal of Hydrogen Energy. Int. J. Hydrog. Energy 2013, 38, 4901–4934. [Google Scholar] [CrossRef]

- H2B2.es. Hydrogen. 2020. Available online: http://h2b2.es/hydrogen/ (accessed on 1 June 2021).

- Daylan, B.; Ciliz, N. Life cycle assessment and environmental life cycle costing analysis of lignocellulosic bioethanol as an alternative transportation fuel. Renew. Energy 2016, 89, 578–587. [Google Scholar] [CrossRef]

- Bertuccioli, L.; Chan, A.; Hart, D.; Lehner, F.; Madden, B.; Standen, E. Development of water electrolysis in the European union. Final report, fuel cells and hydrogen joint undertaking (FCH-JU). 2014. Available online: http://www.fch.europa.eu/sites/default/files/study%20electrolyser_0-Logos_0.pdf (accessed on 1 June 2021).

- UK Government. Energy Trends: UK Electricity. 2020. Available online: https://www.gov.uk/government/statistics/electricity-section-5-energy-trends (accessed on 1 June 2021).

- International Renewable Energy Agency. Hydrogen from Renewable Power: Technology Outlook for the Energy Transition; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2018. [Google Scholar]

- Schmidt, O.; Gambhir, A.; Staffell, I.; Hawkes, A.; Nelson, J.; Few, S. Future cost and performance of water electrolysis: An expert elicitation study. Int. J. Hydrog. Energy 2017, 42, 30470–30492. [Google Scholar] [CrossRef]

- Dotan, H.; Landman, A.; Sheehan, S.W.; Malviya, K.D.; Shter, G.; Grave, D.A.; Arzi, Z.; Yehudai, N.; Halabi, M.; Gal, N.; et al. Decoupled hydrogen and oxygen evolution by a two-step electrochemical–chemical cycle for efficient overall water splitting. Nat. Energy 2019, 4, 786–795. [Google Scholar] [CrossRef]

- Viktorsson, L.; Heinonen, J.T.; Skulason, J.B.; Unnthorsson, R. A Step towards the Hydrogen Economy—A Life Cycle Cost Analysis of A Hydrogen Refueling Station. Energies 2017, 10, 763. [Google Scholar] [CrossRef]

- Lümmen, N.; Karouach, A.; Tveitan, S. Thermo-economic study of waste heat recovery from condensing steam for hydrogen production by PEM electrolysis. Energy Convers. Manag. 2019, 185, 21–34. [Google Scholar] [CrossRef]

- Sdanghi, G.; Maranzana, G.; Celzard, A.; Fierro, V. Towards Non-Mechanical Hybrid Hydrogen Compression for Decentralized Hydrogen Facilities. Energies 2020, 13, 3145. [Google Scholar] [CrossRef]

- Greiner, C.J.; KorpÅs, M.; Holen, A.T. A Norwegian case study on the production of hydrogen from wind power. Int. J. Hydrog. Energy 2007, 32, 1500–1507. [Google Scholar] [CrossRef]

- Bruce, S.; Temminghoff, M.; Hayward, J.; Schmidt, E.; Munnings, C.; Palfreyman, D.; Hartley, P. National Hydrogen Roadmap. 2018. Available online: https://www.csiro.au/en/work-with-us/services/consultancy-strategic-advice-services/CSIRO-futures/Futures-reports/Hydrogen-Roadmap (accessed on 1 June 2021).

- BloombergNEF. Hydrogen Economy Outlook. 2020. Available online: https://about.bnef.com/new-energy-outlook/ (accessed on 1 June 2021).

- Baldino, C.; O’Malley, J.; Searle, S.; Zhou, Y.; Christensen, A. Hydrogen for Heating? Decarbonization Options for Households in the United Kingdom in 2050. 2020. Available online: https://theicct.org/sites/default/files/publications/Hydrogen-heating-UK-dec2020.pdf (accessed on 1 June 2021).

- Smallbone, A.; Jia, B.; Atkins, P.; Roskilly, A.P. The impact of disruptive powertrain technologies on energy consumption and carbon dioxide emissions from heavy-duty vehicles. Energy Convers. Manag. X 2020, 6, 100030. [Google Scholar] [CrossRef]

- Staffell, I.; Scamman, D.; Velazquez Abad, A.; Balcombe, P.; Dodds, P.E.; Ekins, P.; Shah, N.; Ward, K.R. The role of hydrogen and fuel cells in the global energy system. Energy Environ. Sci. 2019, 12, 463–491. [Google Scholar] [CrossRef] [Green Version]

- Tsuchiya, H.; Kobayashi, O. Fuel Cell Cost Study by Learning Curve. In Proceedings of the Annual Meeting of the International Energy Group Organised by EMF/IIASA, Stanford, CA, USA, 18–20 June 2002; pp. 18–20. [Google Scholar]

- Sono-Tek. Products. 2020. Available online: https://www.sono-tek.com/products/ (accessed on 1 June 2021).

- JM Bullion. Platinum Spot Prices & Charts. 2020. Available online: https://www.jmbullion.com/charts/platinum-price/ (accessed on 1 June 2021).

- Chi, J.; Yu, H. Water electrolysis based on renewable energy for hydrogen production. Chin. J. Catal. 2018, 39, 390–394. [Google Scholar] [CrossRef]

- Bullionbypost.co.uk. Gold Price In USD Per Gram For Last Year. 2020. Available online: https://www.bullionbypost.co.uk/gold-price/year/grams/USD/ (accessed on 1 June 2021).

- Fraser, J. Carbon Gas Diffusion Layers for Fuel Cell Membrane Electrode Assemblies. 2012. Available online: https://nuvant.com/pdfs/Foresight%20Niche%20Analysis.pdf (accessed on 1 June 2021).

| Parameter | Scenario | Year | Scale-Up | Scale-Up |

|---|---|---|---|---|

| 2020 | ×10 | ×100 | ||

| upper | 0.03 | 0.02 | ||

| Electricity cost [$/kWh] [35] | baseline | 0.06 | 0.04 | 0.03 |

| lower | 0.05 | 0.04 | ||

| upper | 55.0 | 55.0 | ||

| Capacity factor [%] | baseline | 34.0 | 44.5 | 44.5 |

| lower | 34.5 | 34.5 | ||

| upper | 90,000 | 150,000 | ||

| Operating lifetime [hours] | baseline | 60,000 | 80,000 | 125,000 |

| low | 70,000 | 100,000 | ||

| upper | 90 | 95 [37] | ||

| Efficiency [% of HHV] | baseline | 80 | 86 | 92.5 |

| low | 82 | 90 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bristowe, G.; Smallbone, A. The Key Techno-Economic and Manufacturing Drivers for Reducing the Cost of Power-to-Gas and a Hydrogen-Enabled Energy System. Hydrogen 2021, 2, 273-300. https://doi.org/10.3390/hydrogen2030015

Bristowe G, Smallbone A. The Key Techno-Economic and Manufacturing Drivers for Reducing the Cost of Power-to-Gas and a Hydrogen-Enabled Energy System. Hydrogen. 2021; 2(3):273-300. https://doi.org/10.3390/hydrogen2030015

Chicago/Turabian StyleBristowe, George, and Andrew Smallbone. 2021. "The Key Techno-Economic and Manufacturing Drivers for Reducing the Cost of Power-to-Gas and a Hydrogen-Enabled Energy System" Hydrogen 2, no. 3: 273-300. https://doi.org/10.3390/hydrogen2030015

APA StyleBristowe, G., & Smallbone, A. (2021). The Key Techno-Economic and Manufacturing Drivers for Reducing the Cost of Power-to-Gas and a Hydrogen-Enabled Energy System. Hydrogen, 2(3), 273-300. https://doi.org/10.3390/hydrogen2030015