1. Introduction

The supply chain of a product refers to all activities between initially sourcing raw materials to the sale of goods to customers, and includes equipment, production, inventory, sales, after-sales service and other matters. Even while companies in the supply chain are accepting orders or conducting operations, there might be funding gaps in their respective production and sales operations, thus forming capital needs. However, most upstream and downstream manufacturers are small and medium-sized enterprises, and it is not easy for them to get loans from banks. The issuer provides financing for the guarantor, resulting in a system of supply chain finance (SCF).

However, SCF is easier said than done. It’s scope is generally divided into cash flow management, financial instruments, and buyer-to-pay solutions [

1,

2]. And it’s complexity being clear from twelve categories of financial instruments [

3], and from the horizontal and vertical relationships in the supply chain [

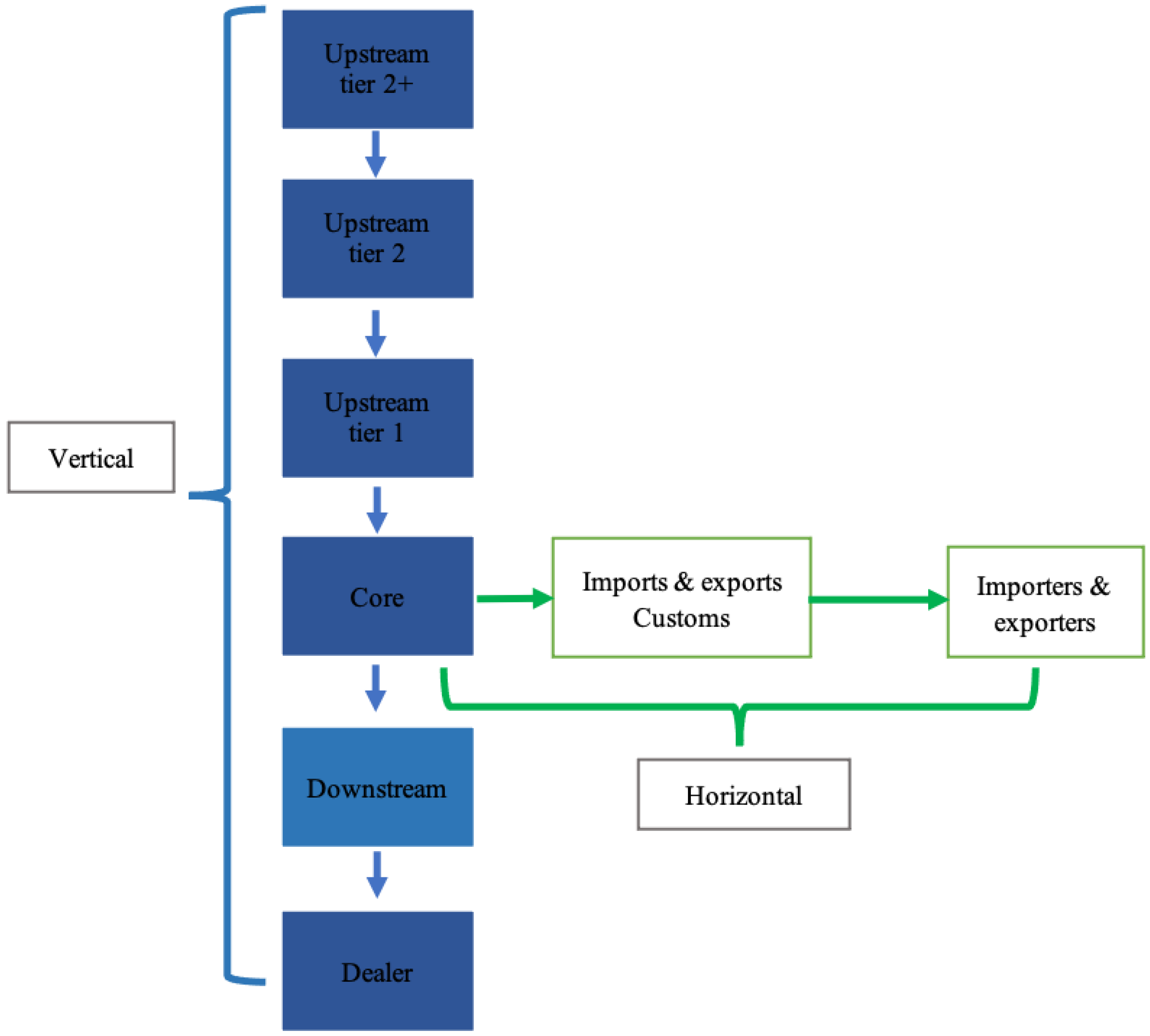

4] (p. 5), as shown in

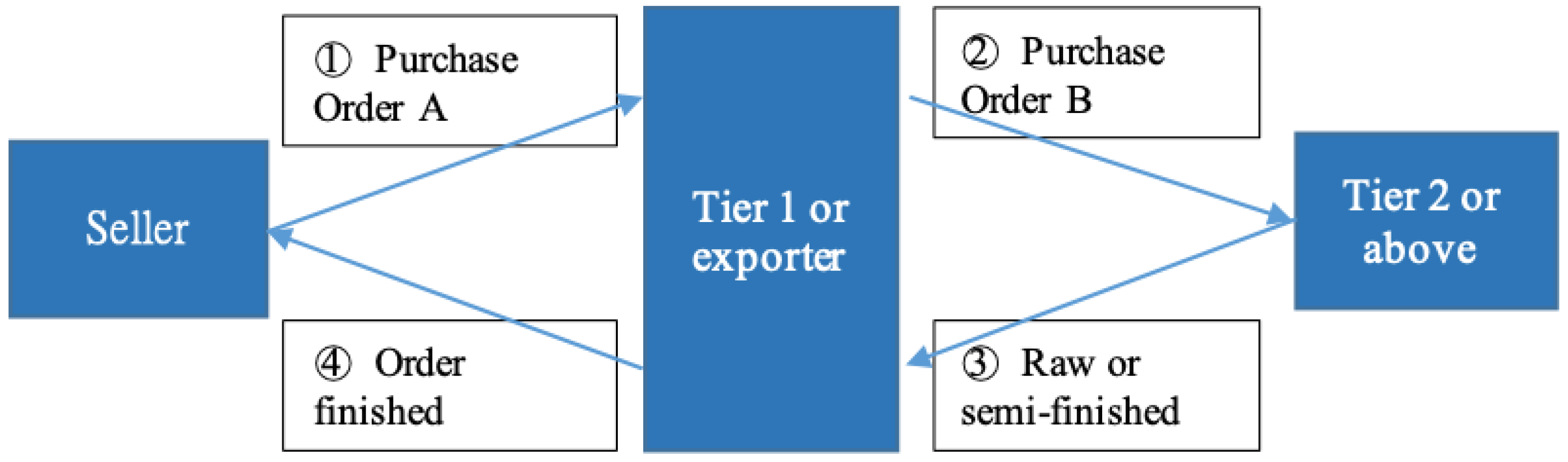

Figure 1.

The vertical relationship is also portrayed as N + 1 + N. The first N is the upstream manufacturer, 1 is the core manufacturer, and the second N is downstream manufacturer or distribution channels. The types of SCF in the vertical relationship include receivables purchase agreements, loans and prepayments [

5]. There are also three other types according to the specific supply chain process: purchase order financing, inventory financing, and accounts receivable financing after delivery happened [

3]. In addition, letters of credit and bank guarantees are used in international trade which are classified as horizontal relationships, and which can improve the enabling framework of SCF [

5]. The vertical and horizontal relationship increases the difficulty for financial institutions to clarify the relationship with core enterprises in financing, and reduces the willingness of core enterprises to guarantee supply chain manufacturers, reducing the overall effectiveness of SCF. The solution proposed in this study, is applicable to the relationships as shown in

Figure 1, and covers the cash flow management of the supply chain.

Figure 1 shows that there are many participants in SCF. Therefore, the financial industry expects core companies to act as guarantor and expects them to reduce the default risk. However, the difficulty of verifying the transfer of claims, easily leads to fraudulent claims and an increase in social costs. In addition, insufficient information also creates obstacles for legal compliance, accounting and transaction costs.

To improve the transparency of information, some scholars have begun to propose solutions by means of blockchain and securitization [

6,

7,

8]. Blockchain technology has become famous since it was first applied to Bitcoin transactions in 2013. It is characterized by the fact that the recorded peer-to-peer information cannot be forged and tampered with, and is easy to trace [

9]. Ethereum proposed the use of smart contracts, which provides a programming language to write programs. After compiling and deploying virtual machines on each node, the nodes of the blockchain can be used to execute the functions in the program or change the state of the blockchain, with that creating an open ledger [

10].

Theoretically, through the use of game theory, Dong [

11] argues that blockchain technology can improve the visibility of deep-tier financing (higher than the tier 2 in

Figure 1). Choi [

12] applied the Nash bargain model to prove that blockchain-enabled supply chains have lower operational risks than traditional supply chains, and that suppliers will benefit from blockchain-based supply chain financing. For practical use, Hofmann et al. [

6] studied blockchain-oriented reverse financing mechanisms (Reverse Securitization), Lahkani [

13] combined the blockchain with the e-commerce supply chain to achieve a simplified supply chain, Chen [

14] provided a framework for implementing SCF for the automotive industry, Tsai et al. [

15] studies the use of elliptic curve cryptography as a security mechanism of SCF in the agricultural industry, which is actually a blockchain verification methodology, lastly, Du et al. [

16] proposed a blockchain-based SCF platform system.

Supervisory agencies, international institutions, and scholars study affirm that the application of blockchain in supply chains make sharing of information possible, and that it can be more efficient for parties new in the financing industry [

17,

18,

19], can facilitate international payments [

20], automate transactions, duplicate financing and secret protection [

21]. In practice, FNCONN Financial [

22] issues “Fujin” as a payment commitment and combined with Chain Finance issues “FP” Tokens in the form of a consortium chain as debt certificates (credit asset certificates).

However, the decentralized nature of the blockchain, coupled with the application of internet, reduces the intermediary role of banks. Currently, to assist small enterprises in financing, peer-to-peer/person-to-person (P2P) lending through internet or e-commerce platforms, has been put to use in SCF, for example: Ant Financial Services, Zopa UK, The Receivables Exchange USA etc. However, as unspecified persons are being served, identity verification, personal information protection or money laundering prevention and control are all the difficult issues or even obstacles, resulting in a dilemma between supervision on one side and inclusiveness on the other side [

23]. As a matter of fact, it is confirmed that reducing the quality of financing does bring a lot of drawbacks to the P2P financial lending platform [

24]. With that the issue of legal compliance begins [

25,

26].

Therefore, this study believes that the current use of blockchain for SCF still requires three issues that need to be solved. First, current research [

13,

14,

17] focuses on the passive nature of using the blockchain in log records, which fails to use the advantages of smart contract programs to issue and operate tokens. Second, the application of blockchain in SCF mostly adopts permission-based (or membership-based) consortium chains [

14,

16,

27], which limits the inclusiveness, and the credibility of the system because of the limited number of nodes. Third, is the feasibility of blockchain in SCF, including its cost-effectiveness and legal nature.

In addition, asset tokenization becomes popular recently, either physical assets or intangible assets. Tokenization is a technology that allows the representation of real-world assets in a digital form on a blockchain network [

28]. These tokens can then be traded on a blockchain network, allowing for improved liquidity, fractional ownership, and reduced transaction costs. To achieve this, tokenization and operations require the use of smart contracts mentioned in the above, such as ERC-20 [

29] or ERC-721 [

30]. In this article, we tokenized the obligation conditions of debt, and the right conditions of investment which is called conditional token. The conditional tokens are used to solve the issues in SCF.

Concluding the above, conditional token is defined mathematically and issued and driven by operations proposed in this research. All can be written down in smart contracts and deployed on the public blockchain, not only to record the specific conditions of using these tokens, but also for the purpose of transferring among different tiers of manufacturers as to achieve N + 1 + N, and can even act as account receivable or accounts payable in line with common accounting principles. In addition, the public blockchain is the most credible, and can therefore improve credibility of users in its P2P architecture thus achieve a higher inclusiveness. For practical purposes, this article discusses the legal nature of CT, as the “verdinglichung obligatorischer rechte”, introduces a risk management tool, and proofs that a system which uses CT is more cost-effective than current banking practices.

For illustration and implementation purposes, the related smart contracts are deployed on the testnet as shown in the

Appendix A, the system has finished a proof of concept, as well as participated in the competition in which it achieved good results (the First prize of Academia and Industry Collaboration, ITeam PRI-08, International ICT Innovative Service Awards,

https://innoserve.tca.org.tw/en/guidelines.aspx, access date: 1 March 2023).

The remainder of this article is organized as follows,

Section 2 introduces and reviews the articles of blockchain, smart contract, and tokenization.

Section 3 explains the issuance, conditional and operational functions of CT’s.

Section 4 describes how to apply CT’s for the purpose of SCF.

Section 5 analyzes the feasibility of practical operations, while the conclusions and recommendations are being given in the final section.

3. Conditional Tokens

This section will explain the definition of CT’s in both a mathematical and descriptive manner, as well as through the operation (aka functions) and operation processes that are being used. The smart contract is deployed in the blockchain by using an unique address, all of its functions will be driven by the system’s backend and the results can be saved in a transparent manner on the blockchain.

3.1. Definitions

Define is the ith condition is the set of all “conditions”, and is the power set of C.

Definition 1. An activated function , we called is activated or achieved if , and is called a conditional token (CT), denoted by .

In computer, CT can be programmed as the structure type as in

Table 1.

In addition, define , for the purpose of completeness, and is called currency token which is equivalent to fiat currency.

CT is a struct or vector type, it cannot be operated or measured by the current standard such as ERC-20 [

29] or ERC-721 [

30], thus operations or functions are requires to measure and operate CT. By the way, an address is required for the ownership of CT. The address in blockchain represents the account as well as the public key of the token holder, let

be the set of all the addresses in blockchain.

Definition 2. and is the total number of that belongs to address a.

In this article, a time index is used, to specify different times if needed. Besides, is the total number of currency token or of fiat-backed currency of account a. For convenience, we define for currency token .

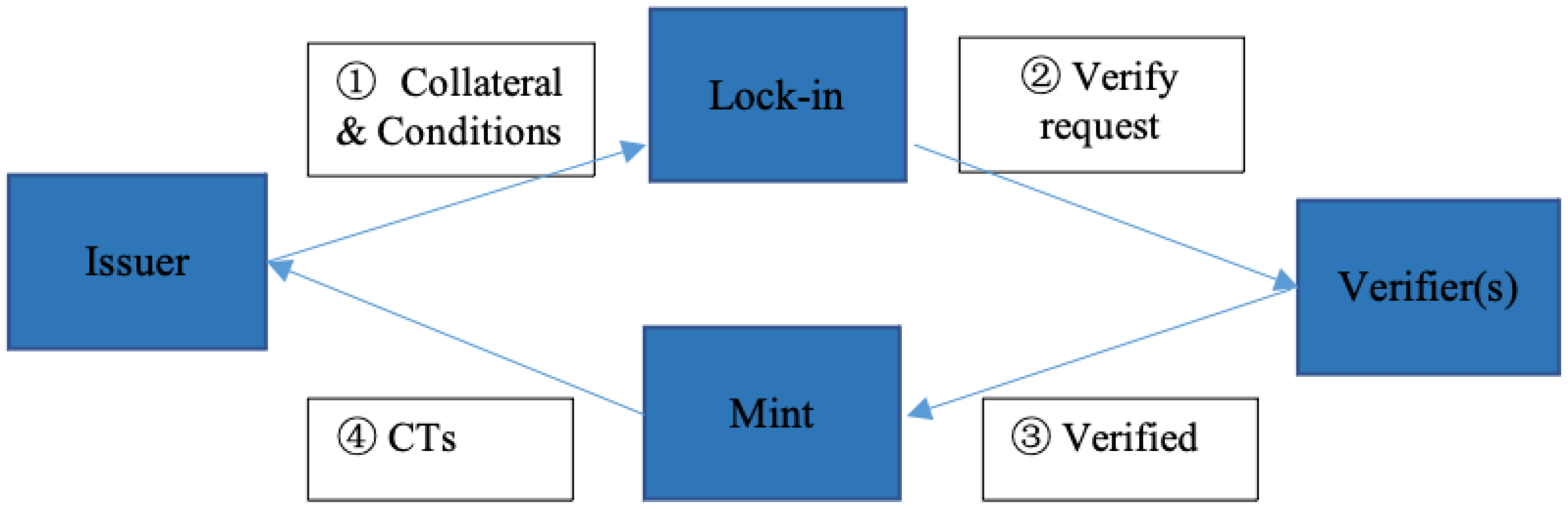

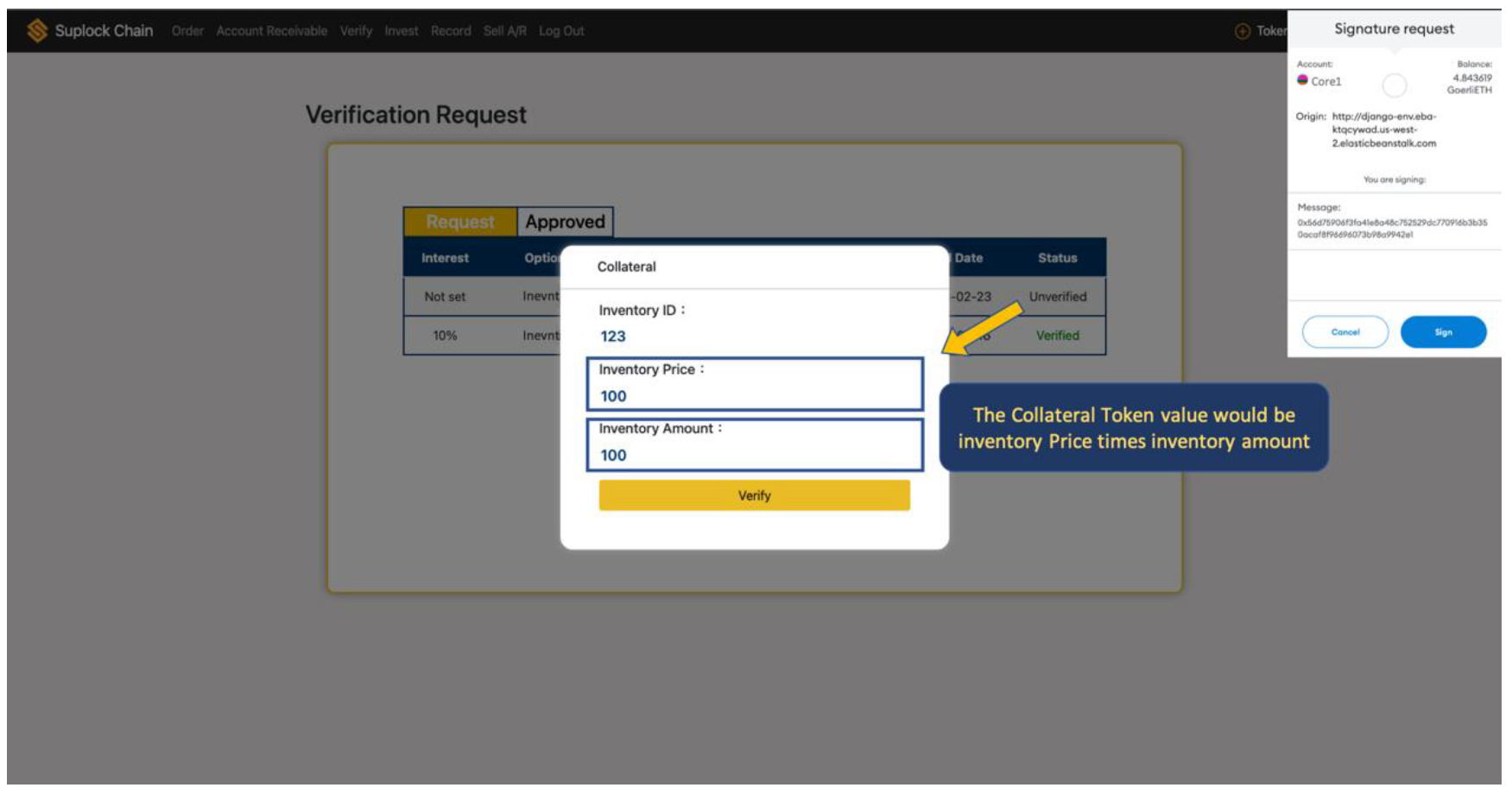

In practice, two types of CT are used, one is an obligation-type, the other is a right-type. For the obligation-type, there are two processes of issuing (aka tokenized collateral), with the first process locking-in collateral. It is very convenient for crypto collateral, however IoT devices are required for physical collateral, which is not address in this paper. Then, as the second process, CT’s backed by collaterals are minted.

Figure 2 shows the process of issuing the obligation-type CT, the demand (issuing) side requests to set mortgage as collateral tokens and provides the specific loan conditions, where the collateral tokens are held in smart contracts (①). If the collateral tokens are created by a third-party such as ETH, or need to be evaluated by a third party, then verification from a third party is required (②). After the verification is completed (③), the smart contract issues/mints a predetermined number of CT’s (④).

The above-mentioned custody mechanism is to transfer the collateral to the address deployed in the smart contract, which is equivalent to “locking in” the collateral as a trust mechanism. The protocol of “lock” or “unlock” can apply or revise ERC-1132 [

68], however, this will not be addressed in this article.

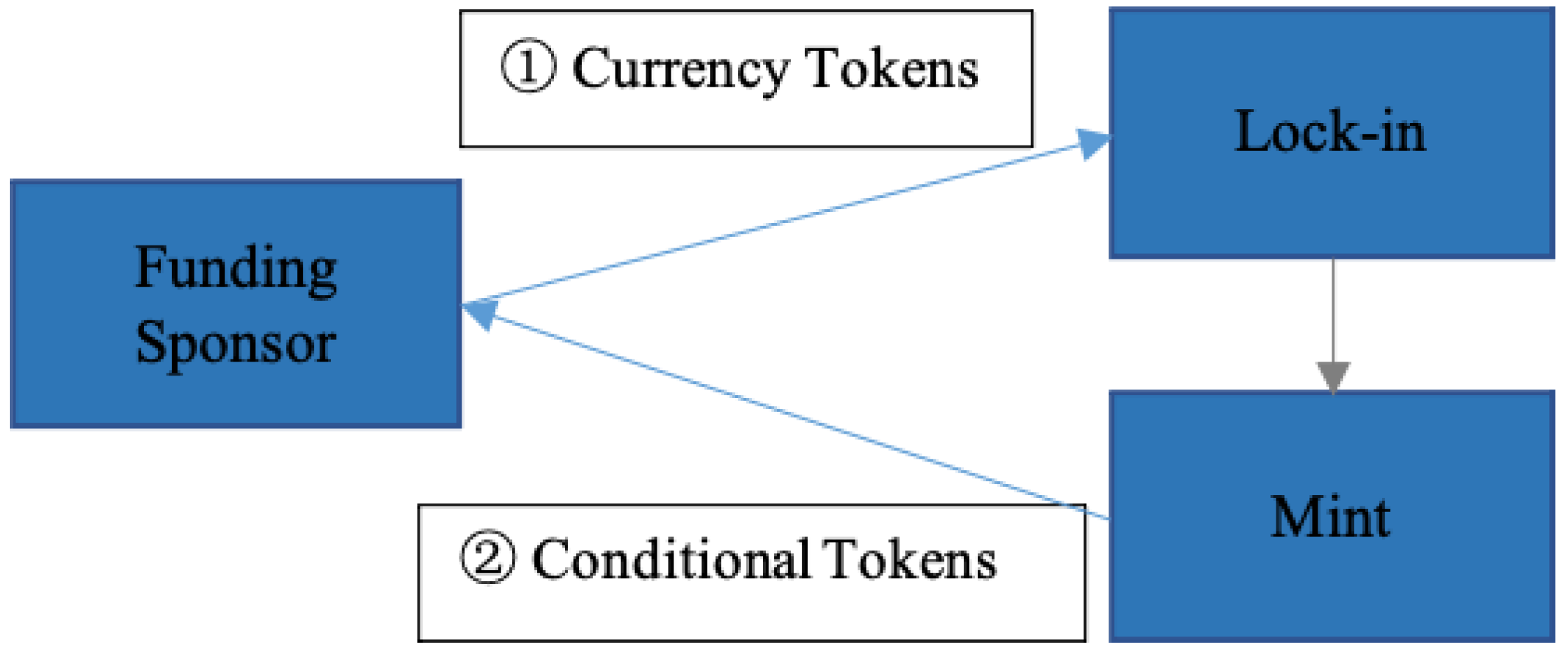

Similar to the obligation-type, there are two processes of issuing right-type CT, depositing fiat currency to receive account tokens (aka collateral in obligation-type), then transfer account tokens to the “lock-in” address, followed by deciding the “rights”. The first process can be done by an application program interface (API) from a third-party payment or bank service. The smart contract will issue the account tokens to represent the fiat currency after a successful deposit.

For the second process, the supply side transfers account tokens (①), locks them into the smart contract, then applies the mint function of smart contract to issue the conditional tokens (②) according to

Figure 3. The operations are similar to the obligation-type CT.

Definition 3. Mint function of account a, increase the amount of CT’s from the CT balance of a with the same conditions as E. That is, .

The mint function is used to issuing of CT’s. If the number of m is minted for address a of CT, then add amount

to

T, the use case for “mint” are illustrated in the

Appendix A.

Based on the definitions and the mint operation mentioned above, CT’s are minted (or issued) by a smart contract, while the (either obligations or rights) conditions are confirmed and recorded on the blockchain. When the CT is used, the agreed conditions are achieved. In other words, the use of CT needs to fulfill (exercise) the agreed obligations (rights) at the same time.

Simply put, the obligation-type CT is divided into three types: inventory CT’s (inventory backed), pledge CT’s (backed by something other than inventory) and margin CT’s (cash backed). The right-type CT’s are called investment CT’s.

3.2. Conditions

The scope of conditions includes, but is not limited to, interest rate, term, and restrictions on transfer manufacturers, donation criteria, etc., and are determined by the issuer, fund providers based on the funding purposes or are based on market conditions.

Naturally, because conditions must be fulfilled to be valid, there is no need to assume conditional responsibility until they are fulfilled. Thus, for interest rate conditions, the obligation-type is a divisible Line of Credit Mortgages (detailed in

Section 6.1), or a CT equal to a mortgage with a one-unit limit. The maximum amount of mortgage rights is the number of CT’s issued after the mortgage is created.

Issuers who transfer CT’s to upstream or downstream manufacturers can change the “conditions” or “terms” according to their own needs and can provide different conditions to different manufacturers. In addition, they can also limit the number of times the conditions can be transferred.

For the right-type CT, the fund providers can decide on a certain set of conditions, such as the minimum rate of return, and determine the conditions once more through matching, or directly select and agree on the conditions in advance. Similarly, the rights cannot be exercised until the conditions are fulfilled.

Therefore, the conditions can be an investment tranche with different returns, with each CT acting like a divisible fixed-income bond.

3.3. Operations

Besides minting, we will define more operations used for CT, including exchanging, transferring, modification, and burning.

Operations are the functions in smart contract which changes the state of blockchain.

Definition 4. The exchange function is an operator that projects from to currency token X, so that , where is the exchange rate for one CT to currency token X, and , .

It means if CT exchanges to X, then E is activated, meaning, all of the conditions in E are achieved.

Definition 5. The transfer function , so that , transfer amount of CT’s from address a to address b.

Definition 6. The modification function , where , .

After modifying account a, decreases, and increases.

Definition 7. The burn function of account a decreases the amounts of CT from the CT balance of a with the respective condition E. That is, .

All the functions or operations are programmed in the programming language Solidity and represent the smart contract [10].

Summarize the functions as in

Table 2.

4. The Application of CT to SCF

SCF is divided into three categories: loan or advance payments, purchase of receivables, and bank payment obligations [

5].

The third category is mainly for enabling the SCF, one of the management processes, and is not within the scope of this paper. This article will apply CT’s to the first type of accounts receivable (aka factoring and forfaiting), and the second type of advance funding and inventory financing, with purchase order and distributor financing being part of advance funding.

4.1. Advance Funding

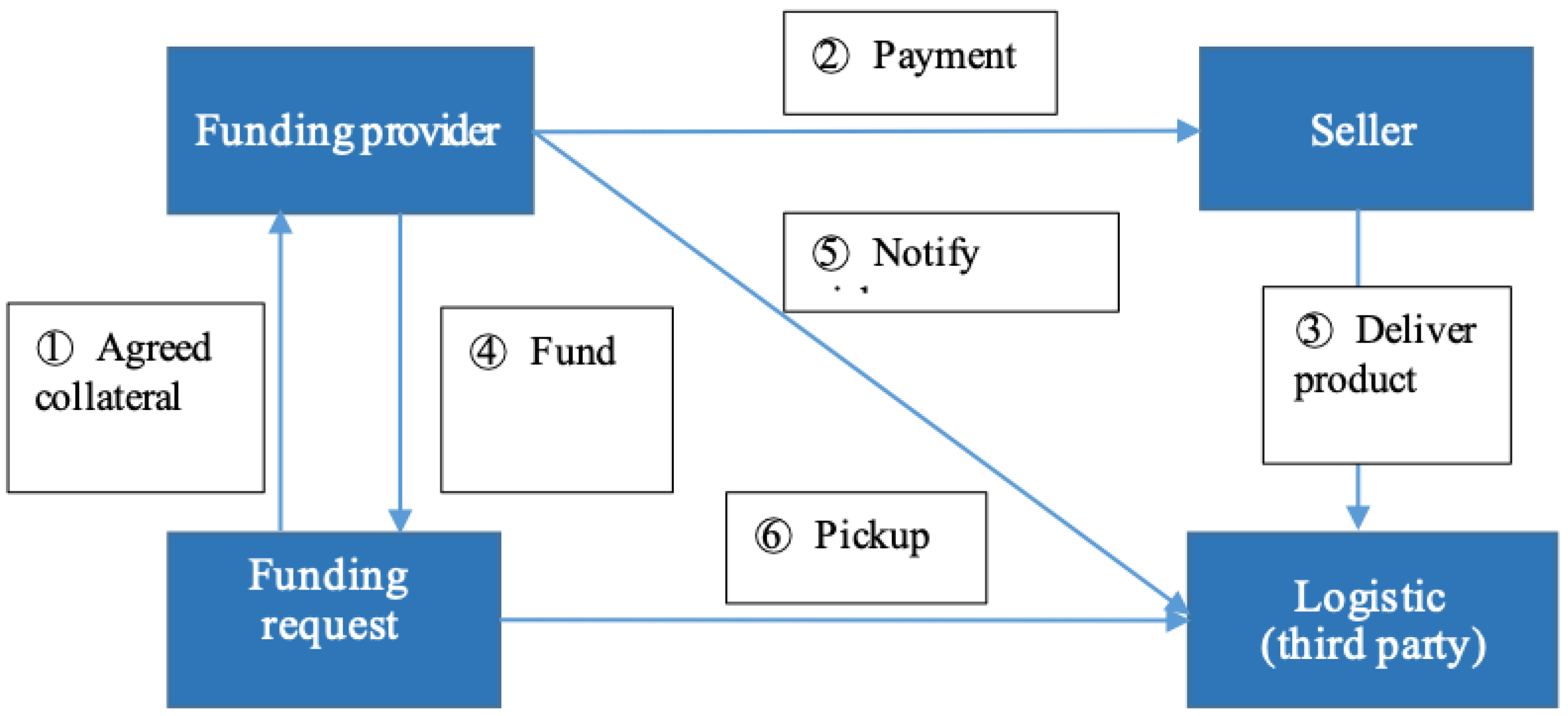

Traditionally, the buyer pays in advance for the goods, however has not yet received the goods for sale or needs an early planning of its sales, resulting in a funding gap, therefore, it secures it financing by using “future trade receivables” as guarantee (Forum, 2016), which is called channel financing in case the buyer is a channel distributor. In practice, in addition to future trade receivables, it also includes the right to take future delivery of goods, or the bill of lading certificate when the goods are delivered, or picking up the goods in a third-party warehouse, and use the sales receipt to first repay the financing service (see

Figure 4).

On the other hand, if the seller receives a purchase order for goods, but has not yet received cash before the product or delivery is finished, the situation results in a gap in raw material funds, leading to the purchase order being similar to the “future trade receivables” as described above (Forum, 2016). Such a situation is called purchase order or pre-shipment financing.

Regarding channel financing, in addition to risks in repayment arising due to poor sales performance, if the buyer were to be the core company, and already collateralized its inventory, then the downstream dealer can no longer obtain financing through using the same collateral.

Purchase order financing is based on the demand for funds in the entire process from placing an order until payment is received. The “future trade revenue “ of the order is used as the source for loan repayment. However, because there are many upstream levels involved (

Figure 1), transmission or passing on of information limited, resulting in the highest risk in this way of financing, which presents an excellent opportunity for CT’s. The basic architecture is shown in

Figure 5.

If CT’s are used, no matter whether for channel or purchase order financing, they can replace the collateral agreed upon by both parties as shown in

Figure 4, because we assume core company has proof of credits already. That is, mint CTs form core company to funding requester a, and then transfer them to another company b. The operation will be

, where m is amount of CT.

For channel financing, the CT is provided at the same time the sale happens, helping the dealer solve the funding problem caused by repeated pledges. For purchase order financing, the deposit can be either cash or currency tokens. Manufacturers who accept the CT can exchange it for capital, or transfer it to other manufacturers, basically solve and mitigate the risk of multi-level information transmission of purchase order financing in a system as portrayed by

Figure 1. In addition, it is also possible to reset the conditions and limitations of manufacturers, such as: interest rate or term adjustment, included companies, or limit the number of suppliers, etc.

The processes and the operation algorithm of advance financing are listed as Algorithm 1

| Algorithm 1 The processes and the operations of advance financing |

- 1.

Input core company address a, then calls mint function

. - 2.

Input channel address b for channel financing, or input manufacturer address b for purchase order financing, then the core company calls transfer function

to transfer n CTs to address b, where

(when placing purchase order to b, for purchase order financing) - 3.

Address b can either exchange CTs to currency or transfer them to another company.

If transfer is true, then input manufacturer address c, and calls modification function to modify the required conditions, and then call to transfer k CTs to address c, where . |

| Algorithm 2 The processes and the operations of inventory financing |

- 1.

Input collateral company address a, after validate the inventory, then calls mint function

. - 2.

Address a can either exchange CTs to currency or transfer them to another company address c:

If exchange is true, then calls exchange function If transfer is true, then input address c, and calls modification function to modify the required conditions, and then call to transfer k CTs to address c, where .

|

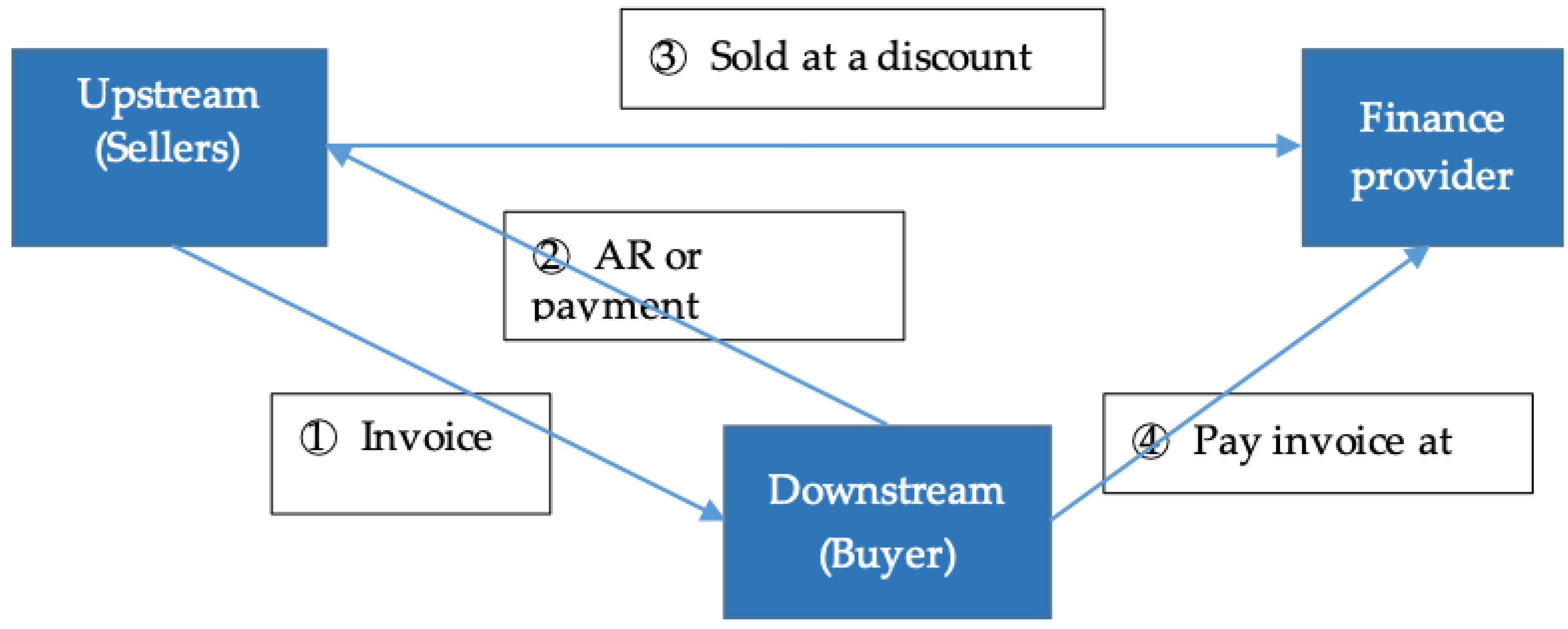

4.2. Purchase of Account Receivable

After upstream companies (or exporters), being the sellers, complete the order and ship the goods to the core company (or importer), while the buyer did not pay upon delivery, it will create accounts receivable (AR) that are received by the seller. The upstream manufacturers (or exporters) can use this AR for financing by selling all or a part of it to a finance provider [

5], as shown in

Figure 6.

If AR is sold directly, it is called factoring, with the fund provider being called factor. If the buyer issues a payment instrument such as a post-dated check to the seller, which the seller in turn sells to a fund provider, it is called forfaiting, with the fund provider being called forfeiter.

AR financing discounts short-term financing, which accountant can easily hide. It will be even more difficult to verify if second-tier or above manufacturers are involved. In practice, there are cases where the accountant letter is incorrect or even appears to be a scam (98-Jin-3, Taiwan Shilin District Court 2015, after line 137).

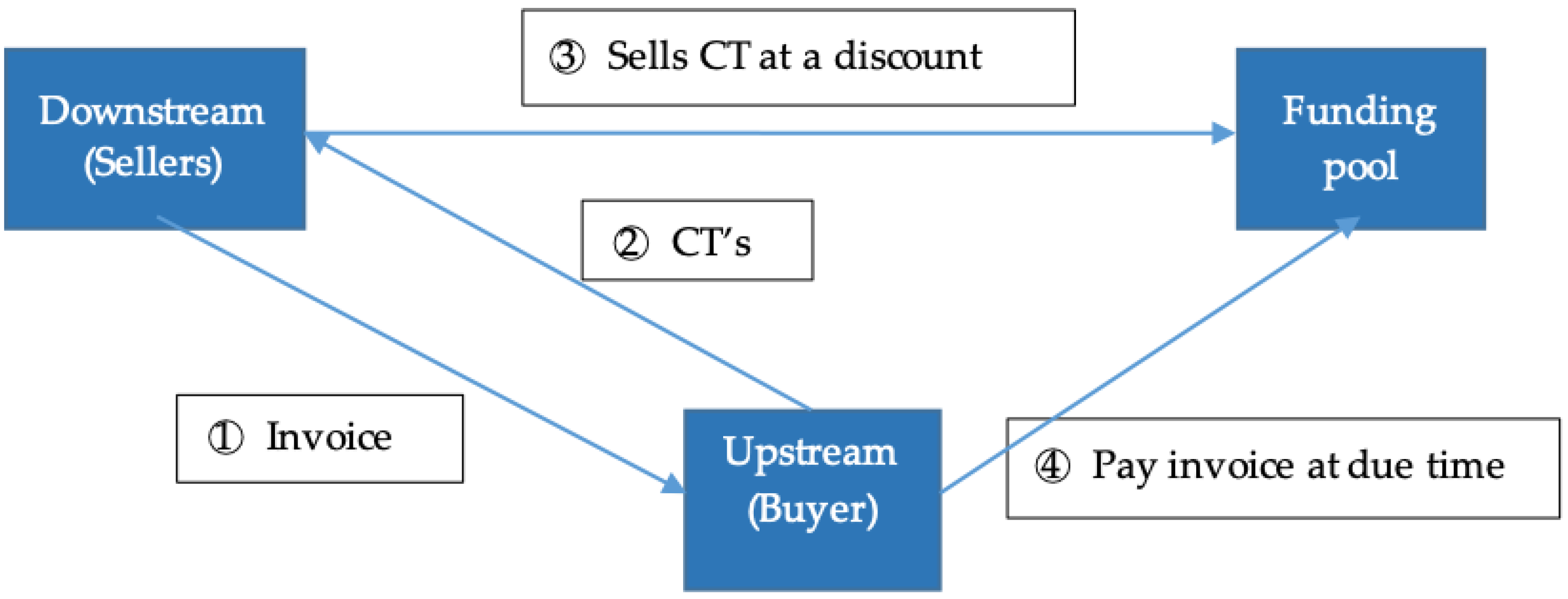

Figure 7 shows the structure in which CT’s act as accounts receivable. The process is similar to

Figure 6, and the algorithm is in Algorithm 3. The difference is that the CT’s are used as accounts receivable or as a payment instrument of the buyer, so that the sellers (upstream) can sell the CT’s to fund providers. Sellers can also use the tokens as AR or payment instruments when dealing with higher tier manufacturers, and can modify the conditions of the CT to reflect time value (discount) and the respective expiration date, waiting until expiration date, or to show the CT to claim payment for the goods. The transfer process of the CT will be recorded in the blockchain where anyone can verify it and thus know whether the information is correct or not.

| Algorithm 3 The processes and the operations of purchase account receivables |

- 1.

Company address a, check the CT amounts, calls balance function

. - 2.

Address a want to sell m CTs to address b, where

then

address b transfer m currency token X to address a. address a call to transfer k CTs to address b.

|

Here, for the upstream manufacturers, the conditional tokens are equivalent to the traditional bank checks for AR, and thus can be used as a proxy for AR, while core company can the conditional tokens as proxy for accounts payable. The discount price is part of the conditions. Even so, it still needs to meet accounting principles, however this is beyond the scope of this study.

4.3. Inventory Financing

Inventory financing uses inventory of raw materials, semi-finished, and finished goods as collateral to obtain capital [

5]. The use of blockchain technology can reduce the risk of double loans or goods sold [

16].

The CT is obtained by using the inventory as a collateral, and it requires to be verified and evaluated before issuing as in

Figure 2. Because information of the CT is recorded publicly, it is easy to do verification. The core company can use the CT for itself or transfer the CT to other companies. In practice, it can be transferred to upstream manufacturers as accounts receivable (

Figure 7), or provided to downstream manufacturers, such as distributors (

Figure 5). Except using inventory as the collateral, the remaining operations are similar to Algorithm 1, and list in the Algorithm 2.

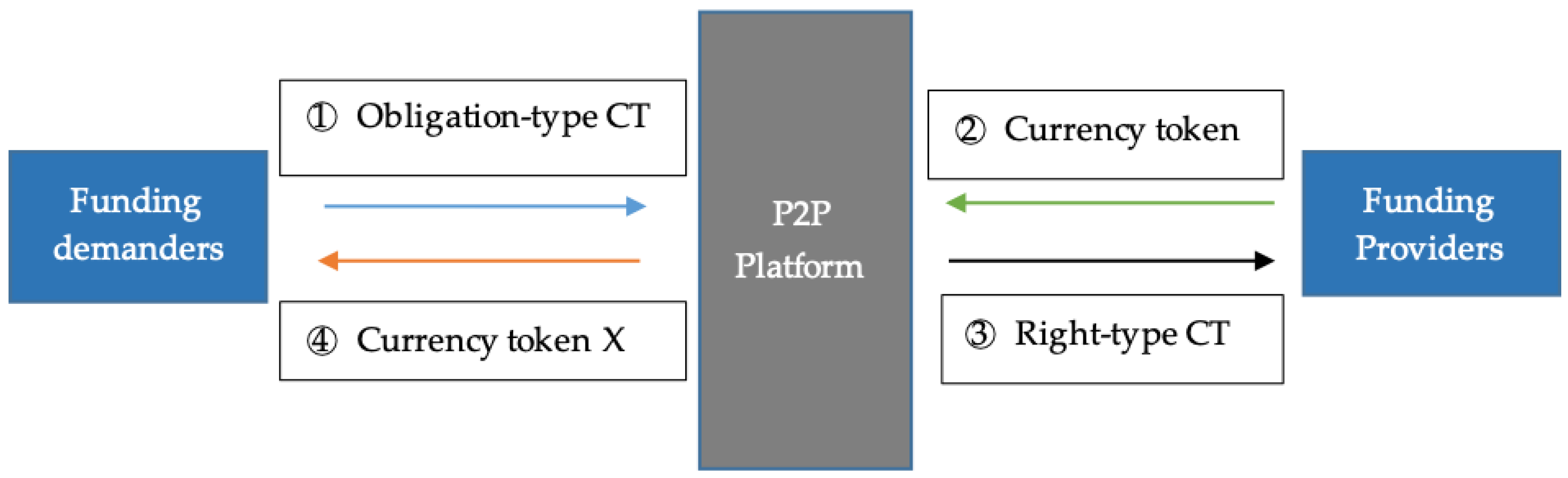

4.4. Peer-to-Peer/Person-to-Person (P2P) Financing

In P2P financing, it requires to distinguish obligation-type and right-type CTs, uses of the indices denoted by and , respectively.

’s holders want exchange currency from the currency token holders by P2P financing and the investors deposit currency token X to swap

for condition

. The relationship is in

Figure 8 and the algorithm as below Algorithm 4:

| Algorithm 4 The processes and the operations of P2P financing |

- 1.

’s holders address , call transfer their CTs to platform address b, where is the transfer amount of address , for - 2.

Platform revised condition

of , and shows the investment terms conditions of listed s - 3.

Investors address

deposit cash or transfer currency token for - 4.

Investor

selects of , and will provide of currency token to fund , where J is the investors who selects , transfer of X to platform, and platform calls mint with condition , then call to transfer to investor j. - 5.

If

, the platform transfers of X to address . - 6.

Payment from

will exchange to currency tokens and then transfer to , based on the . - 7.

Redeem from

, the platform calls burn , and return of currency token to

|

5. System Design and Implementation

Some research proposes a SCF system based on the consortium chain [

14,

16]. This study concludes that the functions of the front-end of the SCF system include user interaction, Internet of Things interaction and third-party control functions. The back-end services include data management functions and blockchain management functions. The latter being the functions of a smart contract in which the interactive function of the IoT is used as a sensing device to convert physical collateral into crypto collateral or crypto tokenized assets. This article will not cover this topic in depth. The benefits of the public blockchain proposed in this study, is that no consortium chain [

14] and consensus agreement system [

16] needs to be build.

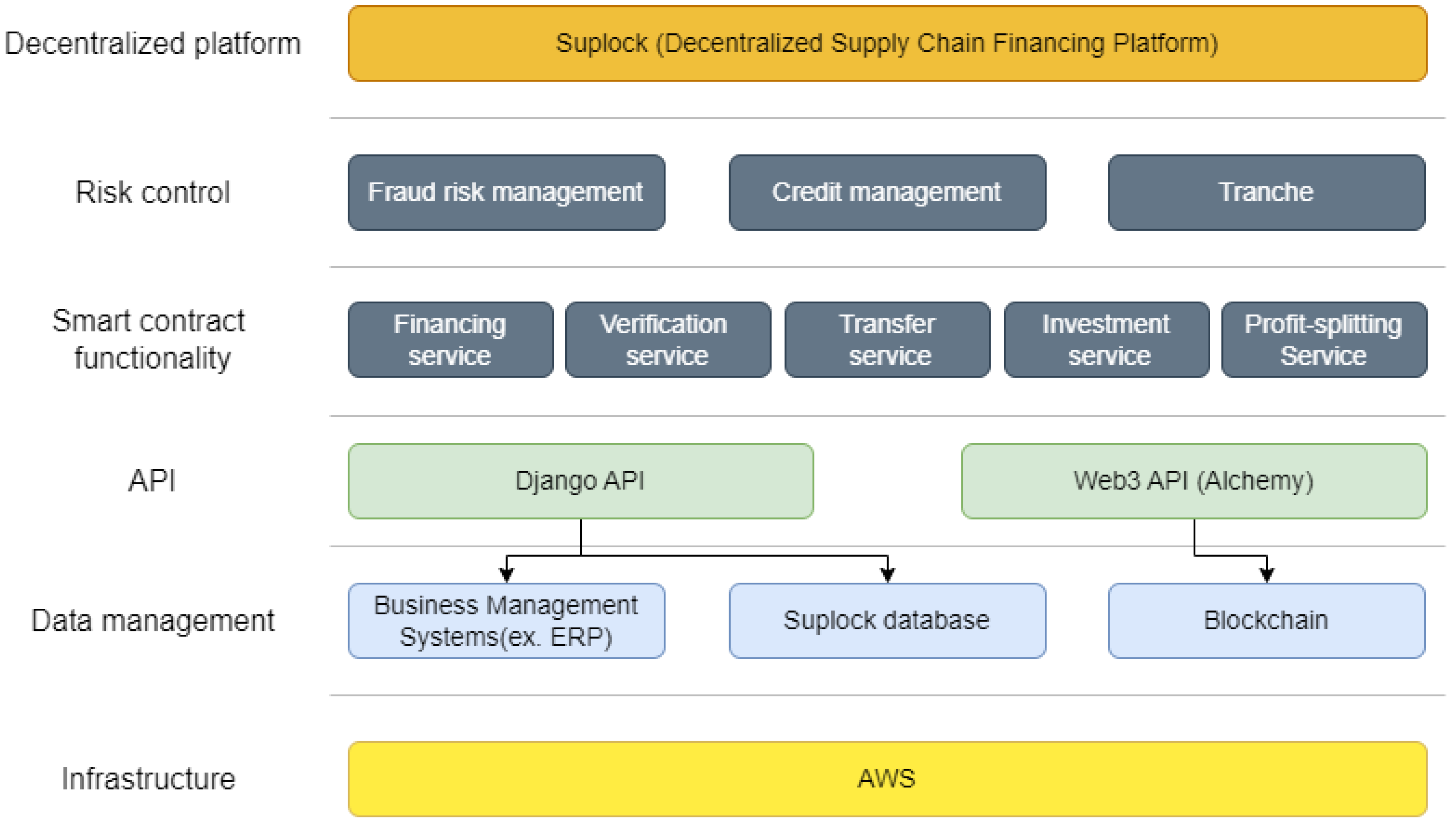

5.1. SCF System

Below figure depicts the structure of SCF system. It could be hierarchically divided into six layers as shown in

Figure 9, and each layer makes full use of the functionality and module provided by its below layer. The infrastructure layer utilized the platform as a service (PaaS) which is provided by a third party provider, such as AWS EB (the Elastic Beanstalk of Amazon Web Service) which is used in this article. It makes the most of capacity provisioning, load balancing, scaling, and application health monitoring. On top of the infrastructure layer, we integrate multiple data sources in the data management layer. The business management system provides data flow regarding supply chain transaction records, the database of this system defines the interface and the relation between data received from management systems and user input, and the blockchain serves as authenticity and validity of information flow. To manage the data, we suggest IoT devices or Application Interfaces (APIs) in the API layer to communicate between corporate’s Enterprise Resource Planning (ERP) system and the blockchain, where ERP provides the information of collateral. With the manageable data flow, the services are proved by a series of smart contracts which are deployed in the public chain in the layer of smart contract functionality. Risk control layer supervises the financing activities, and delivers a set of risk management methods.

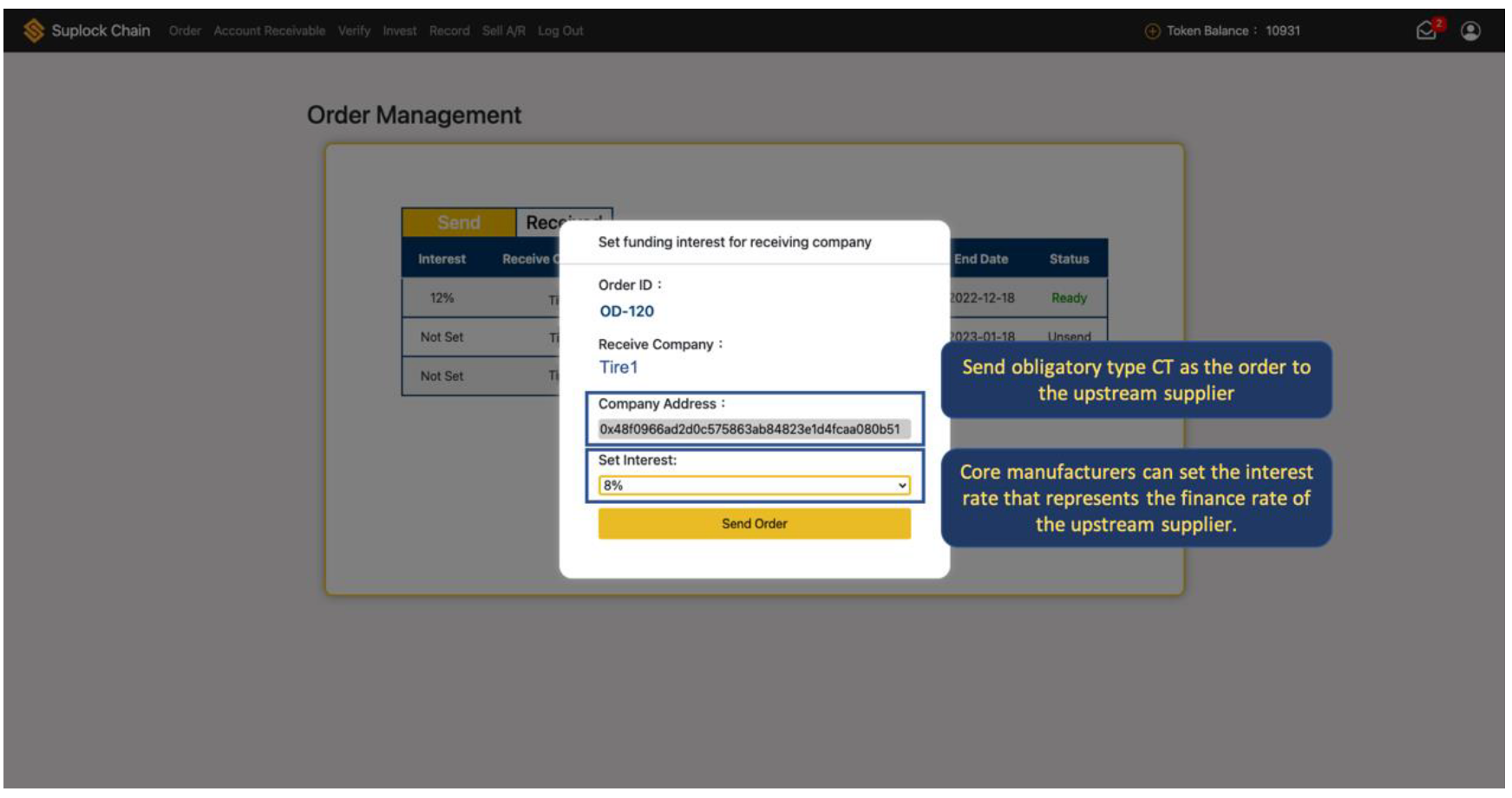

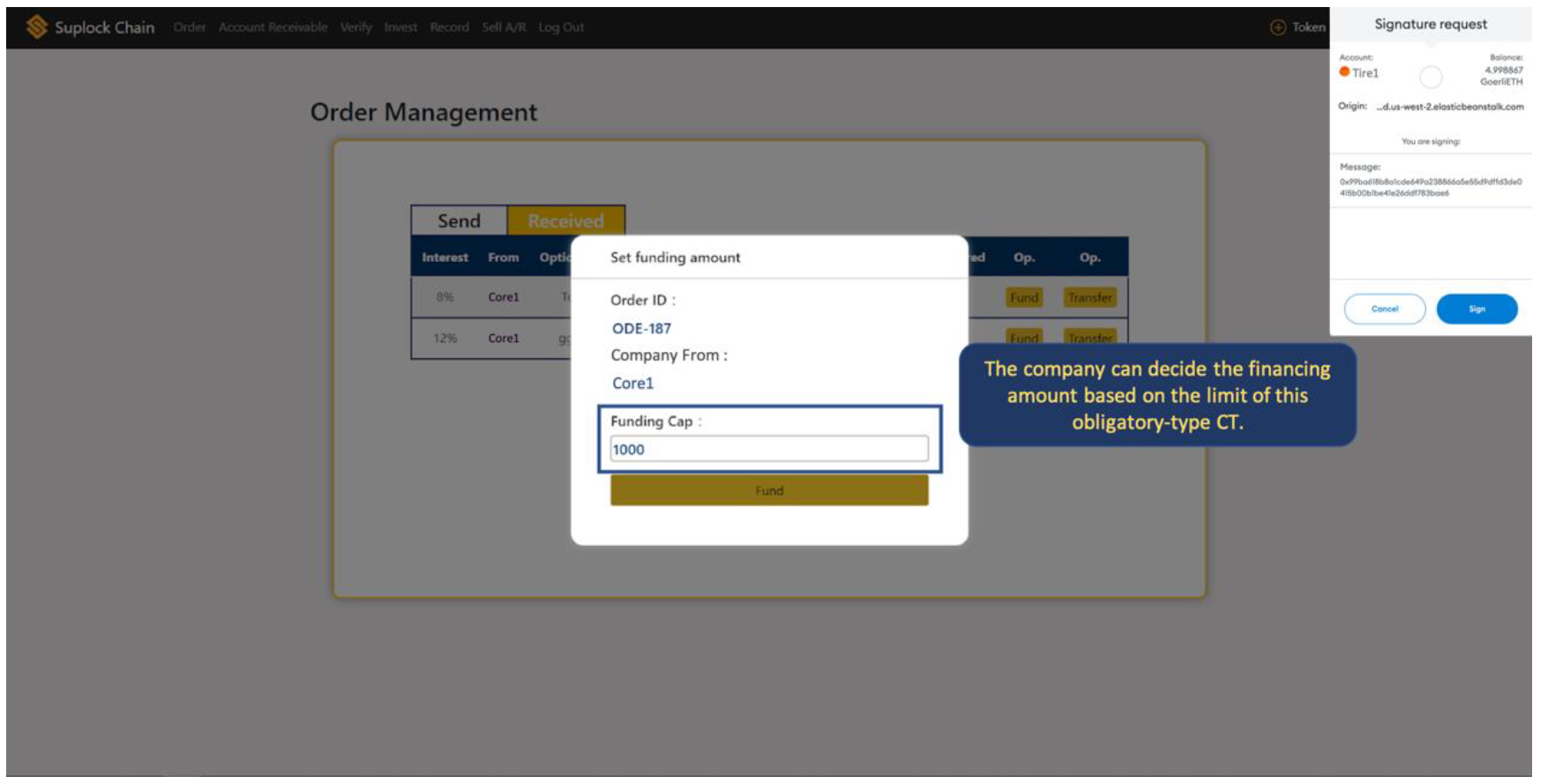

The website of SCF system is under testing, and the examples of operations are illustrated in

Appendix A [

69].

5.2. Blockchain and Smart Contracts

Blockchain is a peer-to-peer decentralized mechanism [

9], making it very suitable for the internet community (P2P, person-to-person) network platforms, or in other words many-to-many social network platform. There is no universal definition of smart contract, in general, a smart contract is an agreements or a transaction protocol which can be written by computer program to automatically execute, control or document events and actions according to the terms of a contract or an agreement [

70].

In this study, four smart contracts are deployed for the account of currency token (introduced in Definition 1), the operations of CT, verification and for the investors.

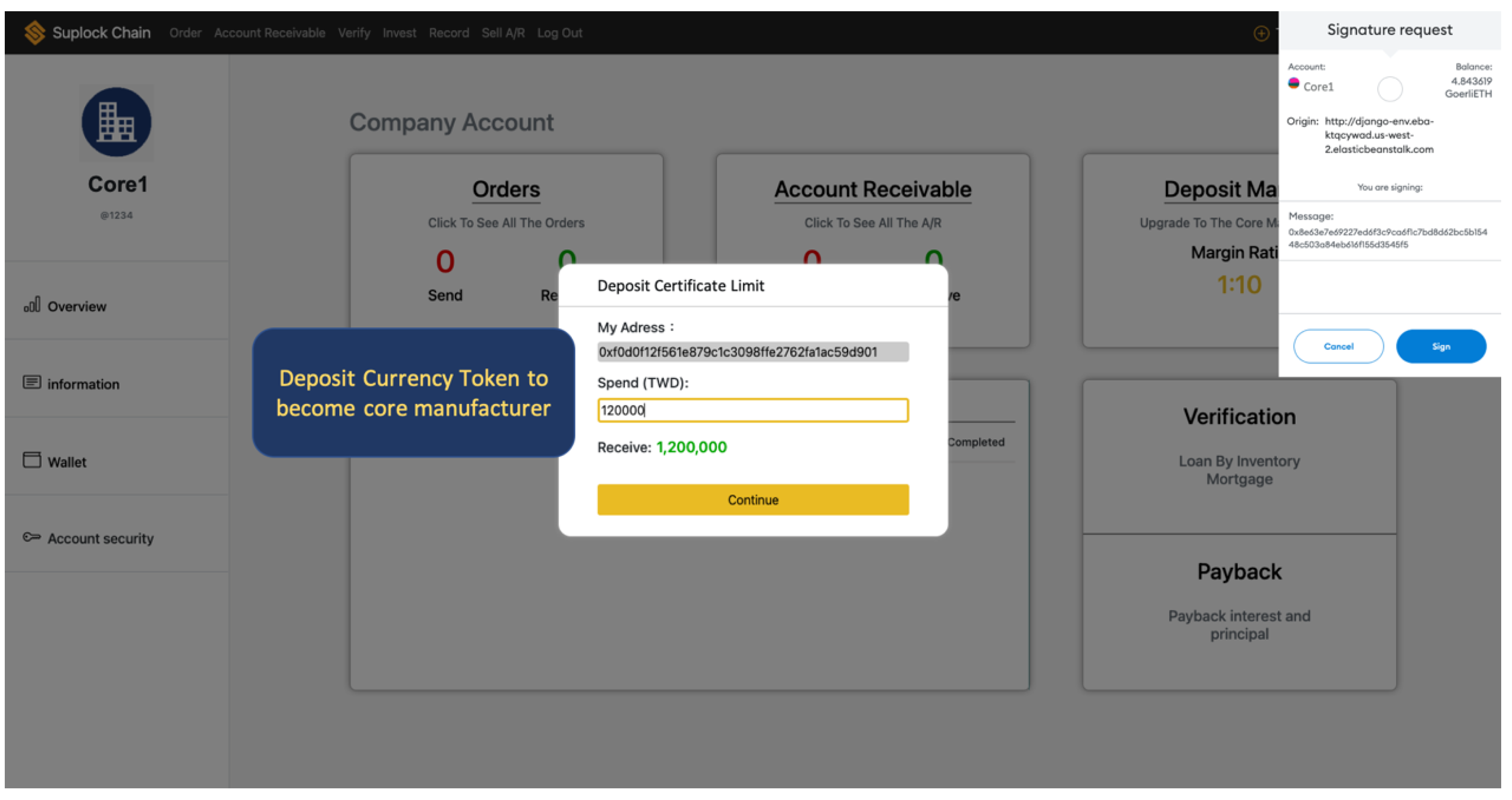

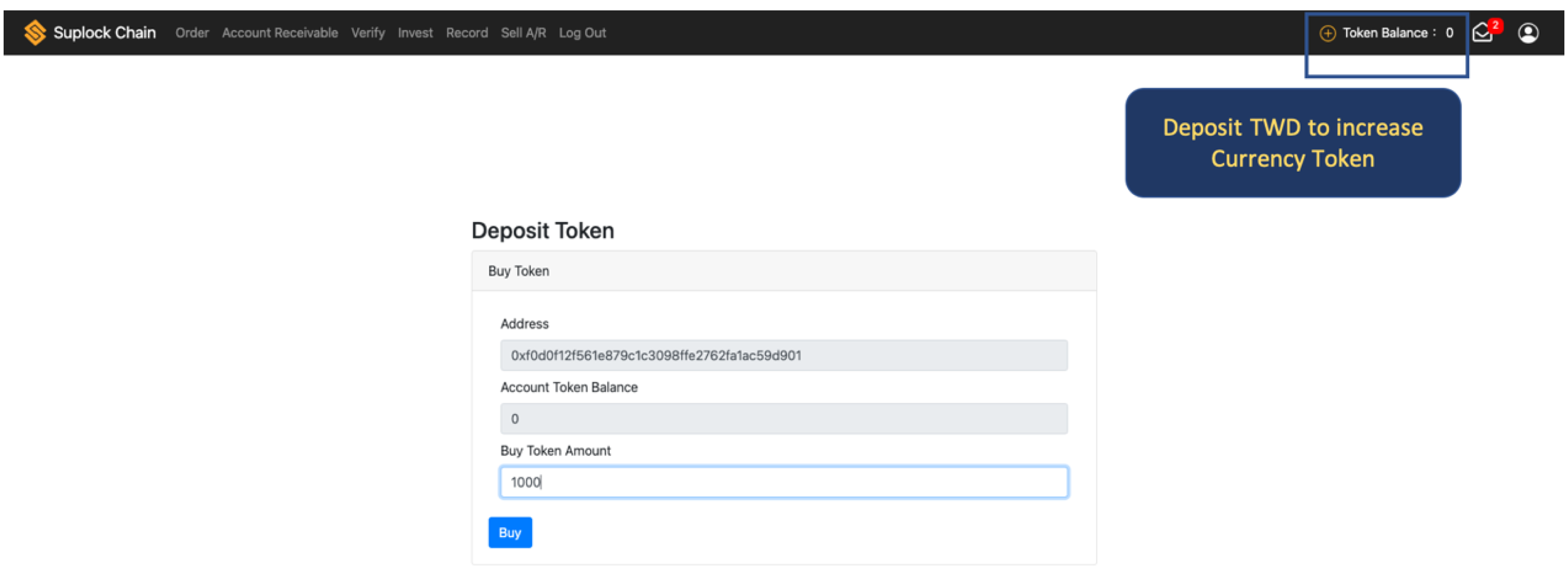

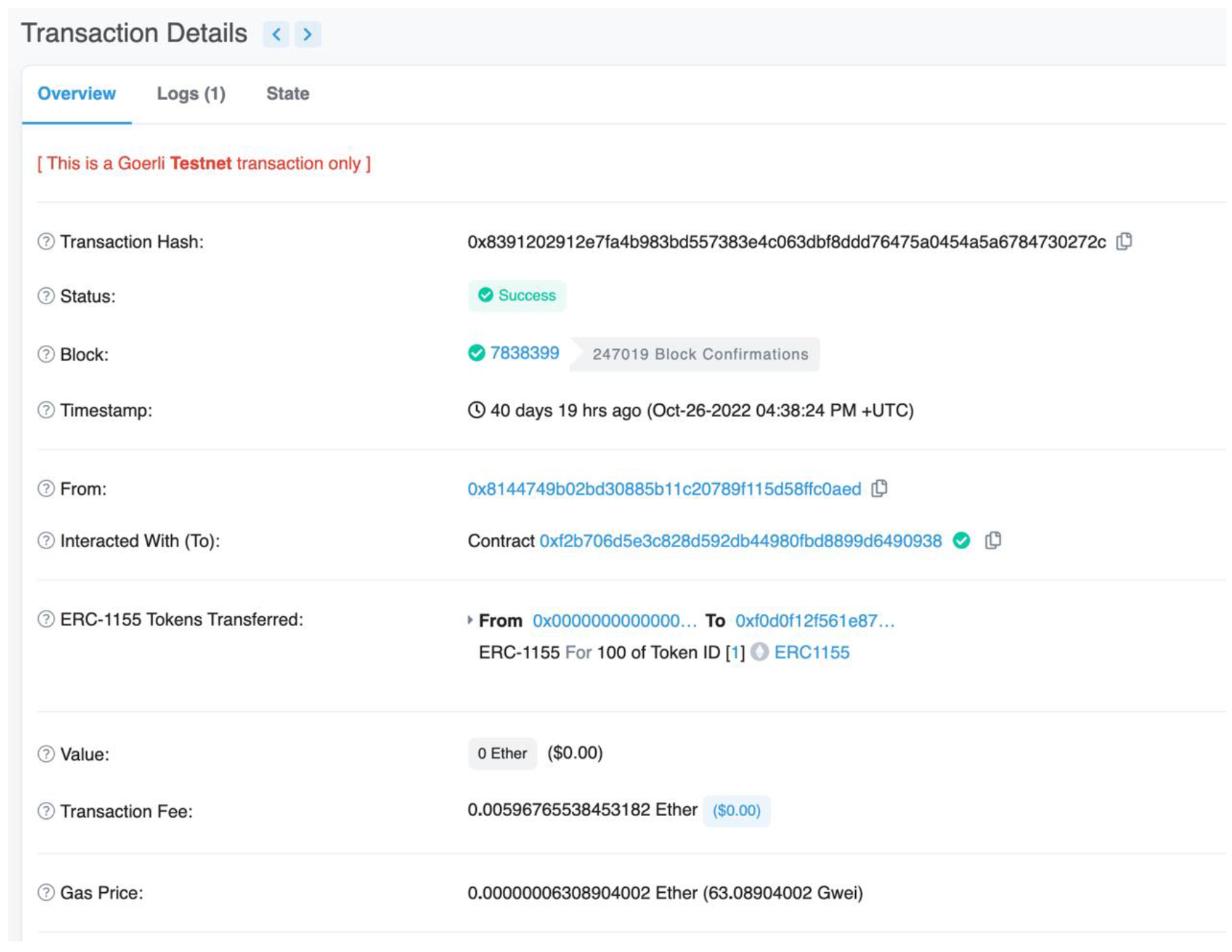

Currency token (XT): this smart contract deals with the cryptocurrency XT issued by our system. All of the transactions submitted through our system are paid in XT. (Deployed at 0x601cdEcd235a43F9181A8213B2a664A9703a742e).

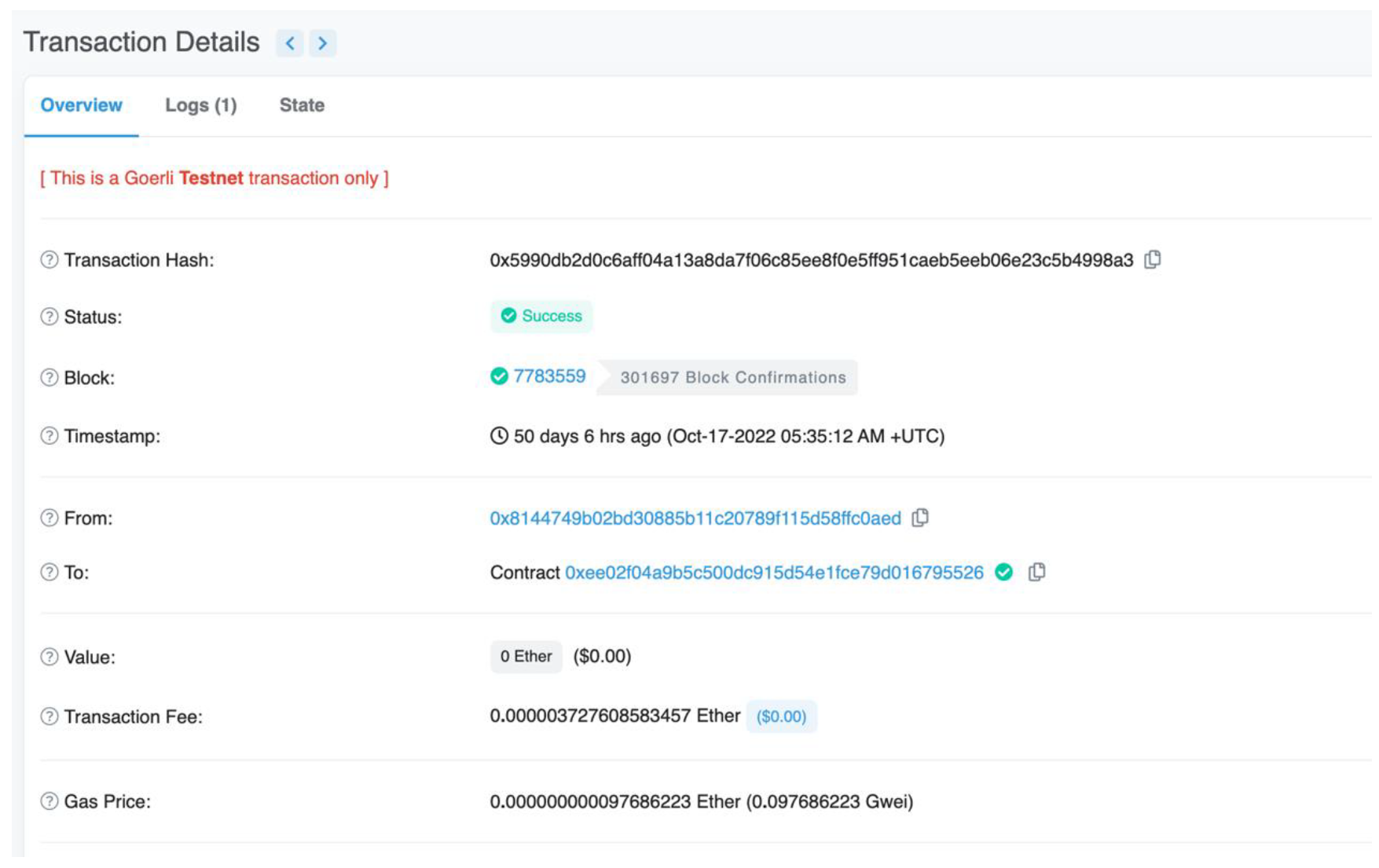

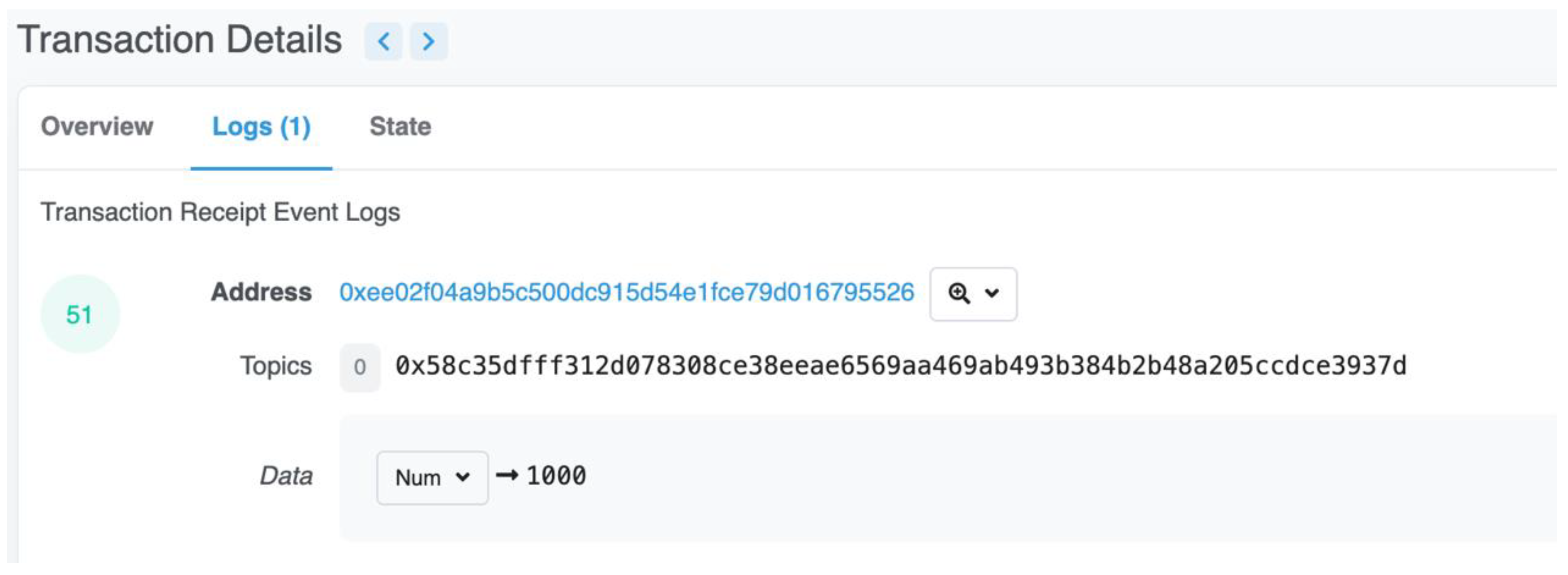

CT operations: this smart contract serves as an oracle to access data from business management systems and mints obligatory-type CTs whenever finance requests or transfer requests are submitted. Each core manufacturer(guarantor) has to deploy its own smart contract, e.g., Core Company Core1′s smart contract deployed at 0xEE02f04A9b5c500dC915D54e1Fce79d016795526.

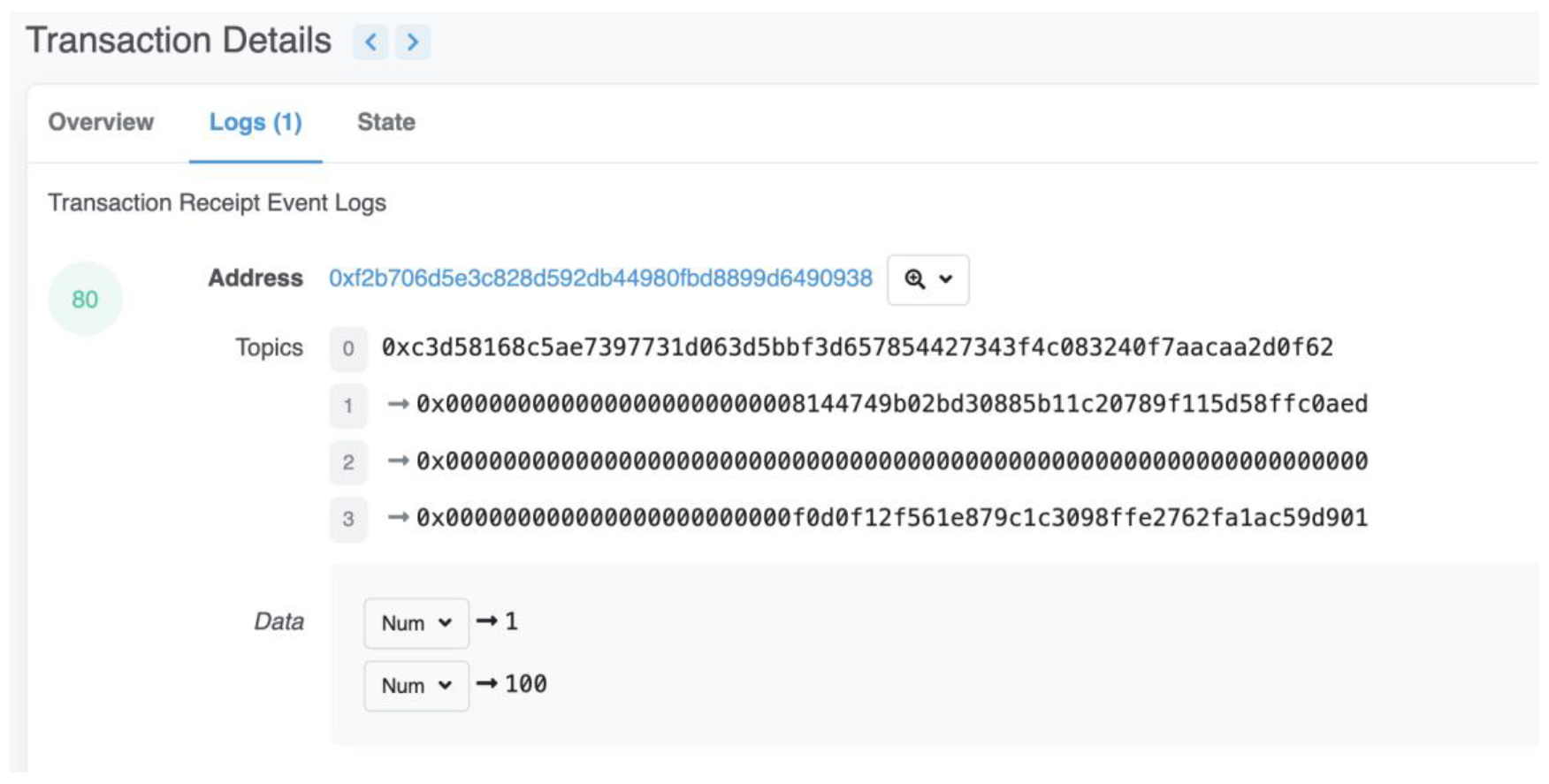

Verification: this smart contract serves as an oracle to access data from business management systems and mints obligatory-type CTs whenever a verification of inventory is passed. (Deployed at 0xf2b706d5e3c828D592Db44980Fbd8899D6490938).

Investment and profit distribution: this smart contract deals with the funding certificates. After a funding provider provides funds by XT, this contract will mint the corresponding right-type CTs to funding provider; and once the system receives repayment from the financing company, this contract will share the profit based on right-type CTs. (Deployed at 0xf788E3cEdfc6E66Cd553CE9636d418F141992DB2).

5.3. Financing Workflows

SCF system is operated by the means specified by business management systems and the use of public chain. The business management system is appointed to serve as the means to provide data that stems from the supply chain and also act as the source to provide verification. While the blockchain is used as a solution to provide traceability to the financing events to mitigate risk events. Based on the data flow combined with the consensus algorithms, we are able to provide below mentioned mechanisms for supply chain financing on the public chain.

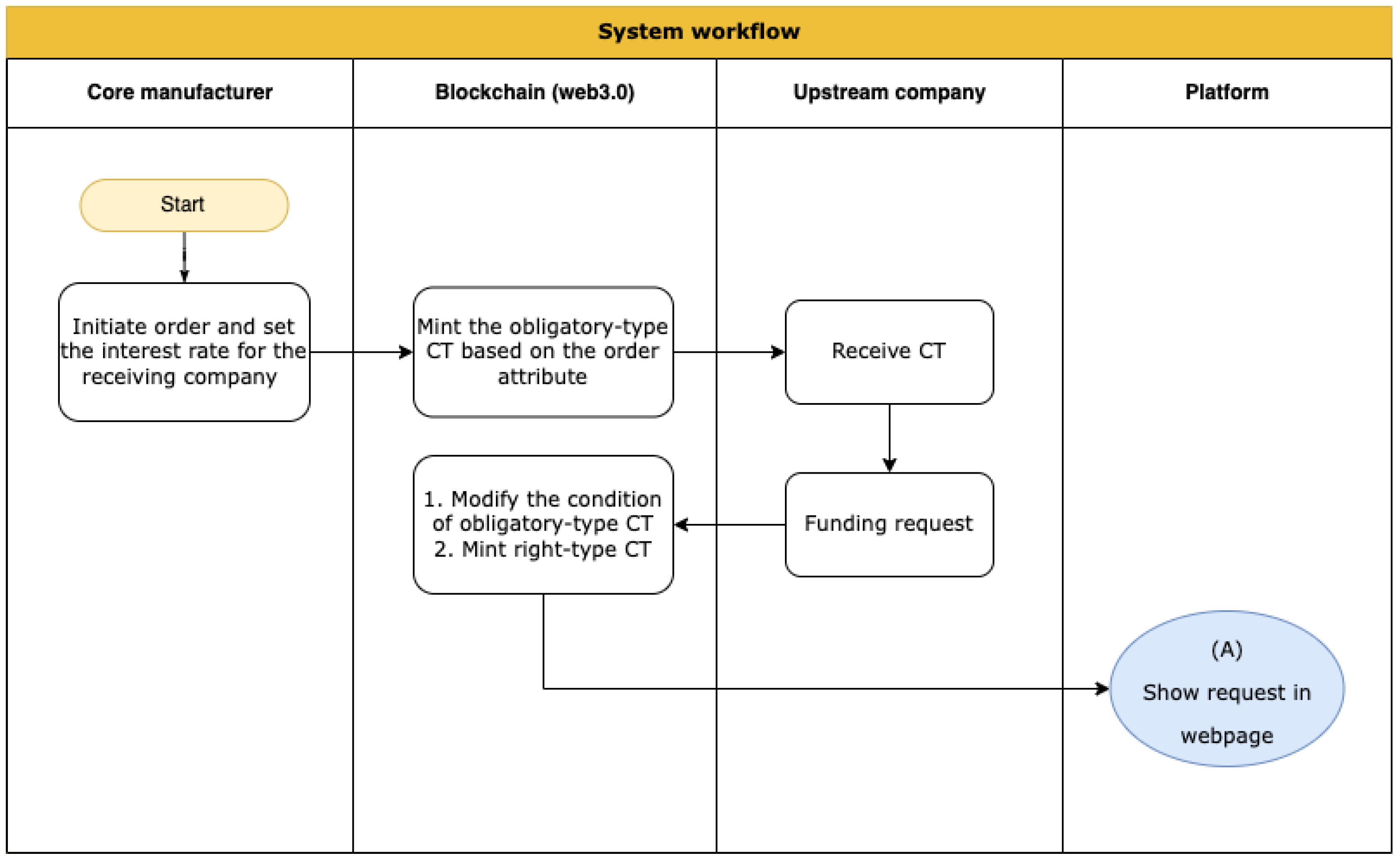

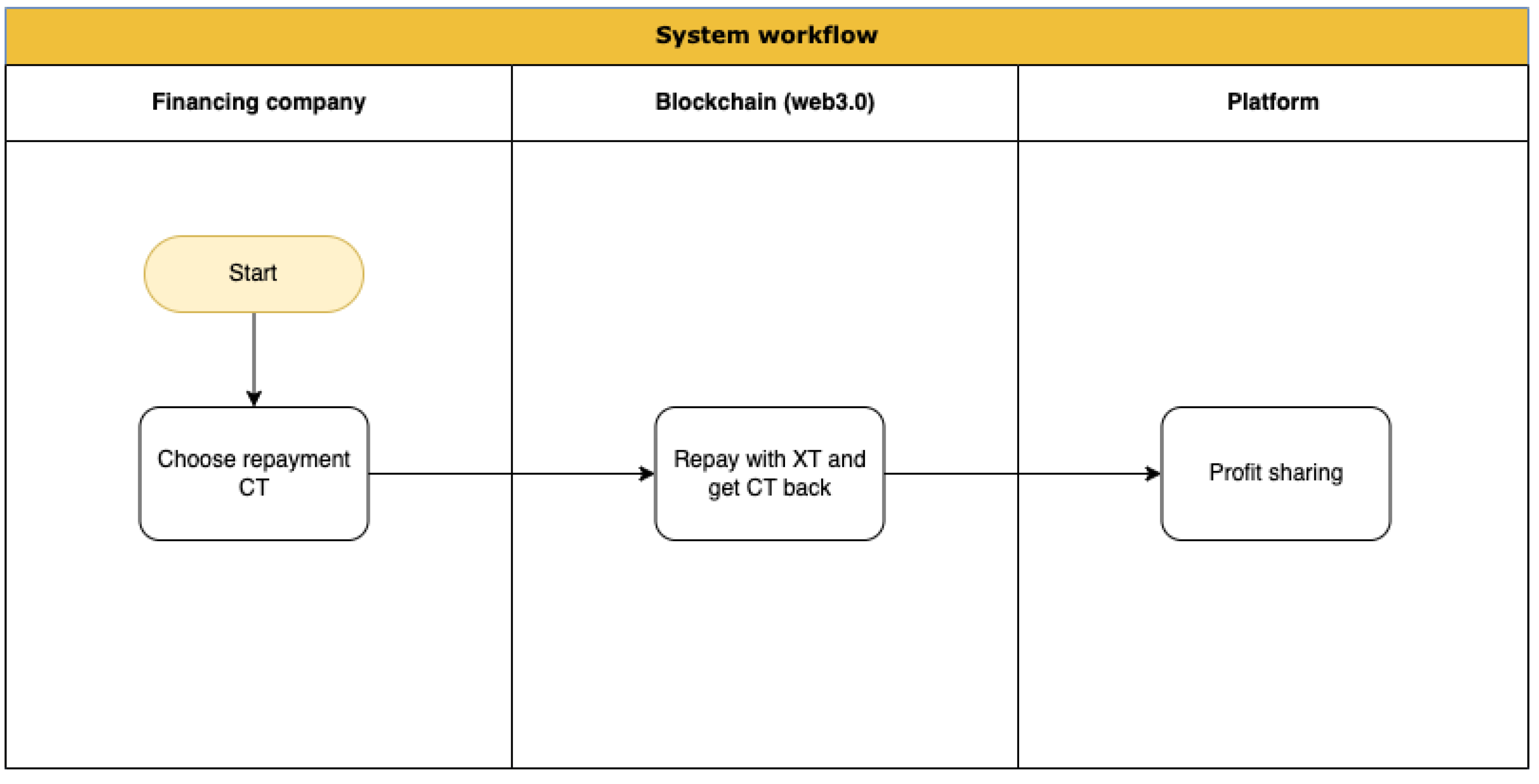

Channel financing: The core company will mint obligatory-type CT with specified conditions on the blockchain to provide guarantee and transparency, then the receiving downstream company can use it for further finance or transfer. The workflow is shown in

Figure 10.

Accounts receivable financing: The obligatory-type CTs are minted to reflect the time value, therefore discounts are applied in the financing process.

Inventory financing: The obligatory-type CTs are authorized by a third-party institution. The inventory is used as the collateral which will be liquidated after a breach of contract, then the funding provider(s) would be able to retrieve payback from the inventory liquidation amount.

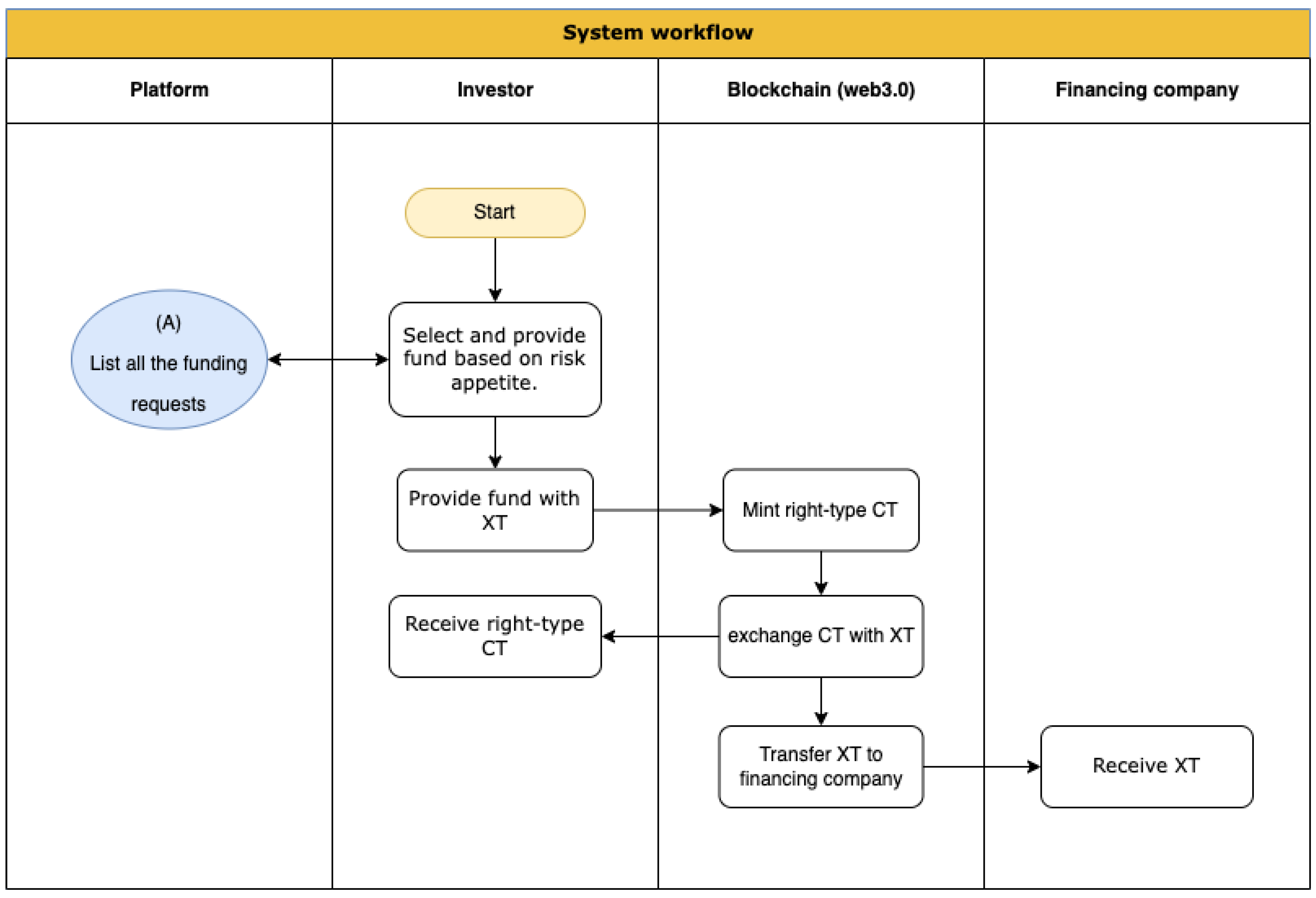

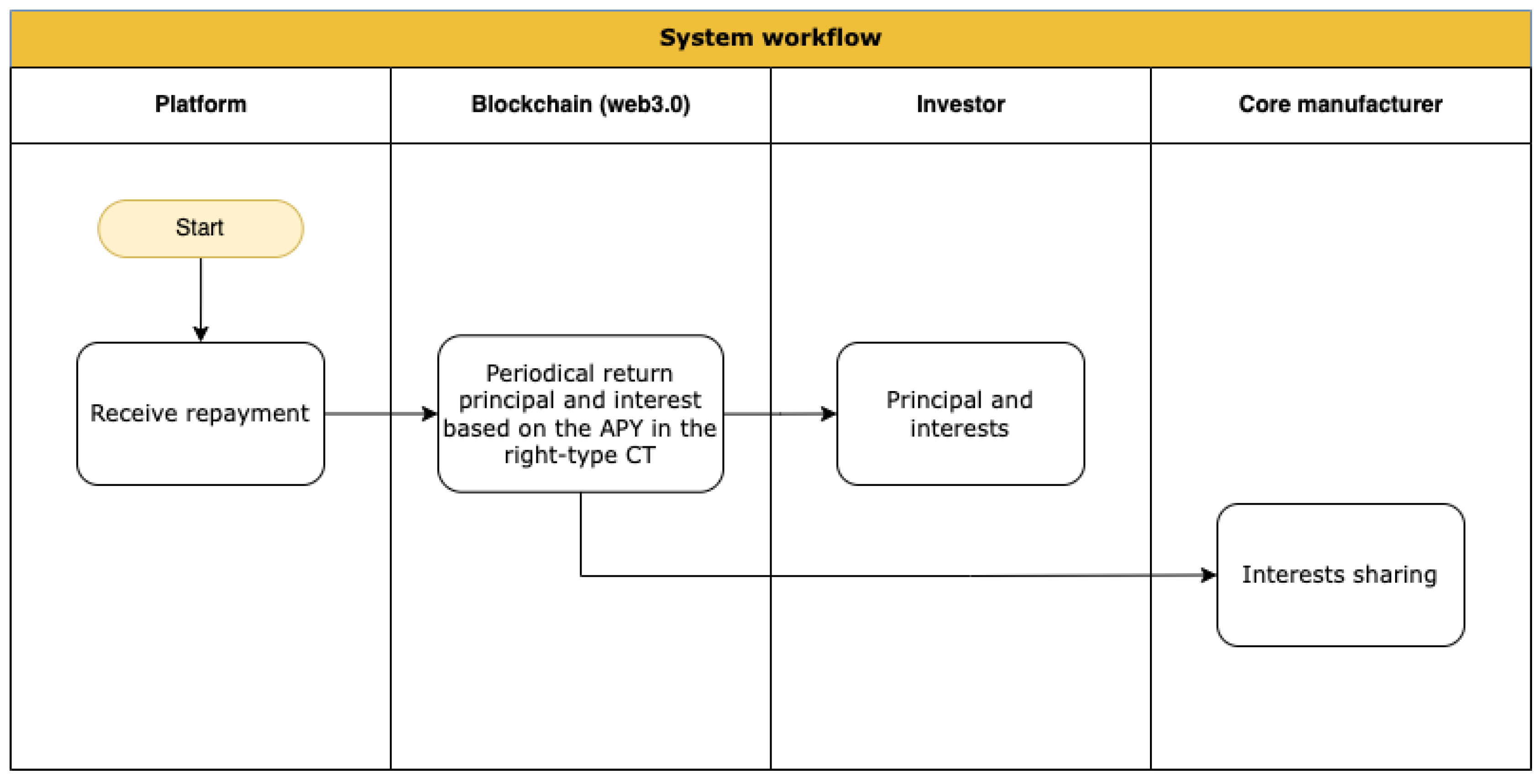

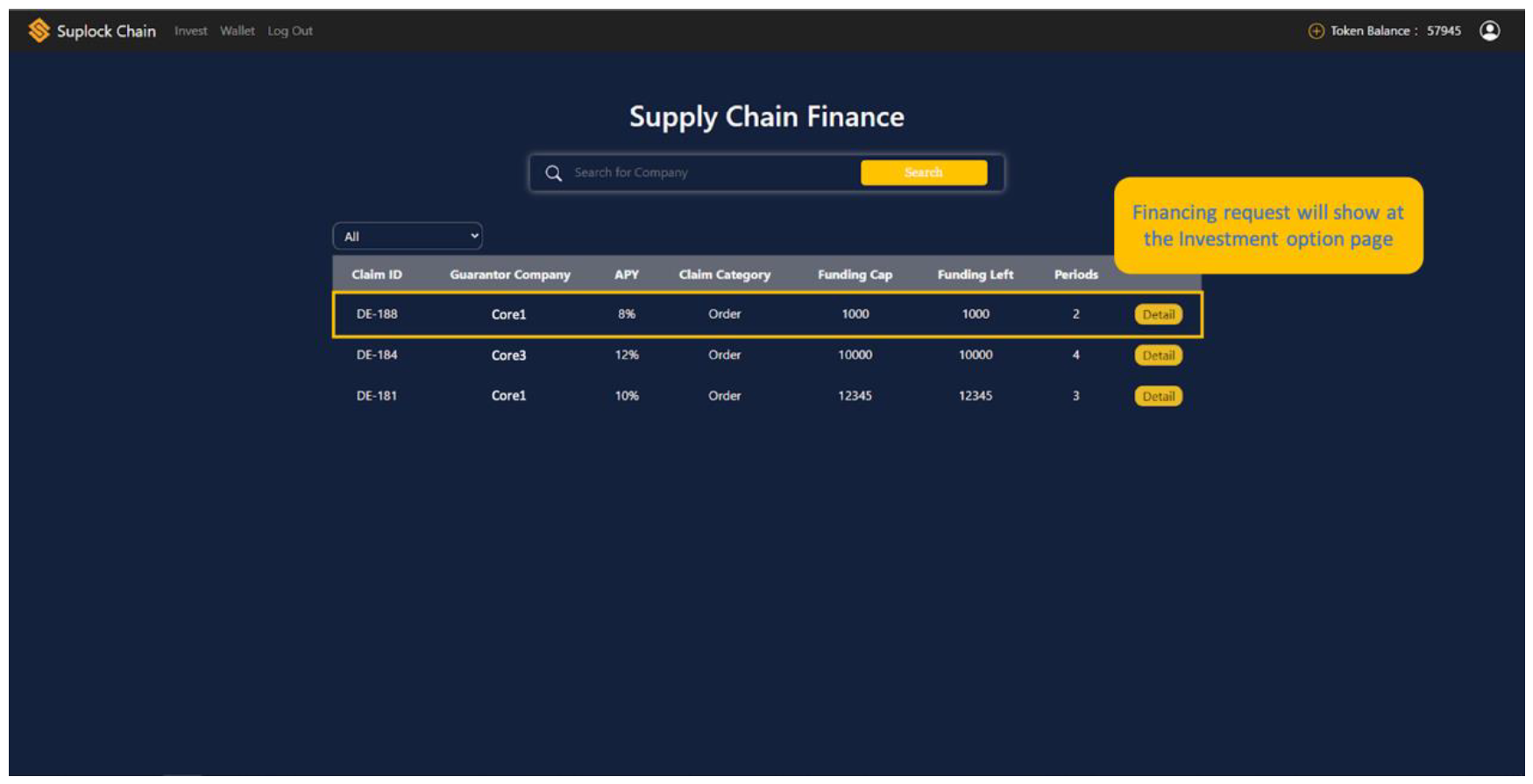

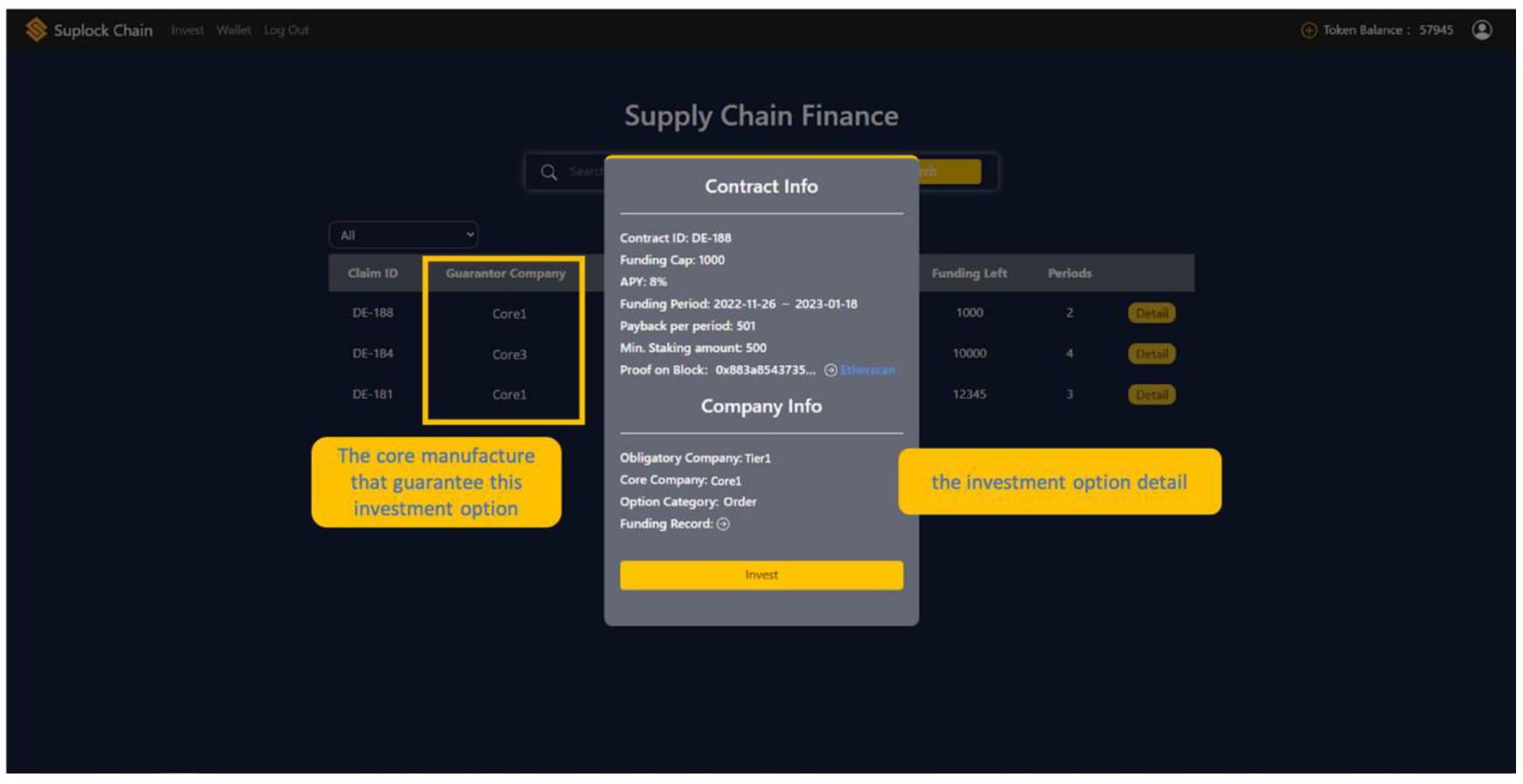

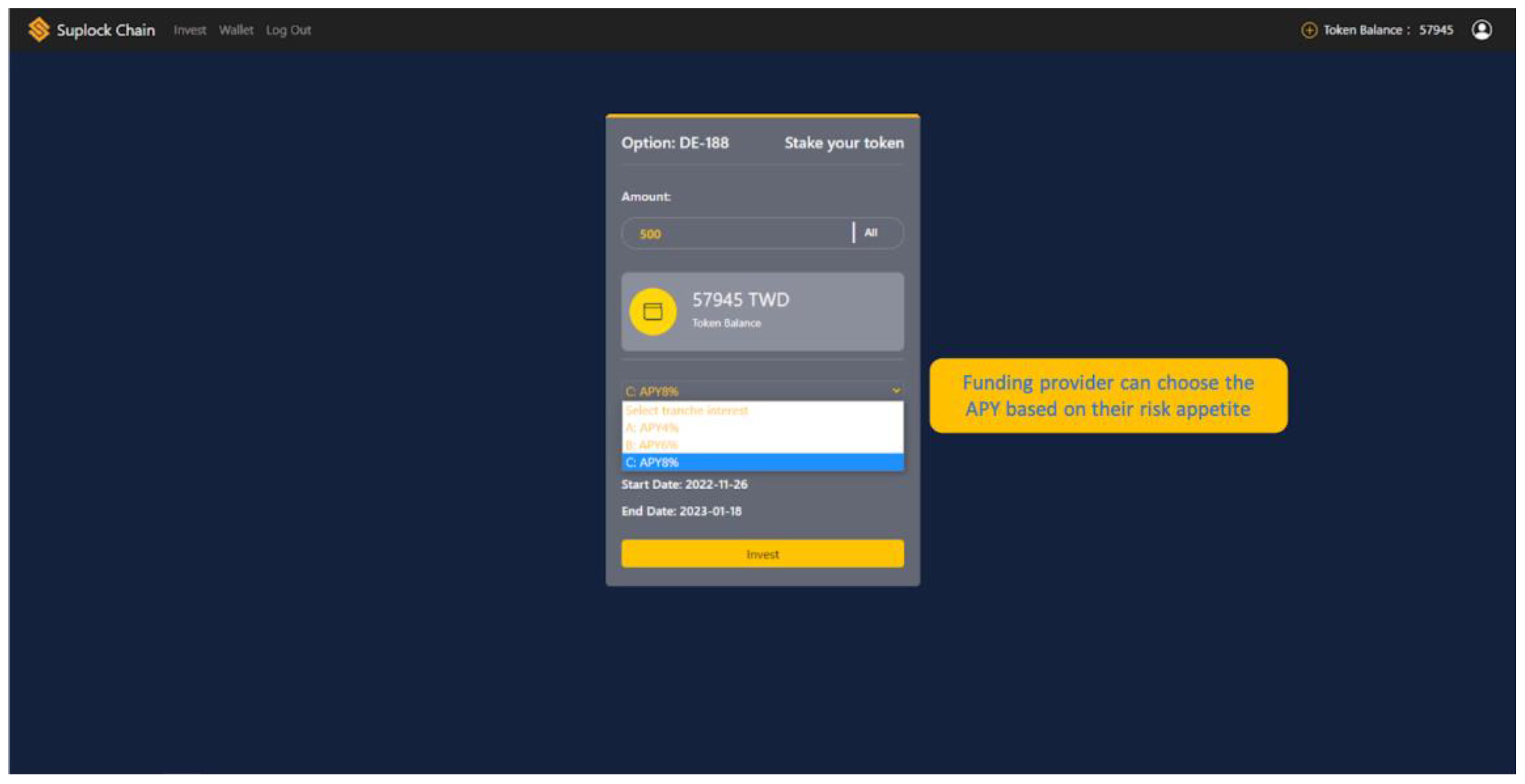

Investment service: Natural person or juridical person can be secured via right-type CTs after providing funds. Every right-type CT offers different annualized payment yield (APY) by investing in different tranches for different ranking of claims. The workflow is shown in

Figure 11.

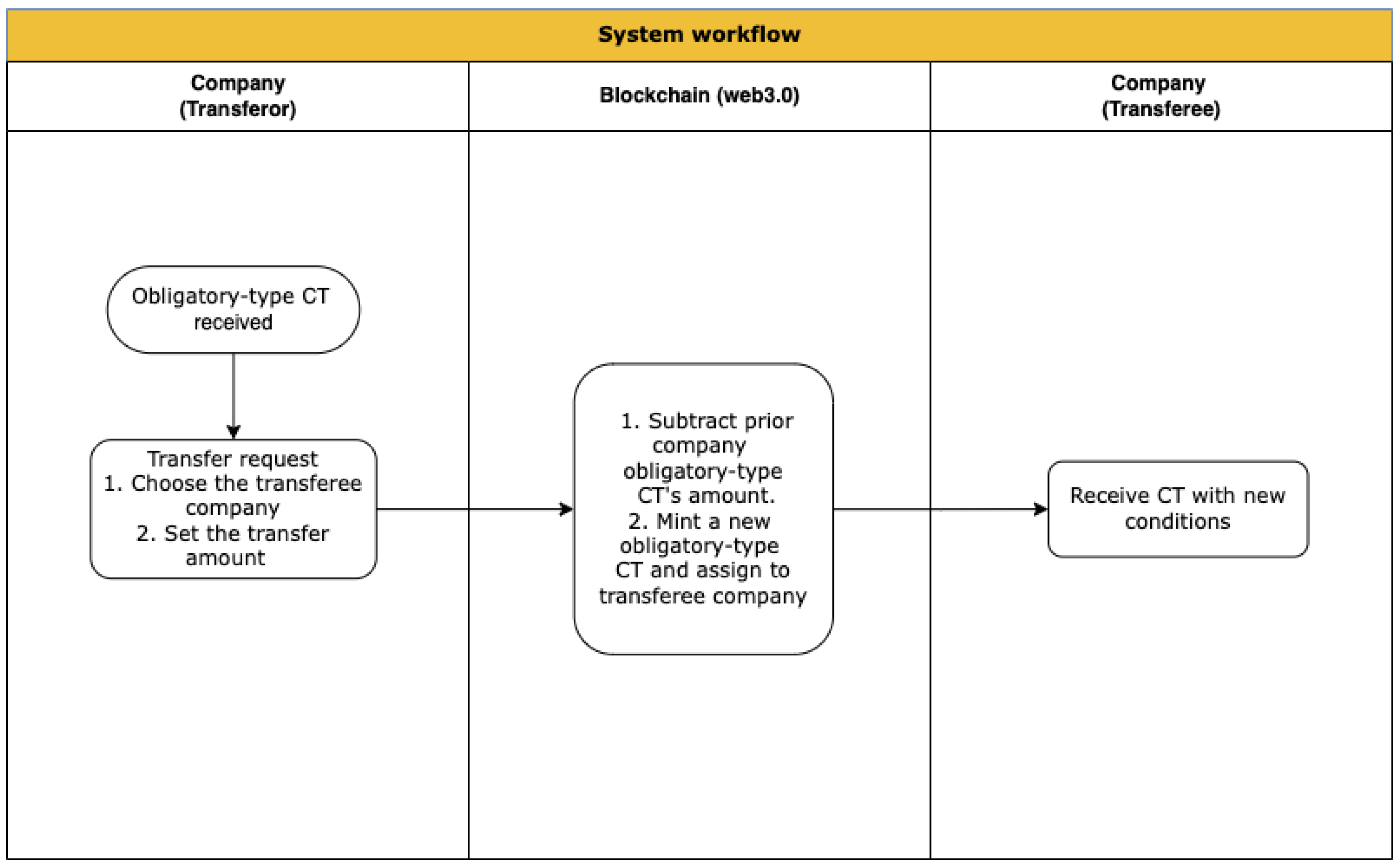

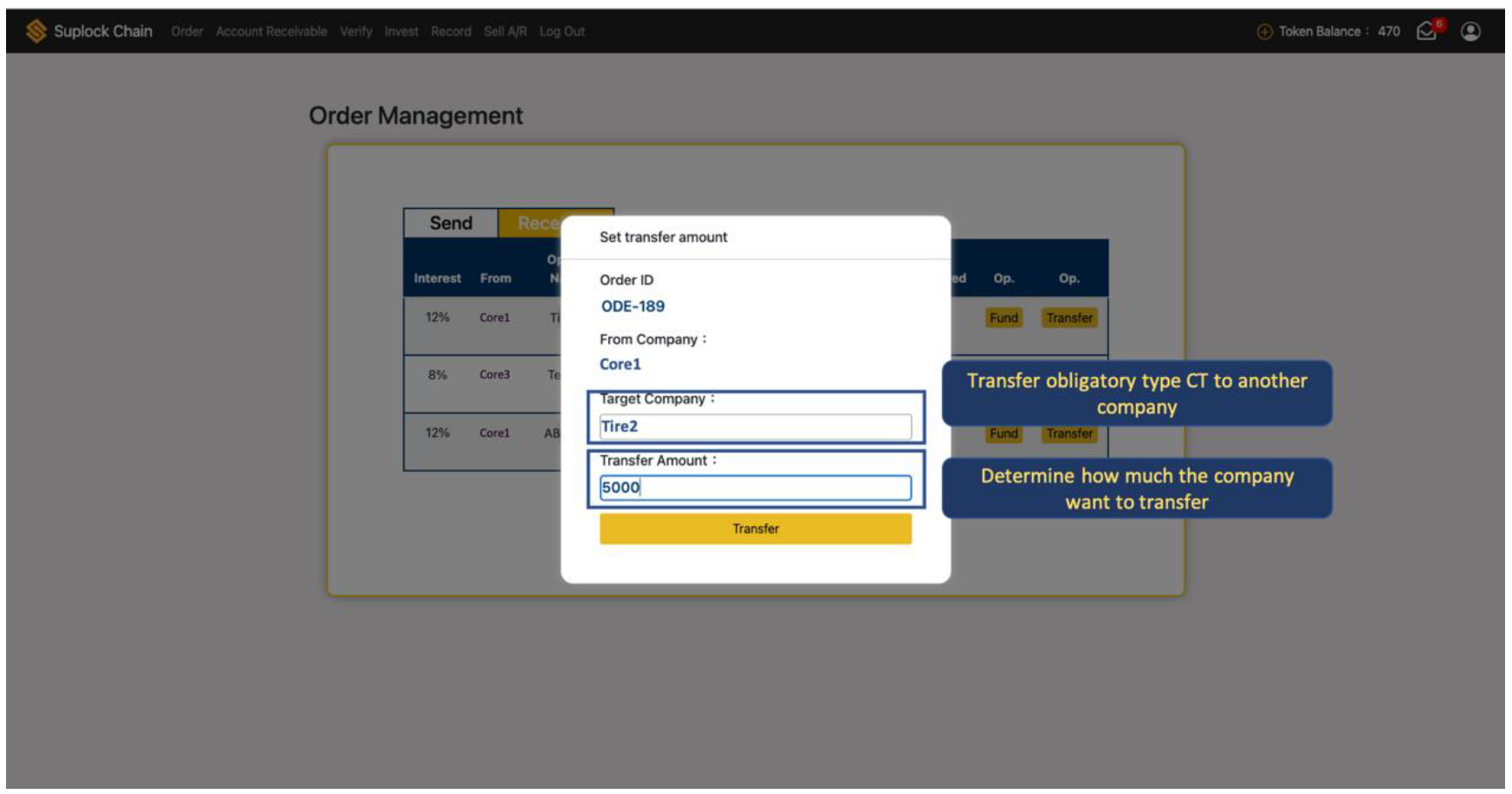

Transfer and conversion of CTs: CTs can be transferred via blockchain as the debt transferring. Companies will be able to manage their obligatory-type CT received from the previous company to conduct risk-control more easily, meanwhile to maximize the efficiency of the supply chain. The workflow is shown in

Figure 12.

Finance management: Profit sharing agreement between core company and investors is programmed in smart contract. The workflows are shown in

Figure 13 and

Figure 14.

Finally, the risk control module is used in case of default, including cases where the user delays repayment, or where the issuer refuses to take responsibility. For the first type the delayed interest and a default penalty charge needs to be calculated as an offset for the value of the goods, while the second type requires auctioning. Both are beyond the scope of this article.

6. Feasibility Analysis

In this section, the legal properties, risk management, and costs and benefits are discussed.

6.1. Legal Analysis

CT used to represent the legal right called “verdinglichung obligatorischer rechte” will be discussed below.

6.1.1. Rights in Rem

As participants in supply chain financing core companies act as someone providing collateral or guarantor, providing the collateral to set up the mortgage, for the CT to be issued in accordance with the mortgage, providing debt guarantee and bearing the final responsibility of full repayment. Among them, the collaterals can be any tangible or intangible asset.

In the inventory CT or collateral CT, the collateral is created by smart contracts and recorded in the blockchain to fulfill the requirements for rights in rem. In addition, the data on the blockchain cannot be tampered with or forged and can be traced back to its source, so that rights in rem can be installed in a similar way of installing rights in rem in the real world. In practice, in response to different legal requirements in various countries for the rights in rem, it is also possible to connect to the authority officially appointed by the government through using the application interface for the rights in rem. The blockchain can provide a proof of existence of these rights.

A line of credit mortgage is a mortgage created for a specified maximum amount by using a debtor’s or third party’s assets as guarantee and thereby secure a creditor’s rights against the debtor. Therefore, there are three elements: one is the assets used as collateral, second is a specific maximum amount, the third is unknown creditor’s rights. That is, the debtor can borrow unspecified amounts of capital as long as it remains within the specified maximum limit and bear the responsibilities (interest and repayment) as agreed upon in the loan terms.

The number and specific conditions of the CT are recorded on the blockchain. When the CT is used, the agreed upon conditions are fulfilled, meaning that the use of the conditional token requires the fulfillment (exercise) of the obligations (rights) endorsed by the set conditions at the same time. An obligation-type CT, providing an (margin, inventory, etc.) as a collateral, setting the number of tokens that can be issued (that is, the maximum limit), a liability only when using (unspecified), plus the public nature the public chain, is like a true line of credit mortgage. In addition, CT’s are issued in multiple quantities and can be transferred to third parties. Each CT represents a dividable (securitized) line of credit mortgage. While the right-type of CT can act as a divisible fixed income bond.

6.1.2. Obligations

Clearly, the obligation-type and right-type CT’s will install a true creditor-debtor relationship as long as the right conditions are set and fulfilled.

Traditionally, disputes between claimants and debtors, needed to be resolved through judicial means. However, with the use of CT, the smart contract will force the creditor-debtor relationship to be activated, with the smart contract sending the transaction to the blockchain, where the debt is recorded. Keeping track of creditor’s rights and debts in public, is equivalent to create of creditor’s rights in rem and can resolve disputes between two parties easier.

6.2. Risk Analysis and Management

The need to fulfill conditions set for CT’s comes from a user’s default or fraud risk. The source of default comes from the guarantor bearing the ultimate responsibility. While fraud mostly happens in case of having double collateral and mortgages.

Investment CT is used for funding the obligation-type CT. So, the ultimate risk of loss is caused by both the risk of default and from an investment loss.

6.2.1. Up/Downstream

Because the CT is divisible and liability only occurs after use, the manufacturer can decide on how to use CT’s according to their specific financial situation: they can decide to not use, or transfer or use all or part of it.

It is even possible to convert the conditional tokens to reduce liability, meaning, modifying its conditions. If the required liability is lower than originally set in its conditions, it is equivalent to a partially using that condition. This will provide flexibility in the use of funds by those who need it. Modifying does not expand the maximum credit, and since the use and transfer of information is recorded in the blockchain and is therefore undeniably true, so as to restrain self-discipline and serve as a risk management mechanism for upstream and downstream manufacturers.

6.2.2. Guarantors

If the CT defaults, the guarantor is ultimately the responsible organization of the conditional certificate. Therefore, the conditional token provides the conditions to use and transfer for the issuer, including but not limited to: interest rate, term or transfer level restrictions, etc. All ensuring that the manufacturer can manage its risk through setting the conditions.

The CT cannot predict a breach of contract between upstream and downstream manufacturers. However, it can provide transparent information on the breach of contract, including the situation on the use or transfer of tokens by the upstream and downstream manufacturers, and thus ensure that the guarantor can use the goods for price reduction after the goods arrive to the warehouse.

6.2.3. Fund Providers

Fund providers undertake the ultimate risk of loss. At this time, risk management can be divided into collateral and investment risk management. Collateral risk management refers to verifying and evaluating the collateral (including credit) when issuing CT’s. If market trading exists, the evaluation will be based on the market value. If not, a verification process done by qualified persons or institution is required.

Holders of investment CT can additionally govern and predict through the use of blockchain. For blockchain governance a voting mechanism can be written in a smart contract, with the voting rights being determined by the number of investment CT’s held, and the value of the collateral for the issuer being determined through vote. Blockchain prediction uses smart contracts to obtain external information. After the external third party has verified and evaluated the core enterprise, the value of the collateral is estimated and evaluated on its value as a security by the blockchain prediction. Both are unique methods of the blockchain, and can be used as methods for value assessment.

Fund providing to SCF is similar to investing in fix-income securities, in both an investment risk exists. In this article, we look at the use of tranche investments and pooled funds as a way of managing investment risk. At least three types of fixed-income securities exist, minimum risk (tranche A), mezzanine risk (tranche B) and residual risk (tranche C). If funds are early redeemed or defaulted, then the principal of tranche C will be returned or lost first, consequently followed by the principals for tranche B and tranche A. The risk linked to tranche A is the lowest, and for tranche C the highest. Therefore, depending on how much risk a fund provider wants to take for what risk reward, a different undertaking of each tranche to manage their risk.

Pooled funds are another investment risk management tool for fund providers. Because there are different types of obligation CT’s in the pool, the risks for fund providers investing in the pool are being reduced due to diversifying the funds into different CT’s.

In addition, the owner of the CT can also transfer the investment CT’s to others, and with that transfer and disperse his risk.

6.2.4. Fraud Risk Management

Another risk management advantage of using CT is that cases of double collateral or guarantees can be avoided. The smart contract can issue a token which needs to be linked to the goods that are provided as collateral by the guaranteeing enterprise (called a goods token) and is used like a barcode. Because the records of the blockchain cannot be tampered with or forged, providing the goods as collateral is equivalent to executing the lock-in function of the smart contract, and thus sending the transaction on the blockchain. Now, the double collateral is equivalent to sending a transaction of the goods token twice, it is impossible to execute because there is no specific token for the second transaction. The use of CT’s means that the supplier and the issuer generate claims and debts. Similarly to the explanation for goods tokens, a smart contract cannot execute the same guarantee twice.

Finally, inventory CT’s and collateral CT’s are recorded on the blockchain, therefore they can be used as a basis for credit scoring and risk management.

6.3. Costs and Benefits

The cost of the conditional token is divided in costs for deploying smart contracts and transaction costs in the public blockchain. With the latter being the most important costs, necessary to change the state of the blockchain (aka the change of the ledger).

The costs of deployment are determined by the amount of code in the smart contract and is a one-time cost. The calculation method comes down to multiplying required gas units with the gas price per unit of it. Take the most popular Ethereum chain (Ethereum) as an example, the total gas fee is equal to the basic gas limit of 32,000 units plus the gas (base) fee of 200 units per byte [

71]. The gas price is divided into three categories: fast, normal, and slow referring to the required deployment speed. The recent average price from 1 November to 30 November 2022 for gas is 23 gwei [

72] (1 gwei = 0.000000001 ETH), making the market price around USD 0.000029 [

73] (1ETH = USD 1276).

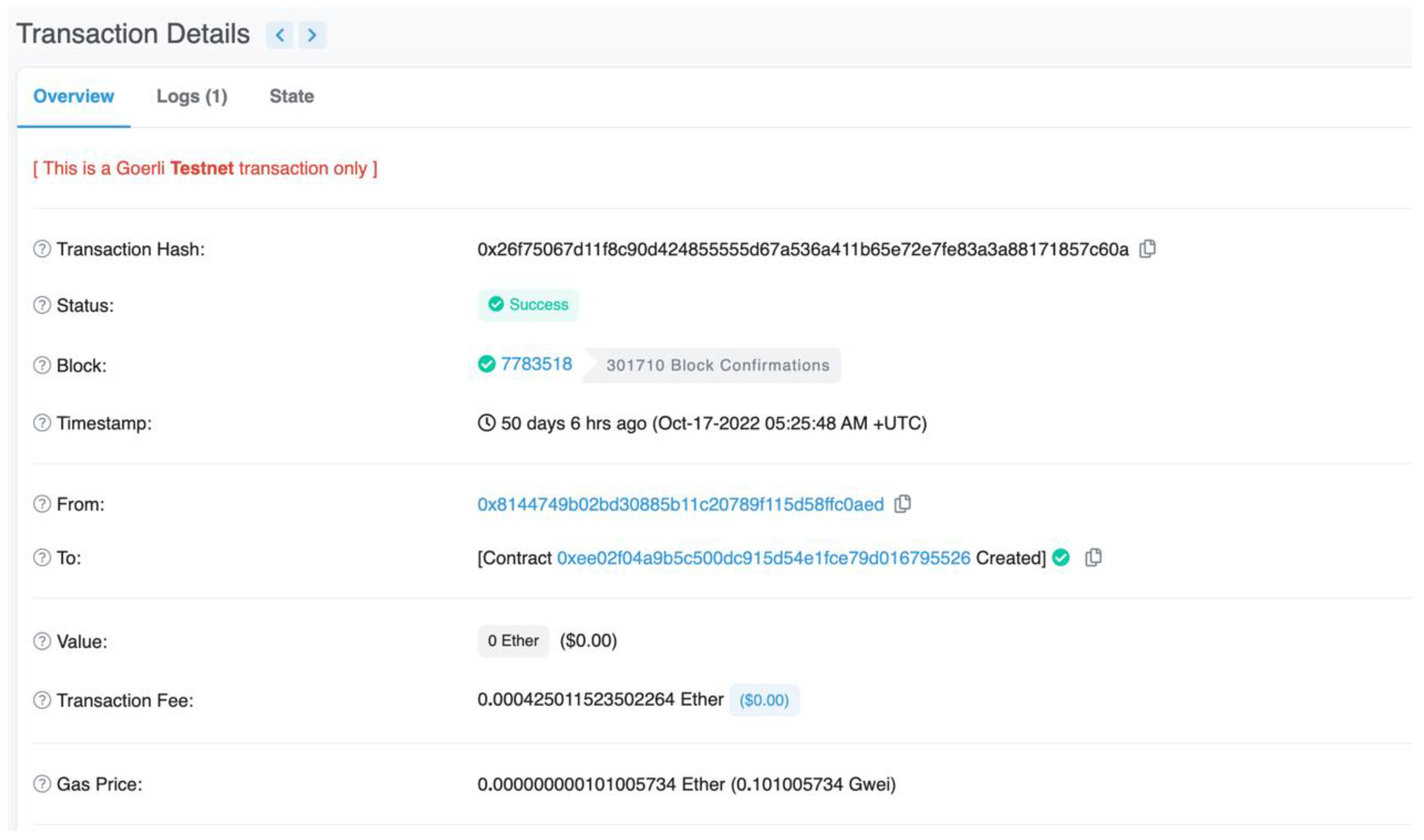

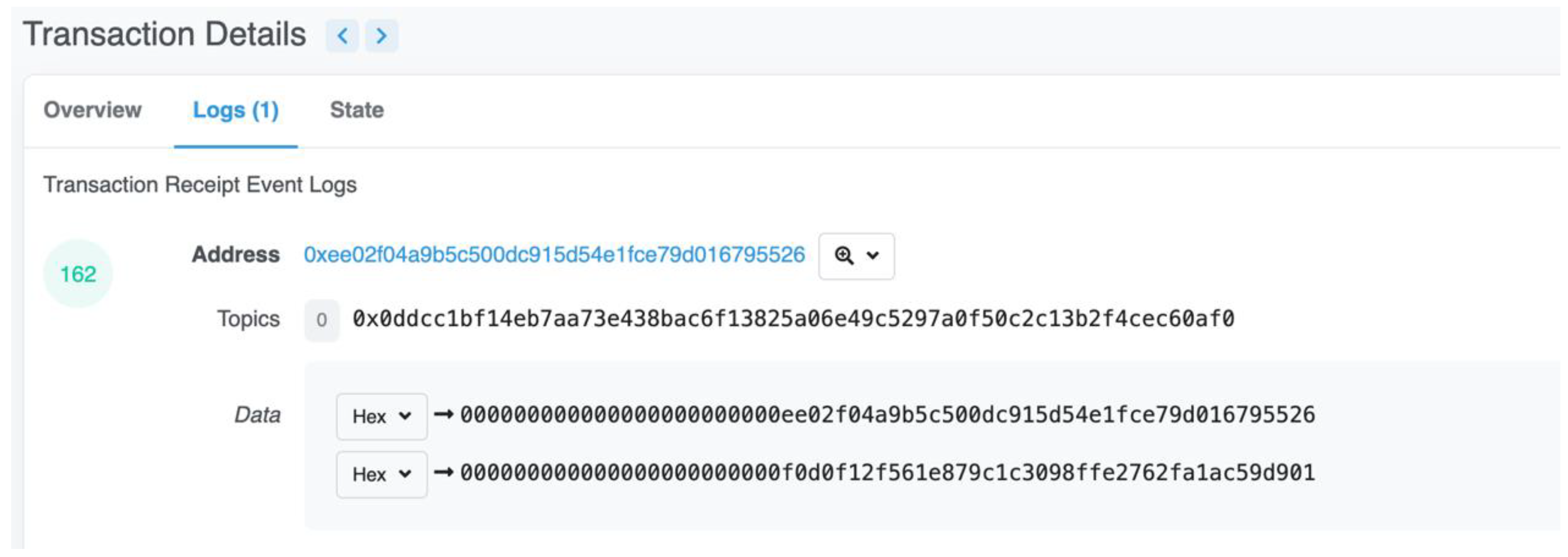

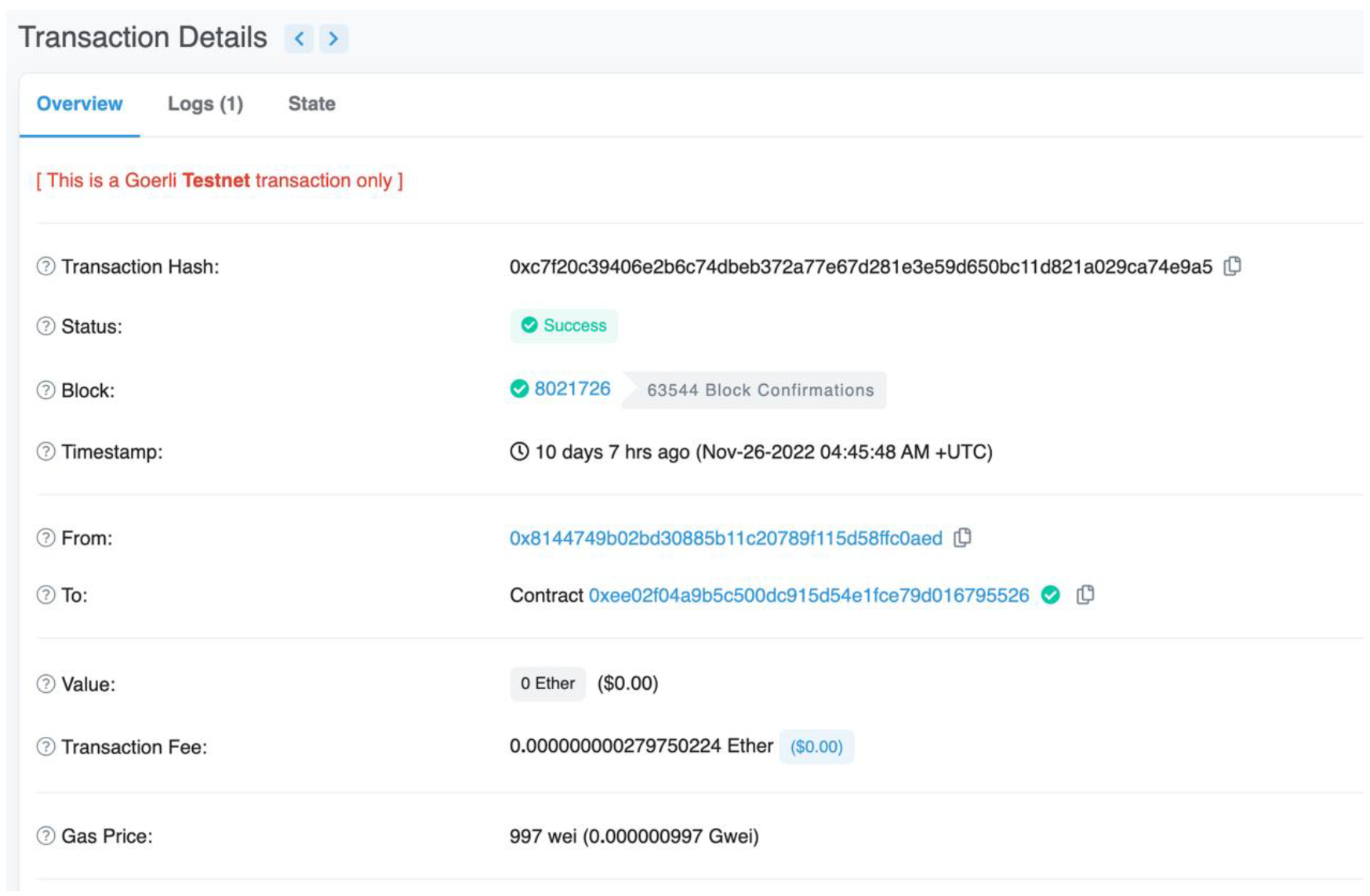

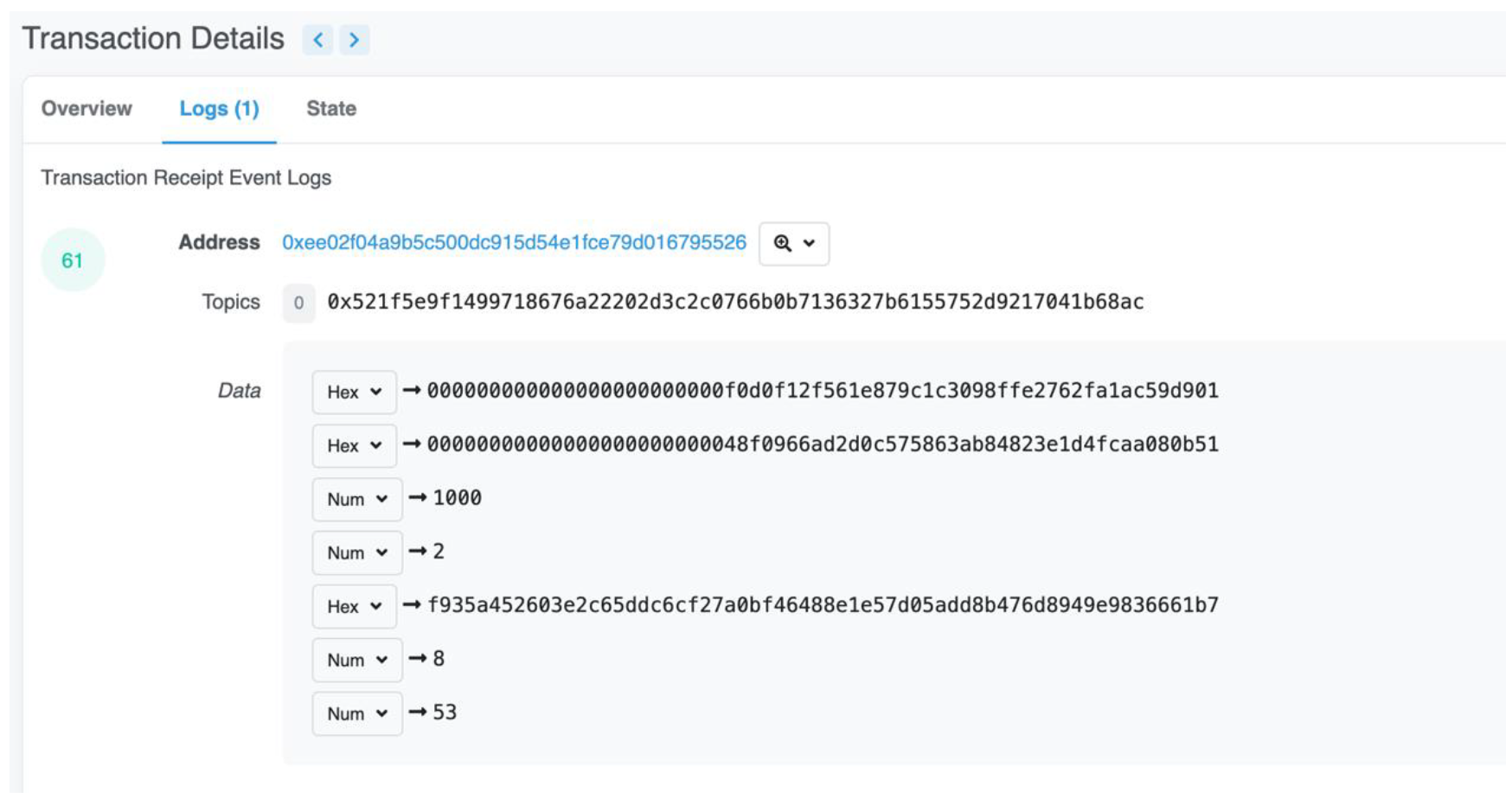

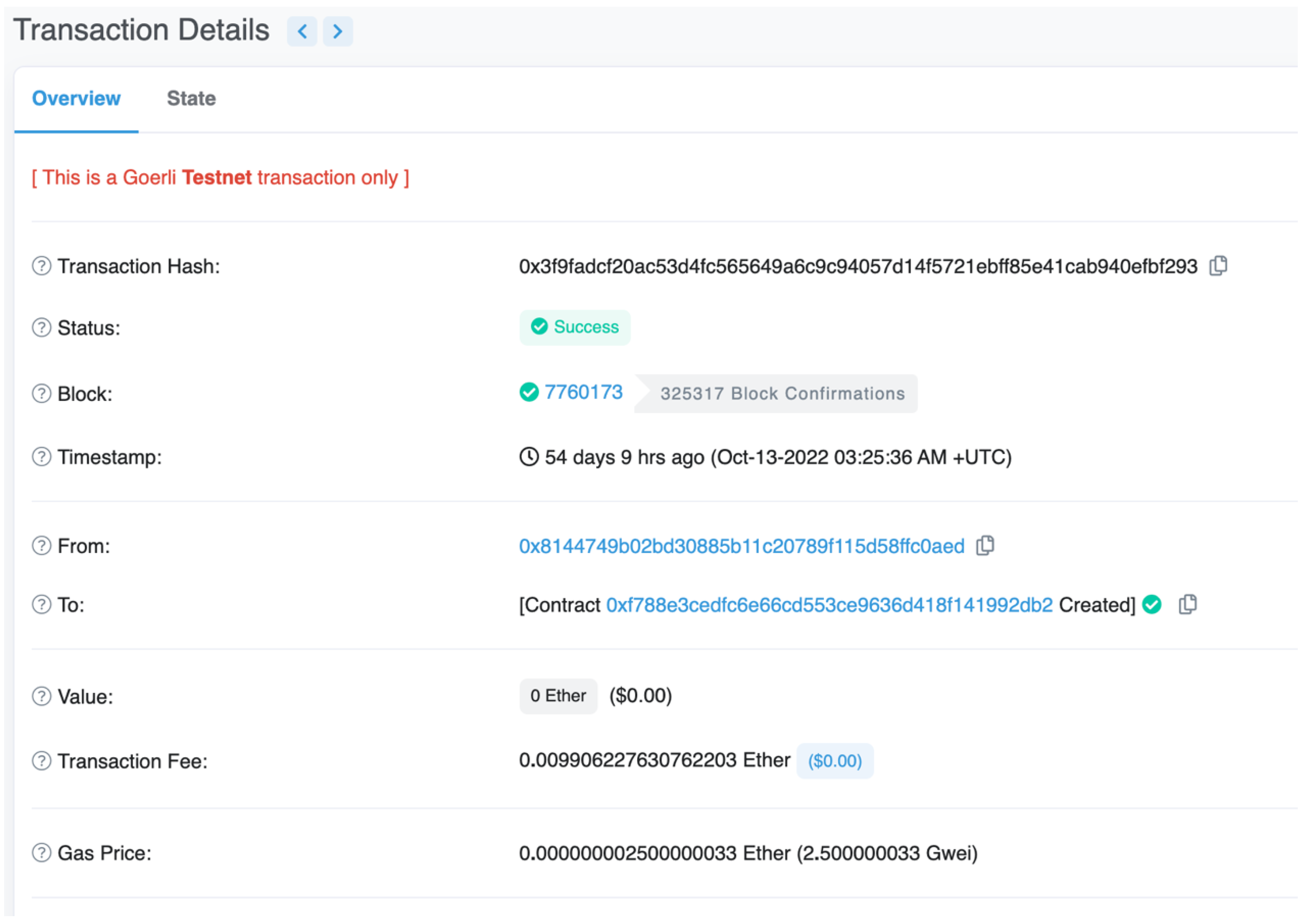

In this study, the smart contract of CT is deployed on the Ethereum test chain, the deployed address: 0xEE02f04A9b5c500dC915D54e1Fce79d016795526. It’s gas fee is about 4.2 million refer to

Figure A2 in

Appendix A, or 0.096 ETH

which equivalent to USD 123. However, these costs can be ignored for each transaction after amortizing to the number years of financing.

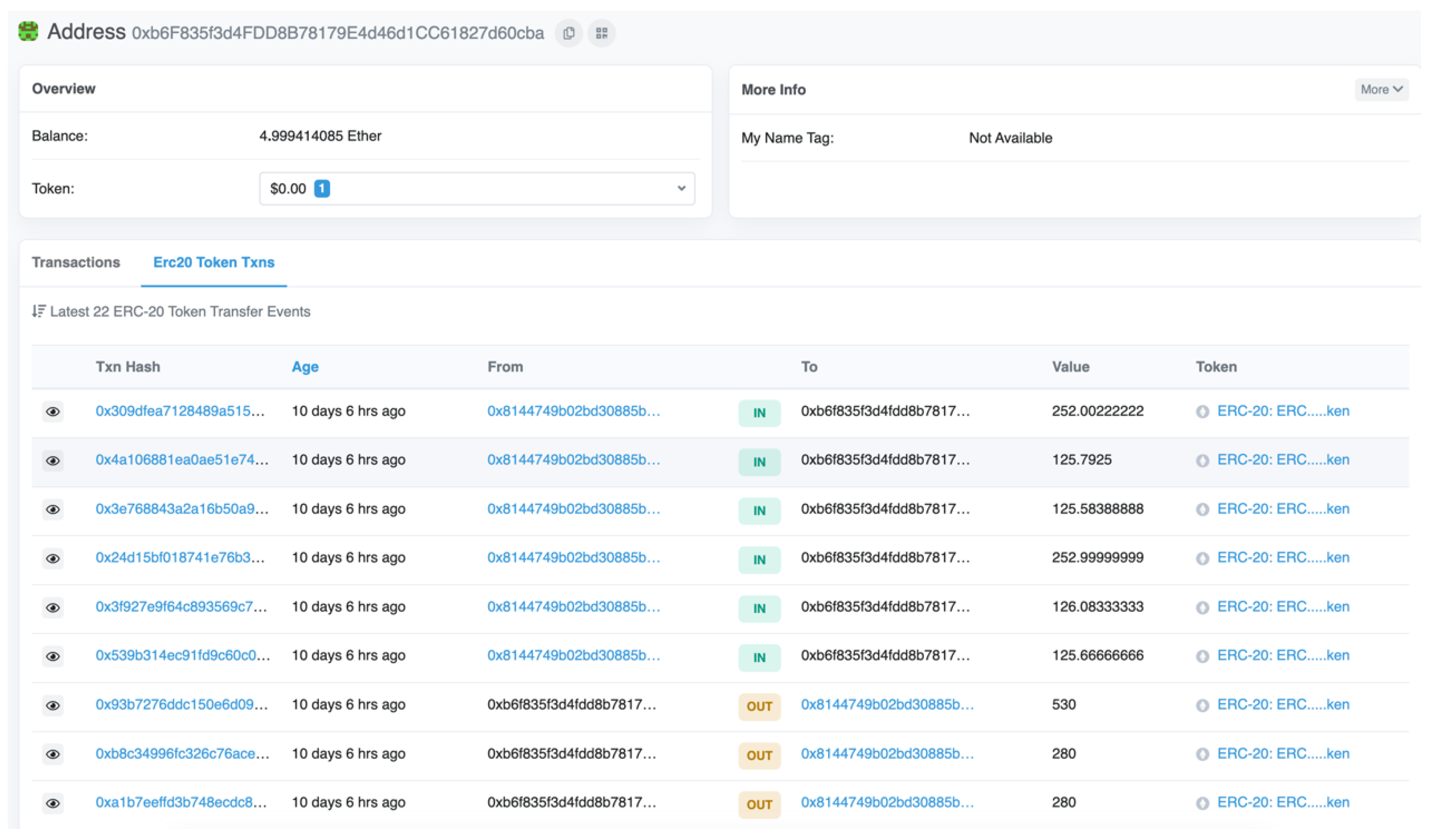

The transaction fee of the public blockchain depends on the type of chain and the number of transactions. Taking the Ethereum chain for example, between November and December of 2022, the fee for each transaction was 0.0014–0.0023 ETH or USD 1.7–2.82 (

Figure 15). At the same time, the collateral fee rate for Taiwan Small and Medium Enterprise’s is 0.375% [

74], thus the fee is USD 37.5 if borrowing USD 10,000. Comparing with the handling and international trading fee of the financial industry, the CT fees are supposed to be lower for the following reasons:

- 1.

There are variety of costs for implementation and running business in traditional SCF [

75], only the fee charged by platform, including transaction fee on blockchain in CT.

- 2.

The transaction costs are high for traditional SCF. The report of International Chamber of Commerce (2020) [

76] shows 83% of banks concern high transaction costs or low fee income on trade finance in future.

- 3.

The losses and the number of people caused by fraud should not be underestimated. For example, the case Yasin in Taiwan has more than 6000 people who filed a lawsuit (98-Jin-3, Taiwan Shilin District Court 2015). If we consider the confidence from general public in SCF, it is even more impossible to compare.

- 4.

Many studies [

11,

18,

77] show the cost effective if apply blockchain technology to supply chain finance, especial for deep-tier companies.

- 5.

CT can improve capital efficiency in society. Traditional SCF seldom provides funds for manufacturers above the second tier or deep-tiers due to risk considerations. However, by the transfer operation, CT can help to increase the sources of funding for deep-tiers and let non-financial entities participate in the role of fund providers, overall improving economic efficiency. The cost of funding thus will be decreased.

Concluding the above, we might claim the benefits of using CT will reduce losses and improving supply chain efficiency, even there is no global statistics on costs of SCF.

6.4. Comparison

The biggest difference between the public blockchain and the consortium chain is its degree of inclusivity and credibility. The source of funds of the consortium chain comes mainly from the financial industry participating in the specific consortium chain. Additionally, because of contradicting with the decentralized nature of blockchain, and the financial industry’s relationship with credit rating the consortium chain cannot be extended towards the public. Fund users also need to be members of the consortium chain. However, CT can be extended to the public and to any of the vertical or horizontal supply chain manufacturers, with that achieving the goal of true inclusive finance.

In terms of credibility, the source of credibility comes from the number of nodes in the blockchain, and the nodes of a consortium chain are far less than the nodes of a public blockchain, so data is more likely to be controlled by more than 51% of computing power, indirectly affecting inclusivity.

In addition to the above-mentioned advantages of the public chain, the CT also increases flexibility because of its transferability, amenability, and the required conditions to be fulfilled to undertake obligations or to enjoy rights.

7. Concluding Remarks

The supply chain provides logistics and flow of information, and includes the vertical supply chain N + 1 + N and the horizontal supply chain of international trade. However, due to the difficulty of credit investigation, the financial industry is limited to SCF focusing on core enterprises in terms of capital flow support.

This study proposes a new model for SCF based on CT issued by smart contracts deployed at the public blockchain. The study explains a method on how to use CT’s, how risks can be managed, and implications for legal compliance, system construction and cost-effectiveness. It is believed that CT’s provide (1) credibility, by adopting the public chain resulting in the highest degree of credibility. The public nature of the blockchain can be exploited to guarantee the rights of securities, mortgages and even creditor’s rights. (2) Flexibility, to set or reset conditions of use and adjusting amounts for transfer or use to meet desired risk requirements, effectively solving problems of financial institutions in financing throughout vertical and horizontal relationships. (3) Security, blockchain use asymmetric public-private key cryptography, therefore CT’s can be used as security verification mechanisms. (4) The transparency of cash flow, the source, destination and authenticity of CT’s can be confirmed through the blockchain, effectively preventing money laundering and suppressing fake transactions.

Based on the above statements, the application of CTs to internet-based community (P2P) or e-commerce financing platforms will effectively remove barriers in the application of SCF. It is applicable to non-specific fund demanders and providers, and it is universal and marketable. In addition, CT’s can of course also be applied for consumer finance, or crowdfunding. In reality, smart contracts for consumer finance (deployed address: 0xf6daae7777472be83633329c2733a9246ab6a1b1 for currency tokens, 0x8c51c69a6bc5d4836da8433ceefdc80e7e60ddd7 for obligation-type CTs, and 0x45176c52685298ae9e6944bfe67bc3924f12e1bb for obligation-type CTs, introduction video is at:

https://youtu.be/3O9Q8kwgsAo, accessed on 21 February 2023 ) and SCF (refer to

Appendix A) have been deployed in the test net, as well as on concept of proof platforms.

In addition, once the CT market is large enough, then CT’s can also be used in market transactions, just like crypto currencies generally do. The CT’s nature is much like a manufacturing issuing corporate bonds, with the market price depending on the financial status of core companies and on market interest rates. It will lead to a maximum capital efficiency in SCF, requiring further development in the future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}