Blockchain-Driven Optimal Strategies for Supply Chain Finance Based on a Tripartite Game Model

Abstract

:1. Introduction

2. Literature Review

2.1. Supply Chain Finance

2.2. “Blockchain + Supply Chain” Finance

2.3. Evolutionary Game Theory

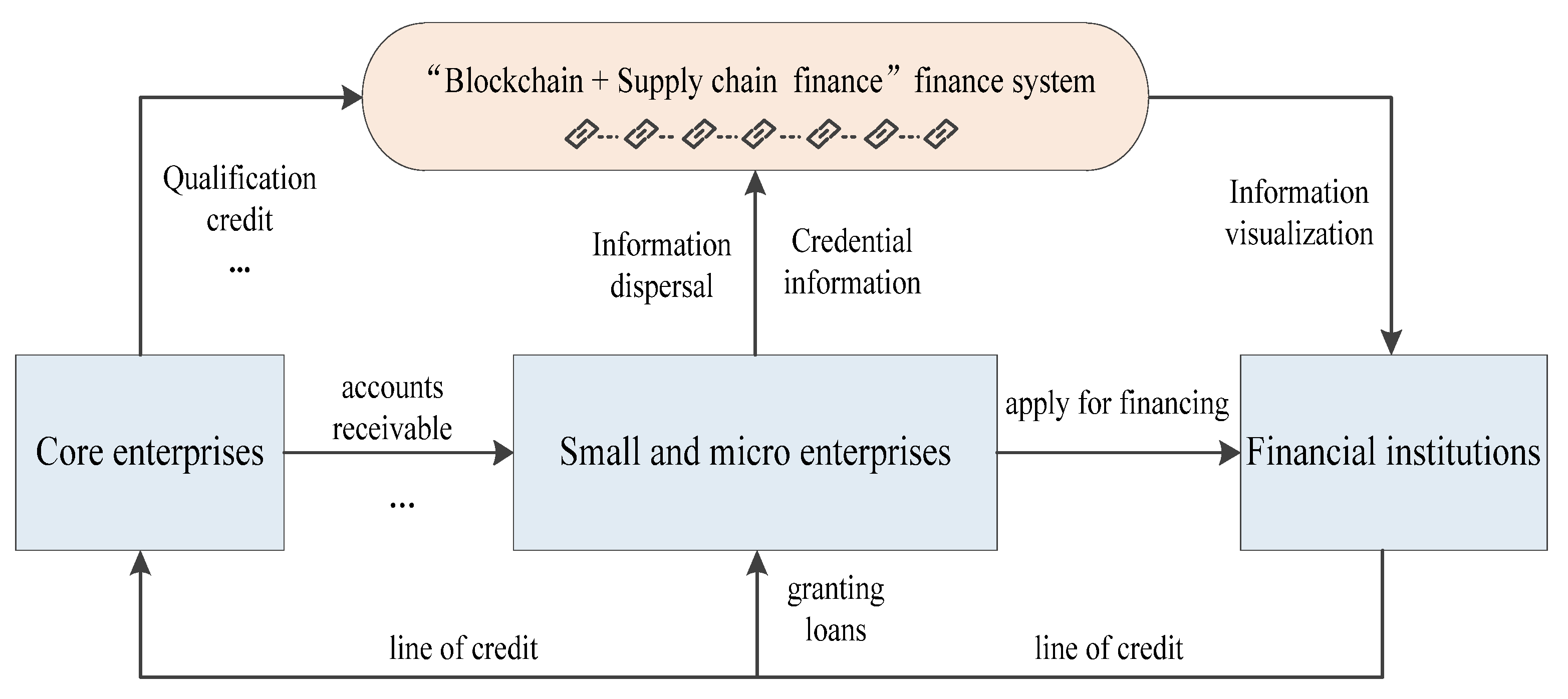

3. Problem Descriptions

3.1. Basic Descriptions of Problem

3.2. Basic Descriptions of Terminologies and Symbols

- (I)

- Supply chain finance: Supply chain finance is a mode in which two or more internal and external entities in the supply chain circulate financial resources within the supply chain organization through the design and implementation of management activities to create value through collaboration.

- (II)

- Pledge rate: Pledge rate refers to the ratio of loan principal to the market value of the standard warehouse receipt, which is generally determined fairly based on the price difference between the futures and spot, the price fluctuation range, the trend, and other factors.

- (III)

- Accounts receivable: Accounts receivable refers to the amount that an enterprise should collect from the purchasing unit due to the sale of goods, products, services, and other businesses in the normal course of business.

- (IV)

- Loan interest rate: The loan interest rate refers to the ratio of the interest amount to the principal amount during the loan term. The level of the loan interest rate directly determines the proportion of profits between the borrowing enterprises and banks, thus affecting the economic interests of both the borrowers and lenders.

- (V)

- Return on investment: Return on investment refers to the value that should be returned through investment; that is, the economic return of an enterprise from an investment activity. It covers the profit objectives of enterprises.

4. Model Development

4.1. Basic Assumptions

4.2. Evolutionary Analysis of Tripartite Game Model with the Dynamic Default Losses of Enterprises

4.3. Influence Analysis of Blockchain on the Parameters and Equilibrium Results

5. Simulation Analysis and Implications of the Results

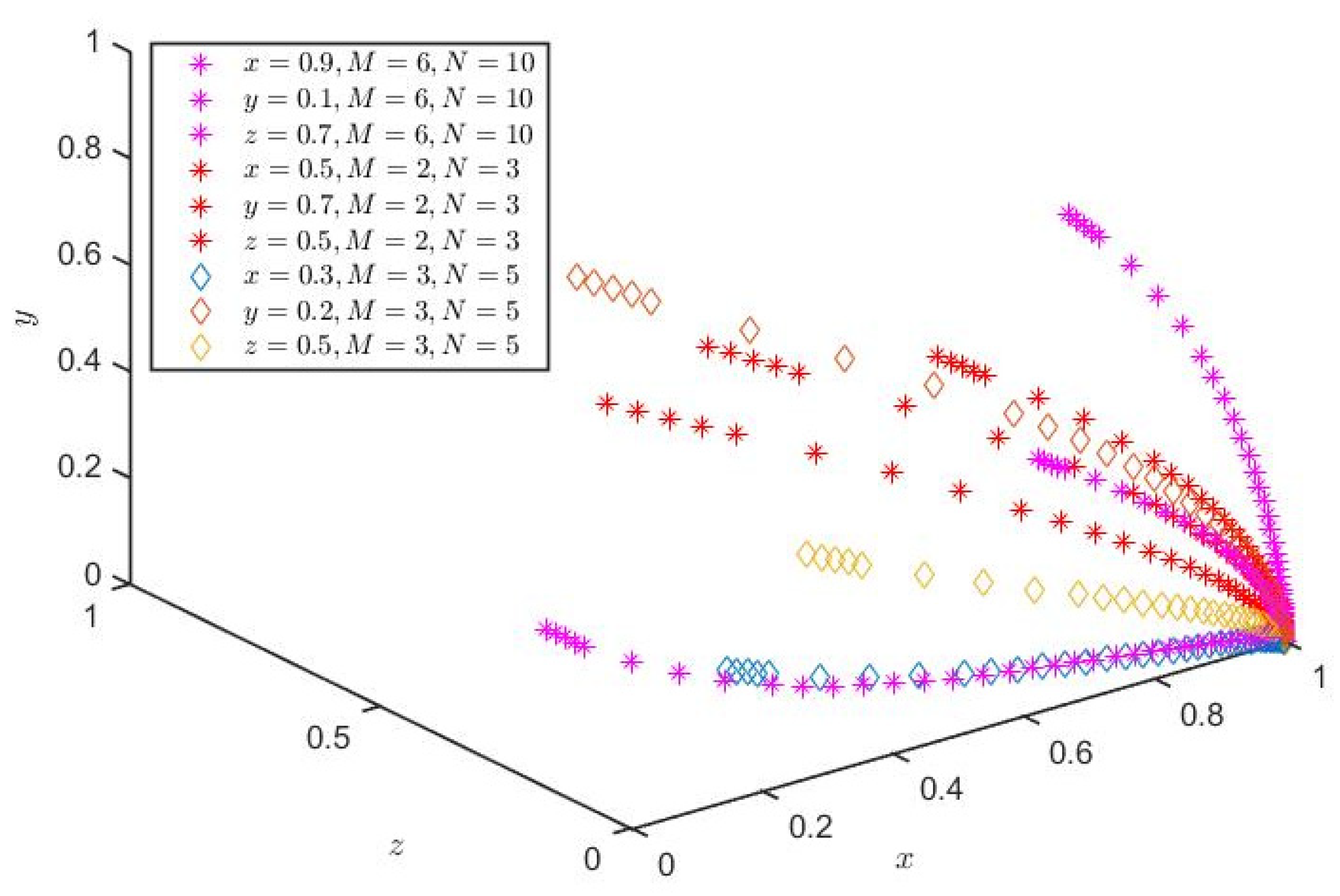

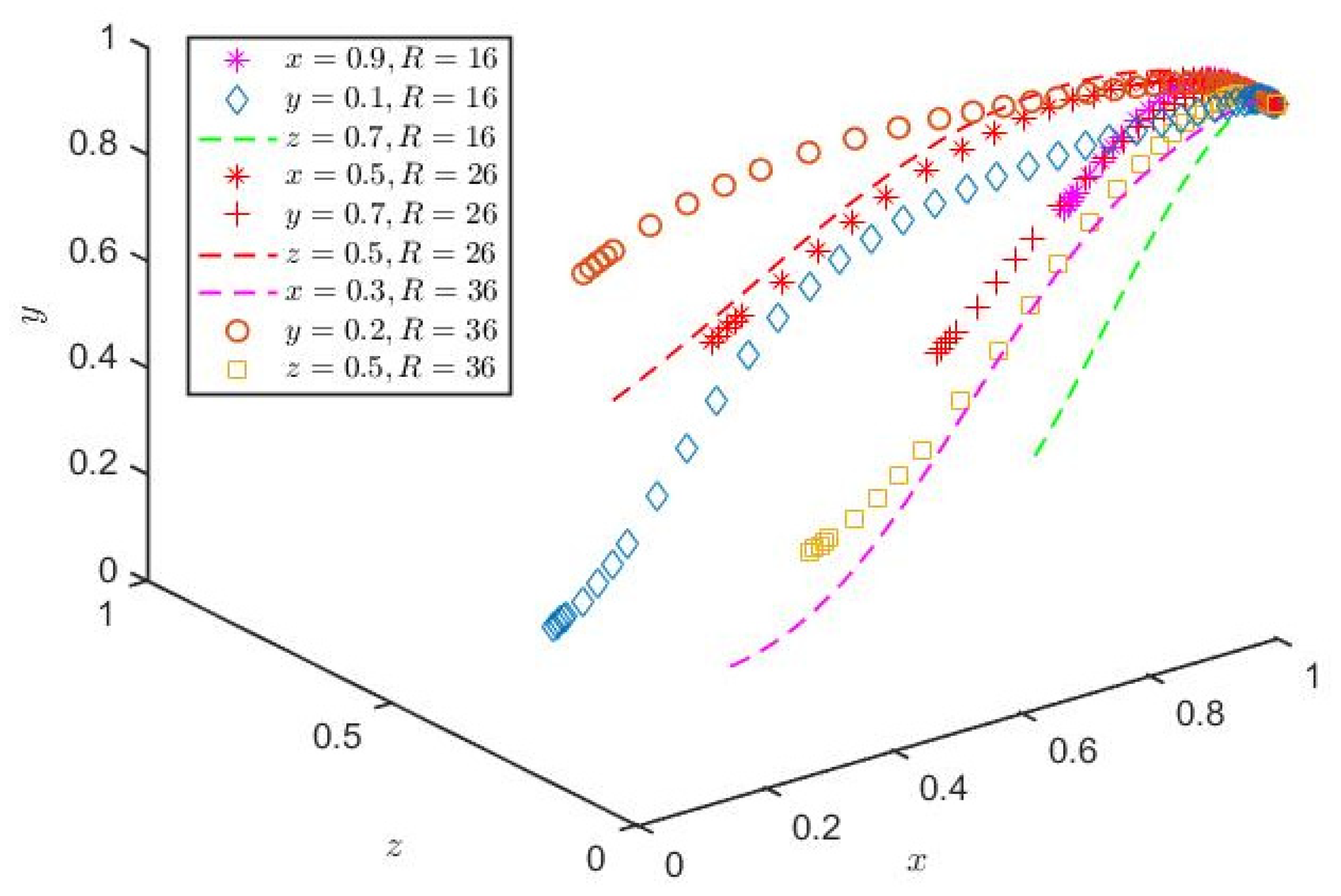

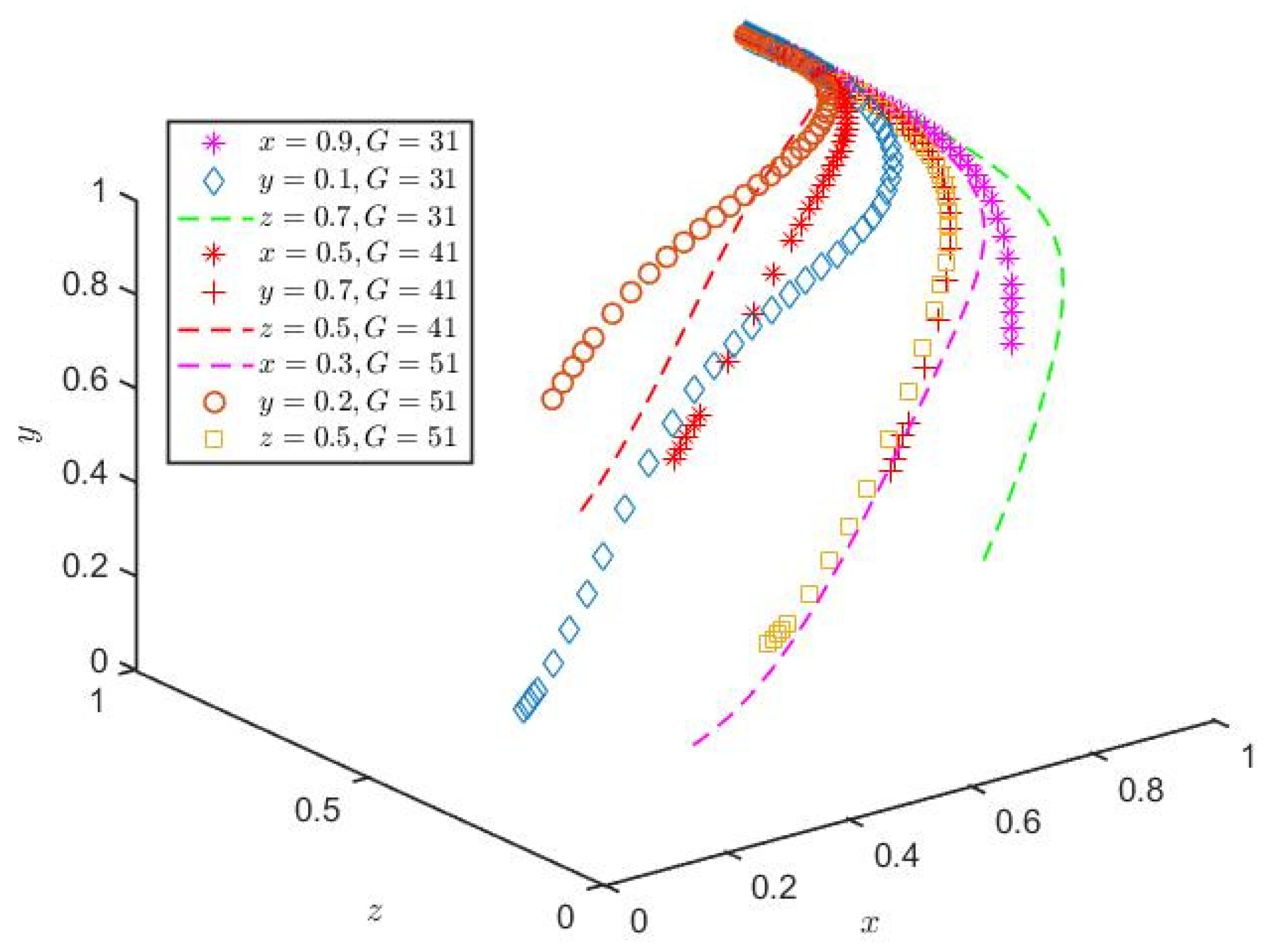

5.1. Analysis the Impact Path of Evolutionary Game Strategies under Different Main Parameters

5.2. Implications of the Results

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| SMZEs | Small and medium-sized enterprises |

| FIs | Financial institutions |

| CEs | Core enterprises |

| BT | Blockchain technology |

| TW | Traditional way |

| RDE | Replicated dynamic equation |

References

- Sun, R.; He, D.; Su, H. Evolutionary game analysis of blockchain technology preventing supply chain financial risks. J. Theor.Appl. Electron. Commer. Res. 2021, 16, 2824–2842. [Google Scholar] [CrossRef]

- Wu, S.; Mu, P.; Shen, J.; Wang, W. An incentive mechanism model of credit behavior of SMEs based on the perspective of credit default swaps. Complexity 2020, 2020, 1–8. [Google Scholar] [CrossRef]

- Li, Q.; Ji, H.; Huang, Y.M. The information leakage strategies of the supply chain under the block chain technology introduction. Omega 2022, 110, 102616. [Google Scholar] [CrossRef]

- Li, J.; Zhu, S.C.; Zhang, W.; Yu, L. Blockchain-driven supply chain finance solution for small and medium enterprises. Front. Eng. Manag. 2020, 7, 500–511. [Google Scholar] [CrossRef]

- Liu, L.; Li, Y.; Jiang, T. Optimal strategies for financing a three-level supply chain through blockchain platform finance. Int. J. Prod. Res. 2021. Early Access. [Google Scholar] [CrossRef]

- Yin, Y. Analysis of revenue incentive dynamic mechanism of financial supply chain from the perspective of the inter-net of things. Complexity 2021, 2021, 5595979. [Google Scholar] [CrossRef]

- Li, X. Debt financing cost evaluation method of shipping enterprises. J. Coast. Res. 2020, 103, 744–748. [Google Scholar] [CrossRef]

- Wang, X.; Han, L.; Huang, X. Bank market power and SME finance: Firm-bank evidence from European countries. J. Int. Financ.Mark.Inst. Money 2020, 64, 101162. [Google Scholar] [CrossRef]

- Dutta, P.; Choi, T.M.; Somani, S.; Butala, R. Blockchain technology in supply chain operations: Applications, challenges and research opportunities. Transp. Res. Part E: Logist. Transp. Rev. 2020, 142, 102067. [Google Scholar] [CrossRef]

- Gayialis, S.P.; Kechagias, E.P.; Papadopoulos, G.A.; Masouras, D. A Review and Classification Framework of Traceability Approaches for Identifying Product Supply Chain Counterfeiting. Sustainability 2022, 14, 6666. [Google Scholar] [CrossRef]

- Gayialis, S.P.; Kechagias, E.P.; Konstantakopoulos, G.D.; Papadopoulos, G.A.; Tatsiopoulos, I.P. An approach for creating a blockchain platform for labeling and tracing wines and spirits. In IFIP International Conference on Advances in Production Management Systems, 5–9 September 2021, Nantes, France; IFIP Advances in Information and Communication Technology; Springer: Berlin, Germany, 2021; pp. 81–89. [Google Scholar]

- Chen, J.; Chen, S.; Liu, Q.; Shen, M. Applying blockchain technology to reshape the service models of supply chain finance for SMEs in china. Singap. Econ. Rev. 2021, 1–18. [Google Scholar] [CrossRef]

- Gomm, M.L. Supply chain finance: Applying finance theory to supply chain management to enhance finance in supply chains. Int. J. Logist. Res. Appl. 2010, 13, 133–142. [Google Scholar] [CrossRef]

- Du, M.; Chen, Q.; Xiao, J.; Yang, H.; Ma, X. Supply chain finance innovation using blockchain. IEEE Trans. Eng. Manag. 2020, 67, 1045–1058. [Google Scholar] [CrossRef]

- Xu, X.; Chen, X.; Jia, F.; Brown, S.; Gong, Y.; Xu, Y. Supply chain finance: A systematic literature review and biblio-metric analysis. Int. J. Prod. Econ. 2018, 204, 160–173. [Google Scholar] [CrossRef]

- Blackman, I.D.; Holland, C.P.; Westcott, T. Motorola’s global financial supply chain strategy. Supply Chain. Manag. Int. J. 2013, 18, 132–147. [Google Scholar] [CrossRef] [Green Version]

- Tsai, S.B. A study on the service quality and competitive strategies of internet financing and FinTech from the perspective of internet finance law. In Economics and Management Innovations (ICEMI); Volkson Press: Cyberjaya, Malaysia, 2017; pp. 378–380. [Google Scholar]

- Wang, Z.; Wang, Q.; Lai, Y.; Liang, C. Drivers and outcomes of supply chain finance adoption: An empirical investigation in China. Int. J. Prod. Econ. 2020, 220, 107453. [Google Scholar] [CrossRef]

- Fu, Y.; Zhu, J. Big production enterprise supply chain endogenous risk management based on blockchain. IEEE Access 2019, 7, 15310–15319. [Google Scholar] [CrossRef]

- Sang, B. Application of genetic algorithm and BP neural network in supply chain finance under information sharing. J. Comput. Appl. Math. 2021, 384, 113170. [Google Scholar] [CrossRef]

- Wang, Y. Research on supply chain financial risk assessment based on blockchain and fuzzy neural networks. Wirel. Commun. Mob. Comput. 2021, 2021, 5565980. [Google Scholar] [CrossRef]

- Kim, K.; Lee, G.; Kim, S. A study on the application of blockchain technology in the construction industry. KSCE J. Civ. Eng. 2020, 24, 2561–2571. [Google Scholar] [CrossRef]

- Omran, Y.; Henke, M.; Heines, R.; Hofmann, E. Blockchain-driven supply chain finance: Towards a conceptual framework from a buyer perspective. In Proceedings of the 26th Annual IPSERA Conference, Budapest, Hungary, 9–12 April 2017. [Google Scholar]

- Jang, K.J. The a study on innovative financial services of business models using blockchain technology. E-Bus. Stud. 2017, 18, 113–130. [Google Scholar] [CrossRef]

- Hofmann, E.; Strewe, U.M.; Bosia, N. Supply Chain Finance and Blockchain Technology; Springer: Berlin, Germany, 2018. [Google Scholar]

- Malik, N.; Alkhatib, K.; Sun, Y.; Knight, E.; Jararweh, Y. A comprehensive review of blockchain applications in industrial internet of things and supply chain systems. Appl. Stoch. Model. Bus. Ind. 2021, 37, 391–412. [Google Scholar] [CrossRef]

- Thurner, T. Supply chain finance and blockchain technology—the case of reverse securitisation. Foresight 2018, 20, 447–448. [Google Scholar] [CrossRef]

- Babich, V.; Hilary, G. Distributed ledgers and operations: What operations management researchers should know about blockchain technology. Manuf. Serv. Oper. Manag. 2019, 22, 223–240. [Google Scholar] [CrossRef] [Green Version]

- Friedman, D. Evolutionary games in economics. Econometrica 1991, 59, 637–666. [Google Scholar] [CrossRef] [Green Version]

- Wang, J.; Peng, X.; Du, Y.; Wang, F.; Dnes, A. A tripartite evolutionary game research on information sharing of the subjects of agricultural product supply chain with a farmer cooperative as the core enterprise. Manag. Decis. Econ. 2021, 43, 159–177. [Google Scholar] [CrossRef]

- Sun, H.; Wan, Y.; Zhang, L.; Zhou, Z. Evolutionary game of the green investment in a two-echelon supply chain un-der a government subsidy mechanism. J. Clean. Prod. 2019, 235, 1315–1326. [Google Scholar] [CrossRef]

- Yan, N.; Sun, B.; Zhang, H.; Liu, C. A partial credit guarantee contract in a capital-constrained supply chain: Financing equilibrium and coordinating strategy. Int. J. Prod. Econ. 2016, 173, 122–133. [Google Scholar] [CrossRef]

- Zhang, B.; Wu, D.; Liang, L.; Olson, D.L. Supply chain loss averse newsboy model with capital constraint. IEEE Trans. Syst.ManCybernetics: Syst. 2016, 46, 646–658. [Google Scholar] [CrossRef]

- Zhang, B.; Ye, Y.; Yue, X. Evolutionary strategies of supply chain finance from the perspective of a return policy. IEEE Access 2019, 7, 110761–110769. [Google Scholar] [CrossRef]

- Yan, B.; Chen, Z.; Yan, C.; Zhang, Z.; Kang, H. Evolutionary multiplayer game analysis of accounts receivable financing based on supply chain financing. Int. J. Prod. Res. 2021. Early Access. [Google Scholar] [CrossRef]

- Li, X.Y. Analysis of SME financing model from the perspective of supply chain finance. Int. Core J. Eng. 2020, 6, 115–117. [Google Scholar]

- Aimin, D.; Bo, Y. Research overview of risk management of SMEs accounts receivable financing based on supply chain finance. World J. Res. Rev. 2017, 4, 16–20. [Google Scholar]

- Khalil, H.K.; Grizzle, J.W. Nonlinear Systems; Michigan State University: Prentice Hall, NJ, USA, 2002. [Google Scholar]

- Zhang, T.L.; Li, J.J.; Jiang, X. Analysis of supply chain finance based on blockchain. Procedia Comput.Sci. 2021, 187, 1–6. [Google Scholar] [CrossRef]

- Jiang, R.; Kang, Y.; Liu, Y.; Liang, Z.; Duan, Y.; Sun, Y.; Liu, J. A trust transitivity model of small and medium-sized manufacturing enterprises un-der blockchain-based supply chain finance. Int. J. Prod. Econ. 2022, 247, 108469. [Google Scholar] [CrossRef]

- Paliszkiewicz, J.; Chen, K. Trust, Organizations and the Digital Economy: Theory and Practice; Routledge: London, UK, 2021. [Google Scholar]

- Corradini, E.; Nicolazzo, S.; Nocera, A.; Ursino, D.; Virgili, L. A two-tier Blockchain framework to increase protection and autonomy of smart objects in the IoT. Comput. Commun. 2022, 181, 338–356. [Google Scholar] [CrossRef]

- Nicolazzo, S.; Nocera, A.; Ursino, D.; Virgili, L. A privacy-preserving approach to prevent feature disclosure in an IoT scenario. Future Gener. Comput. Syst. - Int. J. Escience 2020, 105, 502–519. [Google Scholar] [CrossRef]

- Wu, L.; Lu, W.; Xu, J. Blockchain-based smart contract for smart payment in construction: A focus on the payment freezing and disbursement cycle. Front. Eng. Manag. 2022, 9, 177–195. [Google Scholar] [CrossRef]

- Bonifazi, G.; Corradini, E.; Ursino, D.; Virgili, L. Defining user spectra to classify Ethereum users based on their behavior. J. Big Data 2022, 9, 1–39. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Symbols | Meanings | |

|---|---|---|

| decision variables | Pledge rate required by the FI, which is a constant | |

| Accounts receivable held by the SMZE | ||

| Loan interest rate of the FI | ||

| Investment return rate of the SMZEs after obtaining accounts receivable pledge financing | ||

| Marginal credit audit cost of the FIs under traditional supply chain financing | ||

| The blockchain and supply chain collaborative and trustworthy incentive income with both the SMZE being trustworthy and the CE choosing repayment | ||

| plain parameters | Proportion of collaborative and trustworthy incentive income for the SMZE | |

| The blockchain and supply chain collaborative and trustworthy incentive income with both the SMZE being trustworthy and the CE choosing repayment | ||

| Return rate of reinvestment after deferred payment of accounts payable by the CE | ||

| Default loss of the SMZE under supply chain financing using BT and the traditional way (TW) | ||

| Default loss of the CE under supply chain financing using BT and TW | ||

| The extra benefits of the SMZE under supply chain financing using BT |

| Strategies | FI | ||||

|---|---|---|---|---|---|

| B1 | B2 | ||||

| CE | C1 | SMZE | A1 | ||

| A2 | |||||

| C2 | SMZE | A1 | |||

| A2 | |||||

| Equilibrium Points | |||

|---|---|---|---|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Su, L.; Cao, Y.; Li, H.; Tan, J. Blockchain-Driven Optimal Strategies for Supply Chain Finance Based on a Tripartite Game Model. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 1320-1335. https://doi.org/10.3390/jtaer17040067

Su L, Cao Y, Li H, Tan J. Blockchain-Driven Optimal Strategies for Supply Chain Finance Based on a Tripartite Game Model. Journal of Theoretical and Applied Electronic Commerce Research. 2022; 17(4):1320-1335. https://doi.org/10.3390/jtaer17040067

Chicago/Turabian StyleSu, Limin, Yongchao Cao, Huimin Li, and Jian Tan. 2022. "Blockchain-Driven Optimal Strategies for Supply Chain Finance Based on a Tripartite Game Model" Journal of Theoretical and Applied Electronic Commerce Research 17, no. 4: 1320-1335. https://doi.org/10.3390/jtaer17040067

APA StyleSu, L., Cao, Y., Li, H., & Tan, J. (2022). Blockchain-Driven Optimal Strategies for Supply Chain Finance Based on a Tripartite Game Model. Journal of Theoretical and Applied Electronic Commerce Research, 17(4), 1320-1335. https://doi.org/10.3390/jtaer17040067