Detecting Chaos from Agricultural Product Price Time Series

Abstract

:1. Introduction

2. Data Preprocessing

3. Tests for Nonlinearity and Fractality

3.1. The BDS Test

3.2. The R/S Analysis

4. Detecting Chaos

4.1. Power Spectrum

4.2. The Phase Space Reconstruction

4.2.1. The Mutual Information Method

4.2.2. Cao’s Method

4.3. Recurrence Plot and Recurrence Quantification Analysis

4.4. The Correlation Dimension and Kolmogorov Entropy

4.5. The Largest Lyapunov Exponent

4.5.1. Determine the Mean Period

4.5.2. Calculate the Largest Lyapunov Exponent

5. Empirical Analyses

5.1. Statistical Description and Stationary Tests

5.2. Tests for Nonlinearity

5.2.1. The BDS Test

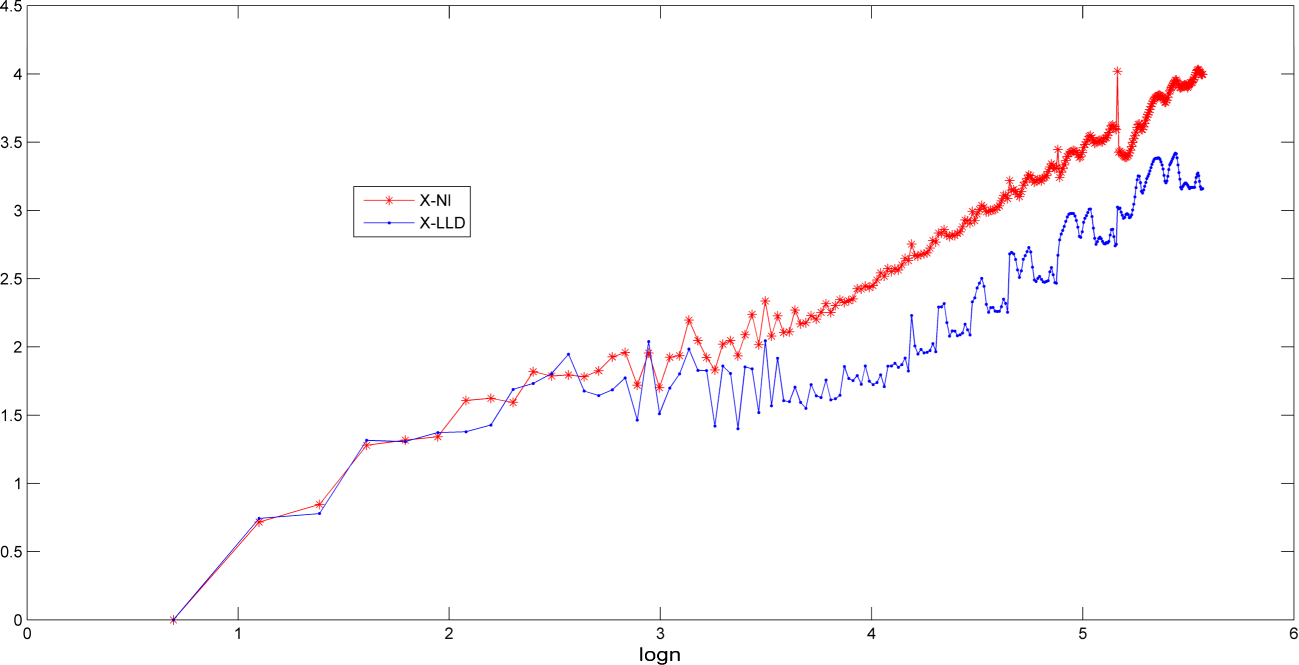

5.2.2. The R/S Analysis

5.3. Detecting Chaos

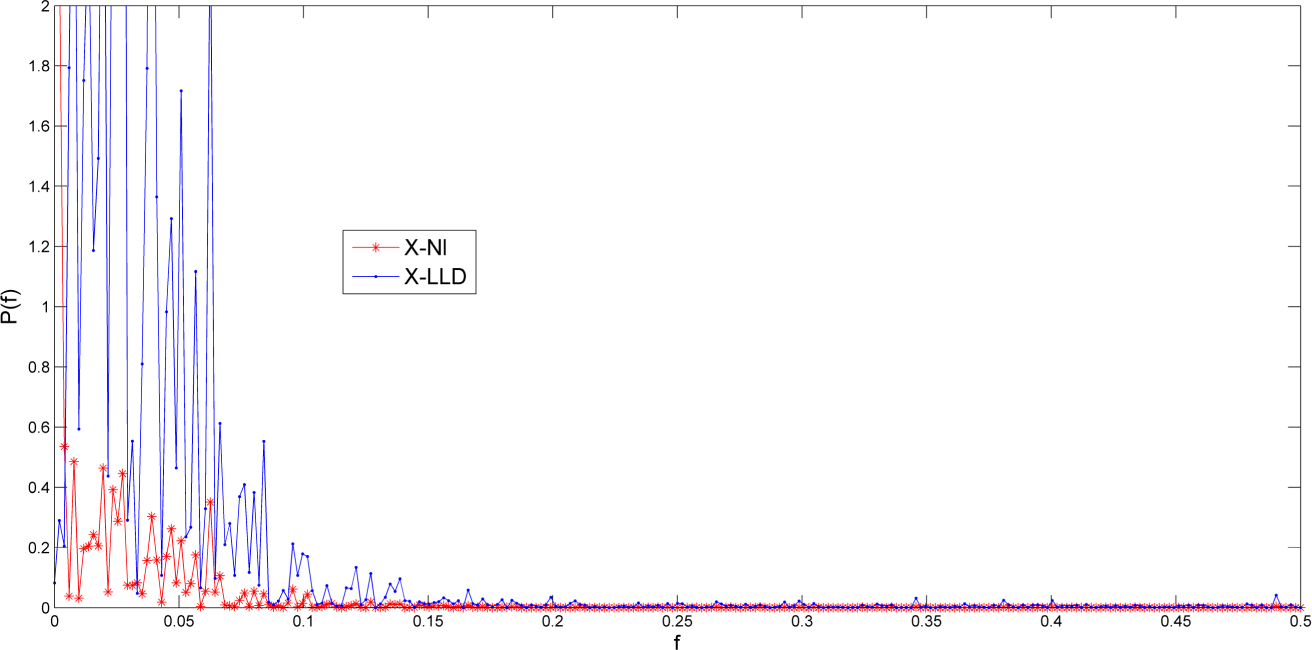

- We plot the power spectrum of XNl and XLLD (see Figure 2), which are decaying, continuous, and not flat.

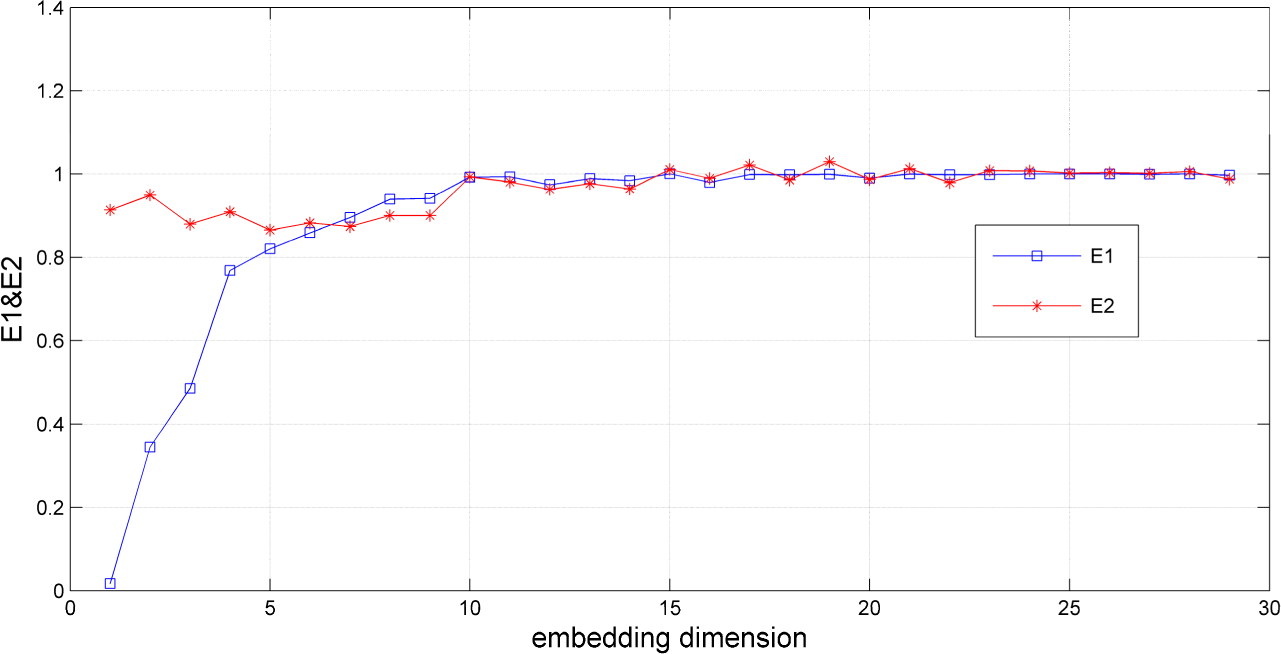

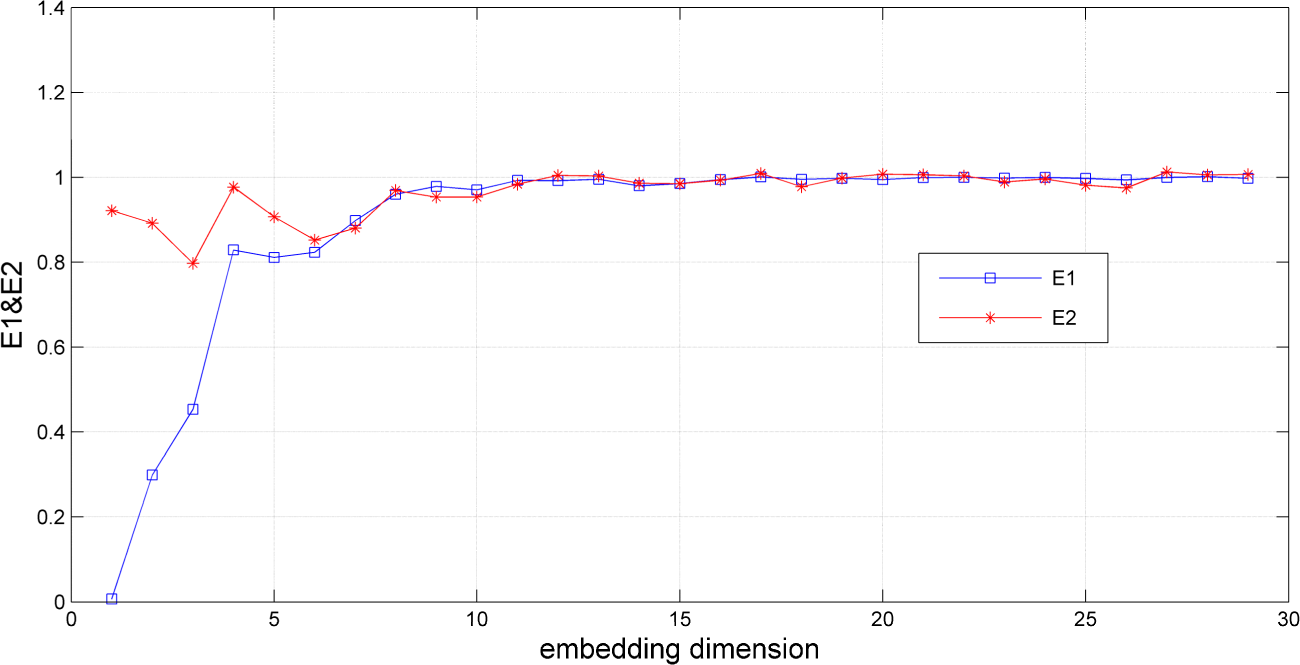

- The phase space is reconstructed using delays and dimensions as selected respectively (see Table 5) from mutual information function and false nearest neighbors. From Figures 3 and 4, it can be seen that E2 increase with m increasing and tend to 1 eventually. Both of the time series exhibit the chaotic behavior instead of the stochastic one.

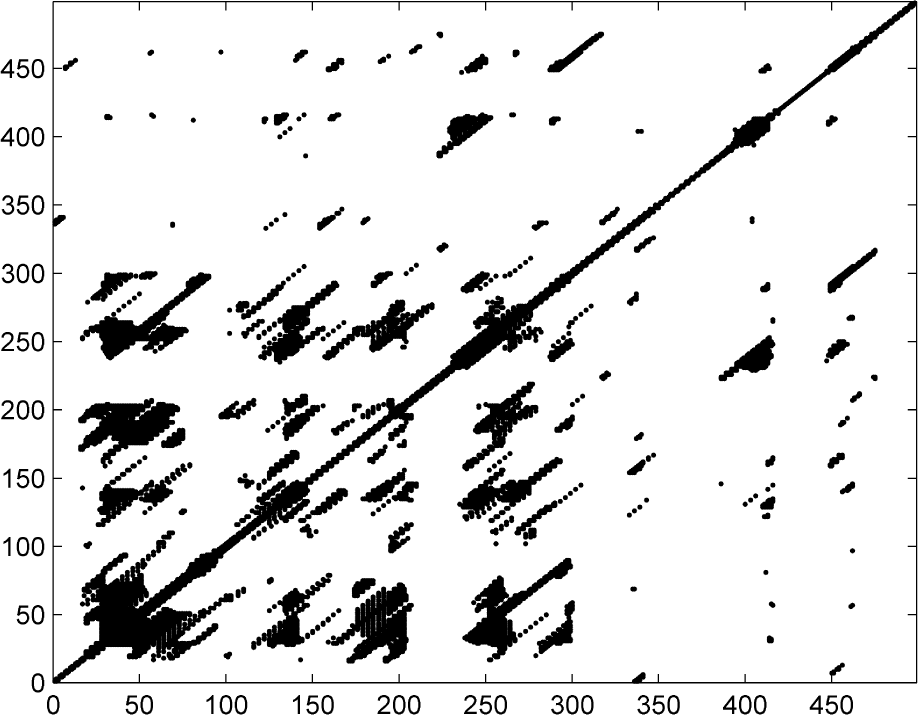

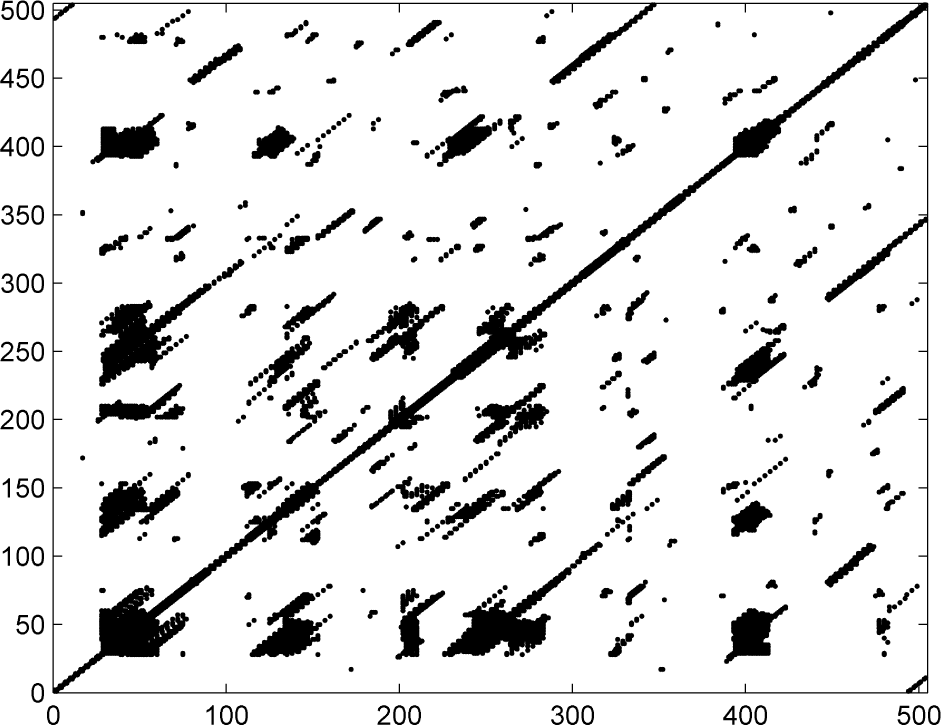

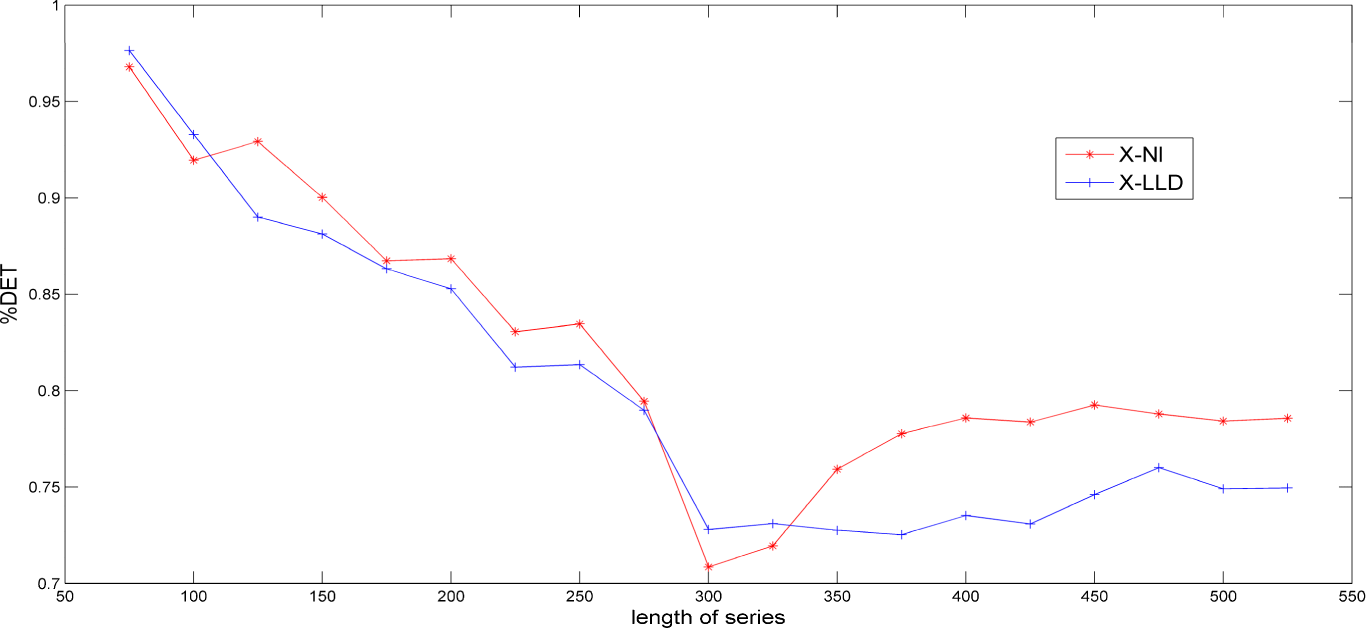

- The RPs are shown in Figures 5 and 6 after selecting the standard deviations as the threshold radius. Very short diagonals can be seen in these figures, which indicate chaotic behavior.We draw the %DET plots of the two time series which show the %DET changes with increasing time (see Figure 7, the red curve is for XNl and the blue one is for XLLD). We can see that the %DET tend to stable values. The %DET of XNl and XLLD are 0.7842 and 0.7479, respectively. We also calculate the %DET values of a random series, a sine series and a logistic series (μ = 4) with the same sample capacity 525. The results are 0.4229, 0.9969, 0.7627, respectively. Hence, the determinism of our time series are stronger than that of random series, are weaker than that of sine series and are similar to that of logistic series. Since the logistic series is chaotic when (μ = 4), it is possible that our series are chaotic, too. The series XNl shows stronger determinism than XLLD.

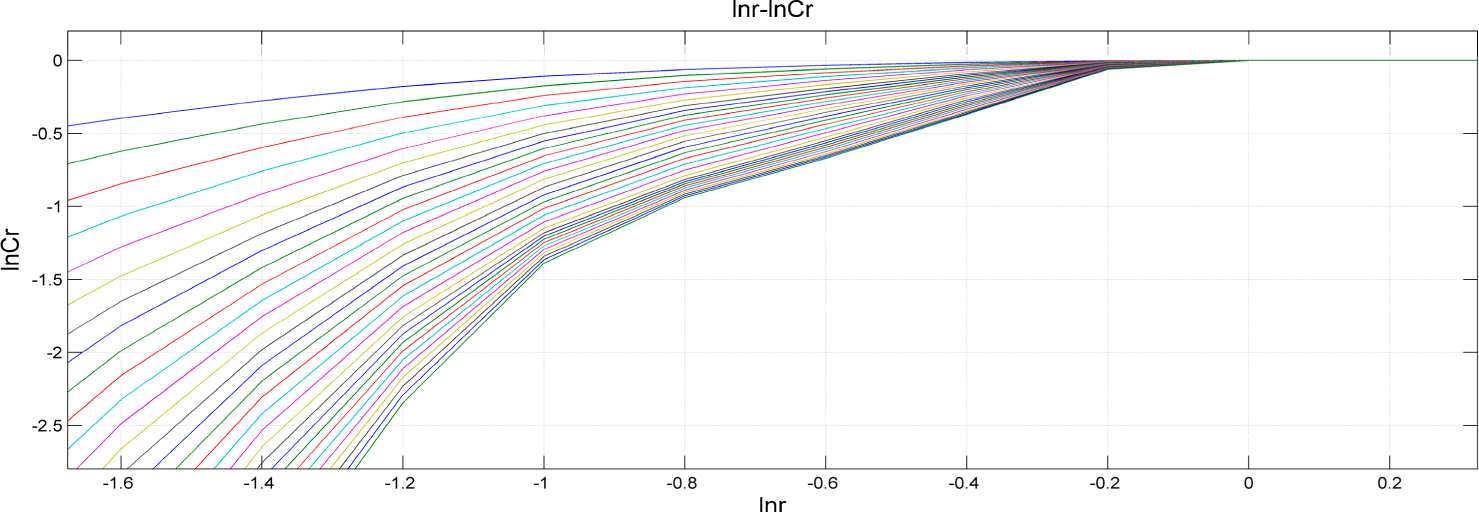

- We compute D2, K2, and the largest Lyapunov exponents λ of the two time series. All the results are listed in Figure 5. When we observe the plot of lnr~lnC(m, N, r, τ), we can get many linear scaling regions (for example, see Figure 8, the plot of XNllnr~lnC(m, N, r, τ)). Therefore, in order to determine the optimal linear scaling region, we compute the derivatives and the second-order derivatives of lnr~lnC(r) curves and draw the plots of lnr~lnC′(r) and lnr~lnC″(r) (for example, see Figure 9, the XNl plots of lnr~lnC'(r) and lnr~lnC″(r)) according to the new algorithm in this paper. Then we can find out the optimal linear scaling region (for example, see Figure 9, the interval [−0.8,−0.6] is optimal). The values of D2, K2 can be obtained in the scaling regions. Following the algorithms of weighted averages and Rosenstein, we can estimate the mean period p and the largest Lyapunov exponent λ (see Figure 5).

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Raneses, A.R.; Glaser, L.K.; Price, J.M.; Duffield, J.A. Potential biodiesel markets and their economic effects on the agricultural sector of the United States. Ind. Crops Prod 1999, 9, 151–162. [Google Scholar]

- Tokgoz, S. The Impact of Energy Markets on the Eu Agricultural Sector; Working Paper 09-WP485; Center for Agricultural and Rural Development, Iowa State University: Ames, IA, USA, 2009. [Google Scholar]

- Benavides, G. Price Volatility Forecasts for Agricultural Commodities: An Application of Historical Volatility Models, Option Implied and Composite Approaches for Futures Prices of Corn and Wheat; Central Bank of Mexico: Mexico City, Mexico, 2004. [Google Scholar]

- Mitra, S.; Boussard, J. A simple model of endogenous agricultural commodity price fluctuations with storage. Agric. Econ 2012, 43, 1–15. [Google Scholar]

- Garner, C.A. Commodity prices: Policy target or information variable note. J. Money Credit Bank 1989, 21, 508–514. [Google Scholar]

- Pindyck, R.S.; Rotemberg, J.J. The excess co-movement of commodity price. Econ. J 1990, 100, 1173–1189. [Google Scholar]

- Cheng, G.; Hu, B.; Xu, X. An analysis of the impact of the new round of rise in the prices of agricultural produce. Manag. World 2008, 1, 57–62. [Google Scholar]

- Xu, X. The New-round fluctuation cycle of agricultural products prices: Characteristics, mechanism and effects. J. Financ. Econ 2008, 34, 110–119. [Google Scholar]

- Ma, J.; Liu, L. Multivariate Nonlinear Analysis and Prediction of Shanghai Stock Market. Discret. Dyn. Nat. Soc 2008, 2008, 526734. [Google Scholar]

- Ma, J.; Cui, Y.; Liu, L. Hopf bifurcation and chaos of financial system on condition of specific combination of parameters. J. Syst. Sci. Complex 2008, 21, 250–259. [Google Scholar]

- Ma, J.; Wang, Z.; Chen, Y. Prediction techniques of chaotic time series and its applications at low noise level. Appl. Math Mech 2006, 1, 7–14. [Google Scholar]

- Hommes, C.H. Dynamics of the cobweb model with expectations and nonlinear supply and adaptive demand. J. Econ. Behav. Organ 1994, 24, 315–335. [Google Scholar]

- Onozaki, T.; Sieg, G.; Yokoo, M. Complex dynamics in a cobweb model with adaptive production adjustment. J. Econ. Behav. Organ 2000, 41, 101–115. [Google Scholar]

- Commendatore, P.; Currie, M. The cobweb, borrowing and financial crises. J. Econ. Behav. Organ 2008, 66, 625–640. [Google Scholar]

- Mandelbert, B.B. New method in statistical economics. J. Polit. Econ 1963, 71, 421–440. [Google Scholar]

- Corazza, M.; Malhairs, A.; Nardelli, C. Searching for fractal structure in agricultural futures markets. J. Futures Mark 1997, 17, 433–473. [Google Scholar]

- Barkoulas, J.T.; Labys, W.C.; Onochie, J.I. Long memory in futures prices. Finical Rev 1999, 34, 91–95. [Google Scholar]

- Wei, A.; Leuthold, R.M. Agricultural Futures Prices and Long Memory Processes; Working Paper 00-04; Office for Futures and Options Research, University of Illinois at Urbana-Champaign: Champaign, IL, USA, 2000. [Google Scholar]

- Yang, S.R.; Brorsen, B.W. Nonlinear dynamics of daily cash prices. Am. J. Agric. Econ 1992, 74, 706–715. [Google Scholar]

- Yang, S.R.; Brorsen, B.W. Nonlinear dynamics of daily futures prices: Conditional heteroscedasticity or chaos? J. Futures Mark 1993, 13, 175–191. [Google Scholar]

- Michael, J., Jr.; Onochie, J. A bivariate generalized autoregressive conditional heteroscedasticity-in-mean study of the relationship between return variability and trading volume in international futures markets. J. Futures Mark 1998, 18, 379–397. [Google Scholar]

- Bhar, R. Return and Volatility Dynamics in the Spot and Futures Markets in Australia: An Intervention Analysis in a Bivariate EGARCH-X Framework. J. Futures Mark 2001, 21, 833–850. [Google Scholar]

- Papaioannou, G.; Karytinos, A. Nonlinear time series analysis of the stock exchange: The case of an emerging market. Int. J. Bifurc. Chaos 1995, 5, 1557–1584. [Google Scholar]

- Chen, P. A random-walk or color-chaos on the stock market?-time-frequency analysis of S&P indexes. Stud. Nonlinear Dyn. Econom 1996, 1, 87–103. [Google Scholar]

- Rolo-Naranjo, A.; Montesino-Otero, M. A method for the correlation dimension estimation for online condition monitoring of large rotating machinery. Mech. Syst. Signal Process 2005, 19, 939–954. [Google Scholar]

- Fraser, A.M.; Swinney, H.L. Independent coordinates for strange attractors from mutual information. Phys. Rev. A 1986, 33, 1134–1140. [Google Scholar]

- Cao, L.Y. Practical method for determining the minimum embedding dimension for a scalar time series. Physica D 1997, 110, 43–50. [Google Scholar]

- Faggini, M. Chaos detection in economics. In Metric versus Topological Tools; MPRA Paper 30928; Munich Personal RePEc Archive: Munich, Germany, 2011. [Google Scholar]

- Webber, C.L., Jr. Dynamical assessment of physiological systems and states using recurrence plot strategies. J. Appl. Physiol 1994, 76, 965–973. [Google Scholar]

- Zbilut, J.P.; Giuliani, A.; Webber, C.L., Jr. Recurrence quantification analysis as an empirical test to distinguish relatively short deterministic versus random number series. Phys. Lett. A 2000, 267, 174–178. [Google Scholar]

- Grassberger, P.; Rorcaccia, I. Measuring the strangeness of strange attractors. Physica D 1983, 9, 189–208. [Google Scholar]

- Grassberger, P.; Rorcaccia, I. Estimation of the Kolmogorov entropy from a chaotic signal. Phys. Rev. Lett 1983, 28, 2591–2593. [Google Scholar]

- Zhao, G.; Shi, Y.; Duan, W.; Yu, H. Computing fractal dimension and the Kolmogorov entropy from chaotic time series. Chin. J. Comput. Phys 1999, 16, 309–315. [Google Scholar]

- Rosenstein, M.T.; Collins, J.J.; de Luca, C.J. A practical method for calculating largest Lyapunov exponents from small data sets. Physica D 1993, 65, 117–134. [Google Scholar]

- Yang, Y.; Wu, M.; Gao, Z.; Wu, Y.; Ren, X. Parameters selection for calculating largest Lyapunov exponent for small data sets. J. Vib. Meas. Diagn 2012, 32, 371–374. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Average | Std. Dev. | Kurtosis | Skewness | Jarque-Bera/Prob. | ADF/Prob. | PP/Prob. | |

|---|---|---|---|---|---|---|---|

| XNl | 0.2777 | 0.1624 | 5.2782 | 1.2559 | 251.5453/0.0000 | −3.3862/0.0007 | −2.6754/0.0074 |

| XLLD | 7.62 × 10−12 | 0.4614 | 2.9657 | −0.4023 | 14.18629/0.0008 | −5.7027/0.0000 | −7.452/0.0000 |

| 0.5σ1 | 1.0σ1 | 1.5σ1 | 2.0σ1 | |

|---|---|---|---|---|

| m = 2 | 7.8591/0.0000 | 5.4748/0.0000 | 4.1701/0.0000 | 5.968/0.0000 |

| m = 3 | 7.6953/0.0000 | 2.8132/0.0049 | 4.9304/0.0000 | 7.1725/0.0000 |

| m = 4 | −6.132/0.0000 | 2.25/0.0045 | 10.9701/0.0000 | 10.8574/0.0000 |

| m = 5 | −3.762/0.0002 | −4.7486/0.0000 | 11.0967/0.0000 | 13.5797/0.0000 |

| 0.5σ2 | 1.0σ2 | 1.5σ2 | 2.0σ2 | |

|---|---|---|---|---|

| m = 2 | 4.7493/0.0000 | 3.3066/0.0009 | 3.0615/0.0000 | 3.4306/0.0006 |

| m = 3 | 2.9711/0.003 | 2.9031/0.0037 | 3.808/0.0000 | 3.2573/0.0011 |

| m = 4 | 3.7979/0.0001 | 3.4747/0.0005 | 4.3133/0.0000 | 2.9763/0.0029 |

| m = 5 | 18.3401/0.0000 | 3.4747/0.0005 | 6.1617/0.0000 | 2.7693/0.0056 |

| H | C | D | t | |

|---|---|---|---|---|

| XNl | 0.8399 | 0.6019 | 1.1601 | 6.024 |

| XLLD | 0.7199 | 0.3565 | 1.2801 | 3.275 |

| τ | m | p | D2 | K2 | λ | |

|---|---|---|---|---|---|---|

| XNl | 3 | 10 | 2.2957 | 1.2625 | 0.0045 | 0.00064 |

| XLLD | 3 | 8 | 2.0048 | 4.7185 | 0.0195 | 0.00025 |

© 2014 by the authors; licensee MDPI, Basel, Switzerland This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Su, X.; Wang, Y.; Duan, S.; Ma, J. Detecting Chaos from Agricultural Product Price Time Series. Entropy 2014, 16, 6415-6433. https://doi.org/10.3390/e16126415

Su X, Wang Y, Duan S, Ma J. Detecting Chaos from Agricultural Product Price Time Series. Entropy. 2014; 16(12):6415-6433. https://doi.org/10.3390/e16126415

Chicago/Turabian StyleSu, Xin, Yi Wang, Shengsen Duan, and Junhai Ma. 2014. "Detecting Chaos from Agricultural Product Price Time Series" Entropy 16, no. 12: 6415-6433. https://doi.org/10.3390/e16126415

APA StyleSu, X., Wang, Y., Duan, S., & Ma, J. (2014). Detecting Chaos from Agricultural Product Price Time Series. Entropy, 16(12), 6415-6433. https://doi.org/10.3390/e16126415