Examining the Research on Business Information-Entropy Correlation in the Accounting Process of Organizations

Abstract

:1. Introduction

- (i)

- How did scientific production on the subject evolve during the 1974–2020 period?

- (ii)

- What are the main journals that have been published on this subject and how do they collaborate with each other?

- (iii)

- What are the collaborative relationships between the main research drivers?

- (iv)

- What are the main lines of research developed between 1974 and 2020 and future directions?

2. Literature Review

3. Materials and Methods

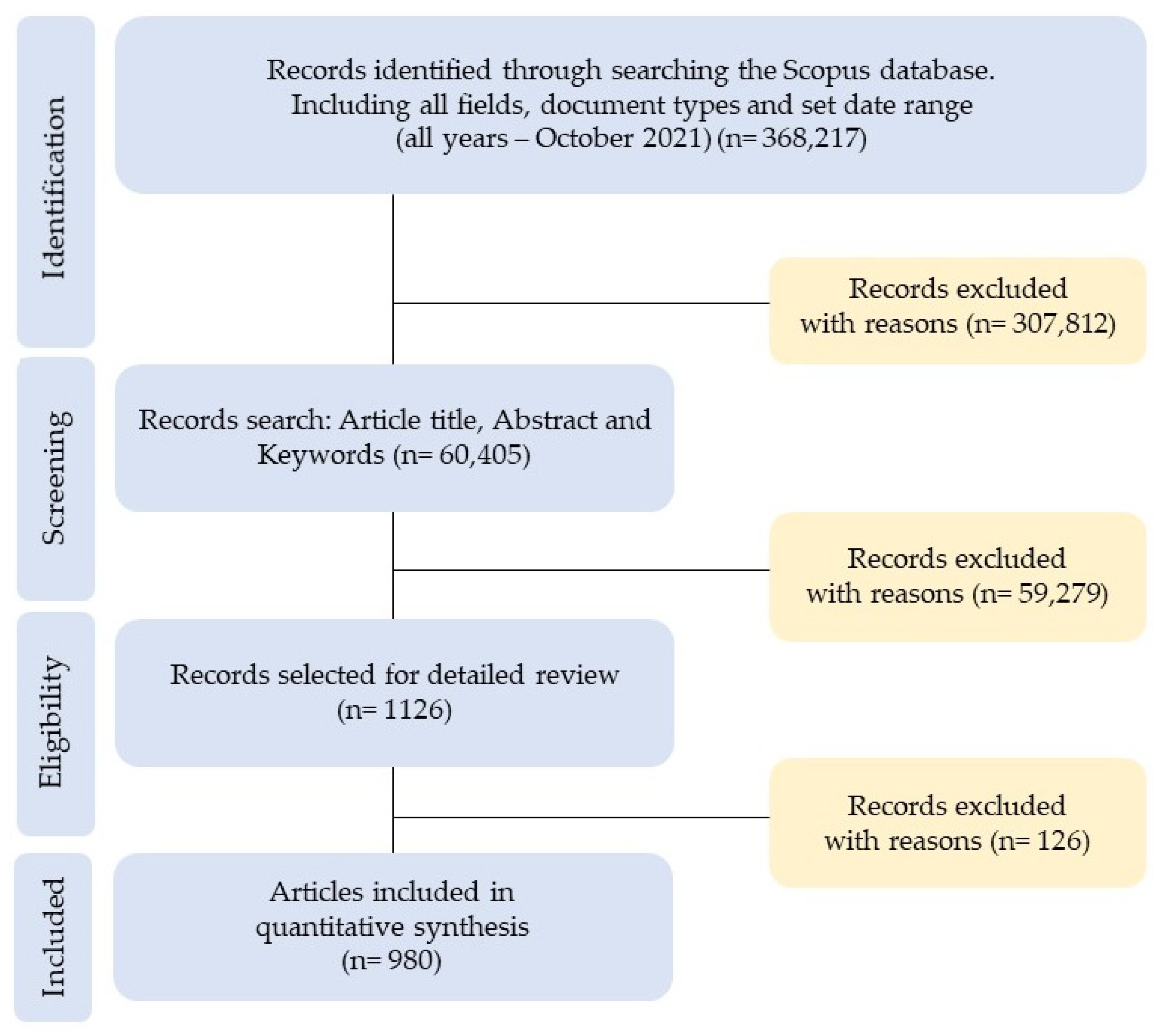

- Identification: 368,217 records were identified from the Scopus database, considering “all fields” for each of the key search terms (“entropy,” “accounting,” “information,” and “business”), “all types of documents,” and all data published in the “data range” (all years–October 2021).

- Screening: the option of “article title, abstract, and keywords” was chosen in the field of each key term, and 307,812 records were excluded.

- Eligibility: Of those 60,405 records, only “articles” were selected as the document type and “journal” as the source type, to ensure the quality of the peer review process. Furthermore, only the following subject areas were included: (i) Economics, Econometrics and Finance and (ii) Business, Management and Accounting. In this phase, 59,279 records were excluded.

- Included: The data referring to the “all years–2020” period were selected, that is, from the first article on the research topic (1974) to the last full year (2020). In this last phase, of the 1126 records, 146 documents were excluded, so the final sample included 980 articles, both open access and non-open access.

- Item: Items are the objects of interest in the maps created, viewed, and explored with VOSviewer, which can be publications, authors, countries, institutions, journals, or keywords.

- Network: This is a set of elements together with the links between the elements.

- Cluster: This is a set of elements included in a map. These do not overlap in VOSviewer, that is, an item can belong to only one group. There may be items that do not belong to any cluster. Groups are labeled with group numbers.

- Attribute: Elements can have multiple attributes, that is, if elements have been assigned to groups, the group numbers are n attributes. Weight and score attributes stand out and are represented by numeric values.

- Weight: Weight attributes are restricted to non-negative values. Score attributes do not have this restriction. The weight of an item indicates the importance of the item. When viewing a map, items with a higher weight are displayed more prominently than items with a lower weight. Items can have multiple weights and scoring attributes. There are two weight attributes: Links and Total Link Strength.

- Links: For a given element, this indicates the number of links of an article with other articles.

- Total Link Strength: For a given element, this indicates the total strength of the links of an article with other articles.

- Occurrence: In VOSviewer, when working with keywords, the occurrences attribute indicates the number of documents in which a keyword appears.

4. Results and Discussion

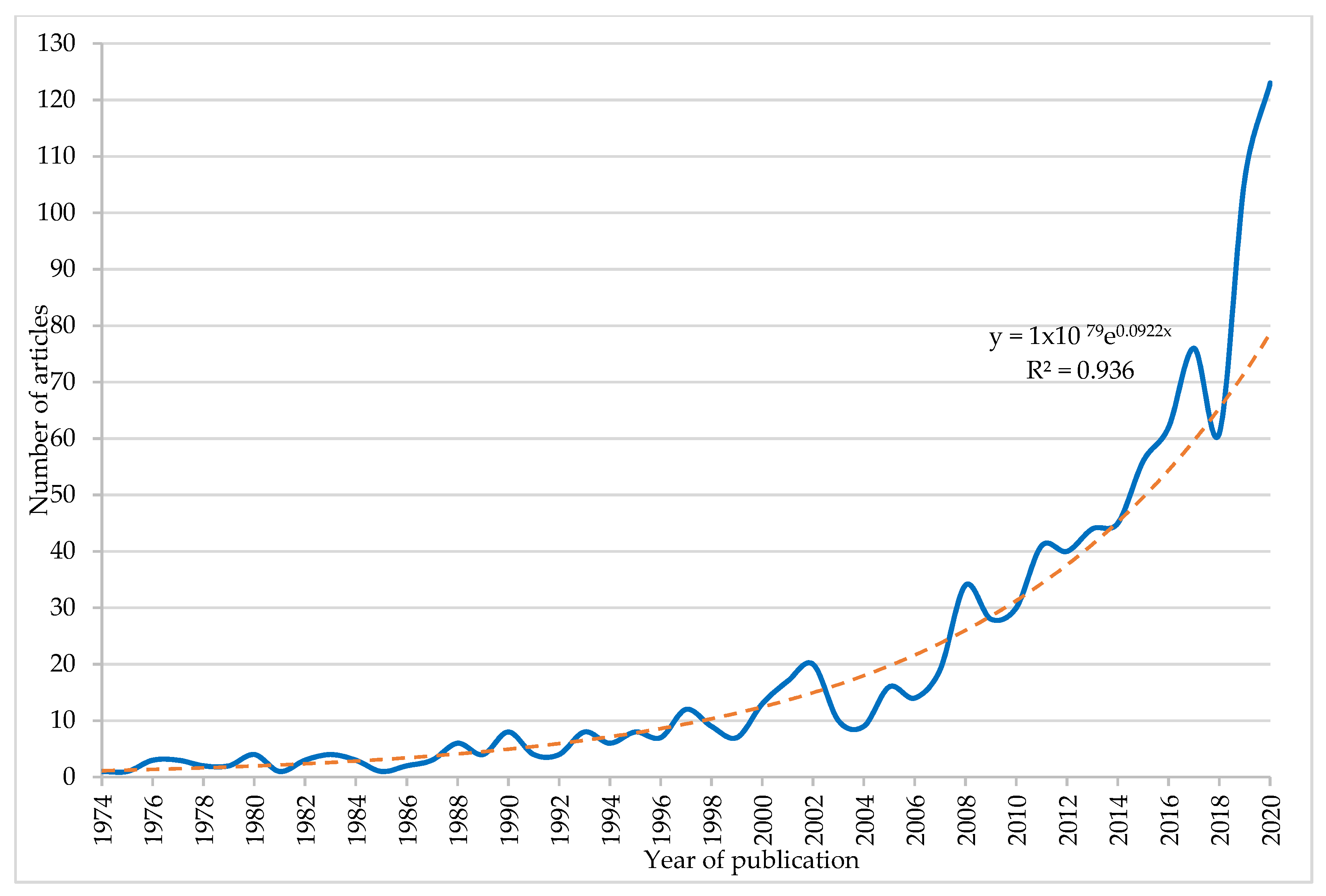

4.1. Scientific Production (1974–2020)

4.1.1. Evolution of the Number of Articles Published

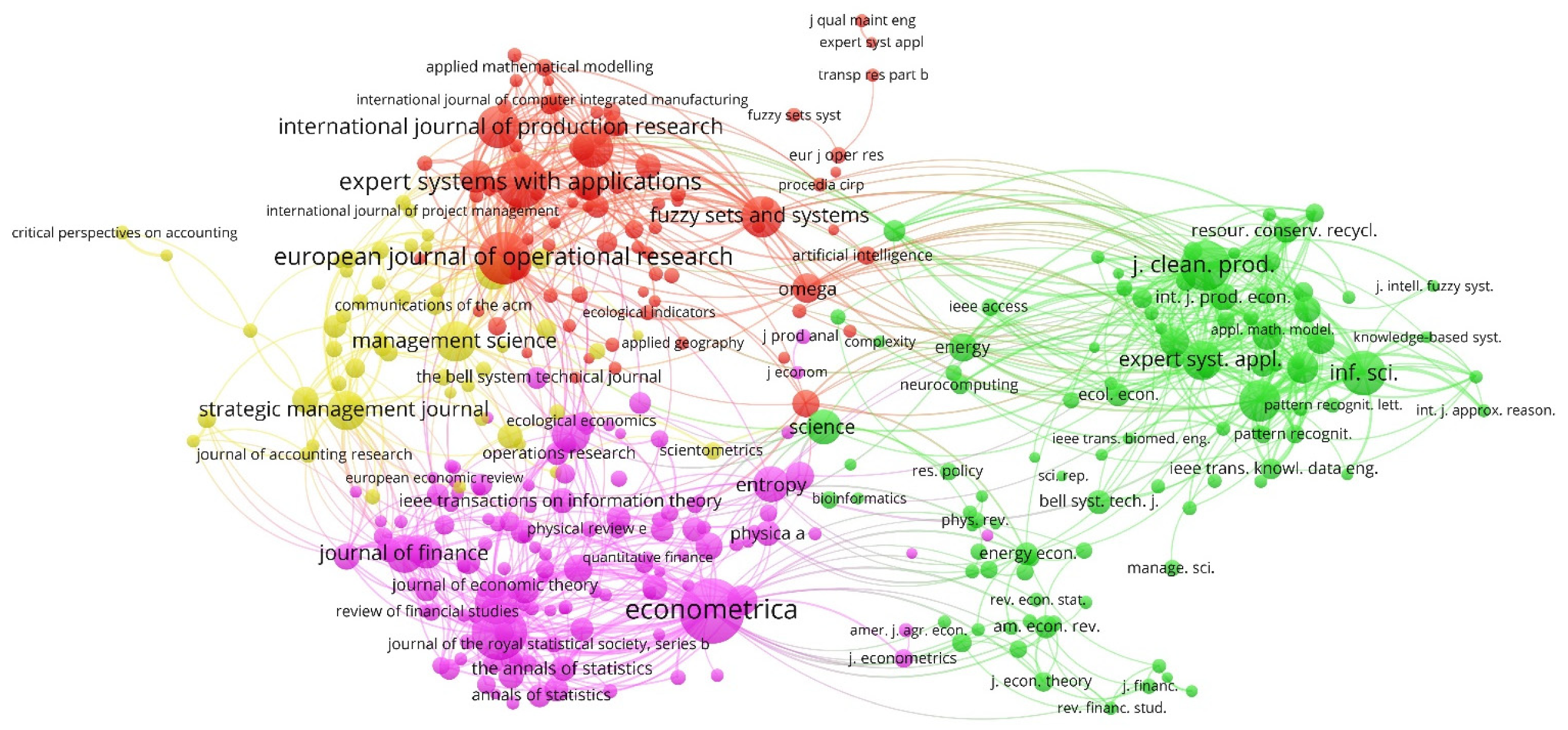

4.1.2. Journals

4.1.3. Main Articles Published

4.2. Analysis of the Main Drivers of the Research

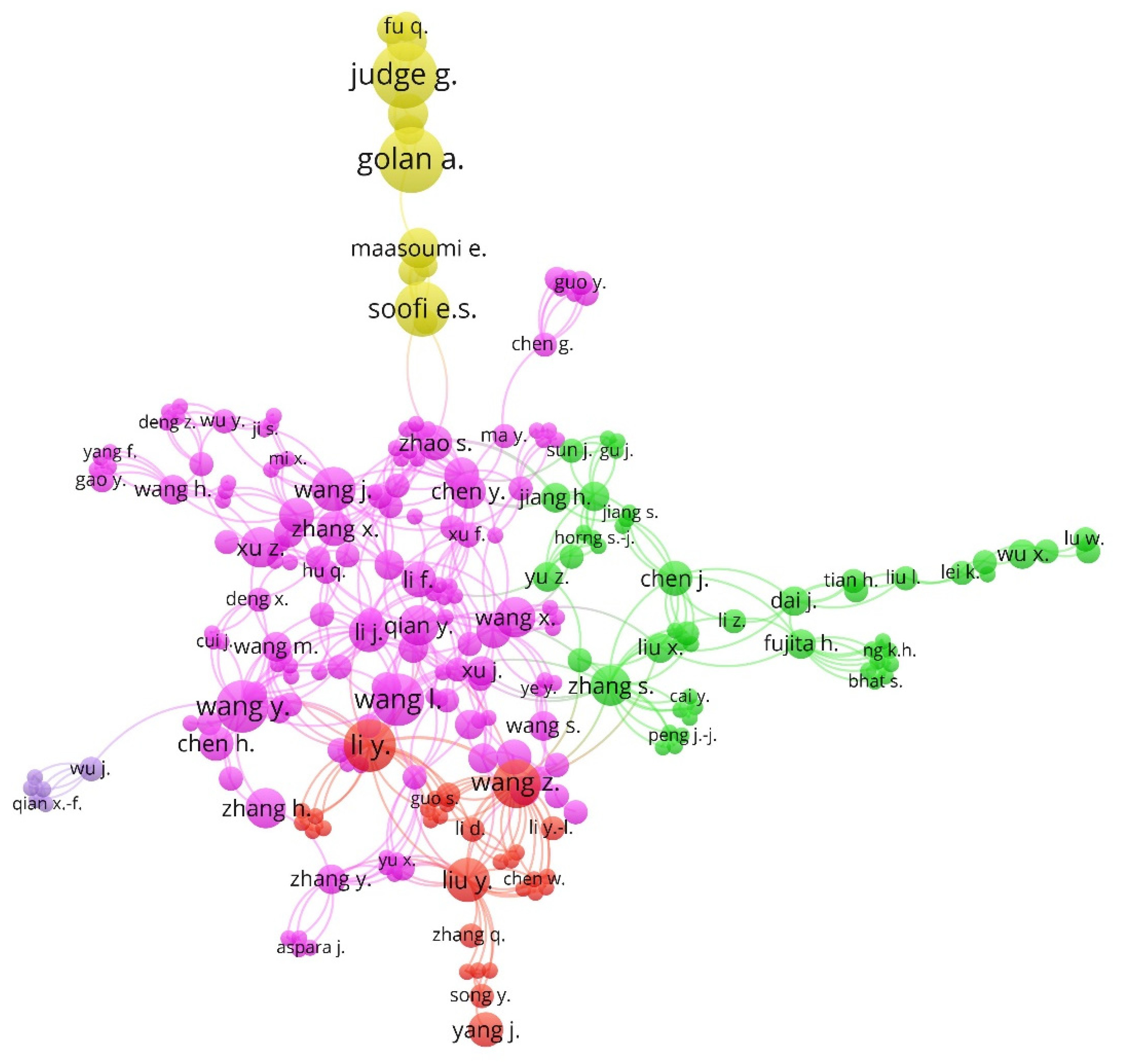

4.2.1. Authors

4.2.2. Research Institutions

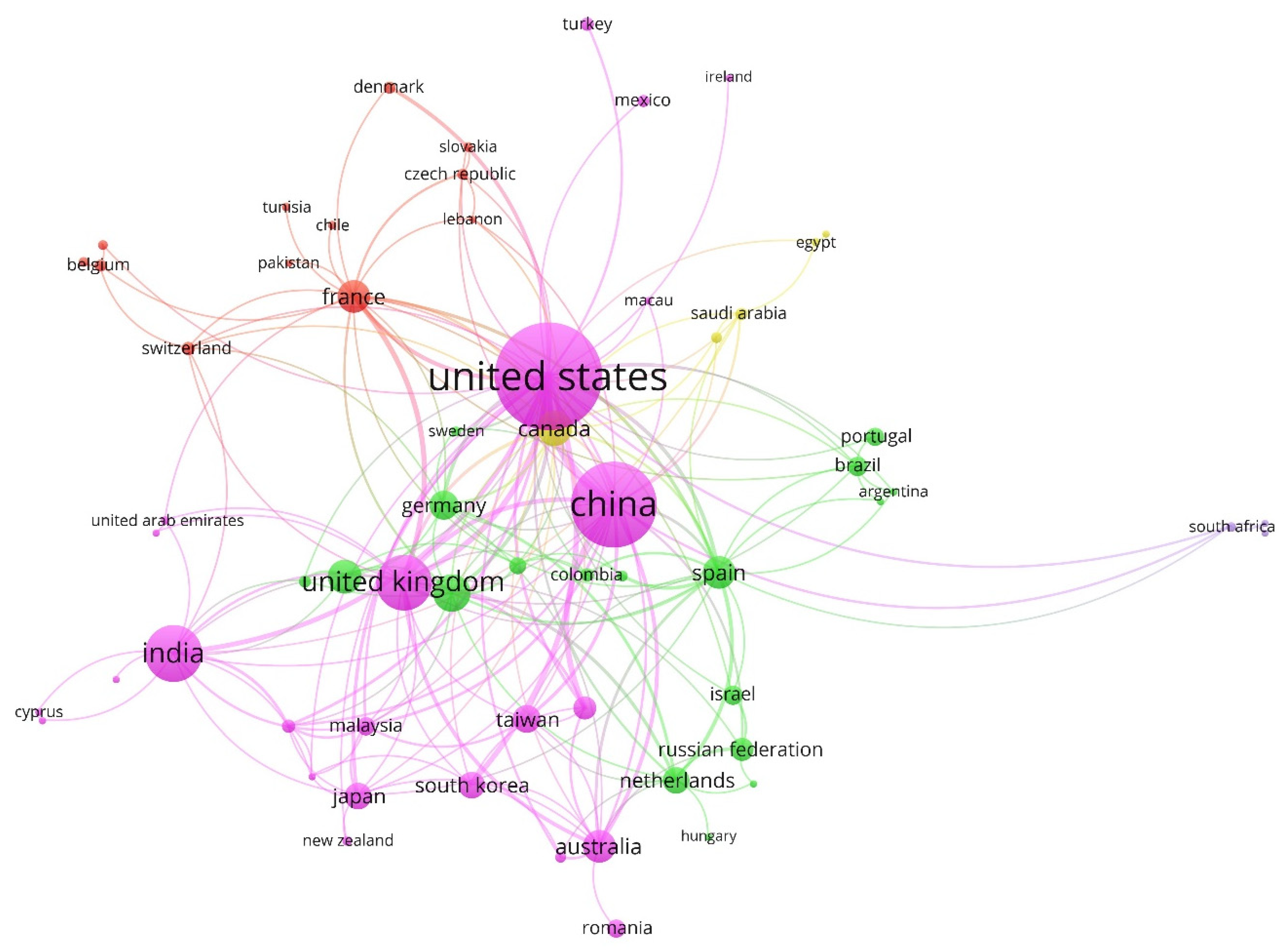

4.2.3. Countries/Territories

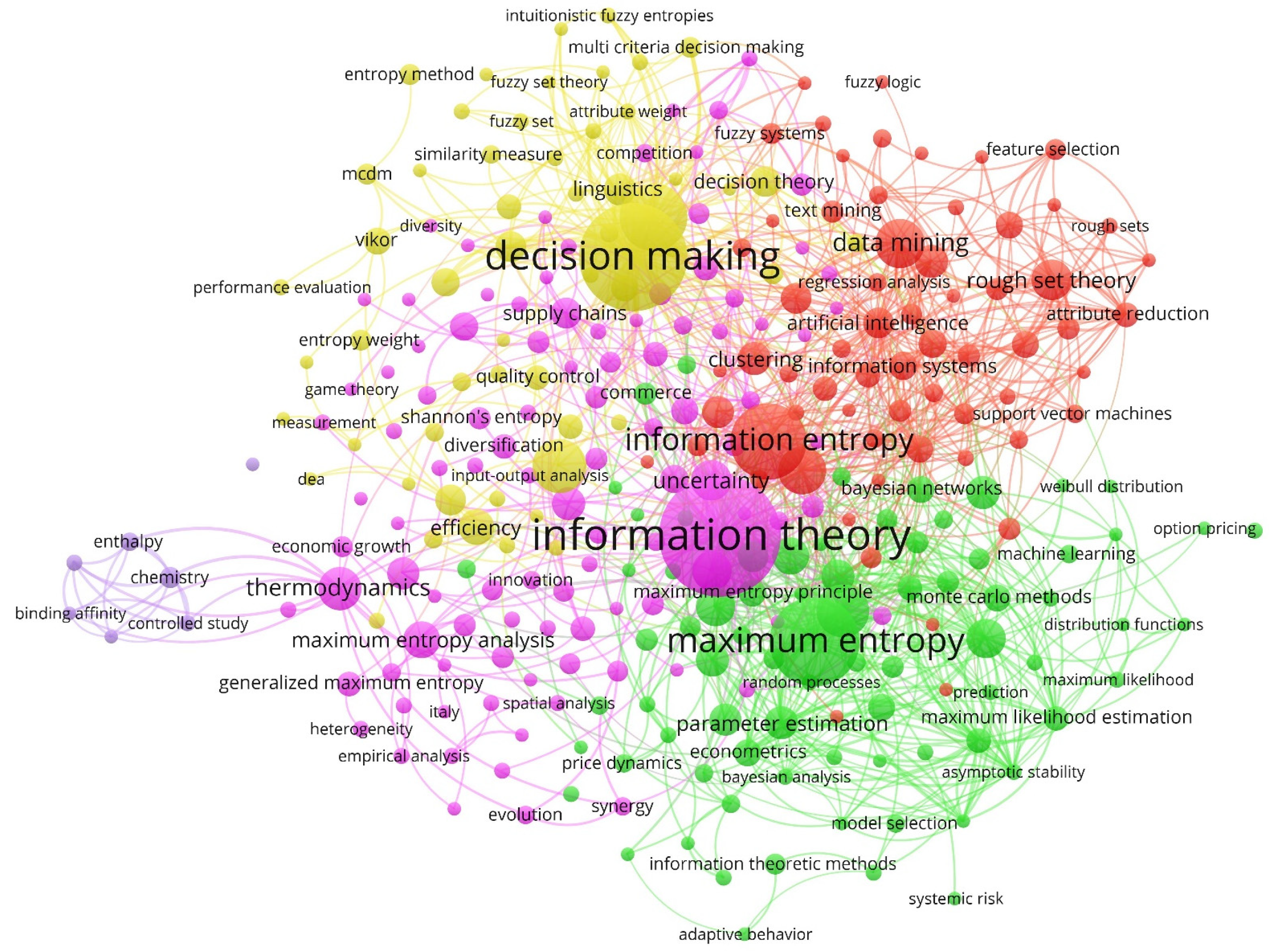

4.3. Analysis of Keywords

- Cluster 1: Information Theory

- Cluster 2: Maximum Entropy

- Cluster 3: Information Entropy

- Cluster 4: Decision-Making

- Cluster 5: Enthalpy

4.4. Research Implications

- (i)

- Carries out an analysis of the literature that has so far addressed the line of research on business information–entropy correlation in the accounting process of organizations.

- (ii)

- Identifies that planning at all levels of an organization is essential to controlling entropy in the company, both at a strategic and tactical level, that is, to project the continuous process without interruptions by which, once the different plans are defined and implemented, the information must be constantly updated to be able to take corrective measures if necessary. The periodic review of the set of plans will generate information in terms of feedback that can be used in subsequent planning.

- (iii)

- To avoid chaos in the company, you have to know where you are going, in order to plan how to do it. People, organizations, and the way they are organized have an obligation to adapt or are doomed to disappear. Dogmas are history; history must be taken into account, but it is history and in the future what awaits us will be different. The recipes of the past will not work in a radically new context, in a very open economy, in an increasingly globalized and competitive world, in a world where markets have assumed the authority of economic policy.

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Jaber, M.Y.; Bonney, M.; Moualek, I. An Economic Order Quantity Model for an Imperfect Production Process with Entropy Cost. Int. J. Prod. Econ. 2009, 118, 26–33. [Google Scholar] [CrossRef]

- Istudor, N.; Ursacescu, M.; Sendroiu, C.; Radu, I. Theoretical Framework of Organizational Intelligence: A Managerial Approach to Promote Renewable Energy in Rural Economies. Energies 2016, 9, 639. [Google Scholar] [CrossRef] [Green Version]

- Uecker, W.C. A Behavioral Study of Information System Choice. J. Account. Res. 1978, 16, 169. [Google Scholar] [CrossRef]

- Qian, M.; Zhang, F. Entropy Production Rate of the Coupled Diffusion Process. J. Theor. Probab. 2011, 24, 729–745. [Google Scholar] [CrossRef]

- Carroll, T.L. Do Reservoir Computers Work Best at the Edge of Chaos? Chaos Interdiscip. J. Nonlinear Sci. 2020, 30, 121109. [Google Scholar] [CrossRef]

- Sweet, C.; Moskal, S.; Yang, S.J. On the Variety and Veracity of Cyber Intrusion Alerts Synthesized by Generative Adversarial Networks. ACM Trans. Manag. Inf. Syst. 2020, 11, 1–21. [Google Scholar] [CrossRef]

- Wang, X.; Chen, N.; Zhao, Y.W. Value Evaluation of Innovative Technical Talents in Enterprises Based on Entropy Weight TOPSIS. Dongbei Daxue Xuebao/J. Northeast. Univ. 2020, 41, 1788–1793. [Google Scholar] [CrossRef]

- Kourteli, L. Scanning the Business Environment: Some Conceptual Issues. Benchmarking Int. J. 2000, 7, 406–413. [Google Scholar] [CrossRef]

- Escobar-Sierra, M.; Lara-Valencia, L.A.; Valencia-DeLara, P. Model for Innovation Management by Companies Based on Corporate Entrepreneurship. Probl. Perspect. Manag. 2017, 15, 234–241. [Google Scholar] [CrossRef] [Green Version]

- Ayres, R.U. Eco-Thermodynamics: Economics and the Second Law. Ecol. Econ. 1998, 26, 189–209. [Google Scholar] [CrossRef]

- Rane, S.B.; Narvel, Y.A.M. Re-Designing the Business Organization Using Disruptive Innovations Based on Blockchain-IoT Integrated Architecture for Improving Agility in Future Industry 4.0. Benchmarking Int. J. 2021, 28, 1883–1908. [Google Scholar] [CrossRef]

- Kasaev, B.S.; Petrovskaya, M.V.; Kasaev, M.B. Innovative Approaches to Business Managing Functional Areas in a Territory. Ind. Eng. Manag. Syst. 2019, 18, 440–453. [Google Scholar] [CrossRef]

- Grabner, I.; Moers, F. Management Control as a System or a Package? Conceptual and Empirical Issues. Account. Organ. Soc. 2013, 38, 407–419. [Google Scholar] [CrossRef]

- Eshaghpour, S.; Hosseini, S.H.; Aghaei, S.A.; Seif, M.S. A Hybrid Systems Approach to Determine Effective Factors on the Growth of Marine Industries in Developing Countries. Int. J. Bus. Syst. Res. 2021, 15, 124–142. [Google Scholar] [CrossRef]

- Cotta, D.; Salvador, F. Exploring the Antecedents of Organizational Resilience Practices—A Transactive Memory Systems Approach. Int. J. Oper. Prod. Manag. 2020, 40, 1531–1559. [Google Scholar] [CrossRef]

- Sokka, L.; Pakarinen, S.; Melanen, M. Industrial Symbiosis Contributing to More Sustainable Energy Use—An Example from the Forest Industry in Kymenlaakso, Finland. J. Clean. Prod. 2011, 19, 285–293. [Google Scholar] [CrossRef]

- Peters, J.C.; Hertel, T.W. Matrix Balancing with Unknown Total Costs: Preserving Economic Relationships in the Electric Power Sector. Economic Systems Research 2016, 28, 1–20. [Google Scholar] [CrossRef]

- Harvey, D.W.; Rhode, J.G.; Merchant, K.A. Accounting Aggregation: User Preferences and Decision Making. Account. Organ. Soc. 1979, 4, 187–210. [Google Scholar] [CrossRef]

- Fellingham, J.; Lin, H. Is Accounting an Information Science? Account. Econ. Law A Conviv. 2020, 10, 1–17. [Google Scholar] [CrossRef] [Green Version]

- Ugrin, J.C. The Effect of System Characteristics, Stage of Adoption, and Experience on Institutional Explanations for ERP Systems Choice. Account. Horiz. 2009, 23, 365–389. [Google Scholar] [CrossRef]

- Pierce, B.; O’Dea, T. Management Accounting Information and the Needs of Managers. Perceptions of Managers and Accountants Compared. Br. Account. Rev. 2003, 35, 257–290. [Google Scholar] [CrossRef]

- Li, M.; Ning, X.; Li, M.; Xu, Y. An Approach to the Evaluation of the Quality of Accounting Information Based on Relative Entropy in Fuzzy Linguistic Environments. Entropy 2017, 19, 152. [Google Scholar] [CrossRef]

- Hsu, L.C. A Hybrid Multiple Criteria Decision-Making Model for Investment Decision Making. J. Bus. Econ. Manag. 2014, 15, 509–529. [Google Scholar] [CrossRef] [Green Version]

- Wei-Wei, L.; Qing-Hua, L.; Mei, L. Performance Evaluation of Coal-Electricity Supply Chain Based on IAHP-Entropy Evaluation Model. Adv. Inf. Sci. Serv. Sci. 2012, 4, 163–171. [Google Scholar] [CrossRef]

- Garbaczewski, P. Differential Entropy and Dynamics of Uncertainty. J. Stat. Phys. 2006, 123, 315–355. [Google Scholar] [CrossRef] [Green Version]

- Margolin, L. On the Convergence of the Cross-Entropy Method. Ann. Oper. Res. 2005, 134, 201–214. [Google Scholar] [CrossRef]

- Robinson, S.; Cattaneo, A.; El-Said, M. Updating and Estimating a Social Accounting Matrix Using Cross Entropy Methods. Econ. Syst. Res. 2001, 13, 47–64. [Google Scholar] [CrossRef]

- Krisement, V.M. An Approach for Measuring the Degree of Comparability of Financial Accounting Information. Eur. Account. Rev. 1997, 6, 465–485. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Hitt, M.A.; Johnson, R.A.; Moesel, D.D. Construct Validity of an Objective (Entropy) Categorical Measure of Diversification Strategy. Strateg. Manag. J. 1993, 14, 215–235. [Google Scholar] [CrossRef]

- Bryant, J. A Thermodynamic Approach to Economics. Energy Econ. 1982, 4, 36–50. [Google Scholar] [CrossRef]

- Xi, N.; Muneepeerakul, R.; Azaele, S.; Wang, Y. Maximum Entropy Model for Business Cycle Synchronization. Phys. A Stat. Mech. Its Appl. 2014, 413, 189–194. [Google Scholar] [CrossRef]

- McCauley, J.L. Thermodynamic Analogies in Economics and Finance: Instability of Markets. Phys. A Stat. Mech. Its Appl. 2003, 329, 199–212. [Google Scholar] [CrossRef] [Green Version]

- Anupama, G.; Kesava Rao, V.V.S. Some Objective Methods for Determining Relative Importance of Financial Ratios. Int. J. Manag. 2019, 10, 76–96. [Google Scholar] [CrossRef]

- Jawad, H.; Jaber, M.Y.; Bonney, M.; Rosen, M.A. Deriving an Exergetic Economic Production Quantity Model for Better Sustainability. Appl. Math. Model. 2016, 40, 6026–6039. [Google Scholar] [CrossRef]

- Maqbool, A.; Afzal, F.; Rana, T.; Mirza, A. Thermodynamics Inspired Co-Operative Self-Organization of Multiple Autonomous Vehicles. Intell. Autom. Soft Comput. 2021, 28, 653–667. [Google Scholar] [CrossRef]

- Bratianu, C. From Thermodynamic Entropy to Knowledge Entropy. Proc. Int. Conf. Bus. Excell. 2020, 14, 589–596. [Google Scholar] [CrossRef]

- De Bruyn, P.; Huysmans, P.; Mannaert, H.; Verelst, J. Understanding Entropy Generation during the Execution of Business Process Instantiations: An Illustration from Cost Accounting. Lect. Notes Bus. Inf. Process. 2013, LNBIP 146, 103–117. [Google Scholar] [CrossRef]

- Bo, S.; Celani, A. Entropy Production in Stochastic Systems with Fast and Slow Time-Scales. J. Stat. Phys. 2014, 154, 1325–1351. [Google Scholar] [CrossRef]

- Wang, J.; Ma, W. A Study on Factors Influencing Team Human Error in Subway Traffic Dispatching Systems. Int. J. Simul. Syst. Sci. Technol. 2016, 17. [Google Scholar] [CrossRef]

- Dikranjan, D.; Bruno, A.G. Entropy in a Category. Appl. Categ. Struct. 2013, 21, 67–101. [Google Scholar] [CrossRef] [Green Version]

- Hall, D.J. Organisational Change: Kinetic Theory and Organisational Resonance. Technovation 1997, 17, 11–24. [Google Scholar] [CrossRef]

- Lawless, W.F. The Physics of Teams: Interdependence, Measurable Entropy, and Computational Emotion. Front. Phys. 2017, 5, 30. [Google Scholar] [CrossRef] [Green Version]

- De Almeida, R.M.C.; Mombach, J.C.M. Scaling Properties of Three-Dimensional Foams. Phys. A Stat. Mech. Its Appl. 1997, 236, 268–278. [Google Scholar] [CrossRef]

- Zhang, J.; Schmidt, K.; Li, H. An Integrated Diagnostic Framework to Manage Organization Sustainable Growth: An Empirical Case. Sustainability 2016, 8, 301. [Google Scholar] [CrossRef] [Green Version]

- Robins, J.A.; Wiersema, M.F. The Measurement of Corporate Portfolio Strategy: Analysis of the Content Validity of Related Diversification Indexes. Strateg. Manag. J. 2003, 24, 39–59. [Google Scholar] [CrossRef]

- Ramshaw, J.D. Thermodynamic vs Statistical Entropy Production in Thermostatted Hamiltonian Dynamics. J. Phys. A Math. Theor. 2020, 53, 495001. [Google Scholar] [CrossRef]

- Crutchfield, J.P.; Packard, N.H. Symbolic Dynamics of Noisy Chaos. Phys. D Nonlinear Phenom. 1983, 7, 201–223. [Google Scholar] [CrossRef]

- Altieri, L.; Cocchi, D.; Roli, G. A New Approach to Spatial Entropy Measures. Environ. Ecol. Stat. 2018, 25, 95–110. [Google Scholar] [CrossRef]

- Tantillo, D.J. Dynamic Effects on Organic Reactivity—Pathways to (and from) Discomfort. J. Phys. Org. Chem. 2021, 34, e4202. [Google Scholar] [CrossRef]

- Jaber, M.Y.; Rosen, M.A. The Economic Order Quantity Repair and Waste Disposal Model with Entropy Cost. Eur. J. Oper. Res. 2008, 188, 109–120. [Google Scholar] [CrossRef]

- Lazareva, M.G. Entropy and Information in Scenario Modeling of a Firm: New Approaches in Business Economics. Probl. Perspect. Manag. 2019, 17, 202–215. [Google Scholar] [CrossRef]

- Singh, J.P.; Irani, S.; Rana, N.P.; Dwivedi, Y.K.; Saumya, S.; Kumar Roy, P. Predicting the “Helpfulness” of Online Consumer Reviews. J. Bus. Res. 2017, 70, 346–355. [Google Scholar] [CrossRef] [Green Version]

- Murphy, S.M.; Friesner, D.L.; Rosenman, R. Business Firms’ Responses to the Crises of 2009. Int. J. Soc. Ecol. Sustain. Dev. 2014, 5, 92–110. [Google Scholar] [CrossRef]

- Jona Lasinio, G.; Pollice, A.; Marcon, É.; Fano, E.A. Assessing the Role of the Spatial Scale in the Analysis of Lagoon Biodiversity. A Case-Study on the Macrobenthic Fauna of the Po River Delta. Ecol. Indic. 2017, 80, 303–315. [Google Scholar] [CrossRef] [Green Version]

- Jaber, M.Y. Lot Sizing with Permissible Delay in Payments and Entropy Cost. Comput. Ind. Eng. 2007, 52, 78–88. [Google Scholar] [CrossRef]

- Garfield, E. From the Science of Science to Scientometrics Visualizing the History of Science with HistCite Software. J. Informetr. 2009, 3, 173–179. [Google Scholar] [CrossRef] [Green Version]

- Cronin, B. Bibliometrics and beyond: Some Thoughts on Web-Based Citation Analysis. J. Inf. Sci. 2004, 27, 1–7. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.D.; López-Meneses, E.; Vázquez-Cano, E. Financial Technology: Review of Trends, Approaches and Management. Mathematics 2020, 8, 951. [Google Scholar] [CrossRef]

- González-Zamar, M.-D.; Abad-Segura, E.; López-Meneses, E.; Gómez-Galán, J. Managing ICT for Sustainable Education: Research Analysis in the Context of Higher Education. Sustainability 2020, 12, 8254. [Google Scholar] [CrossRef]

- López-Meneses, E.; Vázquez-Cano, E.; González-Zamar, M.-D.; Abad-Segura, E. Socioeconomic Effects in Cyberbullying: Global Research Trends in the Educational Context. Int. J. Environ. Res. Public Health 2020, 17, 4369. [Google Scholar] [CrossRef]

- Waltman, L.; van Eck, N.J.; van Leeuwen, T.N.; Visser, M.S.; van Raan, A.F.J. Towards a New Crown Indicator: An Empirical Analysis. Scientometrics 2011, 87, 467–481. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Noyons, E.C.M.; van Raan, A.F.J. Monitoring Scientific Developments from a Dynamic Perspective: Self-organized Structuring to Map Neural Network Research. J. Am. Soc. Inf. Sci. 1998, 49, 68–81. [Google Scholar] [CrossRef]

- Stewart, L.A.; Clarke, M.; Rovers, M.; Riley, R.D.; Simmonds, M.; Stewart, G.; Tierney, J.F. Preferred Reporting Items for a Systematic Review and Meta-Analysis of Individual Participant Data. JAMA—J. Am. Med. Assoc. 2015, 313, 1657–1665. [Google Scholar] [CrossRef] [PubMed]

- Jensen, P.; Rouquier, J.B.; Croissant, Y. Testing Bibliometric Indicators by Their Prediction of Scientists Promotions. Scientometrics 2009, 78, 467–479. [Google Scholar] [CrossRef] [Green Version]

- Nadel, E. Citation and Co-Citation Indicators of a Phased Impact of the BCS Theory in the Physics of Superconductivity. Scientometrics 1981, 3, 203–221. [Google Scholar] [CrossRef]

- Perianes-Rodriguez, A.; Waltman, L.; van Eck, N.J. Constructing Bibliometric Networks: A Comparison between Full and Fractional Counting. J. Informetr. 2016, 10, 1178–1195. [Google Scholar] [CrossRef] [Green Version]

- Abad-Segura, E.; González-Zamar, M.D.; de la Rosa, A.L.; Gallardo-Pérez, J. Management of the Digital Economy in Higher Education: Trends and Future Perspectives. Campus Virtuales 2020, 9, 57–68. [Google Scholar]

- van Eck, N.J.; Waltman, L. Visualizing Bibliometric Networks. In Measuring Scholarly Impact; Springer International Publishing: Cham, Switzerland, 2014; pp. 285–320. [Google Scholar]

- Tijssen, R.J.W.; Van Raan, A.F.J. Mapping Changes in Science and Technology: Bibliometric Co-Occurrence Analysis of the R&D Literature. Eval. Rev. 1994, 18, 98–115. [Google Scholar] [CrossRef]

- van Eck, N.J.; Waltman, L. Software Survey: VOSviewer, a Computer Program for Bibliometric Mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [Green Version]

- van Eck, N.J.; Waltman, L. VOS: A New Method for Visualizing Similarities Between Objects. In Studies in Classification, Data Analysis, and Knowledge Organization; Kluwer Academic Publishers: Berlin, Germany, 2007; pp. 299–306. ISBN 9783540709800. [Google Scholar]

- Abad-Segura, E.; Infante-Moro, A.; González-Zamar, M.-D.; López-Meneses, E. Blockchain Technology for Secure Accounting Management: Research Trends Analysis. Mathematics 2021, 9, 1631. [Google Scholar] [CrossRef]

- MacKey, M.C.; Tyran-Kamińska, M. Temporal Behavior of the Conditional and Gibbs’ Entropies. J. Stat. Phys. 2006, 124, 1443–1470. [Google Scholar] [CrossRef] [Green Version]

- Waltman, J.L. Entropy and Business Communication. J. Bus. Commun. 1984, 21, 63–80. [Google Scholar] [CrossRef]

- Palepu, K. Diversification Strategy, Profit Performance and the Entropy Measure. Strateg. Manag. J. 1985, 6, 239–255. [Google Scholar] [CrossRef]

- Argentiero, A.; Bovi, M.; Cerqueti, R. Bayesian Estimation and Entropy for Economic Dynamic Stochastic Models: An Exploration of Overconsumption. Chaos Solitons Fractals 2016, 88, 143–157. [Google Scholar] [CrossRef]

- Ijadi Maghsoodi, A.; Abouhamzeh, G.; Khalilzadeh, M.; Zavadskas, E.K. Ranking and Selecting the Best Performance Appraisal Method Using the MULTIMOORA Approach Integrated Shannon’s Entropy. Front. Bus. Res. China 2018, 12, 2. [Google Scholar] [CrossRef] [Green Version]

- Chen, C.; Huang, T.; Garg, M.; Khedmati, M. Governments as Customers: Exploring the Effects of Government Customers on Supplier Firms’ Information Quality. J. Bus. Financ. Account. 2021. [Google Scholar] [CrossRef]

- Eremeyev, V.A.; Pietraszkiewicz, W. Nonlinear Resultant Theory of Shells Accounting for Thermodiffusion. Contin. Mech. Thermodyn. 2020, 33, 893–909. [Google Scholar] [CrossRef]

- Fahimnia, B.; Davarzani, H.; Eshragh, A. Planning of Complex Supply Chains: A Performance Comparison of Three Meta-Heuristic Algorithms. Comput. Oper. Res. 2018, 89, 241–252. [Google Scholar] [CrossRef]

- Swales, J.M.; Leeder, C. A Reception Study of the Articles Published in English for Specific Purposes from 1990–1999. Engl. Specif. Purp. 2012, 31, 137–146. [Google Scholar] [CrossRef]

- Mongeon, P.; Paul-Hus, A. The Journal Coverage of Web of Science and Scopus: A Comparative Analysis. Scientometrics 2016, 106, 213–228. [Google Scholar] [CrossRef]

- Marschak, J. Limited Role of Entropy in Information Economics. Theory Decis. 1974, 5, 1–7. [Google Scholar] [CrossRef]

- Liu, L. Entropy Weight Fuzzy Synthesis Evaluation Based on the Measurement of Environmental Accounting. BioTechnology Indian J. 2013, 8, 601–606. [Google Scholar]

- Wang, X.; Zhan, W. Evaluation of the Organization Structure of Large Construction Companies Based on the Entropy Theory. Appl. Mech. Mater. 2014, 584–586, 2224–2229. [Google Scholar] [CrossRef]

- Abbasnejad, M.; Arghami, N.R. Renyi Entropy Properties of Order Statistics. Commun. Stat.—Theory Methods 2011, 40, 40–52. [Google Scholar] [CrossRef]

- Cheng, Y.; Li, Y. Some Properties of the Kth-Partial Rényi Entropy. Int. J. Theor. Phys. 2014, 53, 2931–2943. [Google Scholar] [CrossRef]

- Ross, J. The Information Content of Accounting Reports: An Information Theory Perspective. Information 2016, 7, 48. [Google Scholar] [CrossRef] [Green Version]

- Wang, Z.; Chen, Y.; Zhou, Y.; Jin, Y. An Entropy Testing Model Research on the Quality of Internal Control and Accounting Conservatism: Empirical Evidence from the Financial Companies of China from 2007 to 2011. Math. Probl. Eng. 2014, 2014, 475050. [Google Scholar] [CrossRef] [Green Version]

- Bejan, A. Fundamentals of Exergy Analysis, Entropy Generation Minimization, and the Generation of Flow Architecture. Int. J. Energy Res. 2002, 26, 1–43. [Google Scholar] [CrossRef]

- Adler, P.S. Building Better Bureaucracies. Acad. Manag. Perspect. 1999, 13, 36–47. [Google Scholar] [CrossRef]

- Ebrahimi, N.; Maasoumi, E.; Soofi, E.S. Ordering Univariate Distributions by Entropy and Variance. J. Econom. 1999, 90, 317–336. [Google Scholar] [CrossRef]

- Rao, M. More on a New Concept of Entropy and Information. J. Theor. Probab. 2005, 18, 967–981. [Google Scholar] [CrossRef]

- Chakrabarti, C.G.; Sarker, N.G. On Information, Negentropy and H-Theorem. Z. Für Phys. B Condens. Matter 1983, 51, 265–269. [Google Scholar] [CrossRef]

- Smulders, S. Entropy, Environment, and Endogenous Economic Growth. Int. Tax Public Financ. 1995, 2, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Jaber, M.Y.; Nuwayhid, R.Y.; Rosen, M.A. A Thermodynamic Approach to Modelling the Economic Order Quantity. Appl. Math. Model. 2006, 30, 867–883. [Google Scholar] [CrossRef]

- Jung, J.Y.; Chin, C.H.; Cardoso, J. An Entropy-Based Uncertainty Measure of Process Models. Inf. Process. Lett. 2011, 111, 135–141. [Google Scholar] [CrossRef]

- Mills, J.A. Making Inflexible Investment Decisions with Incomplete Information. Comput. Math. Appl. 1992, 24, 247–258. [Google Scholar] [CrossRef] [Green Version]

- Kim, S.J.; Bae Lee, K. Constructing Decision Trees with Multiple Response Variables. Int. J. Manag. Decis. Mak. 2003, 4, 337–353. [Google Scholar] [CrossRef]

- Sudha, M.R.; Sumathi, C.P.; Saravanakumar, A. An Optimal Energy Consumption Based Resource Management in Mobile Cloud Computing. Int. J. Recent Technol. Eng. 2019, 8, 103–109. [Google Scholar] [CrossRef]

- Chirico, R.D.; Steele, W.V. Thermodynamic Properties of 1,2-Dihydronaphthalene: Glassy Crystals and Missing Entropy. J. Chem. Thermodyn. 2008, 40, 806–817. [Google Scholar] [CrossRef]

- Zhang, Y.; Lu, B.; Zheng, H. Can Buzzing Bring Business? Social Interactions, Network Centrality and Sales Performance: An Empirical Study on Business-to-Business Communities. J. Bus. Res. 2020, 112, 170–189. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Ref. | Year | Article Title | Author(s) | Journal | BC |

|---|---|---|---|---|---|

| [22] | 2017 | An approach to the evaluation of the quality of accounting information based on relative entropy in fuzzy linguistic environments | Li et al. | Entropy | E-A-I |

| [23] | 2014 | A hybrid multiple criteria decision-making model for investment decision-making | Hsu | Journal of Business Economics and Management | E-B |

| [24] | 2012 | Performance evaluation of coal–electricity supply chain based on IAHP–entropy evaluation model | Wei-Wei et al. | Advances in Information Sciences and Service Sciences | E-B-I |

| [1] | 2009 | An economic order quantity model for an imperfect production process with entropy cost | Jaber et al. | International Journal of Production Economics | E-A |

| [25] | 2006 | Differential entropy and dynamics of uncertainty | Garbaczewski | Journal of Statistical Physics | E-B |

| [26] | 2005 | On the convergence of the cross-entropy method | Margolin | Annals of Operations Research | E-B |

| [27] | 2001 | Updating and estimating a social accounting matrix using cross-entropy methods | Robinson et al. | Economic Systems Research | E-A |

| [28] | 1997 | An approach for measuring the degree of comparability of financial accounting information | Krisement | European Accounting Review | E-A-B-I |

| [29] | 1993 | Construct validity of an objective (entropy) categorical measure of diversification strategy | Hoskisson et al. | Strategic Management Journal | E-B |

| [30] | 1982 | A thermodynamic approach to economics | Bryant | Energy Economics | E-A-B |

| Period | Number of Articles | % | % Accumulated |

|---|---|---|---|

| 2011–2020 | 654 | 66.73% | 100.00% |

| 2001–2010 | 197 | 20.10% | 33.27% |

| 1991–2000 | 78 | 7.96% | 13.16% |

| 1981–1990 | 35 | 3.57% | 5.20% |

| 1971–1980 | 16 | 1.63% | 1.63% |

| Total | 980 | 100.00% |

| Cluster | Journal | Weight | ||||

|---|---|---|---|---|---|---|

| Number | % | Color | Links | Total Link Strength | Citations | |

| 1 | 35.36% | Pink | Econometrica | 231 | 5998 | 380 |

| Journal of Econometrics | 181 | 5153 | 270 | |||

| Journal of the American Statistical Association | 179 | 3124 | 162 | |||

| Bell System Technical Journal | 242 | 2194 | 128 | |||

| Journal of Finance | 134 | 2667 | 127 | |||

| Entropy | 243 | 2194 | 114 | |||

| 2 | 27.62% | Green | Journal of Cleaner Production | 79 | 6180 | 218 |

| Information Sciences | 93 | 4070 | 175 | |||

| Knowledge-Based Systems | 63 | 4549 | 150 | |||

| Expert Systems with Applications | 111 | 3863 | 134 | |||

| Science | 203 | 1798 | 111 | |||

| IEEE Transactions on Fuzzy Systems | 70 | 2597 | 70 | |||

| 3 | 22.65% | Red | European Journal of Operational Research | 210 | 5519 | 245 |

| Expert Systems with Applications | 158 | 5168 | 233 | |||

| International Journal of Production Research | 130 | 3568 | 158 | |||

| Fuzzy Sets and Systems | 160 | 3180 | 152 | |||

| International Journal of Production Economics | 139 | 2594 | 94 | |||

| Tourism Management | 96 | 1215 | 88 | |||

| 4 | 14.36% | Yellow | Management Science | 213 | 3167 | 141 |

| Strategic Management Journal | 115 | 3149 | 140 | |||

| Decision Support Systems | 136 | 2105 | 108 | |||

| Academy of Management Journal | 88 | 1631 | 64 | |||

| Research Policy | 76 | 775 | 58 | |||

| Harvard Business Review | 116 | 899 | 49 | |||

| Author | A | Research Institution | City (Country) | Keyword 1 | Keyword 2 | Keyword 3 |

|---|---|---|---|---|---|---|

| Golan, A. | 12 | Santa Fe Institute | Santa Fe (USA) | Maximum entropy | Generalized maximum entropy | Censored data |

| American University Department of Economics | Washington, D.C. (USA) | |||||

| Judge, G. | 12 | University of California | Berkeley (USA) | Information theoretic methods | Adaptive behavior | Empirical likelihood |

| Leydesdorff, L. | 9 | The Amsterdam School of Communications Research-ASCoR | Amsterdam (Netherlands) | Triple helix | Information theory | Knowledge-based systems |

| Soofi, E.S. | 9 | Lubar School of Business | Milwaukee (USA) | Kullback–Leibler information | Dirichlet process | Model fitting |

| Gossner, O. | 6 | London School of Economics and Political Science | London (UK) | Incomplete information | Relative entropy | Bayesian learning |

| Institut Polytechnique de Paris | Palaiseau (France) | |||||

| Bailey, K.D. | 5 | University of California Department of Sociology | Los Angeles (USA) | Living systems | Social entropy theory | Behavioral research |

| Gzyl, H. | 5 | IESA, Center for Finance | Caracas (Venezuela) | Maximum entropy in the mean | Commerce | Costs |

| Maasoumi, E. | 5 | Emory University Department of Economics | Atlanta (USA) | Adaptive estimation | Computer simulation | Correlation methods |

| Miller, D.J. | 5 | Iowa State University Department of Economics | Ames (USA) | Maximum entropy | Adaptive behavior | Controlled stochastic process |

| Qian, Y. | 5 | Shanxi University | Taiyuan (China) | Rough set theory | Attribute reduction | Decision systems |

| Robinson, S. | 5 | Peterson Institute for International Economics | Washington, D.C. (USA) | Bayesian estimation | Computable general equilibrium (CGE) | Economic conditions |

| Tavana, M. | 5 | La Salle University Distinguished Chair of Business Analytics | Philadelphia (USA) | Decision support systems | Analytic network process | Business excellence |

| Universität Paderborn Business Information Systems Department | Paderborn (Germany) | |||||

| Xu, Z. | 5 | Sichuan University, School of Business | Chengdu (China) | Decision-making | Aggregated information | Aleatory and epistemic uncertainties |

| Cluster | Author | Weight | |||||

|---|---|---|---|---|---|---|---|

| Number | % | Color | Links | Total Link Strength | Occurrences | Citations | |

| 1 | 59.43% | Pink | Wang L. | 15 | 18 | 8 | 145 |

| Wang Y. | 18 | 19 | 8 | 108 | |||

| Wang J. | 21 | 21 | 6 | 67 | |||

| Li J. | 20 | 20 | 5 | 201 | |||

| Qian Y. | 12 | 16 | 5 | 169 | |||

| 2 | 20.90% | Green | Zhang S. | 20 | 20 | 5 | 78 |

| Chen J. | 13 | 13 | 4 | 32 | |||

| Dai J. | 7 | 9 | 3 | 213 | |||

| Fujita H. | 12 | 12 | 3 | 85 | |||

| Jiang H. | 6 | 8 | 3 | 25 | |||

| 3 | 12.30% | Red | Li Y. | 23 | 25 | 8 | 108 |

| Wang Z. | 22 | 24 | 7 | 205 | |||

| Liu Y. | 22 | 22 | 6 | 71 | |||

| Yang J. | 1 | 1 | 4 | 25 | |||

| Li D. | 7 | 8 | 2 | 85 | |||

| 4 | 4.92% | Yellow | Golan A. | 4 | 6 | 12 | 380 |

| Judge G. | 5 | 10 | 12 | 183 | |||

| Soofi E.S. | 5 | 7 | 9 | 235 | |||

| Maasoumi E. | 3 | 3 | 5 | 300 | |||

| Miller D.J. | 1 | 1 | 5 | 86 | |||

| 5 | 2.46% | Purple | Wu J. | 6 | 6 | 2 | 47 |

| Chen Y.-W. | 5 | 5 | 1 | 28 | |||

| Liu X.-B. | 5 | 5 | 1 | 28 | |||

| Qian X.-F. | 5 | 5 | 1 | 28 | |||

| Yang J.-B. | 5 | 5 | 1 | 28 | |||

| Research Institution | City (Country) | A | Keyword 1 | Keyword 2 | Keyword 3 |

|---|---|---|---|---|---|

| University of California Berkeley | Berkeley (USA) | 16 | Information theoretic methods | Adaptive behavior | Empirical likelihood |

| City University of Hong Kong | Kowloon (Hong Kong) | 12 | Decision-making | Fuzzy sets | Maximum entropy methods |

| Sichuan University | Sichuan (China) | 12 | Decision-making | Fuzzy sets | Decision theory |

| Ministry of Education China | Beijing (China) | 11 | Information entropy | Rough set | Artificial intelligence |

| Universiteit van Amsterdam | Noord-Holland (Netherlands) | 11 | Triple helix | Information theory | Knowledge-based systems |

| Universidad de Oviedo | Oviedo (Spain) | 10 | Empirical analysis | Decomposition analysis | Econometrics |

| University of Wisconsin-Milwaukee | Milwaukee (USA) | 10 | Kullback–Leibler information | Dirichlet process | Model fitting |

| London School of Economics and Political Science | London (UK) | 9 | Relative entropy | Blackwell ordering | Divergence measures |

| Chinese Academy of Sciences | Beijing (China) | 9 | Transfer entropy | Decision-making | Information entropy |

| Lubar School of Business | Milwaukee (USA) | 9 | Kullback–Leibler information | Dirichlet process | Model fitting |

| Cluster | Country | Weight | |||||

|---|---|---|---|---|---|---|---|

| Number | % | Color | Links | Total Link Strength | Occurrences | Citations | |

| 1 | 38.71% | Pink | USA | 40 | 137 | 281 | 8279 |

| China | 23 | 80 | 190 | 5148 | |||

| India | 16 | 27 | 89 | 945 | |||

| 2 | 29.03% | Green | Italy | 13 | 22 | 42 | 649 |

| Iran | 7 | 10 | 36 | 605 | |||

| Spain | 19 | 40 | 32 | 439 | |||

| 3 | 19.35% | Red | France | 19 | 38 | 33 | 632 |

| Switzerland | 7 | 7 | 7 | 100 | |||

| Belgium | 4 | 4 | 6 | 52 | |||

| 4 | 8.06% | Yellow | Canada | 17 | 35 | 37 | 748 |

| Saudi Arabia | 7 | 8 | 6 | 153 | |||

| Poland | 3 | 3 | 5 | 30 | |||

| 5 | 4.84% | Purple | South Africa | 5 | 7 | 4 | 25 |

| Kenya | 2 | 2 | 1 | 2 | |||

| Uganda | 2 | 2 | 1 | 2 | |||

| Cluster | Keyword | Weight | ||||

|---|---|---|---|---|---|---|

| Number | % | Color | Links | Total Link Strength | Occurrences | |

| 1 | 33.77% | Pink | Information theory (*) | 139 | 238 | 86 |

| Thermodynamics | 37 | 69 | 20 | |||

| Uncertainty | 51 | 65 | 18 | |||

| Probability | 48 | 69 | 17 | |||

| Maximum entropy analysis | 39 | 54 | 16 | |||

| Supply chains | 37 | 51 | 12 | |||

| 2 | 25.00% | Green | Maximum entropy (*) | 96 | 151 | 56 |

| Mathematical models | 86 | 172 | 26 | |||

| Optimization | 64 | 86 | 17 | |||

| Probability distributions | 61 | 111 | 17 | |||

| Computer simulation | 67 | 99 | 14 | |||

| Economics | 55 | 82 | 14 | |||

| 3 | 20.78% | Red | Information entropy (*) | 71 | 107 | 44 |

| Data mining | 62 | 95 | 24 | |||

| Rough set theory | 44 | 98 | 18 | |||

| Learning systems | 56 | 79 | 14 | |||

| Artificial intelligence | 56 | 73 | 12 | |||

| Decision trees | 37 | 56 | 11 | |||

| 4 | 17.86% | Yellow | Decision-making (*) | 149 | 336 | 73 |

| Fuzzy sets | 104 | 191 | 37 | |||

| Shannon entropy | 43 | 52 | 27 | |||

| Efficiency | 51 | 62 | 15 | |||

| Decision theory | 39 | 57 | 12 | |||

| Sensitivity analysis | 33 | 46 | 11 | |||

| 5 | 2.60% | Purple | Enthalpy (*) | 9 | 26 | 6 |

| Controlled study | 8 | 22 | 5 | |||

| Hydrophobicity | 7 | 25 | 5 | |||

| Binding affinity | 7 | 20 | 4 | |||

| Kinetics | 7 | 17 | 4 | |||

| Quantitative analysis | 22 | 22 | 4 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abad-Segura, E.; González-Zamar, M.-D.; Squillante, M. Examining the Research on Business Information-Entropy Correlation in the Accounting Process of Organizations. Entropy 2021, 23, 1493. https://doi.org/10.3390/e23111493

Abad-Segura E, González-Zamar M-D, Squillante M. Examining the Research on Business Information-Entropy Correlation in the Accounting Process of Organizations. Entropy. 2021; 23(11):1493. https://doi.org/10.3390/e23111493

Chicago/Turabian StyleAbad-Segura, Emilio, Mariana-Daniela González-Zamar, and Massimo Squillante. 2021. "Examining the Research on Business Information-Entropy Correlation in the Accounting Process of Organizations" Entropy 23, no. 11: 1493. https://doi.org/10.3390/e23111493

APA StyleAbad-Segura, E., González-Zamar, M. -D., & Squillante, M. (2021). Examining the Research on Business Information-Entropy Correlation in the Accounting Process of Organizations. Entropy, 23(11), 1493. https://doi.org/10.3390/e23111493