The Impacts of Selling Expense Structure on Enterprise Growth in Large Enterprises: A Study from Vietnam

Abstract

:1. Introduction

2. Literature Review

- Koga and Kato (2017) thought that the traditional way many businesses using to measure growth is to compare their revenues between this year and the previous year instead of comparing the respective profits annually (Delmar et al. 2003; Storey 2009; Huynh and Petrunia 2010; Davidsson et al. 2010). With this traditional way of measurement, however, it is easy to lead administrators and businesses to an “illusion” in growth: while corporate revenue increases, the profitability of the business decreases. This is because the “growth in that dream” is made by the trade-off between the decrease in selling price and the increase in the quantity of sold products, whereas the production cost remains constant or even higher. Many other scientists such as Delmar et al. (2003) agreed with Koga and Kato’s (2017) opinion that business growth is dependent on the characteristics of the industry and the objectives of the business in a phased manner. More specifically, for some service sectors, the growth of the business is measured by the number of customers that the business serves in specific years such as the tourism industry. With several newly established companies, the growth of these businesses is decided through the business pricing (firm value) in merger and acquisition transactions. Ultimately, in large-scale companies, the best way to measure business growth is to compare the performance of your business to that of competitors (Delmar et al. 2003).

- Coad and Hölzl (2010) have made a separate rule and doctrine entitled Gibrat’s Law Gibrat (1931) to measure the growth rates of a business. Gibrat’s law indicated that the best way to measure business growth is to rely on the scale of the business. Many scientists also agreed with this measurement method such as Mansfield (1962), Hart and Oulton (1996), Dunne and Hughes (1994), Lotti et al. (2010), Calvo (2006), and Mengistae (1999). Indeed, these scientists have pointed out that firm size is one of the most important factors to compare the growth of businesses to each other or to evaluate the growth factor of businesses in the present year with the previous year. Any change in the enterprise size can directly influence the business growth in the present period or in the subsequent period.

- (i).

- Upgrading sales means encouraging customer commitments, which help the company with reputation and market share achievement. This is because if the customers are more interested in buying products from a company, they tend to make several “free marketing” these products to their friends and family members with a great review. In the digital age, attracting more customers is an important key to quickly increase sales and service provision, for any type of business. Approving with this opinion, Melfi (2016), Jena (2013), Haas et al. (2012), Levitt (1960), Lindgreen and Wynstra (2005), and Ramsey and Sohi (1997) indicated that “sales are tied to revenue, and setting sales goals makes it possible to forecast quarterly performance”. Sales not only guarantee the ability of any business to achieve its growth goals but also plays an important role in motivating employees and helping managers set strategies in the right direction (Ramsey and Sohi 1997). This is the reason why many large enterprises have spent over 10% of their annual revenue on marketing for dominating the market and becoming a “monopoly” in the industry (Markdao 2019).

- (ii).

- Affirming the position of sale staffs in generating revenue and, thereby, motivating business growth is one of the vital aspects that previous researchers tend to. Indeed, finding the right weighted formula for who (individuals, stores, e-commerce personnel) gets what is the challenge (Haas et al. 2012, Lindgreen and Wynstra 2005, Ramsey and Sohi 1997). In other words, this sentence means that finding ways to make sales and marketing strategies reasonable to a customer audience through different sales channels is the best method to achieve business goals (Drucker 1973, Woodruff 1997, Ramsey and Sohi 1997). Furthermore, sales employees act as a bridge between businesses and customers, building relationships and creating value from these relationships (Haas et al. 2012).

- (iii).

- The impact of marketing on business growth showed that marketing and advertising expenditures are recognised as an essential element influencing the profitability negatively in the short term, but they can add more value for the firm in the long-term (Konak 2015). In each marketing campaign or a business’s sales strategy launched, the most important purpose of business is not just upgrading the revenue figure or the amount of money that customers are willing to spend on products and services provided by that business, but it is for developing customer loyalty and competitive advantages (Konak 2015; Kumar 1985; Blattberg et al. 2009). Therefore, it is possible to assume that the cost of marketing and selling activity is directly correlated to the revenue and market size of the business, influencing significantly the business growth.

3. Hypothesis, Empirical Models, and Research Methods

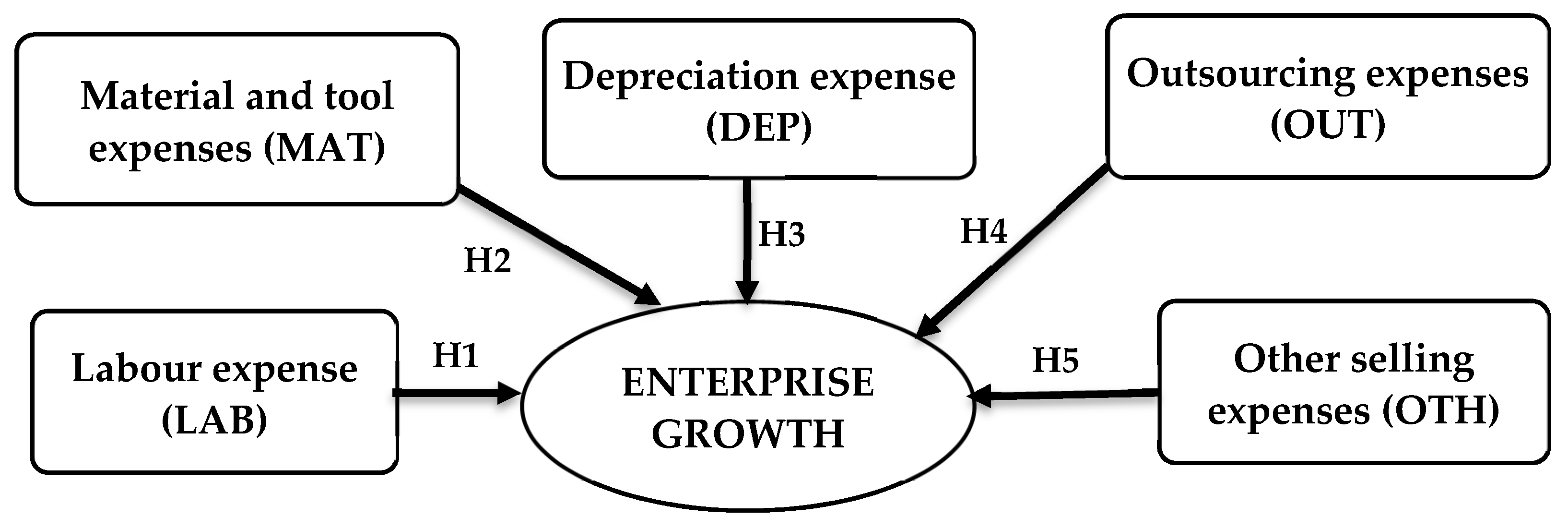

3.1. Hypothesis

3.2. Empirical Models

- -

- Model 1: PGRit = α + β1 × LABit + β2 × MATit + β3 × DEPit + β4 × OUTit + β5 × OTHit + ε

- -

- Model 2: RGRit = α + β1 × LABit + β2 × MATit + β3 × DEPit + β4 × OUTit + β5 × OTHit + ε

- -

- Model 3: SGRit = α + β1 × LABit + β2 × MATit + β3 × DEPit + β4 × OUTit + β5 × OTHit + ε

- -

- Suitable to study the dynamics of change.

- -

- Detect and measure efficiently effects that could not be observed in time series data and cross-section data.

- -

- Used to study more complex behavioural models

- -

- Minimises discrepancies if authors aggregate individuals or businesses into aggregate figures.

3.3. Research Method

- -

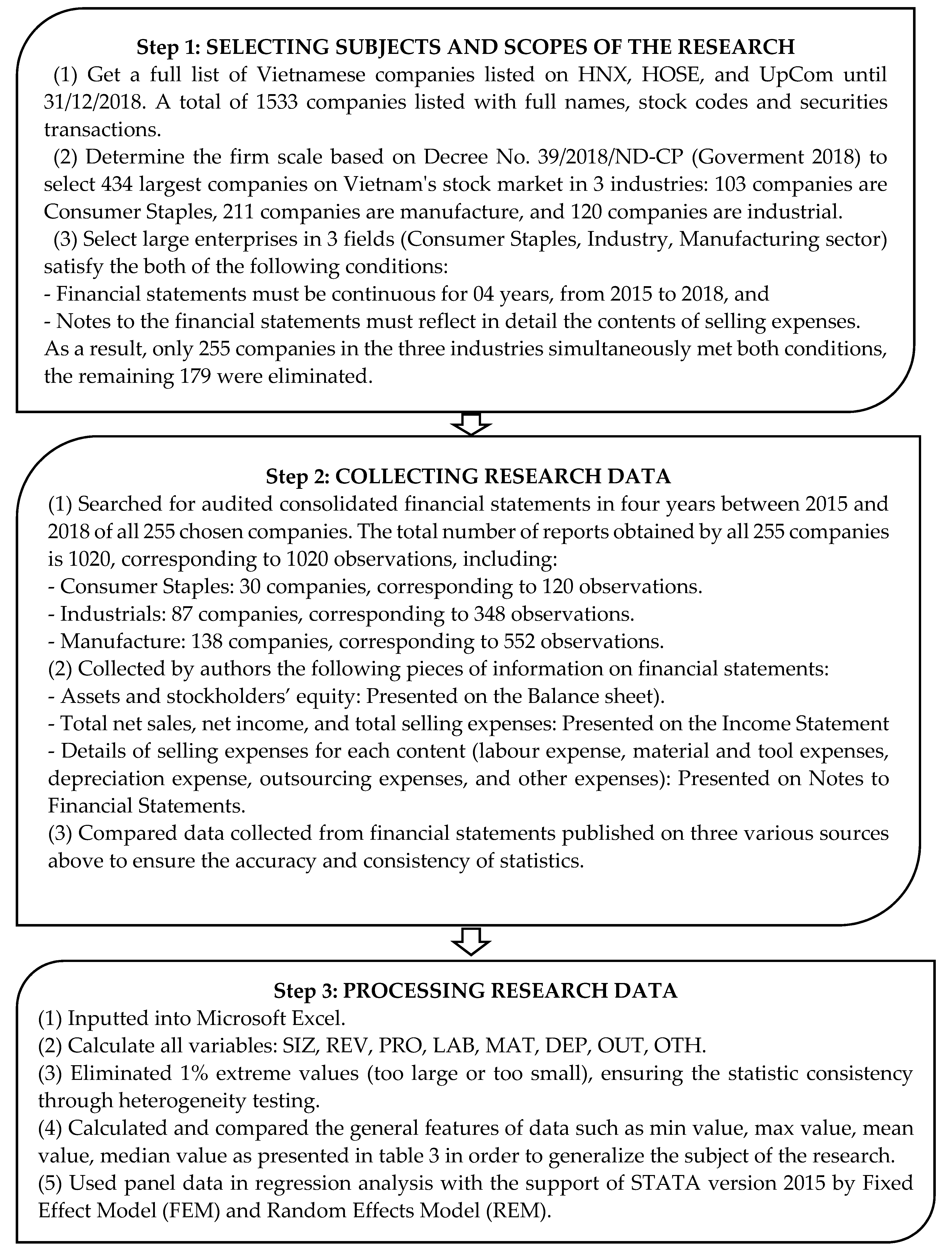

- Time period: Data is collected from financial statements of large enterprises throughout the last four years from 2015 to 2018 when Vietnam’s economy witnessed a recovery period of positive GDP growth and lower inflation compared to the financial difficulties during the period of 2011–2014 despite facing various challenges from the global economic environment (World Bank 2018). Vietnam’s economy has witnessed a strong domestic demand in export-oriented Industrial and Manufacture sectors, which are significantly contributed to by large enterprises. Moreover, the last four-year period helps the study to ensure the updated information to provide topical results before giving an overview of the whole process as well as tracking in detail the specific fluctuations each year.

- -

- The observations scale: To ensure the validity and reliability of the study, we proceeded to select relevance sampling, which is also called purposive sampling (Krippendorf 2004). This paper selects the sample by the business scale rather than the industry, which is the way previous studies often do, thereby increasing the justice and objectivity in assessing the selling cost structure and the growth of businesses with the same size. The study of large enterprises in Vietnam is essential because the number of large enterprises accounts for only 2.5% of enterprises nationwide but contributes up to 60% of GDP in Vietnam (Ha 2018).

- -

- The number of observations: Currently, there are 1533 companies listed on the three biggest stock exchanges in Vietnam including HNX, HOSE, and UpCom, from which the authors selected 255 enterprises (including Consumer Staples, Industrials and Manufacture sectors) to ensure the criteria: meeting the large enterprise standards according to the Decree No. 39/2018/ND-CP (Goverment 2018), having full financial statements for the 2015–2018 period, and especially having full explanation of the selling expense structure on notes to financial statements. Like most countries in the world, the classification of large, small, medium, and micro enterprises in Vietnam is also based on criteria such as the number of employees and either turnover or balance sheet total (European Commission 2015; Dotdash 2019). Table 2 indicates the list of criteria for the big enterprise in Vietnam according to Decree No. 39/2018/ND-CP (Goverment 2018).

4. Results

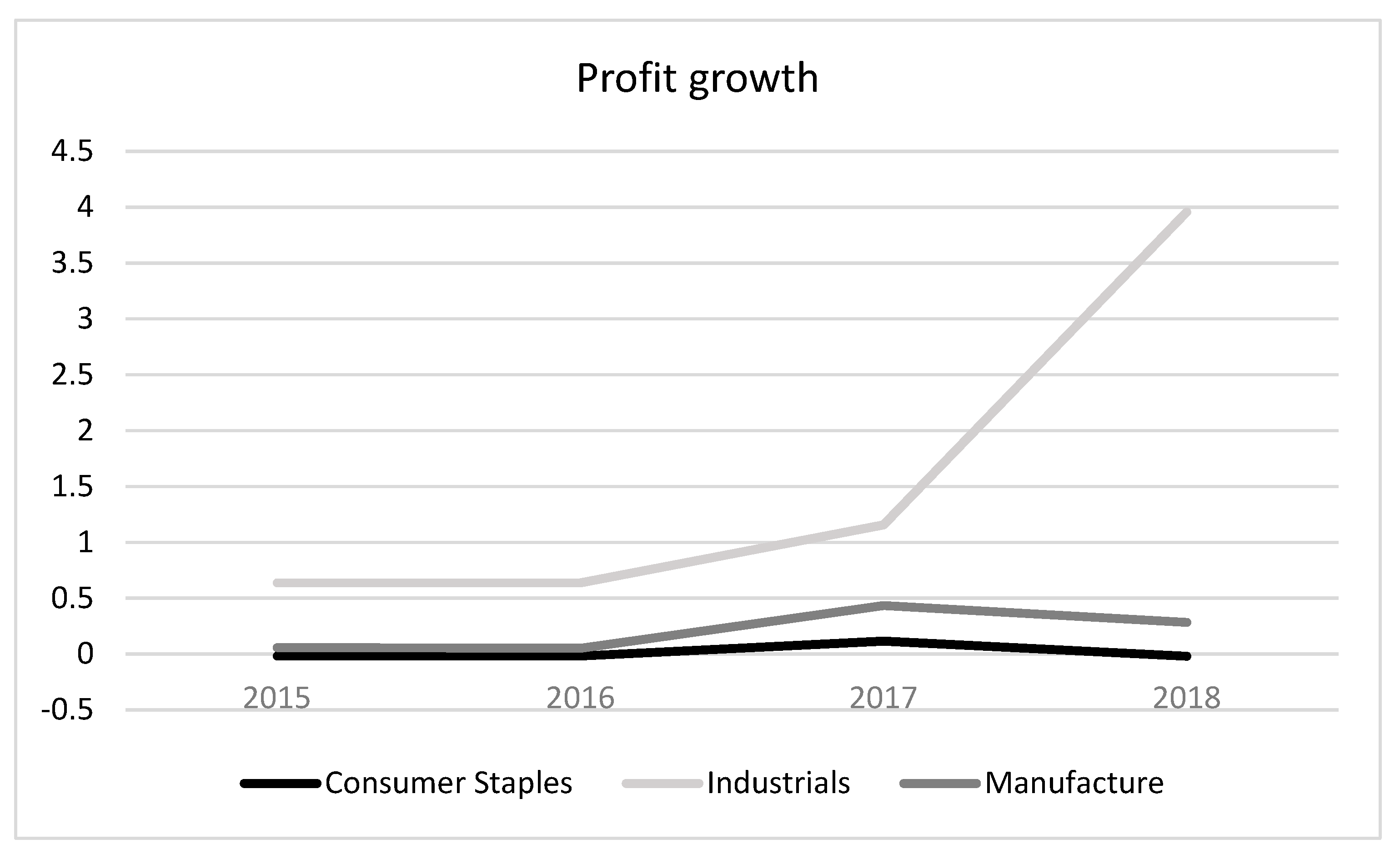

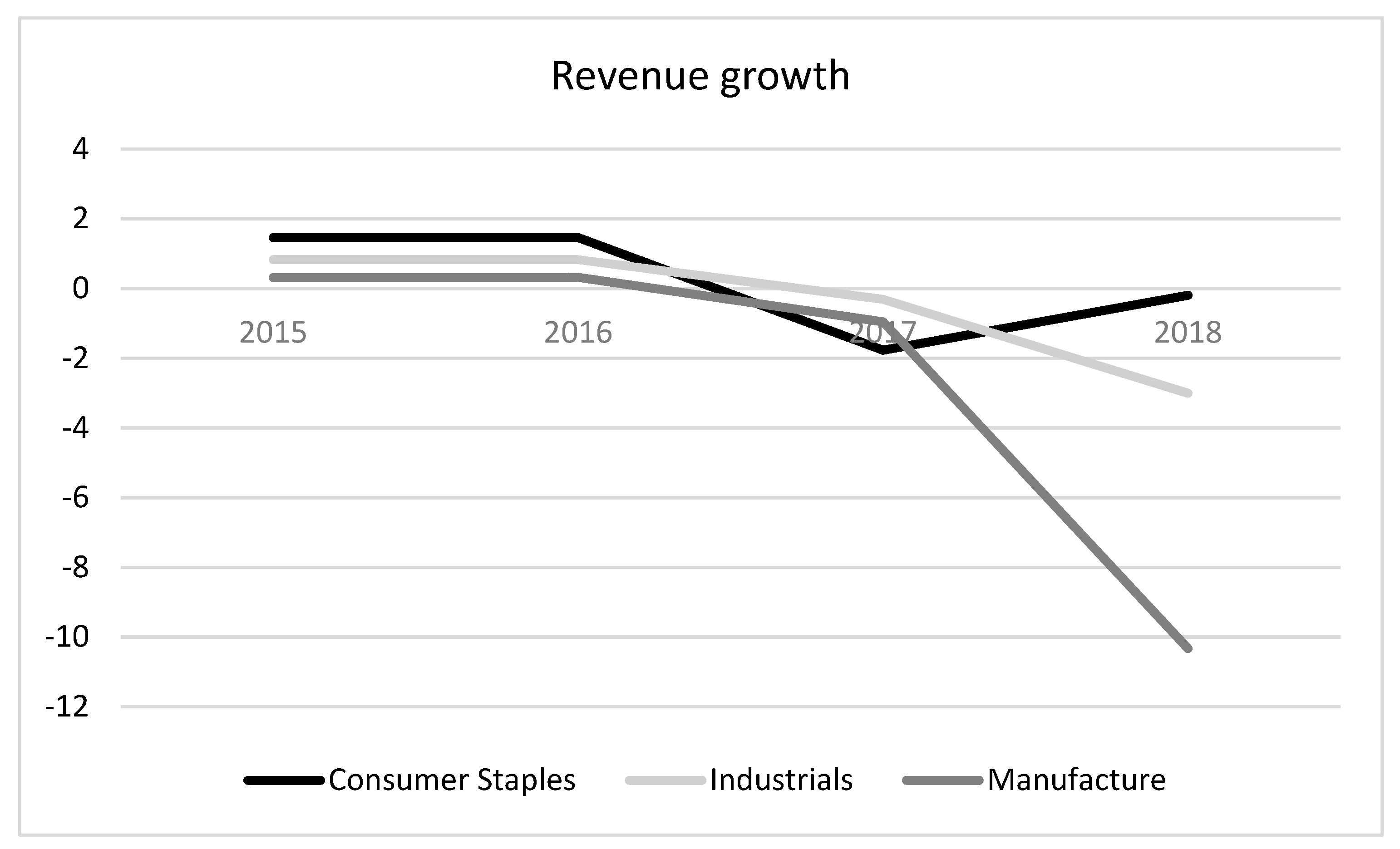

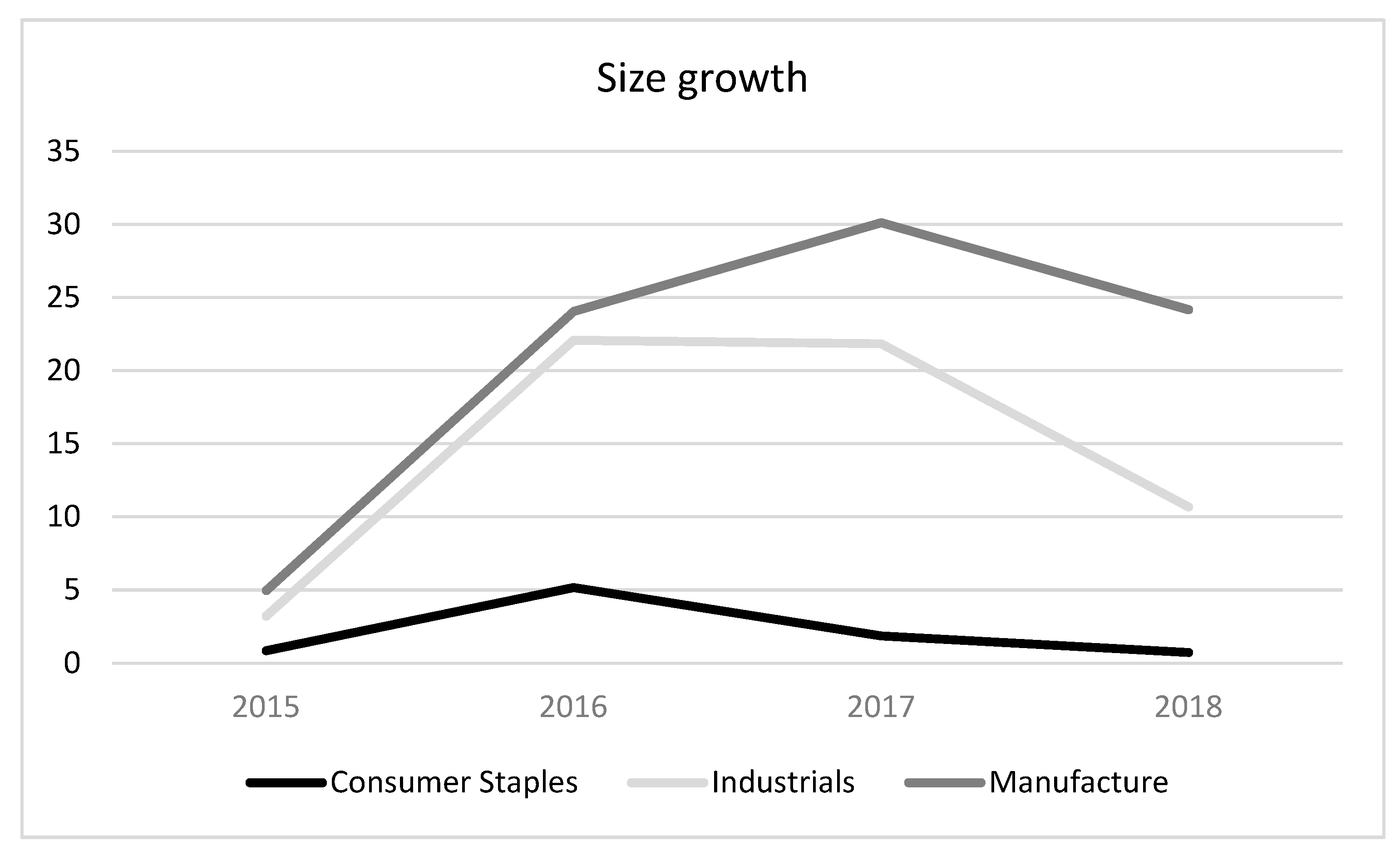

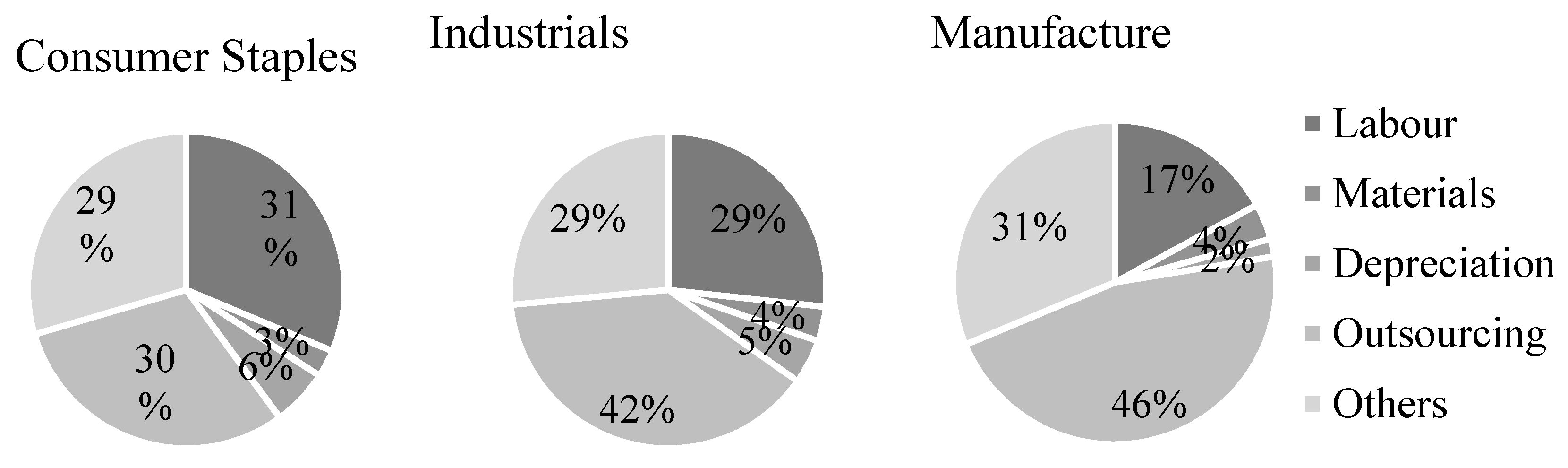

4.1. Descriptive Analysis

4.2. Empirical Models

- Model 1:

- PGRi,t = 1.162 + 0.170 × LABi,t − 0.377 × MATi,t + 2.237* × DEPi,t − 0.826 × OUTi,t −0.729 × OTHi,t + εi,t.

- Model 2:

- RGRi,t = −3.930 − 0.850 × LABi,t − 3.946 × MATi,t −0.281 × DEPi,t + 2.122 × OUTi,t + 5.153 × OTHi,t + εi,t.

- Model 3:

- SGRi,t = 0.150*** + 0.000491 × LABi,t − 0.240 × MATi,t − 0.148 × DEPi,t + 0.105* × OUTi,t −0.121 × OTHi,t + εi,t.

5. Conclusions and Recommendation

5.1. Conclusions

5.2. Limitations

5.3. Recommendation

5.3.1. For the State

5.3.2. For Vietnamese Enterprises

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Agarwal, Anupam, Eric Harmon, and Michael Viertler. 2009. Cutting Sales Costs, Not Revenues. Available online: https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/cutting-sales-costs-not-revenues (accessed on 9 October 2019).

- Ailawadi, Kusum L., and Scott A. Neslin. 1998. The Effect of Promotion on Consumption: Buying More and Consuming it Faster. Journal of Marketing Research 35: 390–98. [Google Scholar] [CrossRef]

- Ailawadi, Kusum L., Bari A. Harlam, Jacques César, and David Trounce. 2007. Quantifying and Improving Promotion Effectiveness at CVS. Marketing Science 26: 566–75. [Google Scholar] [CrossRef]

- Alchian, Arfiguremen A. 1950. Uncertainty, Evolution, and Economic Theory. Journal of Political Economy 58: 211–21. [Google Scholar] [CrossRef] [Green Version]

- Audretsch, David B., and Steven Klepper. 2000. Innovation, Evolution of Industry and Economic Growth. The International Library of Critical Writings in Economics Series; Pittsburgh: Carnegie Mellon University. [Google Scholar]

- Biesebroeck, Johannes Van. 2005. Firm Size Matters: Growth and Productivity Growth in African Manufacturing. Economic Development and Cultural Change 53: 543–83. [Google Scholar] [CrossRef]

- Blattberg, Robert C., Edward C. Malthouse, and Scott A. Neslin. 2009. Customer Lifetime Value: Empirical Generalizations and Some Conceptual Questions. Journal of Interactive Marketing 23: 157–68. [Google Scholar] [CrossRef]

- Calvo, José L. 2006. Testing Gibrat’s Law for Small, Young and Innovating Firms. Small Business Economics 26: 117–23. [Google Scholar] [CrossRef]

- Carey, Peter, Nava Subramaniam, and Karin Chua Wee Ching. 2006. Internal audit outsourcing in Australia. Accounting and Finance Association of Australia and New Zealand 46: 11–30. [Google Scholar] [CrossRef]

- Caves, Richard E. 1998. Industrial Organization and New Findings on the Turnover and Mobility of Firms. Journal of Economic Literature 36: 1947–82. [Google Scholar]

- Chandle, Gaylen N., and Erik Jansen. 1992. The founder’s self-assessed competence and venture performance. Journal of Business Venturing 7: 223–36. [Google Scholar] [CrossRef]

- Chen, Kwo-Shin, Emerson M. Babb, and Lee F. Schrader. 1985. Growth of large cooperative and proprietary firms in the US food sector. Agribusiness 1: 201–10. [Google Scholar] [CrossRef]

- Coad, Alex. 2007. Testing the principle of ‘growth of the fitter’: The relationship between profits and firm growth. Structural Change and Economic Dynamics 18: 370–86. [Google Scholar] [CrossRef]

- Coad, Alex, and Werner Hölzl. 2010. Firm Growth: Empirical Analysis. WIFO Working Papers. Available online: https://www.wifo.ac.at/jart/prj3/wifo/resources/person_dokument/person_dokument.jart?publikationsid=38423&mime_type=application/pdf (accessed on 18 February 2018).

- Connor, John M., and Scott Weimer. 1986. The intensity of advertising and other selling expenses in food and tobacco manufacturing: Measurement, determinants, and impacts. Agribusiness An International Journal 2: 293–319. [Google Scholar] [CrossRef]

- Davidsson, Per. 1989. Entrepreneurship—And after? A study of growth willingness in small firms. Journal of Business Venturing 4: 211–26. [Google Scholar] [CrossRef]

- Davidsson, Per, and Frederic Delmar. 1997. High-growth firms: Characteristics, job contribution and method observations. In RENT XI Conference. Mannhiem: Queensland University of Technology. [Google Scholar]

- Davidsson, Per, Leona Achtenhagen, and Lucia Naldi. 2010. Small Firm Growth. Foundations and Trends in Entrepreneurship 6: 69–166. [Google Scholar] [CrossRef] [Green Version]

- Delmar, Frédéric, Per Davidsson, and William Gartner. 2003. Arriving at the High-Growth Firm. Journal of Business Venturing 18: 189–216. [Google Scholar] [CrossRef] [Green Version]

- Dotdash. 2019. SME Definition. Available online: https://www.thebalancesmb.com/sme-small-to-medium-enterprise-definition-2947962#us-sme-definition (accessed on 30 September 2019).

- Drucker, Peter. 1973. Management: Tasks, responsibilities, practices. In Management: Tasks, Responsibilities, Practices. Edited by P. Drucker. New York: Harper & Row, pp. 23–29. [Google Scholar]

- Dunne, Paul, and Alan Hughes. 1994. Age, Size, Growth and Survival: UK Companies in the 1980s. Journal of Industrial Economics 42: 115–40. [Google Scholar] [CrossRef]

- European Commission. 2015. What Is an SME? Available online: https://web.archive.org/web/20150208090338/http://ec.europa.eu/enterprise/policies/sme/facts-figures-analysis/sme-definition/index_en.htm (accessed on 15 September 2019).

- Freel, Mark S., and Paul J. A. Robson. 2004. Small Firm Innovation, Growth and Performance: Evidence from Scotland and Northern England. International Small Business Journal: Researching Entrepreneurship 22: 561–75. [Google Scholar] [CrossRef]

- Gibrat, Robert. 1931. Les Inégalités Économiques. Paris: Librairie du Recueil Sirey. [Google Scholar]

- Goddard, John, Phil Molyneux, and John O. S. Wilson. 2004. Dynamics of Growth and Profitability in Banking. Journal of Money Credit and Banking 36: 1069–90. [Google Scholar] [CrossRef]

- Goverment, Vietnamese. 2018. The Decree Details Some Articles of the Law Supporting Small and Medium-Sized Businesses. 39/2018/NĐ-CP. Hanoi. Available online: http://vanban.chinhphu.vn/portal/page/portal/chinhphu/hethongvanban?class_id=1&_page=1&mode=detail&document_id=193166 (accessed on 26 December 2019).

- Gross, Jenna. 2016. Why Marketing Is SO Important? Business Market. Available online: https://movingtargets.com/blog/business-marketing/why-marketing-is-so-important/ (accessed on 15 April 2019).

- Gupta, Priya Dhamija, Samapti Guha, and Shiva Subraman. 2013. Firm growth and its determinants. Journal of Innovation and Entrepreneurship 2: 15. [Google Scholar] [CrossRef] [Green Version]

- Hölzl, Werner, and Klaus Friesenbichler. 2010. High-growth firms, innovation and the distance to the frontier. Economics Bulletin 30: 1016–24. [Google Scholar]

- Ha, Anh. 2018. Announcing and Introducing ASEAN’s Small and Medium-Sized Enterprise Policy in 2018. Available online: http://www.dangcongsan.vn/preview/newid/499741.html (accessed on 1 October 2019).

- Haas, Alexander, Ivan Snehota, and Daniela Corsaro. 2012. Creating value in business relationships: The role of sales. Industrial Marketing Management 41: 94–105. [Google Scholar] [CrossRef]

- Harabi, Najib. 2005. Determinants of Firm Growth: An Empirical Analysis from Morocco. Northwestern Switzerland: University of Applied Sciences. [Google Scholar]

- Hart, Peter E., and Nicholas Oulton. 1996. Growth and Size of Firms. Economic Journal 106: 1242–52. [Google Scholar] [CrossRef]

- Henrekson, Magnus, and Dan Johansson. 2010. Gazelles as job creators: A survey and interpretation of the evidence. Small Business Economics 35: 227–44. [Google Scholar] [CrossRef]

- Hermans, Julie, Johanna Vanderstraeten, Arjen Van Witteloostuijn, Marcus Dejardin, Dendi Ramdani, and Erik Stam. 2015. Ambitious Entrepreneurship: A Review of Growth Aspirations, Intentions, and Expectations. In Advances in Entrepreneurship, Firm Emergence, and Growth. Emerald: Emerald Group Publishing Limited, vol. 17, pp. 127–60. [Google Scholar] [CrossRef]

- Hiemstra, Stephen J. 1962. Depreciation: A Rising Cost of Processing Food Products. Journal of Farm Economics 44: 1577–82. [Google Scholar] [CrossRef]

- Huynh, Kim P., and Robert J. Petrunia. 2010. Age effects, leverage and firm growth. Journal of Economic Dynamics and Control 34: 1003–13. [Google Scholar] [CrossRef]

- Jang, SooCheong (Shawn), and Kwangmin Park. 2011. Inter-relationship between firm growth and profitability. International Journal of Hospitality Management 30: 1027–35. [Google Scholar] [CrossRef]

- Jena, Abhinash. 2013. Project Guru. PG. Available online: https://www.projectguru.in/publications/importance-marketing-success-organization/ (accessed on 12 November 2018).

- Jones, Geoffrey, and Peter Miskell. 2007. Acquisitions and firm growth: Creating Unilever’s ice cream and tea business. Business History 49: 8–28. [Google Scholar] [CrossRef]

- Ketler, Karen, and John Walstrom. 1993. The outsourcing decision. International Journal of Information Management 13: 449–59. [Google Scholar] [CrossRef]

- Koga, Maiko, and Haruko Kato. 2017. Behavioral Biases in Firms’ Growth Expectations. Ideas. Available online: https://ideas.repec.org/p/boj/bojwps/wp17e09.html (accessed on 10 June 2019).

- Konak, Fatih. 2015. The Effects of Marketing Expenses on Firm Performance: Empirical Evidence from the BIST Textile, Leather Index. Journal of Economics, Business and ManagementJournal of Economics Business and Management 3: 1068–71. [Google Scholar] [CrossRef]

- Krippendorf, Klaus. 2004. Content Analysis—An Introduction to Its Methodology, 2nd ed. California: Sage Publications, Inc. [Google Scholar]

- Kumar, Manmohan S. 1985. Growth, acquisition activity and firm size: Evidence from the United Kingdom. Journal of Industrial Economics 33: 327–38. [Google Scholar] [CrossRef]

- Levitt, Theodore. 1960. Marketing myopia. Harvard Business Review 38: 45–56. [Google Scholar] [CrossRef]

- Lindgreen, Adam, and Finn Wynstra. 2005. Value in business markets: What do we know? Where are we going? Industrial Marketing Management 34: 732–48. [Google Scholar] [CrossRef]

- Loh, Lawrence, and Natarjan Venkatraman. 1992. Determinants of Information Technology Outsourcing: A Cross-Sectional Analysis. Journal of Management Information Systems 9: 7–24. [Google Scholar] [CrossRef]

- Lotti, Francesca, Enrico Santarelli, and Marco Vivarelli IV. 2010. The relationship between size and growth: The case of Italian newborn firms. Applied Economics Letters 8: 451–54. [Google Scholar] [CrossRef]

- Lowe, D. Jordan, Marshall A. Geiger, and Kurt Pany. 1999. The Effects of Internal Audit Outsourcing on Perceived External Auditor Independence. Auditing A Journal of Practice & Theory 18: 41–44. [Google Scholar]

- Maltz, Arnold. 1994. Outsourcing the warehousing function: Economic and strategic considerations. Logistics and Transportation Review 30: 245–65. [Google Scholar]

- Mansfield, Edwin. 1962. Entry, Gibrat’s Law, Innovation, and the Growth of Firms. The American Economic Review 52: 1023–51. [Google Scholar]

- Markdao. 2019. Hire Marketing Agency—How Much Money That Business Should Spend? Markdao_Digital Marketing Solutions. Available online: https://www.markdao.com.vn/blog/thue-marketing-agency-doanh-nghiep-nen-chi-bao-nhieu-tien (accessed on 3 October 2019).

- Marris, Robin, and Adrian Wood. 1971. Growth, Competition, and Innovative Potential. Cambridge: Harvard. [Google Scholar]

- Martin, Charles L., and Michael K. Lavine. 2000. Outsourcing the internal audit function. The CPA Journal 70: 58–59. [Google Scholar]

- Melfi, Michael S. 2016. The Importance of Sales for an Entrepreneurial Organization. National Association of Sales Professionals. Available online: https://www.nasp.com/article/E7E6606D-4E51/the-importance-of-sales-for-an-entrepreneurial-organization.html (accessed on 12 October 2019).

- Mendelson, Haim. 2000. Organizational Architecture and Success in the Information Technology Industry. Management Science 46: 1–596. [Google Scholar] [CrossRef]

- Mengistae, Taye. 1999. Indigenous Ethnicity and Entrepreneurial Success in Africa: Some Evidence from Ethiopia. WB Policy Research Working Paper. Washington: SSRN. [Google Scholar]

- Minh, Hai. 2019. Business Grows Fast, but Must Be Sustainable. Available online: https://tinnhanhchungkhoan.vn/thoi-su/doanh-nghiep-phat-trien-nhanh-nhung-phai-ben-vung-278805.html (accessed on 11 October 2019).

- Ministry of Finance. 2014. Guidance on Enterprise Accounting Regime. Hanoi: Finance. [Google Scholar]

- Nelson, Eshe. 2019. The Global Economy Has Entered a Synchronized Slowdown. Available online: https://qz.com/1590499/the-global-economy-has-entered-a-synchronized-slowdown/ (accessed on 15 September 2019).

- Nguyen, Nguyen Phuc. 2016. Improve the Dynamic Competitiveness of Businesses: Research in the Field of Tourism. Research Gate. Available online: https://www.researchgate.net/publication/323474461_Nang_cao_nang_luc_canh_tranh_dong_cua_cac_doanh_nghiep_Nghien_cuu_trong_linh_vuc_du_lich (accessed on 26 December 2019).

- Nguyen, Thang Cong, Tan Ngoc Vu, Duc Hong Vo, and Dao Thi Thieu Ha. 2019. Financial Development and Income Inequality in Emerging Markets: A New Approach. Journal of Risk and Financial Management 12: 1–14. [Google Scholar] [CrossRef] [Green Version]

- Nijs, Vincent R., Marnik G. Dekimpe, Jan-Benedict E. M. Steenkamps, and Dominique M. Hanssens. 2001. The Category-Demand Effects of Price Promotions. Marketing Science 20: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Nunes, Paulo Maçãs, Zelia Serrasqueiro, Antonio Nunes, and Luis Mendes. 2013. The Relationship Between Companies Growth and Labour Productivity in Portuguese SMEs: A Dynamic Panel Data Approach. Transformations in Business and Economics 12: 20–39. [Google Scholar]

- Okpara, John O. 2011. Factors constraining the growth and survival of SMEs in Nigeria: Implications for poverty alleviation. Management Research Review 34: 156–71. [Google Scholar] [CrossRef]

- Pavitt, Keith. 1984. Sectoral patterns of technical change: Towards a taxonomy and a theory. Research Policy 13: 343–73. [Google Scholar] [CrossRef]

- Phung, Hai Trong. 2018. Vietnamese Enterprises. 2 Options: Growth Directions for SEMs. Available online: https://doanhnghiepvn.vn/doanh-nghiep/2-lua-chon-mo-hinh-tang-truong-cho-smes/20181116092546424 (accessed on 16 November 2019).

- Ramsey, Rosemary P., and Ravipreet S. Sohi. 1997. Listening to your customers: The impact of perceived salesperson listening behavior on relational outcomes. Journal of the Academy of Marketing Science 22: 127–37. [Google Scholar] [CrossRef]

- Scott, Lever. 1997. An Analysis of Managerial Motivations Behind Outsourcing Practices in Human Resources. Human Resource Planning 20: 37–47. [Google Scholar]

- Stam, Erik, and Karl Wennberg. 2009. The roles of R&D in new firm growth. Small Business Economics 33: 77–89. [Google Scholar]

- Storey, David J. 2009. Understanding the Small Business Sector: Reflextions and Confessions. SSRN. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1496214 (accessed on 4 November 2019).

- Teau, Anna Miheala. 2013. Sales Force Motivation and Compensation. Romanian Statistical Review Supplement 61: 44–50. [Google Scholar]

- Tyagi, Pradeep K., and Carl E. Block. 1983. Monetary incentives and salesmen performance. Industrial Marketing Management 12: 263–69. [Google Scholar] [CrossRef]

- Variyan, Jayachandran N., and David S. Kraybill. 1992. Empirical evidence on determinants of firm growth. Economic Letters 38: 31–36. [Google Scholar] [CrossRef]

- VCCorp Joint Stock Company. 2019. Enterprise Data. Available online: http://s.cafef.vn/du-lieu-doanh-nghiep.chn (accessed on 20 September 2019).

- Vietstock. 2019. A-Z Enterprise. Available online: https://finance.vietstock.vn/doanh-nghiep-a-z?page=1 (accessed on 16 September 2019).

- Vndirect Securities Corporation. 2019. Select Symbol. Available online: https://www.vndirect.com.vn/portal/thong-tin-co-phieu/nhap-ma-chung-khoan.shtml?request_locale=en_GB (accessed on 30 September 2019).

- Wiklund, Johan. 1999. The Sustainability of the Entrepreneurial Orientation-Performance Relationship. Entrepreneurship Theory and Practice 24: 37–48. [Google Scholar] [CrossRef]

- Wong, Poh Kam, Yuen Ping Ho, and Erkko Autio. 2005. Entrepreneurship, Innovation and Economic Growth: Evidence from GEM data. Small Business Economics 24: 335–50. [Google Scholar] [CrossRef]

- Woodruff, Robert B. 1997. Customer value: The next source for competitive advantage. Journal of the Academy of Marketing Science 25: 139–53. [Google Scholar] [CrossRef]

- World Bank. 2018. Review Updated Situation of Vietnam’s Economy. Available online: http://documents.worldbank.org/curated/en/188661544471831249/pdf/132828-VIETNAMESE-REVISED-Taking-Stock-December-2018-Vietnamese.pdf (accessed on 12 September 2019).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Role | Explanation | Calculation | Model |

|---|---|---|---|---|

| SGR | Dependent variable | Size Growth Ratio | Ln (total asset)t − Ln (total asset)t−1 | Y1 |

| Ln (total asset)t−1 | ||||

| RGR | Dependent variable | Revenue Growth Ratio | Net Sales t − Net Sales t−1 | Y2 |

| Net Sales t−1 | ||||

| PGR | Dependent variable | Profit Growth Ratio | Net Income t − Net Income t−1 | Y3 |

| Net Income t−1 | ||||

| LAB | Independent variable | Labour Expense | Labour Expense t − Labour Expense t−1 | X1 |

| Labour Expense t−1 | ||||

| MAT | Independent variable | Material and Tool Expenses | Material and Tool Expenses t − Material and Tool Expenses t−1 | X2 |

| Material and Tool Expenses t−1 | ||||

| DEP | Independent variable | Depreciation expense | Depreciation expense t − Depreciation expense t−1 | X3 |

| Depreciation expense t−1 | ||||

| OUT | Independent variable | Outsourcing Expenses | Outsourcing expenses t − Outsourcing expenses t−1 | X4 |

| Outsourcing expenses t−1 | ||||

| OTH | Independent variable | Other Expenses | Other expenses t − Other expenses t−1 | X5 |

| Other expenses t − 1 |

| Industry | Agriculture, Forestry, and Fishery | Industrials and Construction | Trade and Services | |

|---|---|---|---|---|

| Criteria | ||||

| Total revenue per year or balance sheet total | Total Revenue per year from over 200 billion VND or balance sheet total from over 100 billion VND | Total Revenue per year from over 200 billion VND or balance sheet total from over 100 billion VND | Total Revenue per year from over 300 billion VND or balance sheet total from over 100 billion VND | |

| Total employees | More than 200 people | More than 200 people | More than 100 people | |

| Profit Growth Ratio (PGR) | Revenue Growth Ratio (RGR) | Size Growth Ratio (SGR) | Labour Expense (LAB) | Material and Tool Expenses (MAT) | Depreciation Expense (DEP) | Outsourcing Expenses (OUT) | Other Expenses (OTH) | |

|---|---|---|---|---|---|---|---|---|

| Mean | 0.653 | −1.540 | 0.145 | 0.226 | 0.035 | 0.033 | 0.427 | 0.300 |

| Median | 0.097 | 0.068 | 0.038 | 0.186 | 0.002 | 0.004 | 0.410 | 0.237 |

| Maximum | 85.005 | 19.090 | 4.336 | 2.437 | 0.512 | 2.427 | 2.667 | 1.000 |

| Minimum | −0.990 | −344.302 | −0.595 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Std. Dev. | 4.978 | 20.936 | 0.402 | 0.209 | 0.076 | 0.139 | 0.304 | 0.234 |

| Skewness | 14.798 | −13.680 | 5.271 | 3.860 | 3.662 | 15.175 | 1.376 | 0.936 |

| Kurtosis | 243.503 | 214.117 | 44.074 | 37.980 | 18.555 | 260.792 | 10.225 | 3.343 |

| Jerque—Bera | 2,517,513 | 1,943,055 | 77,099 | 55,018 | 12,675 | 2,888,821 | 2562 | 155 |

| Probability | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Sum | 672 | −1585 | 150 | 233 | 36 | 34 | 439 | 309 |

| Sum Sq. Dev. | 25,473 | 450,587 | 166 | 45 | 6 | 20 | 95 | 56 |

| Observations | 1029 | 1029 | 1029 | 1029 | 1029 | 1029 | 1029 | 1029 |

| Profit Growth Ratio (PGR) | Revenue Growth Ratio (RGR) | Size Growth Ratio (SGR) | Labour Expense (LAB) | Material and Tool Expenses (MAT) | Depreciation Expense (DEP) | Outsourcing Expenses (OUT) | Other Expenses (OTH) | |

|---|---|---|---|---|---|---|---|---|

| PGR | RGR | SGR | LAB | MAT | DEP | OUT | OTH | |

| PGR | 1.000 | −0.209 | 0.077 | 0.018 | −0.008 | 0.069 | −0.029 | 0.005 |

| RGR | −0.209 | 1.000 | 0.115 | −0.017 | −0.005 | −0.002 | −0.005 | 0.036 |

| SGR | 0.077 | 0.115 | 1.000 | −0.004 | −0.049 | −0.031 | 0.132 | −0.113 |

| EGR | 0.095 | 0.150 | 0.568 | 0.018 | −0.106 | 0.224 | 0.136 | −0.134 |

| LAB | 0.018 | −0.017 | −0.004 | 1.000 | 0.003 | 0.055 | −0.221 | −0.165 |

| MAT | −0.008 | −0.005 | −0.049 | 0.003 | 1.000 | 0.031 | −0.189 | −0.104 |

| DEP | 0.069 | −0.002 | −0.031 | 0.055 | 0.031 | 1.000 | −0.036 | −0.042 |

| OUT | −0.029 | −0.005 | 0.132 | −0.221 | −0.189 | −0.036 | 1.000 | −0.594 |

| OTH | 0.005 | 0.036 | −0.113 | −0.165 | −0.104 | −0.042 | −0.594 | 1.000 |

| (PGR) | (PGR) | (PGR) | (RGR) | (RGR) | (RGR) | (SGR) | (SGR) | |

| VARIABLES | FEM | REM | REM * | FEM | REM | REM * | FEM | REM |

| LAB (Labour Expense) | −0.729 | 0.0349 | 0.170 | −4.299 | −0.362 | −0.850 | −0.167 | 0.000491 |

| (1.416) | (0.840) | (0.918) | (5.822) | (3.585) | (3.864) | (0.105) | (0.0684) | |

| MAT (Material and Tool Expenses) | 4.772 | −1.163 | −0.377 | −22.14 | 0.128 | −3.946 | −0.722 * | −0.240 |

| (5.161) | (2.253) | (2.645) | (21.23) | (9.741) | (11.21) | (0.382) | (0.188) | |

| DEP (Depreciation expense) | 0.582 | 2.399 ** | 2.237 * | −1.333 | 0.130 | −0.281 | −0.610 *** | −0.148 |

| (1.382) | (1.130) | (1.156) | (5.685) | (4.769) | (4.833) | (0.102) | (0.0903) | |

| OUT (Outsourcing Expenses) | 0.425 | −0.671 | −0.826 | 3.905 | 1.768 | 2.122 | 0.142 * | 0.105 * |

| (1.056) | (0.745) | (0.777) | (4.343) | (3.158) | (3.252) | (0.0782) | (0.0600) | |

| OTH (Other Expenses) | −0.978 | −0.393 | −0.729 | 6.136 | 4.642 | 5.153 | −0.0674 | −0.121 |

| (1.676) | (0.945) | (1.048) | (6.892) | (4.039) | (4.417) | (0.124) | (0.0772) | |

| Constant | 0.757 | 1.016 | 1.162 | −3.300 | −3.638 | −3.930 | 0.188 *** | 0.150 *** |

| (0.931) | (0.712) | (0.744) | (3.830) | (3.018) | (3.118) | (0.0690) | (0.0573) | |

| Observations | 1020 | 1020 | 1020 | 1020 | 1020 | 1020 | 1020 | 1020 |

| Number of No | 255 | 255 | 255 | 255 | 255 | 255 | 255 | 255 |

| R-squared | 0.003 | 0.005 | 0.054 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nguyen, V.C.; Nguyen, T.N.L.; Pham, T.H.; Vu, S.H. The Impacts of Selling Expense Structure on Enterprise Growth in Large Enterprises: A Study from Vietnam. J. Risk Financial Manag. 2020, 13, 4. https://doi.org/10.3390/jrfm13010004

Nguyen VC, Nguyen TNL, Pham TH, Vu SH. The Impacts of Selling Expense Structure on Enterprise Growth in Large Enterprises: A Study from Vietnam. Journal of Risk and Financial Management. 2020; 13(1):4. https://doi.org/10.3390/jrfm13010004

Chicago/Turabian StyleNguyen, Van Cong, Thi Ngoc Lan Nguyen, Thanh Hang Pham, and Song Hoa Vu. 2020. "The Impacts of Selling Expense Structure on Enterprise Growth in Large Enterprises: A Study from Vietnam" Journal of Risk and Financial Management 13, no. 1: 4. https://doi.org/10.3390/jrfm13010004

APA StyleNguyen, V. C., Nguyen, T. N. L., Pham, T. H., & Vu, S. H. (2020). The Impacts of Selling Expense Structure on Enterprise Growth in Large Enterprises: A Study from Vietnam. Journal of Risk and Financial Management, 13(1), 4. https://doi.org/10.3390/jrfm13010004