Are Family Firms Financially Healthier Than Non-Family Firm?

,

,

Abstract

:1. Introduction and Literature Review

2. Family Control and Firm Value

Hypotheses

3. The Hypothesis, Methods and Data

3.1. Empirical Model

3.1.1. Leverage

+ α5 × Profitability measure + α6 × Interactive Variables

- Leverage: Debt/EBITDA and Interest Coverage Ratio.

- Family firm takes: dummy equals 1 when a firm is a family firm or zero otherwise

- Profitability measure: refers to return of equity, return on assets, EBITDA margin, netincome margin

- Size measure: refers to number of employees, total revenues, total assets

- Age: calculate based on the company date of establishment.

- Industry dummy: equaling 1 as dummy for each IAC classification code,

- Year dummy: equals 1 for each year considered in the analysis.

3.1.2. Risk Exposure

Dummy + α5 × Profitability measure + α6 × Interactive Variables

- Altman Z-Score: 6.5X1 + 3.2X2 + 6.72X3 + 1.0X4

- Family firm takes: dummy equals 1 when a firm is a family firm or zero otherwise

- Profitability measure: refers to return of equity, return on assets, EBITDA margin, netincome margin

- Size measure: refers to number of employees, total revenues, total assets

- Age: calculated based on the company date of establishment.

- Industry dummy: equaling 1 as dummy for each IAC classification code,

- Year dummy: equals 1 for each year considered in the analysis.

3.2. Data

3.3. Variables Measurement

3.3.1. Dependent Variables

3.3.2. Independent Variables—Ownership structure

3.3.3. Other Independent Variables

3.4. Descriptive Statistics

4. Empirical Analysis

4.1. Leverage

4.2. Risk Exposure

4.3. Robustness Test

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Altman, Edward I., John Hartzell, and Matthew Peck. 1998. Emerging market corporate bonds a scoring system. In Emerging Market Capital Flows. Boston: Springer, pp. 391–400. [Google Scholar]

- Altman, Edward I., Alessandro Danovi, and Alberto Falini. 2013. ‘Z-Score Models’ Application to Italian Companies Subject to Extraordinary Administration’. Journal of Applied Finance 23: 128–37. [Google Scholar]

- Altman, Edward I., and Edith Hotchkiss. 2006. Corporate Financial Distress & Bankruptcy, 3rd ed. Hoboken: John Wiley & Sons. [Google Scholar]

- Anderson, Ronald C., and David M. Reeb. 2003. Founding-family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance 58: 1301–28. [Google Scholar]

- Asghar Butt, Affaf, Main SajidNazir, Hamera Arshad, and Aamer Shahzad. 2018. Corporate Derivatives and Ownership Concentration: Empirical Evidence of Non-Financial Firms Listed on Pakistan Stock Exchange. Journal of Risk and Financial Management 11: 33. [Google Scholar] [CrossRef] [Green Version]

- Barontini, Roberto, and Lorenzo Caprio. 2006. The effect of family control on firm value and performance: Evidence from continental Europe. European Financial Management 12: 689–723. [Google Scholar] [CrossRef]

- Bernstein, Peter L., and Peter L. Bernstein. 1996. Against the Gods: The Remarkable Story of Risk. New York: Wiley, pp. 1269–75. [Google Scholar]

- Chrisman, James J., Jess H. Chua, and Reginald A. Litz. 2004. Comparing the agency costs of family and non‐family firms: Conceptual issues and exploratory evidence. Entrepreneurship Theory and Practice 28: 335–54. [Google Scholar]

- DeAngelo, Harry, and Linda DeAngelo. 2000. Controlling stockholders and the disciplinary role of corporate payout policy: A study of the Times Mirror Company. Journal of Financial Economics 56: 153–207. [Google Scholar] [CrossRef]

- De Vries, Manfred FR Kets. 1993. The dynamics of family controlled firms: The good and the bad news. Organizational Dynamics 21: 59–71. [Google Scholar]

- Dey, Ripon, Syed Hossain, and Zabihollah Rezaee. 2018. Financial risk disclosure and financial attributes among publicly traded manufacturing companies: Evidence from Bangladesh. Journal of Risk and Financial Management 11: 50. [Google Scholar] [CrossRef] [Green Version]

- European Family Businesses. 2012. Family Business Statistics. Available online: http://www.europeanfamilybusinesses.eu/uploads/Modules/Publications/family-business-statistics.pdf (accessed on 30 September 2018).

- Garland, David. 2003. The rise of risk. In Risk and Morality. Toronto: University of Toronto Press, pp. 48–86. [Google Scholar]

- Grossman, Sanford J., and Oliver D. Hart. 1986. The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration. Journal of Political Economy 94: 691–719. [Google Scholar] [CrossRef] [Green Version]

- Hollenbeck, John R., Daniel R. Ilgen, Jean M. Phillips, and Jennifer Hedlund. 1994. Decision risk in dynamic two-stage contexts: Beyond the status quo. Journal of Applied Psychology 79: 592. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- March, James G., and Zur Shapira. 1987. Managerial perspectives on risk and risk taking. Management Science 33: 1404–18. [Google Scholar] [CrossRef] [Green Version]

- Masulis, Ronald W. 1988. The Debt/Equity Choice. Tampa: Financial Management Assoc, pp. 14–16. [Google Scholar]

- May, Don O. 1995. Do managerial motives influence firm risk reduction strategies? The Journal of Finance 50: 1291–308. [Google Scholar] [CrossRef]

- Miller, Danny, Isabelle Le Breton-Miller, Richard H. Lester, and Albert A. Canella Jr. 2007. Are family firm’s really superior performers? The Journal of Corporate Finance 13: 829–58. [Google Scholar] [CrossRef]

- Mishra, Chandra S., and Daniel L. McConaughy. 1999. Founding family control and capital structure: The risk of loss of control and the aversion to debt. Entrepreneurship: Theory and Practice 23: 53. [Google Scholar] [CrossRef]

- Neubauer, Fred, and Alden G. Lank. 2016. The Family Business: ItsGovernance for Sustainability. Berlin/Heidelberg: Springer. [Google Scholar]

- Ntoung, Agbor Tabot Lious, Helena Maria Santos De Oliveira, Cláudia M. F. Pereira, Benjamim Mamuel Ferreira De Sousa, Susana A. M. C. Bastos, and Cacilia Kome. 2017. Family Involvement in Ownership, Management and Firm Performance in Spain. Revista Contabilidade e Gestão, 21/Novembro. Lisboa: Ordem dos Contabilistas Certificados, pp. 123–53. [Google Scholar]

- Ntoung, Agbor Tabot Lious, Carlos Ferro Soto, and Ben C. Outman. 2016a. Ownership Structure and Financial Performance of Small Firms in Spain. Corporate Ownership & Control 13. [Google Scholar] [CrossRef] [Green Version]

- Ntoung, Agbor Tabot Lious, Puime Guillén Felix, and Miguel Angel Crespos Cibrán. 2016b. The Effectiveness of Spanish Banking Reforms: Application of Altman’s Z-Score. Risk Governance & Control: Financial Markets & Institution 6: 40–47. [Google Scholar]

- Oswald, Sharon L., and John S. Jahera. 1991. The influence of ownership on performance: An empirical study. Strategic Management Journal 12: 321–26. [Google Scholar] [CrossRef]

- Pérez, Paloma Fernández, and Andrea Lluch, eds. 2015. Familias Empresarias y Grande Sempresas Familiares en América Latina y España: Una Visión de Largo Plazo. Madrid: Fundacion BBVA. [Google Scholar]

- Pison, F. Irene, Cibrán F. Pilar, and Ntoung A. T. Lious. 2014. Cash flow fixing: A new approach to Economic Downturn (Small and Medium Size Enterprise). International Journal of Current Research and Academic Review 2: 271–90. [Google Scholar]

- Schulze, Willam S., Michael H. Lubatkin, Richard N. Dino, and Ann K. Buchholtz. 2001. Agency relationships in family firms: theory and evidence. Organization Science 12: 99–116. [Google Scholar] [CrossRef]

- Shleifer, Andrei, and Robert W. Vishny. 1986. Large shareholders and corporate control. The Journal of Political Economy 94: 461–88. [Google Scholar] [CrossRef] [Green Version]

- Sraer, Dvid, and David Thesmar. 2007. Performance and behavior of family firms: Evidence from the French stock market. Journal of the European Economic Association 5: 709–51. [Google Scholar] [CrossRef] [Green Version]

- Villalonga, Belen, and Raphael Amit. 2006. How do family ownership, control and management affect firm value? Journal of Financial Economics 80: 385–417. [Google Scholar] [CrossRef] [Green Version]

- Yang, Songling, Muhammad Ishtiaq, and Muhammad Anwar. 2018. Enterprise risk management practices and firm performance, the mediating role of competitive advantage and the moderating role of financial literacy. Journal of Risk and Financial Management 11: 35. [Google Scholar]

{kind=link}

| Dependent Variables | Debt/Earnings before interest, tax, depreciation and amortization (EBITDA), Interest Coverage Ratio and Altman Z-Score. |

| Independent Variables | |

| “A” | “Indicates a dummy equaling 1 if no shareholder with more than 25% of ownership of ultimate voting rights);” |

| “B” | “Indicates a dummy equaling 1 if no shareholder with more than 50% but exist one shareholder with voting rights between 25.1% and 50%.” |

| “C” | “Indicates a dummy equaling 1 if a recorded shareholder with a total or a calculated ownership of 50.1% or higher” |

| “D” | “Indicates a dummy equaling 1 if a recorded shareholder with a direct ownership of over 50% with branches and foreign companies” |

| Family Firms | “B”, “C” and “D” |

| Non-family firms | “A” |

| Family characteristics | “A family member is CEO, Chairman, CEO and Chairman, respectively in a family firm; the family only holds shares in the company without taking an active position; and the founder or a descendant is actively managing the company as Chairman or CEO.” |

| Widely held corporation | “Denote a dummy variable 1 if the largest ultimate shareholder owns more than 25% of the shares in one of the categories.” |

| Profitability measure | ROA, ROE, EBITDA margin, and Net income margin. |

| Size measure | Number of employees, total revenues, and total assets. |

| Firm age | “Defined the logarithm of the date of establishment” |

| Industry | “Defined according IAC classification code” |

| Descriptive Statistics | All Sample | Non-Family Firms | Family Firms | Difference in mean (Non-Family-Family Firms) | t-Test | |||

|---|---|---|---|---|---|---|---|---|

| Mean | Std. | Mean | Std. | Mean | Std. | |||

| Independent Variables | ||||||||

| Number of Employees | 110.79 | 96.77 | 123.63 | 221.34 | 112.78 | 73.17 | 10.85 | 1.41 |

| Total Assets | 20,108.90 | 14,480.30 | 18,331.50 | 9231.54 | 26,191.18 | 27,523.31 | −7859.66 | −8.248 * |

| Total Revenue | 20,206.30 | 13,224.60 | 19,062.50 | 9356.42 | 22,025.11 | 23,499.49 | −2962.58 | −3.514 |

| Age | 24.44 | 11.41 | 25.50 | 11.21 | 28.61 | 11.82 | 3.11 | 7.05 ** |

| Return on Assets | 2.84 | 8.05 | 2.57 | 6.45 | 2.60 | 7.60 | −0.03 | −0.10 ** |

| Return on Equity | 7.79 | 48.41 | 6.96 | 14.23 | 7.28 | 21.60 | −0.32 | −0.38 * |

| Net Income Margin | −19.22 | 1812.36 | 2.33 | 6.79 | 2.14 | 9.67 | 0.19 | −0.50 * |

| Industry dummy | ||||||||

| Cattle raising | 0.82 | 0.39 | 0.11 | 0.31 | 0.19 | 0.31 | −0.08 | −55.338 *** |

| Energy and water | 1.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Extraction, transformation of non-energetic minerals | 0.10 | 0.47 | 0.15 | 0.36 | 0.06 | 0.36 | 0.09 | 25.974 *** |

| Metal transforming industries | 0.09 | 0.50 | 0.12 | 0.33 | 0.08 | 0.33 | 0.04 | 39.118 * |

| Other manufacturing industries | 0.43 | 0.50 | 0.17 | 0.30 | 0.10 | 0.30 | 0.07 | 58.663 ** |

| Construction | 0.85 | 0.36 | 0.15 | 0.36 | 0.85 | 0.36 | −0.70 | −17.507 *** |

| Restaurant and lodging trade | 0.00 | 0.06 | 0.17 | 0.38 | 0.83 | 0.38 | −0.65 | −38.056 *** |

| Transport and Communication | 0.47 | 0.31 | 0.66 | 0.23 | 0.34 | 0.23 | 0.32 | 44.443 ** |

| Management and insurance activities | 0.35 | 0.42 | 0.54 | 0.69 | 0.39 | 0.31 | 0.13 | 14.924 ** |

| Other services | 0.86 | 0.34 | 0.14 | 0.34 | 0.86 | 0.34 | −0.73 | −18.331 ** |

| Dependent Variables | ||||||||

| Z-Score | 2.91 | 1.41 | 2.75 | 1.46 | 3.04 | 1.41 | −0.30 | −4.502 * |

| Debt/Capital | 71.92 | 319.88 | 36.67 | 60.27 | 68.61 | 197.29 | −31.95 | −4.678 *** |

| EBIT/Interest Expense | 5.78 | 1.33 | 4.17 | 1.32 | 9.05 | 51.21 | −4.88 | 2.875 ** |

| Debt/EBITDA | 3.09 | 0.45 | −1.45 | 184.97 | 3.11 | 210.59 | −4.56 | 0.49 ** |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| Intercept | −6.37 ** | −1.82 | 5.74 ** | −9.88 * | −8.65 * |

| (−0.843) | (−0.04) | (0.015) | (−0.13) | (0.61) | |

| Family Dummy | −6.78 *** | −2.89 ** | −4.72 ** | −3.34 ** | −8.32 ** |

| (−0.366) | (−0.12) | (−0.23) | (−0.01) | (0.46) | |

| Return on Assets | −1.53 * | −2.30 * | −5.74 ** | −5.44 | |

| (0.547) | (0.55) | (0.04) | (−0.11) | ||

| Return on Equity | −0.033 * | −4.63 * | −1.39 ** | −0.01 * | −5.55 ** |

| (0.01) | (0.039) | (−0.10) | (0.00) | (0.07) | |

| Total Revenue | −0.037 * | −0.04 | −0.034 | −0.00 | |

| (−1.32) | (−1.40) | (−1.25) | (−0.09) | ||

| Age of Firm | 0.64 * | 0.03 * | −3.30 ** | 3.41 | |

| (−0.24) | (0.01) | (0.06) | (0.05) | ||

| Number of Employees | 1.66 *** | 4.80 | −3.11 ** | −5.23 * | |

| (0.518) | (−0.50) | (−0.33) | (−0.55) | ||

| Size (log of Total Assets) | 5.26 * | 7.715 ** | 3.58 ** | 1.40 | 9.89 * |

| (1.042) | (0.06) | (0.01) | (0.26) | (1.25) | |

| EBITDA Margin | −0.55 * | −0.37 ** | 0.22 * | −1.38 ** | −2.78 ** |

| (0.02) | (−0.02) | (0.14) | (−0.06) | (4.32) | |

| Net Income Margin | −0.22 * | −5.14 ** | −2.34 ** | −6.36 * | |

| (−0.143) | (0.21) | (−0.59) | (0.137) | ||

| Return on Assets*Family | −2.74 ** | ||||

| (−2.17) | |||||

| Return on Equity*Family | −1.68 ** | −5.72 ** | 0.02 * | −7.74 ** | |

| (−0.03) | (0.10) | (−0.12) | (−0.07) | ||

| Total Revenue*Family | −5.35 * | ||||

| (−1.18) | |||||

| Age of Firm*Family | 2.16 ** | −7.86 | −4.80 ** | ||

| (−0.12) | (0.92) | (−0.11) | |||

| Number of Employees*Family | 5.04 | 3.00 | 5.35 | ||

| (0.72) | (0.44) | (0.76) | |||

| Size (log of Total Assets)*Family | 5.28 ** | −1.23 * | −0.35 ** | ||

| (0.12) | (2.19) | (−0.22) | |||

| EBITDA Margin*Family | −0.26 | −0.85 ** | |||

| (0.17) | (−0.77) | ||||

| Net Income Margin*Family | −0.02 | −0.02 | |||

| (−0.02) | (−2.19) | ||||

| Adjusted R2 | 23.2 *** | 23.2 *** | 21.5 *** | 28.7 *** | 29.4 *** |

| Industry Dummy included | Yes | Yes | No | No | No |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| Intercept | −7.27 ** | 5.88 | −6.44 ** | −15.35 ** | −19.62 |

| (−4.44) | (0.90) | (1.94) | (2.69) | (0.39) | |

| Family Dummy | −1.72 ** | −30.23 | −0.52 | −4.50 *** | −3.04 ** |

| (−1.98) | (−0.93) | (−0.32) | (−3.70) | (−2.44) | |

| Return on Assets | −1.95 *** | −1.98 *** | 1.20 | ||

| (30.34) | (30.28) | (0.18) | |||

| Return on Equity | −0.016 | −0.77 *** | −0.69 *** | −0.74 *** | −0.64 * |

| (−1.48) | (3.75) | (−3.54) | (3.61) | (−1.75) | |

| Total Revenue | −0.00 | −0.00 *** | −0.00 | −0.00 | |

| (1.48) | (−0.00) | (−0.06) | (−0.50) | ||

| Age of Firm | −9.64 | 11.59 ** | −11.79 * | −10.88 | |

| (−0.24) | (−5.73) | (−1.77) | (−1.73) | ||

| Number of Employees | −2.64 * | −0.00 | 0.01 ** | −0.01 ** | |

| (−2.89) | (−0.18) | (0.52) | (−0.33) | ||

| Size (log of Total Assets) | −3.125 | 1.78 ** | 0.64 ** | 2.79 ** | 2.53 * |

| (2.72) | (−0.29) | (0.32) | (2.21) | (2.09) | |

| EBITDA Margin | −0.01 | −1.69 | −0.063 | −1.16 | |

| (−0.28) | (−1.20) | (−1.34) | (−0.00) | ||

| Net Income Margin | −2.35 * | −0.00 | −7.20 *** | −5.27 *** | |

| (1.65) | (−0.34) | (−4.66) | (−1.18) | ||

| Return on Assets*Family | −0.05 ** | ||||

| (0.91) | |||||

| Return on Equity*Family | −1.68 ** | −0.33 ** | −0.31 ** | ||

| (−0.03) | (−3.22) | (−1.71) | |||

| Total Revenue*Family | −4.45 *** | ||||

| (−4.46) | |||||

| Age of Firm*Family | 5.23 | 5.46 ** | −4.96 ** | ||

| (1.49) | (1.57) | (1.51) | |||

| Number of Employees*Family | 0.00 | −0.11 | 0.00 | ||

| (0.16) | (−0.89) | (0.35) | |||

| Size (log of Total Assets)*Family | 1.88 ** | −2.53 ** | |||

| (0.58) | (2.09) | ||||

| EBITDA Margin*Family | −2.98 | ||||

| (−2.18) | |||||

| Net Income Margin*Family | −7.46 | ||||

| (−4.85) | |||||

| Adjusted R2 | 23.3 *** | 23.2 *** | 24.5 *** | 27.4 *** | 31.3 *** |

| Industry Dummy included | Yes | Yes | Yes | No | No |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| Intercept | −0.16 | 1.13 | −1.92 ** | 1.52 *** | 1.28 *** |

| (−0.48) | (3.36) | (2.82) | (9.80) | (8.21) | |

| Family Dummy | 0.13 ** | 0.06 | 0.31 | 3.16 *** | 0.58 ** |

| (2.89) | (0.74) | (0.88) | (11.05) | (3.15) | |

| Return on Assets | 0.07 *** | 0.25 *** | 0.00 ** | ||

| (38.28) | (2.81) | (0.00) | |||

| Return on Equity | 0.00 ** | 0.01 *** | 0.01 *** | 0.02 *** | 0.05 * |

| (2.41) | (14.15) | (13.90) | (3.69) | (4.62) | |

| Total Revenue | 0.00 *** | 0.04 *** | 0.00 | 0.00 *** | |

| (11.59) | (0.52) | (0.28) | (13.38) | ||

| Age of Firm | 9.64 | 0.07 | 0.09 ** | 0.07 ** | |

| (0.24) | (0.34) | (2.69) | (2.16) | ||

| Number of Employees | 1.34 * | 0.00 ** | 0.00 *** | 0.00 ** | |

| (4.21) | (3.56) | (0.52) | (6.15) | ||

| Size (log of Total Assets) | 0.23 ** | 0.36 *** | 0.18 ** | 6.30 *** | 0.37 *** |

| (6.5) | (10.88) | (0.56) | (2.21) | (4.19) | |

| EBITDA Margin | 0.00 | 0.00 ** | 36.11 *** | 0.00 *** | |

| (2.05) | (2.30) | (−3.54) | (2.13) | ||

| Net Income Margin | 16.62 *** | 0.00 * | 17.27 *** | 3.21 *** | |

| (12.59) | (0.00) | (13.06) | (5.38) | ||

| Return on Assets*Family | 0.04 ** | ||||

| (3.37) | |||||

| Return on Equity*Family | 0.00 | 0.33 ** | 0.03 *** | ||

| (0.21) | (3.22) | (4.56) | |||

| Total Revenue*Family | 4.45 *** | ||||

| (4.46) | |||||

| Age of Firm*Family | 0.32 *** | 0.09 ** | 0.07 ** | ||

| (1.68) | (2.11) | (2.39) | |||

| Number of Employees*Family | 0.00 ** | 0.00 | 0.00 ** | ||

| (0.00) | (−7.01) | (6.97) | |||

| Size (log of Total Assets)*Family | 0.00 ** | 0.11 ** | |||

| (0.00) | (5.92) | ||||

| EBITDA Margin*Family | −37.70 | ||||

| (−3.73) | |||||

| Net Income Margin*Family | −23.34 *** | ||||

| (−17.37) | |||||

| Adjusted R2 | 23.6 *** | 23.2 *** | 23.8 *** | 30.1 | 31.3 |

| Industry Dummy included | Yes | Yes | Yes | No | No |

| Family Ownership | |||||

|---|---|---|---|---|---|

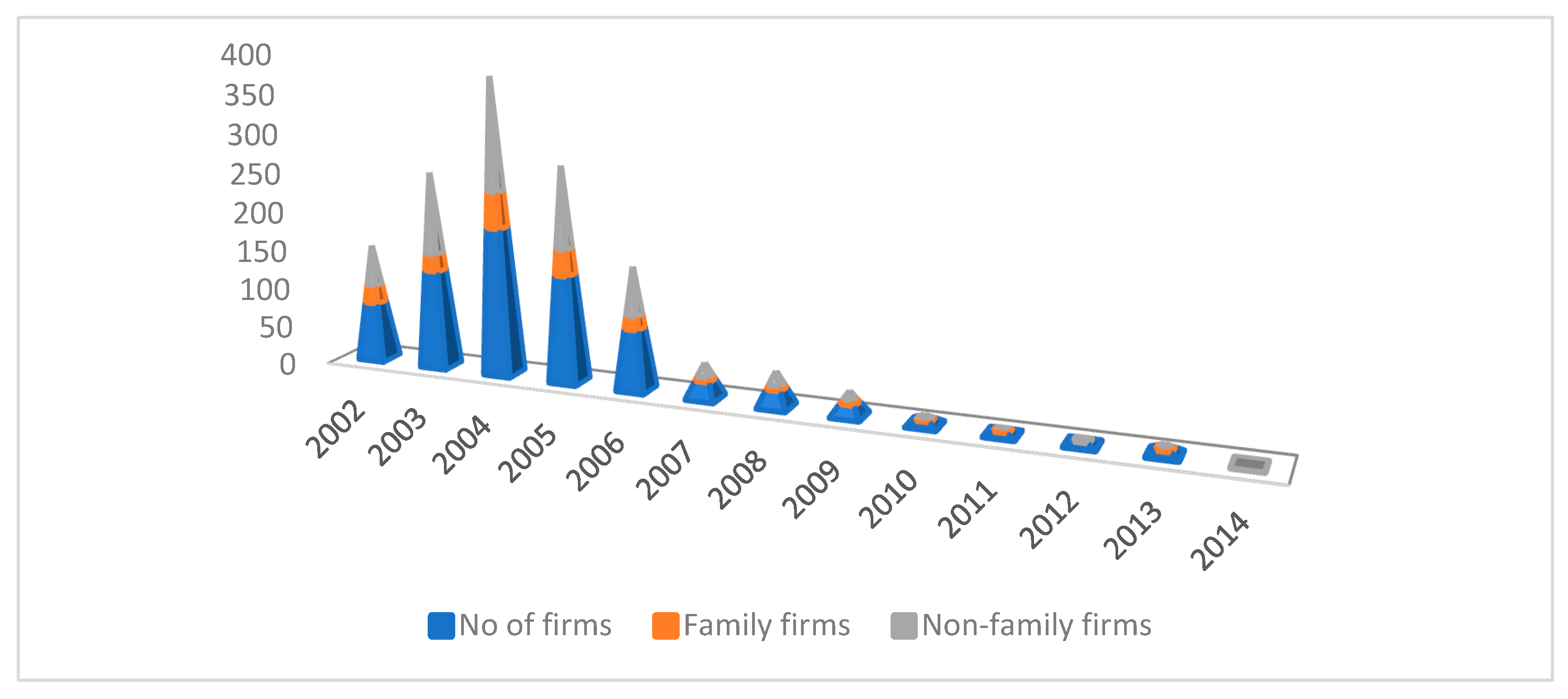

| Year | Number of Firms | Family Firms % | Family Insiders % | Family Blockholders % | Both Insiders & Blockholders % |

| 2014 | 0 | 0% | 0% | 0% | 0% |

| 2013 | 6 | 50% | 50% | 50% | 0% |

| 2012 | 4 | 0% | 0% | 0% | 0% |

| 2011 | 4 | 33.3% | 100% | 0% | 0% |

| 2010 | 6 | 20% | 0% | 100% | 0% |

| 2009 | 15 | 50% | 80% | 20% | 0% |

| 2008 | 22 | 29.4% | 60% | 40% | 0% |

| 2007 | 22 | 29.4% | 60% | 40% | 0% |

| 2006 | 78 | 27.9% | 65% | 35% | 0% |

| 2005 | 137 | 31.7% | 67% | 33% | 0% |

| 2004 | 189 | 32.2% | 76% | 24% | 0% |

| 2003 | 126 | 21.2% | 91% | 9% | 0% |

| 2002 | 75 | 44.2% | 65% | 35% | 0% |

| Year | Mean Age All Bankrupt Firms | Mean Age (Non-Family Firms) | Mean Age (Family) Firms | Difference (Non-Family-Family Firms) | t-Test | p-Value |

|---|---|---|---|---|---|---|

| 2014 | 13.441 | 16.267 | 0.000 | 16.267 | 67.673 | 0.000 *** |

| 2013 | 23.280 | 26.850 | 12.330 | 14.530 | 1.360 | 0.268 |

| 2012 | 44.000 | 22.500 | 0.00 | −7.250 | −0.298 | 0.816 |

| 2011 | 16.500 | 26.700 | 23.900 | 2.800 | 0.000 | 0.000 *** |

| 2010 | 19.843 | 26.900 | 8.467 | 18.433 | 1.307 | 0.321 |

| 2009 | 19.096 | 23.900 | 2.600 | 21.230 | 3.597 | 0.023 ** |

| 2008 | 17.755 | 7.380 | 14.240 | −6.860 | −2.568 | 0.062 * |

| 2007 | 19.382 | 0.000 | 17.540 | −17.540 | −4.236 | 0.013 ** |

| 2006 | 14.691 | 0.000 | 18.760 | −18.760 | −3.028 | 0.039 ** |

| 2005 | 14.738 | 0.000 | 13.429 | −13.429 | −7.551 | 0.000 *** |

| 2004 | 12.192 | 18.013 | 12.392 | 5.621 | 1.989 | 0.054 * |

| 2003 | 10.274 | 14.246 | 4.015 | 10.229 | 7.902 | 0.000 *** |

| 2002 | 9.046 | 12.059 | 2.152 | 9.908 | 10.118 | 0.000 *** |

| Family Ownership | |||||

|---|---|---|---|---|---|

| Year | Number of Firms % | Family Firms % | Family Insiders % | Family Blockholders % | Both Insiders & Blockholders % |

| 2014 | 0 | 0 | 0 | 0 | |

| 2013 | 4 | 17% | 17% | 0% | 0 |

| 2012 | 0 | 0% | 0% | 0% | 0 |

| 2011 | 4 | 25% | 25% | 0% | 0 |

| 2010 | 3 | 0% | 0% | 0% | 0 |

| 2009 | 7 | 0% | 0% | 0% | 0 |

| 2008 | 13 | 18% | 14% | 5% | 0 |

| 2007 | 13 | 18% | 14% | 5% | 0 |

| 2006 | 16 | 21% | 19% | 1% | 0 |

| 2005 | 18 | 24% | 18% | 7% | 0 |

| 2004 | 21 | 22% | 16% | 6% | 0 |

| 2003 | 0 | 0% | 0% | 0% | 0 |

| 2002 | 0 | 0% | 0% | 0% | 0 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ntoung, L.A.T.; Santos de Oliveira, H.M.; Sousa, B.M.F.d.; Pimentel, L.M.; Bastos, S.A.M.C. Are Family Firms Financially Healthier Than Non-Family Firm? J. Risk Financial Manag. 2020, 13, 5. https://doi.org/10.3390/jrfm13010005

Ntoung LAT, Santos de Oliveira HM, Sousa BMFd, Pimentel LM, Bastos SAMC. Are Family Firms Financially Healthier Than Non-Family Firm? Journal of Risk and Financial Management. 2020; 13(1):5. https://doi.org/10.3390/jrfm13010005

Chicago/Turabian StyleNtoung, Lious Agbor Tabot, Helena Maria Santos de Oliveira, Benjamim Manuel Ferreira de Sousa, Liliana Marques Pimentel, and Susana Adelina Moreira Carvalho Bastos. 2020. "Are Family Firms Financially Healthier Than Non-Family Firm?" Journal of Risk and Financial Management 13, no. 1: 5. https://doi.org/10.3390/jrfm13010005

APA StyleNtoung, L. A. T., Santos de Oliveira, H. M., Sousa, B. M. F. d., Pimentel, L. M., & Bastos, S. A. M. C. (2020). Are Family Firms Financially Healthier Than Non-Family Firm? Journal of Risk and Financial Management, 13(1), 5. https://doi.org/10.3390/jrfm13010005