Banking Development and Economy in Greece: Evidence from Regional Data

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Banking Efficiency

3.2. Measuring Efficiency with DEA

3.3. Panel Regressions

4. Results and Conclusions

4.1. DEA Results

4.2. Panel Data Results

4.3. Summary and Conclusion

Funding

Conflicts of Interest

References

- Altunbas, Yener, and Phil Molyneux. 1996. Economies of scale and scope in European banking. Applied Financial Economics 6: 367–75. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, Davis Gabauer, and Rangan Gupta. 2019. Greek Economic Policy Uncertainty: Does it Matter for Europe? Evidence from a Dynamic Connectedness Decomposition Approach. Physica A: Statistical Mechanics and Its Applications 535: 122280. [Google Scholar] [CrossRef]

- Asmild, Mette, and Minyan Zhu. 2016. Controlling for the use of extreme weights in bank efficiency assessments during the financial crisis. European Journal of Operational Research 251: 999–1015. [Google Scholar] [CrossRef]

- Asteriou, Dimitrios, and Stephen G. Hall. 2015. Applied Econometrics, 3rd ed. London: Macmillan International Higher Education. [Google Scholar]

- Athanassopoulos, Andreas D. 1997. Service quality and operating efficiency synergies for management control in the provision of financial services: Evidence from Greek bank branches. European Journal of Operational Research 98: 300–13. [Google Scholar] [CrossRef]

- Avramidis, Panagiotis, Ioannis Asimakopoulos, Dimitris Malliaropoulos, and Nickolaos G. Travlos. 2020. Do banks appraise internal capital markets during credit shocks? Evidence from the Greek Crisis. Journal of Financial Intermediation. [Google Scholar] [CrossRef]

- Berger, Allen N., and Loretta J. Mester. 2003. Explaining the dramatic changes in performance of US banks: Technological change, deregulation, and dynamic changes in competition. Journal of Financial Intermediation 12: 57–95. [Google Scholar] [CrossRef] [Green Version]

- Berger, Allen N., John H. Leusner, and John J. Mingo. 1997. The efficiency of bank branches. Journal of Monetary Economics 40: 141–62. [Google Scholar] [CrossRef]

- Bernini, Cristina, and Paola Brighi. 2018. Bank branches expansion, efficiency and local economic growth. Regional Studies 52: 1332–45. [Google Scholar] [CrossRef]

- Charnes, Abraham, William W. Cooper, and Edwardo Rhodes. 1978. Measuring the efficiency of decision making units. European Journal of Operational Research 2: 429–44. [Google Scholar] [CrossRef]

- Christodoulakis, Nicos. 2016. Greek crisis in perspective: Origins, effects and ways-out. In Banking Crises: Perspectives from the New Palgrave Dictionary of Economics. Edited by Garret Jones. Hampshire: Palgrave MacMillan, pp. 119–43. [Google Scholar]

- Coccorese, Paolo, and Sherrill Shaffer. 2020. Cooperative banks and local economic growth. Regional Studies. [Google Scholar] [CrossRef]

- Degl’Innocenti, Marta, Stavros A. Kourtzidis, Zeljko Sevic, and Nickolaos G. Tzeremes. 2017a. Investigating bank efficiency in transition economies: A window-based weight assurance region approach. Economic Modelling 67: 23–33. [Google Scholar] [CrossRef] [Green Version]

- Degl’Innocenti, Marta, Stavros A. Kourtzidis, Zeljko Sevic, and Nickolaos G. Tzeremes. 2017b. Bank productivity growth and convergence in the European Union during the financial crisis. Journal of Banking & Finance 75: 184–99. [Google Scholar]

- Delis, Manthos. 2009. Banking Lecture Notes. Ioannina: University of Ioannina. [Google Scholar]

- Dietsch, Michel, and Ana Lozano-Vivas. 2000. How the environment determines banking efficiency: A comparison between French and Spanish industries. Journal of Banking & Finance 24: 985–1004. [Google Scholar]

- Donatos, Gekrge S., and Dimitris I. Gikas. 2008. Relative Efficiency in the branch network of a Greek bank: A quantitative analysis. European Research Studies 3: 53–72. [Google Scholar]

- Du, Kai, Andrew C. Worthington, and Valentin Zelenyuk. 2018. Data envelopment analysis, truncated regression and double-bootstrap for panel data with application to Chinese banking. European Journal of Operational Research 265: 748–764. [Google Scholar] [CrossRef] [Green Version]

- Floros, Christos, and Ioannis Chatziantoniou. 2017. The Greek Debt Crisis: In Quest of Growth in Times of Austerity. London: Palgrave MacMillan. [Google Scholar]

- Floros, Christos, and Georgia Giordani. 2008. ATM and Banking efficiency: The case of Greece. Banks and Bank Systems 3: 55–64. [Google Scholar]

- Floros, Christos, Zacharias Voulgaris, and Christos Lemonakis. 2014. Regional firm performance: The case of Greece. Procedia Economics and Finance 14: 210–19. [Google Scholar] [CrossRef] [Green Version]

- Floros, Christos, Constantin Zopounidis, Yong Tan, Christos Lemonakis, Alexandros Garefalakis, and Efthalia Tabouratzi. 2020. Efficiency in Banking: Does the Choice of inputs and outputs matter? International Journal of Computational Economics and Econometrics 10: 129–48. [Google Scholar] [CrossRef]

- Gaganis, Chrysovalantis, Aggeliki Liadaki, Michael Doumpos, and Constantin Zopounidis. 2009. Estimating and analyzing the efficiency and productivity of bank branches. Managerial Finance 35: 202–18. [Google Scholar] [CrossRef]

- Galenianos, Manolis. 2015. The Greek Crisis: Origins and Implications. Research Paper Νο 16. Athens: Hellenic Foundation for European and Foreign Policy (ELIAMEP). [Google Scholar]

- Giokas, Dimitris I. 1991. Bank branch operating efficiency: A comparative application of DEA and the loglinear model. Omega 19: 549–57. [Google Scholar] [CrossRef]

- Hartman, Thomas E., James E. Storbeck, and Patricia Byrnes. 2001. Allocative efficiency in branch banking. European Journal of Operational Research 134: 232–42. [Google Scholar] [CrossRef]

- Hasan, Iftekhar, Michael Koetter, and Michael Wedow. 2009. Regional growth and finance in Europe: Is there a quality effect of bank efficiency? Journal of Banking and Finance 33: 1446–53. [Google Scholar] [CrossRef] [Green Version]

- Humphrey, David B. 1994. Delivering deposit services: ATMs versus Branches. Federal Reserve Bank of Richmond Economic Quarterly 80: 59–81. [Google Scholar]

- Kevork, Ilias S., Jenny Pange, Panayiotis Tzeremes, and Nickoloas G. Tzeremes. 2017. Estimating Malmquist productivity indexes using probabilistic directional distances: An application to the European banking sector. European Journal of Operational Research 261: 1125–40. [Google Scholar] [CrossRef]

- Maudos, Joaquin, Jose M. Pastor, Francisco Pérez, and Javier Quesada. 2002. Cost and profit efficiency in European banks. Journal of International Financial Markets, Institutions and Money 12: 33–58. [Google Scholar] [CrossRef]

- Meghir, Costas, Christopher A. Pissarides, Dimitri Vayanos, and Nikolaos Vettas. 2017. Beyond Austerity: Reforming the Greek Economy. Cambridge: The MIT Press. [Google Scholar]

- Monokroussos, Platon, Anna Dimitriadou, Ioannis Gkionis, Stylianos G. Gogos, Paraskevi Petropoulou, and Theodoros Stamatiou. 2016. One Year Capital Controls in Greece. Eurobank Economic Research. Available online: https://www.eurobank.gr/Uploads/Reports/GLOBAL_FOCUS_NOTE_20160805.pdf (accessed on 12 October 2020).

- Oral, Muhittin, and Reha Yolalan. 1990. An empirical study on measuring operating efficiency and profitability of bank branches. European Journal of Operational Research 46: 282–94. [Google Scholar] [CrossRef]

- Parkan, Celik. 1987. Measuring the efficiency of service operations: An application to bank branches. Engineering Costs and Production Economics 12: 237–42. [Google Scholar] [CrossRef]

- Pastor, Jesus T., C. A. Knox Lovell, and Henry Tulkens. 2006. Evaluating the financial performance of bank branches. Annals of Operations Research 145: 321–37. [Google Scholar] [CrossRef]

- Pavlopoulos, Panayiotos G., and A. K. Kouzelis. 1989. Cost behaviour in the banking industry: Evidence from a Greek commercial bank. Applied Economics 21: 285–93. [Google Scholar] [CrossRef]

- Portela, Maria Conceiçao A. Silva, and Emmanuel Thanassoulis. 2007. Comparative efficiency analysis of Portuguese bank branches. European Journal of Operational Research 177: 1275–88. [Google Scholar] [CrossRef] [Green Version]

- Samitas, Aristeidis, and Stathis Polyzos. 2016. Freeing Greece from capital controls: Were the restrictions enforced in time? Research in International Business and Finance 37: 196–213. [Google Scholar] [CrossRef]

- Schaffnit, Claire, Dan Rosen, and Joseph C. Paradi. 1997. Best practice analysis of bank branches: An application of DEA in a large Canadian bank. European Journal of Operational Research 98: 269–89. [Google Scholar] [CrossRef]

- Shamim, Farkhanda, Nobuyoshi Yamori, and Shahid Anjum. 2017. Clicks business of deposit-taking institutions: An efficiency analysis. Journal of Economic Studies 44: 911–30. [Google Scholar] [CrossRef]

- Sherman, David H., and Franklin Gold. 1985. Bank branch operating efficiency. Evaluation with data envelopment analysis. Journal of Banking and Finance 9: 297–315. [Google Scholar] [CrossRef]

- Sherman, David H., and George Ladino. 1995. Managing bank productivity using data envelopment analysis. Interfaces 25: 60–73. [Google Scholar] [CrossRef]

- Soteriou, Andreas, and Stavros A. Zenios. 1999. Operations, quality and profitability in the provision of banking services. Management Science 45: 1221–38. [Google Scholar] [CrossRef]

- Spiezia, Vincenzo. 2003. Measuring Regional Economies. In OECD Statistics Brief. No. 6. Paris: OECD. [Google Scholar]

- Spokeviciute, Laima, Kevin Keasey, and Francesco Vallascas. 2019. Do financial crises cleanse the banking industry? Evidence from us commercial bank exits. Journal of Banking & Finance 99: 222–36. [Google Scholar]

- Stournaras, Yannis. 2019. Lessons from the Greek crisis: Past, present, future. Atlantic Economic Journal 47: 127–35. [Google Scholar] [CrossRef]

- Tan, Yong, and Christos Floros. 2012. Bank profitability and inflation: The case of China. Journal of Economic Studies 39: 675–96. [Google Scholar] [CrossRef] [Green Version]

- Tan, Yong, and Christos Floros. 2013. Risk, capital and efficiency in Chinese banking. Journal of International Financial Markets, Institutions and Money 26: 378–93. [Google Scholar] [CrossRef] [Green Version]

- Tan, Yong, and Christos Floros. 2014. Risk, profitability and competition: Evidence from the Chinese banking industry. Journal of Developing Areas 48: 303–49. [Google Scholar] [CrossRef]

- Tan, Yong, and Christos Floros. 2018. Risk, competition, and efficiency in banking: Evidence from China. Global Finance Journal 35: 223–36. [Google Scholar] [CrossRef]

- Tan, Yong, and Christos Floros. 2020. Risk, competition and efficiency in the Chinese banking industry. International Journal of Banking, Accounting, and Finance 10: 144–61. [Google Scholar] [CrossRef]

- Tziogkidis, Panagiotis, Kent Matthews, and Dionisis Philippas. 2018. The effects of sector reforms on the productivity of Greek Banks: A step-by-step analysis of the pre-Euro Era. Annals of Operations Research 266: 531–49. [Google Scholar] [CrossRef]

- Valverde, Santiago Carbo, David B. Humphrey, and Rafael Lopez del Paso. 2007. Do cross-country differences in bank efficiency support a policy of “national champions”? Journal of Banking & Finance 31: 2173–88. [Google Scholar]

- Vassiloglou, Myrto, and Dimitrios Giokas. 1990. A study of the relative efficiency of bank branches: An application of data envelopment analysis. The Journal of the Operational Research Society 41: 591–97. [Google Scholar] [CrossRef]

- Walter, Ingo. 1999. Financial service strategies in the euro-zone. EIB Cahiers Papers 4: 145–68. [Google Scholar] [CrossRef] [Green Version]

- Williams, Jonathan, and Edward Gardener. 2003. The efficiency of European banking. Regional Studies 37: 321–30. [Google Scholar] [CrossRef]

- Wu, Desheng, Yang Zijiang, and Liang Liang. 2006a. Using DEA-neural network approach to evaluate branch efficiency of a large Canadian bank. Expert Systems with Applications 31: 108–15. [Google Scholar] [CrossRef]

- Wu, Desheng, Yang Zijiang, and Liang Liang. 2006b. Efficiency analysis of cross-region bank branches using fuzzy data envelopment analysis. Applied Mathematics and Computation 181: 271–81. [Google Scholar] [CrossRef]

- Zilberfarb, Ben-Zion. 1989. The effect of Automated Teller Machines on demand deposits: An empirical analysis. Journal of Financial Services Research 2: 49–57. [Google Scholar] [CrossRef]

| 1 | For more information about the Greek crisis, see Galenianos (2015); Christodoulakis (2016); Floros and Chatziantoniou (2017). |

| 2 | After several years of financial assistance programs, Greek economy returned to growth. According to the International Monetary Fund, the primary fiscal surplus was 3.8% in 2018 and the economy grows at 2% a year. |

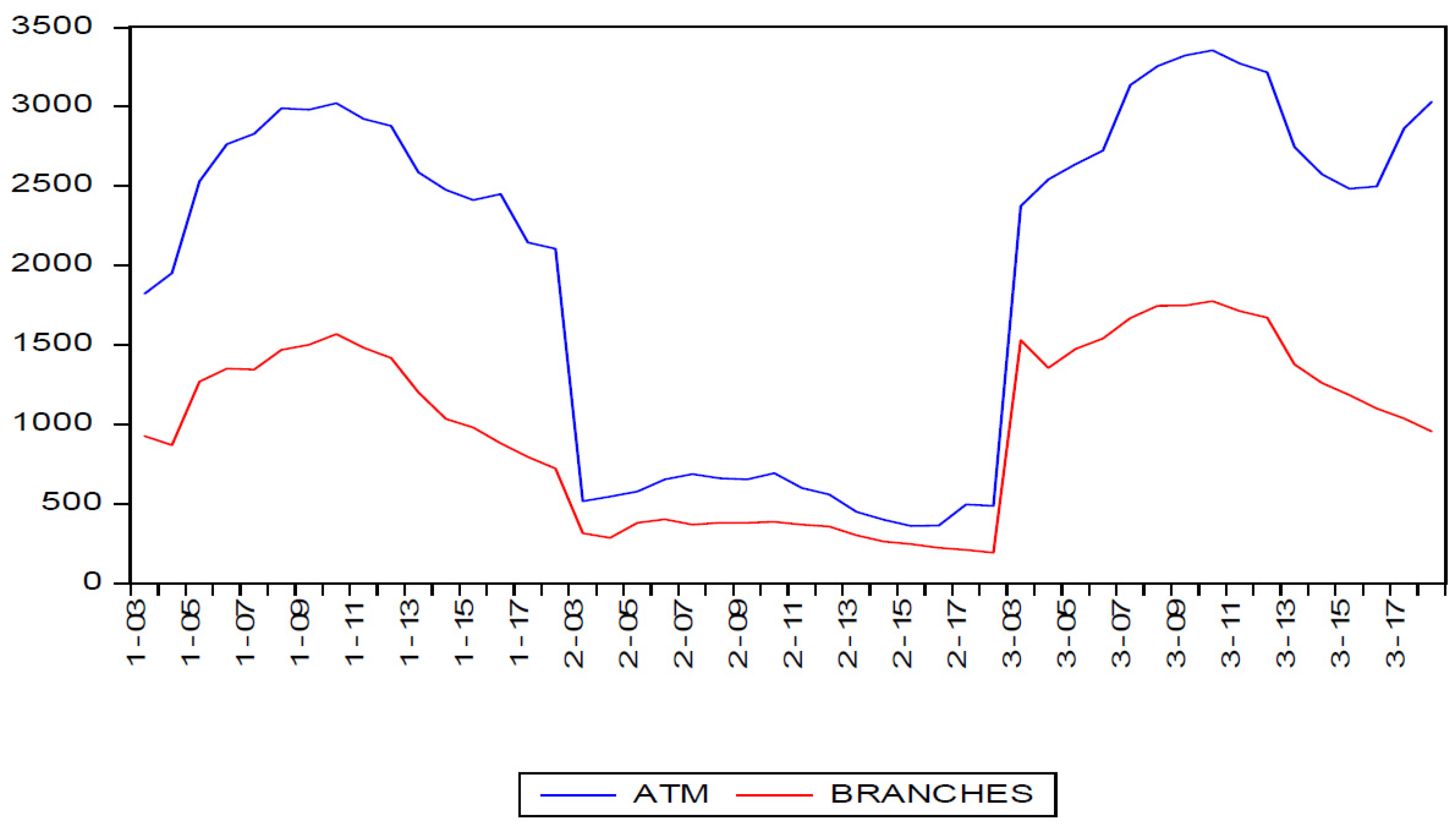

| 3 | Greek banking uncertainty was related to the capital controls imposed in Greece in June 2015 in an attempt to avoid an uncontrolled bank run; see Antonakakis et al. (2019); Samitas and Polyzos (2016). |

| 4 | Williams and Gardener (2003) suggest that segmentation of the European banking system could realize higher growth rates in European regions through information asymmetries. For more information about European regional banking, see Williams and Gardener (2003). |

| 5 | Asmild and Zhu (2016) find that the 2008 financial crisis has affected negatively European banks efficiency levels over the period 2006–2009. Degl’Innocenti et al. (2017a) find that, after 2010, European banks’ efficiency levels have decreased, suggesting a negative effect when the sovereign debt crisis appeared. Spokeviciute et al. (2019) report that crises periods have a disproportionate effect on young banks regardless of their efficiency levels. For a brief review of the relative literature, see Kevork et al. (2017), Degl’Innocenti et al. (2017b). |

| 6 | The Greek banking system includes four systemic banks that operate branches in the whole country. These are: Piraeus Bank (founded in 1916, it is the largest bank in terms of assets), National Bank of Greece (founded in 1841, it is the largest bank in terms of deposits), Eurobank (founded in 1990, it is the second largest bank in Greece), and Alpha Bank (founded in 1879, it is the largest bank in terms of market capitalization). |

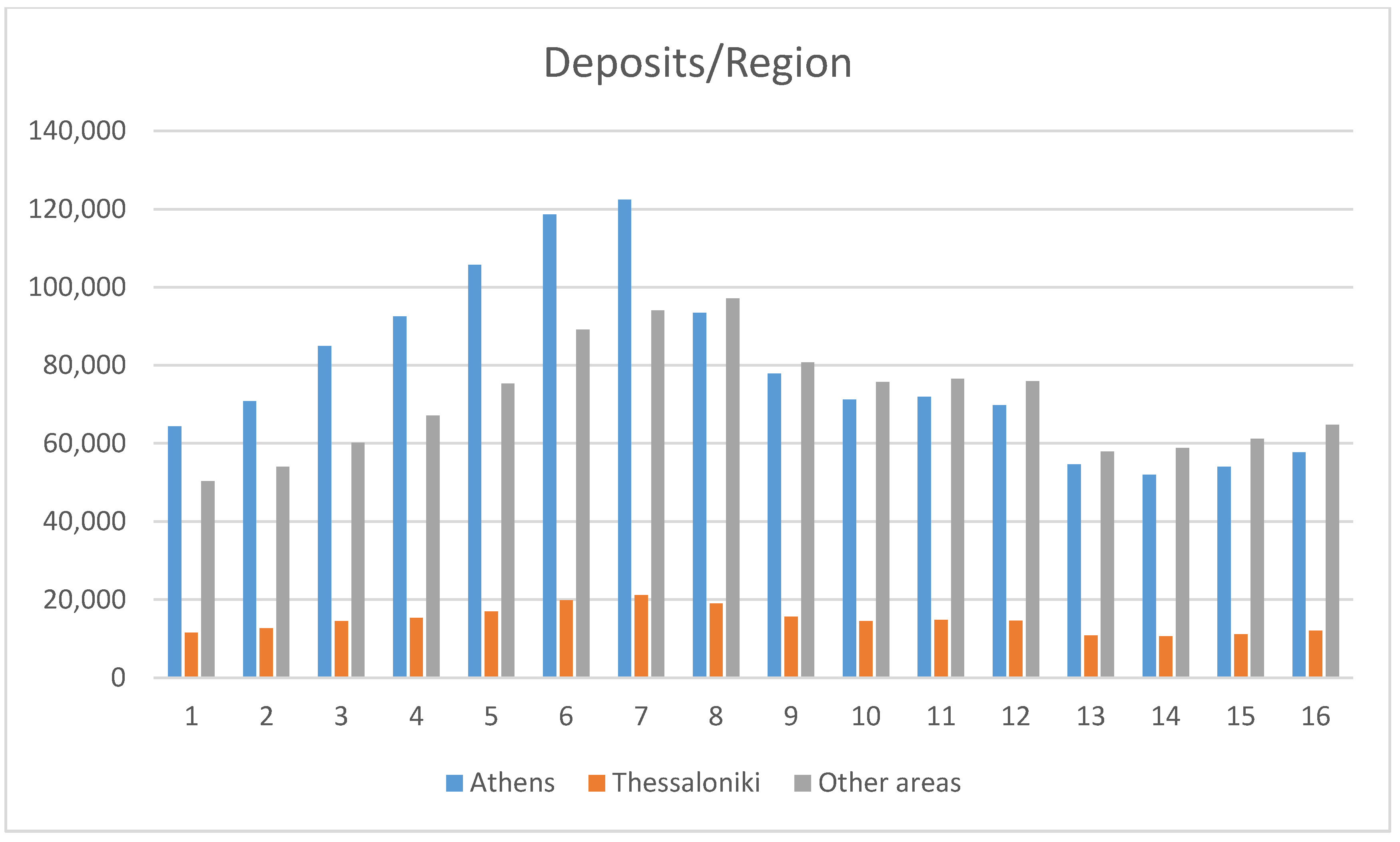

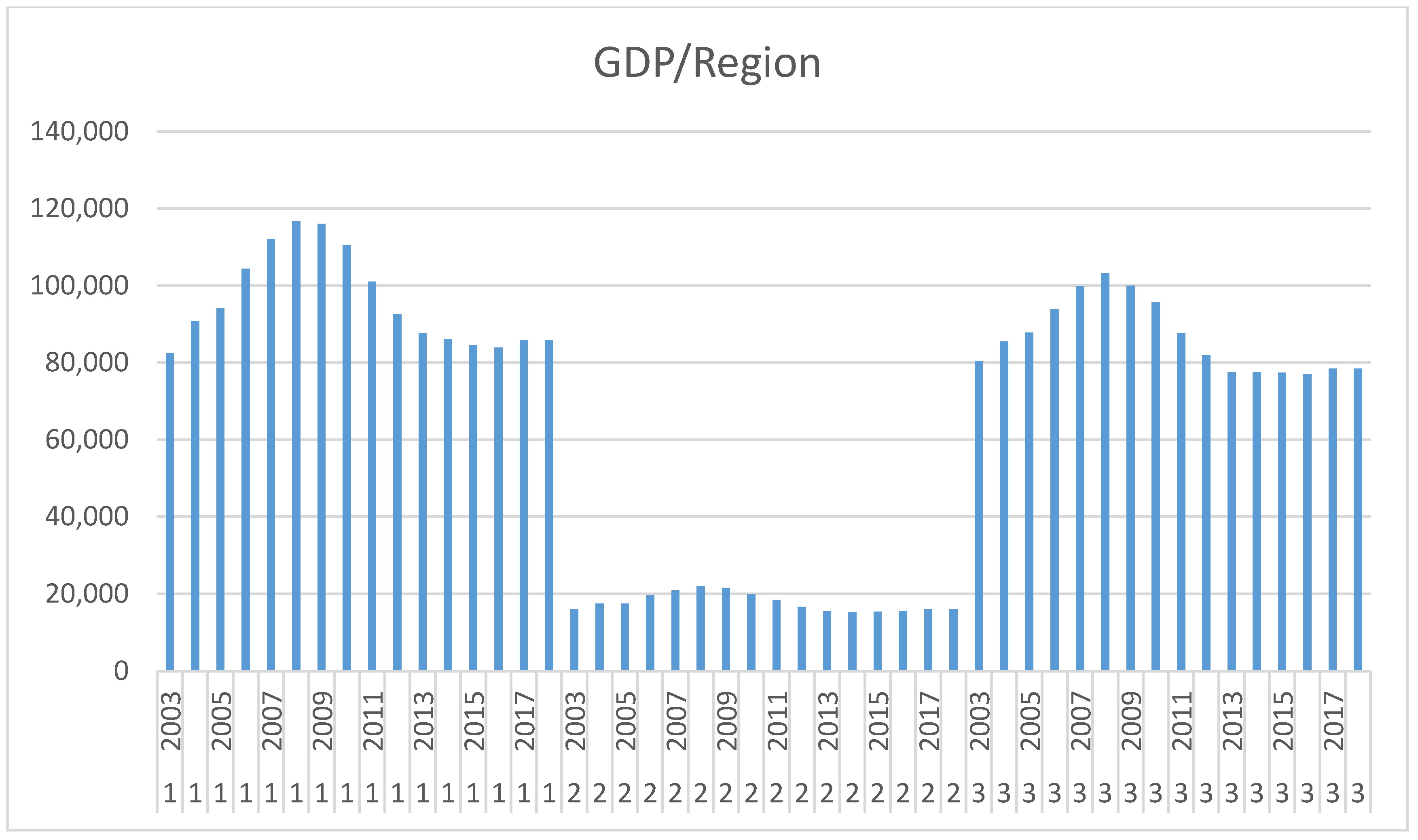

| 7 | Following the official demographics of Greece as of 2011 (with total population of c. 10.8 m), the largest Metropolitan city is Athens which is the capital of Greece, with population of c. 4m. The second-largest Metropolitan city is Thessaloniki with population of c. 1.3 m. Based on the above official statistics of population reported from the Hellenic Statistical Authority and the available data, we consider three large regions for our analysis: Athens, Thessaloniki, Other areas—the rest of Greece. |

| 8 | In the context of CRS formulation, the efficiency score with output orientation is equivalent (and reciprocal) to that in the input orientation, which is an advantage of using CRS formulation (Du et al. 2018, p. 752). |

| 9 | These results are not reported, but available from the author upon request. |

{kind=link}

{kind=link}

{kind=link}

| Dependent Variable: DEPOSITS | ||||

|---|---|---|---|---|

| Method: Panel Least Squares | ||||

| Variable | Coeff. | Std. Error | t-Statistic | Prob. |

| α | 5.332780 | 0.859322 | 6.205798 | 0.0000 * |

| ATM | 0.279117 | 0.161614 | 1.727057 | 0.0913 * |

| BRANCHES | 0.489688 | 0.137343 | 3.565444 | 0.0009 * |

| Dependent Variable: Efficiency | ||||

|---|---|---|---|---|

| Method: Panel Least Squares | ||||

| Variable | Coeff. | Std. Error | t-Statistic | Prob. |

| α | −280.3578 | 115.5239 | −2.426839 | 0.0225 * |

| GDP | 26.44015 | 10.63201 | 2.486844 | 0.0196 * |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Floros, C. Banking Development and Economy in Greece: Evidence from Regional Data. J. Risk Financial Manag. 2020, 13, 243. https://doi.org/10.3390/jrfm13100243

Floros C. Banking Development and Economy in Greece: Evidence from Regional Data. Journal of Risk and Financial Management. 2020; 13(10):243. https://doi.org/10.3390/jrfm13100243

Chicago/Turabian StyleFloros, Christos. 2020. "Banking Development and Economy in Greece: Evidence from Regional Data" Journal of Risk and Financial Management 13, no. 10: 243. https://doi.org/10.3390/jrfm13100243

APA StyleFloros, C. (2020). Banking Development and Economy in Greece: Evidence from Regional Data. Journal of Risk and Financial Management, 13(10), 243. https://doi.org/10.3390/jrfm13100243