Refined Measures of Dynamic Connectedness based on Time-Varying Parameter Vector Autoregressions

Abstract

:1. Introduction

2. Methodology

TVP-VAR

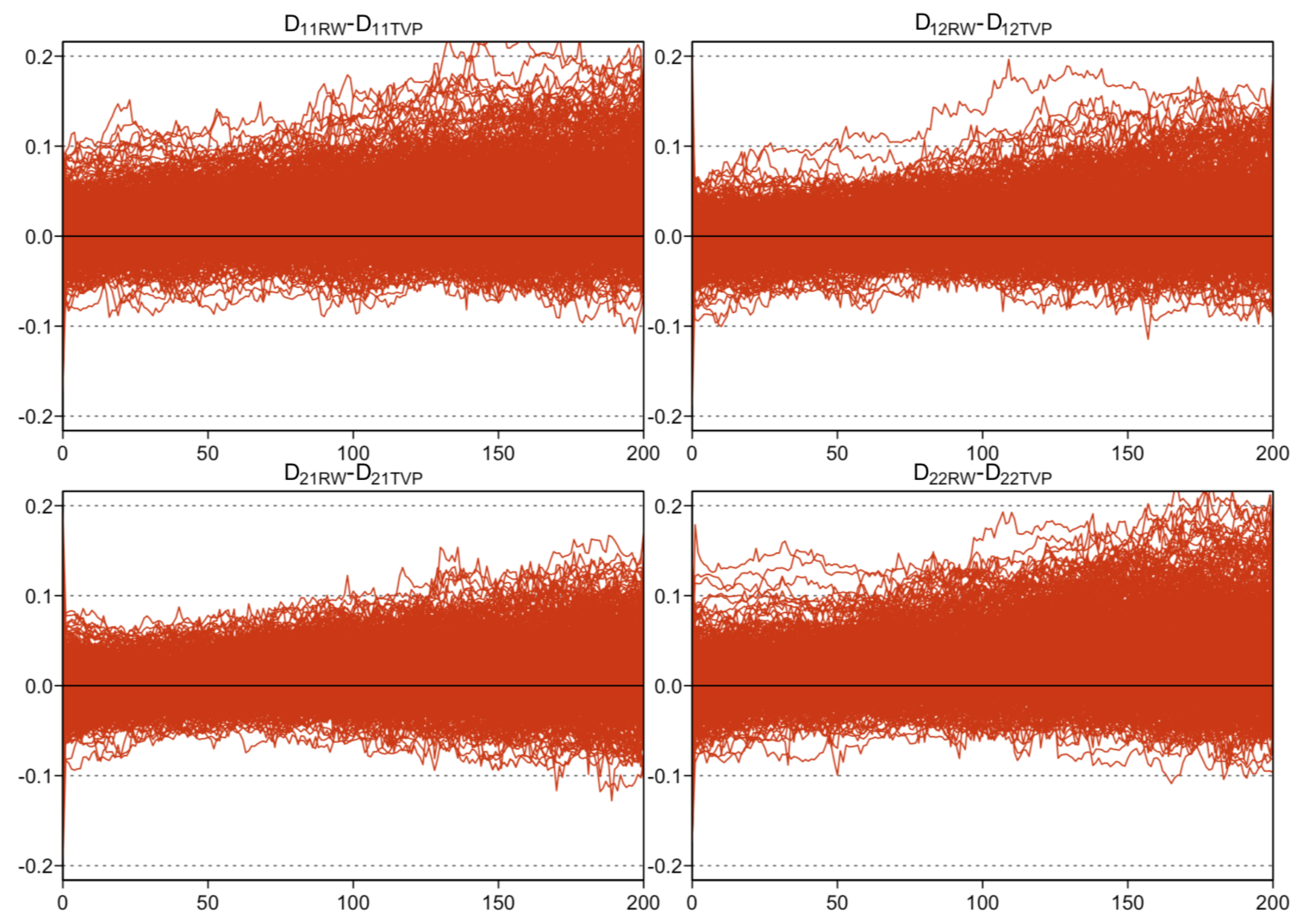

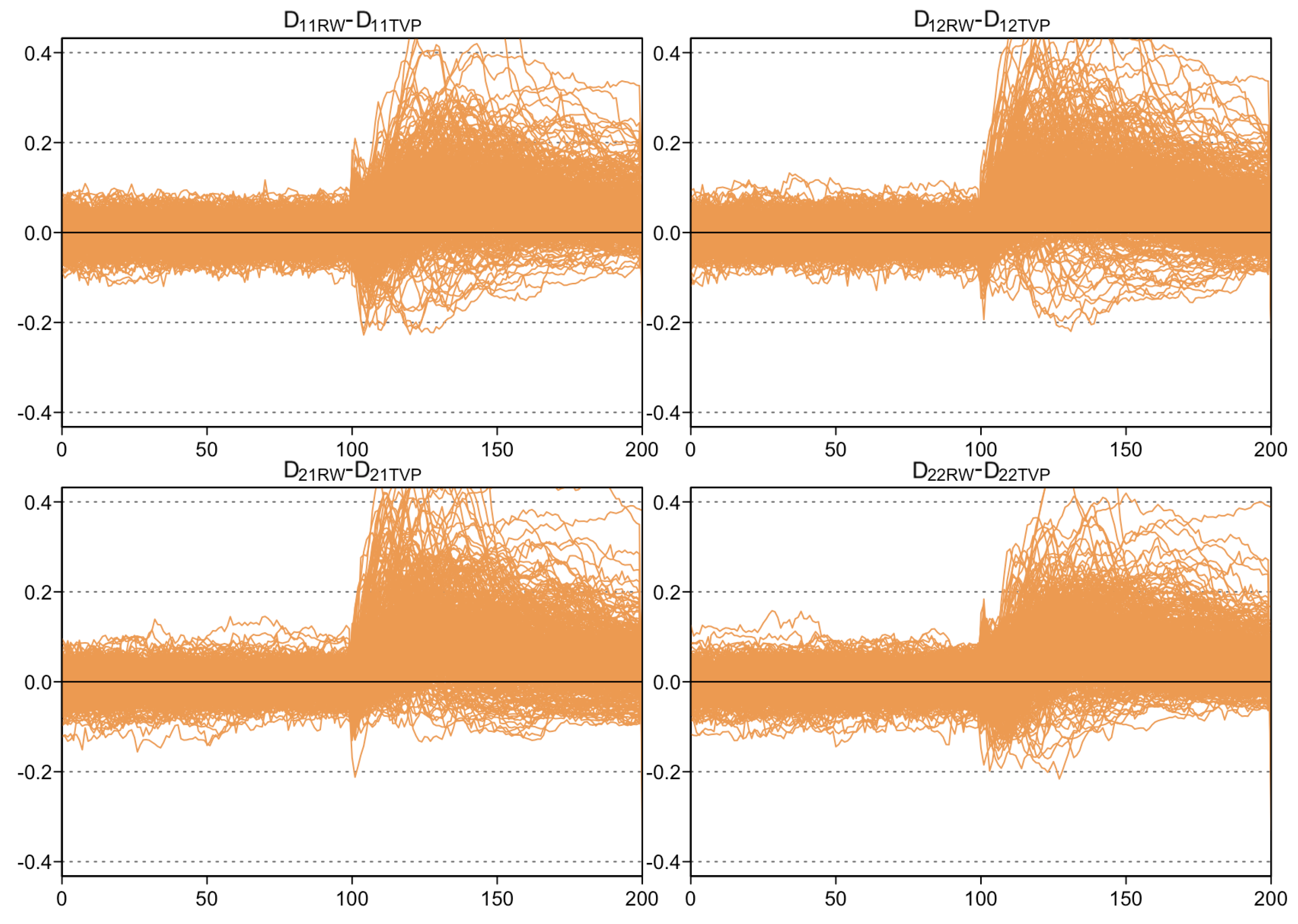

3. Monte Carlo Simulation

4. Data and Summary Statistics

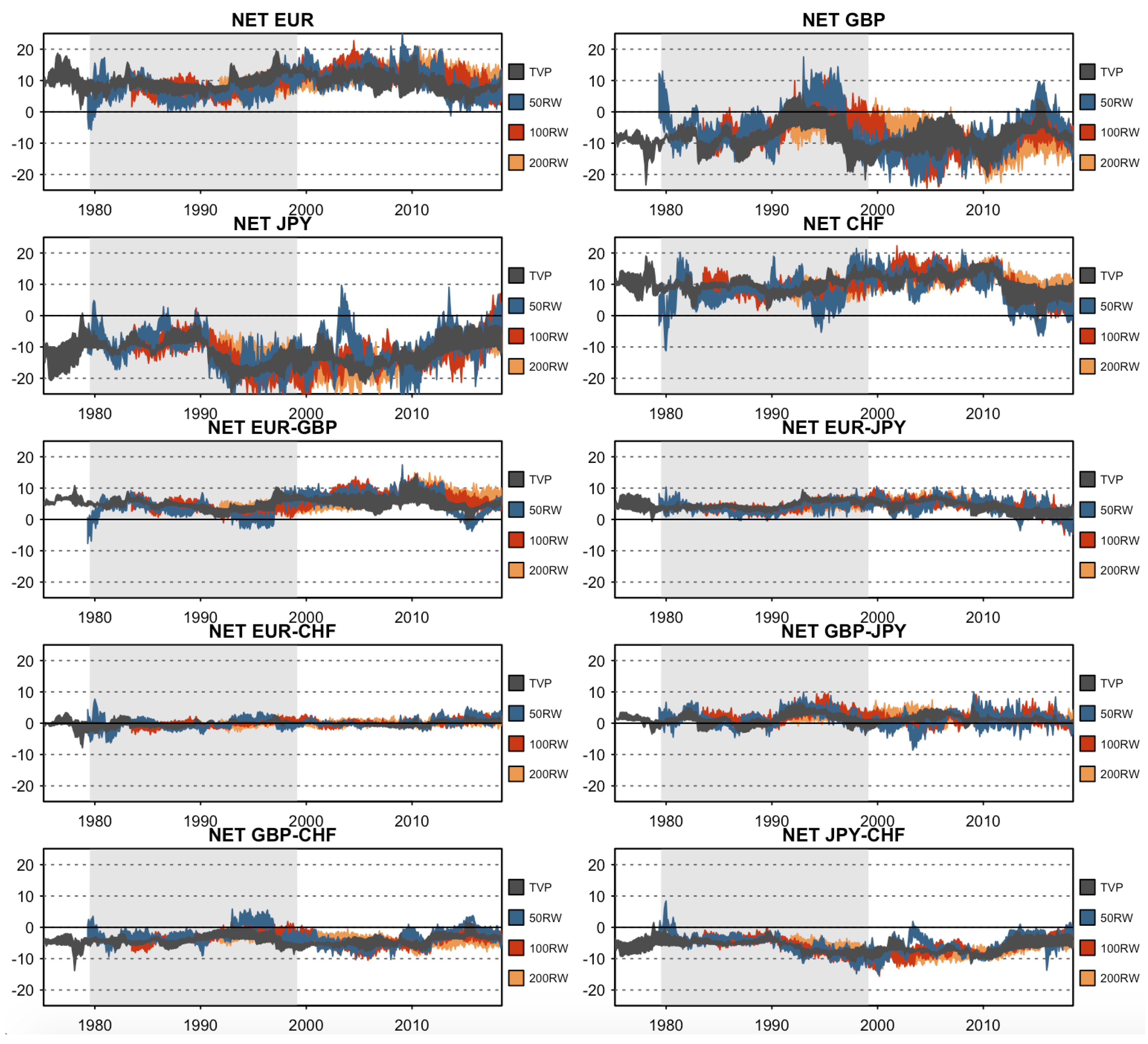

5. Empirical Illustration

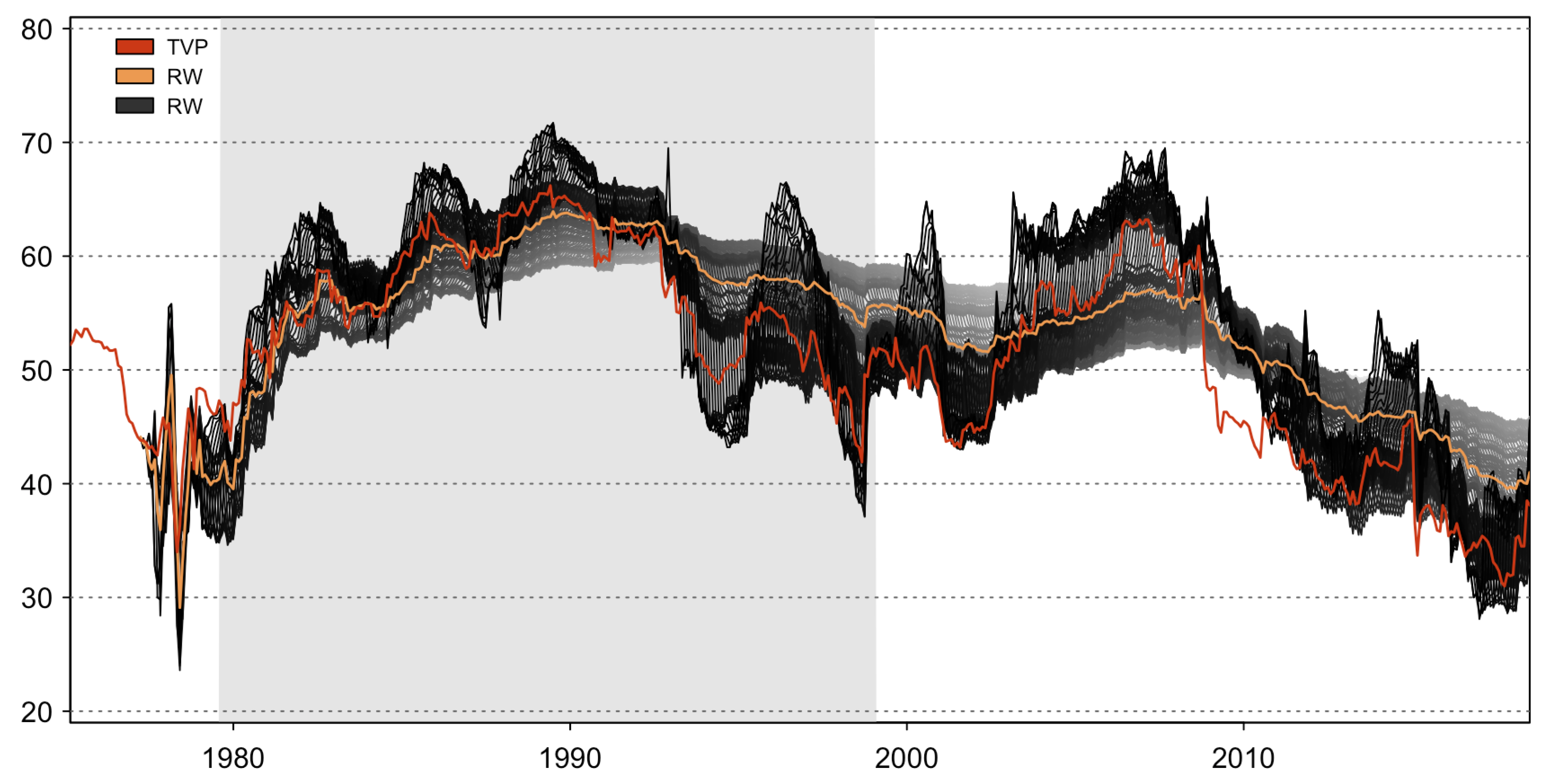

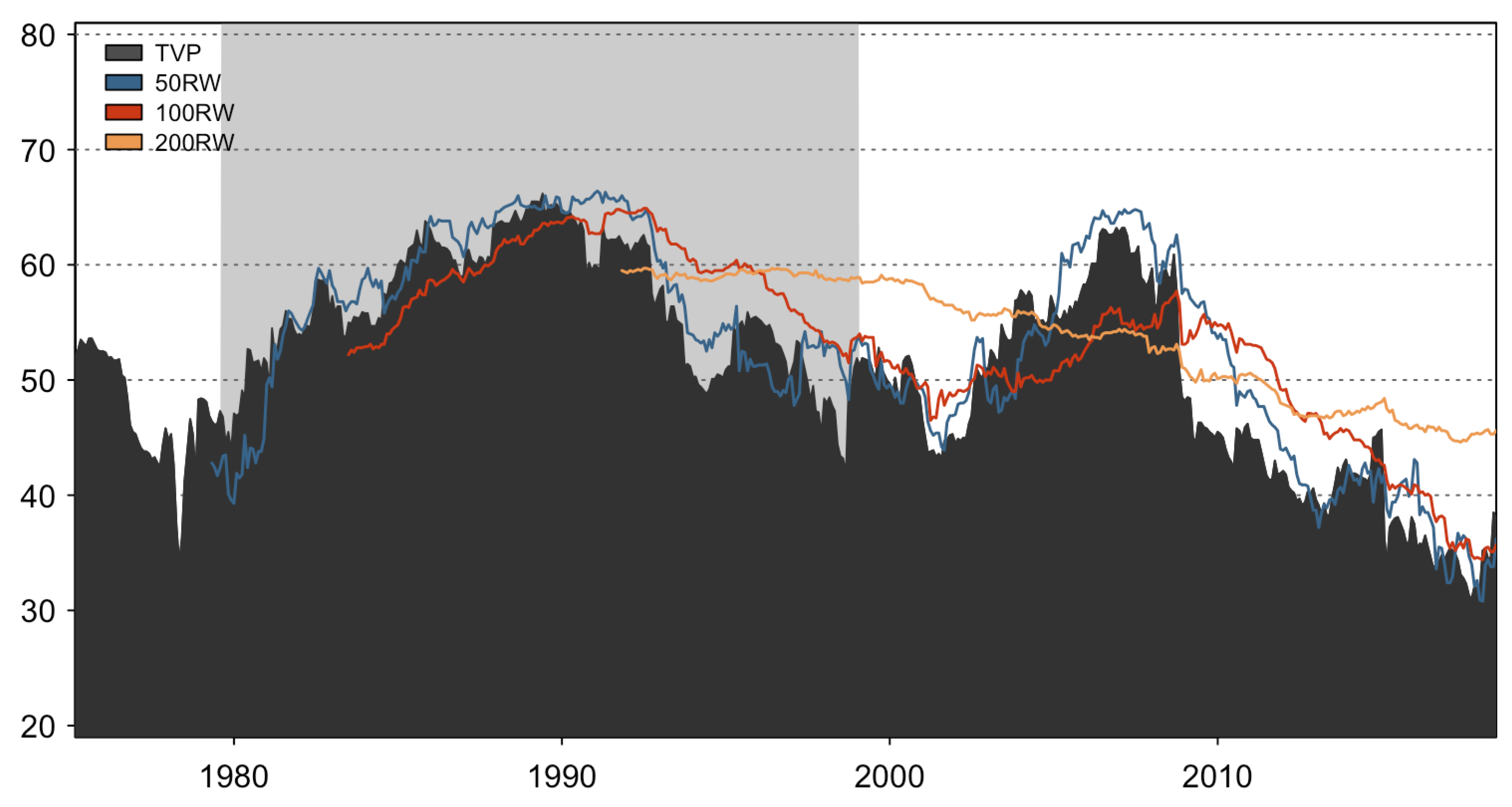

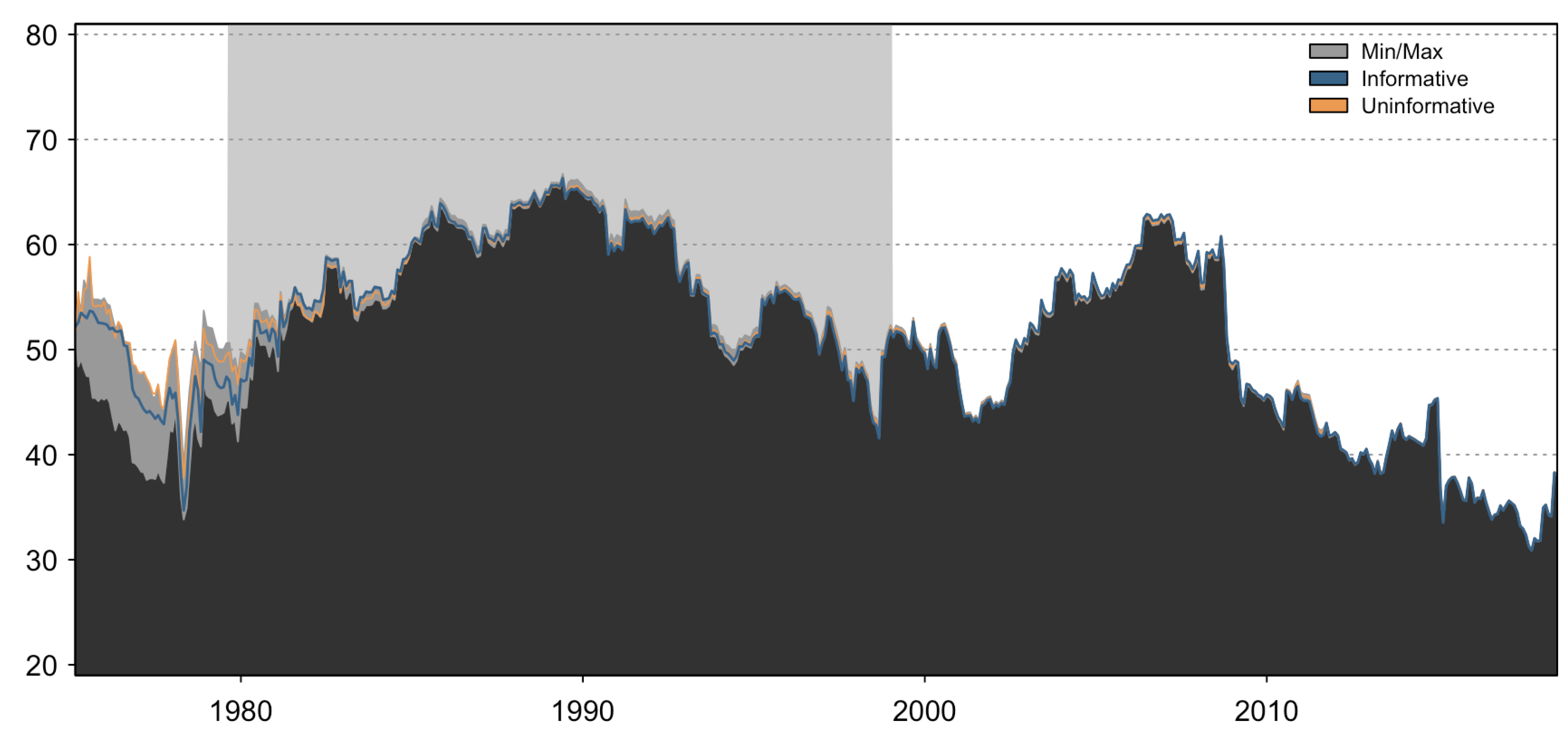

5.1. Dynamic Total Connectedness

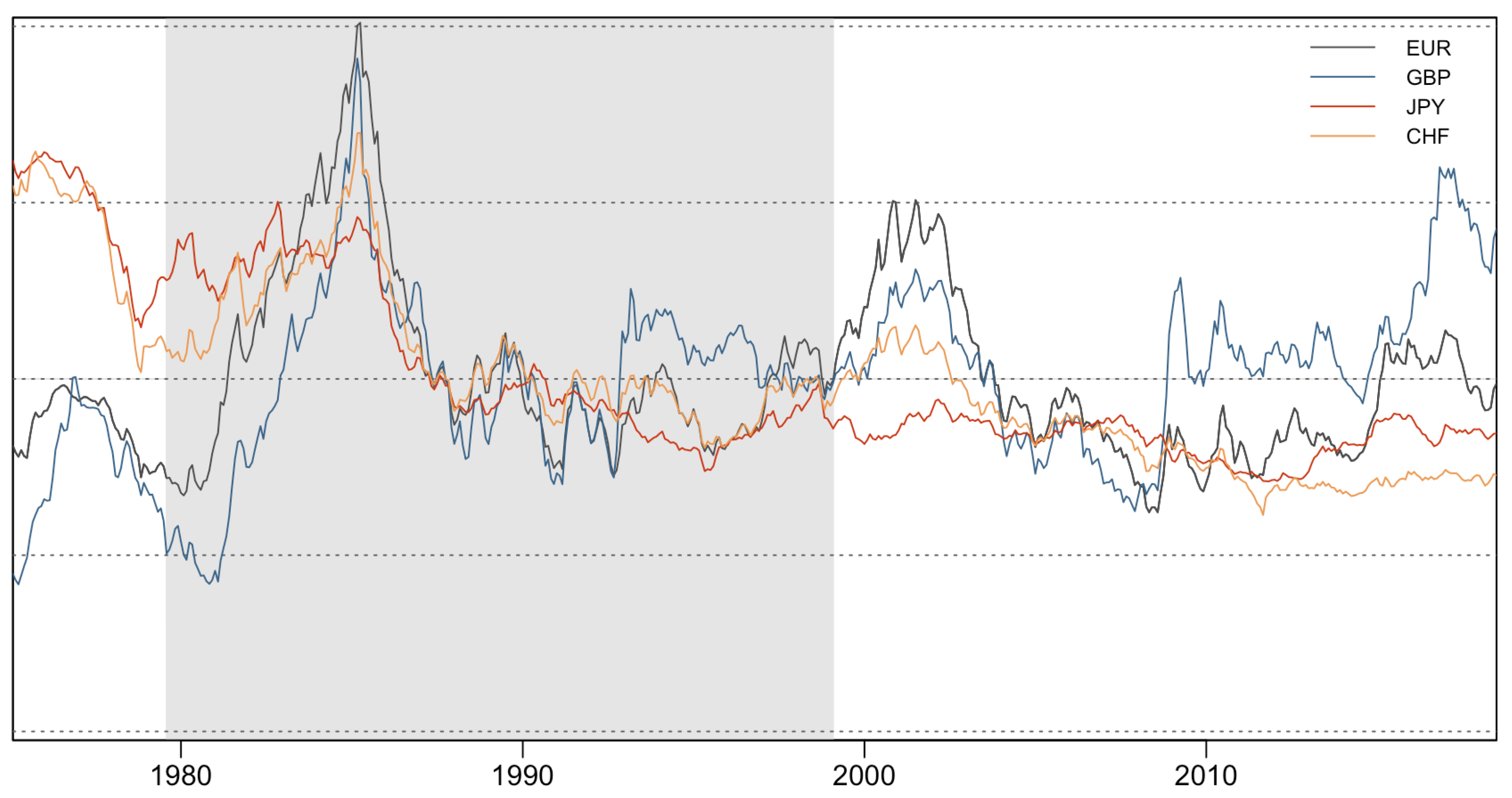

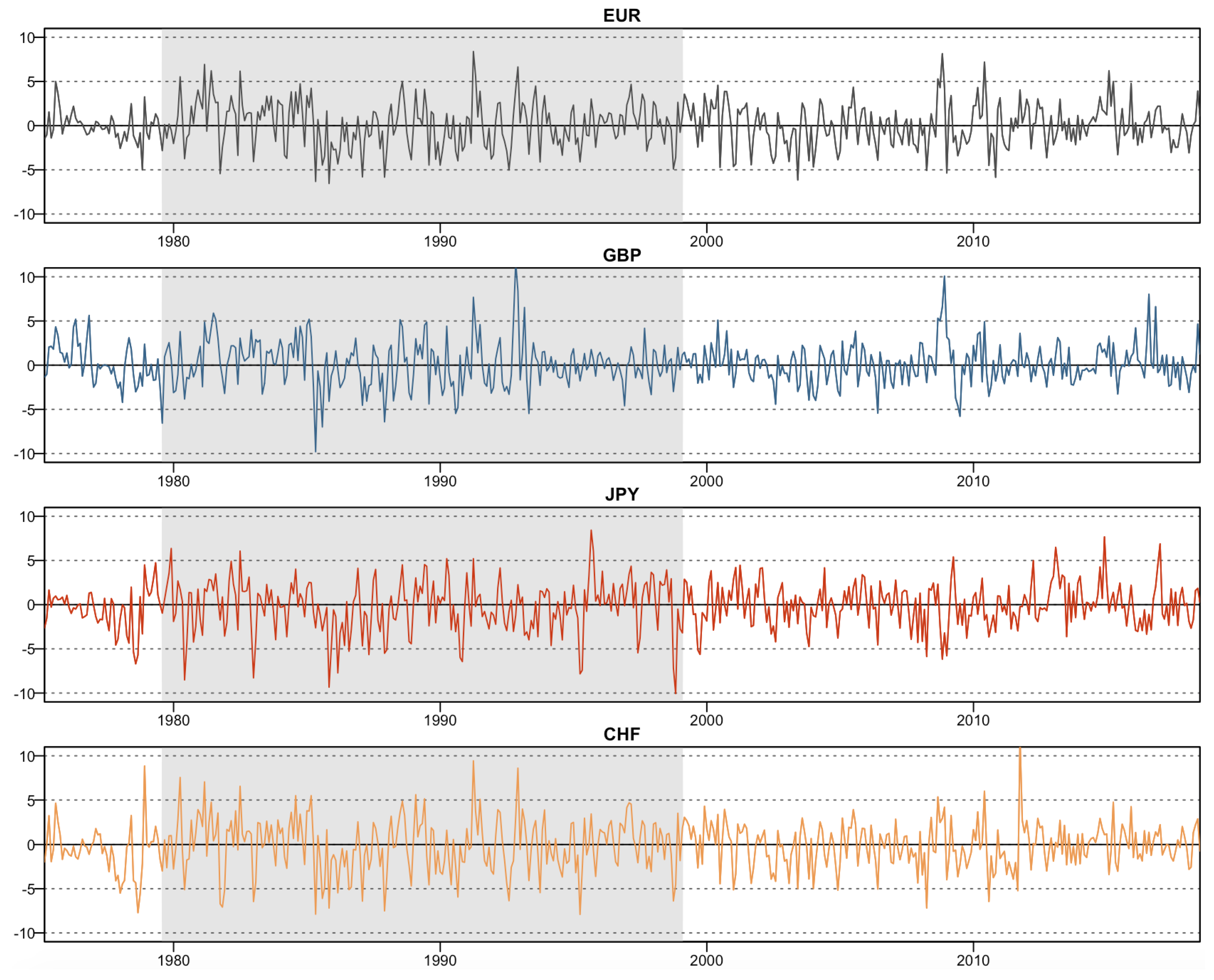

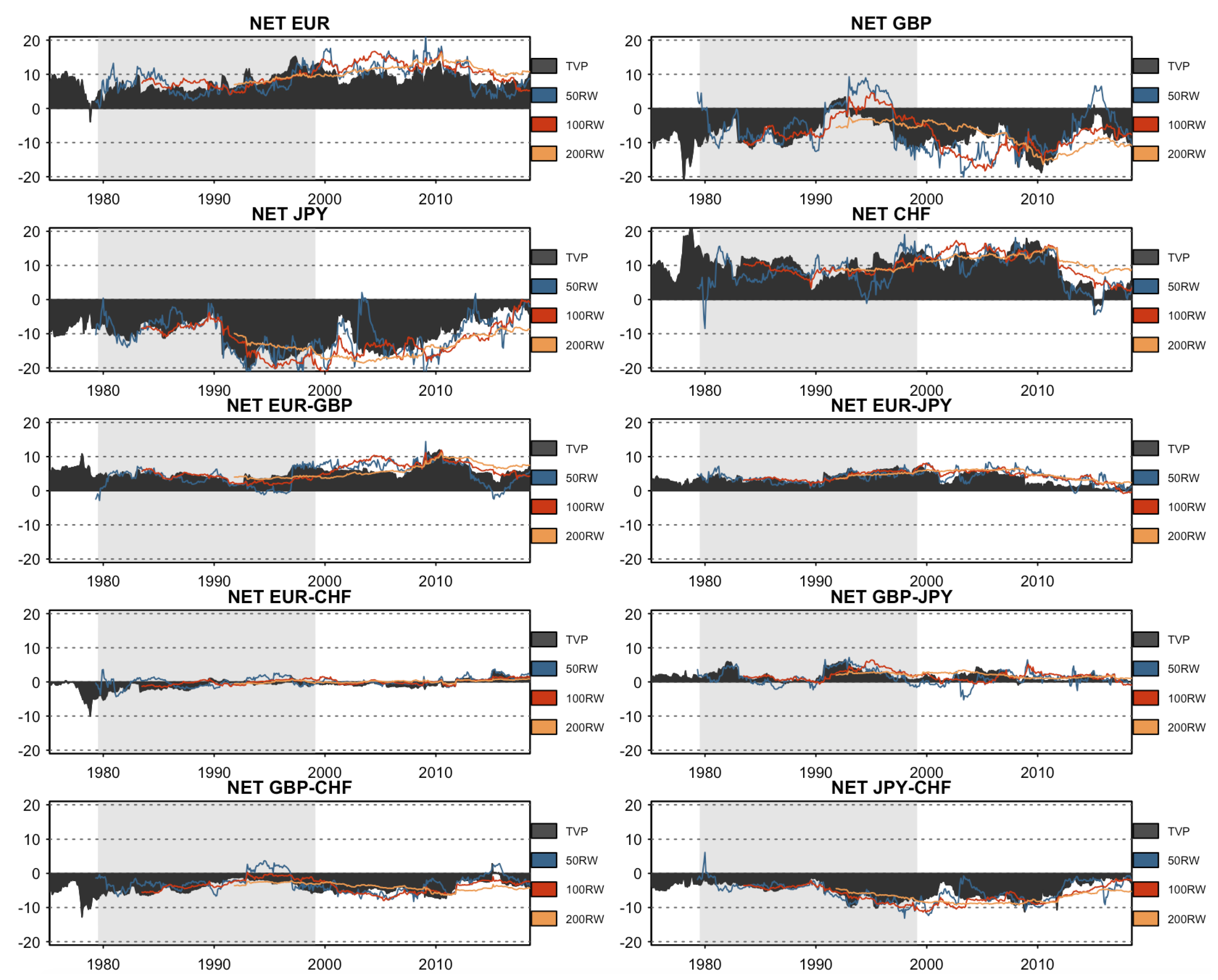

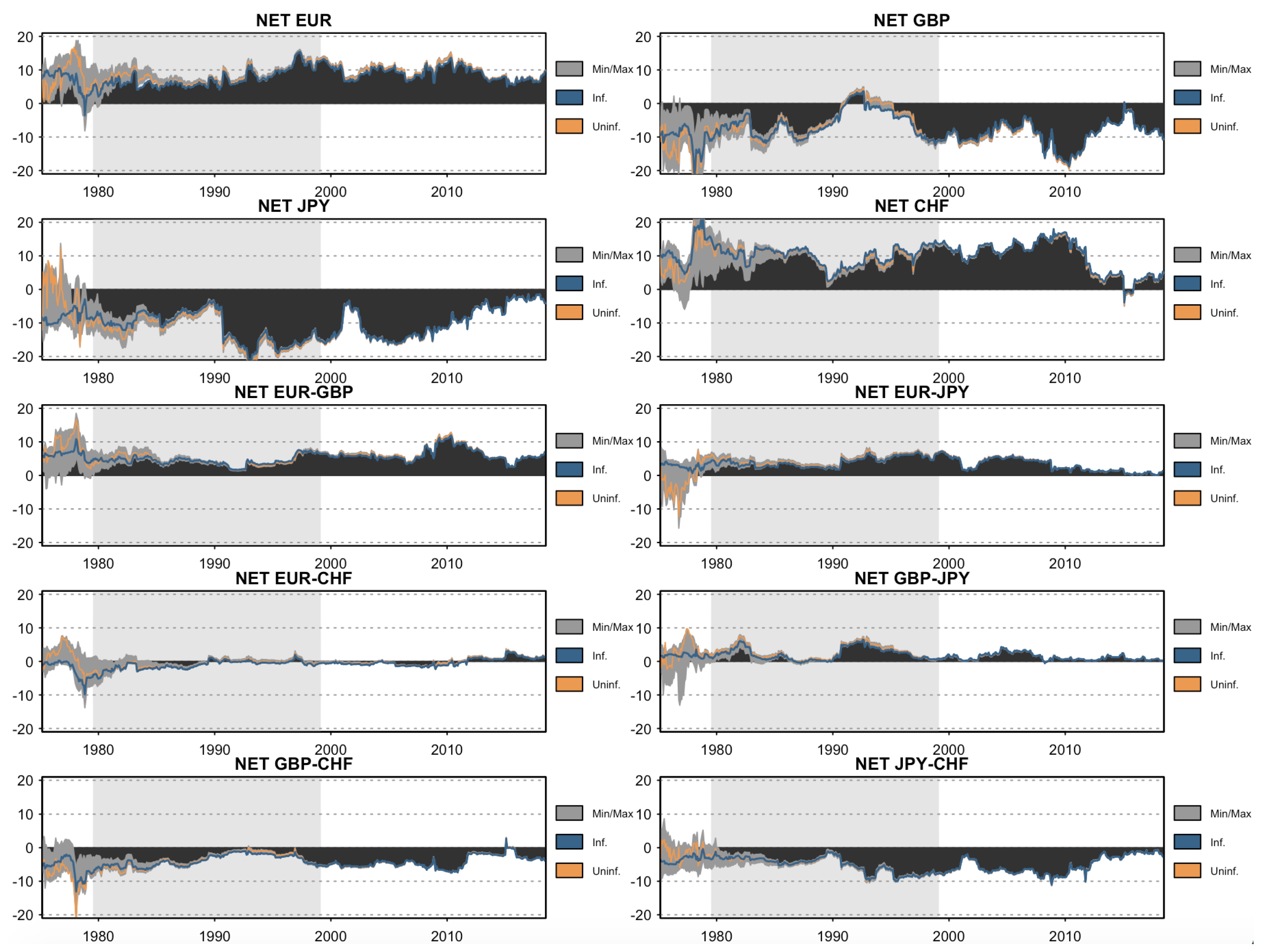

5.2. Net Total and Net Pairwise Directional Connectedness

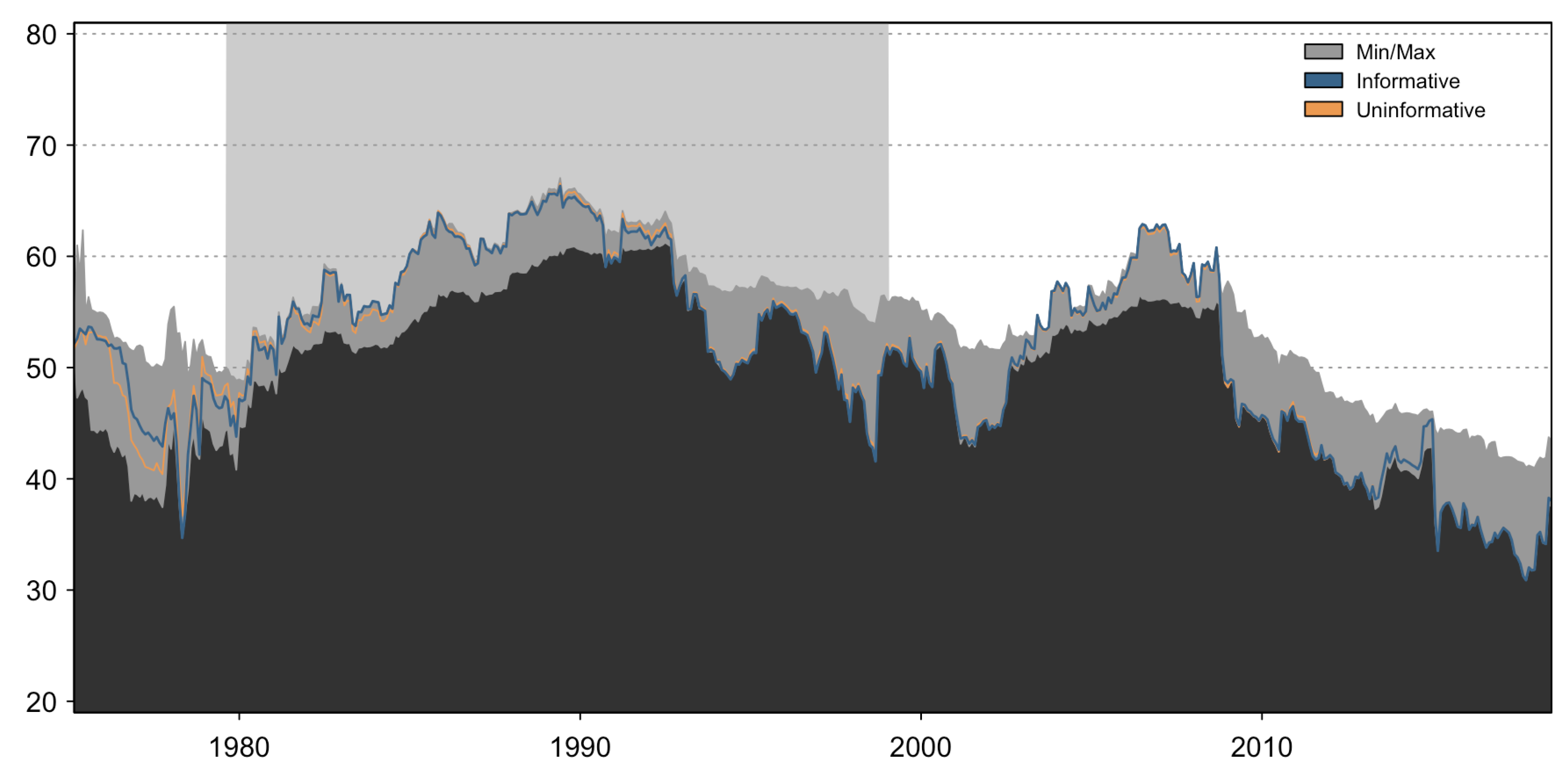

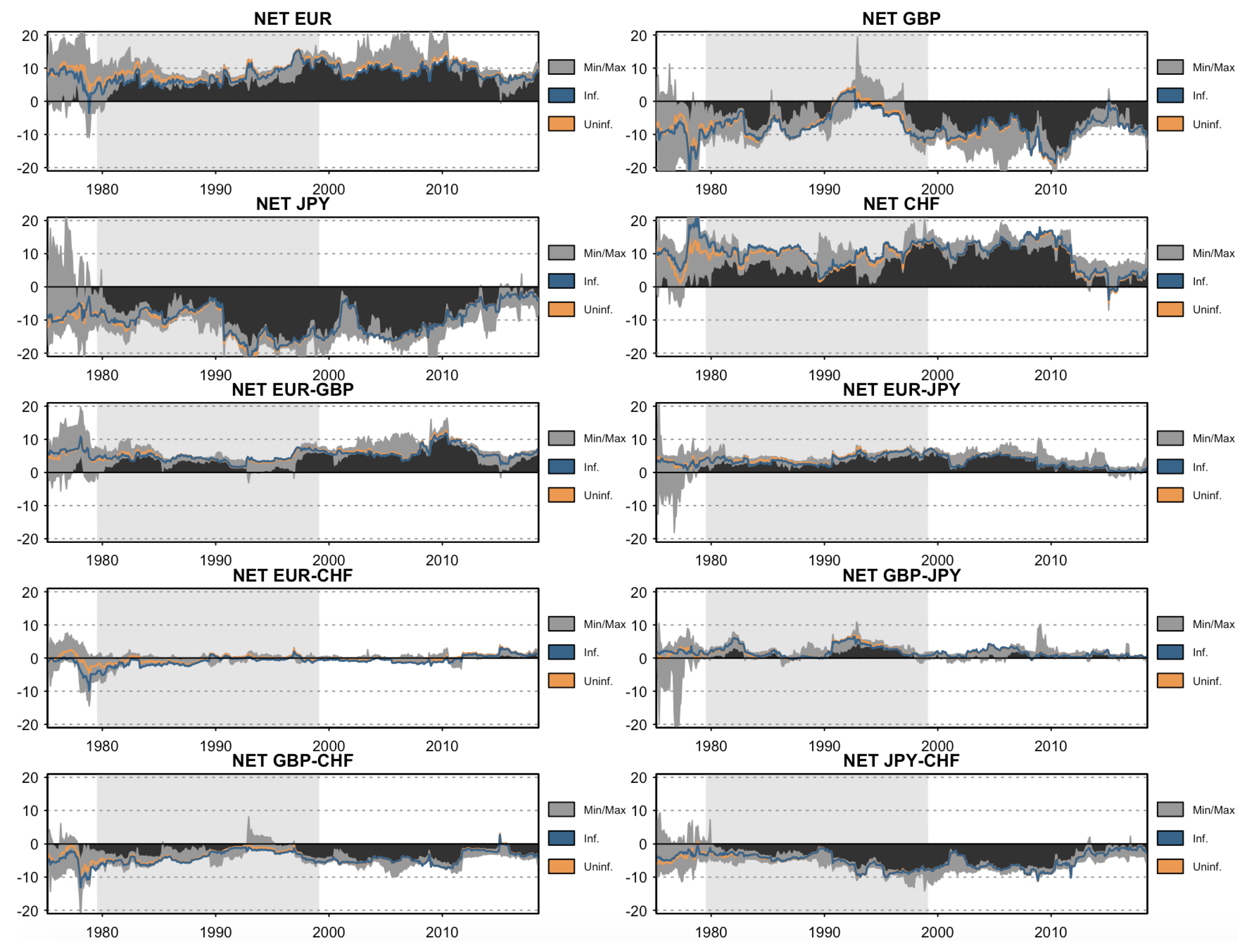

5.3. Sensitivity Analysis

5.3.1. Prior Sensitivity Analysis

5.3.2. Forgetting Factor Sensitivity Analysis

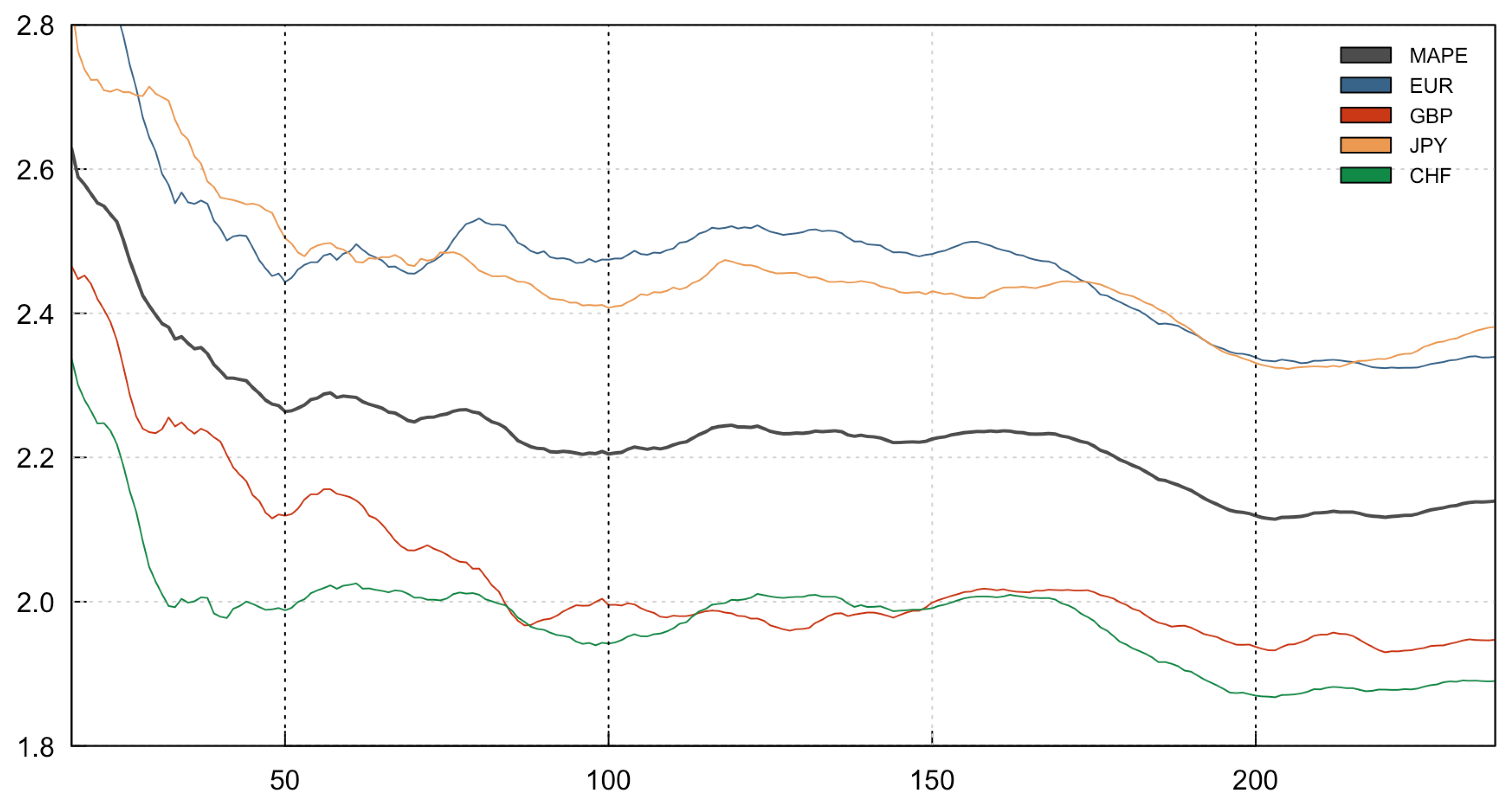

5.4. Forecast Performance

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Alter, Adrian, and Andreas Beyer. 2014. The Dynamics of Spillover Effects during the European Sovereign Debt Turmoil. Journal of Banking and Finance 42: 134–53. [Google Scholar] [CrossRef] [Green Version]

- Anscombe, Francis J., and William J. Glynn. 1983. Distribution of the Kurtosis Statistic B2 for Normal Samples. Biometrika 70: 227–34. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, and David Gabauer. 2017. Refined Measures of Dynamic Connectedness Based On TVP-VAR. Technical Report. Munich: University Library of Munich. [Google Scholar]

- Antonakakis, Nikolaos, Ioannis Chatziantoniou, and David Gabauer. 2019. Cryptocurrency Market Contagion: Market Uncertainty, Market Complexity, and Dynamic Portfolios. Journal of International Financial Markets, Institutions and Money 61: 37–51. [Google Scholar] [CrossRef] [Green Version]

- Antonakakis, Nikolaos, David Gabauer, Rangan Gupta, and Vasilios Plakandaras. 2018. Dynamic Connectedness of Uncertainty across Developed Economies: A Time-Varying Approach. Economics Letters 166: 63–75. [Google Scholar] [CrossRef] [Green Version]

- Antonakakis, Nikolaos, David Gabauer, and Rangan Gupta. 2019a. Greek Economic Policy Uncertainty: Does it Matter for Europe? Evidence from a Dynamic Connectedness Decomposition Approach. Physica A: Statistical Mechanics and Its Applications 535: 122280. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, David Gabauer, and Rangan Gupta. 2019b. International Monetary Policy Spillovers Evidence from A Time-Varying Parameter Vector Autoregression. International Review of Financial Analysis 65: 101382. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos. 2012. Exchange Return Co-movements and Volatility Spillovers before and after the Introduction of Euro. Journal of International Financial Markets, Institutions and Money 22: 1091–109. [Google Scholar] [CrossRef] [Green Version]

- Awartani, Basel, and Aktham Issa Maghyereh. 2013. Dynamic Spillovers Between Oil and Stock Markets in the Gulf Cooperation Council Countries. Energy Economics 36: 28–42. [Google Scholar] [CrossRef]

- Baruník, Jozef, Evžen Kočenda, and Lukáš Vácha. 2016. Asymmetric Connectedness On the U.S. Stock Market: Bad and Good Volatility Spillovers. Journal of Financial Markets 27: 55–78. [Google Scholar] [CrossRef]

- Baruník, Jozef, and Tomáš Křehlík. 2018. Measuring the Frequency Dynamics of Financial Connectedness and Systemic Risk. Journal of Financial Econometrics 16: 271–96. [Google Scholar] [CrossRef]

- Baruník, Jozef, Evžen Kočenda, and Lukáš Vácha. 2017. Asymmetric Volatility Connectedness On the Forex Market. Journal of International Money and Finance 77: 39–56. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, Michael Ehrmann, Marcel Fratzscher, and Arnaud Mehl. 2014. The Global Crisis and Equity Market Contagion. Journal of Finance 69: 2597–649. [Google Scholar] [CrossRef] [Green Version]

- Bubák, Vít, Evzen Kocenda, and Filip Zikes. 2011. Volatility Transmission in Emerging European Foreign Exchange Markets. Journal of Banking and Finance 35: 2829–41. [Google Scholar] [CrossRef] [Green Version]

- Chatziantoniou, Ioannis, and David Gabauer. 2019. EMU-Risk Synchronisation and Financial Fragility Through the Prism of Dynamic Connectedness. Working Papers in Economics and Finance. Portsmouth: University of Portsmouth, Portsmouth Business School, Economics and Finance Subject Group. [Google Scholar]

- Cogley, Timothy, and Thomas J Sargent. 2005. Drifts and Volatilities: Monetary Policies and Outcomes in the Post WWII US. Review of Economic Dynamics 8: 262–302. [Google Scholar] [CrossRef] [Green Version]

- D’Agostino, Ralph B. 1970. Transformation to Normality of the Null Distribution of G1. Biometrika 57: 679–81. [Google Scholar]

- Del Negro, Marco, and Giorgio E Primiceri. 2015. Time Varying Structural Vector Autoregressions and Monetary Policy: A Corrigendum. Review of Economic Studies 82: 1342–45. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yilmaz. 2015. Trans-Atlantic Equity Volatility Connectedness: U.S. and European Financial Institutions, 2004–2014. Journal of Financial Econometrics 14: 81–127. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yılmaz. 2009. Measuring Financial Asset Return and Volatility Spillovers, with Application to Global Equity Markets. Economic Journal 119: 158–71. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yılmaz. 2012. Better to Give Than to Receive: Predictive Directional Measurement of Volatility Spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yılmaz. 2014. On the Network Topology of Variance Decompositions: Measuring the Connectedness of Financial Firms. Journal of Econometrics 182: 119–34. [Google Scholar] [CrossRef] [Green Version]

- Fisher, Thomas J., and Colin M Gallagher. 2012. New weighted portmanteau statistics for time series goodness of fit testing. Journal of the American Statistical Association 107: 777–87. [Google Scholar] [CrossRef]

- Gabauer, David, and Rangan Gupta. 2018. On the Transmission Mechanism of Country-Specific and International Economic Uncertainty Spillovers: Evidence From A TVP-VAR Connectedness Decomposition Approach. Economics Letters 171: 63–71. [Google Scholar] [CrossRef] [Green Version]

- Geraci, Marco Valerio, and Jean-Yves Gnabo. 2018. Measuring Interconnectedness Between Financial Institutions with Bayesian Time-Varying Vector Autoregressions. Journal of Financial and Quantitative Analysis 53: 1–20. [Google Scholar] [CrossRef] [Green Version]

- Jarque, Carlos M., and Anil K. Bera. 1980. Efficient Tests for Normality, Homoscedasticity and Serial Independence of Regression Residuals. Economics Letters 6: 255–59. [Google Scholar] [CrossRef]

- Kilian, Lutz. 1998. Small-Sample Confidence Intervals for Impulse Response Functions. Review of Economics and Statistics 80: 218–30. [Google Scholar] [CrossRef]

- Kilian, Lutz. 1999. Finite-Sample Properties of Percentile and Percentile-t Bootstrap Confidence Intervals for Impulse Responses. Review of Economics and Statistics 81: 652–60. [Google Scholar] [CrossRef]

- Koop, Gary, and Dimitris Korobilis. 2013. Large Time-Varying Parameter VARs. Journal of Econometrics 177: 185–98. [Google Scholar] [CrossRef] [Green Version]

- Koop, Gary, and Dimitris Korobilis. 2014. A New Index of Financial Conditions. European Economic Review 71: 101–116. [Google Scholar] [CrossRef] [Green Version]

- Koop, Gary, M. Hashem Pesaran, and Simon M. Potter. 1996. Impulse Response Analysis in Nonlinear Multivariate Models. Journal of Econometrics 74: 119–47. [Google Scholar] [CrossRef]

- Korobilis, Dimitris, and Kamil Yilmaz. 2018. SSRN Electronic Journal. [CrossRef] [Green Version]

- Lütkepohl, Helmut, Anna Staszewska-Bystrova, and Peter Winker. 2015. Comparison of Methods for Constructing Joint Confidence Bands for Impulse Response Functions. International Journal of Forecasting 31: 782–98. [Google Scholar] [CrossRef] [Green Version]

- McMillan, David G., and Alan E. H. Speight. 2010. Return and Volatility Spillovers in Three Euro Exchange Rates. Journal of Economics and Business 62: 79–93. [Google Scholar] [CrossRef]

- Pesaran, H. Hashem, and Yongcheol Shin. 1998. Generalized Impulse Response Analysis in Linear Multivariate Models. Economics Letters 58: 17–29. [Google Scholar] [CrossRef]

- Petrova, Katerina. 2019. A Quasi-Bayesian Local Likelihood Approach to Time Varying Parameter VAR Models. Journal of Econometrics 212: 286–306. [Google Scholar] [CrossRef]

- Primiceri, Giorgio E. 2005. Time Varying Structural Vector Autoregressions and Monetary Policy. Review of Economic Studies 72: 821–52. [Google Scholar] [CrossRef]

- Reinhart, Carmen M., and Kenneth S. Rogoff. 2008. Is the 2007 US Sub-Prime Financial Crisis so Different? An International Historical Comparison. American Economic Review 98: 339–44. [Google Scholar] [CrossRef] [Green Version]

- Stock, James H., Graham Elliott, and Thomas J. Rothenberg. 1996. Efficient Tests for an Autoregressive Unit Root. Econometrica 64: 813–36. [Google Scholar]

| 1. | Although there is in fact a wealth of literature regarding TVP-VAR models (see, inter alia, Primiceri 2005; Cogley and Sargent 2005; Koop and Korobilis 2013, 2014; Del Negro and Primiceri 2015; Petrova 2019) we do not focus on the TVP-VAR framework specifically, but we are rather concerned with utilising the TVP-VAR framework in order to improve the accuracy of the dynamic connectedness measures. |

| 2. | Both the code for Monte Carlo simulation and the results of different rolling-windows are available upon request. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Outlier | 0.025 *** | 0.016 *** | 0.012 *** | 0.027 *** |

| (0.0003) | (0.0002) | (0.0002) | (0.0003) | |

| Structural Break | 0.033 *** | 0.040 *** | 0.032 *** | 0.028 *** |

| in Parameters | (0.0005) | (0.001) | (0.0005) | (0.0004) |

| EUR | GBP | JPY | CHF | |

|---|---|---|---|---|

| Mean | 0.056 | 0.14 | −0.156 | −0.141 |

| Variance | 5.996 | 5.988 | 7.121 | 7.785 |

| Skewness | 0.124 | 0.411 *** | −0.320 *** | 0.057 |

| (0.244) | (0.000) | (0.003) | (0.591) | |

| 0.270 | 1.932 *** | 0.794 *** | 0.913 *** | |

| (0.196) | (0.000) | (0.003) | (0.001) | |

| 2.913 | 95.694 *** | 22.557 *** | 18.375 *** | |

| (0.233) | (0.000) | (0.000) | (0.000) | |

| −6.171 *** | −6.605 *** | −5.372 *** | −6.446 *** | |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| 57.561 *** | 64.935 *** | 79.655 *** | 42.297 *** | |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| 18.874 ** | 59.908 *** | 30.270 *** | 12.111 | |

| (0.028) | (0.000) | (0.000) | (0.300) | |

| Unconditional Correlation | ||||

| EUR | ||||

| GBP | ||||

| JPY | ||||

| CHF | ||||

| TVP-VAR | |||||

|---|---|---|---|---|---|

| TO (i) | EUR | GBP | JPY | CHF | FROM (i) |

| EUR | 40.1 | 18.2 | 10.9 | 30.8 | 59.9 |

| GBP | 23.8 | 48.3 | 7.4 | 20.5 | 51.7 |

| JPY | 15.1 | 9.0 | 57.5 | 18.3 | 42.5 |

| CHF | 30.7 | 16.3 | 12.5 | 40.5 | 59.5 |

| Contribution TO others | 69.5 | 43.6 | 30.9 | 69.6 | 213.6 |

| NET directional connectedness | 9.6 | -8.1 | −11.6 | 10.1 | TCI |

| NPSO transmitter | 2 | 1 | 0 | 3 | 53.4 |

| 50-Month Rolling-Window VAR | |||||

| EUR | 40.0 | 19.8 | 9.9 | 30.2 | 60.0 |

| GBP | 24.6 | 47.4 | 7.6 | 20.5 | 52.6 |

| JPY | 13.9 | 8.9 | 60.0 | 17.3 | 40.0 |

| CHF | 30.3 | 17.5 | 11.8 | 40.4 | 59.6 |

| Contribution TO others | 68.7 | 46.2 | 29.3 | 68.0 | TCI |

| NET directional connectedness | 8.8 | -6.4 | −10.7 | 8.4 | 53.0 |

| NPDC transmitter | 3 | 1 | 0 | 2 | |

| 100-month Rolling-Window VAR | |||||

| EUR | 39.8 | 20.0 | 9.1 | 31.2 | 60.2 |

| GBP | 25.7 | 46.4 | 6.5 | 21.4 | 53.6 |

| JPY | 13.3 | 8.2 | 60.6 | 17.8 | 39.4 |

| CHF | 31.2 | 17.8 | 11.3 | 39.7 | 60.3 |

| Contribution TO others | 70.2 | 46.0 | 26.9 | 70.4 | TCI |

| NET directional connectedness | 10.0 | -7.6 | −12.5 | 10.1 | 53.4 |

| NPDC transmitter | 3 | 1 | 0 | 2 | |

| 200-Month Rolling-Window VAR | |||||

| EUR | 39.3 | 20.3 | 8.6 | 31.8 | 60.7 |

| GBP | 26.2 | 46.1 | 5.7 | 21.9 | 53.9 |

| JPY | 13.4 | 7.7 | 60.9 | 18.1 | 39.1 |

| CHF | 31.9 | 18.1 | 10.9 | 39.1 | 60.9 |

| Contribution TO others | 71.5 | 46.1 | 25.3 | 71.8 | TCI |

| NET directional connectedness | 10.8 | -7.8 | −13.9 | 10.9 | 53.7 |

| NPDC transmitter | 3 | 1 | 0 | 2 | |

| EUR | GBP | JPY | CHF | EUR | GBP | JPY | CHF | |||

|---|---|---|---|---|---|---|---|---|---|---|

| 1-Step Ahead Forecast | 2-Step Ahead Forecast | |||||||||

| 0.99,0.99 | ||||||||||

| 0.99,0.98 | ||||||||||

| 0.99,0.97 | ||||||||||

| 0.99,0.96 | ||||||||||

| 0.98,0.99 | ||||||||||

| 0.98,0.98 | ||||||||||

| 0.98,0.97 | ||||||||||

| 0.98,0.96 | ||||||||||

| 0.97,0.99 | ||||||||||

| 0.97,0.98 | ||||||||||

| 0.97,0.97 | ||||||||||

| 0.97,0.96 | ||||||||||

| 0.96,0.99 | ||||||||||

| 0.96,0.98 | ||||||||||

| 0.96,0.97 | ||||||||||

| 0.96,0.96 | ||||||||||

| RW 50 | ||||||||||

| RW 100 | ||||||||||

| RW 200 | ||||||||||

| 3-Step Ahead Forecast | 6-Step Ahead Forecast | |||||||||

| 0.99,0.99 | ||||||||||

| 0.99,0.98 | ||||||||||

| 0.99,0.97 | ||||||||||

| 0.99,0.96 | ||||||||||

| 0.98,0.99 | ||||||||||

| 0.98,0.98 | ||||||||||

| 0.98,0.97 | ||||||||||

| 0.98,0.96 | ||||||||||

| EUR | GBP | JPY | CHF | EUR | GBP | JPY | CHF | |||

|---|---|---|---|---|---|---|---|---|---|---|

| 9-Step Ahead Forecast | 12-Step Ahead Forecast | |||||||||

| 0.99,0.99 | ||||||||||

| 0.99,0.98 | ||||||||||

| 0.99,0.97 | ||||||||||

| 0.99,0.96 | ||||||||||

| 0.98,0.99 | ||||||||||

| 0.98,0.98 | ||||||||||

| 0.98,0.97 | ||||||||||

| 0.98,0.96 | ||||||||||

| 0.97,0.99 | ||||||||||

| 0.97,0.98 | ||||||||||

| 0.97,0.97 | ||||||||||

| 0.97,0.96 | ||||||||||

| 0.96,0.99 | ||||||||||

| 0.96,0.98 | ||||||||||

| 0.96,0.97 | ||||||||||

| 0.96,0.96 | ||||||||||

| RW 50 | ||||||||||

| RW 100 | ||||||||||

| RW 200 | ||||||||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Antonakakis, N.; Chatziantoniou, I.; Gabauer, D. Refined Measures of Dynamic Connectedness based on Time-Varying Parameter Vector Autoregressions. J. Risk Financial Manag. 2020, 13, 84. https://doi.org/10.3390/jrfm13040084

Antonakakis N, Chatziantoniou I, Gabauer D. Refined Measures of Dynamic Connectedness based on Time-Varying Parameter Vector Autoregressions. Journal of Risk and Financial Management. 2020; 13(4):84. https://doi.org/10.3390/jrfm13040084

Chicago/Turabian StyleAntonakakis, Nikolaos, Ioannis Chatziantoniou, and David Gabauer. 2020. "Refined Measures of Dynamic Connectedness based on Time-Varying Parameter Vector Autoregressions" Journal of Risk and Financial Management 13, no. 4: 84. https://doi.org/10.3390/jrfm13040084

APA StyleAntonakakis, N., Chatziantoniou, I., & Gabauer, D. (2020). Refined Measures of Dynamic Connectedness based on Time-Varying Parameter Vector Autoregressions. Journal of Risk and Financial Management, 13(4), 84. https://doi.org/10.3390/jrfm13040084