True versus Spurious Long Memory in Cryptocurrencies

Abstract

:1. Introduction

2. Background Literature

3. Long Memory Explained

4. Tests of Long Memory

5. Results

5.1. Data

5.2. Findings

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Beran, Jan. 1994. Statistics for Long-Memory Processes. Boca Raton: CRC Press, vol. 61. [Google Scholar]

- Betken, Annika. 2016. Testing for Change-Points in Long-Range Dependent Time Series by Means of a Self-Normalized Wilcoxon Test. Journal of Time Series Analysis 37: 785–809. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Rangan Gupta, Luis Gil-Alana, and David Roubaud. 2019. Modelling long memory volatility in the Bitcoin market: Evidence of persistence and structural breaks. International Journal of Finance & Economics 24: 412–26. [Google Scholar]

- Cheah, Eng-Tuck, and John Fry. 2015. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Economics Letters 130: 32–36. [Google Scholar] [CrossRef] [Green Version]

- Davidson, James, and Dooruj Rambaccussing. 2015. A Test of the Long Memory Hypothesis Based on Self-Similarity. Journal of Time Series Econometrics 7: 115–41. [Google Scholar] [CrossRef] [Green Version]

- Davidson, James, and Phillip Sibbertsen. 2009. Tests of bias in log-periodogram regression. Economics Letters 102: 83–86. [Google Scholar] [CrossRef] [Green Version]

- Dehling, Herold, Aeneas Rooch, and Murad. S. Taqqu. 2013. Non-Parametric Change-Point Tests for Long-Range Dependent Data. Scandinavian Journal of Statistics 40: 153–73. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Atushi Inoue. 2001. Long memory and regime switching. Journal of Econometrics 105: 131–59. [Google Scholar] [CrossRef] [Green Version]

- Geweke, John, and Susan Porter-Hudak. 1983. The Estimation and Application of Long Memory Time Series Models. Journal of Time Series Analysis 4: 221–38. [Google Scholar] [CrossRef]

- Granger, Clive, and Namwon Hyung. 2004. Occasional structural breaks and long memory with an application to the S&P 500 absolute stock returns. Journal of Empirical Finance 11: 399–421. [Google Scholar] [CrossRef]

- Hurvich, Clifford, and Rohit Deo. 1999. Plug-in Selection of the Number of Frequencies in Regression Estimates of the Memory Parameter of a Long-memory Time Series. Journal of Time Series Analysis 20: 331–41. [Google Scholar] [CrossRef] [Green Version]

- Iacone, Fabrizio, Stephen Leybourne, and Robert Taylor. 2014. A fixed-b test for a break in level at an unknown time under fractional integration. Journal of Time Series Analysis 35: 40–54. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2017. Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters 158: 3–6. [Google Scholar] [CrossRef] [Green Version]

- Kaya Soylu, Pınar, Mustapha Okur, Özgur Çatıkkaş, and Ayca Altintig. 2020. Long Memory in the Volatility of Selected Cryptocurrencies: Bitcoin, Ethereum and Ripple. J. Risk Financial Management 13: 107. [Google Scholar] [CrossRef]

- Lahmiri, Salim, Stelios Bekiros, and andAntonio Salvi. 2018. Long-range memory, distributional variation and randomness of bitcoin volatility. Chaos, Solitons & Fractals 107: 43–48. [Google Scholar]

- Mensi, Walid, Khamis Hamed Al-Yahyaee, and Sang Hoon Kang. 2019. Structural breaks and double long memory of cryptocurrency prices: A comparative analysis from Bitcoin and Ethereum. Finance Research Letters 29: 222–30. [Google Scholar] [CrossRef]

- Moulines, Eric, and Phillipe Soulier. 1999. Broadband log-periodogram regression of time series with long-range dependence. Annals of Statistics 27: 1415–39. [Google Scholar] [CrossRef]

- Nadarajah, Saralees, and Jeffrey Chu. 2017. On the inefficiency of Bitcoin. Economics Letters 150: 6–9. [Google Scholar] [CrossRef] [Green Version]

- Ohanissian, Arek, Jeffrey Russell, and Ruey Tsay. 2008. True or spurious long memory? A new test. Journal of Business and Economic Statistics 26: 161–75. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer S. K. Chan, and Shelton Peiris. 2018. A new look at Cryptocurrencies. Economics Letters 163: 6–9. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer Chan, and Shelton Peiris. 2019. On long memory effects in the volatility measure of Cryptocurrencies. Finance Research Letters 28: 95–100. [Google Scholar] [CrossRef]

- Qu, Zhongjun. 2011. A test against spurious long memory. Journal of Business and Economic Statistics 29: 423–38. [Google Scholar] [CrossRef]

- Robinson, Peter. 1995. Gaussian Semiparametric Estimation of Long Range Dependence. The Annals of Statistics 23: 1630–61. [Google Scholar] [CrossRef]

- Shimotsu, Katsumi, and Peter Phillips. 2002. Pooled log periodogram regression. Journal of Time Series Analysis 23: 57–93. [Google Scholar] [CrossRef] [Green Version]

- Sibbertsen, Phillip, Christian Leschinski, and Marie Busch. 2018. A multivariate test against spurious long memory. Journal of Econometrics 203: 33–49. [Google Scholar] [CrossRef] [Green Version]

- Tiwari, Aviral, R. K. Jana, Debojyoti Das, and David Roubaud. 2018. Informational efficiency of Bitcoin—An extension. Economics Letters 163: 106–9. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2016. The inefficiency of Bitcoin. Economics Letters 148: 80–82. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2017. Price clustering in Bitcoin. Economics Letters 159: 145–48. [Google Scholar] [CrossRef]

- Wenger, Kai, Christian Leschinski, and Phillip Sibbertsen. 2018. A simple test on structural change in long-memory time series. Economics Letters 163: 90–94. [Google Scholar] [CrossRef] [Green Version]

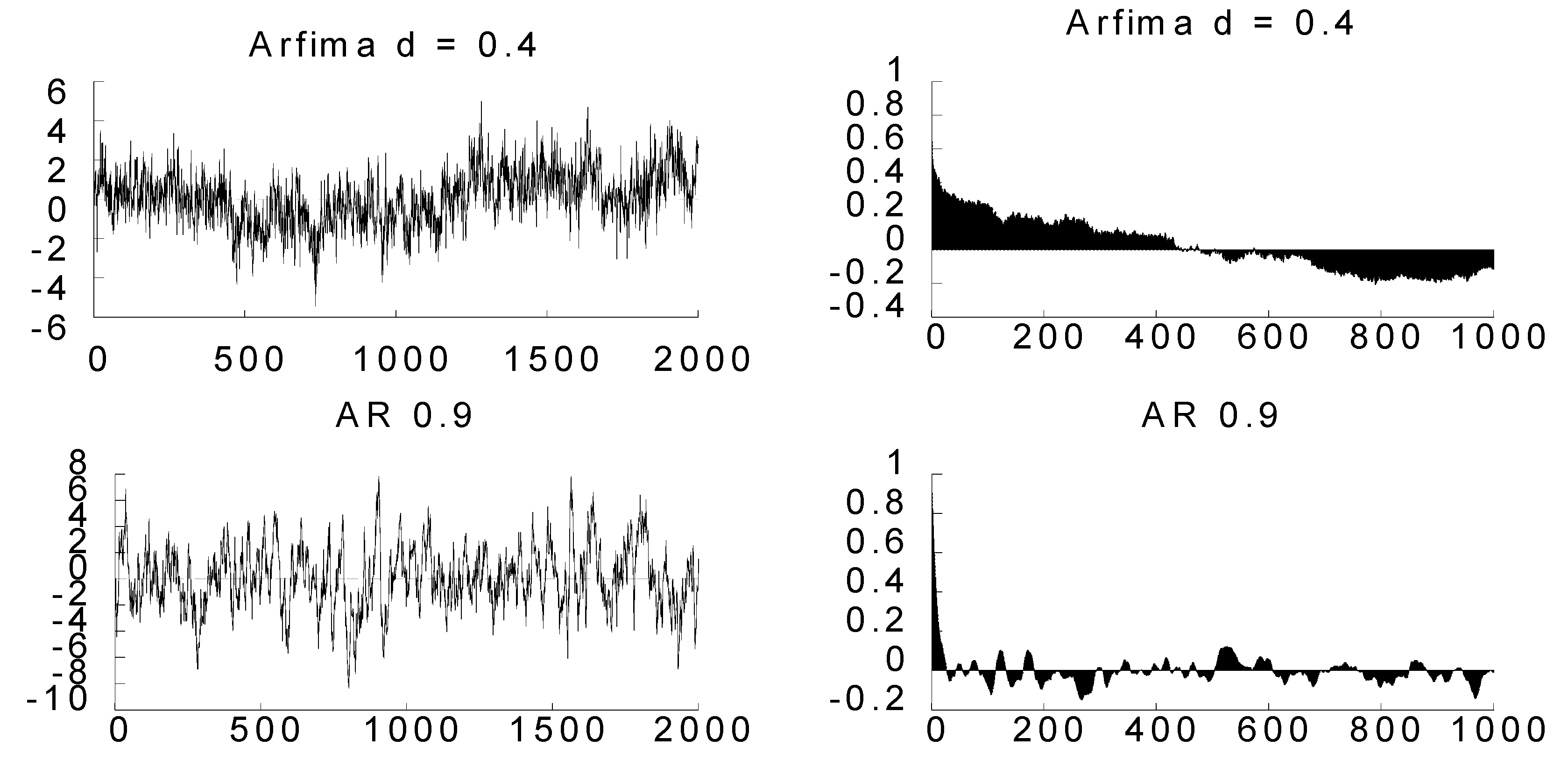

| 1 | Geometric decay would be easily discerned in the bottom right plot in Figure 1 if the number of lags was set at most at 30 (or at any low amount). |

{kind=link}

{kind=link}

{kind=link}

| GPH (M = T0.5) | GPH (M = T0.8) | Fourier Estimations | Local Whittle | |

|---|---|---|---|---|

| Model 1 | 0.141 | 0.557 | 0.467 | 0.140 |

| (0.109) | (0.026) | (0.125) | (0.089) | |

| Model 2 | 0.284 | 0.741 | 0.447 | 0.282 |

| (0.147) | (0.051) | (0.168) | (0.135) |

| Bitcoin | Bitcoin Cash | XRP | Litecoin | Ethereum | |

|---|---|---|---|---|---|

| Mean | 0.00102 | −0.0007 | 0.00149 | 0.00098 | 0.00332 |

| Std dev | 0.03897 | 0.07881 | 0.07271 | 0.06444 | 0.06104 |

| Skewness | −0.340 | 0.612 | 2.076 | 1.720 | 0.271 |

| Kurtosis | 8.459 | 10.651 | 32.91 | 28.618 | 7.052 |

| Jarque–Bera | 2761 | 2206 | 88925 | 67783 | 1082 |

| N | 2190 | 882 | 2340 | 2435 | 1553 |

| Bitcoin | Ethereum | Litecoin | Bitcoin Cash | XRP | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| T = 2190 | T = 1553 | T = 2435 | T = 883 | T = 2340 | ||||||

| Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | Estimate | p-Value | |

| Panel A: Return | ||||||||||

| GPH () | 0.153 | 0.165 | 0.259 ** | 0.036 | 0.170 | 0.111 | 0.121 | 0.405 | 0.057 | 0.589 |

| Bias Test | −0.454 | 0.675 | −1.407 | 0.920 | −0.122 | 0.549 | 0.806 | 0.210 | −0.886 | 0.812 |

| Skip-Sampling (h = 4) | −0.522 | 0.699 | −0.816 | 0.793 | 0.946 | 0.172 | −1.084 | 0.861 | 0.624 | 0.266 |

| Skip-Sampling (h = 8) | 0.378 | 0.353 | 0.168 | 0.433 | 0.044 | 0.482 | −0.486 | 0.686 | 0.544 | 0.293 |

| Panel B: Volatility | ||||||||||

| Volatility (LHR) | ||||||||||

| GPH () | 0.536 *** | 0.000 | 0.505 *** | 0.000 | 0.584 *** | 0.000 | 0.541 *** | 0.001 | 0.486 *** | 0.000 |

| Bias Test | −0.590 | 0.722 | 0.044 | 0.483 * | 0.084 | 0.467 | 0.322 | 0.374 | 2.356 *** | 0.009 |

| Skip-Sampling (h =4) | −0.073 | 0.529 | 0.431 | 0.333 | −0.768 | 0.779 | −0.451 | 0.674 | −0.406 | 0.658 |

| Skip-Sampling (h = 8) | 0.193 | 0.424 | 0.560 | 0.288 | −0.423 | 0.664 | −0.307 | 0.645 | −0.560 | 0.712 |

| Volatility (SR) | ||||||||||

| GPH () | 0.326 *** | 0.004 | 0.202* | 0.099 | 0.359 *** | 0.000 | 0.174 | 0.235 | 0.191 * | 0.077 |

| Bias Test | 1.524 * | 0.064 | −1.865 | 0.969 | 0.365 | 0.357 | 3.119 *** | 0.001 | 0.868 | 0.193 |

| Skip-Sampling (h = 4) | −0.860 | 0.805 | 0.637 | 0.262 | 0.142 | 0.443 | 0.585 | 0.279 | −0.737 | 0.770 |

| Skip-Sampling (h = 8) | −1.055 | 0.854 | 0.370 | 0.356 | 0.539 | 0.295 | 0.289 | 0.386 | −0.752 | 0.774 |

| Volatility (AR) | ||||||||||

| GPH () | 0.375 *** | 0.001 | 0.378 *** | 0.003 | 0.466 *** | 0.000 | 0.336 ** | 0.026 | 0.381 *** | 0.001 |

| Bias Test | −2.229 | 0.987 | −1.535 | 0.938 | 2.086 ** | 0.018 | 1.957 ** | 0.025 | −1.185 | 0.882 |

| Skip-Sampling (h = 4) | −1.027 | 0.848 | 0.423 | 0.336 | −1.229 | 0.890 | −0.013 | 0.505 | 0.070 | 0.472 |

| Skip-Sampling (h = 8) | −1.081 | 0.860 | 0.848 | 0.198 | −0.482 | 0.685 | −0.257 | 0.601 | −0.421 | 0.663 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rambaccussing, D.; Mazibas, M. True versus Spurious Long Memory in Cryptocurrencies. J. Risk Financial Manag. 2020, 13, 186. https://doi.org/10.3390/jrfm13090186

Rambaccussing D, Mazibas M. True versus Spurious Long Memory in Cryptocurrencies. Journal of Risk and Financial Management. 2020; 13(9):186. https://doi.org/10.3390/jrfm13090186

Chicago/Turabian StyleRambaccussing, Dooruj, and Murat Mazibas. 2020. "True versus Spurious Long Memory in Cryptocurrencies" Journal of Risk and Financial Management 13, no. 9: 186. https://doi.org/10.3390/jrfm13090186

APA StyleRambaccussing, D., & Mazibas, M. (2020). True versus Spurious Long Memory in Cryptocurrencies. Journal of Risk and Financial Management, 13(9), 186. https://doi.org/10.3390/jrfm13090186