Sanctions as a Catalyst for Russia’s and China’s Balance of Trade: Business Opportunity

Abstract

:1. Introduction

- (1)

- Have the sanctions imposed on the Russian Federation strengthened the trade with the People’s Republic of China since 2014?

- (2)

- Can we expect mutual trade between these countries to grow in the future?

2. Literary Research

3. Materials and Methods

- 1-month lag in the time series,

- 3-month lag in the time series,

- 6-month lag in the time series.

- Overview of the retained networks: in each case, it contains the structures of five retained neural networks, performance of the datasets, error function, function of the activation of the neural network hidden and output layers.

- Correlation coefficients: characterize the network performance in the individual data subsets.

- Basic statistics of equalized time series.

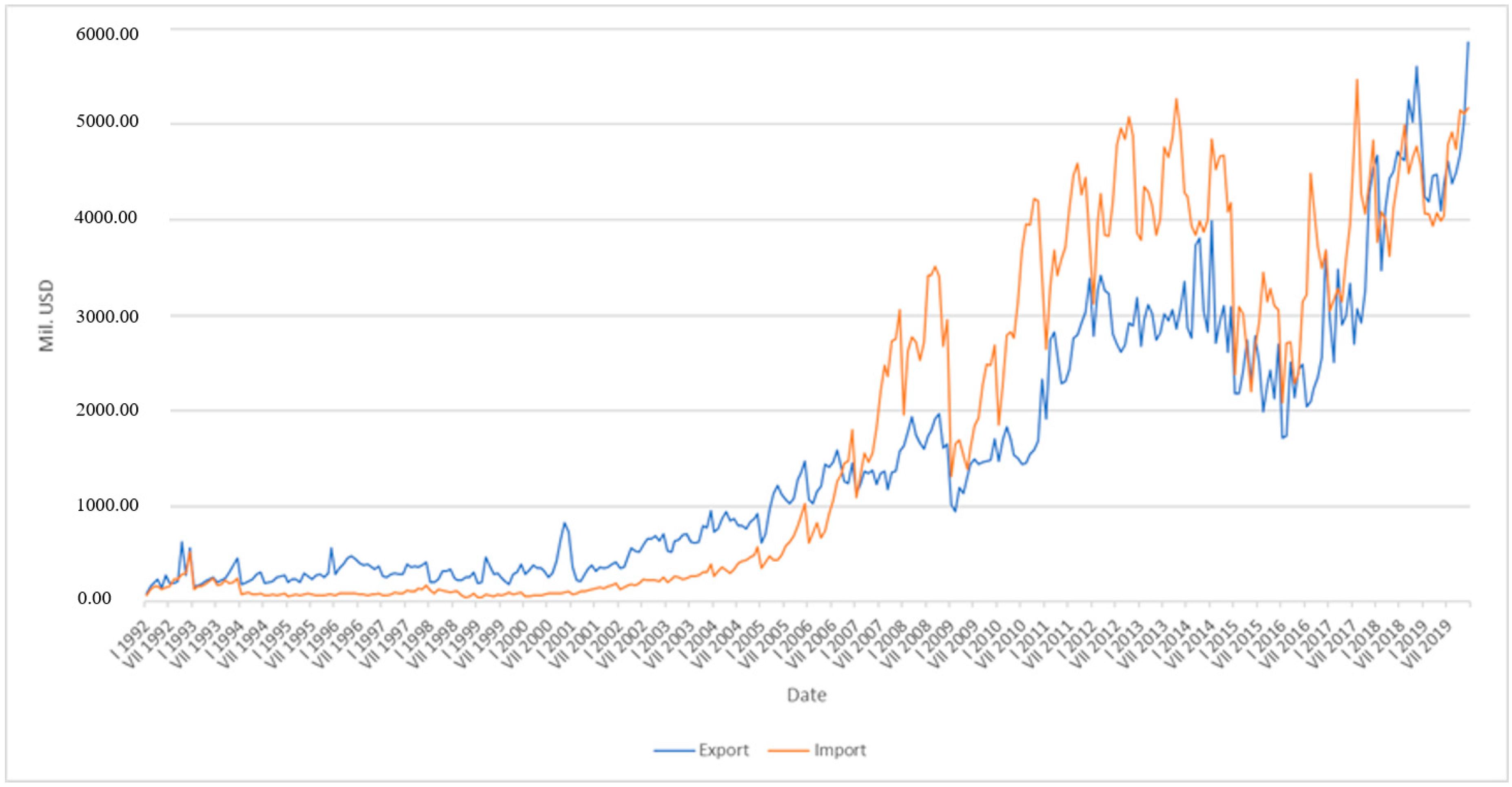

- Graph of equalized time series.

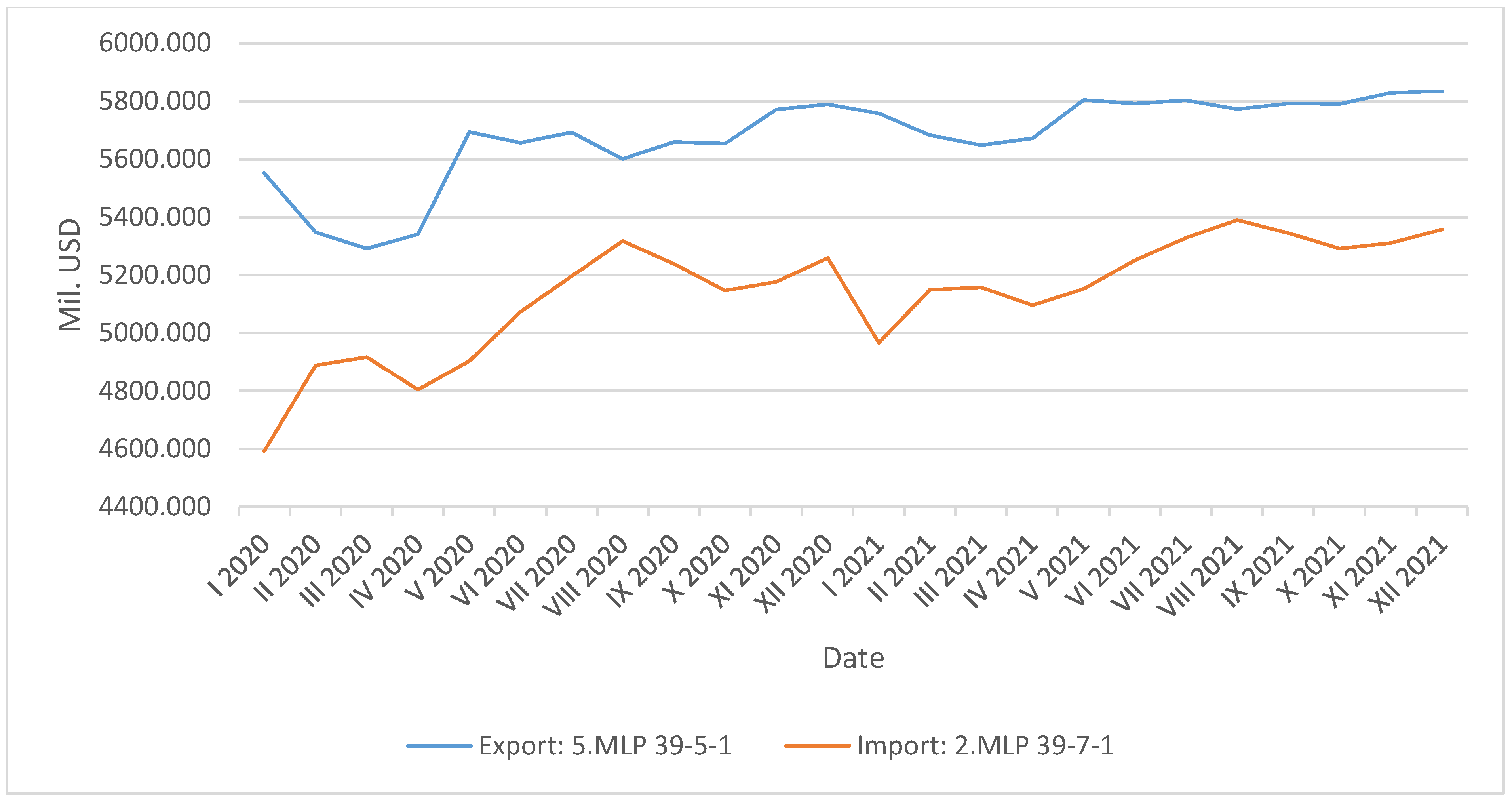

- Predicted values from January 2020 and December 2021.

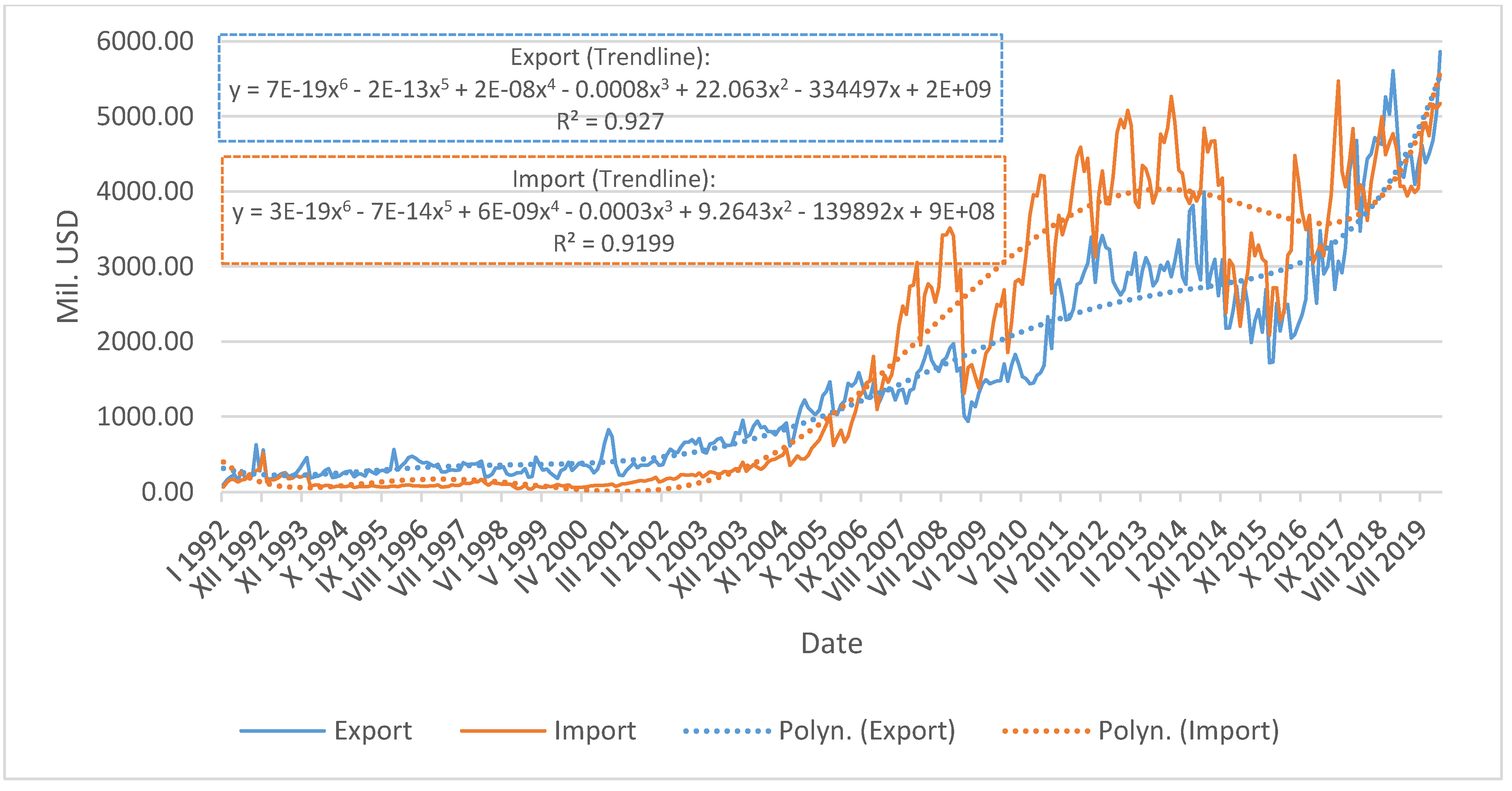

- Graph of the actual time series development with the predictions, that is, a possible development of the time series from January 1992 to December 2021.

4. Results

- Structure of the neural network in the following form: serial number of the neural network retained from the experiment, designation of the neural network type (MLP), number of neurons in the input layer and output layer. The objective is to predict the result—either import or export. Therefore, the output layer always contains only one neuron.

- Neural network performance: it is the value of the correlation coefficient indicating the result of equalizing the time series by the neural network (or to which extent the actual and equalized time series’ course are identical). The performance is given separately for the training, testing, and validation datasets.

- Error of neural network.

- Training algorithm: in all cases, the Broyden–Fletcher–Goldfarb–Shanno training algorithm (Avriel 2003) is used.

- Error function: Statistica software will choose either entropy or sum of least squares.

- Activation function of the hidden layer of neurons.

- Activation function of the output neuron.

4.1. Selection of Most Suitable Networks

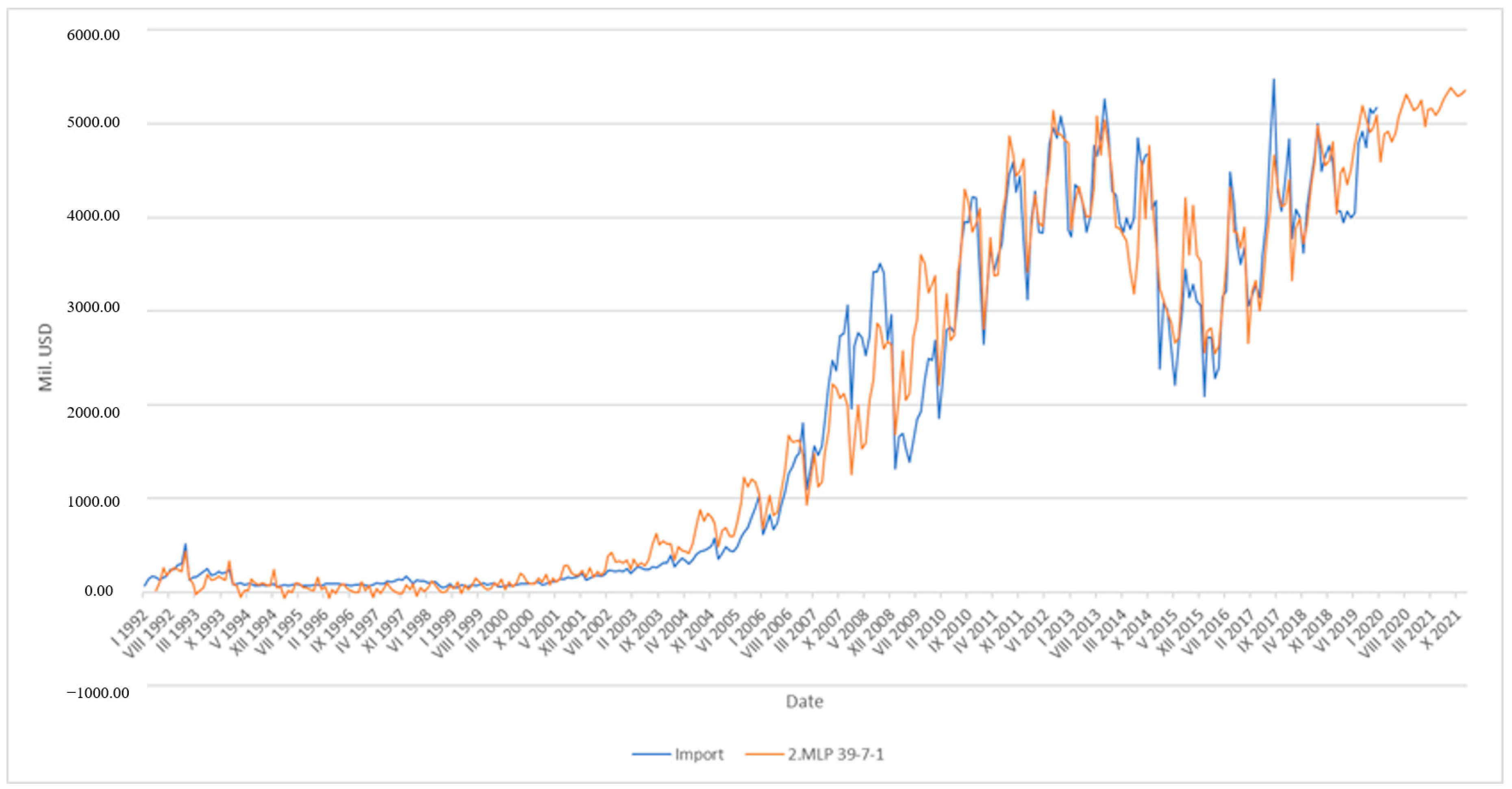

4.2. Prediction

5. Discussion

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix A.1. Export

Appendix A.1.1. 1-Month Time Series Lag

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Summary of Active Networks: Export | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Index | Net. Name | Training Perf. | Test Perf. | Validation Perf. | Training Error | Test Error | Validation Error | Training Algorithm | Error Function | Hidden Activation | Output Activation |

| 1 | MLP 13-5-1 | 0.964118 | 0.941782 | 0.965376 | 64,633.79 | 98,418.7 | 90,892.15 | BFGS 94 | SOS | Logistic | Tanh |

| 2 | MLP 13-6-1 | 0.962371 | 0.934458 | 0.962191 | 68,071.21 | 109,802.9 | 74,079.67 | BFGS 36 | SOS | Logistic | Logistic |

| 3 | MLP 13-4-1 | 0.971666 | 0.942705 | 0.96687 | 51,599.89 | 99,085.5 | 68,101.9 | BFGS 61 | SOS | Logistic | Exponential |

| 4 | MLP 13-7-1 | 0.981881 | 0.958261 | 0.976365 | 33,173.23 | 72,821.7 | 48,599.45 | BFGS 133 | SOS | Logistic | Exponential |

| 5 | MLP 13-4-1 | 0.97653 | 0.951515 | 0.978344 | 44,456.05 | 93,516.9 | 60,713.31 | BFGS 83 | SOS | Logistic | Tanh |

| Predictions Statistics, Target: Export | |||||

| Statistics | 1.MLP 13-5-1 | 2.MLP 13-6-1 | 3.MLP 13-4-1 | 4.MLP 13-7-1 | 5.MLP 13-4-1 |

| Minimum prediction (Train) | −48.14 | 92.81 | 204.91 | 92.76 | 87.22 |

| Maximum prediction (Train) | 5703.67 | 5504.56 | 5285.57 | 4888.29 | 5786.67 |

| Minimum prediction (Test) | 16.49 | 116.52 | 205.20 | 92.76 | 180.41 |

| Maximum prediction (Test) | 5085.96 | 4594.78 | 5075.24 | 4888.22 | 5596.38 |

| Minimum prediction (Validation) | −195.58 | 93.64 | 205.17 | 92.76 | 215.92 |

| Maximum prediction (Validation) | 5314.03 | 4706.45 | 4914.68 | 4888.29 | 5279.32 |

| Minimum residual (Train) | −1409.63 | −1278.85 | −1121.77 | −1042.61 | −1043.81 |

| Maximum residual (Train) | 1105.42 | 1339.59 | 1127.94 | 1048.73 | 725.73 |

| Minimum residual (Test) | −1182.00 | −1063.78 | −914.06 | −896.18 | −1448.43 |

| Maximum residual (Test) | 1116.97 | 1282.21 | 1289.08 | 1228.61 | 1320.54 |

| Minimum residual (Validation) | −1447.06 | −1408.09 | −1087.19 | −1031.41 | −1038.28 |

| Maximum residual (Validation) | 615.20 | 877.11 | 764.88 | 641.54 | 574.97 |

| Minimum standard residual (Train) | −5.54 | −4.90 | −4.94 | −5.72 | −4.95 |

| Maximum standard residual (Train) | 4.35 | 5.13 | 4.97 | 5.76 | 3.44 |

| Minimum standard residual (Test) | −3.77 | −3.21 | −2.90 | −3.32 | −4.74 |

| Maximum standard residual (Test) | 3.56 | 3.87 | 4.10 | 4.55 | 4.32 |

| Minimum standard residual (Validation) | −4.80 | −5.17 | −4.17 | −4.68 | −4.21 |

| Maximum standard residual (Validation) | 2.04 | 3.22 | 2.93 | 2.91 | 2.33 |

Appendix A.1.2. 3-Month Time Series Lag

| Summary of Active Networks: Export | |||||||||||

| Index | Net. Name | Training Perf. | Test Perf. | Validation Perf. | Training Error | Test Error | Validation Error | Training Algorithm | Error Function | Hidden Activation | Output Activation |

| 1 | MLP 39-3-1 | 0.97532033 | 0.94195947 | 0.96247204 | 44,059.0306 | 97,526.5858 | 67,426.7124 | BFGS 403 | SOS | Logistic | Exponential |

| 2 | MLP 39-4-1 | 0.97357597 | 0.9452088 | 0.98021157 | 47,495.3908 | 94,752.6937 | 40,929.7788 | BFGS 63 | SOS | Logistic | Tanh |

| 3 | MLP 39-4-1 | 0.96949132 | 0.94504827 | 0.96890301 | 54,425.1995 | 94,208.2191 | 60,900.6634 | BFGS 62 | SOS | Logistic | Sine |

| 4 | MLP 39-4-1 | 0.97813455 | 0.94161045 | 0.96616922 | 39,075.6848 | 97,471.407 | 60,995.4233 | BFGS 210 | SOS | Logistic | Exponential |

| 5 | MLP 39-5-1 | 0.98254397 | 0.93703105 | 0.97883517 | 31,273.7412 | 105,188.295 | 46,845.2416 | BFGS 130 | SOS | Tanh | Logistic |

| Predictions Statistics, Target: Export | |||||

| Statistics | 1.MLP 39-3-1 | 2.MLP 39-4-1 | 3.MLP 39-4-1 | 4.MLP 39-4-1 | 5.MLP 39-5-1 |

| Minimum prediction (Train) | 284.66 | 134.96 | 54.53 | 216.58 | 224.25 |

| Maximum prediction (Train) | 4921.19 | 5653.00 | 5764.33 | 4911.88 | 5047.28 |

| Minimum prediction (Test) | 287.81 | 131.02 | 55.82 | 217.17 | 316.00 |

| Maximum prediction (Test) | 4883.37 | 5374.72 | 5204.20 | 4850.73 | 5001.04 |

| Minimum prediction (Validation) | 287.20 | 108.24 | 72.92 | 216.85 | 315.92 |

| Maximum prediction (Validation) | 4904.14 | 5008.12 | 5107.40 | 4906.46 | 4998.94 |

| Minimum residual (Train) | −953.33 | −924.71 | −948.70 | −934.85 | −1036.51 |

| Maximum residual (Train) | 1115.98 | 801.98 | 1128.49 | 963.43 | 1087.54 |

| Minimum residual (Test) | −862.53 | −1282.22 | −1118.09 | −880.37 | −1123.55 |

| Maximum residual (Test) | 1294.05 | 1451.70 | 1078.16 | 1320.29 | 1766.29 |

| Minimum residual (Validation) | −1054.21 | −875.06 | −921.31 | −1022.13 | −1008.88 |

| Maximum residual (Validation) | 1287.41 | 567.66 | 619.39 | 1333.29 | 668.48 |

| Minimum standard residual (Train) | −4.54 | −4.24 | −4.07 | −4.73 | −5.86 |

| Maximum standard residual (Train) | 5.32 | 3.68 | 4.84 | 4.87 | 6.15 |

| Minimum standard residual (Test) | −2.76 | −4.17 | −3.64 | −2.82 | −3.46 |

| Maximum standard residual (Test) | 4.14 | 4.72 | 3.51 | 4.23 | 5.45 |

| Minimum standard residual (Validation) | −4.06 | −4.33 | −3.73 | −4.14 | −4.66 |

| Maximum standard residual (Validation) | 4.96 | 2.81 | 2.51 | 5.40 | 3.09 |

Appendix A.1.3. 6-Month Time Series Lag

| Summary of Active Networks: Export | |||||||||||

| Index | Net. Name | Training Perf. | Test Perf. | Validation Perf. | Training Error | Test Error | Validation Error | Training Algorithm | Error Function | Hidden Activation | Output Activation |

| 1 | MLP 78-3-1 | 0.97644692 | 0.95202612 | 0.98359434 | 41,858.6744 | 83,708.843 | 46,262.5535 | BFGS 62 | SOS | Logistic | Sine |

| 2 | MLP 78-3-1 | 0.97564053 | 0.9442971 | 0.96913162 | 43,239.5805 | 96,061.9557 | 57,371.2003 | BFGS 182 | SOS | Logistic | Exponential |

| 3 | MLP 78-3-1 | 0.97541954 | 0.94265005 | 0.96675215 | 43,610.1888 | 96,817.8135 | 57,072.2957 | BFGS 141 | SOS | Logistic | Exponential |

| 4 | MLP 78-4-1 | 0.97629068 | 0.94894962 | 0.98091908 | 42,169.8767 | 87,437.7493 | 45,852.2848 | BFGS 91 | SOS | Tanh | Tanh |

| 5 | MLP 78-4-1 | 0.97673919 | 0.94871987 | 0.98170221 | 41,307.2543 | 86,825.5632 | 41,116.7293 | BFGS 100 | SOS | Tanh | Tanh |

| Predictions Statistics, Target: Export | |||||

| Statistics | 1.MLP 78-3-1 | 2.MLP 78-3-1 | 3.MLP 78-3-1 | 4.MLP 78-4-1 | 5.MLP 78-4-1 |

| Minimum prediction (Train) | 297.90 | 207.16 | 262.14 | 159.52 | 172.26 |

| Maximum prediction (Train) | 5816.45 | 4950.51 | 4935.57 | 5644.4 | 5574.49 |

| Minimum prediction (Test) | 298.73 | 208.22 | 264.52 | 239.96 | 218.05 |

| Maximum prediction (Test) | 5405.34 | 4914.97 | 4898.08 | 5338.78 | 5261.11 |

| Minimum prediction (Validation) | 299.10 | 213.43 | 273.65 | 373.34 | 384.65 |

| Maximum prediction (Validation) | 5376.65 | 4924.78 | 4917.57 | 5271.58 | 5173.10 |

| Minimum residual (Train) | −834.67 | −964.01 | −1022.59 | −808.13 | −759.34 |

| Maximum residual (Train) | 981.55 | 1119.31 | 1124.36 | 825.71 | 890.25 |

| Minimum residual (Test) | −1197.71 | −873.81 | −860.74 | −1138.27 | −1031.82 |

| Maximum residual (Test) | 1198.67 | 1295.36 | 1305.34 | 1347.08 | 1359.34 |

| Minimum residual (Validation) | −1001.30 | −1051.11 | −1049.21 | −891.97 | −806.97 |

| Maximum residual (Validation) | 401.8 | 847.69 | 849.64 | 470.37 | 477.99 |

| Minimum standard residual (Train) | −4.08 | −4.64 | −4.90 | −3.94 | −3.74 |

| Maximum standard residual (Train) | 4.80 | 5.38 | 5.38 | 4.02 | 4.38 |

| Minimum standard residual (Test) | −4.14 | −2.82 | −2.77 | −3.85 | −3.50 |

| Maximum standard residual (Test) | 4.14 | 4.18 | 4.20 | 4.56 | 4.61 |

| Minimum standard residual (Validation) | −4.66 | −4.39 | −4.39 | −4.17 | −3.98 |

| Maximum standard residual (Validation) | 1.87 | 3.54 | 3.56 | 2.20 | 2.36 |

Appendix A.2. Import

Appendix A.2.1. 1-Month Time Series Lag

| Summary of Active Networks: IMPORT | |||||||||||

| Index | Net. Name | Training Perf. | Test Perf. | Validation Perf. | Training Error | Test Error | Validation Error | Training Algorithm | Error Function | Hidden Activation | Output Activation |

| 1 | MLP 13-7-1 | 0.98211663 | 0.95546928 | 0.98489223 | 57,955.1319 | 139,584.498 | 46,306.5759 | BFGS 167 | SOS | Tanh | Identity |

| 2 | MLP 13-4-1 | 0.98273425 | 0.95747403 | 0.98434451 | 55,937.4497 | 128,193.356 | 48,507.2954 | BFGS 169 | SOS | Tanh | Identity |

| 3 | MLP 13-8-1 | 0.98412979 | 0.9581458 | 0.98526247 | 51,449.4647 | 131,787.876 | 49,657.3749 | BFGS 116 | SOS | Tanh | Identity |

| 4 | MLP 13-4-1 | 0.98211731 | 0.9515452 | 0.98393823 | 58,018.5351 | 152,635.45 | 50,054.0195 | BFGS 109 | SOS | Tanh | Identity |

| 5 | MLP 13-5-1 | 0.98559157 | 0.96022997 | 0.98312111 | 46,746.8031 | 121,708.496 | 57,921.0907 | BFGS 197 | SOS | Tanh | Identity |

| Predictions Statistics, Target: Import | |||||

| Statistics | 1.MLP 13-7-1 | 2.MLP 13-4-1 | 3.MLP 13-8-1 | 4.MLP 13-4-1 | 5.MLP 13-5-1 |

| Minimum prediction (Train) | −283.72 | −267.90 | −14.83 | 101.94 | 38.51 |

| Maximum prediction (Train) | 5441.74 | 5290.27 | 5382.37 | 4989.72 | 5586.51 |

| Minimum prediction (Test) | −66.12 | −87.62 | 19.27 | 103.32 | 47.90 |

| Maximum prediction (Test) | 5002.03 | 4962.02 | 5215.37 | 4740.85 | 4883.06 |

| Minimum prediction (Validation) | −104.23 | −31.10 | −4.29 | 102.26 | 51.10 |

| Maximum prediction (Validation) | 5057.82 | 5134.64 | 4988.22 | 4990.36 | 5050.67 |

| Minimum residual (Train) | −1212.89 | −1030.75 | −1110.61 | −1310.34 | −1199.08 |

| Maximum residual (Train) | 1095.78 | 1184.97 | 1164.59 | 1095.67 | 1033.33 |

| Minimum residual (Test) | −1677.56 | −1538.15 | −1679.91 | −1734.11 | −1813.82 |

| Maximum residual (Test) | 1267.85 | 1338.18 | 1328.27 | 1310.81 | 1110.90 |

| Minimum residual (Validation) | −772.36 | −740.95 | −833.57 | −836.22 | −812.02 |

| Maximum residual (Validation) | 752.94 | 913.17 | 785.70 | 960.33 | 987.50 |

| Minimum standard residual (Train) | −5.04 | −4.36 | −4.90 | −5.44 | −5.55 |

| Maximum standard residual (Train) | 4.55 | 5.01 | 5.13 | 4.55 | 4.78 |

| Minimum standard residual (Test) | −4.49 | −4.30 | −4.63 | −4.44 | −5.20 |

| Maximum standard residual (Test) | 3.39 | 3.74 | 3.66 | 3.36 | 3.18 |

| Minimum standard residual (Validation) | −3.59 | −3.36 | −3.74 | −3.74 | −3.37 |

| Maximum standard residual (Validation) | 3.50 | 4.15 | 3.53 | 4.29 | 4.10 |

Appendix A.2.2. 3-Month Time Series Lag

| Summary of Active Networks: IMPORT | |||||||||||

| Index | Net. Name | Training Perf. | Test Perf. | Validation Perf. | Training Error | Test Error | Validation Error | Training Algorithm | Error Function | Hidden Activation | Output Activation |

| 1 | MLP 39-3-1 | 0.982084293 | 0.955739315 | 0.982493276 | 57,496.5482 | 142,352.549 | 58,376.4509 | BFGS 79 | SOS | Tanh | Sine |

| 2 | MLP 39-7-1 | 0.985733635 | 0.961027279 | 0.983817619 | 45,763.9348 | 120,769.779 | 58,875.8861 | BFGS 159 | SOS | Tanh | Sine |

| 3 | MLP 39-5-1 | 0.984727318 | 0.955798472 | 0.981888107 | 48,998.1328 | 135,649.617 | 55,682.3959 | BFGS 93 | SOS | Tanh | Identity |

| 4 | MLP 39-5-1 | 0.983538279 | 0.961110378 | 0.983026428 | 52,813.4803 | 125,365.301 | 58,710.492 | BFGS 101 | SOS | Tanh | Sine |

| 5 | MLP 39-4-1 | 0.980490573 | 0.945832085 | 0.981664831 | 62,563.002 | 173,455.585 | 56,615.7557 | BFGS 104 | SOS | Tanh | Sine |

| Predictions Statistics, Target: Import | |||||

| Statistics | 1.MLP 39-3-1 | 2.MLP 39-7-1 | 3.MLP 39-5-1 | 4.MLP 39-5-1 | 5.MLP 39-4-1 |

| Minimum prediction (Train) | −42.02 | −62.84 | −25.60 | −6.66 | 92.08 |

| Maximum prediction (Train) | 5077.02 | 5188.27 | 5475.82 | 5379.54 | 5384.16 |

| Minimum prediction (Test) | −12.48 | −64.68 | 10.49 | 4.68 | 92.12 |

| Maximum prediction (Test) | 4762.13 | 4968.92 | 4623.28 | 5160.24 | 4883.31 |

| Minimum prediction (Validation) | −13.08 | −57.71 | −36.59 | −42.16 | 91.66 |

| Maximum prediction (Validation) | 5026.38 | 5080.21 | 5142.23 | 4992.38 | 4915.67 |

| Minimum residual (Train) | −1167.65 | −1060.10 | −1140.91 | −1144.08 | −1437.42 |

| Maximum residual (Train) | 1128.87 | 1192.25 | 1058.99 | 1091.53 | 1253.09 |

| Minimum residual (Test) | −1701.33 | −1673.42 | −1669.27 | −1686.41 | −1914.78 |

| Maximum residual (Test) | 1125.09 | 1257.89 | 1232.87 | 1135.85 | 1115.67 |

| Minimum residual (Validation) | −896.25 | −934.75 | −682.29 | −910.03 | −965.45 |

| Maximum residual (Validation) | 899.06 | 814.72 | 1094.66 | 848.94 | 940.96 |

| Minimum standard residual (Train) | −4.87 | −4.96 | −5.15 | −4.98 | −5.75 |

| Maximum standard residual (Train) | 4.71 | 5.57 | 4.78 | 4.75 | 5.01 |

| Minimum standard residual (Test) | −4.51 | −4.82 | −4.53 | −4.76 | −4.60 |

| Maximum standard residual (Test) | 2.98 | 3.62 | 3.35 | 3.21 | 2.68 |

| Minimum standard residual (Validation) | −3.71 | −3.85 | −2.89 | −3.76 | −4.06 |

| Maximum standard residual (Validation) | 3.72 | 3.36 | 4.64 | 3.50 | 3.95 |

Appendix A.2.3. 6-Month Time Series Lag

| Summary of Active Networks: Import | |||||||||||

| Index | Net. Name | Training Perf. | Test Perf. | Validation Perf. | Training Error | Test Error | Validation Error | Training Algorithm | Error Function | Hidden Activation | Output Activation |

| 1 | MLP 78-8-1 | 0.980660 | 0.947515 | 0.977350 | 61,538.73 | 166,992.1 | 65,690.75 | BFGS 89 | SOS | Tanh | Identity |

| 2 | MLP 78-4-1 | 0.982732 | 0.955443 | 0.981321 | 54,946.94 | 136,337.8 | 55,504.71 | BFGS 102 | SOS | Tanh | Identity |

| 3 | MLP 78-3-1 | 0.984100 | 0.955061 | 0.982016 | 50,601.03 | 139,823.6 | 59,876.39 | BFGS 126 | SOS | Logistic | Identity |

| 4 | MLP 78-5-1 | 0.980382 | 0.953199 | 0.976726 | 62,829.26 | 148,745.4 | 77,402.81 | BFGS 146 | SOS | Tanh | Logistic |

| 5 | MLP 78-5-1 | 0.985191 | 0.959920 | 0.982193 | 47,285.03 | 119,485.7 | 51,174.38 | BFGS 154 | SOS | Tanh | Exponential |

| Predictions Statistics, Target: Import | |||||

| Statistics | 1.MLP 78-8-1 | 2.MLP 78-4-1 | 3.MLP 78-3-1 | 4.MLP 78-5-1 | 5.MLP 78-5-1 |

| Minimum prediction (Train) | −37.96 | 27.26 | 23.46 | 42.79 | 42.92 |

| Maximum prediction (Train) | 5557.44 | 5547.49 | 5702.71 | 5145.17 | 5602.16 |

| Minimum prediction (Test) | 0.06 | 28.20 | 28.53 | 42.79 | 42.99 |

| Maximum prediction (Test) | 5052.58 | 5104.16 | 5334.23 | 5002.21 | 5085.20 |

| Minimum prediction (Validation) | −1.30 | 30.35 | 29.95 | 42.79 | 43.02 |

| Maximum prediction (Validation) | 4776.93 | 5126.97 | 5201.12 | 4549.86 | 4993.25 |

| Minimum residual (Train) | −1367.68 | −1066.21 | −1290.16 | −1537.74 | −1167.61 |

| Maximum residual (Train) | 1124.21 | 1142.49 | 992.10 | 1079.38 | 982.56 |

| Minimum residual (Test) | −1742.63 | −1557.97 | −1565.99 | −1634.06 | −1571.91 |

| Maximum residual (Test) | 1125.11 | 1296.51 | 1331.98 | 1342.31 | 1173.03 |

| Minimum residual (Validation) | −1012.55 | −702.37 | −890.03 | −784.47 | −676.09 |

| Maximum residual (Validation) | 859.16 | 1000.17 | 957.20 | 1163.80 | 1007.69 |

| Minimum standard residual (Train) | −5.51 | −4.55 | −5.74 | −6.13 | −5.37 |

| Maximum standard residual (Train) | 4.53 | 4.87 | 4.41 | 4.31 | 4.52 |

| Minimum standard residual (Test) | −4.26 | −4.22 | −4.19 | −4.24 | −4.55 |

| Maximum standard residual (Test) | 2.75 | 3.51 | 3.56 | 3.48 | 3.39 |

| Minimum standard residual (Validation) | −3.95 | −2.98 | −3.64 | −2.82 | −2.99 |

| Maximum standard residual (Validation) | 3.35 | 4.25 | 3.91 | 4.18 | 4.45 |

References

- Afesorgbor, Sylvanus Kwaku. 2019. The impact of economic sanctions on international trade: How do threatened sanctions compare with imposed sanctions? European Journal of Political Economy 56: 11–26. [Google Scholar] [CrossRef] [Green Version]

- Afesorgbor, Sylvanus Kwaku, and Renuka Mahadevan. 2016. The impact of economic sanctions on income inequality of target states. World Development 83: 1–11. [Google Scholar] [CrossRef] [Green Version]

- Amiri, Hossein, Farzaneh Samadian, Masoud Yahoo, and Seyed Jafar Jamali. 2019. Natural resource abundance, institutional quality and manufacturing development: Evidence from resource-rich countries. Resources Policy 62: 550–60. [Google Scholar] [CrossRef]

- Ankudinov, Andrei, Rustam Ibragimov, and Oleg Lebedev. 2017. Sanctions and the Russian stock market. Research in International Business and Finance 40: 150–62. [Google Scholar] [CrossRef]

- Ashton, Catherine. 2014. Council Decision 2014/145/CFSP of 17 March 2014: Concerning Restrictive Measures in Respect of Actions Undermining or Threatening the Territorial Integrity, Sovereignty and Independence of Ukraine. Brussel: Publications Office EUR-lex, Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014D0145&from=CS (accessed on 15 September 2020).

- Avriel, Mordecai. 2003. Nonlinear Programming: Analysis and Methods. New York: Dover Publishing, p. 544. ISBN 978-0-486-43227-4. [Google Scholar]

- Baev, Pavel K. 2016. Russia’s pivot to China goes astray: The impact on the Asia-Pacific security architecture. Contemporary Security Policy 37: 89–110. [Google Scholar] [CrossRef]

- Belkin, Mikhail, Daniel Hsu, Siyuan Ma, and Soumik Mandal. 2019. Reconciling modern machine-learning practice and the classical bias–variance trade-off. Proceedings of the National Academy of Sciences 116: 15849–54. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Biersteker, Thomas J., Sue E. Eckert, Marcos Tourinho, and Zuzana Hudáková. 2018. UN targeted sanctions datasets (1991–2013). Journal of Peace Research 55: 404–12. [Google Scholar] [CrossRef]

- Bishop, Christopher M. 1995. Neural Networks for Pattern Recognition. New York: Oxford University Press, ISBN 0-19-853864-2. [Google Scholar]

- Bloom, Nicholas, Mirko Draca, and John Van Reenen. 2016. Trade induced technical change? The impact of Chinese imports on innovation, IT and productivity. The Review of Economic Studies 83: 87–117. [Google Scholar] [CrossRef] [Green Version]

- Boulanger, Pierre, Hasan Dudu, Emanuele Ferrari, and George Philippidis. 2016. Russian roulette at the trade table: A specific factors CGE analysis of an agri-food import ban. Journal of Agricultural Economics 67: 272–91. [Google Scholar] [CrossRef] [Green Version]

- Bradshaw, Michael, and Alec Waterworth. 2020. China’s dash for gas: Local challenges and global consequences. Eurasian Geography and Economics, 1–39. [Google Scholar] [CrossRef]

- Carmona, Pedro, Francisco Climent, and Alexandre Momparler. 2019. Predicting failure in the U.S. banking sector: An extreme gradient boosting approach. International Review of Economics & Finance 61: 304–23. [Google Scholar] [CrossRef]

- Charap, Samuel, John Drennan, and Pierre Noël. 2017. Russia and China: A new model of great-power relations. Survival 59: 25–42. [Google Scholar] [CrossRef]

- Chen, Yin E., Qiang Fu, Xinxin Zhao, Xuemei Yuan, and Chun-Ping Chang. 2019. International sanctions’ impact on energy efficiency in target states. Economic Modelling 82: 21–34. [Google Scholar] [CrossRef]

- Connolly, Richard. 2016. The empire strikes back: Economic statecraft and the securitisation of political economy in Russia. Europe-Asia Studies 68: 750–73. [Google Scholar] [CrossRef]

- Dreger, Christian, Konstantin A. Kholodilin, Dirk Ulbricht, and Jarko Fidrmuc. 2016. Between the hammer and the anvil: The impact of economic sanctions and oil prices on Russia’s ruble. Journal of Comparative Economics 44: 295–308. [Google Scholar] [CrossRef] [Green Version]

- Du, Julan, and Yifei Zhang. 2018. Does One Belt One Road initiative promote Chinese overseas direct investment? China Economic Review 47: 189–205. [Google Scholar] [CrossRef]

- Dudlák, Tamás. 2018. After the sanctions: Policy challenges in transition to a new political economy of the Iranian oil and gas sectors. Energy Policy 121: 464–75. [Google Scholar] [CrossRef] [Green Version]

- Early, Bryan R., and Amira Jadoon. 2016. Do sanctions always stigmatize? The effects of economic sanctions on foreign aid. International Interactions 42: 217–43. [Google Scholar] [CrossRef]

- Early, Bryan R., and Keith A. Peksen. 2019. Searching in the shadows: The impact of economic sanctions on informal economies. Political Research Quarterly 72: 821–34. [Google Scholar] [CrossRef]

- Early, Bryan R., and Keith A. Preble. 2020. Going fishing versus hunting whales: Explaining changes in how the US enforces economic sanctions. Security Studies, 1–37. [Google Scholar] [CrossRef]

- Ekinci, Aykut, and Halil İbrahim Erdal. 2017. Forecasting bank failure: Base learners, ensembles and hybrid ensembles. Computational Economics 49: 677–86. [Google Scholar] [CrossRef]

- Esen, Vedat, and Bulent Oral. 2016. Natural gas reserve/production ratio in Russia, Iran, Qatar and Turkmenistan: A political and economic perspective. Energy Policy 93: 101–9. [Google Scholar] [CrossRef]

- Fedoseeva, Svetlana, and Roland Herrmann. 2019. The price of sanctions: An empirical analysis of German export losses due to the Russian agricultural ban. Canadian Journal of Agricultural Economics/Revue Canadienne D’agroeconomie 67: 417–31. [Google Scholar] [CrossRef]

- Feldman, Nizan, and Tal Sadeh. 2016. War and third-party trade. Journal of Conflict Resolution 62: 119–42. [Google Scholar] [CrossRef] [Green Version]

- Fortescue, Stephen. 2015. Russia’s “turn to the east”: A study in policy making. Post-Soviet Affairs 32: 423–54. [Google Scholar] [CrossRef] [Green Version]

- Gartzke, Erik, and Oliver Westerwinter. 2016. The complex structure of commercial peace contrasting trade interdependence, asymmetry, and multipolarity. Journal of Peace Research 53: 325–43. [Google Scholar] [CrossRef]

- Gharehgozli, Orkideh. 2017. An estimation of the economic cost of recent sanctions on Iran using the synthetic control method. Economics Letters 157: 141–44. [Google Scholar] [CrossRef]

- Gholz, Eugene, and Llewelyn Hughes. 2019. Market structure and economic sanctions: The 2010 rare earth elements episode as a pathway case of market adjustment. Review of International Political Economy, 1–24. [Google Scholar] [CrossRef]

- Giumelli, Francesco. 2017. The redistributive impact of restrictive measures on EU members: Winners and losers from imposing sanctions on Russia. JCMS: Journal of Common Market Studies 55: 1062–80. [Google Scholar] [CrossRef]

- Gladkov, Igor S. 2016. European Union in modern international trade. Contemporary Europe-Sovremennaya Evropa 1: 85–94. [Google Scholar] [CrossRef]

- Góis, António R., Fernando P. Santos, Jorge M. Pacheco, and Francisco C. Santos. 2019. Reward and punishment in climate change dilemmas. Scientific Reports 9. [Google Scholar] [CrossRef]

- Golikova, Victoria, and Boris Kuznetsov. 2016. Perception of risks associated with economic sanctions: The case of Russian manufacturing. Post-Soviet Affairs 33: 49–62. [Google Scholar] [CrossRef]

- Gowa, Joanne, and Raymond Hicks. 2017. Commerce and conflict: New data about the Great War. British Journal of Political Science 47: 653–74. [Google Scholar] [CrossRef]

- Hamori, Shigeyuki. 2009. The sustainability of trade accounts of the G-7 countries. Applied Economics Letters 16: 1691–94. [Google Scholar] [CrossRef]

- He, Yaping, Pengfei Sheng, and Marek Vochozka. 2017. Pollution caused by finance and the relative policy analysis in China. Energy & Environment 28: 808–23. [Google Scholar] [CrossRef]

- Huang, Yi. 2020. International trade development and supply chain optimization of marine resources. Journal of Coastal Research 110: 183–87. [Google Scholar] [CrossRef]

- International Monetary Fund. 2020. Direction of Trade Statistics (DOTS). Available online: https://data.imf.org/?sk=9D6028D4-F14A-464C-A2F2-59B2CD424B85 (accessed on 20 September 2020).

- Jeong, Jin Mun. 2020. Economic sanctions and income inequality: Impacts of trade restrictions and foreign aid suspension on target countries. Conflict Management and Peace Science 37. [Google Scholar] [CrossRef]

- Kapustin, Nikita O., and Dmitry A. Grushevenko. 2019. A long-term outlook on Russian oil industry facing internal and external challenges. Oil & Gas Science and Technology—Revue d’IFP Energies Nouvelles 74. [Google Scholar] [CrossRef] [Green Version]

- Kholodilin, Konstantin A., and Aleksei Netšunajev. 2019. Crimea and punishment: The impact of sanctions on Russian economy and economies of the euro area. Baltic Journal of Economics 19: 39–51. [Google Scholar] [CrossRef]

- Kushniruk, Viktor, and Tetiana Ivanenko. 2017. Analysis of trends and prospects for development of export and import of goods and services by enterprises of Ukraine at the regional level. Baltic Journal of Economic Studies 3: 252–59. [Google Scholar] [CrossRef] [Green Version]

- Kwon, Jaebeom. 2020. Taming neighbors: Exploring China’s economic statecraft to change neighboring countries’ policies and their effects. Asian Perspective 44: 103–38. [Google Scholar] [CrossRef]

- Mau, Vladimir. 2016. Russia’s economic policy in 2015–2016: The imperative of structural reform. Post-Soviet Affairs 33: 63–83. [Google Scholar] [CrossRef]

- Mendoza, Ronald Umali, Charles Siriban, and Tea Jalin Ty. 2019. Survey of economic implications of maritime and territorial disputes. Journal of Economic Surveys 33: 1028–49. [Google Scholar] [CrossRef]

- Narayan, Paresh Kumar. 2006. Examining the relationship between trade balance and exchange rate: The case of China’s trade with the USA. Applied Economics Letters 13: 507–10. [Google Scholar] [CrossRef]

- Nasir, Muhammad Ali, Lutchmee Naidoo, Muhammad Shahbazb, and Nii Amoo. 2018. Implications of oil prices shocks for the major emerging economies: A comparative analysis of BRICS. Energy Economics 76: 76–88. [Google Scholar] [CrossRef]

- Neuenkirch, Matthias, and Florian Neumeier. 2016. The impact of US sanctions on poverty. Journal of Development Economics 121: 110–19. [Google Scholar] [CrossRef]

- Pak, Olga, and Gavin Lee Kretzschmar. 2016. Western sanctions—Only half the challenge to Russia’s economic union. Research in International Business and Finance 38: 577–92. [Google Scholar] [CrossRef]

- Røseth, Tom. 2017. Russia’s energy relations with China: Passing the strategic threshold? Eurasian Geography and Economics 58: 23–55. [Google Scholar] [CrossRef]

- Rousek, Pavel, and Jan Mareček. 2019. Use of neural networks for predicting development of USA export to China taking into account time series seasonality. Ad Alta: Journal of Interdisciplinary Research 9: 299–304. [Google Scholar]

- Rowland, Zuzana, Petr Šuleř, and Marek Vochozka. 2019. Comparison of neural networks and regression time series in estimating the Czech Republic and China trade balance. Paper presented at Innovative Economic Symposium 2018—Milestones and Trends of World Economy (IES2018), Beijing, China, 8–9 November 2018. [Google Scholar]

- Sadeh, Tal, and Nizan Feldman. 2020. Globalization and wartime trade. Cooperation and Conflict 55. [Google Scholar] [CrossRef]

- Scheidegger, Simon, and Ilias Bilionis. 2019. Machine learning for high-dimensional dynamic stochastic economies. Journal of Computational Science 33: 68–82. [Google Scholar] [CrossRef]

- Schmitz, Troy G. 2018. Impact of the Chinese embargo against MIR162 corn on Canadian corn producers. Canadian Journal of Agricultural Economics/Revue Canadienne D’agroeconomie 66: 571–86. [Google Scholar] [CrossRef]

- Seyfi, Siamak, and C. Michael Hall. 2019. Sanctions and tourism: Effects, complexities and research. Tourism Geographies, 1–19. [Google Scholar] [CrossRef]

- Shea, Patrick E., and Paul Poast. 2017. War and default. Journal of Conflict Resolution 62: 1876–904. [Google Scholar] [CrossRef]

- Shin, Geiguen, Seung-Whan Choi, and Shali Luo. 2016. Do economic sanctions impair target economies? International Political Science Review 37: 485–99. [Google Scholar] [CrossRef]

- Skalamera, Morena. 2018. Explaining the 2014 Sino–Russian gas breakthrough: The primacy of domestic politics. Europe-Asia Studies 70: 90–107. [Google Scholar] [CrossRef]

- Strange, Austin M., Axel Dreher, Andreas Fuchs, Bradley Parks, and Michael J. Tierney. 2017. Tracking underreported financial flows: China’s development finance and the aid—Conflict nexus revisited. Journal of Conflict Resolution 61: 935–63. [Google Scholar] [CrossRef] [Green Version]

- Šuleř, Petr, and Veronika Machová. 2020. Better results of artificial neural networks in predicting ČEZ share prices. Journal of International Studies 13: 259–78. [Google Scholar] [CrossRef]

- Talipova, Aminam, Sergei G. Parsegov, and Pavel Tukpetov. 2019. Russian gas exchange: A new indicator of market efficiency and competition or the instrument of monopolist? Energy Policy 135. [Google Scholar] [CrossRef]

- Tuzova, Yelena, and Faryal Qayum. 2016. Global oil glut and sanctions: The impact on Putin’s Russia. Energy Policy 90: 140–51. [Google Scholar] [CrossRef]

- Vochozka, Marek, and Veronika Machová. 2018. Determination of value drivers for transport companies in the Czech Republic. Nase More 65: 197–201. [Google Scholar] [CrossRef] [Green Version]

- Vochozka, Marek, and Jaromír Vrbka. 2019. Estimation of the development of the Euro to Chinese Yuan exchange rate using artificial neural networks. Paper presented at Innovative Economic Symposium 2018—Milestones and Trends of World Economy (IES2018), Beijing, China, 8–9 November 2018. [Google Scholar]

- Vochozka, Marek, Jakub Horák, and Petr Šuleř. 2019. Equalizing seasonal time series using artificial neural networks in predicting the Euro-Yuan exchange rate. Journal of Risk and Financial Management 12: 76. [Google Scholar] [CrossRef] [Green Version]

- Vochozka, Marek, Zuzana Rowland, Petr Šuleř, and Josef Maroušek. 2020a. The influence of the international price of oil on the value of the EUR/USD exchange rate. Journal of Competitiveness 12: 167–90. [Google Scholar] [CrossRef]

- Vochozka, Marek, Jaromír Vrbka, and Petr Šuleř. 2020b. Bankruptcy or success? The effective prediction of a company’s financial development using LSTM. Sustainability 12: 7529. [Google Scholar] [CrossRef]

- Vrbka, Jaromír, Zuzana Rowland, and Petr Šuleř. 2019. Comparison of neural networks and regression time series in estimating the development of the EU and the PRC trade balance. Paper presented at Innovative Economic Symposium 2018—Milestones and Trends of World Economy (IES2018), Beijing, China, 8–9 November 2018. [Google Scholar]

- Wang, Yiwei, Ke Wang, and Chun-Ping Chang. 2019. The impacts of economic sanctions on exchange rate volatility. Economic Modelling 82: 58–65. [Google Scholar] [CrossRef]

- Zhao, Yabo, Xiaofeng Liu, Shaojian Wang, and Yuejing Ge. 2019. Energy relations between China and the countries along the Belt and Road: An analysis of the distribution of energy resources and interdependence relationships. Renewable and Sustainable Energy Reviews 107: 133–44. [Google Scholar] [CrossRef]

| 1 | As shown below, one neuron will represent the continuous variable in the form of the year of the measurement, 12 neurons will represents the months in which the values were measured. |

| 2 | Least squares method will be used. Networks generating will be terminated if there is no improvement, that is, if the sum of squares is not reduced. We will thus retain only those neural structures whose sum of residual squares to the actual export of the RF to the PRC is as low as possible (zero in ideal case). |

| Samples | Year (Input) | Export (Target) | Import (Target) |

|---|---|---|---|

| Minimum (Train) | 1992.000 | 92.760 | 42.790 |

| Maximum (Train) | 2019.000 | 5860.110 | 5472.530 |

| Mean (Train) | 2005.504 | 1539.326 | 1821.468 |

| Standard deviation (Train) | 8.085 | 1358.751 | 1815.649 |

| Minimum (Test) | 1993.000 | 173.400 | 62.960 |

| Maximum (Test) | 2019.000 | 5028.780 | 4844.440 |

| Mean (Test) | 2005.880 | 1516.249 | 1741.595 |

| Standard deviation (Test) | 8.019 | 1320.065 | 1728.356 |

| Minimum (Validation) | 1992.000 | 145.860 | 44.730 |

| Maximum (Validation) | 2019.000 | 4473.790 | 5081.240 |

| Mean (Validation) | 2005.100 | 1439.480 | 1543.822 |

| Standard deviation (Validation) | 11.680 | 1193.594 | 1423.217 |

| Minimum (Overall) | 1992.000 | 92.760 | 42.790 |

| Maximum (Overall) | 2019.000 | 5860.110 | 5472.530 |

| Mean (Overall) | 2005.500 | 1521.034 | 1768.266 |

| Standard deviation (Overall) | 8.090 | 1349.768 | 1793.636 |

| Function | Definition | Range |

|---|---|---|

| Identity (Linear) | A | |

| Logistic sigmoid | (0; 1) | |

| Hyperbolic tangent | (−1; +1) | |

| Exponential | ||

| Sine |

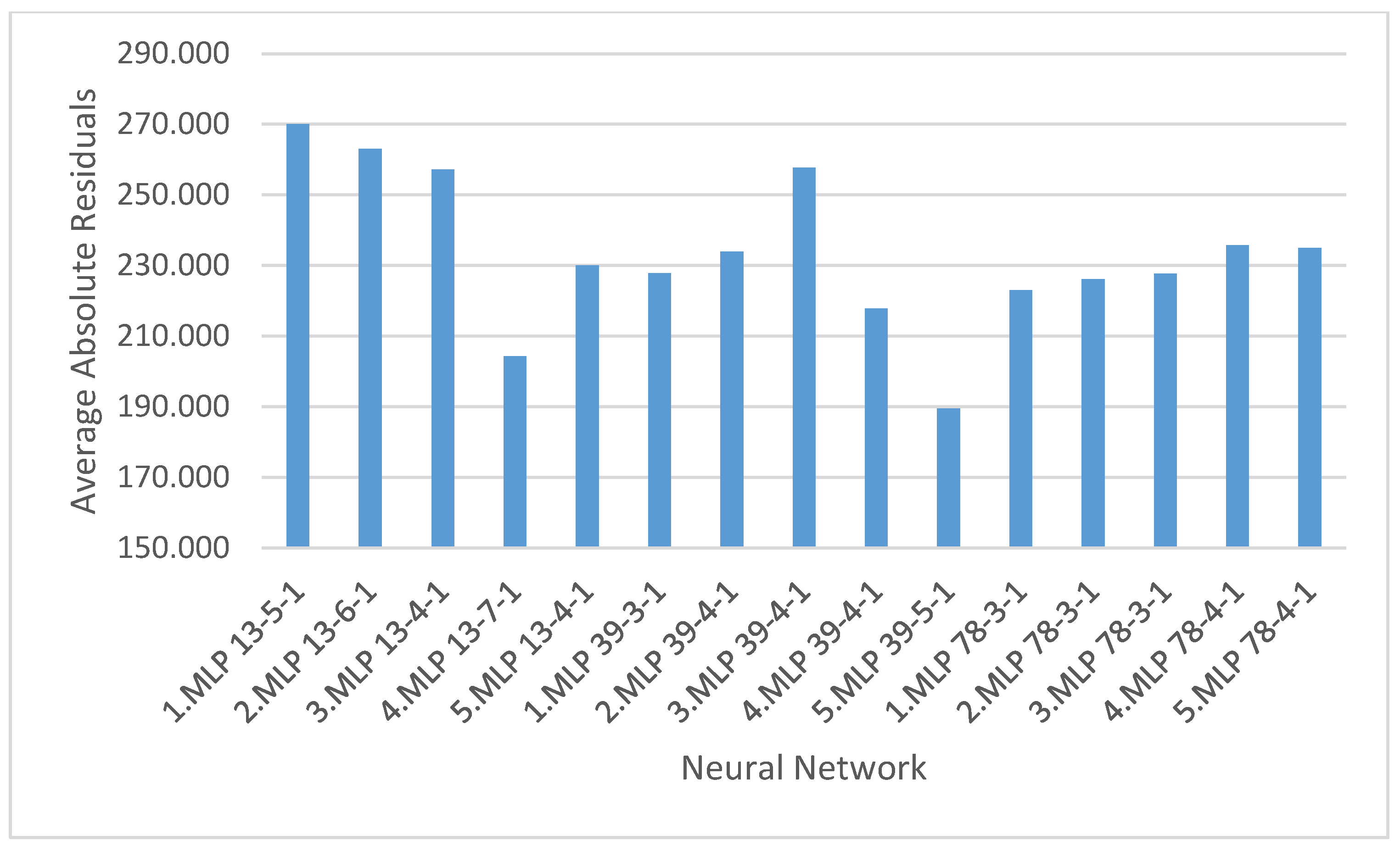

| Neural Network Equalizing the Export Time Series | Absolute Residuals | Average Absolute Residuals |

|---|---|---|

| 1.MLP 13-5-1 | 90,463.533 | 270.040 |

| 2.MLP 13-6-1 | 88,100.067 | 262.985 |

| 3.MLP 13-4-1 | 86,168.063 | 257.218 |

| 4.MLP 13-7-1 | 68,463.937 | 204.370 |

| 5.MLP 13-4-1 | 77,062.563 | 230.038 |

| 1.MLP 39-3-1 | 75,867.255 | 227.830 |

| 2.MLP 39-4-1 | 77,909.645 | 233.963 |

| 3.MLP 39-4-1 | 85,808.995 | 257.685 |

| 4.MLP 39-4-1 | 72,553.107 | 217.877 |

| 5.MLP 39-5-1 | 63,135.839 | 189.597 |

| 1.MLP 78-3-1 | 73,588.614 | 222.996 |

| 2.MLP 78-3-1 | 74,619.158 | 226.119 |

| 3.MLP 78-3-1 | 75,161.585 | 227.762 |

| 4.MLP 78-4-1 | 77,786.433 | 235.716 |

| 5.MLP 78-4-1 | 77,536.134 | 234.958 |

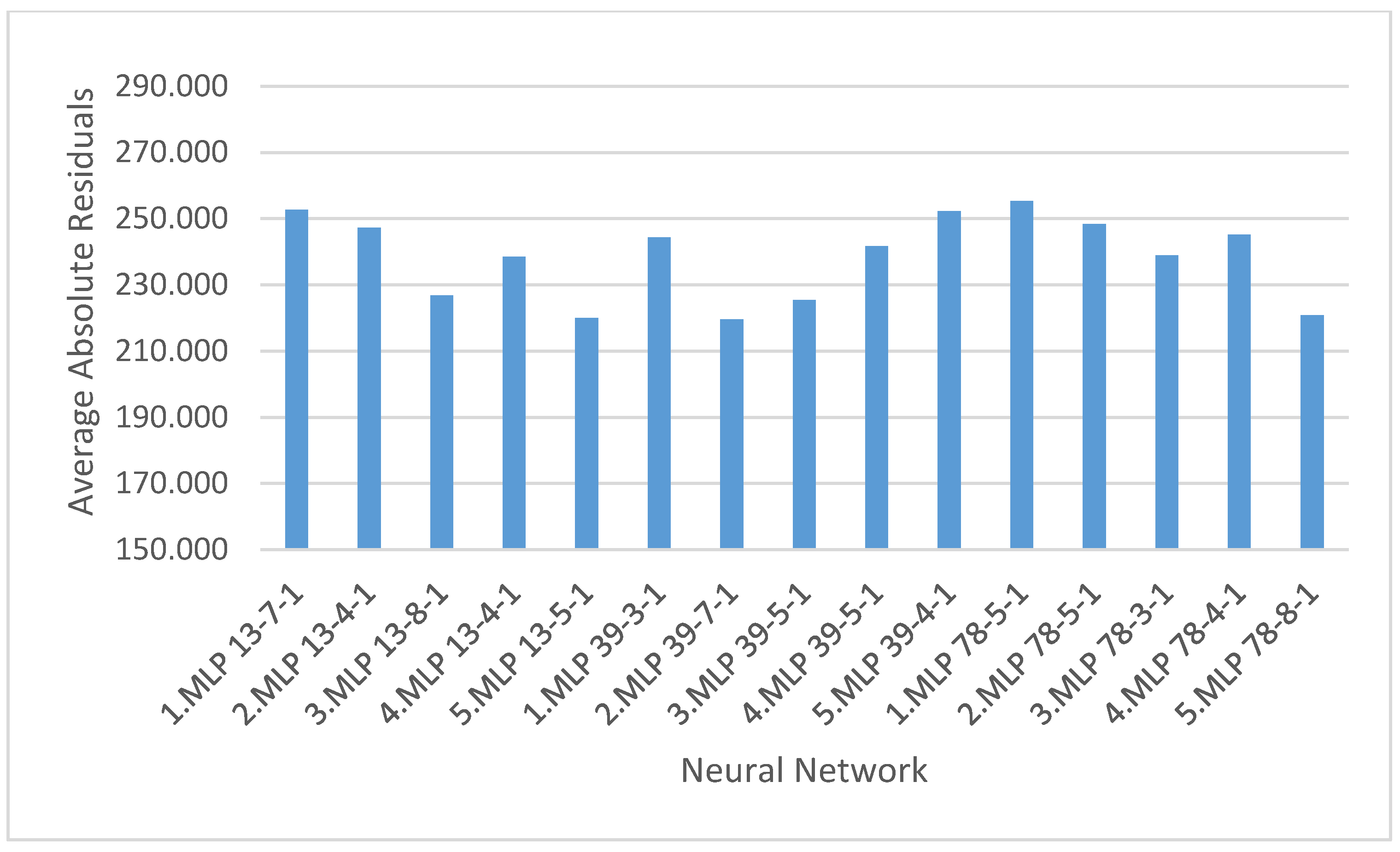

| Neural Network Equalizing the Export Time Series | Absolute Residuals | Average Absolute Residuals |

|---|---|---|

| 1.MLP 13-7-1 | 84,659.737 | 252.716 |

| 2.MLP 13-4-1 | 82,844.840 | 247.298 |

| 3.MLP 13-8-1 | 75,969.699 | 226.775 |

| 4.MLP 13-4-1 | 79,909.030 | 238.534 |

| 5.MLP 13-5-1 | 73,711.346 | 220.034 |

| 1.MLP 39-3-1 | 81,368.085 | 244.349 |

| 2.MLP 39-7-1 | 73,128.771 | 219.606 |

| 3.MLP 39-5-1 | 75,067.048 | 225.427 |

| 4.MLP 39-5-1 | 80,507.543 | 241.764 |

| 5.MLP 39-4-1 | 84,015.830 | 252.300 |

| 1.MLP 78-5-1 | 84,270.077 | 255.364 |

| 2.MLP 78-5-1 | 81,965.733 | 248.381 |

| 3.MLP 78-3-1 | 78,856.170 | 238.958 |

| 4.MLP 78-4-1 | 80,889.255 | 245.119 |

| 5.MLP 78-8-1 | 72,859.601 | 220.787 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Horak, J. Sanctions as a Catalyst for Russia’s and China’s Balance of Trade: Business Opportunity. J. Risk Financial Manag. 2021, 14, 36. https://doi.org/10.3390/jrfm14010036

Horak J. Sanctions as a Catalyst for Russia’s and China’s Balance of Trade: Business Opportunity. Journal of Risk and Financial Management. 2021; 14(1):36. https://doi.org/10.3390/jrfm14010036

Chicago/Turabian StyleHorak, Jakub. 2021. "Sanctions as a Catalyst for Russia’s and China’s Balance of Trade: Business Opportunity" Journal of Risk and Financial Management 14, no. 1: 36. https://doi.org/10.3390/jrfm14010036

APA StyleHorak, J. (2021). Sanctions as a Catalyst for Russia’s and China’s Balance of Trade: Business Opportunity. Journal of Risk and Financial Management, 14(1), 36. https://doi.org/10.3390/jrfm14010036