Volatility Spillover Dynamics between Large-, Mid-, and Small-Cap Stocks in the Time-Frequency Domain: Implications for Portfolio Management

,

,

Abstract

:1. Introduction

2. Literature Review

3. Methodology and Data Specification

3.1. Diebold and Yilmaz Model

3.2. Baruník and Krehlik Model

4. Data Description

5. Empirical Results and Discussions

5.1. Static Analysis of Volatility Spillover

5.1.1. Total Volatility Spillover

5.1.2. Net Volatility Spillover

5.1.3. Pairwise Net Volatility Spillover

5.2. Dynamic Volatility of Spillover Analysis

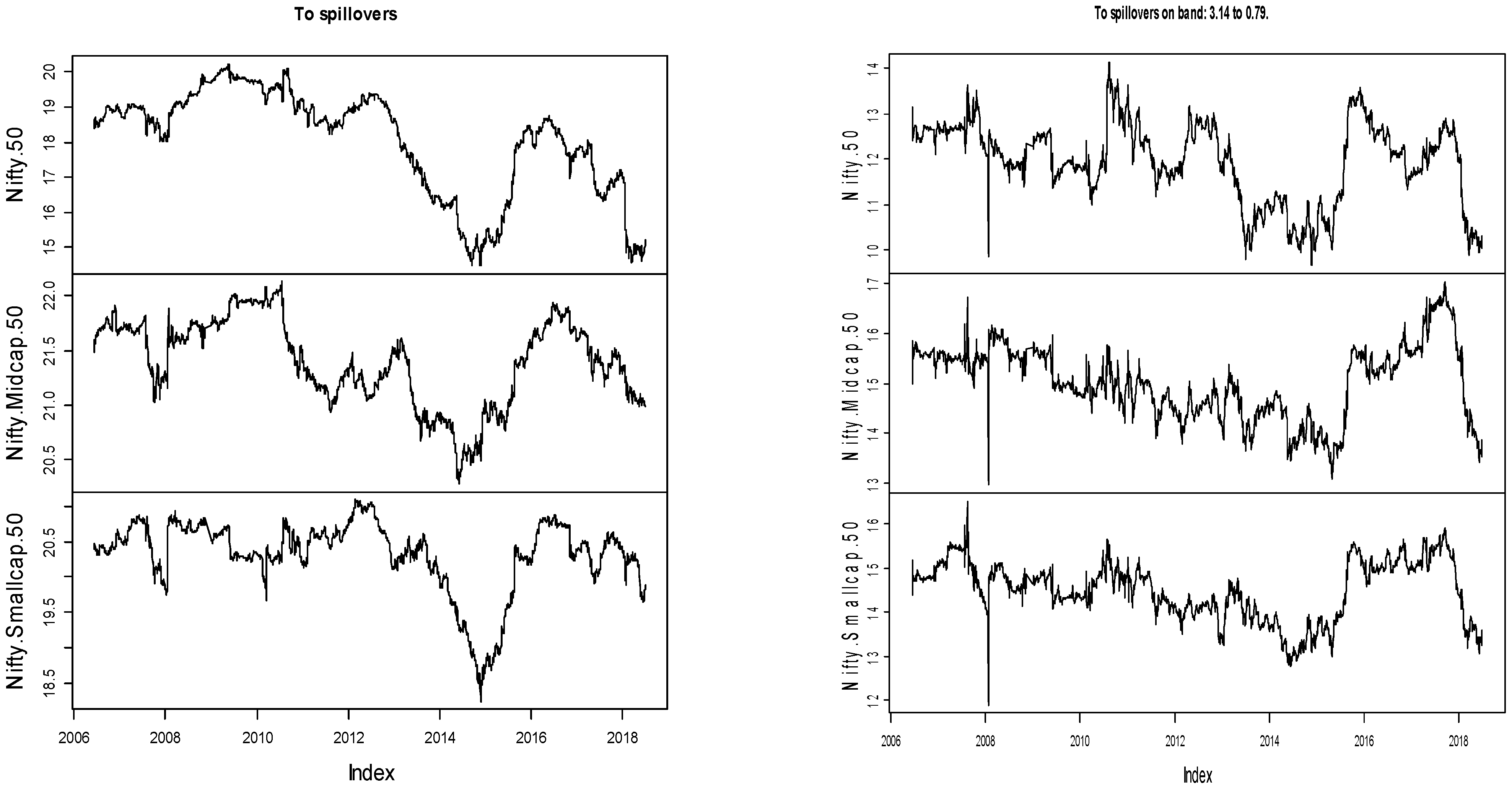

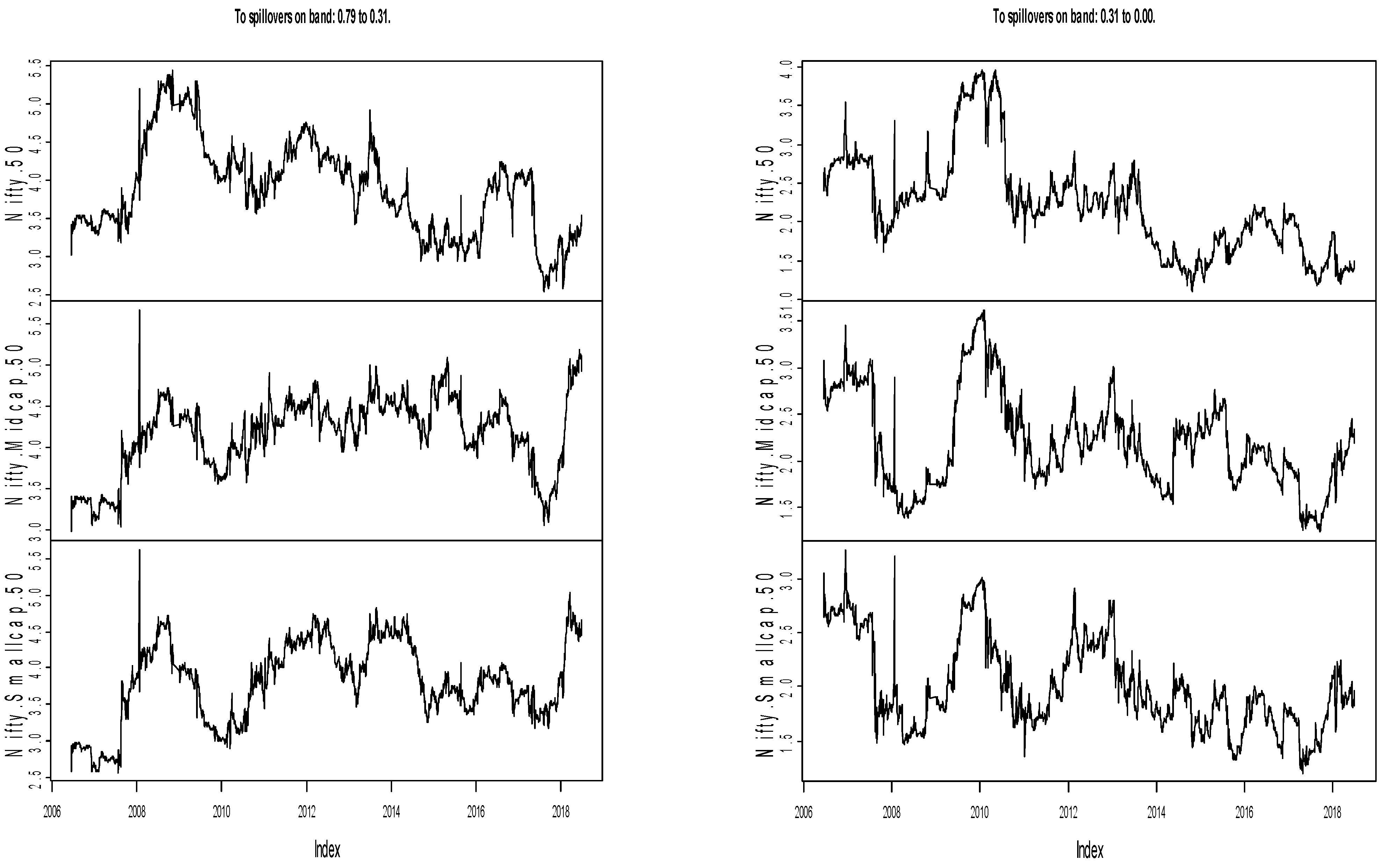

5.2.1. Rolling Total Volatility Spillover

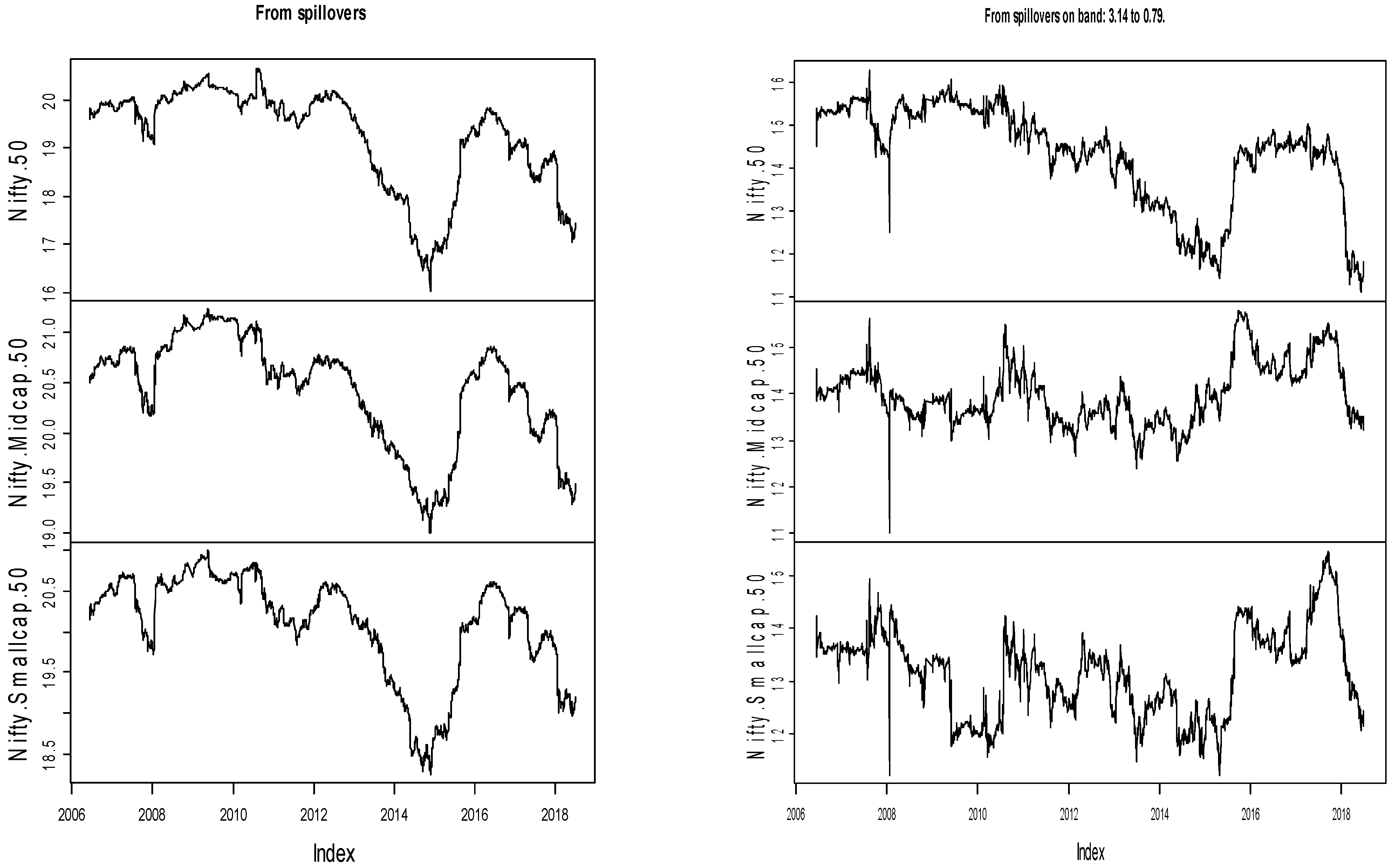

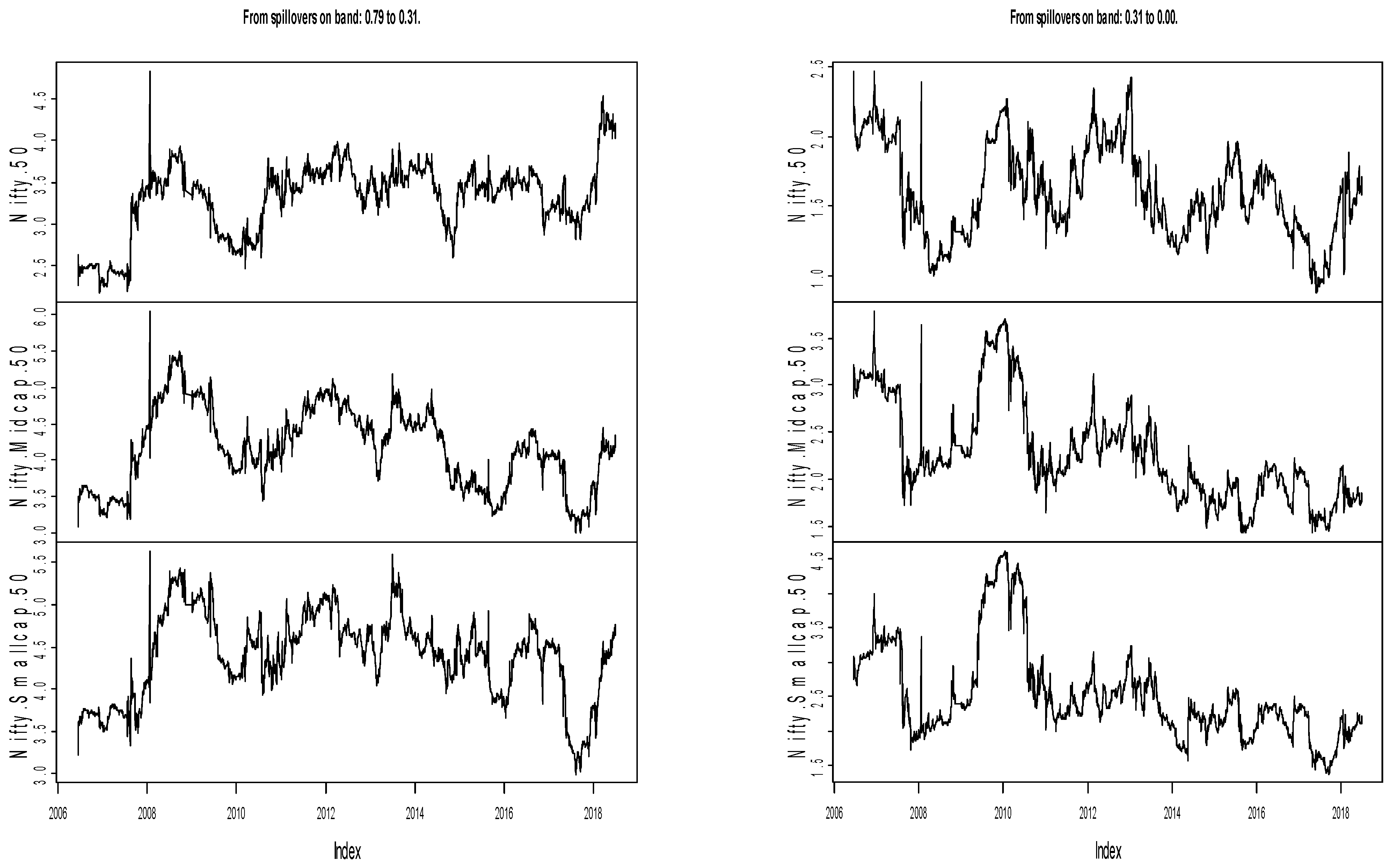

5.2.2. Rolling Net Volatility Spillover

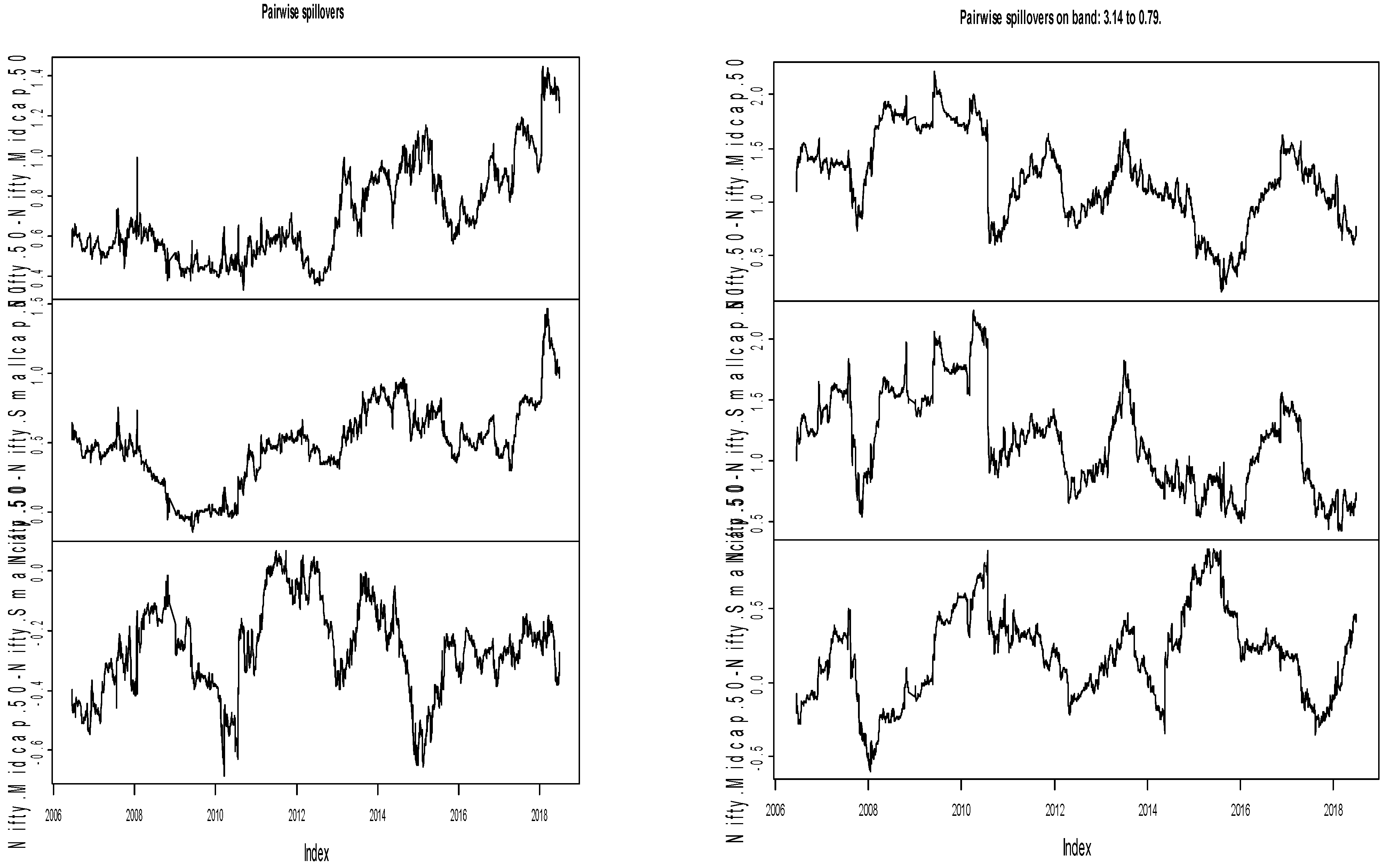

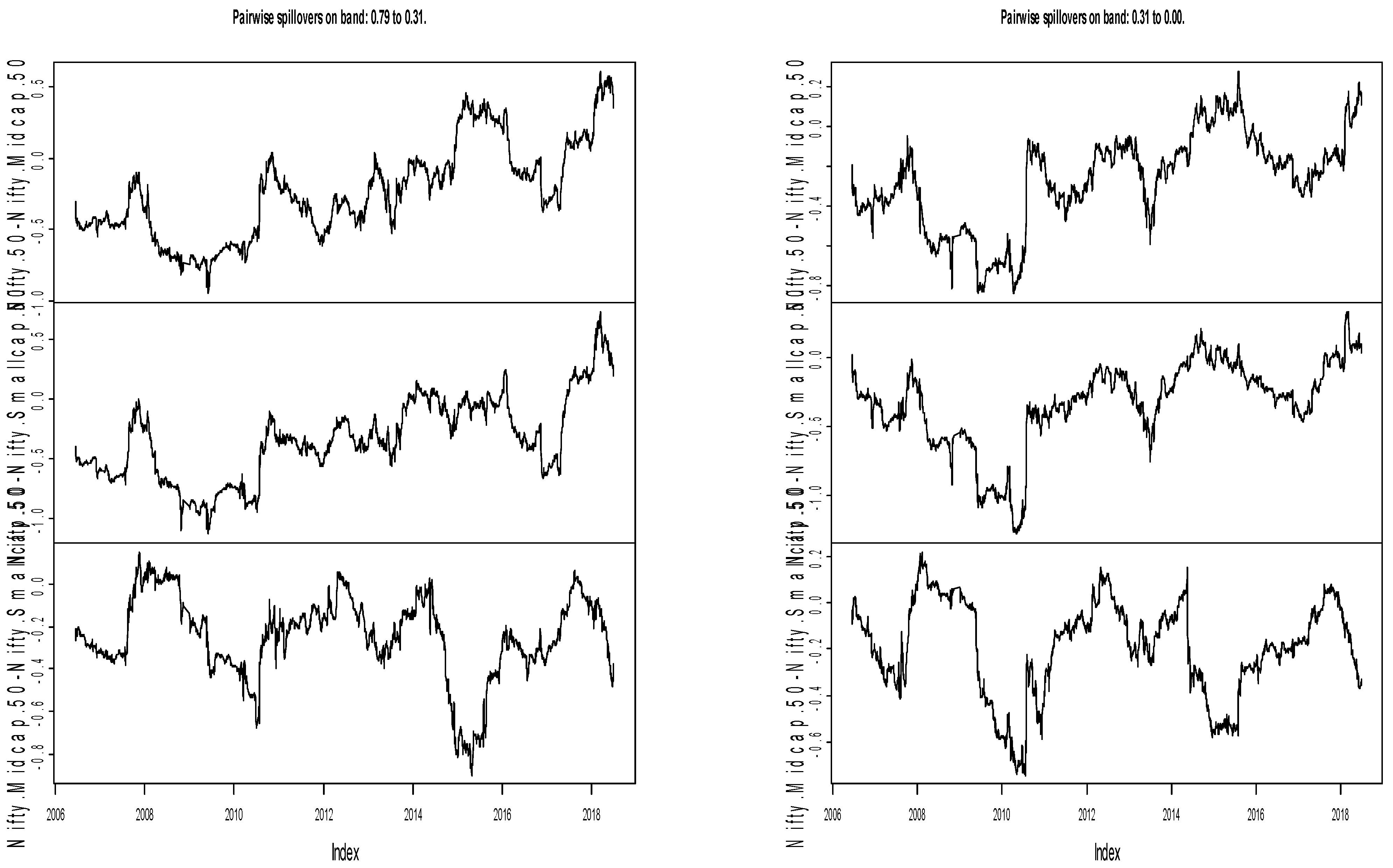

5.2.3. Rolling Pairwise Net Volatility Spillover

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

| 1 | Vide the circular SEBI/HO/IMD/DF3/CIR/P/2017/114, the Securities and Exchange Board of India (SEBI) defines large-, mid-, and small-cap stocks as the 1st–100th, 101st–250th companies, and the 251st company onwards, respectively, in terms of full market capitalization. |

| 2 | |

| 3 | In terms of dollar-adjusted performance, India has been the most consistent performer, and an important destination for investment for foreign investors. It has been ranked third among the top twenty most followed global indices in terms of 1-year, 2-year, 3-year, and 4-year performances, i.e., a return of 6%, 20%, 42%, and 21%, respectively. In terms of the 5-year and 10-year performances, it has been ranked second and fifth, with a return of 53% and 150%, respectively (source: Bloomberg) ET: 17 April 2019. |

| 4 | The BDS test of nonlinearity (Broock et al. 1996) is applied on the residual of a regression estimate in a bilateral context. The results are available upon request. |

| 5 | The total pairwise connectedness is obtained for the example in the case of the mid- and small-caps by summing up the volatility crossover in both directions, i.e., 34.06 plus 33. |

| 6 | The union government was formed by the Bhartiya Janata Party (BJP) with an absolute majority in the Parliament. |

References

- Asli, Ascioglu. 2014. US small-cap indexes: An empirical analysis of factor exposure and return. The Journal of Index Investing 5: 21–32. [Google Scholar] [CrossRef]

- Bai, Ye, and Christopher J. Green. 2010. International diversification strategies: Revisited from the risk perspective. Journal of Banking and Finance 34: 236–45. [Google Scholar] [CrossRef]

- Bai, Jushan, and Pierre Perron. 2003. Computation and analysis of multiple structural change models. Journal of Applied Econometrics 18: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Baruník, Jozef, and Tomáš Krehlik. 2018. Measuring the frequency dynamics of financial connectedness and systemic risk. Journal of Financial Econometrics 16: 271–96. [Google Scholar] [CrossRef]

- Baruník, Jozef, Evžen Kočenda, and Lukáš Vácha. 2016a. Asymmetric connectedness on the US stock market: Bad and good volatility spillovers. Journal of Financial Markets 27: 55–78. [Google Scholar] [CrossRef]

- Baruník, Jozef, Evžen Kočenda, and Lukáš Vácha. 2016b. Gold, oil, and stocks: Dynamic correlations. International Review of Economics and Finance 42: 186–201. [Google Scholar] [CrossRef] [Green Version]

- Baur, Dirk G., and Brian M. Lucey. 2009. Flights and contagion—An empirical analysis of stock–bond correlations. Journal of Financial Stability 5: 339–52. [Google Scholar] [CrossRef]

- Beirne, John, Maria Caporale Guglielmo, Schulze-Ghattas Marianne, and Spagnolo Nicola. 2013. Volatility spillovers and contagion from mature to emerging stock markets. Review of International Economics 21: 1060–75. [Google Scholar] [CrossRef] [Green Version]

- Broock, William A., José Alexandre Scheinkman, W. Davis Dechert, and Blake LeBaron. 1996. A test for independence based on the correlation dimension. Econometric Reviews 15: 197–235. [Google Scholar] [CrossRef]

- Carrieri, Francesca, Vihang Errunza, and Sergei Sarkissian. 2004. Industry risk and market integration. Management Science 50: 207–21. [Google Scholar] [CrossRef]

- Copeland, Maggie, and Thomas Copeland. 2016. VIX versus Size. The Journal of Portfolio Management 42: 76–83. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2009. Measuring financial asset return and volatility spillovers, with application to global equity markets. The Economic Journal 119: 158–71. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef] [Green Version]

- Elias, Christopher J. 2016. Asset pricing with expectation shocks. Journal of Economic Dynamics and Control 65: 68–82. [Google Scholar] [CrossRef]

- Eun, Cheol S., Wei Huang, and Sandy Lai. 2008. International diversification with large-and small-cap stocks. Journal of Financial and Quantitative Analysis 43: 489–524. [Google Scholar] [CrossRef] [Green Version]

- Ferrer, Román, Syed Jawad Hussain Shahzad, Raquel López, and Francisco Jareño. 2018. Time and frequency dynamics of connectedness between renewable energy stocks and crude oil prices. Energy Economics 76: 1–20. [Google Scholar] [CrossRef]

- Fleming, Jeff, Chris Kirby, and Barbara Ostdiek. 1998. Information and volatility linkages in the stock, bond, and money markets. Journal of Financial Economics 49: 111–37. [Google Scholar] [CrossRef]

- Gorman, Larry. 2003. Conditional performance, portfolio rebalancing, and momentum of small-cap mutual funds. Review of Financial Economics 12: 287–300. [Google Scholar] [CrossRef]

- Huang, Wei. 2007. Financial integration and the price of world covariance risk: Large-vs small-cap stocks. Journal of International Money and Finance 26: 1311–37. [Google Scholar] [CrossRef]

- Kim, Moon K., and David A. Burnie. 2002. The firm size effect and the economic cycle. Journal of Financial Research 25: 111–24. [Google Scholar] [CrossRef]

- Koop, Gary, M. Hashem Pesaran, and Simon M. Potter. 1996. Impulse response analysis in nonlinear multivariate models. Journal of Econometrics 74: 119–47. [Google Scholar] [CrossRef]

- Kumar, Gaurav, and Arun Kumar Misra. 2018. Commonality in liquidity: Evidence from India’s national stock exchange. Journal of Asian Economics 59: 1–15. [Google Scholar] [CrossRef]

- Li, Lingfeng. 2002. Macroeconomic Factors and the Correlation of Stock and Bond Returns. Yale ICF Working Paper. New Haven: Yale International Centre for Finance, Department of Economics, Yale University, pp. 2–46. Available online: https://ssrn.com/abstract=363641 (accessed on 10 December 2018).

- Li, Yanan, and David E. Giles. 2015. Modelling volatility spillover effects between developed stock markets and Asian emerging stock markets. International Journal of Finance and Economics 20: 155–77. [Google Scholar] [CrossRef] [Green Version]

- Lin, Pin-Te. 2013. Examining volatility spillover in Asian REIT markets. Applied Financial Economics 23: 1701–5. [Google Scholar] [CrossRef]

- Maghyereh, Aktham I., Hussein Abdoh, and Basel Awartani. 2019. Connectedness and hedging between gold and Islamic securities: A new evidence from time-frequency domain approaches. Pacific-Basin Finance Journal 54: 13–28. [Google Scholar] [CrossRef]

- Mayer, Jörg. 2009. The Growing Interdependence between Financial and Commodity Markets (No. 195). Geneva: United Nations Conference on Trade and Development. [Google Scholar]

- Mensi, Walid, Mobeen Ur Rehman, and Xuan Vinh Vo. 2020. Spillovers and co-movements between precious metals and energy markets: Implications on portfolio management. Resources Policy 69: 101836. [Google Scholar] [CrossRef]

- Moreira, Alan, and Tyler Muir. 2017. Volatility-Managed Portfolios. The Journal of Finance 72: 1611–44. [Google Scholar] [CrossRef]

- Moreira, Alan, and Tyler Muir. 2019. Should Long-Term Investors Time Volatility? Journal of Financial Economics 131: 507–27. [Google Scholar] [CrossRef]

- Müller, Ulrich A., Michel M. Dacorogna, Rakhal D. Davé, Richard B. Olsen, Olivier V. Pictet, and Jacob E. Von Weizsäcker. 1997. Volatilities of different time resolutions—analyzing the dynamics of market components. Journal of Empirical Finance 4: 213–39. [Google Scholar]

- Oberholzer, Niel, and Sven T. von Boetticher. 2015. Volatility spill-over between the JSE/FTSE indices and the South African Rand. Procedia Economics and Finance 24: 501–10. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, H. Hashem, and Yongcheol Shin. 1998. Generalized impulse response analysis in linear multivariate models. Economics Letters 58: 17–29. [Google Scholar] [CrossRef]

- Reinganum, Marc R. 1999. The significance of market capitalization in portfolio management over time. The Journal of Portfolio Management 25: 39–50. [Google Scholar] [CrossRef]

- Semenov, Andrei. 2015. The small-cap effect in the predictability of individual stock returns. International Review of Economics and Finance 38: 178–97. [Google Scholar] [CrossRef]

- Sensoy, Ahmet. 2017. Firm size, ownership structure, and systematic liquidity risk: The case of an emerging market. Journal of Financial Stability 31: 62–80. [Google Scholar] [CrossRef]

- Siegel, Jeremy J. 2021. Stocks for the Long Run: The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies. New York: McGraw-Hill Education. [Google Scholar]

- Switzer, Lorne N. 2010. The behaviour of small cap vs. large cap stocks in recessions and recoveries: Empirical evidence for the United States and Canada. The North American Journal of Economics and Finance 21: 332–46. [Google Scholar] [CrossRef]

- Switzer, Lorne N., and Mingjun Tang. 2009. The Impact of Corporate Governance on the Performance of US Small-Cap Firms. International Journal of Business 14: 341–55. [Google Scholar]

- Tiwari, Aviral Kumar, Juncal Cunado, Rangan Gupta, and Mark E. Wohar. 2018. Volatility spillovers across global asset classes: Evidence from time and frequency domains. The Quarterly Review of Economics and Finance 70: 194–202. [Google Scholar] [CrossRef]

- Underwood, Shane. 2009. The cross-market information content of stock and bond order flow. Journal of Financial Markets 12: 268–89. [Google Scholar] [CrossRef]

- Wang, Xunxiao, and Yudong Wang. 2019. Volatility spillovers between crude oil and Chinese sectoral equity markets: Evidence from a frequency dynamics perspective. Energy Economics 80: 995–1009. [Google Scholar] [CrossRef]

- Wang, Jun, Robert Brooks, Xing Lu, and Hunter M. Holzhauer. 2014. Growth/Value, Market Cap, and Momentum. The Journal of Investing 23: 33–42. [Google Scholar] [CrossRef]

- Zhang, Dayong, and David C. Broadstock. 2018. Global financial crisis and rising connectedness in the international commodity markets. International Review of Financial Analysis 68: 101239. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Nifty.50 (Large-Cap) | Nifty.Midcap.50 (Mid-Cap) | Nifty.Smallcap.50 (Small-Cap) | |

|---|---|---|---|

| Panel A: descriptive statistics | |||

| Mean | 0.001 | 0.000 | 0.000 |

| Median | 0.001 | 0.002 | 0.002 |

| Maximum | 0.163 | 0.131 | 0.107 |

| Minimum | −0.130 | −0.162 | −0.138 |

| Std. Dev. | 0.014 | 0.017 | 0.017 |

| Skewness | −0.051 | −0.725 | −0.965 |

| Kurtosis | 13.523 | 10.674 | 9.953 |

| Jarque-Bera | 15,172.320 | 8358.190 | 7135.885 |

| Probability | 0.000 *** | 0.000 *** | 0.000 *** |

| Observations | 3288 | 3288 | 3288 |

| ADF t-statistic | −53.937 | −50.372 | −48.014 |

| (0.000 ***) | (0.000 ***) | (0.000 ***) | |

| Zivot-Andrews t-statistic | −54.032 | −28.629 | −27.113 |

| (0.011 **) | (0.002 ***) | (0.001 ***) | |

| UDMax F statistic | Large-mid | Large-small | Mid-small |

| 106.13 ** | 92.79 ** | 48.02 ** | |

| Panel B: Unconditional correlation matrix | |||

| Large-cap | 1 | ||

| Mid-cap | 0.847 | 1 | |

| (91.258 ***) | |||

| Small-cap | 0.785 | 0.917 | 1 |

| (72.610 ***) | (131.795 ***) | ||

| Panel A: Diebold and Yilmaz (2012) volatility spillover matrix between Nifty.50 (Large-cap), Nifty. Midcap.50 (Mid-cap), and Nifty.Smallcap.50 (Small-cap) indices | |||||

| Nifty.50 | Nifty.Midcap.50 | Nifty.Smallcap.50 | FROM | ||

| Nifty.50 | 42.04 | 30.62 | 27.34 | 19.32 | |

| Nifty.Midcap.50 | 28.51 | 38.49 | 33 | 20.5 | |

| Nifty.Smallcap.50 | 26.26 | 34.06 | 39.68 | 20.11 | |

| TO | 18.26 | 21.56 | 20.11 | 59.93 | |

| Panel B: Baruník and Krehlik (2018) volatility spillover matrix between Nifty.50 (Large-cap), Nifty. Midcap.50 (Mid-cap), and Nifty.Smallcap.50 (Small-cap) indices | |||||

| Freq1: 3.14 to 0.79 (corresponds to 1 to 4 days) | |||||

| Nifty.50 | Nifty.Midcap.50 | Nifty.Smallcap.50 | FROM_ABS | FROM_WTH | |

| Nifty.50 | 30.93 | 23.06 | 20.38 | 14.48 | 21.06 |

| Nifty.Midcap.50 | 18.64 | 26.48 | 22.41 | 13.68 | 19.9 |

| Nifty.Smallcap.50 | 16.48 | 22.03 | 25.83 | 12.84 | 18.67 |

| TO_ABS | 11.71 | 15.03 | 14.26 | 41 | |

| TO_WTH | 17.03 | 21.86 | 20.75 | ||

| Freq2: 0.79 to 0.31 (corresponds to 4 to 10 days) | |||||

| Nifty.50 | Nifty.Midcap.50 | Nifty.Smallcap.50 | FROM_ABS | FROM_WTH | |

| Nifty.50 | 7.4 | 5.11 | 4.52 | 3.21 | 16.08 |

| Nifty.Midcap.50 | 6.29 | 7.81 | 6.7 | 4.33 | 21.67 |

| Nifty.Smallcap.50 | 6.02 | 7.55 | 8.53 | 4.53 | 22.65 |

| TO_ABS | 4.1 | 4.22 | 3.74 | 12.07 | |

| TO_WTH | 20.54 | 21.14 | 18.72 | ||

| Freq3: 0.31 to 0.0 (corresponds to more than 10 days) | |||||

| Nifty.50 | Nifty.Midcap.50 | Nifty.Smallcap.50 | FROM_ABS | FROM_WTH | |

| Nifty.50 | 3.71 | 2.44 | 2.44 | 1.63 | 14.44 |

| Nifty.Midcap.50 | 3.58 | 4.19 | 3.89 | 2.49 | 22.1 |

| Nifty.Smallcap.50 | 3.76 | 4.47 | 5.33 | 2.74 | 24.35 |

| TO_ABS | 2.45 | 2.31 | 2.11 | 6.86 | |

| TO_WTH | 21.72 | 20.46 | 18.72 | ||

| Nifty.50 | Nifty.Midcap.50 | Nifty.Smallcap.50 | |

|---|---|---|---|

| Panel A: Overall Diebold and Yilmaz (2012) | −1.06 | 1.05 | 0.01 |

| Panel B: Frequency domain Baruník and Krehlik (2018) | |||

| Freq. 1 | −2.77 | 1.35 | 1.43 |

| Freq. 2 | 0.89 | −0.11 | −0.79 |

| Freq. 3 | 0.82 | −0.19 | −0.63 |

| Pairwise | Pairwise Total | |||||

|---|---|---|---|---|---|---|

| Large-Mid | Large-Small | Mid-Small | Large-Mid | Large-Small | Mid-Small | |

| Overall DY (2012) | −2.11 | −1.08 | 1.06 | 59.13 | 53.6 | 67.06 |

| Frequency domain BK (2018) | ||||||

| Freq. 1 | −4.42 | −3.9 | −0.38 | 41.7 | 36.86 | 44.44 |

| Freq. 2 | 1.18 | 1.5 | 0.85 | 11.4 | 10.54 | 14.25 |

| Freq. 3 | 1.14 | 1.32 | 0.58 | 6.02 | 6.2 | 8.36 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jena, S.K.; Tiwari, A.K.; Dash, A.; Aikins Abakah, E.J. Volatility Spillover Dynamics between Large-, Mid-, and Small-Cap Stocks in the Time-Frequency Domain: Implications for Portfolio Management. J. Risk Financial Manag. 2021, 14, 531. https://doi.org/10.3390/jrfm14110531

Jena SK, Tiwari AK, Dash A, Aikins Abakah EJ. Volatility Spillover Dynamics between Large-, Mid-, and Small-Cap Stocks in the Time-Frequency Domain: Implications for Portfolio Management. Journal of Risk and Financial Management. 2021; 14(11):531. https://doi.org/10.3390/jrfm14110531

Chicago/Turabian StyleJena, Sangram Keshari, Aviral Kumar Tiwari, Ashutosh Dash, and Emmanuel Joel Aikins Abakah. 2021. "Volatility Spillover Dynamics between Large-, Mid-, and Small-Cap Stocks in the Time-Frequency Domain: Implications for Portfolio Management" Journal of Risk and Financial Management 14, no. 11: 531. https://doi.org/10.3390/jrfm14110531

APA StyleJena, S. K., Tiwari, A. K., Dash, A., & Aikins Abakah, E. J. (2021). Volatility Spillover Dynamics between Large-, Mid-, and Small-Cap Stocks in the Time-Frequency Domain: Implications for Portfolio Management. Journal of Risk and Financial Management, 14(11), 531. https://doi.org/10.3390/jrfm14110531