Corporate Governance from a Cross-Country Perspective and a Comparison with Romania

Abstract

:1. Introduction

2. Data and Research Methods

3. Results

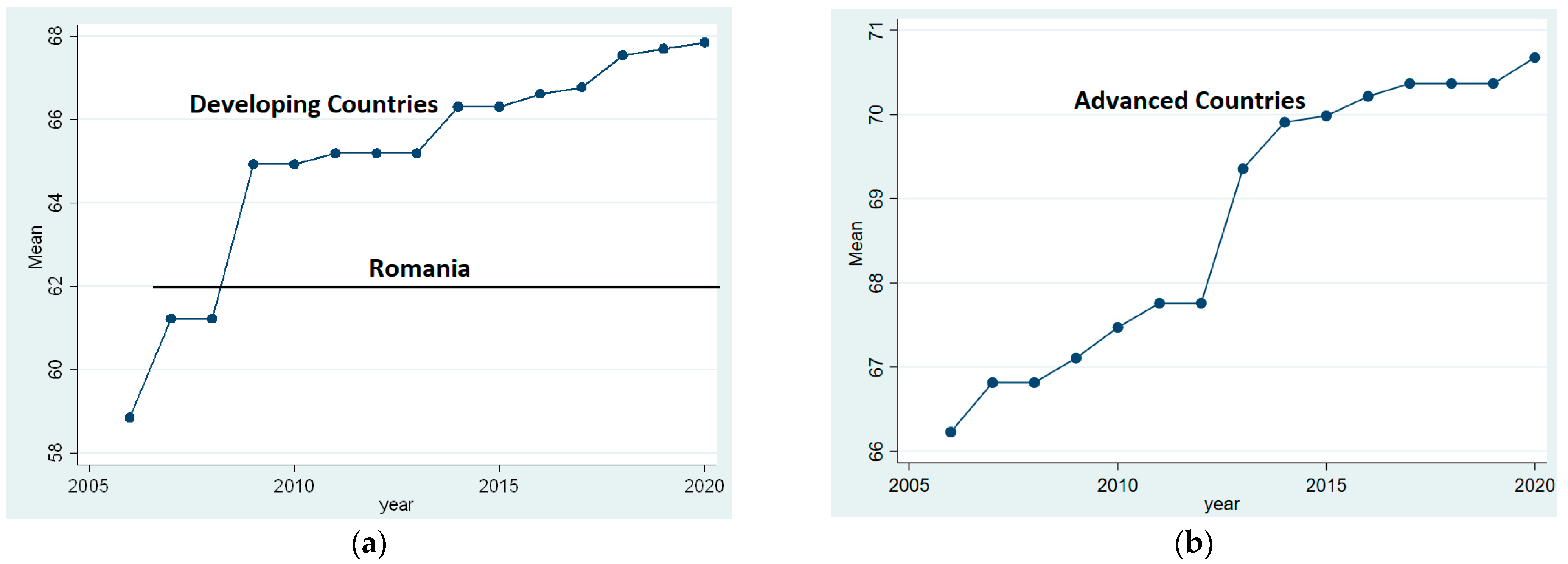

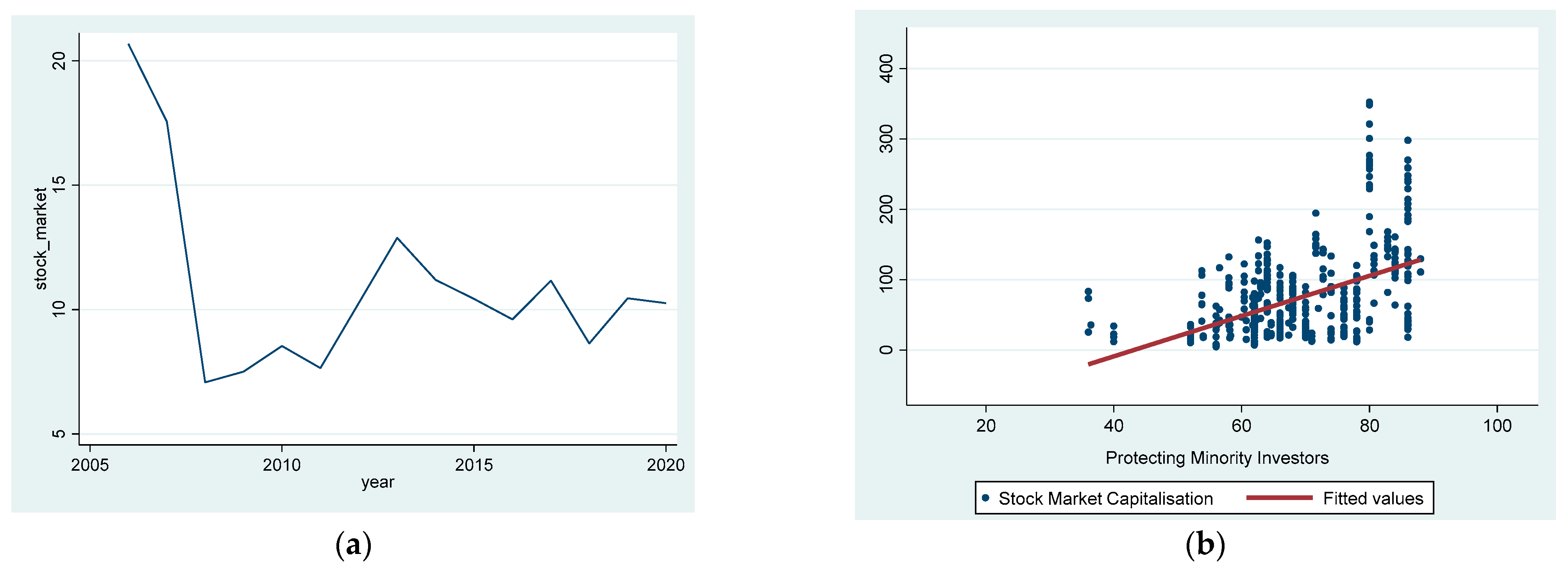

3.1. Descriptive Analysis

3.2. Regression Analysis

4. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Aggarwal, Reena, Isil Erel, René M. Stulz, and Rohan Williamson. 2007. Do US Firms Have the Best Corporate Governance? A Cross-Country Examination of the Relation between Corporate Governance and Shareholder Wealth. Fisher College of Business Working Paper No. 2006-03-006, ECGI - Finance Working Paper No. 145/2007, Charles A. Dice Center Working Paper No. 2006-25. Available online: https://ssrn.com/abstract=954169 (accessed on 15 October 2021). [CrossRef] [Green Version]

- Aguilera, Ruth V., and Gregory Jackson. 2010. Comparative and international corporate governance. Academy of Management Annals 4: 485–556. [Google Scholar] [CrossRef]

- Badulescu, Alina. 2008. Corporate Governance In Romania (II-Considerations On Romania’s Compliance On OECD Principles On Corporate Governance). Annals of Faculty of Economics 2: 571–75. [Google Scholar]

- Baker, C. Richard, and Dwight M. Owsen. 2002. Increasing the role of auditing in corporate governance. Critical Perspectives on Accounting 13: 783–95. [Google Scholar] [CrossRef]

- Barro, Robert J. 1991. Economic growth in a cross section of countries. The Quarterly Journal of Economics 106: 407–43. [Google Scholar] [CrossRef] [Green Version]

- Barro, Robert J. 2003. Determinants of economic growth in a panel of countries. Annals of Economics and Finance 4: 231–74. [Google Scholar]

- Basco, Rodrigo, Giovanna Campopiano, Andrea Calabrò, and Sascha Kraus. 2019. They are not all the same! Investigating the effect of executive versus non-executive family board members on firm performance. Journal of Small Business Management 57: 637–57. [Google Scholar] [CrossRef]

- Bebchuk, Lucian, Alma Cohen, and Allen Ferrell. 2009. What matters in corporate governance? The Review of Financial Studies 22: 783–827. [Google Scholar] [CrossRef] [Green Version]

- Becht, Marco, Patrick Bolton, and Ailsa Röell. 2003. Corporate governance and control. Handbook of the Economics of Finance 1: 1–109. [Google Scholar]

- Belloc, Filippo. 2012. Corporate governance and inovation: A survey. Journal of Economic Surveys 26: 835–64. [Google Scholar] [CrossRef]

- Bhagat, Sanjai, and Brian Bolton. 2008. Corporate governance and firm performance. Journal of Corporate Finance 14: 257–73. [Google Scholar] [CrossRef]

- Bhagat, Sanjai, and Brian Bolton. 2019. Corporate governance and firm performance: The sequel. Journal of Corporate Finance 58: 142–68. [Google Scholar] [CrossRef]

- Buşu, Mihail. 2015. Corporate Governance Codes in Romania and European Union Countries. Revista de Management Comparat International 16: 119–28. [Google Scholar]

- Cavaco, Sandra, Patricia Crifo, Antoine Rebérioux, and Gwenael Roudaut. 2017. Independent directors: Less informed but better selected than affiliated board members? Journal of Corporate Finance 43: 106–21. [Google Scholar] [CrossRef]

- Chowdhury, Abdur, and George Mavrotas. 2006. FDI and growth: What causes what? World Economy 29: 9–19. [Google Scholar] [CrossRef]

- Claessens, Stijn, and B. Burcin Yurtoglu. 2012. Corporate Governance and Development: An Update. Global Corporate Governance Network. Washington, DC: World Bank. [Google Scholar]

- Claessens, Stijn, and B. Burcin Yurtoglu. 2013. Corporate governance in emerging markets: A survey. Emerging Markets Review 15: 1–33. [Google Scholar] [CrossRef]

- Classens, Stijn. 2006. Corporate governance and development. The World Bank Research Observer 21: 91–122. [Google Scholar] [CrossRef]

- Cooray, Arusha. 2010. Do stock markets lead to economic growth? Journal of Policy Modeling 32: 448–60. [Google Scholar] [CrossRef]

- Doidge, Craig, G. Andrew Karolyi, and René M. Stulz. 2007. Why do countries matter so much for corporate governance? Journal of Financial Economics 86: 1–39. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, Thomas. 2013. Corporate governance. International Encyclopedia of Ethics, 1–9. [Google Scholar] [CrossRef]

- Elsayed, Khaled. 2007. Does CEO duality really affect corporate performance? Corporate Governance: An International Review 15: 1203–14. [Google Scholar] [CrossRef]

- Feleagă, Niculae, Liliana Feleagă, Voicu Dan Dragomir, and Adrian Doru Bigioi. 2011. Corporate Governance in Emerging Economies: The Case of Romania. Theoretical and Applied Economics 18: 5–16. [Google Scholar]

- Fernandes, Nuno. 2008. EC: Board compensation and firm performance: The role of “independent” board members. Journal of Multinational Financial Management 18: 30–44. [Google Scholar] [CrossRef]

- Grosu, Maria. 2011. Codes and practices of implementation of corporate governance in Romania and results reporting. Annals of Faculty of Economics 1: 251–56. [Google Scholar]

- Iwaisako, Tatsuro, and Koichi Futagami. 2013. Patent protection, capital accumulation, and economic growth. Economic Theory 52: 631–68. [Google Scholar] [CrossRef]

- Khanna, Tarun, Joe Kogan, and Krishna Palepu. 2006. Globalization and similarities in corporate governance: A cross-country analysis. Review of Economics and Statistics 88: 69–90. [Google Scholar] [CrossRef] [Green Version]

- Krause, Ryan, Matthew Semadeni, and Albert A. Cannella Jr. 2014. CEO duality: A review and research agenda. Journal of Management 40: 256–86. [Google Scholar] [CrossRef]

- Larcker, David, and Brian Tayan. 2015. Corporate Governance Matters: A Closer Look at Organizational Choises and Their Consequences. London: Pearson Education. [Google Scholar]

- Law, Siong Hook, and Nirvikar Singh. 2014. Does too much finance harm economic growth? Journal of Banking & Finance 41: 36–44. [Google Scholar]

- Lee, Thomas A. 2007. Financial Reporting and Corporate Governance. Hoboken: John Wiley & Sons. [Google Scholar]

- Manolescu, Maria, Aureliana Geta Roman, and Mihaela Mocanu. 2011. Corporate governance in Romania: From regulation to implementation. Accounting and Management Information Systems 10: 4. [Google Scholar]

- Mennicken, Andrea, and Michael Power. 2013. Auditing and Corporate Governance. In The Oxford Handbook of Corporate Governance. Oxford: Oxford University Press. [Google Scholar] [CrossRef]

- Misangyi, Vilmos F., and Abhijith G. Acharya. 2014. Substitutes or complements? A configurational examination of corporate governance mechanisms. Academy of Management Journal 57: 1681–705. [Google Scholar] [CrossRef] [Green Version]

- Mohan, Ramesh. 2006. Causal relationship between savings and economic growth in countries with different income levels. Economics Bulletin 5: 1–12. [Google Scholar]

- OECD. 2021. OECD Corporate Governance Factbook. Available online: https://www.oecd.org/corporate/OECD-Corporate-Governance-Factbook.pdf (accessed on 27 September 2021).

- Ong, Audra. 2018. Financial reporting and corporate governance: Bridging the divide. Journal of Management Research 18: 37–43. [Google Scholar]

- Popescu, Gheorghe N., Veronica Adriana Popescu, and Cristina Raluca Popescu. 2015. Corporate Governance in Romania: Theories and Practices. In Corporate Governance and Corporate Social Responsibility: Emerging Markets Focus. Singapore: World Scientific Publishing Co. Pte. Ltd., chp. 14. pp. 375–401. [Google Scholar]

- Sarchizian, Sergiu, and Veronica Popovici. 2019. Corporate Governance in Romania—Current Trends. Ovidius University Annals, Economic Sciences Series 19: 115–22. [Google Scholar]

- Singh, Tarlok. 2010. Does international trade cause economic growth? A survey. The World Economy 33: 1517–64. [Google Scholar] [CrossRef]

- Tihanyi, Laszlo, Scott Graffin, and Gerard George. 2014. Rethinking governance in management research. Academy of Management Journal 57: 1535–43. [Google Scholar] [CrossRef]

- Tofan, Mihaela, and Elena Cigu. 2020. A view on Corporate Governance in Romania: Regulation and Effects. In Corporate Governance in Central Europe and Russia. Cham: Springer, pp. 177–97. [Google Scholar] [CrossRef]

- Vărzaru, Anca Antoaneta, Claudiu George Bocean, and Michael Marian Nicolescu. 2021. Rethinking Corporate Responsibility and Sustainability in Light of Economic Performance. Sustainability 13: 2660. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press. [Google Scholar]

- World Bank. 2021. Doing Business. Available online: https://databank.worldbank.org/source/doing-business (accessed on 22 September 2021).

- Young, Steven. 2000. The increasing use of non-executive directors: Its impact on UK board structure and governance arangements. Journal of Business Finance & Accounting 27: 1311–42. [Google Scholar]

{kind=link}

{kind=link}

| Variable | Definition |

| Protecting Minority Investors | The score for protecting minority investor benchmark economies, with respect to the regulatory best practice on the indicator set. |

| Corporate Transparency | The extent of the corporate transparency index measures ans the level of information that companies must share. |

| Director Liability | The extent of the director liability index measures when board members can be held liable for harm caused by related-party transactions and which sanctions are available. |

| Disclosure | The extent of the disclosure index measures the approval and disclosure requirements of related-party transactions. |

| Ownership and Control | The extent of ownership and control index measures the rules governing the structure and change in control of companies. |

| Shareholder Rights | The extent of the shareholder rights index measures the role of shareholders in key corporate decisions. |

| A: Descriptive Statistics—Romania | |||||

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| Protection of Minority Investors | 15 | 61.752 | 0.96 | 58.282 | 62 |

| Corporate Transparency | 7 | 71.429 | 0 | 71.429 | 71.429 |

| Director Liability | 15 | 40 | 0 | 40 | 40 |

| Disclosure | 15 | 89.333 | 2.582 | 80 | 90 |

| Ownership and Control | 7 | 42.857 | 0 | 42.857 | 42.857 |

| Shareholder Rights | 7 | 83.333 | 0 | 83.333 | 83.333 |

| B: Descriptive Statistics—Developing Countries | |||||

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| Protection of Minority Investors | 180 | 65.328 | 13.371 | 13.98 | 88 |

| Corporate Transparency | 84 | 67.347 | 28.013 | 0 | 100 |

| Director Liability | 180 | 52.167 | 24.728 | 0 | 90 |

| Disclosure | 180 | 73.833 | 24.638 | 0 | 100 |

| Ownership and Control | 84 | 63.605 | 22.659 | 0 | 85.714 |

| Shareholder Rights | 84 | 75.595 | 26.567 | 0 | 100 |

| C: Descriptive Statistics—Advanced Countries | |||||

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| Protection of Minority Investors | 390 | 68.746 | 9.693 | 36.023 | 86 |

| Corporate Transparency | 182 | 81.538 | 11.63 | 57.143 | 100 |

| Director Liability | 390 | 56.59 | 19.545 | 20 | 90 |

| Disclosure | 390 | 65.077 | 23.672 | 10 | 100 |

| Ownership and Control | 182 | 67.881 | 19.426 | 28.571 | 100 |

| Shareholder Rights | 182 | 78.48 | 14.946 | 33.333 | 100 |

| Pairwise correlations—Full Sample | ||||||||

| Variables | −1 | −2 | −3 | −4 | −5 | −6 | −7 | −8 |

| (1) GDP Growth | 1 | |||||||

| (2) Stock Market Capitalization | 0.123 * | 1 | ||||||

| (3) Protection of Minority Investors | 0.064 | 0.468 * | 1 | |||||

| (4) Corporate Transparency | −0.021 | −0.024 | 0.415 * | 1 | ||||

| (5) Director Liability | 0.047 | 0.446 * | 0.540 * | −0.242 * | 1 | |||

| (6) Disclosure | 0.130 * | 0.399 * | 0.705 * | 0.121 * | 0.249 * | 1 | ||

| (7) Ownership and Control | −0.072 | −0.028 | 0.468 * | 0.315 * | 0.088 | −0.114 | 1 | |

| (8) Shareholder Rights | −0.019 | −0.232 * | 0.402 * | 0.322 * | −0.132 * | −0.031 | 0.564 * | 1 |

| Pairwise correlations—Developing Countries | ||||||||

| Variables | −1 | −2 | −3 | −4 | −5 | −6 | −7 | −8 |

| (1) GDP Growth | 1 | |||||||

| (2) Stock Market Capitalization | −0.027 | 1 | ||||||

| (3) Protection of Minority Investors | −0.006 | 0.606 * | 1 | |||||

| (4) Corporate Transparency | 0.061 | −0.05 | 0.580 * | 1 | ||||

| (5) Director Liability | −0.034 | 0.627 * | 0.333 * | −0.255 * | 1 | |||

| (6) Disclosure | 0.075 | 0.306 * | 0.708 * | 0.002 | 0.171 * | 1 | ||

| (7) Ownership and Control | 0.043 | 0.489 * | 0.755 * | 0.646 * | 0.123 | 0.075 | 1 | |

| (8) Shareholder Rights | 0.021 | 0.027 | 0.606 * | 0.574 * | −0.278 * | 0.146 | 0.746 * | 1 |

| Pairwise correlations—Advanced Countries | ||||||||

| Variables | −1 | −2 | −3 | −4 | −5 | −6 | −7 | −8 |

| (1) GDP Growth | 1 | |||||||

| (2) Stock Market Capitalization | 0.229 * | 1 | ||||||

| (3) Protection of Minority Investors | 0.153 * | 0.381 * | 1 | |||||

| (4) Corporate Transparency | −0.088 | 0.033 | 0.135 | 1 | ||||

| (5) Director Liability | 0.121 * | 0.308 * | 0.697 * | −0.359 * | 1 | |||

| (6) Disclosure | 0.119 * | 0.475 * | 0.785 * | 0.462 * | 0.332 * | 1 | ||

| (7) Ownership and Control | −0.126 | −0.320 * | 0.239 * | −0.097 | 0.054 | −0.201 * | 1 | |

| (8) Shareholder Rights | −0.047 | −0.451 * | 0.155 * | −0.173 * | −0.001 | −0.170 * | 0.410 * | 1 |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Variables | Full Sample | Full Sample | Full Sample | Developing | Advanced |

| Investment | 0.206 *** | 0.266 *** | 0.265 *** | 0.370 *** | 0.251 *** |

| (0.0326) | (0.0362) | (0.0369) | (0.0728) | (0.0510) | |

| Savings | 0.0636 ** | 0.0186 | 0.00460 | 0.0284 | −0.0174 |

| (0.0253) | (0.0243) | (0.0236) | (0.0430) | (0.0293) | |

| Trade | 0.000665 | −0.000983 | −0.00427 | 0.00555 | −0.0100 ** |

| (0.00303) | (0.00338) | (0.00373) | (0.00585) | (0.00471) | |

| FDI | 0.0484 | 0.0444 | 0.0544 | −0.00899 | 0.0892 * |

| (0.0305) | (0.0346) | (0.0341) | (0.0144) | (0.0481) | |

| Credit | −0.00993 *** | −0.0210 *** | −0.0262 *** | −0.0237 ** | −0.0321 *** |

| (0.00295) | (0.00390) | (0.00409) | (0.00959) | (0.00619) | |

| Stock Markets | 0.0147 *** | 0.0115 *** | 0.0119 ** | 0.0172 *** | |

| (0.00294) | (0.00320) | (0.00499) | (0.00483) | ||

| Corporate Governance | 0.0773 *** | 0.0520 * | 0.0886 *** | ||

| (0.0196) | (0.0308) | (0.0249) | |||

| Observations | 520 | 425 | 425 | 154 | 271 |

| R-squared | 0.223 | 0.287 | 0.322 | 0.226 | 0.390 |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Variables | Full Sample | Full Sample | Full Sample | Developing | Advanced |

| Investment | 0.239 *** | 0.286 *** | 0.338 *** | 0.571 *** | 0.225 *** |

| (0.0392) | (0.0449) | (0.0471) | (0.0881) | (0.0613) | |

| Savings | 0.243 *** | 0.183 *** | 0.151 ** | 0.0562 | 0.242 *** |

| (0.0530) | (0.0585) | (0.0586) | (0.0975) | (0.0829) | |

| Trade | 0.0238 ** | 0.0292 ** | 0.0267 ** | 0.0424 * | 0.0236 * |

| (0.0111) | (0.0119) | (0.0118) | (0.0241) | (0.0128) | |

| FDI | 0.0641 *** | 0.0556 *** | 0.0534 *** | −0.0148 | 0.0979 *** |

| (0.0133) | (0.0154) | (0.0152) | (0.0247) | (0.0192) | |

| Credit | −0.0415 *** | −0.0499 *** | −0.0540 *** | −0.0516 * | −0.0434 *** |

| (0.00939) | (0.0103) | (0.0103) | (0.0264) | (0.0114) | |

| Stock Markets | 0.0205 *** | 0.0221 *** | 0.0160 | 0.0284 *** | |

| (0.00608) | (0.00602) | (0.0105) | (0.00719) | ||

| Corporate Governance | 0.116 *** | 0.0380 | 0.124 *** | ||

| (0.0353) | (0.0703) | (0.0456) | |||

| Observations | 520 | 425 | 425 | 154 | 271 |

| R-squared | 0.315 | 0.361 | 0.378 | 0.288 | 0.497 |

| Number of id | 39 | 35 | 35 | 12 | 23 |

| Country FE | Yes | Yes | Yes | Yes | Yes |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mihail, B.A.; Dumitrescu, D. Corporate Governance from a Cross-Country Perspective and a Comparison with Romania. J. Risk Financial Manag. 2021, 14, 600. https://doi.org/10.3390/jrfm14120600

Mihail BA, Dumitrescu D. Corporate Governance from a Cross-Country Perspective and a Comparison with Romania. Journal of Risk and Financial Management. 2021; 14(12):600. https://doi.org/10.3390/jrfm14120600

Chicago/Turabian StyleMihail, Bogdan Aurelian, and Dalina Dumitrescu. 2021. "Corporate Governance from a Cross-Country Perspective and a Comparison with Romania" Journal of Risk and Financial Management 14, no. 12: 600. https://doi.org/10.3390/jrfm14120600

APA StyleMihail, B. A., & Dumitrescu, D. (2021). Corporate Governance from a Cross-Country Perspective and a Comparison with Romania. Journal of Risk and Financial Management, 14(12), 600. https://doi.org/10.3390/jrfm14120600