A Bayesian Semiparametric Realized Stochastic Volatility Model

Abstract

:1. Introduction

2. Ex-Post Volatility Estimation and Data

2.1. Ex-Post Volatility Estimation

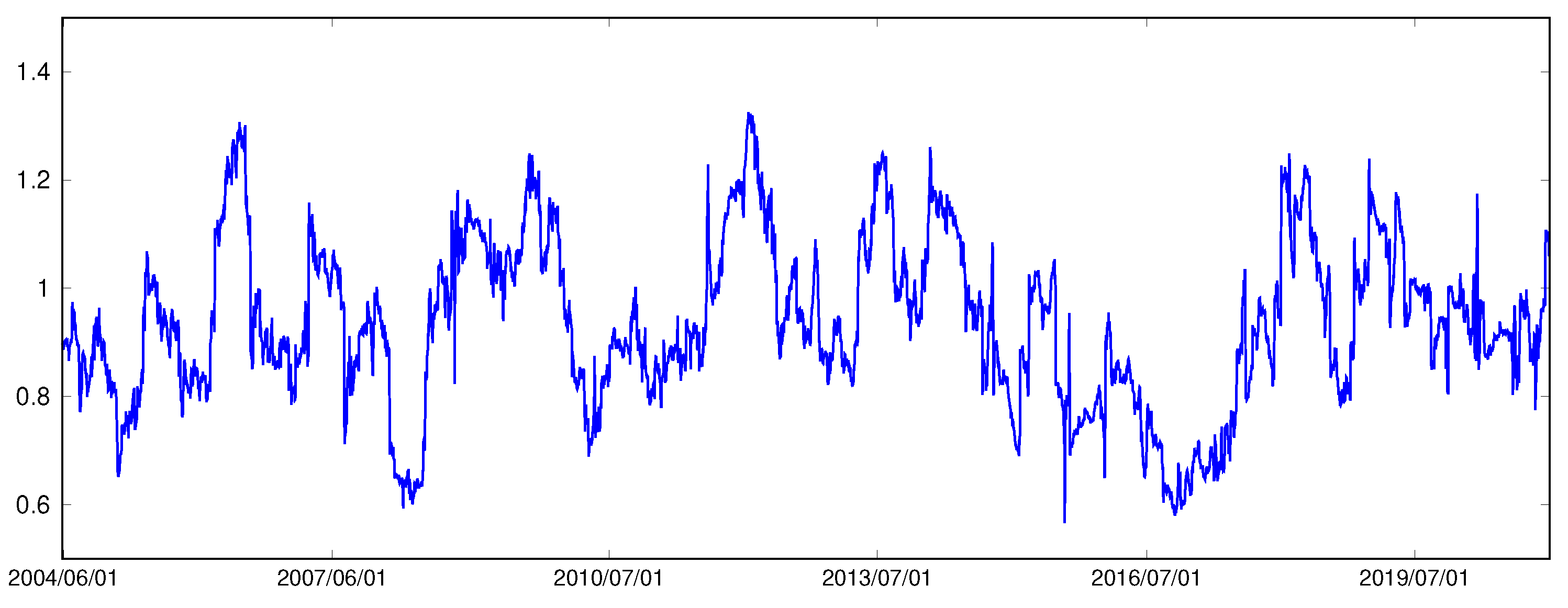

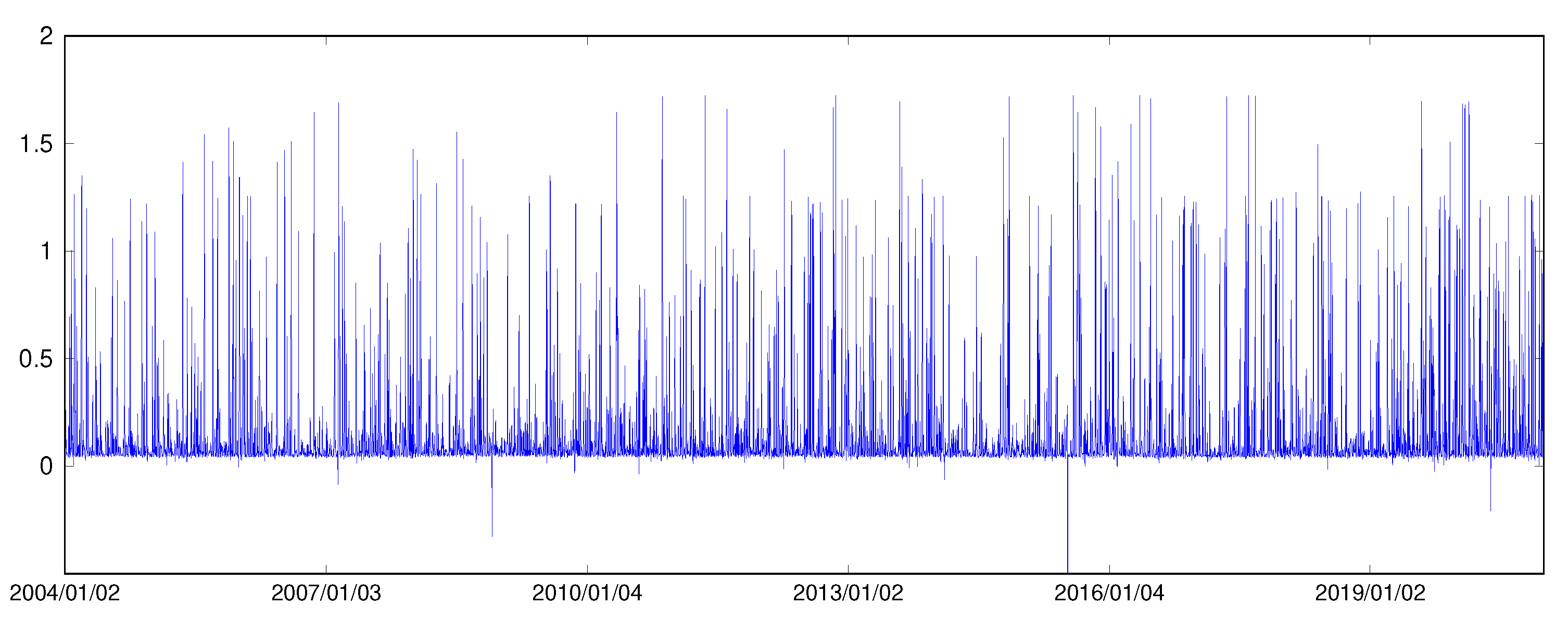

2.2. Data Source and Motivation

3. Models

3.1. Semiparametric Realized Stochastic Volatility Models

3.2. Benchmark Models

3.3. Bayesian Inference

- 1.

- Sample model parameters and conditional on .Given conjugate priors, the conditional posterior distributions of , , , , , and can be easily derived. See the Appendix A for details. Model parameters are estimated by iteratively using Gibbs samplers as follows.

- (a).

- for .

- (b).

- for .

- (c).

- for .

- (d).

- for .

- (e).

- .

- (f).

- .

- 2.

- Sample latent volatility for .Latent volatility variables are sampled using the Metropolis-Hasting algorithm with a single move sampler. The conditional posterior of is given asThe proposal distribution for is derived from the conditional posterior following the approach in Kim et al. (1998). We leave the details to the Appendix A. A proposed value is accepted with probability .

- 3.

- Sample state variable for from

- 4.

- Sample auxiliary variable for .

- (a).

- Calculate for , where is sampled from

- (b).

- Sampling for from .

- (c).

- Find the smallest K such that .

- 5.

- Sample based on K.Following the method proposed by Escobar and West (1994), is sampled from the Gamma mixture below.where and .

3.4. Prediction

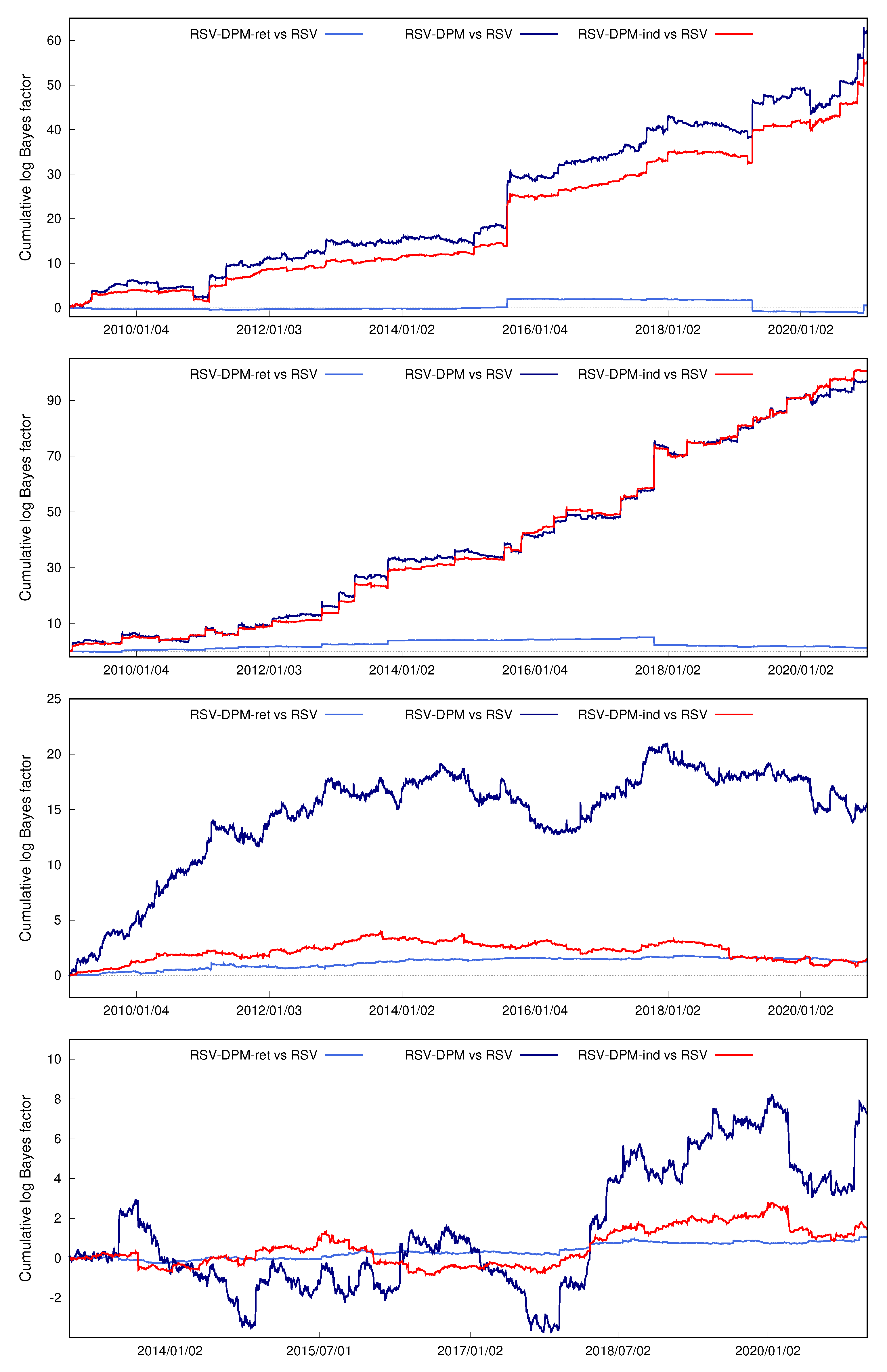

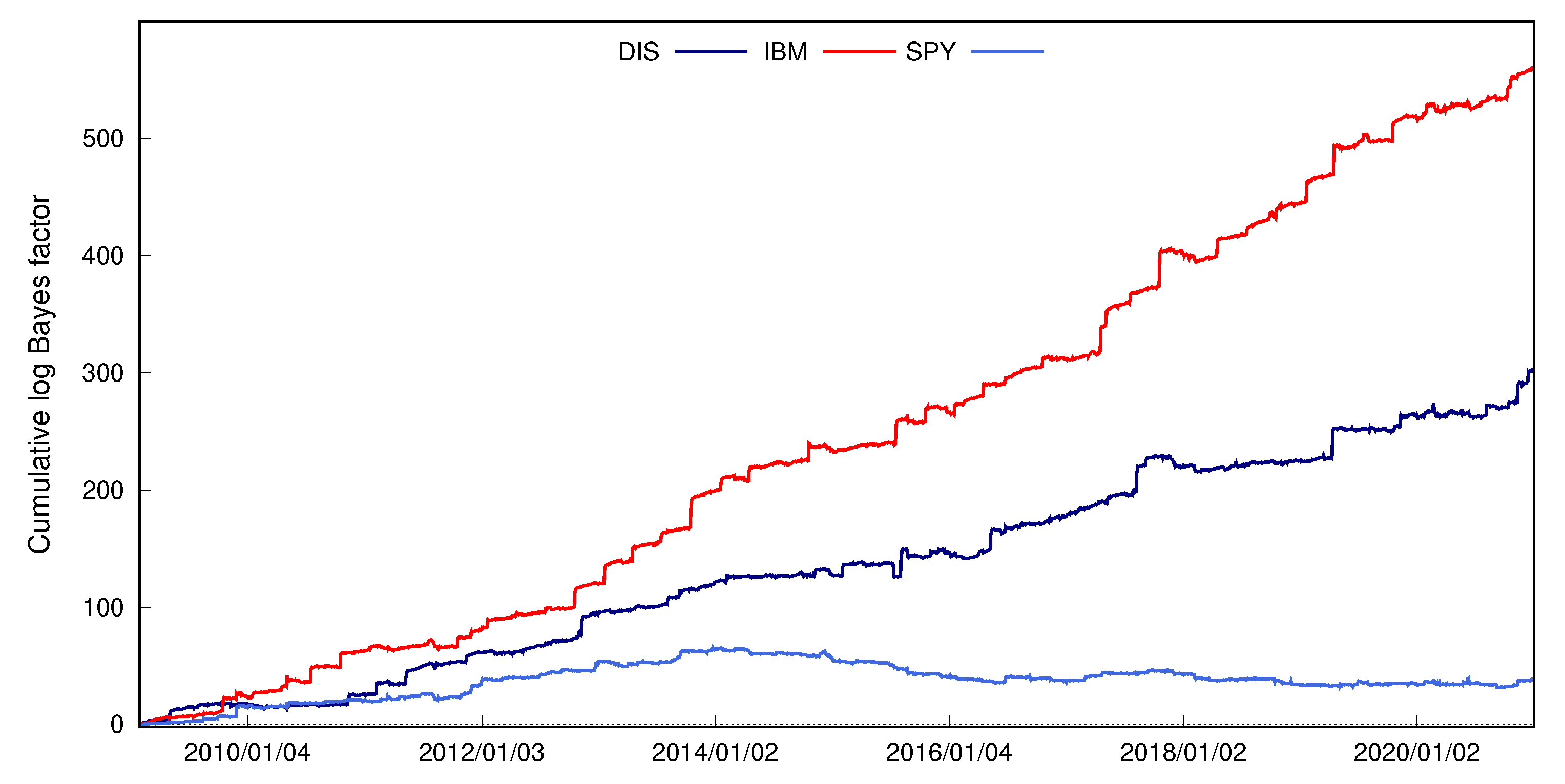

4. Empirical Applications

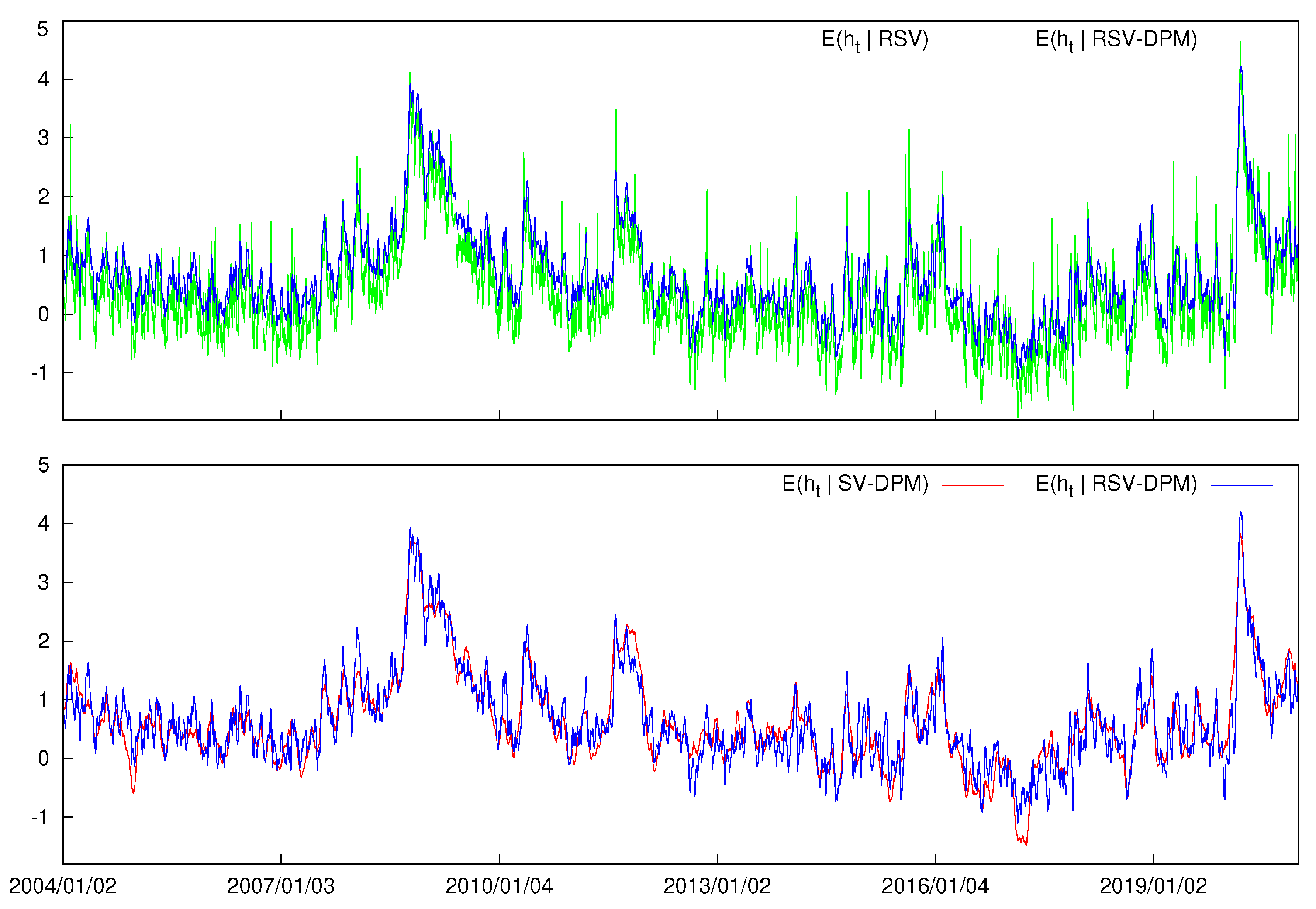

4.1. Parameter Estimates

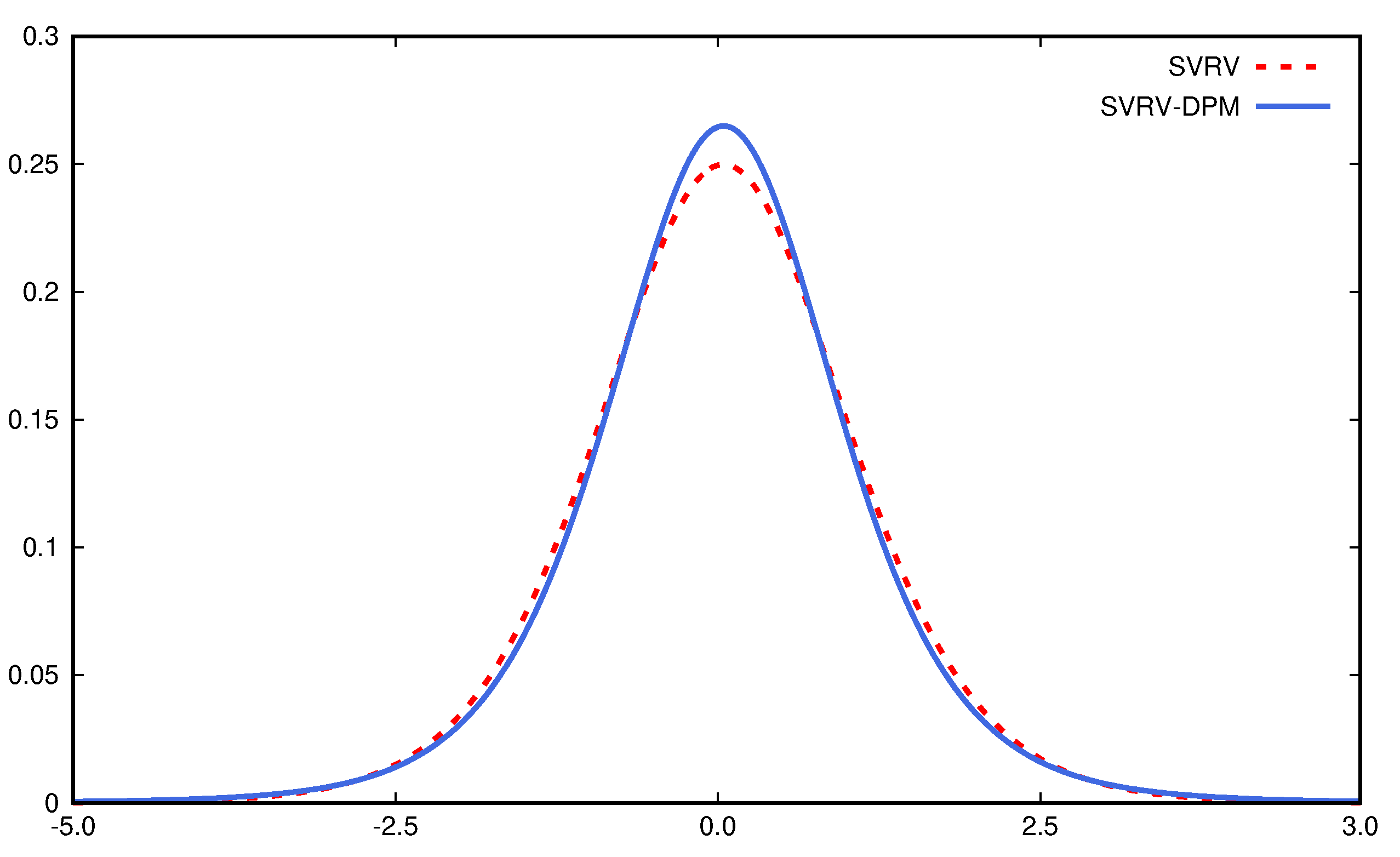

4.2. Density Forecasts

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- 1.

- for .Given prior , the conditional posterior of is given aswhere

- 2.

- .Given prior , the conditional posterior of is given aswhere .

- 3.

- Given prior , the conditional posterior of is given aswhere

- 4.

- Given prior , the conditional posterior of is given as

- 5.

- Let , and , where . Given prior , the conditional posterior of is given aswhere

- 6.

- Given prior , the conditional posterior of is given as

- 7.

- for .The conditional posterior of is given aswhereandKim et al. (1998) show thatwhereand is the proposal distribution for drawing . A new value is accepted with probability .

| 1 | Under the previous-tick scheme, is the price observed the nearest before time . |

| 2 | The Parzen kernel function is given as

|

| 3 | is calculated using high-frequency returns such as every q trades, and is the number of nonzero returns. I set . |

| 4 | https://www.tickdata.com/, accessed on 15 August 2021. |

| 5 | The kurtosis measure is calculated using formula . |

| 6 | The innovation term , where is the degree of freedom. |

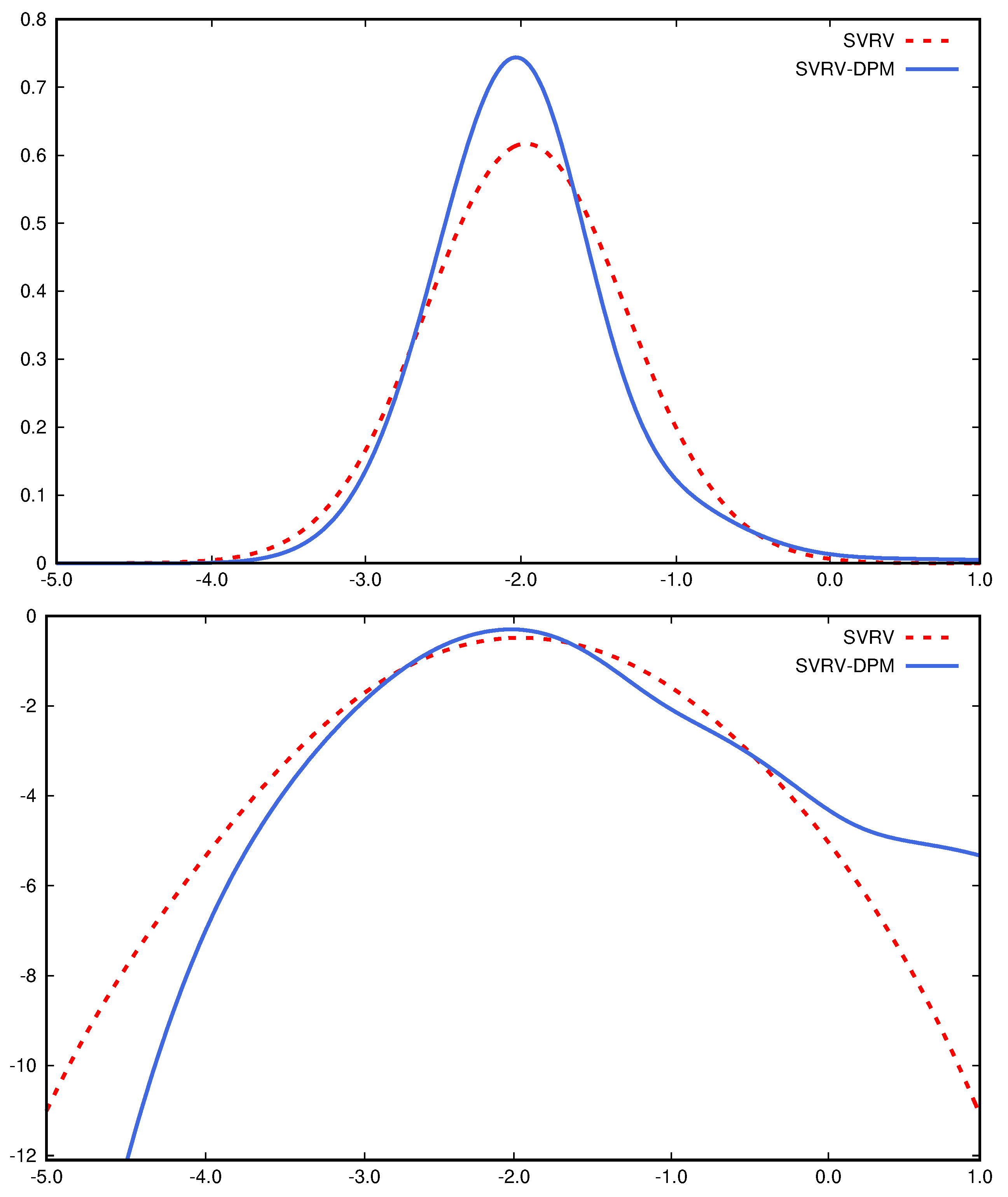

| 7 | To better visualize the bias correction difference in RSV-DPM and RSV models, we set the scaling parameter to be 1 to make two models have the same setting in return variance. |

References

- Andersen, Torben G., Tim Bollerslev, Francis X. Diebold, and Heiko Ebens. 2001. The distribution of realized stock return volatility. Journal of Financial Economics 61: 43–76. [Google Scholar] [CrossRef]

- Asai, Manabu, Chia-Lin Chang, and Michael McAleer. 2017. Realized stochastic volatility with general asymmetry and long memory. Journal of Econometrics 199: 202–12. [Google Scholar] [CrossRef] [Green Version]

- Bandi, Federico M., and Jeffrey R. Russell. 2008. Microstructure noise, realized variance, and optimal sampling. The Review of Economic Studies 75: 339–69. [Google Scholar] [CrossRef]

- Bandi, Federico M., Jeffrey R. Russell, and Chen Yang. 2013. Realized volatility forecasting in the presence of time-varying noise. Journal of Business & Economic Statistics 31: 331–45. [Google Scholar]

- Barndorff-Nielsen, Ole E. 1997. Normal inverse gaussian distributions and stochastic volatility modelling. Scandinavian Journal of Statistics 24: 1–13. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2002. Estimating quadratic variation using realized variance. Journal of Applied Econometrics 17: 457–77. [Google Scholar] [CrossRef] [Green Version]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2004. Power and Bipower Variation with Stochastic Volatility and Jumps. Journal of Financial Econometrics 2: 1–37. [Google Scholar] [CrossRef] [Green Version]

- Barndorff-Nielsen, Ole E., Peter Reinhard Hansen, Asger Lunde, and Neil Shephard. 2008. Designing realized kernels to measure the ex post variation of equity prices in the presence of noise. Econometrica 76: 1481–536. [Google Scholar]

- Barndorff-Nielsen, Ole E., Peter Reinhard Hansen, Asger Lunde, and Neil Shephard. 2009. Realized kernels in practice: Trades and quotes. Econometrics Journal 12: C1–C32. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef] [Green Version]

- Chib, Siddhartha, Federico Nardari, and Neil Shephard. 2002. Markov chain monte carlo methods for stochastic volatility models. Journal of Econometrics 108: 281–316. [Google Scholar] [CrossRef]

- Christensen, Kim, and Mark Podolskij. 2007. Realized range-based estimation of integrated variance. Journal of Econometrics 141: 323–49. [Google Scholar] [CrossRef]

- Corsi, Fulvio, Stefan Mittnik, Christian Pigorsch, and Uta Pigorsch. 2008. The volatility of realized volatility. Econometric Reviews 27: 46–78. [Google Scholar] [CrossRef]

- Delatola, Eleni-Ioanna, and Jim E. Griffin. 2013. A bayesian semiparametric model for volatility with a leverage effect. Computational Statistics & Data Analysis 60: 97–110. [Google Scholar]

- Escobar, Michael D., and Mike West. 1994. Bayesian Density Estimation and Inference Using Mixtures. Journal of the American Statistical Association 90: 577–88. [Google Scholar] [CrossRef]

- Ferguson, Thomas S. 1973. A Bayesian analysis of some nonparametric problems. The Annals of Statistics 1: 209–30. [Google Scholar] [CrossRef]

- Hansen, Peter Reinhard, and Asger Lunde. 2005. A Realized Variance for the Whole Day Based on Intermittent High-Frequency Data. Journal of Financial Econometrics 3: 525–54. [Google Scholar] [CrossRef]

- Hansen, Peter Reinhard, Zhuo Huang, and Howard Howan Shek. 2012. Realized garch: A joint model for returns and realized measures of volatility. Journal of Applied Econometrics 27: 877–906. [Google Scholar] [CrossRef]

- Huang, Darien, Christian Schlag, Ivan Shaliastovich, and Julian Thimme. 2019. Volatility-of-volatility risk. Journal of Financial and Quantitative Analysis 54: 2423–52. [Google Scholar] [CrossRef] [Green Version]

- Jacod, Jean, Yingying Li, Per A. Mykland, Mark Podolskij, and Mathias Vetter. 2009. Microstructure noise in the continuous case: The pre-averaging approach. Stochastic Processes and their Applications 119: 2249–76. [Google Scholar] [CrossRef] [Green Version]

- Jensen, Mark J., and John M. Maheu. 2010. Bayesian semiparametric stochastic volatility modeling. Journal of Econometrics 157: 306–16. [Google Scholar] [CrossRef] [Green Version]

- Jensen, Mark J., and John M. Maheu. 2014. Estimating a semiparametric asymmetric stochastic volatility model with a dirichlet process mixture. Journal of Econometrics 178: 523–38. [Google Scholar] [CrossRef] [Green Version]

- Kalli, Maria, Jim E. Griffin, and Stephen G. Walker. 2011. Slice sampling mixture models. Statistics and Computing 21: 93–105. [Google Scholar] [CrossRef]

- Kim, Sangjoon, Neil Shephard, and Siddhartha Chib. 1998. Stochastic volatility: Likelihood inference and comparison with arch models. The Review of Economic Studies 65: 361–93. [Google Scholar] [CrossRef]

- Liu, Jia, and John M. Maheu. 2018. Improving markov switching models using realized variance. Journal of Applied Econometrics 33: 297–318. [Google Scholar] [CrossRef] [Green Version]

- Maheu, John, and Thomas McCurdy. 2011. Do high-freuqency measures of volatility improve forecasts of returns distributions? Journal of Econometrics 160: 69–76. [Google Scholar] [CrossRef] [Green Version]

- Mahieu, Ronald, and Peter C. Schotman. 1998. An empirical application of stochastic volatility models. Journal of Applied Econometrics 13: 333–60. [Google Scholar] [CrossRef] [Green Version]

- Nakajima, Jouchi, and Yasuhiro Omori. 2012. Stochastic volatility model with leverage and asymmetrically heavy-tailed error using gh skew student’s t-distribution. Computational Statistics & Data Analysis 56: 3690–704. [Google Scholar]

- Sandmann, Gleb, and Siem Jan Koopman. 1998. Estimation of stochastic volatility models via monte carlo maximum likelihood. Journal of Econometrics 87: 271–301. [Google Scholar] [CrossRef]

- Sethuraman, Jayaram. 1994. A constructive definition of Dirichlet priors. Statistica Sinica 4: 639–50. [Google Scholar]

- Shephard, Neil, and Kevin Sheppard. 2010. Realising the future: Forecasting with high-frequency-based volatility (heavy) models. Journal of Applied Econometrics 25: 197–231. [Google Scholar] [CrossRef] [Green Version]

- Shirota, Shinichiro, Takayuki Hizu, and Yasuhiro Omori. 2014. Realized stochastic volatility with leverage and long memory. Computational Statistics and Data Analysis 76: 618–41. [Google Scholar] [CrossRef] [Green Version]

- Takahashi, Makoto, Yasuhiro Omori, and Toshiaki Watanabe. 2009. Estimating stochastic volatility models using daily returns and realized volatility simultaneously. Computational Statistics & Data Analysis 53: 2404–26. [Google Scholar]

- Taylor, Stephen J. 1986. Modelling Financial Time Series. Chichester: John Wiley. [Google Scholar]

- Virbickaitė, Audronė, and Hedibert F. Lopes. 2019. Bayesian semiparametric markov switching stochastic volatility model. Applied Stochastic Models in Business and Industry 35: 978–97. [Google Scholar] [CrossRef]

- Walker, Stephen G. 2007. Sampling the Dirichlet mixture model with slices. Communications in Statistics—Simulation and Computation 36: 45–54. [Google Scholar] [CrossRef]

- Xiu, Dacheng. 2010. Quasi-maximum likelihood estimation of volatility with high frequency data. Journal of Econometrics 159: 235–50. [Google Scholar] [CrossRef]

- Yu, Jun. 2012. A semiparametric stochastic volatility model. Journal of Econometrics 167: 473–82. [Google Scholar] [CrossRef]

- Zhang, Lan, Per A. Mykland, and Yacine Aït-Sahalia. 2005. A tale of two time scales: Determining integrated volatility with noisy high-frequency data. Journal of the American Statistical Association 100: 1394–411. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Data | Mean | St. Dev. | Skewness | Kurtosis | Min | Max | |

|---|---|---|---|---|---|---|---|

| Panel A: DIS | |||||||

| 0.048 | 0.045 | 2.922 | 0.378 | 17.063 | −13.908 | 14.818 | |

| 3.022 | 1.255 | 74.446 | 12.149 | 214.107 | 0.101 | 222.816 | |

| 3.076 | 1.281 | 80.633 | 12.779 | 234.898 | 0.124 | 222.505 | |

| 0.372 | 0.227 | 0.982 | 1.023 | 7.823 | −2.296 | 5.406 | |

| 0.401 | 0.248 | 0.943 | 1.100 | 8.026 | −2.089 | 5.405 | |

| Panel B: IBM | |||||||

| 0.007 | 0.025 | 2.055 | −0.378 | 14.591 | −13.755 | 10.899 | |

| 2.232 | 0.952 | 34.375 | 9.621 | 142.584 | 0.096 | 138.501 | |

| 2.296 | 0.969 | 36.599 | 9.258 | 126.467 | 0.113 | 128.970 | |

| 0.094 | −0.049 | 0.911 | 1.207 | 8.340 | −2.340 | 4.931 | |

| 0.125 | −0.032 | 0.890 | 1.284 | 8.555 | −2.180 | 4.860 | |

| Panel C: SPY | |||||||

| 0.028 | 0.065 | 1.476 | −0.389 | 21.891 | −11.589 | 13.558 | |

| 1.377 | 0.457 | 22.279 | 15.417 | 352.039 | 0.013 | 148.459 | |

| 1.405 | 0.466 | 22.680 | 15.250 | 343.385 | 0.017 | 147.030 | |

| −0.630 | −0.782 | 1.367 | 0.713 | 7.048 | −4.305 | 5.000 | |

| −0.595 | −0.764 | 1.331 | 0.757 | 7.104 | −4.079 | 4.991 | |

| Panel D: SKHY | |||||||

| 0.097 | 0.000 | 6.586 | 0.237 | 5.504 | −13.062 | 13.958 | |

| 6.559 | 4.348 | 54.981 | 4.240 | 28.222 | 0.589 | 87.957 | |

| 6.294 | 4.071 | 55.954 | 4.165 | 26.820 | 0.338 | 85.496 | |

| 1.559 | 1.470 | 0.536 | 0.727 | 6.758 | −0.529 | 4.477 | |

| 1.481 | 1.404 | 0.606 | 0.616 | 6.690 | −1.084 | 4.448 | |

| RSV-DPM | RSV-DPM-ind | RSV | SV-DPM | |||||

|---|---|---|---|---|---|---|---|---|

| Mean | St. Dev. | Mean | St. Dev. | Mean | St. Dev. | Mean | St. Dev. | |

| Panel A: DIS | ||||||||

| 0.0480 | 0.0139 | |||||||

| 0.0538 | 0.0240 | |||||||

| 0.1934 | 0.0124 | |||||||

| 0.0120 | 0.0042 | 0.0607 | 0.0139 | 0.0055 | 0.0074 | 0.0023 | 0.0039 | |

| 0.9711 | 0.0041 | 0.9424 | 0.0072 | 0.8615 | 0.0147 | 0.9704 | 0.0057 | |

| 0.0325 | 0.0026 | 0.0816 | 0.0080 | 0.1922 | 0.0192 | 0.0461 | 0.0095 | |

| K | 6.2806 | 1.3239 | 3.0540 | 1.0079 | 5.5072 | 1.4271 | ||

| 0.4478 | 0.1878 | 0.2448 | 0.1379 | 0.3975 | 0.1857 | |||

| 3.9734 | 1.1658 | |||||||

| 0.2988 | 0.1567 | |||||||

| Panel B: IBM | ||||||||

| 0.0688 | 0.0154 | |||||||

| 0.0525 | 0.0240 | |||||||

| 0.1763 | 0.0102 | |||||||

| 0.0275 | 0.0056 | 0.0446 | 0.0085 | 0.0360 | 0.0075 | 0.0132 | 0.0042 | |

| 0.9662 | 0.0049 | 0.9553 | 0.0058 | 0.8866 | 0.0112 | 0.9795 | 0.0043 | |

| 0.0446 | 0.0042 | 0.0535 | 0.0049 | 0.1776 | 0.0152 | 0.0324 | 0.0053 | |

| K | 5.1318 | 1.1947 | 2.8922 | 1.2027 | 3.5662 | 1.4451 | ||

| 0.3797 | 0.1758 | 0.2363 | 0.1413 | 0.2747 | 0.1576 | |||

| 5.2840 | 2.0734 | |||||||

| 0.3817 | 0.2005 | |||||||

| Panel C: SPY | ||||||||

| 0.0937 | 0.0094 | |||||||

| −0.0808 | 0.0230 | |||||||

| 0.2176 | 0.0088 | |||||||

| −0.0337 | 0.0067 | −0.0484 | 0.0124 | −0.0328 | 0.0068 | −0.0177 | 0.0057 | |

| 0.9667 | 0.0045 | 0.9429 | 0.0066 | 0.9405 | 0.0065 | 0.9793 | 0.0040 | |

| 0.0707 | 0.0056 | 0.1300 | 0.0106 | 0.1357 | 0.0101 | 0.0689 | 0.0090 | |

| K | 5.1950 | 1.2383 | 1.8864 | 0.9991 | 8.3496 | 3.5307 | ||

| 0.3769 | 0.1723 | 0.1746 | 0.1214 | 0.5806 | 0.2952 | |||

| 3.1826 | 1.1761 | |||||||

| 0.2532 | 0.1422 | |||||||

| Panel D: SKHY | ||||||||

| 0.0885 | 0.0384 | |||||||

| −0.0566 | 0.0308 | |||||||

| 0.2068 | 0.0077 | |||||||

| 0.0459 | 0.0087 | 0.0830 | 0.0139 | 0.1074 | 0.0157 | 0.0165 | 0.0053 | |

| 0.9688 | 0.0056 | 0.9473 | 0.0083 | 0.9331 | 0.0096 | 0.9676 | 0.0071 | |

| 0.0175 | 0.0022 | 0.0328 | 0.0043 | 0.0434 | 0.0055 | 0.0199 | 0.0039 | |

| K | 5.9140 | 1.0316 | 2.1472 | 1.2665 | 3.5878 | 1.4628 | ||

| 0.4347 | 0.1782 | 0.1937 | 0.1339 | 0.2848 | 0.1637 | |||

| 3.3990 | 1.3635 | |||||||

| 0.2701 | 0.1531 | |||||||

| Panel A: DIS | ||||||

| SV | −5174.3 | −5194.5 | −5209.1 | |||

| SV-t | −5129.4 | 44.9 | −5157.6 | 36.9 | −5175.1 | 33.9 |

| GARCH | −5383.1 | −208.8 | −5333.2 | −138.7 | −5339.8 | −130.8 |

| GARCH-t | −5149.5 | 24.8 | −5177.0 | 17.6 | −5189.3 | 19.7 |

| SV-DPM | −5121.1 | 53.2 | −5150.5 | 44.0 | −5174.1 | 35.0 |

| RSV (SRV) | −5128.8 | 45.5 | −5185.9 | 8.6 | −5238.6 | −29.5 |

| RSV (RK) | −5140.4 | 33.9 | −5188.8 | 5.7 | −5235.8 | −26.7 |

| RSV-DPM-ret (SRV) | −5128.3 | 46.1 | −5184.9 | 9.6 | −5237.7 | −28.7 |

| RSV-DPM-ret (RK) | −5138.7 | 35.6 | −5189.1 | 5.4 | −5234.2 | −25.2 |

| RSV-DPM (SRV) | −5066.8 | 107.5 | −5142.6 | 51.9 | −5185.3 | 23.7 |

| RSV-DPM (RK) | −5070.2 | 104.1 | −5141.4 | 53.1 | −5185.5 | 23.5 |

| RSV-DPM-ind (SRV) | −5073.9 | 100.4 | −5150.9 | 43.6 | −5195.5 | 13.5 |

| RSV-DPM-ind (RK) | −5075.1 | 99.2 | −5152.0 | 42.5 | −5196.7 | 12.3 |

| Panel B: IBM | ||||||

| SV | −4851.8 | −4872.9 | −4894.2 | |||

| SV-t | −4797.7 | 54.1 | −4832.9 | 40.0 | −4860.6 | 33.60 |

| GARCH | −5127.2 | −275.4 | −4993.1 | −120.2 | −5008.6 | −114.43 |

| GARCH-t | −4825.4 | 26.4 | −4851.7 | 21.2 | −4872.6 | 21.53 |

| SV-DPM | −4792.2 | 59.6 | −4834.0 | 38.8 | −4859.8 | 34.40 |

| RSV (SRV) | −4846.2 | 5.6 | −4880.3 | −7.4 | −4913.3 | −19.10 |

| RSV (RK) | −4841.5 | 10.3 | −4880.3 | −7.4 | −4903.5 | −9.30 |

| RSV-DPM-ret (SRV) | −4844.9 | 6.9 | −4881.6 | −8.7 | −4913.9 | −19.77 |

| RSV-DPM-ret (RK) | −4834.1 | 17.7 | −4878.2 | −5.3 | −4902.0 | −7.84 |

| RSV-DPM (SRV) | −4749.3 | 102.5 | −4812.7 | 60.1 | −4843.2 | 50.95 |

| RSV-DPM (RK) | −4744.9 | 106.8 | −4814.3 | 58.6 | −4845.9 | 48.22 |

| RSV-DPM-ind (SRV) | −4745.5 | 106.2 | −4815.2 | 57.7 | −4844.6 | 49.57 |

| RSV-DPM-ind (RK) | −4739.6 | 112.2 | −4816.5 | 56.4 | −4843.7 | 50.47 |

| Panel C: SPY | ||||||

| SV | −3855.2 | −3956.1 | −4016.2 | |||

| SV-t | −3867.8 | −12.6 | −3943.1 | 12.9 | −3998.0 | 18.1 |

| GARCH | −3975.8 | −120.6 | −4060.3 | −104.3 | −4126.5 | −110.4 |

| GARCH-t | −3851.5 | 3.7 | −3945.9 | 10.1 | −4011.1 | 5.1 |

| SV-DPM | −3843.2 | 12.0 | −3940.1 | 16.0 | −3996.7 | 19.5 |

| RSV (SRV) | −3767.6 | 87.6 | −3908.3 | 47.8 | −3981.1 | 35.1 |

| RSV (RK) | −3768.8 | 86.4 | −3910.0 | 46.0 | −3980.0 | 36.1 |

| RSV-DPM-ret (SRV) | −3766.4 | 88.8 | −3908.0 | 48.1 | −3980.0 | 36.2 |

| RSV-DPM-ret (RK) | −3767.8 | 87.4 | −3909.8 | 46.2 | −3979.1 | 37.0 |

| RSV-DPM (SRV) | −3752.2 | 103.0 | −3891.3 | 64.7 | −3970.7 | 45.5 |

| RSV-DPM (RK) | −3750.6 | 104.6 | −3893.4 | 62.6 | −3972.8 | 43.3 |

| RSV-DPM-ind (SRV) | −3766.2 | 89.0 | −3910.7 | 45.4 | −3980.6 | 35.5 |

| RSV-DPM-ind (RK) | −3766.7 | 88.5 | −3913.3 | 42.7 | −3981.0 | 35.1 |

| Panel D: SKHY | ||||||

| SV | −4308.1 | −4304.7 | −4297.7 | |||

| SV-t | −4320.9 | −12.7 | −4315.2 | −10.6 | −4312.3 | −14.6 |

| GARCH | −4509.3 | −201.2 | −4507.5 | −202.8 | −4509.8 | −212.0 |

| GARCH-t | −4303.2 | 4.9 | −4302.5 | 2.2 | −4302.2 | −4.5 |

| SV-DPM | −4305.0 | 3.1 | −4299.5 | 5.2 | −4293.9 | 3.9 |

| RSV (SRV) | −4290.6 | 17.5 | −4288.5 | 16.1 | −4287.8 | 9.9 |

| RSV (RK) | −4290.5 | 17.6 | −4289.6 | 15.1 | −4288.5 | 9.2 |

| RSV-DPM-ret (SRV) | −4289.5 | 18.6 | −4288.3 | 16.4 | −4287.5 | 10.3 |

| RSV-DPM-ret (RK) | −4290.4 | 17.7 | −4290.0 | 14.6 | −4288.9 | 8.8 |

| RSV-DPM (SRV) | −4283.4 | 24.8 | −4287.3 | 17.4 | −4285.7 | 12.1 |

| RSV-DPM (RK) | −4281.4 | 26.7 | −4290.5 | 14.2 | −4286.4 | 11.3 |

| RSV-DPM-ind (SRV) | −4289.1 | 19.0 | −4289.2 | 15.5 | −4286.4 | 11.3 |

| RSV-DPM-ind (RK) | −4289.7 | 18.4 | −4291.8 | 12.8 | −4287.7 | 10.1 |

| Panel A: DIS | ||||||

| RSV (SRV) | −3166.5 | −3634.7 | −3853.0 | |||

| RSV-DPM-ret (SRV) | −3159.4 | 7.1 | −3618.4 | 16.3 | −3853.4 | −0.5 |

| RSV-DPM (SRV) | −2864.9 | 301.6 | −3313.5 | 321.2 | −3476.9 | 376.0 |

| RSV-DPM-ind (SRV) | −2860.9 | 305.5 | −3346.6 | 288.1 | −3559.6 | 293.3 |

| RSV (RK) | −2985.0 | −3496.2 | −3738.4 | |||

| RSV-DPM-ret (RK) | −2981.8 | 3.2 | −3492.2 | 4.0 | −3735.5 | 2.9 |

| RSV-DPM (RK) | −2614.3 | 370.7 | −3146.6 | 349.6 | −3328.9 | 409.5 |

| RSV-DPM-ind (RK) | −2598.4 | 386.5 | −3170.7 | 325.5 | −3410.2 | 328.2 |

| Panel B: IBM | ||||||

| RSV (SRV) | −3306.9 | −3569.9 | −3784.9 | |||

| RSV-DPM-ret (SRV) | −3304.2 | 2.8 | −3570.1 | −0.2 | −3784.3 | 0.5 |

| RSV-DPM (SRV) | −2746.3 | 560.7 | −3123.1 | 446.8 | −3324.3 | 460.6 |

| RSV-DPM-ind (SRV) | −2748.6 | 558.4 | −3163.0 | 406.9 | −3368.1 | 416.7 |

| RSV (RK) | −3168.4 | −3464.7 | −3669.8 | |||

| RSV-DPM-ret (RK) | −3171.8 | −3.4 | −3461.3 | 3.4 | −3676.9 | −7.0 |

| RSV-DPM (RK) | −2536.9 | 631.5 | −2973.8 | 490.9 | −3201.6 | 468.2 |

| RSV-DPM-ind (RK) | −2526.7 | 641.8 | −3009.4 | 455.3 | −3248.1 | 421.7 |

| Panel C: SPY | ||||||

| RSV (SRV) | −3328.5 | −3846.6 | −4067.6 | |||

| RSV-DPM-ret (SRV) | −3327.4 | 1.1 | −3844.5 | 2.1 | −4071.4 | −3.8 |

| RSV-DPM (SRV) | −3289.9 | 38.6 | −3849.9 | −3.3 | −4031.5 | 36.1 |

| RSV-DPM-ind (SRV) | −3273.7 | 54.8 | −3817.2 | 29.5 | −4042.9 | 24.7 |

| RSV (RK) | −3187.8 | −3762.3 | −3996.4 | |||

| RSV-DPM-ret (RK) | −3187.6 | 0.2 | −3768.1 | −5.8 | −3987.6 | 8.8 |

| RSV-DPM (RK) | −3152.9 | 34.9 | −3742.2 | 20.1 | −3946.6 | 49.8 |

| RSV-DPM-ind (RK) | −3112.3 | 75.5 | −3713.9 | 48.4 | −3955.0 | 41.4 |

| Panel D: SKHY | ||||||

| RSV (SRV) | −1722.1 | −1874.3 | −1911.4 | |||

| RSV-DPM-ret (SRV) | −1722.3 | −0.2 | −1873.0 | 1.2 | −1911.0 | 0.4 |

| RSV-DPM (SRV) | −1632.2 | 90.0 | −1782.0 | 92.3 | −1836.5 | 74.8 |

| RSV-DPM-sep (SRV) | −1629.8 | 92.4 | −1810.1 | 64.2 | −1856.6 | 54.8 |

| RSV (RK) | −1857.5 | −2013.0 | −2052.1 | |||

| RSV-DPM-ret (RK) | −1857.7 | −0.2 | −2013.3 | −0.3 | −2054.5 | −2.4 |

| RSV-DPM (RK) | −1803.7 | 53.8 | −1962.2 | 50.8 | −2003.0 | 49.1 |

| RSV-DPM-ind (RK) | −1798.2 | 59.3 | −1975.9 | 37.1 | −2016.2 | 35.9 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, J. A Bayesian Semiparametric Realized Stochastic Volatility Model. J. Risk Financial Manag. 2021, 14, 617. https://doi.org/10.3390/jrfm14120617

Liu J. A Bayesian Semiparametric Realized Stochastic Volatility Model. Journal of Risk and Financial Management. 2021; 14(12):617. https://doi.org/10.3390/jrfm14120617

Chicago/Turabian StyleLiu, Jia. 2021. "A Bayesian Semiparametric Realized Stochastic Volatility Model" Journal of Risk and Financial Management 14, no. 12: 617. https://doi.org/10.3390/jrfm14120617

APA StyleLiu, J. (2021). A Bayesian Semiparametric Realized Stochastic Volatility Model. Journal of Risk and Financial Management, 14(12), 617. https://doi.org/10.3390/jrfm14120617