The Skewness Risk in the Energy Market

Abstract

:1. Introduction

2. Literature Review

3. Data

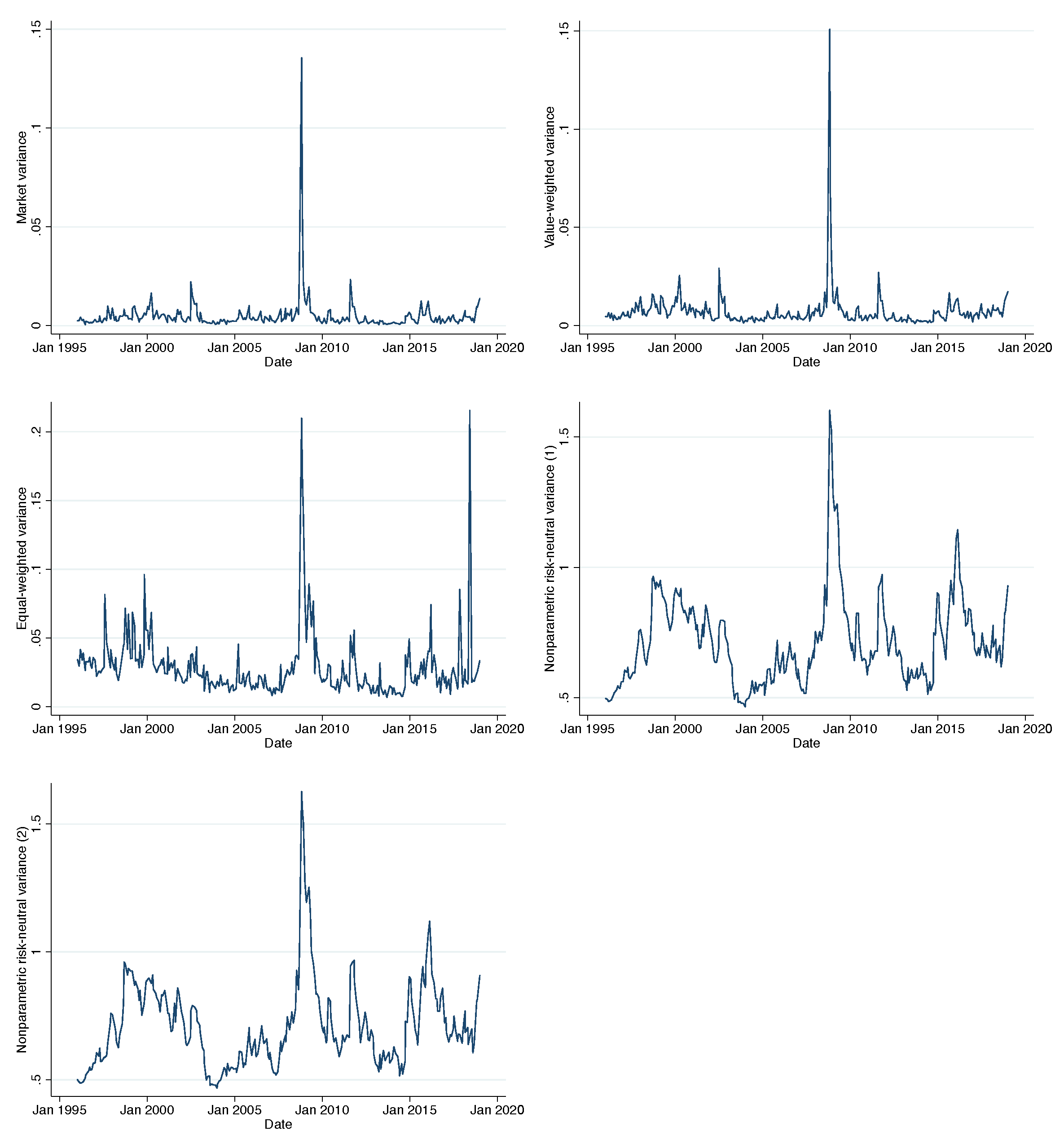

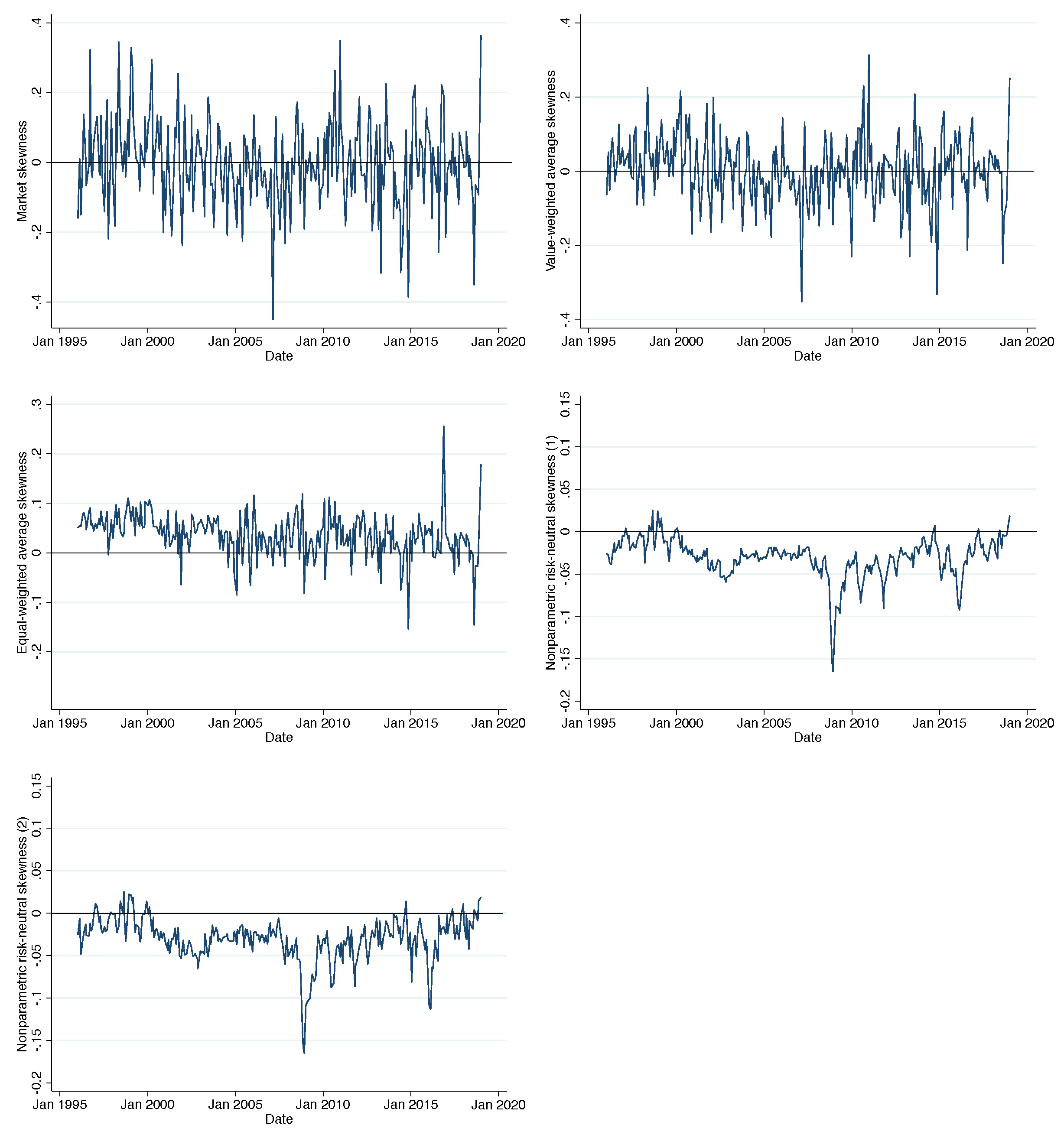

3.1. Energy Market Index (EMI)

3.2. The Energy Market Return and Average Factors

3.3. Control Variables

Default Spread

Term Spread

Illiquidity Measure

Average Correlation

Implied Volatility

Implied Volatility Skew

Put-Call-Parity Implied Volatility Spread

Variance Risk Premium

3.4. Preliminary Analysis

4. Methodology

4.1. Theoretical Background of Predictability in Average Variance and Skewness Factors

4.2. Average Variance and Skewness of the Energy Stocks

4.3. Nonparametric Risk-Neutral Moments

5. Empirical Results

5.1. Baseline Regression

5.2. Controlling for the Economic and Financial Variables

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix A.1. Additional Table

{kind=link}

{kind=link}

| 1.00 | ||

| 0.98 | 1.00 |

Appendix A.2. Predictability in Average Skewness

Appendix A.3. SIC: Standard Industry Classification Codes

- 1300–1300 Oil and gas extraction.

- 1310–1319 Crude petroleum & natural gas.

- 1320–1329 Natural gas liquids.

- 1330–1339 Petroleum and natural gas.

- 1370–1379 Petroleum and natural gas.

- 1380–1380 Oil and gas field services.

- 1381–1381 Drilling oil & gas wells.

- 1382–1382 Oil-gas field exploration.

- 1389–1389 Oil and gas field services.

- 2900–2912 Petroleum refining.

- 2990–2999 Misc. petroleum products.

| 1 | This is also found in Boyer et al. (2009); Bali and Murray (2013); Conrad et al. (2013) and Boyer and Vorkink (2014), among others. |

| 2 | The difficulty in measuring skewness is still present to date; for example, Neuberger (2012) and Jiang et al. (2020), who propose a different measure of computing the skewness factor due to the inconclusive predictive power of skewness that is measured in a standard way; Stilger et al. (2016) and Chordia et al. (2020), who find positive predictive power on the skewness factor and Albuquerque (2012), who reconciles evidence of skewness of return on firm versus aggregate returns. The result observed in this study, together with the current state of the literature, confirms that an accurate measure of skewness of returns is needed to strengthen this area of research. Further, studying the driver of a positive relationship between the cross-sectional average skewness and energy market return should be further investigated and is left for future work. |

| 3 | The authors argue that the results are driven mainly by individual stocks that were less liquid and more expensive to short-sell. |

| 4 | The authors argue that the results are driven mainly by individual stocks that were less liquid and more expensive to short-sell. |

| 5 | The ETF XLE provides precise exposure not only to companies in the oil and gas but also in consumable fuel, energy equipment and services. Details can be found in https://www.ssga.com/library-content/products/factsheets/etfs/us/factsheet-us-en-xle.pdf, accessed on 1 October 2021. |

| 6 | Due to the availablity of data, our sample starts from January 1996 and ends December 2018. The size of a sample period is appropriate for our study to (1) precisely estimates the coefficient of beta (i.e., average skewness variable) and (2) draw a conclusions with acceptable significance level. |

| 7 | Moody’s Corporation, often referred to as Moody’s, is an American business and financial services company. |

| 8 | Following Bollerslev et al. (2009), we first need to quantify the actual return variation. denotes the logarithmic price of the asset. The realized variation over the set period time t to time interval can then be measured in a “model-free” style as: → Return variation , where the convergence depends on , i.e., an increasing number of within-period price observations. This “model-free” realized variance measure based on high-frequency data can generate much more accurate historical observations of the true (unobserved) return variation than other traditional sample variances based on daily or less frequent returns. |

| 9 | The correlation table can be found in Appendix A.1. |

| 10 | See Appendix A.2 for more detail. |

| 11 | The first measure, following by Goyal and Santa-Clara (2003), is based on equal weights: , where is the number of energy firms available in month t. The second measure is following by Bali et al. (2005), is based on value weights: , where is the relative market capitalization of energy stock i in month t. |

| 12 | This confirms that there is no significant difference between (1) taking the average across equal-weighted average individual volatility or (2) selecting at the end of each month the value of individual or and then taking the average. |

| 13 | denotes the time-to-maturity which is set to 30 days. |

| 14 | Values range from 100 to −100 (or 1.0 to −1.0, depending on the convention employed). |

| 15 | Denoted as w for equal and value weights, respectively. |

| 16 | The authors defined two investors, indexed by , update their beliefs following Bayes’s rule and a standard Kalma-Bucy filter. They define an uncertainty parameter that models the investor-specific perception of the noisiness of certain market signals. This is then said to affect investors’ belief and thus their future dividend disagreement. The authors then estimate the comovement of belief disagreement between two investors. |

| 17 |

References

- Albuquerque, Rui. 2012. Skewness in stock returns: Reconciling the evidence on firm versus aggregate returns. Review of Financial Studies 25: 1630–73. [Google Scholar] [CrossRef]

- Amaya, Diego, Peter Christoffersen, Kris Jacobs, and Aurelio Vasquez. 2015. Does realized skewness predict the cross-section of equity returns? Journal of Financial Economics 118: 135–67. [Google Scholar] [CrossRef] [Green Version]

- Amihud, Yakov. 2002. Llliquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets 5: 31–56. [Google Scholar] [CrossRef] [Green Version]

- Atilgan, Yigit, Turan G. Bali, K. Ozgur Demirtas, and A. Doruk Gunaydin. 2019. Global downside risk and equity returns. Journal of International Money and Finance 98: 102065. [Google Scholar] [CrossRef]

- Bali, Turan G., and Scott Murray. 2013. Does risk-neutral skewness predict the cross-section of equity option portfolio returns? Journal of Financial and Quantitative Analysis 48: 1145–71. [Google Scholar] [CrossRef] [Green Version]

- Bali, Turan G., Jianfeng Hu, and Scott Murray. 2019. Option implied volatility, skewness, and kurtosis and the cross-section of expected stock returns. Available online: https://ssrn.com/abstract=2322945 (accessed on 1 October 2021).

- Bali, Turan G., K. Ozgur Demirtas, and Haim Levy. 2009. Is there an intertemporal relation between downside risk and expected returns? Journal of Financial and Quantitative Analysis 44: 883–909. [Google Scholar] [CrossRef] [Green Version]

- Bali, Turan G., Nusret Cakici, Xuemin Yan, and Zhe Zhang. 2005. Does idiosyncratic risk really matter? Journal of Finance 60: 905–29. [Google Scholar] [CrossRef]

- Bollerslev, Tim, George Tauchen, and Hao Zhou. 2009. Expected stock returns and variance risk premia. Review of Financial Studies 22: 4463–92. [Google Scholar] [CrossRef]

- Bollerslev, Tim, Viktor Todorov, and Lai Xu. 2015. Tail risk premia and return predictability. Journal of Financial Economics 118: 113–34. [Google Scholar]

- Boyer, Brian H., and Keith Vorkink. 2014. Stock options as lotteries. Journal of Finance 69: 1485–527. [Google Scholar]

- Boyer, Brian, Todd Mitton, and Keith Vorkink. 2009. Expected idiosyncratic skewness. Review of Financial Studies 23: 169–202. [Google Scholar] [CrossRef]

- Buraschi, Andrea, Fabio Trojani, and Andrea Vedolin. 2014. When uncertainty blows in the orchard: Comovement and equilibrium volatility risk premia. Journal of Finance 69: 101–37. [Google Scholar] [CrossRef]

- Byun, Suk-Joon, and Da-Hea Kim. 2016. Gambling preference and individual equity option returns. Journal of Financial Economics 122: 155–74. [Google Scholar] [CrossRef]

- Chang, Bo Young, Peter Christoffersen, and Kris Jacobs. 2013. Market skewness risk and the cross section of stock returns. Journal of Financial Economics 107: 46–68. [Google Scholar] [CrossRef]

- Chordia, Tarun, Tse-Chun Lin, and Vincent Xiang. 2020. Risk-neutral skewness, informed trading, and the cross-section of stock returns. Journal of Financial and Quantitative Analysis 56: 1713–37. [Google Scholar] [CrossRef]

- Chuliá, Helena, Dolores Furió, and Jorge M. Uribe. 2019. Volatility spillovers in energy markets. Energy Journal 40: 127–52. [Google Scholar] [CrossRef]

- Ciner, Cetin. 2013. Oil and stock returns: Frequency domain evidence. Journal of International Financial Markets, Institutions and Money 23: 1–11. [Google Scholar] [CrossRef]

- Conrad, Jennifer, Robert F. Dittmar, and Eric Ghysels. 2013. Ex ante skewness and expected stock returns. Journal of Finance 68: 85–124. [Google Scholar] [CrossRef] [Green Version]

- Da Fonseca, José, and Yahua Xu. 2017. Higher moment risk premiums for the crude oil market: A downside and upside conditional decomposition. Energy Economics 67: 410–22. [Google Scholar] [CrossRef]

- Dawar, Ishaan, Anupam Dutta, Elie Bouri, and Tareq Saeed. 2021. Crude oil prices and clean energy stock indices: Lagged and asymmetric effects with quantile regression. Renewable Energy 163: 288–99. [Google Scholar] [CrossRef]

- Dertwinkel-Kalt, Markus, and Mats Köster. 2019. Salience and skewness preferences. Journal of the European Economic Association 18: 2057–107. [Google Scholar] [CrossRef]

- Dittmar, Robert F. 2002. Nonlinear pricing kernels, kurtosis preference, and evidence from the cross section of equity returns. Journal of Finance 57: 369–403. [Google Scholar] [CrossRef]

- Dutta, Anupam, Elie Bouri, Debojyoti Das, and David Roubaud. 2020. Assessment and optimization of clean energy equity risks and commodity price volatility indexes: Implications for sustainability. Journal of Cleaner Production 243: 118669. [Google Scholar] [CrossRef]

- Gagnon, Marie-Hélène, and Gabriel J. Power. 2020. International oil market risk anticipations and the cushing bottleneck: Option-implied evidence. Energy Journal 41. [Google Scholar] [CrossRef]

- Gao, Xuechen, Xuewu Wang, and Zhipeng Yan. 2019. Attention: Implied volatility spreads and stock returns. Journal of Behavioral Finance 21: 385–98. [Google Scholar] [CrossRef]

- Gennaioli, Nicola, Pedro Bordalo, and Andrei Shleifer. 2013. Salience theory of choice under risk. Quarterly Journal of Economics 127: 1243–85. [Google Scholar]

- Gilbert, Richard J., and Knut Anton Mork. 1984. Will oil markets tighten again? A survey of policies to manage possible oil supply disruptions. Journal of Policy Modeling 6: 111–42. [Google Scholar] [CrossRef]

- Goyal, Amit, and Pedro Santa-Clara. 2003. Idiosyncratic risk matters! Journal of Finance 58: 975–1007. [Google Scholar] [CrossRef]

- Hamilton, James Douglas. 1983. Oil and the macroeconomy since World War II. Journal of Political Economy 91: 228–48. [Google Scholar]

- Harvey, Campbell Russell, and Akhtar Siddique. 2000. Conditional skewness in asset pricing tests. Journal of Finance 55: 1263–95. [Google Scholar] [CrossRef]

- Huang, Wei, Qianqiu Liu, S. Ghon Rhee, and Feng Wu. 2012. Extreme downside risk and expected stock returns. Journal of Banking and Finance 36: 1492–502. [Google Scholar] [CrossRef]

- Jiang, Lei, Ke Wu, Guofu Zhou, and Yifeng Zhu. 2020. Stock return asymmetry: Beyond skewness. Journal of Financial and Quantitative Analysis 55: 357–86. [Google Scholar] [CrossRef]

- Jondeau, Eric, Qunzi Zhang, and Xiaoneng Zhu. 2019. Average skewness matters. Journal of Financial Economics 134: 29–47. [Google Scholar] [CrossRef]

- Kelly, Bryan, and Hao Jiang. 2014. Tail risk and asset prices. Review of Financial Studies 27: 2841–71. [Google Scholar] [CrossRef] [Green Version]

- Kumar, Alok. 2009. Who gambles in the stock market? Journal of Finance 64: 1889–933. [Google Scholar] [CrossRef]

- Londono, Juan M., and Hao Zhou. 2017. Variance risk premiums and the forward premium puzzle. Journal of Financial Economics 124: 415–40. [Google Scholar] [CrossRef] [Green Version]

- Long, Huaigang, Yanjian Zhu, Lifang Chen, and Yuexiang Jiang. 2019. Tail risk and expected stock returns around the world. Pacific-Basin Finance Journal 56: 162–78. [Google Scholar] [CrossRef]

- López, Raquel. 2018. The behaviour of energy-related volatility indices around scheduled news announcements: Implications for variance swap investments. Energy Economics 72: 356–64. [Google Scholar] [CrossRef]

- Maghyereh, Aktham I., Basel Awartani, and Elie Bouri. 2016. The directional volatility connectedness between crude oil and equity markets: New evidence from implied volatility indexes. Energy Economics 57: 78–93. [Google Scholar] [CrossRef] [Green Version]

- Merton, Robert C. 1976. Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics 3: 125–44. [Google Scholar] [CrossRef] [Green Version]

- Mitton, Todd, and Keith Vorkink. 2007. Equilibrium underdiversification and the preference for skewness. Review of Financial Studies 20: 1255–88. [Google Scholar] [CrossRef]

- Mohrschladt, Hannes, and Judith C. Schneider. 2021. Option-implied skewness: Insights from itm-options. Journal of Economic Dynamics and Control 131: 104227. [Google Scholar] [CrossRef]

- Neuberger, Anthony. 2012. Realized skewness. Review of Financial Studies 25: 3423–55. [Google Scholar] [CrossRef]

- Pollet, Joshua M., and Mungo Wilson. 2010. Average correlation and stock market returns. Journal of Financial Economics 96: 364–80. [Google Scholar] [CrossRef]

- Press, S. James. 1967. A compound events model for security prices. Journal of Business 40: 317–35. [Google Scholar] [CrossRef]

- Ruan, Xinfeng, and Jin E. Zhang. 2018. Risk-neutral moments in the crude oil market. Energy Economics 72: 583–600. [Google Scholar] [CrossRef]

- Ruan, Xinfeng, and Jin E. Zhang. 2019. Moment spreads in the energy market. Energy Economics 81: 598–609. [Google Scholar] [CrossRef]

- Stilger, Przemysaw S., Alexandros Kostakis, and Ser-Huang Poon. 2016. What does risk-neutral skewness tell us about future stock returns? Management Science 63: 1814–34. [Google Scholar] [CrossRef] [Green Version]

- Van Hoang, Thi Hong, Syed Jawad Hussain Shahzad, Robert L. Czudaj, and Javed Ahmad Bhat. 2019. How do oil shocks impact energy consumption? A disaggregated analysis for us. Energy Journal 40. [Google Scholar] [CrossRef] [Green Version]

- Xing, Yuhang, Xiaoyan Zhang, and Rui Zhao. 2010. What does the individual option volatility smirk tell us about future equity returns? Journal of Financial and Quantitative Analysis 45: 641–62. [Google Scholar] [CrossRef]

- Yan, Shu. 2011. Jump risk, stock returns, and slope of implied volatility smile. Journal of Financial Economics 99: 216–33. [Google Scholar] [CrossRef]

| Year | Mean | SD | Skewness | Kurtosis | Minimum | Median | Maximum |

|---|---|---|---|---|---|---|---|

| 1996 | 0.0249 | 0.0288 | −0.8207 | 3.4403 | −0.0442 | 0.0258 | 0.0630 |

| 1997 | 0.0224 | 0.0418 | −0.1868 | 1.9234 | −0.0558 | 0.0211 | 0.0782 |

| 1998 | 0.0048 | 0.0633 | 0.2638 | 2.6285 | −0.1042 | −0.0084 | 0.1364 |

| 1999 | 0.0243 | 0.0645 | 1.1669 | 3.1001 | −0.0512 | 0.0058 | 0.1575 |

| 2000 | 0.0284 | 0.0631 | 0.3469 | 1.6690 | −0.0519 | 0.0062 | 0.1371 |

| 2001 | −0.0050 | 0.0486 | 0.7433 | 2.7513 | −0.0735 | −0.0083 | 0.1005 |

| 2002 | −0.0024 | 0.0518 | −0.5885 | 2.5463 | −0.1086 | 0.0046 | 0.0761 |

| 2003 | 0.0233 | 0.0453 | 1.1138 | 3.2004 | −0.0216 | 0.0191 | 0.1294 |

| 2004 | 0.0262 | 0.0317 | 0.4041 | 2.1495 | −0.0202 | 0.0114 | 0.0885 |

| 2005 | 0.0272 | 0.0664 | 0.2600 | 3.4421 | −0.0966 | 0.0237 | 0.1806 |

| 2006 | 0.0215 | 0.0570 | −0.0465 | 2.2568 | −0.0848 | 0.0370 | 0.1274 |

| 2007 | 0.0269 | 0.0381 | −0.0847 | 1.7228 | −0.0386 | 0.0306 | 0.0778 |

| 2008 | −0.0095 | 0.0759 | −0.3255 | 1.9853 | −0.1512 | 0.0008 | 0.1048 |

| 2009 | 0.0201 | 0.0566 | −0.9197 | 3.8556 | −0.1227 | 0.0331 | 0.1129 |

| 2010 | 0.0209 | 0.0590 | −0.5936 | 2.0549 | −0.0962 | 0.0466 | 0.0913 |

| 2011 | 0.0117 | 0.0712 | 0.2256 | 2.9588 | −0.1152 | 0.0115 | 0.1631 |

| 2012 | 0.0076 | 0.0466 | −0.9331 | 3.7565 | −0.1066 | 0.0171 | 0.0704 |

| 2013 | 0.0234 | 0.0280 | 0.1083 | 2.2029 | −0.0192 | 0.0255 | 0.0767 |

| 2014 | −0.0051 | 0.0510 | −0.4290 | 1.7975 | −0.0957 | 0.0133 | 0.0592 |

| 2015 | −0.0112 | 0.0632 | 0.8119 | 2.7141 | −0.0902 | −0.0353 | 0.1266 |

| 2016 | 0.0291 | 0.0504 | 0.5486 | 1.9749 | −0.0324 | 0.0218 | 0.1185 |

| 2017 | 0.0035 | 0.0424 | 1.0075 | 3.4931 | −0.0494 | −0.0087 | 0.1083 |

| 2018 | −0.0101 | 0.0690 | −0.5445 | 2.2442 | −0.1324 | 0.0113 | 0.1007 |

| Total | 0.0132 | 0.0561 | −0.0613 | 3.2927 | −0.1512 | 0.0131 | 0.1806 |

| Energy Stocks | Energy Options | |||

|---|---|---|---|---|

| Year | No. Firms | Market Cap | No. Firms | Market Cap |

| 1996 | 273 | 423 | 90 | 395 |

| 1997 | 270 | 555 | 116 | 523 |

| 1998 | 252 | 567 | 125 | 544 |

| 1999 | 227 | 546 | 122 | 526 |

| 2000 | 196 | 611 | 104 | 568 |

| 2001 | 206 | 652 | 95 | 612 |

| 2002 | 165 | 548 | 86 | 526 |

| 2003 | 150 | 536 | 85 | 515 |

| 2004 | 151 | 712 | 99 | 692 |

| 2005 | 160 | 993 | 116 | 964 |

| 2006 | 175 | 1133 | 123 | 1093 |

| 2007 | 177 | 1334 | 119 | 1284 |

| 2008 | 172 | 1340 | 111 | 1278 |

| 2009 | 170 | 986 | 111 | 950 |

| 2010 | 163 | 1076 | 107 | 1021 |

| 2011 | 170 | 1318 | 116 | 1244 |

| 2012 | 167 | 1290 | 119 | 1214 |

| 2013 | 160 | 1449 | 122 | 1361 |

| 2014 | 159 | 1574 | 127 | 1478 |

| 2015 | 151 | 1238 | 127 | 1177 |

| 2016 | 149 | 1176 | 123 | 1124 |

| 2017 | 152 | 1249 | 125 | 1190 |

| 2018 | 142 | 1345 | 122 | 1273 |

| Total | 494 | 949 | 266 | 934 |

| Panel A: Summary Statistics | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | SD | Skewness | Kurtosis | Minimum | Median | Maximum | N | ||||

| 0.0025 | 0.0132 | 0.1541 | 5.9435 | −0.0435 | 0.0018 | 0.0639 | 276 | ||||

| 0.0050 | 0.0094 | 10.7269 | 142.0966 | 0.0005 | 0.0032 | 0.1356 | 276 | ||||

| −0.0039 | 0.1231 | −0.0376 | 4.1341 | −0.4507 | −0.0071 | 0.3631 | 276 | ||||

| 0.0072 | 0.0105 | 10.1142 | 131.3646 | 0.0011 | 0.0052 | 0.1508 | 276 | ||||

| 0.0031 | 0.0903 | −0.2623 | 4.6761 | −0.3521 | 0.0051 | 0.3135 | 276 | ||||

| 0.0289 | 0.0247 | 4.3528 | 28.6839 | 0.0070 | 0.0232 | 0.2155 | 276 | ||||

| 0.0369 | 0.0441 | −0.3589 | 6.9115 | −0.1538 | 0.0420 | 0.2559 | 276 | ||||

| 0.7162 | 0.1735 | 1.6965 | 8.2693 | 0.4650 | 0.6816 | 1.6018 | 276 | ||||

| −0.0308 | 0.0239 | −1.7400 | 9.7367 | −0.1650 | −0.0283 | 0.0249 | 276 | ||||

| 0.7125 | 0.1717 | 1.7722 | 8.7897 | 0.4678 | 0.6796 | 1.6268 | 276 | ||||

| −0.0302 | 0.0264 | −1.5276 | 8.1326 | −0.1653 | −0.0272 | 0.0251 | 276 | ||||

| Panel B: Correlation Matrix | |||||||||||

| 1 | |||||||||||

| −0.0021 | 1 | ||||||||||

| 0.0413 | 0.0555 | 1 | |||||||||

| 0.0195 | 0.9306 | 0.0752 | 1 | ||||||||

| 0.0648 | 0.0575 | 0.8675 | 0.0753 | 1 | |||||||

| −0.0165 | 0.5973 | 0.0711 | 0.6383 | 0.1031 | 1 | ||||||

| −0.091 | 0.0667 | 0.6617 | 0.0803 | 0.6597 | 0.1594 | 1 | |||||

| −0.0055 | 0.6193 | 0.1045 | 0.7016 | 0.0896 | 0.6291 | 0.0671 | 1 | ||||

| −0.0298 | −0.5175 | −0.0055 | −0.4788 | −0.0234 | −0.3488 | −0.0452 | −0.5381 | 1 | |||

| −0.0076 | 0.6155 | 0.1061 | 0.6979 | 0.0923 | 0.6266 | 0.0691 | 0.9984 | −0.5371 | 1 | ||

| −0.0893 | −0.4776 | 0.0483 | −0.4363 | 0.0162 | −0.2832 | 0.0357 | −0.4777 | 0.9286 | −0.4739 | 1 | |

| Panel A: Summary Statistics of Control Variables | ||||||||

|---|---|---|---|---|---|---|---|---|

| 0.0367 | 0.0091 | −0.2940 | 2.3091 | 0.0173 | 0.0379 | 0.0588 | ||

| −0.0140 | 0.0060 | −1.4891 | 6.9020 | −0.0405 | −0.0134 | −0.0011 | ||

| 0.0600 | 0.0228 | 0.3681 | 3.3019 | 0.0021 | 0.0582 | 0.1330 | ||

| 0.0023 | 0.0196 | 0.1147 | 4.2492 | −0.0676 | 0.0013 | 0.0844 | ||

| 0.0957 | 0.1170 | 3.7187 | 23.2601 | 0.0099 | 0.0593 | 1.0336 | ||

| 0.0124 | 0.0129 | 3.7522 | 26.5037 | 0.0020 | 0.0085 | 0.1273 | ||

| 0.2565 | 0.0880 | 2.6363 | 14.3155 | 0.1377 | 0.2380 | 0.8002 | ||

| 0.0410 | 0.0413 | 4.3437 | 33.3495 | 0.0001 | 0.0333 | 0.4101 | ||

| Panel B: Correlation Matrix between Control Variables | ||||||||

| 1 | ||||||||

| −0.2367 | 1 | |||||||

| −0.2810 | −0.2150 | 1 | ||||||

| 0.0592 | 0.0190 | −0.8616 | 1 | |||||

| −0.0042 | 0.0075 | −0.0245 | −0.0099 | 1 | ||||

| 0.1726 | −0.2115 | 0.0202 | 0.0322 | 0.1392 | 1 | |||

| 0.2091 | −0.5638 | 0.0453 | 0.2064 | 0.0304 | 0.3923 | 1 | ||

| 0.1454 | −0.2335 | −0.0939 | 0.2216 | 0.0202 | 0.1747 | 0.4547 | 1 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

|---|---|---|---|---|---|---|---|---|---|---|

| Panel A: Individual Variables | ||||||||||

| 0.14 | ||||||||||

| (0.202) | ||||||||||

| 0.03 | ||||||||||

| (0.177) | ||||||||||

| 0.14 | ||||||||||

| (0.179) | ||||||||||

| 0.06 ** | ||||||||||

| (0.046) | ||||||||||

| 0.00 | ||||||||||

| (0.982) | ||||||||||

| −0.04 | ||||||||||

| (0.479) | ||||||||||

| −0.00 | ||||||||||

| (0.718) | ||||||||||

| −0.02 | ||||||||||

| (0.849) | ||||||||||

| −0.01 | ||||||||||

| (0.666) | ||||||||||

| −0.05 | ||||||||||

| (0.603) | ||||||||||

| Adj. | −0.26% | 0.20% | −0.24% | 1.11% | −0.37% | −0.18% | −0.33% | −0.35% | −0.32% | −0.26% |

| Panel B: Individual Variables with Current Market Return | ||||||||||

| −0.03 | −0.03 | −0.03 | −0.04 | −0.03 | −0.03 | −0.04 | −0.03 | −0.04 | −0.04 | |

| (0.557) | (0.488) | (0.561) | (0.383) | (0.477) | (0.518) | (0.434) | (0.473) | (0.426) | (0.460) | |

| 0.12 | ||||||||||

| (0.318) | ||||||||||

| 0.03 | ||||||||||

| (0.180) | ||||||||||

| 0.12 | ||||||||||

| (0.272) | ||||||||||

| 0.06 ** | ||||||||||

| (0.041) | ||||||||||

| −0.00 | ||||||||||

| (0.999) | ||||||||||

| −0.04 | ||||||||||

| (0.505) | ||||||||||

| −0.01 | ||||||||||

| (0.656) | ||||||||||

| −0.02 | ||||||||||

| (0.831) | ||||||||||

| −0.01 | ||||||||||

| (0.603) | ||||||||||

| −0.06 | ||||||||||

| (0.594) | ||||||||||

| Adj. | −0.56% | −0.06% | −0.53% | 0.91% | −0.63% | 0.46% | −0.57% | −0.61% | −0.55% | −0.50% |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Panel A: Combination of Variables | |||||

| 0.12 | |||||

| (0.654) | |||||

| 0.03 | |||||

| (0.228) | |||||

| 0.09 | |||||

| (0.694) | |||||

| 0.06 ** | |||||

| (0.050) | |||||

| 0.01 | |||||

| (0.925) | |||||

| −0.04 | |||||

| (0.472) | |||||

| −0.01 | |||||

| (0.622) | |||||

| −0.05 | −0.06 | ||||

| (0.665) | (0.638) | ||||

| Adj. | −0.10% | 0.81% | −0.54% | −0.63% | −0.61% |

| Panel B: Combination Variables with Current Market Return | |||||

| −0.03 | −0.05 | −0.01 | −0.04 | −0.04 | |

| (0.641) | (0.415) | (0.835) | (0.551) | (0.542) | |

| 0.10 | −0.24 | 0.23 | 0.24 | 0.27 | |

| (0.718) | (0.885) | (0.534) | (0.481) | (0.443) | |

| 0.03 | −0.07 | 0.05 ** | 0.03 | 0.03 | |

| (0.227) | (0.161) | (0.042) | (0.182) | (0.175) | |

| 0.27 | |||||

| (0.854) | |||||

| 0.14 ** | |||||

| (0.034) | |||||

| −0.05 | |||||

| (0.698) | |||||

| −0.13 * | |||||

| (0.078) | |||||

| −0.02 | |||||

| (0.297) | |||||

| −0.07 | −0.07 | ||||

| (0.611) | (0.580) | ||||

| Adj. | −0.38% | 0.58% | 0.12% | −0.72% | −0.63% |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Business cycle and market illiquidity (1996–2018) | ||||

| −0.04 | −0.03 | |||

| (0.395) | (0.501) | |||

| 0.06 ** | 0.06 ** | 0.05 * | 0.05 * | |

| (0.036) | (0.036) | (0.076) | (0.070) | |

| −0.09 | −0.11 | −0.13 | ||

| (0.659) | (0.753) | (0.729) | ||

| 0.07 | −0.03 | −0.07 | −0.09 | |

| (0.532) | (0.909) | (0.845) | (0.809) | |

| 0.00 | 0.00 | 0.00 | 0.00 | |

| (0.976) | (0.970) | (0.989) | (0.985) | |

| −0.11 | −0.11 | |||

| (0.801) | (0.799) | |||

| 0.39 | 0.34 | |||

| (0.512) | (0.595) | |||

| Adj. | 0.41% | −0.90% | 0.69% | −0.11% |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Panel A:AC(1996–2018) | ||||

| −0.04 | ||||

| (0.422) | ||||

| 0.06 ** | 0.06 ** | 0.06 ** | ||

| (0.046) | (0.041) | (0.037) | ||

| −0.08 | −0.12 | −0.11 | ||

| (0.589) | (0.419) | (0.472) | ||

| Adj. | 1.46% | −0.69% | 0.76% | 0.12% |

| Panel B:VRP(1998–2018) | ||||

| −0.03 | ||||

| (0.549) | ||||

| 0.06 ** | 0.06 ** | 0.06 ** | ||

| (0.045) | (0.048) | (0.043) | ||

| 0.01 | 0.00 | 0.00 | ||

| (0.797) | (0.952) | (0.965) | ||

| Adj. | 1.27% | −0.40% | 0.85% | 0.52% |

| −0.03 | ||||

| (0.599) | ||||

| 0.06 ** | 0.06 ** | 0.06 ** | ||

| (0.045) | (0.048) | (0.043) | ||

| 0.01 | 0.01 | 0.01 | ||

| (0.611) | (0.698) | (0.764) | ||

| Adj. | 1.27% | −0.33% | 0.90% | 0.55% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yoon, J.; Ruan, X.; Zhang, J.E. The Skewness Risk in the Energy Market. J. Risk Financial Manag. 2021, 14, 620. https://doi.org/10.3390/jrfm14120620

Yoon J, Ruan X, Zhang JE. The Skewness Risk in the Energy Market. Journal of Risk and Financial Management. 2021; 14(12):620. https://doi.org/10.3390/jrfm14120620

Chicago/Turabian StyleYoon, Jungah, Xinfeng Ruan, and Jin E. Zhang. 2021. "The Skewness Risk in the Energy Market" Journal of Risk and Financial Management 14, no. 12: 620. https://doi.org/10.3390/jrfm14120620

APA StyleYoon, J., Ruan, X., & Zhang, J. E. (2021). The Skewness Risk in the Energy Market. Journal of Risk and Financial Management, 14(12), 620. https://doi.org/10.3390/jrfm14120620