Household Wealth: Low-Yielding and Poorly Structured?

Abstract

:1. Introduction

2. A New Dataset on Real Returns of Households’ Wealth—Computation Method and Inputs

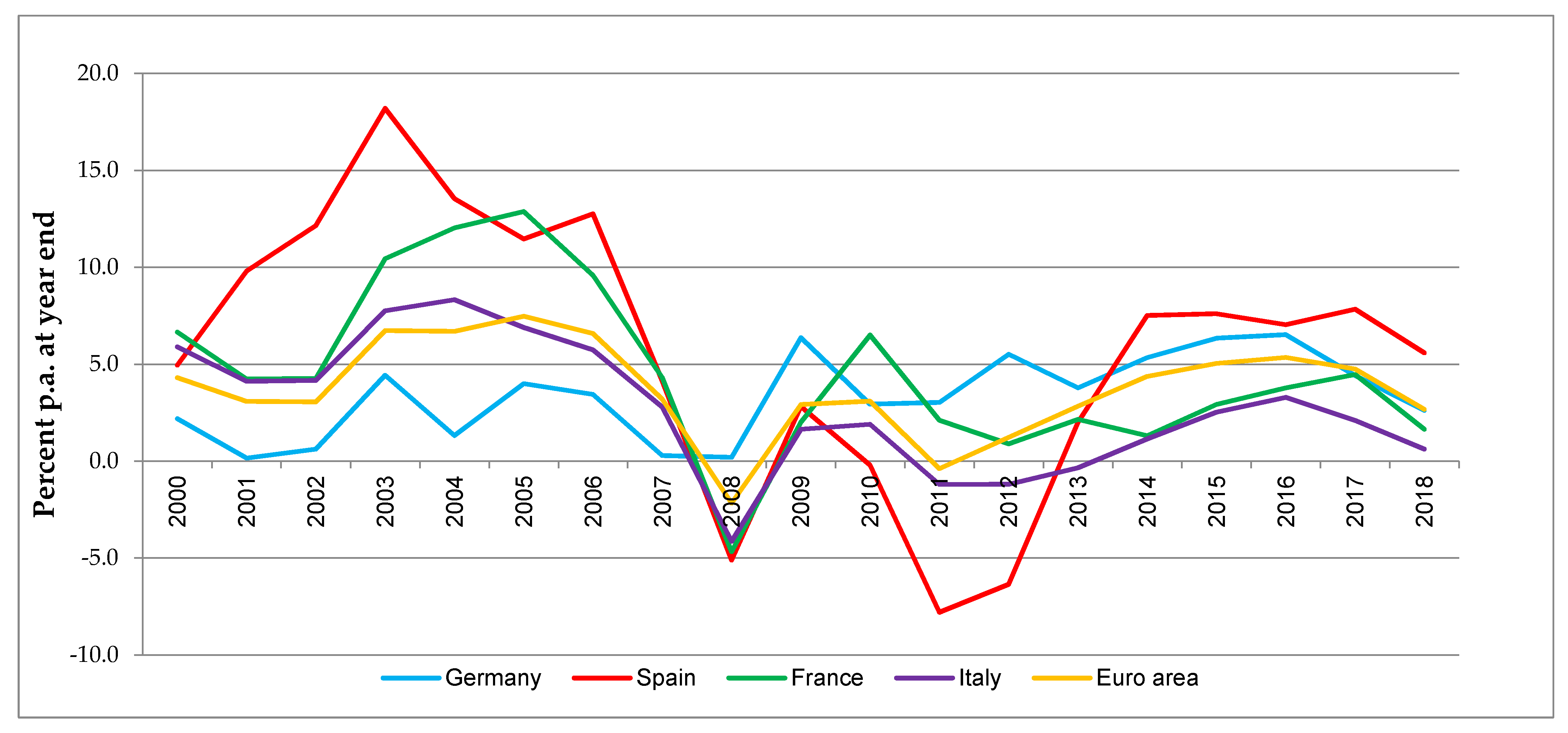

3. Computation Reviewing the “Level Debate”—Developments of Real Yields on Household Wealth from 2000 to 2018

3.1. Real Returns on Total, Financial and Non-Financial Assets

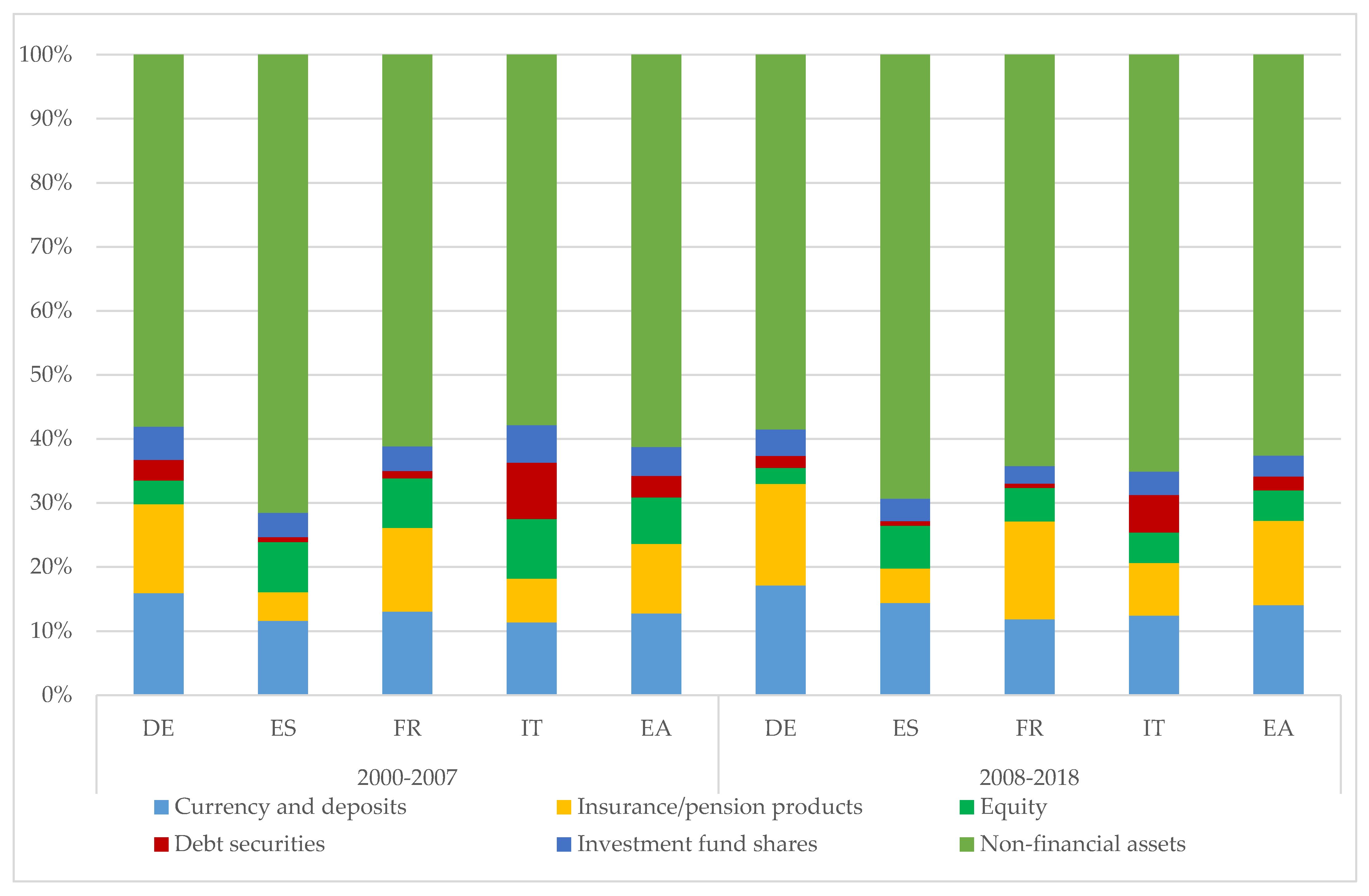

3.2. Portfolio Shifts and Individual Assets’ Contribution to Total Real Return

4. Reviewing the “Efficiency Debate”—Assessment of Households’ Portfolio Performance in 2018

4.1. The Mean-Variance Optimization Approach

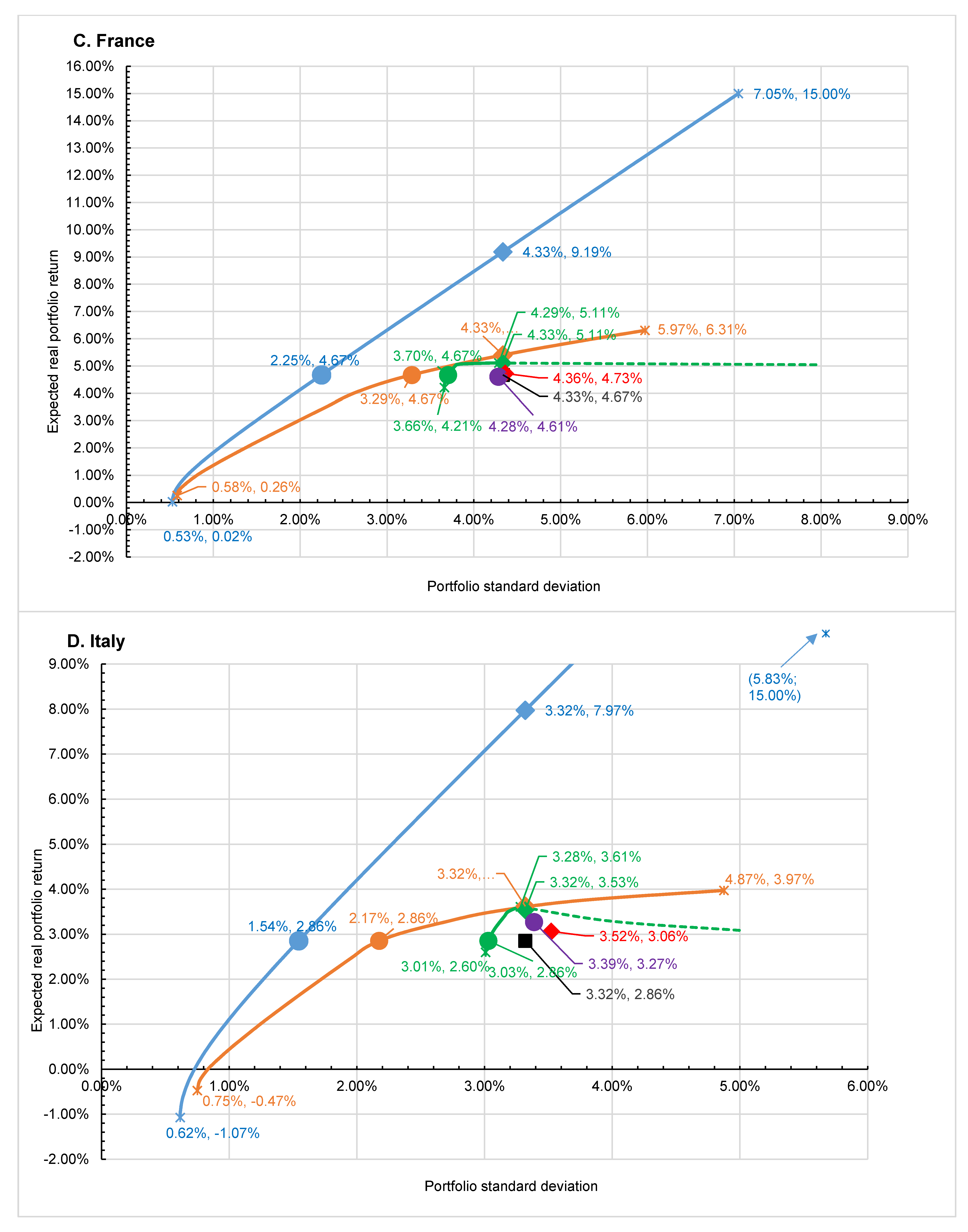

4.1.1. Efficient Frontier Analysis

Model Definitions

An Alternative Portfolio Performance Measure

Model Solutions and Characteristics

4.1.2. Optimal Portfolio Selection—A “Ceteris Paribus” Approach

4.2. The “Heuristic” Approach

4.2.1. Portfolio Definitions

4.2.2. Portfolio Characteristics and Performance

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Adler, Timothy, and Mark Kritzman. 2007. Mean–variance versus full–scale optimisation: In and out of sample. Journal of Asset Management 7: 302–11. [Google Scholar] [CrossRef]

- Andreasch, Michael, Marc Peter Radke, and Manuel Rupprecht. 2020. Rendite privater Haushalte nach Vermögensgruppen—Deutschland versus Österreich. Wirtschaftsdienst 100: 446–53. [Google Scholar] [CrossRef]

- Annuß, Christine, and Manuel Rupprecht. 2016. Anlageverhalten privater Haushalte in Deutschland: Die Rolle der realen Rendite. DIW Quarterly Journal of Economic Research 85: 95–109. [Google Scholar] [CrossRef] [Green Version]

- Badarinza, Christian, John Young Campbell, and Tarun Ramadorai. 2016. International Comparative Household Finance. Annual Review of Economics 8: 111–44. [Google Scholar] [CrossRef] [Green Version]

- Barasinska, Nataliya, Dorothee Schäfer, and Andreas Stephan. 2011. Individual Risk Attitudes and the Composition of Financial Portfolios: Evidence from German Household Portfolios. The Quartery Review of Economics and Finance 52: 1–14. [Google Scholar] [CrossRef] [Green Version]

- Benartzi, Shlomo, and Richard Thaler. 2001. Naive Diversification Strategies in Retirement Saving Plans. The American Economic Review 91: 79–98. [Google Scholar] [CrossRef] [Green Version]

- Benartzi, Shlomo, and Richard Thaler. 2007. Heuristics and Biases in Retirement Savings Behavior. Journal of Economic Perspectives 21: 81–104. [Google Scholar] [CrossRef] [Green Version]

- Bindseil, Ulrich, Clemens Domnick, and Jörg Zeuner. 2015. Critique of accommodating central bank policies and the ‘expropriation of the saver’—A review. In ECB Occasional Paper Series. Frankfurt: European Central Bank, vol. 161, pp. 1–64. [Google Scholar]

- Canner, Niko, Gregory N. Mankiw, and David. N. Weil. 1997. An asset allocation puzzle. The American Economic Review 87: 181–91. [Google Scholar]

- Christensen, Jens Henrik Eggert, and Glenn D. Rudebusch. 2019. A New Normal for Interest Rates? Evidence from Inflation-Indexed Debt. The Review of Economics and Statistics 101: 933–49. [Google Scholar] [CrossRef] [Green Version]

- Corneo, Giacomo, Matthias Keese, and Carsten Schröder. 2009. The Riester Scheme and Private Savings: An Empirical Analysis Based on the German SOEP. Schmollers Jahrbuch 129: 321–32. [Google Scholar] [CrossRef]

- Cremers, Jan-Hein, Mark Kritzman, and Sebastien Page. 2003. Portfolio formation with higher moments and plausible utility. In Revere Street Working Paper Series. Cambridge: Financial Economics, pp. 1–24. [Google Scholar]

- Cremers, Jan-Hein, Mark Kritzman, and Sebastien Page. 2005. Optimal Hedge Fund Allocations: Do Higher Moments Matter. The Journal of Portfolio Management 31: 70–81. [Google Scholar] [CrossRef]

- Deuflhard, Florian, Dimitris Georgarakos, and Inderst Roman. 2019. Financial Literacy and Savings Account Returns. Journal of the European Economic Association 17: 131–64. [Google Scholar] [CrossRef] [Green Version]

- Deutsche Bundesbank. 2015. German households’ saving and investment behavior in light of the low-interest-rate environment. In Monthly Report, October. Frankfurt: Deutsche Bundesbank, pp. 13–31. [Google Scholar]

- Dimson, Elroy, Paul Marsh, and Mike Staunten. 2009. Triumph of the Optimists—101 Years of Global Investment Returns. Princeton: Princeton University Press. [Google Scholar]

- Duca, John, John Muellbauer, and Anthony Murphy. Forthcoming. What Drives House Price Cycles? International Experience and Policy Issues. Journal of Economic Literature.

- Engen, Eric, William G. Gale, and John K. Scholz. 1996. The Illusory Effect of Saving Incentives on Saving. Journal of Economic Perspectives 10: 113–38. [Google Scholar] [CrossRef]

- European Central Bank. 2014. New international standards in statistics—enhancements to methodology and data availability. In Monthly Bulletin, August. Frankfurt: European Central Bank, pp. 83–97. [Google Scholar]

- European Central Bank. 2020a. ECB Announces €750 billion Pandemic Emergency Purchase Programm (PEPP). Available online: https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.pr200318_1~3949d6f266.en.html (accessed on 18 March 2020).

- European Central Bank. 2020b. Monetary Policy Decisions. Available online: https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.mp200604~a307d3429c.en.html (accessed on 4 June 2020).

- European Central Bank. 2020c. Monetary Policy Decisions. Available online: https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.mp201210~8c2778b843.en.html (accessed on 10 December 2020).

- European Commission. 2013. European System of Accounts—ESA 2010. Luxembourg: Publications Office of the European Union. [Google Scholar]

- Fisher, Irving. 1930. The Theory of Interest. New York: The Macmillan Co. [Google Scholar]

- Geiger, Felix, John Muellbauer, and Manuel Rupprecht. 2016. The Housing Market, Household Portfolios and the German Consumer. ECB Working Paper No. 1904. Frankfurt: European Central Bank. [Google Scholar]

- Glick, Reurven. 2020. r* and the Global Economy. Journal of International Money and Finance 102: 102–5. [Google Scholar] [CrossRef]

- Goodhart, Charles, and Manoj Pradhan. 2020. The Great Demographic Reversal—Ageing Society, Waning Inequality, and an Inflation Revival. Cham: Palgrave Macmillan. [Google Scholar]

- Heise, Michael. 2016. How the ECB Hurts Europe’s Savers. The Wall Street Journal. February 2. Available online: https://www.wsj.com/articles/how-the-ecb-hurts-europes-savers-1454445450 (accessed on 22 February 2021).

- Household Finance and Consumption Network. 2020. The Household Finance and Consumption Survey: Results from the 2017 wave. In ECB Statistics Paper 36. Frankfurt: European Central Bank, pp. 1–37. [Google Scholar]

- Jacobs, Heiko, Sebastian Müller, and Marting Weber. 2014. How should individual investors diversify? An empirical evaluation of alternative asset allocation policies. Journal of Financial Markets 19: 62–85. [Google Scholar] [CrossRef] [Green Version]

- Jensen, Michael Cole. 1968. The Performance of Mutual Funds in the Period 1956–64. Journal of Finance 23: 389–416. [Google Scholar] [CrossRef]

- Jorda, Oscar, Katharina Knoll, Dimitry Kuvshinov, Moritz Schularick, and Alan M. Taylor. 2019. The Rate of Return on Everything, 1870–2015. The Quarterly Journal of Economics 134: 1225–98. [Google Scholar] [CrossRef]

- Knoll, Katharina, Moritz Schularick, and Thomas Steger. 2017. No Price Like Home: Global House Prices, 1870–2012. The American Economic Review 107: 331–52. [Google Scholar] [CrossRef] [Green Version]

- Levy, Haim, and Harry Max Markowitz. 1979. Approximating expected utility by a function of mean and variance. The American Economic Review 69: 308–17. [Google Scholar]

- Lukasz, Rachel, and Thomas Smith. 2017. Are Low Real Interest Rates Here to Stay? International Journal of Central Banking 13: 1–42. [Google Scholar]

- Markowitz, Harry Max. 1952. Portfolio Selection. Journal of Finance 7: 77–91. [Google Scholar]

- Markowitz, Harry Max. 1959. Portfolio Selection: Efficient Diversification of Investments. New York: John Wiley & Sons. [Google Scholar]

- Markowitz, Harry Max. 2012. Mean-variance approximation to geometric mean. Annals of Financial Economics 7: 1–30. [Google Scholar] [CrossRef]

- Markowitz, Harry Max. 2014. Mean-variance approximations to expected utility. European Journal of Operational Research 234: 346–55. [Google Scholar] [CrossRef]

- Modigliani, Franco, and Merton Howard Miller. 1958. The Cost of Capital, Corporation Finance and the Theory of Investment. The American Economic Review 48: 261–97. [Google Scholar]

- Oesterreichische Nationalbank. 2019. Liquidität für Haushalte wichtiger als Rendite. Available online: https://www.oenb.at/Presse/20191022_1.html (accessed on 22 October 2019).

- Piketty, Thomas, and Gabriel Zucman. 2014. Capital is Back: Wealth-Income Ratios in Rich Countries 1700–2010. The Quarterly Journal of Economics 129: 1255–310. [Google Scholar] [CrossRef] [Green Version]

- Radke, Marc Peter, and Manuel Rupprecht. 2018. Was zehn Jahre Niedrigzinsen für die Sparer in Europa bedeuten. Börsenzeitung 204. October 24. Available online: https://www.boersen-zeitung.de/index.php?li=1&artid=2018204038&artsubm=&subm=) (accessed on 25 October 2020).

- Radke, Marc Peter, and Manuel Rupprecht. 2019. The Bill, Please! Households’ Real Returns on Financial Assets Since the Introduction of the Euro. Intereconomics, Review of European Economic Policy 54: 106–13. [Google Scholar] [CrossRef] [Green Version]

- Rupprecht, Manuel. 2018. Low Interest Rates and Household Portfolio Behaviour in Euro Area Countries. Intereconomics, Review of European Economic Policy 53: 174–78. [Google Scholar] [CrossRef] [Green Version]

- Rupprecht, Manuel. 2020. Income and Wealth of Euro Area Households in Times of Ultra-Loose Monetary Policy: Stylised facts from new national and financial accounts data. Empirica 47: 281–302. [Google Scholar] [CrossRef]

- Samuelson, Paul Anthony. 1970. The fundamental approximation theorem of portfolio analysis in terms of means, variances and higher moments. The Review of Economic Studies 37: 537–42. [Google Scholar] [CrossRef]

- Schröder, Carsten, Johannes König, Alexandra Fedorets, Jan Goebel, Markus M. Grabka, Holger Lüthen, Maria Metzing, Felicitas Schikora, and Stefan Liebig. 2020. The economic research potentials of the German Socio-Economic Panel study. German Economic Review 21: 313–33. [Google Scholar] [CrossRef]

- Sharpe, William Forsyth. 1966. Mutual Fund Performance. Journal of Business 39: 119–38. [Google Scholar] [CrossRef]

- Sharpe, William Forsyth. 1991. Capital asset prices with and without negative holdings. The Journal of Finance 46: 489–509. [Google Scholar] [CrossRef]

- Tobin, James. 1969a. Liquidiy preference as behaviour towards risk. Review of Economic Studies 25: 65–86. [Google Scholar] [CrossRef]

- Tobin, James. 1969b. A general equilibrium approach to monetary theory. Journal of Money, Credit and Banking 1: 15–29. [Google Scholar] [CrossRef]

- Tobin, James, and William Brainard. 1968. Pitfalls in financial model building. American Economic Review 58: 99–122. [Google Scholar]

- Tobin, James, and William Brainard. 1977. Asset Markets and the Cost of Capital. In Economic Progress: Private Values and Public Policy (Essays in Honor of William Fellner). Edited by R. Nelson and B. Balassa. Amsterdam: Elsevier North-Holland, pp. 235–62. [Google Scholar]

- Treynor, Jack Lawrence. 1965. How to Rate Management of Investment Funds. Harvard Business Review 43: 63–75. [Google Scholar]

- United Nations. 2010. System of National Accounts 2008. New York: United Nations. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| A. Germany | |||||||||

| Total Wealth | Financial Wealth | Non-Financial Wealth | |||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 2.06 | 4.28 | 3.34 | 2.02 | 1.77 | 1.87 | 2.06 | 6.05 | 4.37 |

| Median | 1.75 | 4.41 | 3.44 | 2.17 | 2.55 | 2.55 | 2.60 | 6.47 | 3.86 |

| Maximum | 4.43 | 6.52 | 6.52 | 5.61 | 5.81 | 5.81 | 3.86 | 9.37 | 9.37 |

| Minimum | 0.16 | 0.19 | 0.16 | −1.53 | −3.48 | −3.48 | −0.59 | 2.34 | −0.59 |

| Std. Dev. | 1.72 | 1.99 | 2.15 | 2.54 | 2.74 | 2.58 | 1.76 | 2.25 | 2.85 |

| Skewness | 0.23 | −0.60 | −0.08 | −0.07 | −0.64 | −0.46 | −0.45 | −0.26 | 0.04 |

| Kurtosis | 1.44 | 2.53 | 1.85 | 1.81 | 2.48 | 2.34 | 1.60 | 2.26 | 2.18 |

| Jarque–Bera | 0.88 | 0.76 | 1.07 | 0.48 | 0.88 | 1.00 | 0.92 | 0.37 | 0.54 |

| Probability | 0.64 | 0.68 | 0.59 | 0.79 | 0.64 | 0.61 | 0.63 | 0.83 | 0.76 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| B. Spain | |||||||||

| Total Wealth | Financial Wealth | Non-Financial Wealth | |||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 10.87 | 1.90 | 5.68 | 1.62 | 1.44 | 1.51 | 14.55 | 2.28 | 7.45 |

| Median | 11.80 | 2.81 | 7.04 | 3.29 | 1.55 | 2.01 | 14.89 | 0.29 | 9.19 |

| Maximum | 18.20 | 7.84 | 18.20 | 7.44 | 11.71 | 11.71 | 22.64 | 10.78 | 22.64 |

| Minimum | 4.14 | −7.79 | −7.79 | −7.26 | −8.81 | −8.81 | 4.90 | −10.10 | −10.10 |

| Std. Dev. | 4.59 | 5.96 | 6.98 | 5.38 | 5.39 | 5.23 | 5.65 | 7.99 | 9.30 |

| Skewness | −0.15 | −0.53 | −0.40 | −0.48 | 0.03 | −0.18 | −0.36 | −0.35 | −0.42 |

| Kurtosis | 2.28 | 1.75 | 2.55 | 1.79 | 3.07 | 2.54 | 2.36 | 1.70 | 2.33 |

| Jarque–Bera | 0.20 | 1.23 | 0.66 | 0.80 | 0.00 | 0.27 | 0.32 | 1.00 | 0.90 |

| Probability | 0.90 | 0.54 | 0.72 | 0.67 | 1.00 | 0.87 | 0.85 | 0.61 | 0.64 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| C. France | |||||||||

| Total Wealth | Financial Wealth | Non-Financial Wealth | |||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 8.05 | 2.10 | 4.61 | 2.10 | 1.99 | 2.03 | 12.00 | 2.17 | 6.31 |

| Median | 8.12 | 2.11 | 4.24 | 3.00 | 3.46 | 3.46 | 11.49 | 2.53 | 5.04 |

| Maximum | 12.87 | 6.50 | 12.87 | 7.48 | 8.44 | 8.44 | 16.64 | 8.49 | 16.64 |

| Minimum | 4.24 | −4.67 | −4.67 | −6.88 | −8.47 | −8.47 | 5.58 | −2.78 | −2.78 |

| Std. Dev. | 3.63 | 2.77 | 4.30 | 5.11 | 4.51 | 4.63 | 3.46 | 3.31 | 5.97 |

| Skewness | 0.09 | −1.04 | 0.25 | −0.72 | −1.07 | −0.90 | −0.42 | 0.27 | 0.20 |

| Kurtosis | 1.37 | 4.73 | 3.00 | 2.22 | 3.80 | 3.00 | 2.70 | 2.32 | 1.85 |

| Jarque–Bera | 0.90 | 3.33 | 0.20 | 0.90 | 2.38 | 2.54 | 0.27 | 0.34 | 1.18 |

| Probability | 0.64 | 0.19 | 0.91 | 0.64 | 0.30 | 0.28 | 0.87 | 0.84 | 0.55 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| D. Italy | |||||||||

| Total Wealth | Financial Wealth | Non-Financial Wealth | |||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 5.71 | 0.58 | 2.74 | 1.44 | 1.02 | 1.20 | 8.91 | 0.38 | 3.97 |

| Median | 5.82 | 1.15 | 2.53 | 2.08 | 2.28 | 2.28 | 9.96 | 0.15 | 2.65 |

| Maximum | 8.33 | 3.29 | 8.33 | 5.88 | 6.37 | 6.37 | 11.28 | 4.24 | 11.28 |

| Minimum | 2.79 | −4.14 | −4.14 | −4.00 | −9.98 | −9.98 | 5.04 | −3.82 | −3.82 |

| Std. Dev. | 1.93 | 2.15 | 3.28 | 3.91 | 4.77 | 4.32 | 2.14 | 2.43 | 4.87 |

| Skewness | −0.10 | −0.87 | −0.09 | −0.26 | −1.16 | −0.95 | −0.74 | −0.15 | 0.11 |

| Kurtosis | 1.80 | 3.08 | 2.49 | 1.61 | 3.53 | 3.34 | 2.21 | 2.07 | 1.67 |

| Jarque–Bera | 0.49 | 1.40 | 0.23 | 0.73 | 2.58 | 2.95 | 0.94 | 0.44 | 1.43 |

| Probability | 0.78 | 0.50 | 0.89 | 0.69 | 0.28 | 0.23 | 0.63 | 0.80 | 0.49 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| E. Euro Area | |||||||||

| Total Wealth | Financial Wealth | Non-Financial Wealth | |||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 5.14 | 2.70 | 3.73 | 1.81 | 1.65 | 1.72 | 7.35 | 3.37 | 5.05 |

| Median | 5.44 | 2.91 | 3.20 | 2.88 | 2.73 | 2.73 | 7.70 | 3.53 | 6.24 |

| Maximum | 7.48 | 5.35 | 7.48 | 6.43 | 7.45 | 7.45 | 8.44 | 7.07 | 8.44 |

| Minimum | 3.05 | −2.17 | −2.17 | −5.19 | −7.75 | −7.75 | 4.07 | −0.33 | −0.33 |

| Std. Dev. | 1.91 | 2.35 | 2.45 | 4.15 | 4.17 | 4.04 | 1.40 | 2.81 | 3.04 |

| Skewness | −0.05 | −0.84 | −0.61 | −0.61 | −1.01 | −0.85 | −1.84 | 0.00 | −0.59 |

| Kurtosis | 1.20 | 2.76 | 3.20 | 2.00 | 3.46 | 2.90 | 5.07 | 1.33 | 1.83 |

| Jarque–Bera | 1.08 | 1.31 | 1.19 | 0.83 | 1.96 | 2.29 | 5.93 | 1.27 | 2.18 |

| Probability | 0.58 | 0.52 | 0.55 | 0.66 | 0.38 | 0.32 | 0.05 | 0.53 | 0.34 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| A. Germany | ||||||||||||||||||

| Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets | |||||||||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 0.36 | −0.49 | −0.13 | 3.22 | 3.12 | 3.16 | 2.55 | 4.57 | 3.72 | 3.37 | 4.86 | 4.23 | 3.15 | 2.59 | 2.83 | 2.06 | 6.05 | 4.37 |

| Median | 0.25 | −0.27 | 0.02 | 3.34 | 3.07 | 3.12 | 9.69 | 9.54 | 9.54 | 2.61 | 6.50 | 6.50 | 2.91 | 2.59 | 2.59 | 2.60 | 6.47 | 3.86 |

| Maximum | 0.96 | 1.15 | 1.15 | 7.80 | 10.17 | 10.17 | 28.51 | 23.49 | 28.51 | 13.87 | 18.19 | 18.19 | 6.03 | 4.93 | 6.03 | 3.86 | 9.37 | 9.37 |

| Minimum | −0.17 | −1.71 | −1.71 | −2.03 | −2.09 | −2.09 | 40.69 | 42.73 | 42.73 | −7.95 | 18.82 | 18.82 | 1.61 | 0.47 | 0.47 | −0.59 | 2.34 | −0.59 |

| Std. Dev. | 0.41 | 0.85 | 0.81 | 3.27 | 4.10 | 3.67 | 23.67 | 20.46 | 21.25 | 8.94 | 10.48 | 9.63 | 1.42 | 1.27 | 1.32 | 1.76 | 2.25 | 2.85 |

| Skewness | 0.34 | 0.31 | −0.40 | −0.35 | 0.48 | 0.26 | −0.68 | −1.18 | −0.94 | −0.01 | −1.02 | −0.68 | 0.98 | 0.06 | 0.54 | −0.45 | −0.26 | 0.04 |

| Kurtosis | 1.77 | 2.33 | 2.34 | 2.12 | 1.89 | 2.02 | 2.31 | 3.54 | 2.90 | 1.27 | 3.38 | 2.71 | 3.10 | 2.52 | 3.30 | 1.60 | 2.26 | 2.18 |

| Jarque–Bera | 0.65 | 0.38 | 0.85 | 0.42 | 0.99 | 0.98 | 0.77 | 2.68 | 2.82 | 1.00 | 1.96 | 1.52 | 1.28 | 0.11 | 1.00 | 0.92 | 0.37 | 0.54 |

| Probability | 0.72 | 0.83 | 0.65 | 0.81 | 0.61 | 0.61 | 0.68 | 0.26 | 0.24 | 0.61 | 0.38 | 0.47 | 0.53 | 0.95 | 0.61 | 0.63 | 0.83 | 0.76 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| B. Spain | ||||||||||||||||||

| Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets | |||||||||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | −2.18 | −0.37 | −1.13 | 1.90 | 3.37 | 2.75 | 4.59 | 1.45 | 2.77 | 0.77 | 2.39 | 1.71 | 3.93 | 4.98 | 4.54 | 14.55 | 2.28 | 7.45 |

| Median | −2.20 | −0.56 | −1.40 | 2.74 | 1.92 | 2.17 | 10.78 | 3.19 | 4.25 | 0.05 | 2.19 | 2.02 | 4.33 | 4.45 | 4.45 | 14.89 | 0.29 | 9.19 |

| Maximum | −0.67 | 1.61 | 1.61 | 6.10 | 10.80 | 10.80 | 25.36 | 39.55 | 39.55 | 3.65 | 8.06 | 8.06 | 5.67 | 7.82 | 7.82 | 22.64 | 10.78 | 22.64 |

| Minimum | −3.10 | −1.89 | −3.10 | −3.93 | −1.46 | −3.93 | −30.97 | −39.51 | −39.51 | −2.69 | −3.26 | −3.26 | 1.22 | 3.19 | 1.22 | 4.90 | −10.10 | −10.10 |

| Std. Dev. | 0.73 | 1.20 | 1.36 | 3.23 | 4.21 | 3.81 | 20.30 | 20.70 | 20.02 | 2.22 | 3.71 | 3.20 | 1.55 | 1.68 | 1.67 | 5.65 | 7.99 | 9.30 |

| Skewness | 0.89 | 0.32 | 0.55 | −0.61 | 0.41 | 0.31 | −0.58 | −0.08 | −0.29 | 0.05 | 0.16 | 0.46 | −0.66 | 0.42 | 0.10 | −0.36 | −0.35 | −0.42 |

| Kurtosis | 3.55 | 1.72 | 2.28 | 2.42 | 1.80 | 2.43 | 2.04 | 3.15 | 2.66 | 1.89 | 1.93 | 2.44 | 2.20 | 1.65 | 2.59 | 2.36 | 1.70 | 2.33 |

| Jarque–Bera | 1.17 | 0.94 | 1.37 | 0.60 | 0.96 | 0.56 | 0.76 | 0.02 | 0.35 | 0.42 | 0.58 | 0.91 | 0.80 | 1.15 | 0.17 | 0.32 | 1.00 | 0.90 |

| Probability | 0.56 | 0.62 | 0.50 | 0.74 | 0.62 | 0.76 | 0.68 | 0.99 | 0.84 | 0.81 | 0.75 | 0.64 | 0.67 | 0.56 | 0.92 | 0.85 | 0.61 | 0.64 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| C. France | ||||||||||||||||||

| Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets | |||||||||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | 0.22 | 0.08 | 0.14 | 3.05 | 3.03 | 3.04 | 1.62 | 4.01 | 3.00 | 1.51 | 1.57 | 1.55 | 4.04 | 2.57 | 3.19 | 12.00 | 2.17 | 6.31 |

| Median | 0.23 | −0.13 | 0.18 | 3.60 | 2.39 | 2.44 | 4.36 | 9.19 | 7.80 | 2.00 | 2.63 | 2.63 | 5.90 | 3.28 | 3.98 | 11.49 | 2.53 | 5.04 |

| Maximum | 0.72 | 1.40 | 1.40 | 7.34 | 10.96 | 10.96 | 25.03 | 28.77 | 28.77 | 4.91 | 8.83 | 8.83 | 7.40 | 7.29 | 7.40 | 16.64 | 8.49 | 16.64 |

| Minimum | −0.15 | −1.24 | −1.24 | −2.26 | −1.93 | −2.26 | −34.02 | −41.37 | −41.37 | −3.85 | −9.12 | −9.12 | −2.94 | −5.65 | −5.65 | 5.58 | −2.78 | −2.78 |

| Std. Dev. | 0.27 | 0.76 | 0.60 | 3.12 | 4.18 | 3.67 | 19.66 | 19.48 | 19.04 | 3.48 | 4.73 | 4.14 | 3.78 | 3.35 | 3.51 | 3.46 | 3.31 | 5.97 |

| Skewness | 0.44 | 0.11 | −0.11 | −0.41 | 0.77 | 0.52 | −0.70 | −1.10 | −0.93 | −0.29 | −0.85 | −0.75 | −1.03 | −1.31 | −1.03 | −0.42 | 0.27 | 0.20 |

| Kurtosis | 2.74 | 2.28 | 3.29 | 2.20 | 2.25 | 2.41 | 2.39 | 3.72 | 3.12 | 1.49 | 3.62 | 3.54 | 2.45 | 4.57 | 3.42 | 2.70 | 2.32 | 1.85 |

| Jarque–Bera | 0.28 | 0.26 | 0.11 | 0.44 | 1.35 | 1.13 | 0.77 | 2.47 | 2.74 | 0.87 | 1.51 | 2.01 | 1.53 | 4.29 | 3.53 | 0.27 | 0.34 | 1.18 |

| Probability | 0.87 | 0.88 | 0.95 | 0.80 | 0.51 | 0.57 | 0.68 | 0.29 | 0.25 | 0.65 | 0.47 | 0.37 | 0.47 | 0.12 | 0.17 | 0.87 | 0.84 | 0.55 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| D. Italy | ||||||||||||||||||

| Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets | |||||||||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | −1.11 | −0.68 | −0.86 | 2.81 | 3.10 | 2.98 | 1.41 | −0.10 | 0.54 | 2.37 | 2.84 | 2.64 | 2.60 | 1.89 | 2.19 | 8.91 | 0.38 | 3.97 |

| Median | −1.15 | −0.79 | −0.93 | 3.61 | 2.13 | 2.23 | 6.05 | 7.59 | 7.59 | 1.97 | 3.71 | 2.10 | 2.72 | 3.23 | 2.75 | 9.96 | 0.15 | 2.65 |

| Maximum | −0.35 | 0.53 | 0.53 | 6.82 | 14.34 | 14.34 | 17.82 | 23.46 | 23.46 | 6.34 | 9.88 | 9.88 | 3.98 | 5.06 | 5.06 | 11.28 | 4.24 | 11.28 |

| Minimum | −1.68 | −2.12 | −2.12 | −2.68 | −5.29 | −5.29 | −25.58 | −46.97 | −46.97 | −1.58 | −5.81 | −5.81 | 0.60 | −4.38 | −4.38 | 5.04 | −3.82 | −3.82 |

| Std. Dev. | 0.42 | 0.98 | 0.81 | 3.26 | 5.75 | 4.74 | 17.28 | 19.74 | 18.25 | 3.01 | 5.04 | 4.20 | 1.11 | 2.75 | 2.19 | 2.14 | 2.43 | 4.87 |

| Skewness | 0.39 | −0.18 | 0.31 | −0.46 | 0.67 | 0.64 | −0.56 | −1.20 | −1.02 | 0.09 | −0.22 | −0.11 | −0.61 | −1.11 | −1.53 | −0.74 | −0.15 | 0.11 |

| Kurtosis | 2.53 | 1.69 | 2.18 | 2.03 | 2.71 | 3.36 | 1.78 | 3.89 | 3.44 | 1.55 | 2.03 | 2.34 | 2.39 | 3.40 | 5.32 | 2.21 | 2.07 | 1.67 |

| Jarque–Bera | 0.28 | 0.85 | 0.84 | 0.60 | 0.87 | 1.40 | 0.91 | 2.99 | 3.44 | 0.71 | 0.52 | 0.38 | 0.62 | 2.34 | 11.67 | 0.94 | 0.44 | 1.43 |

| Probability | 0.87 | 0.66 | 0.66 | 0.74 | 0.65 | 0.50 | 0.63 | 0.22 | 0.18 | 0.70 | 0.77 | 0.83 | 0.73 | 0.31 | 0.00 | 0.63 | 0.80 | 0.49 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| E. Euro area | ||||||||||||||||||

| Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets | |||||||||||||

| 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | 2000–2007 | 2008–2018 | 2000–2018 | |

| Mean | −0.30 | −0.37 | −0.34 | 2.91 | 3.10 | 3.02 | 1.90 | 2.91 | 2.49 | 2.38 | 3.22 | 2.87 | 3.44 | 2.63 | 2.97 | 7.35 | 3.37 | 5.05 |

| Median | −0.37 | −0.39 | −0.39 | 3.77 | 2.36 | 2.63 | 7.70 | 6.19 | 6.19 | 2.00 | 4.41 | 4.06 | 3.86 | 3.45 | 3.47 | 7.70 | 3.53 | 6.24 |

| Maximum | 0.15 | 1.03 | 1.03 | 7.10 | 12.71 | 12.71 | 23.61 | 28.02 | 28.02 | 7.78 | 11.99 | 11.99 | 5.47 | 6.01 | 6.01 | 8.44 | 7.07 | 8.44 |

| Minimum | −0.63 | −1.35 | −1.35 | −2.55 | −3.36 | −3.36 | −34.68 | −45.34 | −45.34 | −3.88 | −11.08 | −11.08 | 1.02 | −2.28 | −2.28 | 4.07 | −0.33 | −0.33 |

| Std. Dev. | 0.26 | 0.81 | 0.63 | 3.23 | 4.99 | 4.23 | 20.22 | 20.58 | 19.86 | 4.92 | 6.68 | 5.86 | 1.35 | 2.18 | 1.88 | 1.40 | 2.81 | 3.04 |

| Skewness | 0.75 | 0.33 | 0.28 | −0.48 | 0.71 | 0.59 | −0.74 | −1.14 | −0.98 | 0.02 | −0.80 | −0.58 | −0.42 | −0.86 | −1.06 | −1.84 | 0.00 | −0.59 |

| Kurtosis | 2.40 | 1.76 | 2.61 | 2.12 | 2.50 | 2.90 | 2.28 | 3.78 | 3.18 | 1.29 | 2.94 | 2.74 | 2.65 | 3.59 | 4.49 | 5.07 | 1.33 | 1.83 |

| Jarque–Bera | 0.86 | 0.90 | 0.37 | 0.56 | 1.05 | 1.10 | 0.91 | 2.65 | 3.05 | 0.98 | 1.17 | 1.10 | 0.28 | 1.52 | 5.32 | 5.93 | 1.27 | 2.18 |

| Probability | 0.65 | 0.64 | 0.83 | 0.76 | 0.59 | 0.58 | 0.64 | 0.27 | 0.22 | 0.61 | 0.56 | 0.58 | 0.87 | 0.47 | 0.07 | 0.05 | 0.53 | 0.34 |

| Observations | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 | 8 | 11 | 19 |

| A. Germany | ||||||

| Covariance Correlation | Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets |

| Currency and deposits | 0.66 | |||||

| 1.00 | ||||||

| Debt securities | 1.09 | 13.50 | ||||

| 0.37 | 1.00 | |||||

| Equity | 0.77 | −2.10 | 451.49 | |||

| 0.04 | −0.03 | 1.00 | ||||

| Investment fund shares | 1.07 | 9.74 | 183.74 | 92.64 | ||

| 0.14 | 0.28 | 0.90 | 1.00 | |||

| Insurance products | 0.73 | 2.32 | 4.88 | 4.23 | 1.75 | |

| 0.68 | 0.48 | 0.17 | 0.33 | 1.00 | ||

| Non-financial assets | −0.68 | 0.28 | 14.32 | 8.15 | 0.20 | 8.11 |

| −0.29 | 0.03 | 0.24 | 0.30 | 0.05 | 1.00 | |

| B. Spain | ||||||

| Covariance Correlation | Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets |

| Currency and deposits | 1.84 | |||||

| 1.00 | ||||||

| Debt securities | 1.83 | 14.48 | ||||

| 0.35 | 1.00 | |||||

| Equity | 9.69 | 10.57 | 400.82 | |||

| 0.36 | 0.14 | 1.00 | ||||

| Investment fund shares | 2.38 | 8.02 | 37.73 | 10.23 | ||

| 0.55 | 0.66 | 0.59 | 1.00 | |||

| Insurance products | 1.42 | 3.09 | −1.24 | 2.00 | 2.78 | |

| 0.63 | 0.49 | −0.04 | 0.37 | 1.00 | ||

| Non-financial assets | −5.16 | −5.62 | 28.64 | −2.67 | −1.30 | 86.57 |

| −0.41 | −0.16 | 0.15 | −0.09 | −0.08 | 1.00 | |

| C. France | ||||||

| Covariance Correlation | Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets |

| Currency and deposits | 0.35 | |||||

| 1.00 | ||||||

| Debt securities | 0.53 | 13.47 | ||||

| 0.24 | 1.00 | |||||

| Equity | 4.29 | 2.26 | 362.71 | |||

| 0.38 | 0.03 | 1.00 | ||||

| Investment fund shares | 0.95 | 3.56 | 72.38 | 17.14 | ||

| 0.39 | 0.23 | 0.92 | 1.00 | |||

| Insurance products | 0.91 | 0.16 | 59.83 | 12.88 | 12.34 | |

| 0.43 | 0.01 | 0.89 | 0.89 | 1.00 | ||

| Non-financial assets | −0.35 | −2.35 | 5.17 | 3.78 | 6.31 | 35.65 |

| −0.10 | −0.11 | 0.05 | 0.15 | 0.30 | 1.00 | |

| D. Italy | ||||||

| Covariance Correlation | Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets |

| Currency and deposits | 0.66 | |||||

| 1.00 | ||||||

| Debt securities | 0.11 | 22.51 | ||||

| 0.03 | 1.00 | |||||

| Equity | 6.09 | 16.68 | 333.20 | |||

| 0.41 | 0.19 | 1.00 | ||||

| Investment fund shares | 1.04 | 13.14 | 59.06 | 17.68 | ||

| 0.30 | 0.66 | 0.77 | 1.00 | |||

| Insurance products | 1.15 | 2.39 | 31.99 | 6.52 | 4.82 | |

| 0.64 | 0.23 | 0.80 | 0.71 | 1.00 | ||

| Non-financial assets | −0.71 | −3.81 | −2.11 | −2.17 | 1.95 | 23.76 |

| −0.18 | −0.16 | −0.02 | −0.11 | 0.18 | 1.00 | |

| E. Euro area | ||||||

| Covariance Correlation | Currency and deposits | Debt securities | Equity | Investment fund shares | Insurance/pension products | Non-financial assets |

| Currency and deposits | 0.40 | |||||

| 1.00 | ||||||

| Debt securities | 0.70 | 17.91 | ||||

| 0.26 | 1.00 | |||||

| Equity | 3.82 | 8.79 | 394.60 | |||

| 0.31 | 0.10 | 1.00 | ||||

| Investment fund shares | 1.32 | 10.45 | 103.06 | 34.35 | ||

| 0.36 | 0.42 | 0.89 | 1.00 | |||

| Insurance products | 0.71 | 1.52 | 29.27 | 8.75 | 3.52 | |

| 0.60 | 0.19 | 0.79 | 0.80 | 1.00 | ||

| Non-financial assets | 0.14 | −1.84 | 0.37 | 0.12 | 1.37 | 9.23 |

| 0.07 | −0.14 | 0.01 | 0.01 | 0.24 | 1.00 |

| A. Germany | ||||||||||

| Portfolio 2018 | Optimal mean-variance portfolios | |||||||||

| Model 1 | Model 2 | Model 3 | ||||||||

| Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | |||||

| Asset categories | ||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||

| Currency and deposits | −0.13 | 0.81 | −6.15 | 17.74 | 101.00 | −228.30 | 86.77 | 0.00 | 41.96 | 0.00 |

| Insurance/pension products | 2.83 | 1.32 | 0.47 | 16.03 | −13.54 | 292.46 | 0.00 | 0.00 | 0.00 | 0.00 |

| Equity | 3.72 | 21.25 | 5.71 | 2.66 | 0.57 | 6.02 | 0.00 | 0.00 | 0.00 | 0.00 |

| Debt securities | 3.16 | 3.67 | 1.16 | 1.07 | −1.15 | 10.08 | 0.00 | 0.00 | 0.00 | 0.00 |

| Investment fund shares | 4.23 | 9.63 | 2.27 | 4.46 | −2.47 | −22.61 | 0.00 | 0.00 | 0.00 | 41.96 |

| Non-financial assets | 4.37 | 2.85 | 0.65 | 58.04 | 15.59 | 42.35 | 13.23 | 100.00 | 58.04 | 58.04 |

| Portfolio performance | ||||||||||

| Expected real portfolio return | 3.29 | 0.05 | 10.00 | 0.46 | 4.37 | 2.48 | 4.31 | |||

| Portfolio standard deviation | 2.17 | 0.65 | 3.18 | 0.69 | 2.84 | 1.59 | 4.80 | |||

| Coefficient of variation | 0.66 | 14.17 | 0.32 | 1.50 | 0.65 | 0.64 | 1.11 | |||

| B. Spain | ||||||||||

| Portfolio 2018 | Optimal mean-variance portfolios | |||||||||

| Model 1 | Model 2 | Model 3 | ||||||||

| Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | |||||

| Asset categories | ||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||

| Currency and deposits | −1.13 | 1.36 | −1.20 | 14.55 | 110.80 | −547.57 | 85.99 | 0.00 | 30.21 | 0.00 |

| Insurance/pension products | 4.54 | 1.67 | 0.37 | 5.90 | −19.54 | 673.50 | 7.23 | 0.00 | 0.00 | 32.72 |

| Equity | 2.77 | 20.02 | 7.22 | 6.94 | −3.17 | 16.52 | 0.00 | 0.00 | 0.00 | 0.00 |

| Debt securities | 2.75 | 3.81 | 1.38 | 0.28 | 3.34 | −62.71 | 0.00 | 0.00 | 2.51 | 0.00 |

| Investment fund shares | 1.71 | 3.20 | 1.87 | 5.05 | −0.22 | 35.25 | 0.00 | 0.00 | 0.00 | 0.00 |

| Non-financial assets | 7.45 | 9.30 | 1.25 | 67.28 | 8.79 | −14.99 | 6.78 | 100.00 | 67.28 | 67.28 |

| Portfolio performance | ||||||||||

| Expected real portfolio return | 5.40 | −1.49 | 35.00 | −0.14 | 7.45 | 4.74 | 6.45 | |||

| Portfolio standard deviation | 6.56 | 1.03 | 7.30 | 1.16 | 9.30 | 6.09 | 6.23 | |||

| Coefficient of variation | 1.22 | −0.69 | 0.21 | −8.17 | 1.25 | 1.29 | 0.97 | |||

| C. France | ||||||||||

| Portfolio 2018 | Optimal mean-variance portfolios | |||||||||

| Model 1 | Model 2 | Model 3 | ||||||||

| Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | |||||

| Asset categories | ||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||

| Currency and deposits | 0.14 | 0.60 | 4.34 | 12.82 | 101.18 | −274.42 | 98.08 | 0.00 | 29.09 | 0.00 |

| Insurance/pension products | 3.19 | 3.51 | 1.10 | 16.50 | −7.07 | 451.34 | 0.00 | 0.00 | 0.00 | 38.23 |

| Equity | 3.00 | 19.04 | 6.35 | 6.32 | −1.79 | −29.81 | 0.00 | 0.00 | 0.00 | 0.00 |

| Debt securities | 3.04 | 3.67 | 1.21 | 0.38 | −3.58 | 140.63 | 0.00 | 0.00 | 9.14 | 0.00 |

| Investment fund shares | 1.55 | 4.14 | 2.67 | 2.20 | 9.19 | −198.67 | 0.00 | 0.00 | 0.00 | 0.00 |

| Non-financial assets | 6.31 | 5.97 | 0.95 | 61.77 | 2.08 | 10.93 | 1.92 | 100.00 | 61.77 | 61.77 |

| Portfolio performance | ||||||||||

| Expected real portfolio return | 4.67 | 0.02 | 15.00 | 0.26 | 6.31 | 4.21 | 5.11 | |||

| Portfolio standard deviation | 4.33 | 0.53 | 7.05 | 0.58 | 5.97 | 3.66 | 4.29 | |||

| Coefficient of variation | 0.93 | 21.46 | 0.47 | 2.28 | 0.95 | 0.87 | 0.84 | |||

| D. Italy | ||||||||||

| Portfolio 2018 | Optimal mean-variance portfolios | |||||||||

| Model 1 | Model 2 | Model 3 | ||||||||

| Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | |||||

| Asset categories | ||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||

| Currency and deposits | −0.86 | 0.81 | −0.94 | 14.00 | 114.12 | −392.82 | 91.41 | 0.00 | 27.39 | 0.00 |

| Insurance/pension products | 2.19 | 2.19 | 1.00 | 10.08 | −33.04 | 507.72 | 0.00 | 0.00 | 0.00 | 0.00 |

| Equity | 0.54 | 18.25 | 34.02 | 4.88 | −0.59 | −48.76 | 0.00 | 0.00 | 0.00 | 0.00 |

| Debt securities | 2.98 | 4.74 | 1.59 | 2.95 | 0.56 | −6.19 | 3.01 | 0.00 | 9.42 | 36.82 |

| Investment fund shares | 2.64 | 4.20 | 1.59 | 4.90 | 10.25 | 48.39 | 0.00 | 0.00 | 0.00 | 0.00 |

| Non-financial assets | 3.97 | 4.87 | 1.23 | 63.18 | 8.69 | −8.34 | 5.58 | 100.00 | 63.18 | 63.18 |

| Portfolio performance | ||||||||||

| Expected real portfolio return | 2.86 | −1.07 | 15.00 | −0.47 | 3.97 | 2.56 | 3.61 | |||

| Portfolio standard deviation | 3.32 | 0.62 | 5.83 | 0.75 | 4.87 | 3.01 | 3.28 | |||

| Coefficient of variation | 1.16 | −0.57 | 0.39 | −1.58 | 1.23 | 1.18 | 0.91 | |||

| E. Euro area | ||||||||||

| Portfolio 2018 | Optimal mean-variance portfolios | |||||||||

| Model 1 | Model 2 | Model 3 | ||||||||

| Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | Minimum variance | Maximum expected real return | |||||

| Asset categories | ||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||

| Currency and deposits | −0.34 | 0.63 | −1.85 | 15.03 | 114.08 | −194.23 | 97.28 | 0.00 | 33.22 | 0.00 |

| Insurance/pension products | 2.97 | 1.88 | 0.63 | 14.68 | −19.06 | 283.55 | 0.00 | 0.00 | 0.00 | 0.00 |

| Equity | 2.49 | 19.86 | 7.99 | 5.05 | −0.65 | −10.82 | 0.00 | 0.00 | 0.00 | 0.00 |

| Debt securities | 3.02 | 4.23 | 1.40 | 1.03 | −2.70 | 29.19 | 0.00 | 0.00 | 6.36 | 39.57 |

| Investment fund shares | 2.87 | 5.86 | 2.04 | 3.79 | 4.19 | −31.50 | 0.00 | 0.00 | 0.00 | 0.00 |

| Non-financial assets | 5.05 | 3.04 | 0.60 | 60.43 | 4.13 | 23.82 | 2.72 | 100.00 | 60.43 | 60.43 |

| Portfolio performance | ||||||||||

| Expected real portfolio return | 3.70 | −0.72 | 10.00 | −0.19 | 5.05 | 3.13 | 4.24 | |||

| Portfolio standard deviation | 2.42 | 0.58 | 3.06 | 0.62 | 3.04 | 1.85 | 2.30 | |||

| Coefficient of variation | 0.65 | −0.80 | 0.31 | −3.23 | 0.60 | 0.59 | 0.54 | |||

| A. Germany | ||||||||||||

| Portfolio 2018 | Mean-variance “ceteris paribus” portfolios | Heuristic portfolios | ||||||||||

| Model 1 | Model 2 | Model 3 | ||||||||||

| (1a) | (1b) | (2a) | (2b) | (3a) | (3b) | |||||||

| Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | 1/n portfolio | Opportunity portfolio | |||||

| Asset categories | ||||||||||||

| Expected real return | Standard deviation | Coefficient of variation | Portfolio shares | |||||||||

| Currency and deposits | −0.13 | 0.81 | −6.15 | 17.74 | −117.76 | −6.27 | 0.00 | 0.00 | 0.00 | 14.69 | 8.39 | 4.20 |

| Insurance/pension products | 2.83 | 1.32 | 0.47 | 16.03 | 189.74 | 86.14 | 17.67 | 70.04 | 16.08 | 27.27 | 8.39 | 4.20 |

| Equity | 3.72 | 21.25 | 5.71 | 2.66 | 4.19 | 2.35 | 0.00 | 0.00 | 0.00 | 0.00 | 8.39 | 4.20 |

| Debt securities | 3.16 | 3.67 | 1.16 | 1.07 | 6.31 | 2.51 | 8.95 | 0.00 | 20.36 | 0.00 | 8.39 | 4.20 |

| Investment fund shares | 4.23 | 9.63 | 2.27 | 4.46 | −15.85 | −9.03 | 0.00 | 0.00 | 5.52 | 0.00 | 8.39 | 25.18 |

| Non-financial assets | 4.37 | 2.85 | 0.65 | 58.04 | 33.37 | 24.31 | 73.38 | 29.96 | 58.04 | 58.04 | 58.04 | 58.04 |

| Portfolio performance | ||||||||||||

| Expected real portfolio return | 3.29 | 6.66 | 3.29 | 3.99 | 3.29 | 3.87 | 3.29 | 3.70 | 4.01 | |||

| Portfolio standard deviation | 2.17 | 2.17 | 1.20 | 2.17 | 1.29 | 2.17 | 1.70 | 3.43 | 4.09 | |||

| Coefficient of variation | 0.66 | 0.33 | 0.37 | 0.54 | 0.39 | 0.56 | 0.52 | 0.93 | 1.02 | |||

| B. Spain | ||||||||||||

| Portfolio 2018 | Mean-variance “ceteris paribus” portfolios | Heuristic portfolios | ||||||||||

| Model 1 | Model 2 | Model 3 | ||||||||||

| (1a) | (1b) | (2a) | (2b) | (3a) | (3b) | |||||||

| Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | 1/n portfolio | Opportunity portfolio | |||||

| Asset categories | ||||||||||||

| Expected real return | Standard deviation | Coefficient of variation | Portfolio shares | |||||||||

| Currency and deposits | −1.13 | 1.36 | −1.20 | 14.55 | −479.40 | −13.46 | 0.00 | 0.00 | 0.00 | 13.86 | 6.54 | 3.27 |

| Insurance/pension products | 4.54 | 1.67 | 0.37 | 5.90 | 601.73 | 111.26 | 29.21 | 70.45 | 26.22 | 1.52 | 6.54 | 3.27 |

| Equity | 2.77 | 20.02 | 7.22 | 6.94 | 14.48 | 0.55 | 0.00 | 0.00 | 6.51 | 0.00 | 6.54 | 3.27 |

| Debt securities | 2.75 | 3.81 | 1.38 | 0.28 | −55.86 | −9.12 | 0.00 | 0.00 | 0.00 | 17.34 | 6.54 | 3.27 |

| Investment fund shares | 1.71 | 3.20 | 1.87 | 5.05 | 31.57 | 6.47 | 0.00 | 0.00 | 0.00 | 0.00 | 6.54 | 19.63 |

| Non-financial assets | 7.45 | 9.30 | 1.25 | 67.28 | −12.53 | 4.30 | 70.79 | 29.55 | 67.28 | 67.28 | 67.28 | 67.28 |

| Portfolio performance | ||||||||||||

| Expected real portfolio return | 5.40 | 31.22 | 5.40 | 6.60 | 5.40 | 6.38 | 5.40 | 5.71 | 5.64 | |||

| Portfolio standard deviation | 6.56 | 6.56 | 1.71 | 6.56 | 2.90 | 6.56 | 6.12 | 6.55 | 6.38 | |||

| Coefficient of variation | 1.22 | 0.21 | 0.32 | 0.99 | 0.54 | 1.03 | 1.13 | 1.15 | 1.13 | |||

| C. France | ||||||||||||

| Portfolio 2018 | Mean-variance “ceteris paribus” portfolios | Heuristic portfolios | ||||||||||

| Model 1 | Model 2 | Model 3 | ||||||||||

| (1a) | (1b) | (2a) | (2b) | (3a) | (3b) | |||||||

| Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | 1/n portfolio | Opportunity portfolio | |||||

| Asset categories | ||||||||||||

| Expected real return | Standard deviation | Coefficient of variation | Portfolio shares | |||||||||

| Currency and deposits | 0.14 | 0.60 | 4.34 | 12.82 | −128.76 | −15.46 | 0.00 | 0.00 | 0.00 | 13.16 | 7.65 | 3.82 |

| Insurance/pension products | 3.19 | 3.51 | 1.10 | 16.50 | 273.56 | 135.28 | 0.00 | 11.98 | 37.16 | 0.00 | 7.65 | 3.82 |

| Equity | 3.00 | 19.04 | 6.35 | 6.32 | −18.95 | −10.49 | 0.00 | 0.00 | 1.07 | 0.00 | 7.65 | 3.82 |

| Debt securities | 3.04 | 3.67 | 1.21 | 0.38 | 84.70 | 41.20 | 27.57 | 38.47 | 0.00 | 25.07 | 7.65 | 3.82 |

| Investment fund shares | 1.55 | 4.14 | 2.67 | 2.20 | −118.05 | −55.36 | 0.00 | 0.00 | 0.00 | 0.00 | 7.65 | 22.94 |

| Non-financial assets | 6.31 | 5.97 | 0.95 | 61.77 | 7.50 | 4.83 | 72.43 | 49.55 | 61.77 | 61.77 | 61.77 | 61.77 |

| Portfolio performance | ||||||||||||

| Expected real portfolio return | 4.67 | 9.19 | 4.67 | 5.41 | 4.67 | 5.11 | 4.67 | 4.73 | 4.61 | |||

| Portfolio standard deviation | 4.33 | 4.33 | 2.25 | 4.33 | 3.29 | 4.33 | 3.70 | 4.36 | 4.28 | |||

| Coefficient of variation | 0.93 | 0.47 | 0.48 | 0.80 | 0.70 | 0.85 | 0.79 | 0.92 | 0.93 | |||

| D. Italy | ||||||||||||

| Portfolio 2018 | Mean-variance “ceteris paribus” portfolios | Heuristic portfolios | ||||||||||

| Model 1 | Model 2 | Model 3 | ||||||||||

| (1a) | (1b) | (2a) | (2b) | (3a) | (3b) | |||||||

| Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | 1/n portfolio | Opportunity portfolio | |||||

| Asset categories | ||||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||||

| Currency and deposits | −0.86 | 0.81 | −0.94 | 14.00 | −171.24 | −9.81 | 0.00 | 0.00 | 0.00 | 19.45 | 7.36 | 3.68 |

| Insurance/pension products | 2.19 | 2.19 | 1.00 | 10.08 | 271.36 | 99.16 | 0.00 | 50.85 | 0.00 | 0.00 | 7.36 | 3.68 |

| Equity | 0.54 | 18.25 | 34.02 | 4.88 | −27.71 | −12.37 | 0.00 | 0.00 | 3.14 | 0.00 | 7.36 | 3.68 |

| Debt securities | 2.98 | 4.74 | 1.59 | 2.95 | −3.24 | −1.09 | 35.28 | 21.34 | 33.68 | 15.44 | 7.36 | 3.68 |

| Investment fund shares | 2.64 | 4.20 | 1.59 | 4.90 | 31.73 | 19.58 | 0.00 | 0.00 | 0.00 | 1.93 | 7.36 | 22.09 |

| Non-financial assets | 3.97 | 4.87 | 1.23 | 63.18 | −0.90 | 4.53 | 64.72 | 27.81 | 63.18 | 63.18 | 63.18 | 63.18 |

| Portfolio performance | ||||||||||||

| Expected real portfolio return | 2.86 | 7.97 | 2.86 | 3.62 | 2.86 | 3.53 | 2.86 | 3.06 | 3.27 | |||

| Portfolio standard deviation | 3.32 | 3.32 | 1.54 | 3.32 | 2.17 | 3.32 | 3.03 | 3.52 | 3.39 | |||

| Coefficient of variation | 1.16 | 0.42 | 0.54 | 0.92 | 0.76 | 0.94 | 1.06 | 1.15 | 1.03 | |||

| E. Euro area | ||||||||||||

| Portfolio 2018 | Mean-variance “ceteris paribus” portfolios | Heuristic portfolios | ||||||||||

| Model 1 | Model 2 | Model 3 | ||||||||||

| (1a) | (1b) | (2a) | (2b) | (3a) | (3b) | |||||||

| Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | Standard deviation 2018 + expected real return maximized | Expected real return 2018 + standard deviation minimized | 1/n portfolio | Opportunity portfolio | |||||

| Asset categories | ||||||||||||

| Expected real return | standard deviation | Coefficient of variation | Portfolio shares | |||||||||

| Currency and deposits | −0.34 | 0.63 | −1.85 | 15.03 | −126.48 | −13.07 | 0.00 | 0.40 | 0.00 | 16.06 | 7.91 | 3.96 |

| Insurance/pension products | 2.97 | 1.88 | 0.63 | 14.68 | 217.03 | 105.74 | 4.78 | 50.89 | 0.00 | 10.31 | 7.91 | 3.96 |

| Equity | 2.49 | 19.86 | 7.99 | 5.05 | −8.59 | −4.84 | 0.00 | 0.00 | 4.33 | 0.00 | 7.91 | 3.96 |

| Debt securities | 3.02 | 4.23 | 1.40 | 1.03 | 22.18 | 10.45 | 16.73 | 13.32 | 35.24 | 13.20 | 7.91 | 3.96 |

| Investment fund shares | 2.87 | 5.86 | 2.04 | 3.79 | −23.66 | −10.53 | 0.00 | 0.00 | 0.00 | 0.00 | 7.91 | 23.74 |

| Non-financial assets | 5.05 | 3.04 | 0.60 | 60.43 | 19.50 | 12.25 | 78.49 | 35.39 | 60.43 | 60.43 | 60.43 | 60.43 |

| Portfolio performance | ||||||||||||

| Expected real portfolio return | 3.70 | 7.64 | 3.70 | 4.61 | 3.70 | 4.22 | 3.70 | 3.92 | 4.05 | |||

| Portfolio standard deviation | 2.42 | 2.42 | 1.37 | 2.42 | 1.71 | 2.42 | 1.93 | 2.88 | 2.91 | |||

| Coefficient of variation | 0.65 | 0.32 | 0.37 | 0.52 | 0.46 | 0.57 | 0.52 | 0.74 | 0.72 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Radke, M.P.; Rupprecht, M. Household Wealth: Low-Yielding and Poorly Structured? J. Risk Financial Manag. 2021, 14, 99. https://doi.org/10.3390/jrfm14030099

Radke MP, Rupprecht M. Household Wealth: Low-Yielding and Poorly Structured? Journal of Risk and Financial Management. 2021; 14(3):99. https://doi.org/10.3390/jrfm14030099

Chicago/Turabian StyleRadke, Marc Peter, and Manuel Rupprecht. 2021. "Household Wealth: Low-Yielding and Poorly Structured?" Journal of Risk and Financial Management 14, no. 3: 99. https://doi.org/10.3390/jrfm14030099

APA StyleRadke, M. P., & Rupprecht, M. (2021). Household Wealth: Low-Yielding and Poorly Structured? Journal of Risk and Financial Management, 14(3), 99. https://doi.org/10.3390/jrfm14030099