Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates

Abstract

:1. Introduction

2. Literature Review

3. Research Methodology

4. Results and Discussion

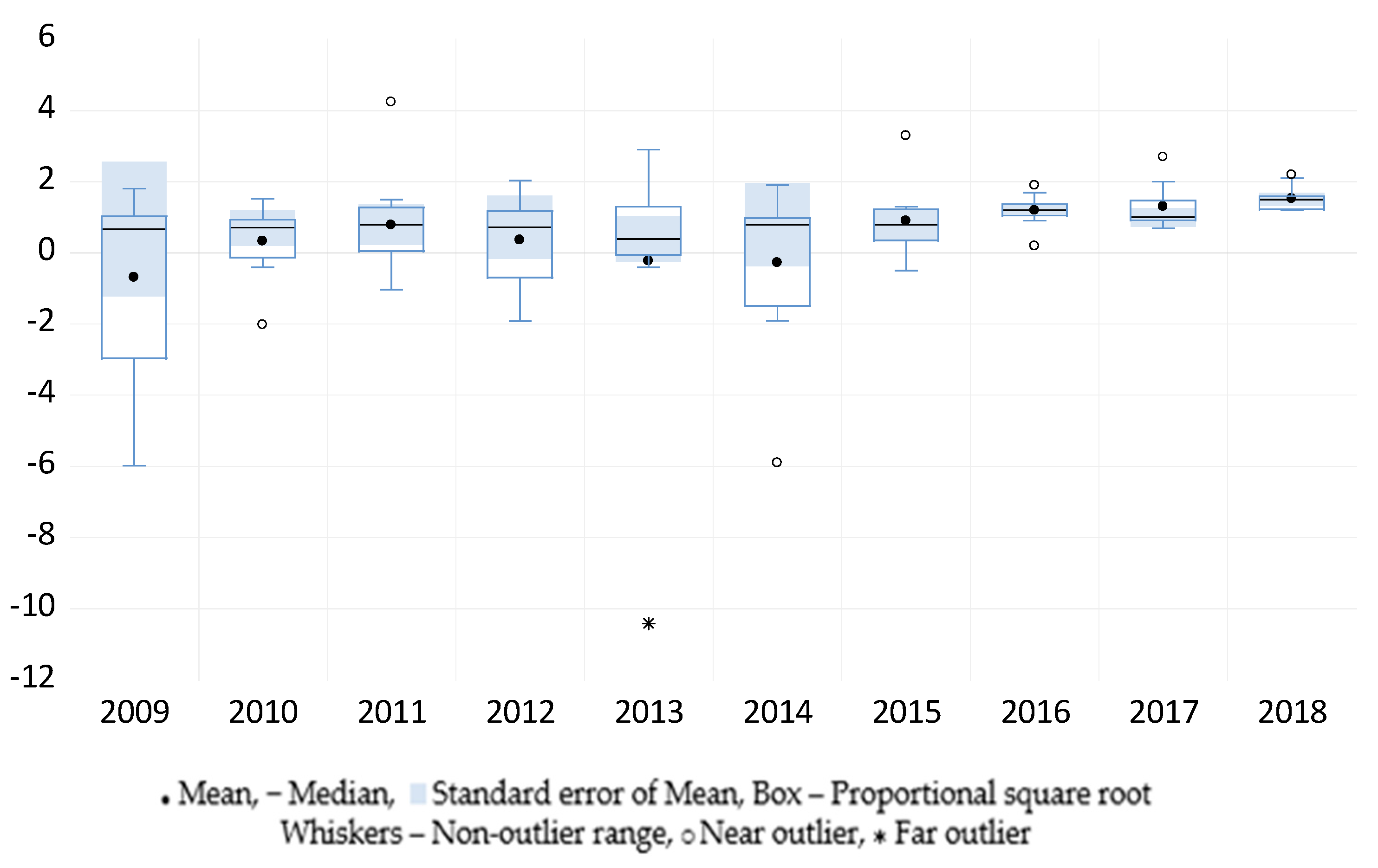

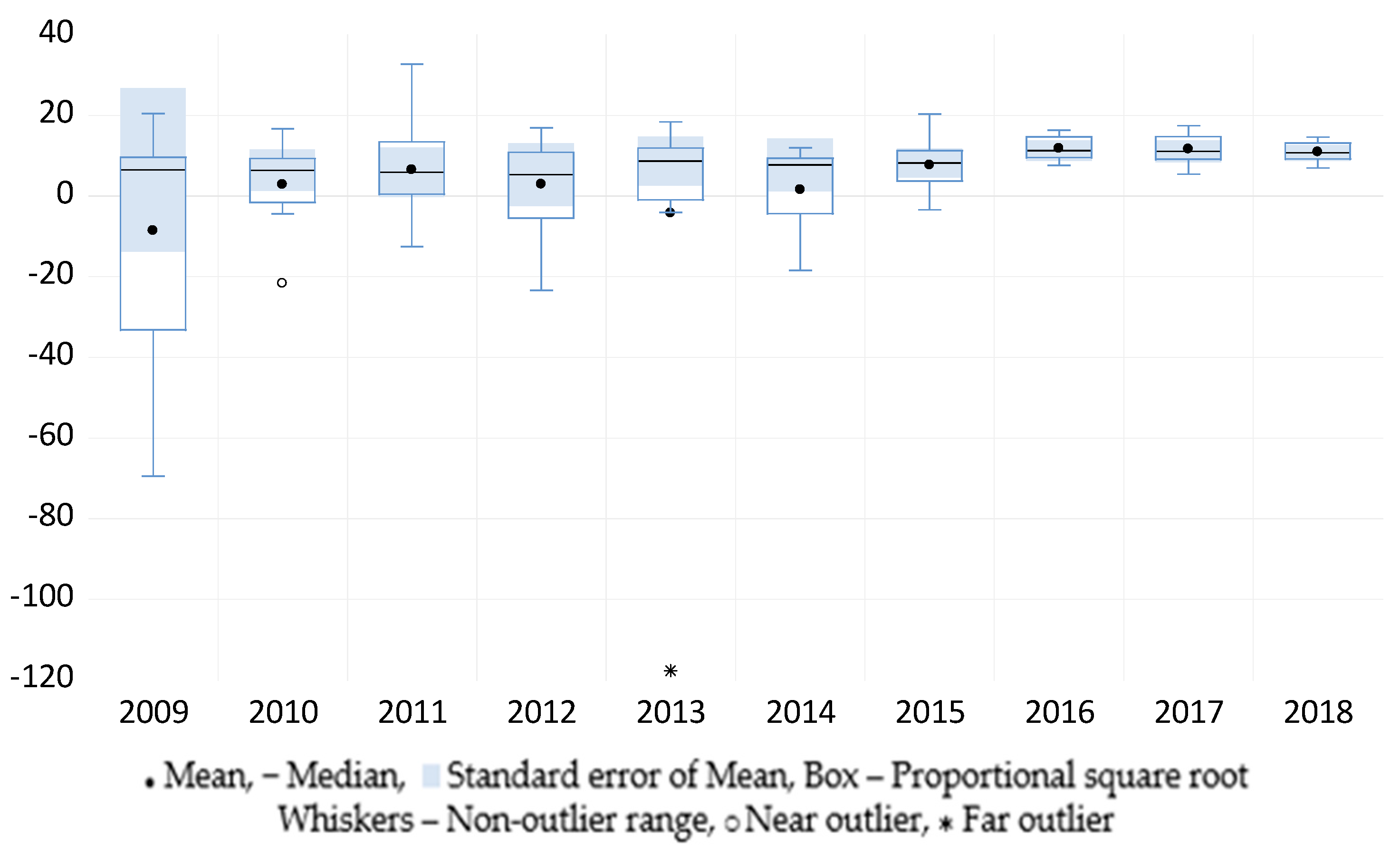

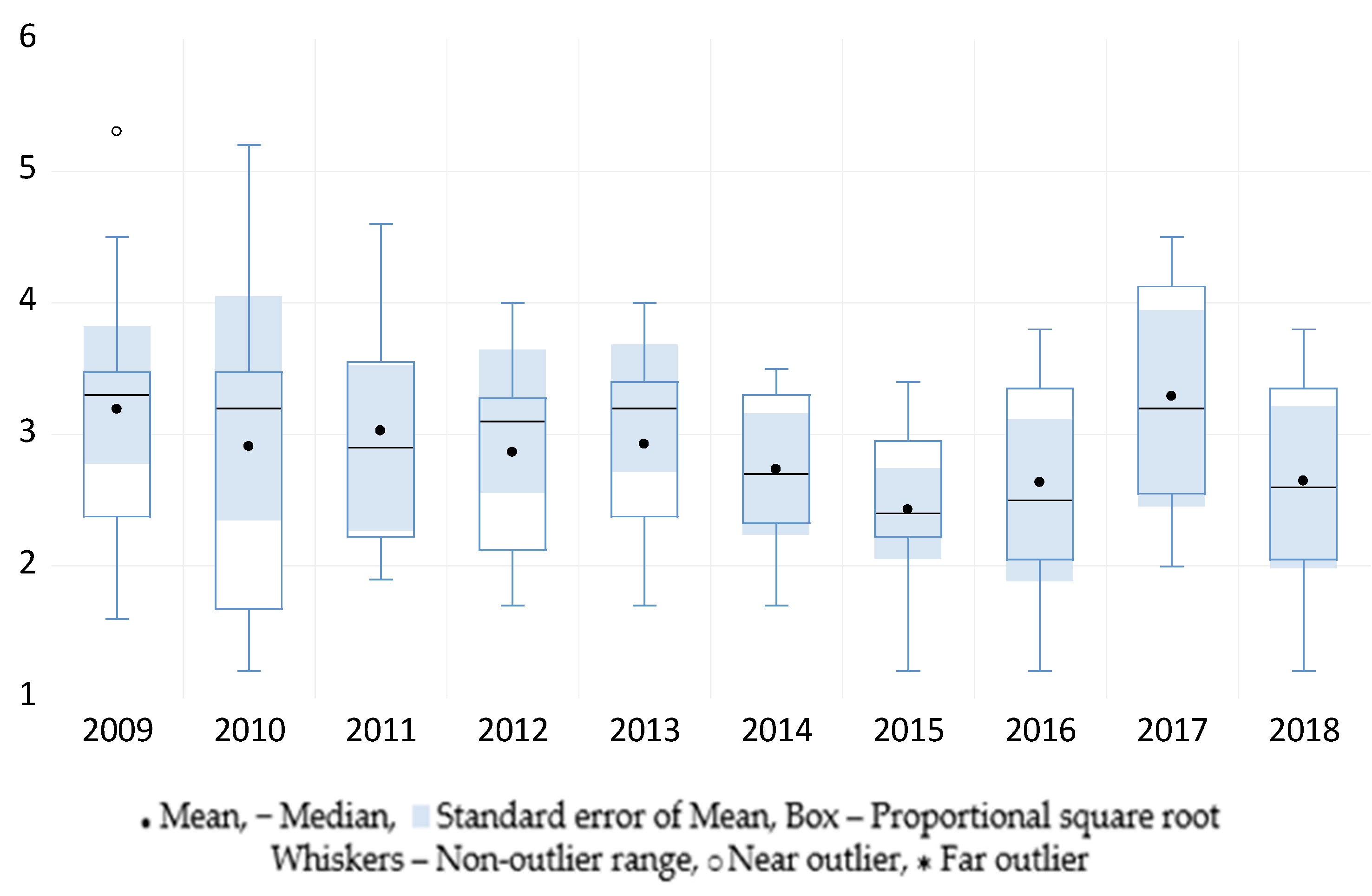

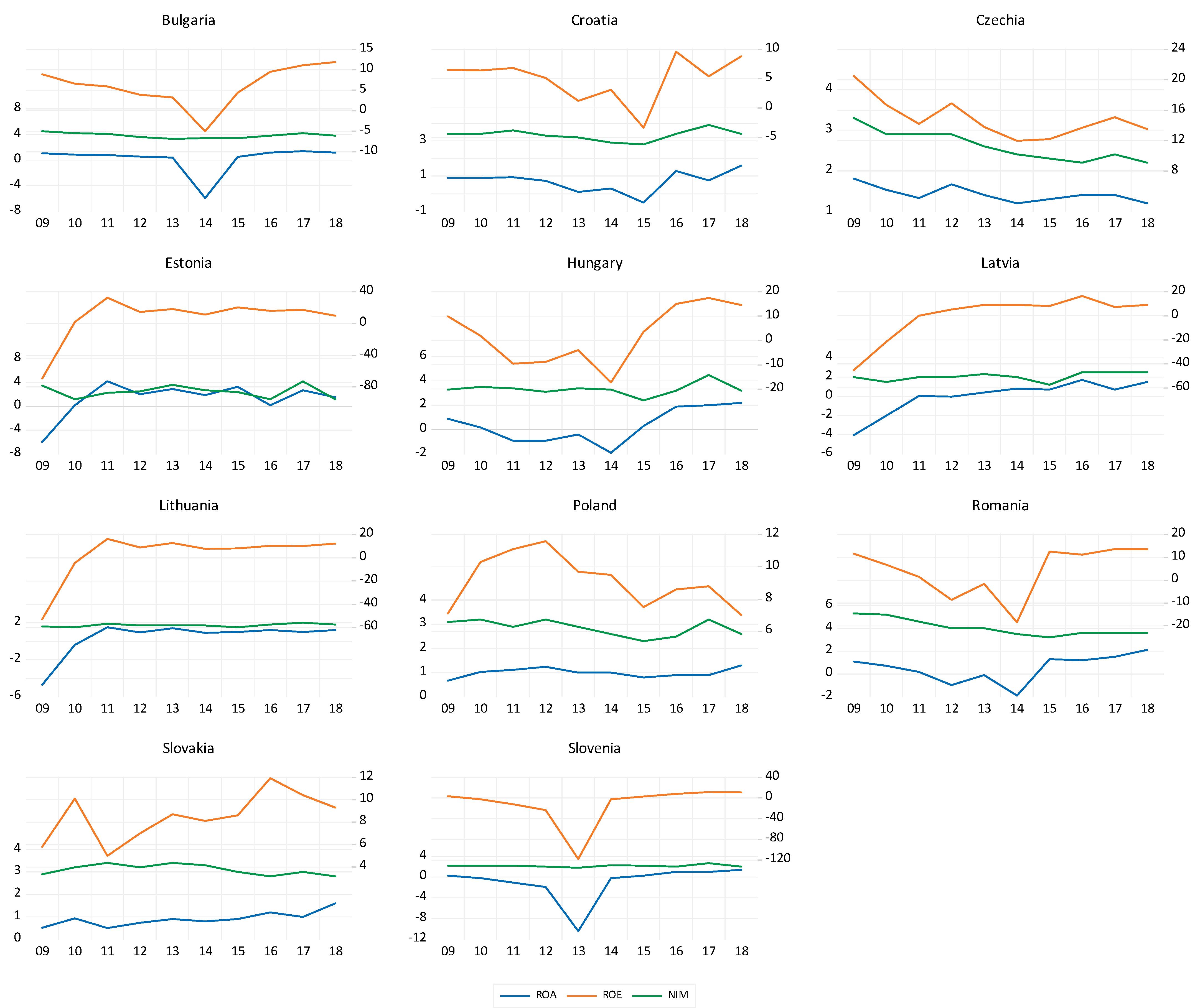

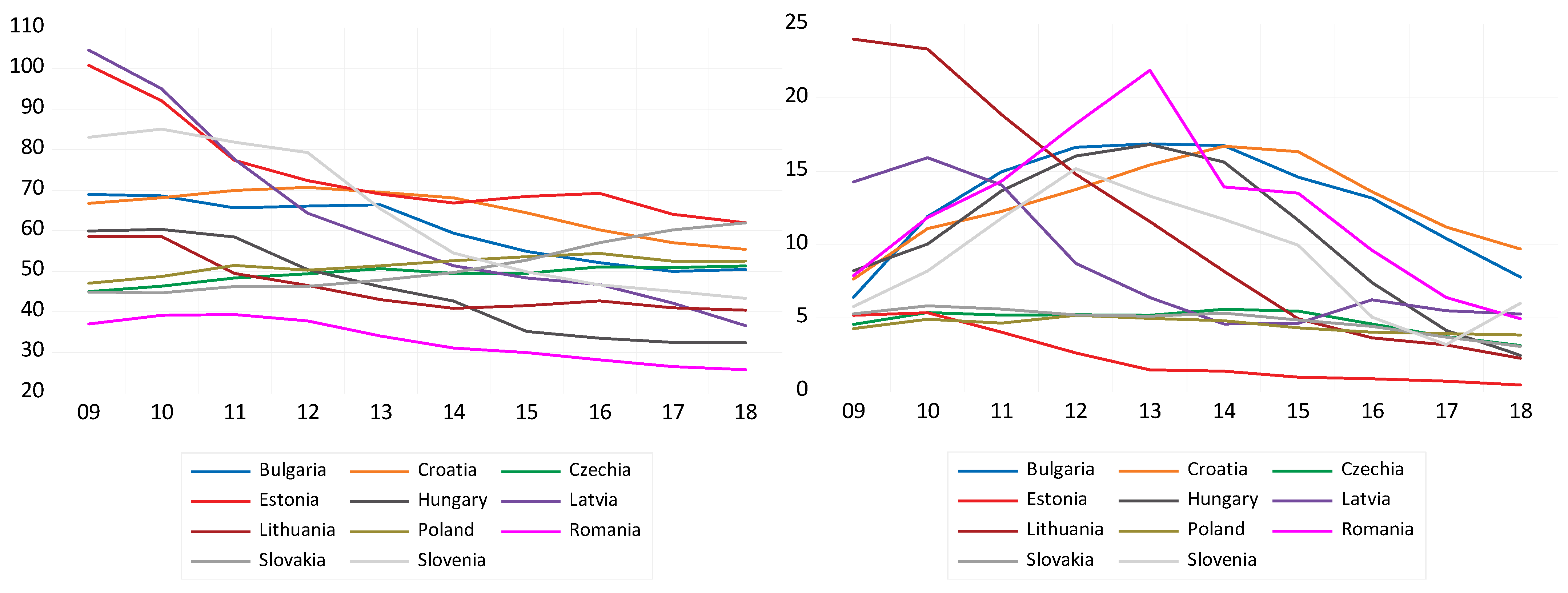

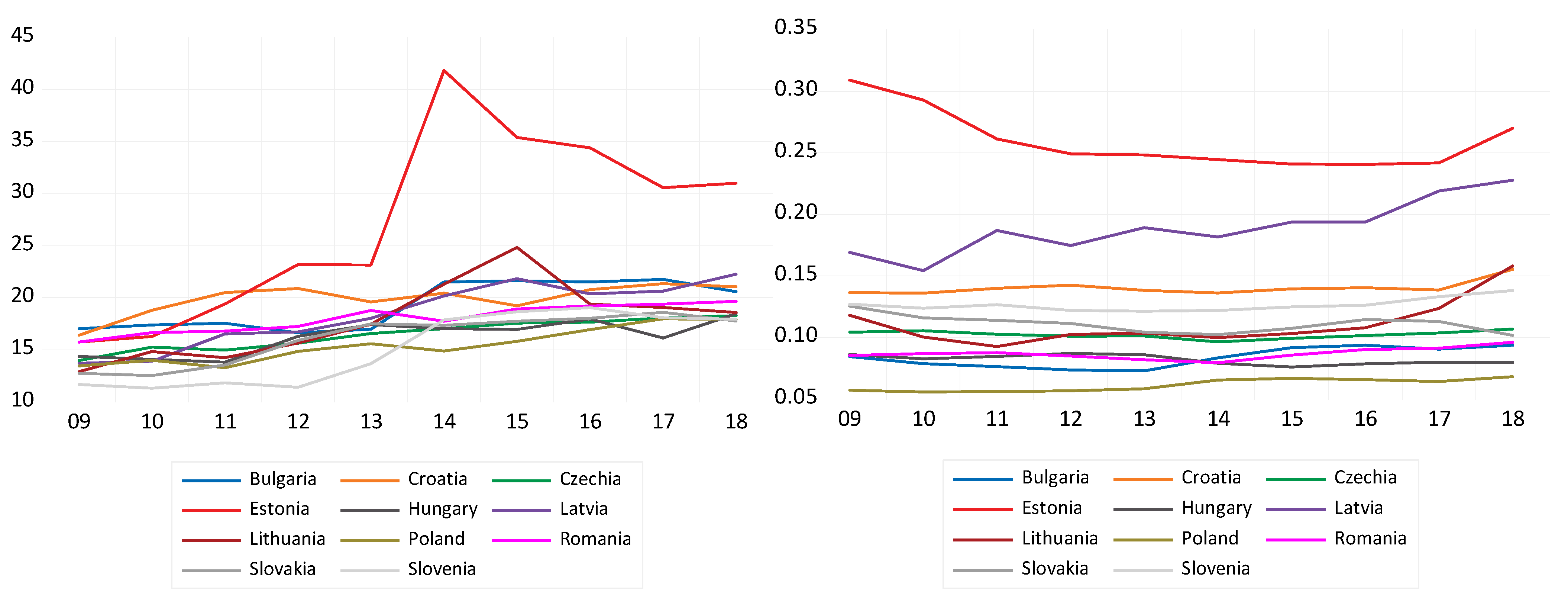

4.1. The Dynamics of Banks’ Profitability in CEE Countries

4.2. The Interplay between Bank Profitability, Financial System Attributes and the Macroeconomic Environment in CEE

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1. | We have tested for preliminary significance with the following variables: Nominal GDP per capita, GDP growth rate, the tax and contribution rate as a percentage of bank profits, 10-year bond yields, Nominal effective exchange rate (NEER), Real effective exchange rate (REER) and Equity market capitalization ratio to GDP. It is difficult to explain the lack of significance of each of these variables for bank profitability in CEE countries; however, most likely, this is due to the limited period under analysis, the particularities of CEE countries’ exchange rate regimes (in the case of NEER and REER) and the specificities of the banking systems included in the analysis. |

References

- Abdelaziz, Hakimi, Djelassi Mouldi, and Helmi Helmi. 2011. Financial Liberalization and Banking Profitability: A Panel Data Analysis for Tunisian Bank. International Journal of Economics and Financial Issues 1: 19–32. [Google Scholar]

- Abreu, Margarida, and Victor Mendes. 2002. Commercial Bank Interest Margins and Profitability: Evidence for Some E.U. Countries. University of Porto Working Paper Series, No. 122; Porto: University of Porto. [Google Scholar]

- Akbas, Halil Emre. 2012. Determinants of Bank Profitability: An Investigation on Turkish Banking Sector. Öneri Dergisi 10: 103–10. [Google Scholar]

- Akter, Rozina, and Jewel Kumar Roy. 2017. Non-Performing Loan on Profitability: Evidence from Banking Sector of Dhaka Stock Exchange. International Journal of Economics and Finance 9: 126–32. [Google Scholar] [CrossRef] [Green Version]

- Alesina, Alberto, Silvia Ardagna, Roberto Perotti, and Fabio Schiantarelli. 2002. Fiscal Policy, Profits, and Investment. American Economic Review 92: 571–89. [Google Scholar] [CrossRef] [Green Version]

- Alexiou, Constantinos, and Vogiazas Sofoklis. 2009. Determinants of bank profitability: Evidence from the Greek banking sector. Economic Annals 182: 93–118. [Google Scholar] [CrossRef]

- Al-Homaidi, Eissa, Faozi Almaqtari, Ali Yahya, and Amgad Khaled. 2020. Internal and external determinants of listed commercial banks’ profitability in India: Dynamic GMM approach. International Journal of Monetary Economics and Finance 13: 34–67. [Google Scholar] [CrossRef]

- Anastasiou, Dimitrios, Helen Louri, and Efthymios Mike Tsionas. 2016. Determinants of non-performing loans: Evidence from Euro-area countries. Finance Research Letters 18: 116–19. [Google Scholar]

- Anbar, Adem, and Deger Alper. 2011. Bank Specific and Macroeconomic Determinants of Commercial Bank Profitability: Empirical Evidence from Turkey. Business and Economics Research Journal 2: 139–52. [Google Scholar]

- Andrieș, Alin, Bogdan Căpraru, Florentina Ieșan-Muntean, and Iulian Ihnatov. 2016. The Impact of International Financial Crisis on Bank Performance in Eastern and Central European Countries. EuroEconomica 35: 111–26. [Google Scholar]

- Arellano, Manuel, and Stephen Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef] [Green Version]

- Arellano, Manuel, and Olympia Bover. 1995. Another look at the instrumental variable estimation of error-components models. Journal of econometrics 68: 29–51. [Google Scholar] [CrossRef] [Green Version]

- Atasoy, Hasan. 2007. Expenditure-Income Analysis in Turkish Banking Sector and Determinants of Profitability. Un Published Dissertations of Senior Specialists. Ankara: Central Bank of Turkey. [Google Scholar]

- Athanasoglou, Panayiotis, Matthaios Delis, and Christos Staikouras. 2006. Determinants of Bank Profitability in the South Eastern European Region. WP No 47. Athens: Bank of Greece. [Google Scholar]

- Athanasoglou, Panayiotis, Sophocles Brissimis, and Matthaios Delis. 2008. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money 18: 121–36. [Google Scholar] [CrossRef] [Green Version]

- Ayaydin, Hasan, and İbrahim Karaaslan. 2014. Stock market development, bank concentration, ownership structure, and bank performance: Evidence from Turkey. Journal of Economics and Political Economy 1: 49–67. [Google Scholar]

- Banto, Jean Michel, and Atoke Fredia Monsia. 2021. Microfinance institutions, banking, growth and transmission channel: A GMM panel data analysis from developing countries. The Quarterly Review of Economics and Finance 79: 126–50. [Google Scholar] [CrossRef]

- Barros, Carlos Pestana, Candida Ferreira, and Jonathan Willians. 2007. Analysing the determinants of performance of best and worst European banks: A mixed logit approach. Journal of Banking and Finance 31: 2189–203. [Google Scholar] [CrossRef]

- Beckmann, Rainer. 2007. Profitability of Western European Banking Systems: Panel Evidence on Structural and Cyclical Determinants. Discussion Paper Series 2: Banking and Financial Studies, no. 17; Frankfurt am Main: Deutsche Bundesbank. [Google Scholar]

- Berge, Tor Oddvar, and Katrine Godding Boye. 2007. An analysis of banks’ problem loans. Economic Bulletin 78: 65–76. [Google Scholar]

- Berger, Allen. 1995. The relationship between capital and earnings in banking. Journal of Money, Credit and Banking 27: 432–56. [Google Scholar] [CrossRef]

- Blanchard, Olivier, and Roberto Perotti. 2002. An Empirical Characterization of the Dynamic Effects of Changes in Government Spending and Taxes on Output. The Quarterly Journal of Economics 117: 1329–68. [Google Scholar] [CrossRef] [Green Version]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Boyd, John, and Bruce Champ. 2006. Inflation, Banking and Economic Growth; Cleveland: Federal Reserve Bank of Cleveland.

- Boyd, John, Ross Levine, and Bruce Smith. 2001. The Impact of Inflation on Financial Sector Performance. Journal of Monetary Economics 47: 221–48. [Google Scholar] [CrossRef]

- Canzoneri, Matthew, Robert Cumby, and Behzad Diba. 2002. Should the European Central Bank and the Federal Reserve be concerned about fiscal policy? Paper presented at Symposium on “Rethinking Stabilization Policy”, Jackson Hole, WY, USA, August 29–31. [Google Scholar]

- Căpraru, Bogdan, and Iulian Ihnatov. 2014. Banks’ Profitability in Selected Central and Eastern European Countries. Procedia Economics and Finance 16: 587–91. [Google Scholar] [CrossRef] [Green Version]

- Černohorský, Jan. 2015. The Concentration and Profitability in the Czech Banking System. Scientific Papers of the University of Pardubice, Series D: Faculty of Economics and Administration 22: 30–41. [Google Scholar]

- Cetin, Huseyin. 2019. Inflation and Bank Profitability: G20 Countries Banks Panel Data Analysis. Paper presented at 2019 International Conference on Management Science and Industrial Engineering, Phuket, Thailand, May 24; pp. 168–72. [Google Scholar]

- Chiorazzo, Vincenzo, Carlo Milani, and Francesca Salvini. 2008. Income diversification and bank performance: Evidence from Italian banks. Journal of Financial Services Research 33: 181–203. [Google Scholar] [CrossRef]

- Christaria, Fiola, and Ratnawati Kurnia. 2016. The Impact of Financial Ratios, Operational Efficiency and Non-Performing Loan Towards Commercial Bank Profitability. Accounting and Finance Review (AFR) 1: 43–50. [Google Scholar]

- Claeys, Sophie, and Rudi van der Vennet. 2004. Determinants of bank interest margins in Central and Eastern Europe: A comparison with the West. Economic Systems 32: 197–216. [Google Scholar] [CrossRef]

- Clair, Robert Wayne. 2004. Macroeconomic Determinants of Banking Financial Performance and Resilience in Singapore, Monetary Authority of Singapore, Staff Paper, No. 38. Available online: https://www.mas.gov.sg/-/media/MAS/resource/publications/staff_papers/MAS_Staff_Paper_No_38_RSTC_V3.pdf (accessed on 29 May 2021).

- Coffinet, Jerome, and Surong Lin. 2010. Stress Testing Banks’ Profitability: The Case of French Banks. Working Paper No. 306. Paris: Banque de France. [Google Scholar]

- Ćurak, Marijana, Klime Poposki, and Sandra Pepur. 2012. Profitability Determinants of the Macedonian Banking Sector in Changing Environment. Procedia—Social and Behavioral Sciences 44: 406–16. [Google Scholar] [CrossRef] [Green Version]

- Deloitte. 2019. CEE Banking Consolidation Perking Up. Available online: https://www2.deloitte.com/content/dam/Deloitte/ce/Documents/finance/ce-banking-study-2019.pdf (accessed on 1 June 2021).

- Demirgüç-Kunt, Ash, and Harry Huizinga. 1999. Determinants of commercial bank interest margins and profitability: Some international evidence. World Bank Economic Review 13: 379–408. [Google Scholar] [CrossRef] [Green Version]

- DeYoung, Robert, and Tara Rice. 2004. Non-interest income and financial performance at US commercial banks. The Financial Review 39: 101–27. [Google Scholar] [CrossRef]

- Dietrich, Andreas, and Gabrielle Wanzenried. 2009. What Determines the Profitability of Commercial Banks? New Evidence from Switzerland. Paper presented at 12th Conference of the Swiss Society for Financial Market Researches, Geneva, Switzerland, April 3. [Google Scholar]

- Eesti Pank. 2014. Stricter Capital Requirements for Banks as of August, Press Release of Eesti Pank. Available online: https://www.eestipank.ee/en/press/stricter-capital-requirements-banks-august-31072014 (accessed on 1 June 2021).

- European Banking Federation. 2019. Banking in Europe: EBF Facts & Figures 2019. Frankfurt am Main: European Banking Federation, Available online: https://www.ebf.eu/wp-content/uploads/2020/01/EBF-Facts-and-Figures-2019-Banking-in-Europe.pdf (accessed on 31 May 2021).

- European Council. 2018. Statement on Bulgaria’s Path towards ERM II Participation. Available online: https://www.consilium.europa.eu/ro/press/press-releases/2018/07/12/statement-on-bulgaria-s-path-towards-erm-ii-participation/ (accessed on 1 June 2021).

- Fadzlan, Sufian. 2009. Determinants of Bank profitability in a Developing Economy: Empirical evidence from the China Banking Sector. Journal of Asia-Pacific Business 10: 201–307. [Google Scholar]

- Firtescu, Bogdan, and Angela Roman. 2015. Internal and external determinants of commercial banks profitability: Empirical evidence from Bulgaria and Romania. Annals of the University of Oradea, Economic Science Series 24: 896–904. [Google Scholar]

- Flamini, Valentina, Calvin McDonalds, and Liliana Schumacher. 2009. Determinants of Commercial Banks Profitability in Sub-Saharan Africa. IMF Working Paper no. 15. Washington D.C., U.S.. Available online: https://www.imf.org/external/pubs/ft/wp/2009/wp0915.pdf (accessed on 1 January 2009).

- Frøyland, Esped, and Kai Larsen. 2002. How Vulnerable Are Financial Institutions to Macroeconomic Changes? An Analysis Based on Stress Testing. Norges Bank. Economic Bulletin 3/2002. Norges Bank. Available online: https://norges-bank.brage.unit.no/norges-bank-xmlui/handle/11250/2504526 (accessed on 4 January 2021).

- García-Herrero, Alicia, Sergio Gavilá, and Daniel Santabárbara. 2009. What explains the low profitability of Chinese banks? Journal of Banking and Finance 33: 2080–92. [Google Scholar] [CrossRef] [Green Version]

- Goddard, John, Phil Molyneux, and John Wilson. 2004. Dynamic of growth and profitability in banking. Journal of Money, Credit and Banking 36: 1069–90. [Google Scholar] [CrossRef]

- Goddard, John, Hong Liu, Phil Molyneux, and John Wilson. 2010. Do bank profits converge? European Financial Management 19: 346–65. [Google Scholar]

- Guru, Balachendher, John Staunton, and Bala Balashanmugam. 2002. Determinants of Commercial Bank Profitability in Malaysia. Paper presented at 12th Annual Australian Finance and Banking Conference, Sydney, Australian, December 16–17. [Google Scholar]

- Hamadi, Hassan, and Ali Awdeh. 2012. The Determinants of Net Interest Margins of Commercial Banks in Lebanon. Journal of Money, Investment and Banking 23: 118–32. [Google Scholar]

- Heffernan, Shelagh, and Maggie Fu. 2008. The Determinants of Bank Performance in China. Working Paper Series (WP-EMG-03-2008); London: Cass Business School, City University, Available online: http://ssrn.com/abstract=1247713 (accessed on 15 May 2021).

- Hernando, Ignacio, and Maria Nieto. 2007. Is the Internet delivery channel changing banks’ performance? The case of Spanish banks. Journal of Banking and Finance 31: 1083–99. [Google Scholar] [CrossRef] [Green Version]

- Iannotta, Giuliano, Giacomo Nocera, and Andrea Sironi. 2007. Ownership structure, risk and performance in the European banking industry. Journal of Banking and Finance 31: 2127–49. [Google Scholar] [CrossRef] [Green Version]

- Ilzetzki, Ethan, Enrique Mendoza, and Carlos Vegh. 2010. How Big (Small?) are Fiscal Multipliers? IMF Working Paper 52. Washington, D.C.: International Monetary Fund. [Google Scholar]

- International Monetary Fund. 2018. Euro Area Policies: Financial Sector Assessment Program-Technical Note-Systemic Risk Analysis. IMF Staff Country Reports 18: 8–86. [Google Scholar]

- Isfaq, Jawad, and Naeem Ullah Khan. 2015. Bank profitability, inflation and cost efficiency—A case of Pakistani banks. International Journal of Business and Management Review 3: 41–53. [Google Scholar]

- Isshaq, Zangina, Benjamin Amoah, and Ishmael Appiah-Gyamerah. 2019. Non-interest income, risk and bank performance. Global Business Review 20: 595–612. [Google Scholar] [CrossRef]

- Jiang, Guorong, Eve Law, and Angela Sze. 2003. The Profitability of the Banking Sector in Hong Kong. Hong Kong Monetary Authority Quarterly Bulletin, September 16. [Google Scholar]

- Kanas, Angelos, Dimitrios Vasiliou, and Nikolaos Eriotis. 2012. Revisiting bank profitability: A semi-parametric approach. Journal of International Financial Markets, Institutions and Money 22: 990–1005. [Google Scholar] [CrossRef]

- Karasulu, Meral. 2001. The Profitability of the Banking Sector in Korea. IMF Country Report, July 2. [Google Scholar]

- Kasman, Adnan, Gokce Tunc, Gulin Vardar, and Berna Okan. 2010. Consolidation and commercial bank net interest margins: Evidence from the old and new European Union members and candidate countries. Economic Modelling 27: 648–55. [Google Scholar] [CrossRef]

- Kaya, Tanya Y. 2002. Determinants of Profitability in Turkish Banking Sector. No 1. Istanbul: Turkish Banking Regulation and Supervision Agency. [Google Scholar]

- Khan, Ihtesham, and Adnan Ahmad. 2017. Assessing banks internal factors as determinants of non-performing loans: Evidence from Pakistani commercial banks. Journal of Managerial Sciences 11: 109–25. [Google Scholar]

- Kingu, Peter, Macha Salvio, and Raphael Gwahula. 2018. Impact of Non-Performing Loans on Bank’s Profitability: Empirical Evidence from Commercial Banks in Tanzania. International Journal of Scientific Research and Management 6: 71–79. [Google Scholar]

- Kirchner, Markus, and Sweder van Wijnbergen. 2012. Fiscal Deficits, Financial Fragility, and the Effectiveness of Government Policies, Tinbergen Institute Discussion Paper, TI 2012-044/2. Available online: https://papers.tinbergen.nl/12044.pdf (accessed on 10 May 2021).

- Kolev, Atanas, and Sanne Zwart. 2013. Banking in Central and Eastern Europe and Turkey. Challenges and Opportunities. EIB 5–13. Available online: https://www.eib.org/attachments/efs/economic_report_banking_cee_turkey_en.pdf (accessed on 3 May 2021).

- Korytowski, Marcin. 2018. Banks’ profitability determinants in post-crisis European Union. IJFBS 7: 1–12. [Google Scholar] [CrossRef]

- Krakah, Anthony Kofi, and Aaron Ameyaw. 2010. Determinants of Bank’s Profitability in Ghana. Working Paper: Blekinge Tekniska Högskola. Available online: http://www.camessays.com/upload/doc/Thesis%20bank.pdf (accessed on 10 May 2021).

- Laubach, Thomas. 2009. New Evidence on the Interest Rate Effects of Budget Deficits and Debt. Journal of the European Economic Association 7: 858–85. [Google Scholar] [CrossRef] [Green Version]

- Messai, Ahlem, Mohamed Gallali, and Fathi Jouini. 2015. Determinants of bank profitability in Western European Countries evidence from system GMM estimates. International Business Research 8: 30. [Google Scholar] [CrossRef] [Green Version]

- Mester, Loretta. 1996. A study of bank efficiency taking into account risk preferences. Journal of Banking and Finance 20: 1025–1045. [Google Scholar] [CrossRef]

- Mihajlović, Ljiljana Stosic, and Ljiljana Jovic. 2017. The financial sector of the state—The structure of the banking system with a banking sector in Central and Eastern European countries. Journal of Process Management—New Technologies, International 5: 13–29. [Google Scholar] [CrossRef] [Green Version]

- Mirzaei, Ali, Tomoe Moore, and Guy Liu. 2013. Does market structure matter on banks’ profitability and stability? Emerging vs. advanced economies. Journal of Banking & Finance 37: 2920–37. [Google Scholar]

- Moinescu, Bogdan. 2008. Banking Stability and unemployment. An empirical analysis on Romania. Paper presented at IMF-NBR Regional Seminar on Financial Stability Issues, Sinaia, Romania, September 18–19. [Google Scholar]

- Molyneux, Phil. 1995. Structure and Performance in European Banking. Applied Economics 27: 155–59. [Google Scholar] [CrossRef]

- Molyneux, Phil, and John Thornton. 1992. Determinants of European bank profitability: A note. Journal of Banking and Finance 16: 1173–78. [Google Scholar] [CrossRef]

- Moyo, Delani, and Turgut Tursoy. 2020. Impact of Inflation and Exchange Rate on the Financial Performance of Commercial Banks in South Africa. Available online: https://mpra.ub.uni-muenchen.de/101383/1/MPRA_paper_101383.pdf (accessed on 19 May 2021).

- Mulas-Granados, Carlos, Emanuele Baldacci, and Sanjeev Gupta. 2009. How Effective is Fiscal Policy Response in Systemic Banking Crises? IMF Working Papers 09/160. Washington, D.C.: International Monetary Fund. [Google Scholar]

- Naceur, Sami Ben. 2003. The Determinants of the Tunisian Banking Industry Profitability: Panel Evidence. Paper presented at Economic Research Forum (ERF) 10th Annual Conference, Marrakesh, Morocco, December 16–18; Available online: http://www.mafhoum.com/press6/174E11.pdf (accessed on 19 May 2021).

- Naceur, Ben Sami, and Mohamed Goaied. 2008. The determinants of commercial bank interest margin and profitability: Evidence from Tunisia. Frontiers in Finance and 19 Economics 5: 106–30. [Google Scholar] [CrossRef] [Green Version]

- Naruševičius, Laurynas. 2018. Bank profitability and macroeconomy: Evidence from Lithuania. Technological and Economic Development of Economy 24: 383–405. [Google Scholar] [CrossRef] [Green Version]

- Nichols, Chris. 2017. The fallacy of NIM. The Data on Net Interest Margin and Bank Performance. Available online: https://www.linkedin.com/pulse/data-net-interest-margin-bank-performance-chris-nichols/ (accessed on 5 June 2021).

- Olson, Dennis, and Taisier Zoubi. 2011. Efficiency and Bank Profitability in MENA Countries. Emerging Markets Review 12: 94–110. [Google Scholar] [CrossRef]

- Onofrei, Mihaela, Ionel Bostan, Angela Roman, and Bogdan Narcis Firtescu. 2018. The determinants of commercial bank profitability in CEE countries. Romanian Statistical Review 2: 33–46. [Google Scholar]

- Pan, Qinhua, and Meiling Pan. 2014. The Impact of Macro Factors on the Profitability of China’s Commercial Banks in the Decade after WTO Accession. Open Journal of Social Sciences 2: 64–69. [Google Scholar] [CrossRef] [Green Version]

- Pasiouras, Fotios, and Kyriaki Kosmidou. 2007. Factors influencing the profitability of domestic and foreign commercial banks in the European Union. Research in International Business and Finance 21: 222–37. [Google Scholar] [CrossRef]

- Pesola, Jarmo. 2005. Banking Fragility and Distress: An Economic Study of Macroeconomic Determinants. Research Discussion Paper 13. Helsinki: Bank of Finland. [Google Scholar]

- Petkovski, Mihail, Jordan Kjosevski, and Kiril Jovanovski. 2018. Empirical Panel Analysis of Non-Performing Loans in the Czech Republic. What are their Determinants and How Strong is Their Impact on the Real Economy? Finance a úvěr-Czech Journal of Economics and Finance 68: 460–80. [Google Scholar]

- Petria, Nicolae, Bogdan Capraru, and Iulian Ihnatov. 2015. Determinants of banks’ profitability: Evidence from EU 27 banking systems. Procedia Economics and Finance 20: 518–24. [Google Scholar] [CrossRef] [Green Version]

- Psaila, Ayrton, Johnatan Spiteri, and Simon Grima. 2019. The Impact of Non-Performing Loans on the Profitability of Listed Euro-Mediterranean Commercial Banks. International Journal of Economics and Business Administration VII: 166–96. [Google Scholar]

- Rumler, Fabio, and Walter Waschiczek. 2012. Have changes in the Financial Structure Affected Bank Profitability? Evidence for Austria. The European Journal of Finance 22: 803–24. [Google Scholar] [CrossRef] [Green Version]

- Saif-Alyousfi, Abdulazeez. 2020. Determinants of bank profitability: Evidence from 47 Asian countries. Journal of Economic Studies. [Google Scholar] [CrossRef]

- Sandor, Gardo, and Martin Reiner. 2010. The Impact of the Global Economic and Financial Crisis on Central, Eastern and South-Eastern Europe: A Stock-Taking Exercise. ECB Occasional Paper, No. 114. Frankfurt am Main: European Central Bank (ECB). [Google Scholar]

- Sayilgan, Guven, and Ozgur Yildirim. 2009. Determinants of Profitability in Turkish Banking Sector: 2002–2007. International Research Journal of Finance and Economics 28: 207–13. [Google Scholar]

- Smirlock, Michael. 1985. Evidence on the (non) relationship between concentration and profitability in banking. Journal of Money, Credit, and Banking 17: 69–83. [Google Scholar] [CrossRef]

- Staikouras, Christos, and Geoffrey Wood. 2004. The Determinants of European Bank Profitability. International Business and Economics Research Journal 3: 57–68. [Google Scholar] [CrossRef] [Green Version]

- Sufian, Fadzlan. 2009. Factors Influencing Bank Profitability in a Developing Economy: Empirical Evidence from Malaysia. Global Business Review 10: 225–41. [Google Scholar] [CrossRef]

- Sufian, Fadzlan. 2011. Profitability of the Korean banking sector: Panel evidence on bank-specific and macroeconomic determinants. Journal of Economics and Management 7: 43–72. [Google Scholar]

- Tan, Yong Aaron, and Christos Floros. 2012. Bank profitability and inflation: The case of China. Journal of Economic Studies 39: 675–96. [Google Scholar] [CrossRef] [Green Version]

- Tennant, David, and Richard Sutherland. 2014. What types of banks profit most from fees charged? A cross-country examination of bank-specific and country-level determinants. Journal of Banking & Finance 49: 178–90. [Google Scholar]

- Trujillo-Ponce, Antonio. 2013. What determines the profitability of banks? Evidence from Spain. Accounting and Finance 53: 561–86. [Google Scholar] [CrossRef]

- Valahzaghard, Mohammad, and Elham Bilandi. 2014. The impact of electronic banking on profitability and market share: Evidence from banking industry. Management Science Letters 4: 2531–36. [Google Scholar] [CrossRef]

- Vivaldi, Carlo, and Marrano Mauro Giorgio. 2017. Banking Outlook: CEE Region—The Place to be, Presentation at 2017 EBRD Annual Meeting. Available online: https://www.unicreditgroup.eu/content/dam/unicreditgroup-eu/documents/en/press-and-media/press-releases/2017/2017_EBRD_Annual_Meeting_Media_Presentation.pdf (accessed on 31 May 2021).

- Vong, Anna, and Hoi Si Chan. 2009. Determinants of Bank Profitability in Macau. Macau Monetary Research Bulletin 12: 93–113. [Google Scholar]

- Yilmaz, Ayse Altiok. 2013. Profitability of Banking System: Evidence from Emerging Markets. Paper presented at WEI International Academic Antalya Conference, Antalya, Turkey, January 14–16. [Google Scholar]

- Zoghlami, Feten, and Yassine Bouchemia. 2020. Competition in the banking industry, is it beneficial? Evidence from MENA region. Journal of Banking Regulation 22: 169–79. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Notation and Measurement | Definition | Data Source |

|---|---|---|---|

| Bank profitability | |||

| Return on assets | ROA (%) | Ratio of the total profit (loss) for the year to the total assets | European Central Bank Statistical Warehouse |

| Return on equity | ROE (%) | Ratio of the total profit (loss) for the year to the total equity | |

| Net interest income margin | NIM (%) | Difference between the interest incomes on assets (i.e., loans granted, and securities held) and interest expenses from interest paid on liabilities (i.e., customer deposits, bonds) relative to the total assets. | |

| Banking system characteristics | |||

| Domestic credit to private sector | CREDIT (%) | All financial resources provided to the private sector by depository corporations, deposit-taking corporations except central banks through loans, purchases of nonequity securities, trade credits and other accounts receivable that establish a claim for repayment. | World Bank |

| Non-performing loans | NPL | Ratio of banking non-performing loans to total loans | |

| Herfindahl index for credit institutions | HERFIND | The degree of concentration of banking business (based on the total assets) calculated by summing the squares of the market shares of all the credit institutions in the banking sector | European Central Bank Statistical Warehouse |

| Solvency ratio | SOLVRATE (%) | The ratio between banks’ capital and their risk-weighted assets (CET1 ratio) | |

| Macroeconomic attributes | |||

| Public deficit/surplus | BUDBAL (%) | General government net lending (+)/net borrowing (-) ratio to gross domestic product. The general government sector comprises central government, state government, local government and social security funds. | Eurostat |

| Inflation rate | INFLATION (%) | Harmonized Index of Consumer Prices (HICP), which measures the change over time of the prices of consumer goods and services acquired by households | |

| Unemployment rate | UNEMP (%) | Unemployment share of the total labor force | World Bank |

| Variable | Mean | Median | Maximum | Minimum | Standard Deviation | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|

| ROA | 0.525 | 0.903 | 4.241 | −10.400 | 1.827 | −3.054 | 16.181 |

| ROE | 4.343 | 8.750 | 32.700 | −117.600 | 17.892 | −4.081 | 24.442 |

| NIM | 2.865 | 2.900 | 5.300 | 1.200 | 0.859 | 0.223 | 2.894 |

| CREDIT | 54.674 | 51.374 | 104.560 | 25.727 | 15.322 | 0.780 | 3.903 |

| NPL | 8.562 | 6.132 | 23.990 | 0.453 | 5.377 | 0.737 | 2.708 |

| HERFIND | 0.123 | 0.104 | 0.309 | 0.056 | 0.056 | 1.444 | 4.497 |

| SOLVRATE | 18.190 | 17.615 | 41.826 | 11.320 | 4.617 | 2.302 | 10.995 |

| BUDBAL | −2.928 | −2.600 | 2.000 | −14.600 | 2.960 | −0.924 | 4.073 |

| INFLATION | 1.794 | 1.600 | 6.100 | −1.600 | 1.763 | 0.274 | 2.368 |

| UNEMP | 9.395 | 8.900 | 19.480 | 2.240 | 3.710 | 0.574 | 2.729 |

| ROA | ROE | NIM | CREDIT | HERFIND | NPL | SOLVRATE | BUDBAL | INFLATION | UNEMP | |

|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 1 | |||||||||

| ROE | 0.937 * | 1 | ||||||||

| NIM | 0.130 | 0.131 | 1 | |||||||

| CREDIT | −0.320 * | −0.360 * | −0.238 * | 1 | ||||||

| HERFIND | 0.023 | −0.057 | −0.347 * | 0.488 * | 1 | |||||

| NPL | −0.490 * | −0.440 * | 0.134 | 0.106 | −0.295 * | 1 | ||||

| SOLVRATE | 0.306 * | 0.288 * | −0.054 | −0.009 | 0.521 * | −0.299 * | 1 | |||

| BUDBAL | 0.206 * | 0.192 * | −0.041 | −0.342 * | −0.059 | −0.071 | 0.304 * | 1 | ||

| INFLATION | 0.070 | −0.007 | 0.255 * | 0.019 | 0.029 | 0.053 | −0.194 * | −0.314 * | 1 | |

| UNEMP | −0.326 * | −0.301 * | −0.174 | 0.497 * | 0.207 * | 0.493 * | −0.211 * | −0.415 * | 0.016 | 1 |

| Variables | ROA | ROE | NIM | |||

|---|---|---|---|---|---|---|

| Coefficient | p-Value | Coefficient | p-Value | Coefficient | p-Value | |

| ROA(−1) | −0.126 | 0.000 | na | na | na | na |

| ROE(−1) | na | na | −0.098 | 0.000 | na | na |

| NIM(−1) | na | na | na | na | 0.353 | 0.000 |

| CREDIT | −0.059 | 0.039 | −0.598 | 0.003 | −0.021 | 0.046 |

| HERFIND | −39.558 | 0.018 | −384.180 | 0.010 | −10.113 | 0.375 |

| NPL | −0.236 | 0.004 | −1.945 | 0.001 | −0.029 | 0.136 |

| SOLVRATE | −0.111 | 0.013 | −1.094 | 0.032 | −0.082 | 0.000 |

| S.E of regression | 1.394 | 13.185 | 0.513 | |||

| Sargan test | 5.876 | 4.588 | 5.266 | |||

| p-value | 0.437 | 0.598 | 0.510 | |||

| AR(1) test | z = −4.308 | p = 0.000 | na | na | z = −0.013 | p = 0.989 |

| AR(2) test | z = −0.962 | p = 0.335 | z = −0.075 | p = 0.940 | z = na | p = na |

| Variables | ROA | ROE | NIM | |||

|---|---|---|---|---|---|---|

| Coefficient | p-Value | Coefficient | p-Value | Coefficient | p-Value | |

| ROA(−1) | 0.106 | 0.057 | na | na | na | na |

| ROE(−1) | na | na | 0.265 | 0.193 | na | na |

| NIM(−1) | na | na | na | na | −0.201 | 0.003 |

| BUDBAL | −0.200 | 0.010 | −2.388 | 0.000 | −0.064 | 0.011 |

| INFLATION | 0.032 | 0.320 | −2.170 | 0.045 | 0.116 | 0.000 |

| UNEMP | −0.267 | 0.000 | −1.375 | 0.081 | −0.068 | 0.020 |

| S.E of regression | 1.509 | 14.568 | 0.442 | |||

| Sargan test | 5.681 | 8.164 | 6.964 | |||

| p-value | 0.577 | 0.318 | 0.433 | |||

| AR(1) test | z = −0.144 | p = 0.885 | z = −0.845 | p = 0.398 | z = −0.267 | p = 0.789 |

| AR(2) test | z = na | p = na | z = −0.109 | p = 0.912 | z = −1.714 | p = 0.086 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Horobet, A.; Radulescu, M.; Belascu, L.; Dita, S.M. Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates. J. Risk Financial Manag. 2021, 14, 307. https://doi.org/10.3390/jrfm14070307

Horobet A, Radulescu M, Belascu L, Dita SM. Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates. Journal of Risk and Financial Management. 2021; 14(7):307. https://doi.org/10.3390/jrfm14070307

Chicago/Turabian StyleHorobet, Alexandra, Magdalena Radulescu, Lucian Belascu, and Sandra Maria Dita. 2021. "Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates" Journal of Risk and Financial Management 14, no. 7: 307. https://doi.org/10.3390/jrfm14070307

APA StyleHorobet, A., Radulescu, M., Belascu, L., & Dita, S. M. (2021). Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates. Journal of Risk and Financial Management, 14(7), 307. https://doi.org/10.3390/jrfm14070307