Stimulating Non-Energy Exports in Trinidad and Tobago: Evidence from a Small Petroleum-Exporting Economy Experiencing the Dutch Disease

Abstract

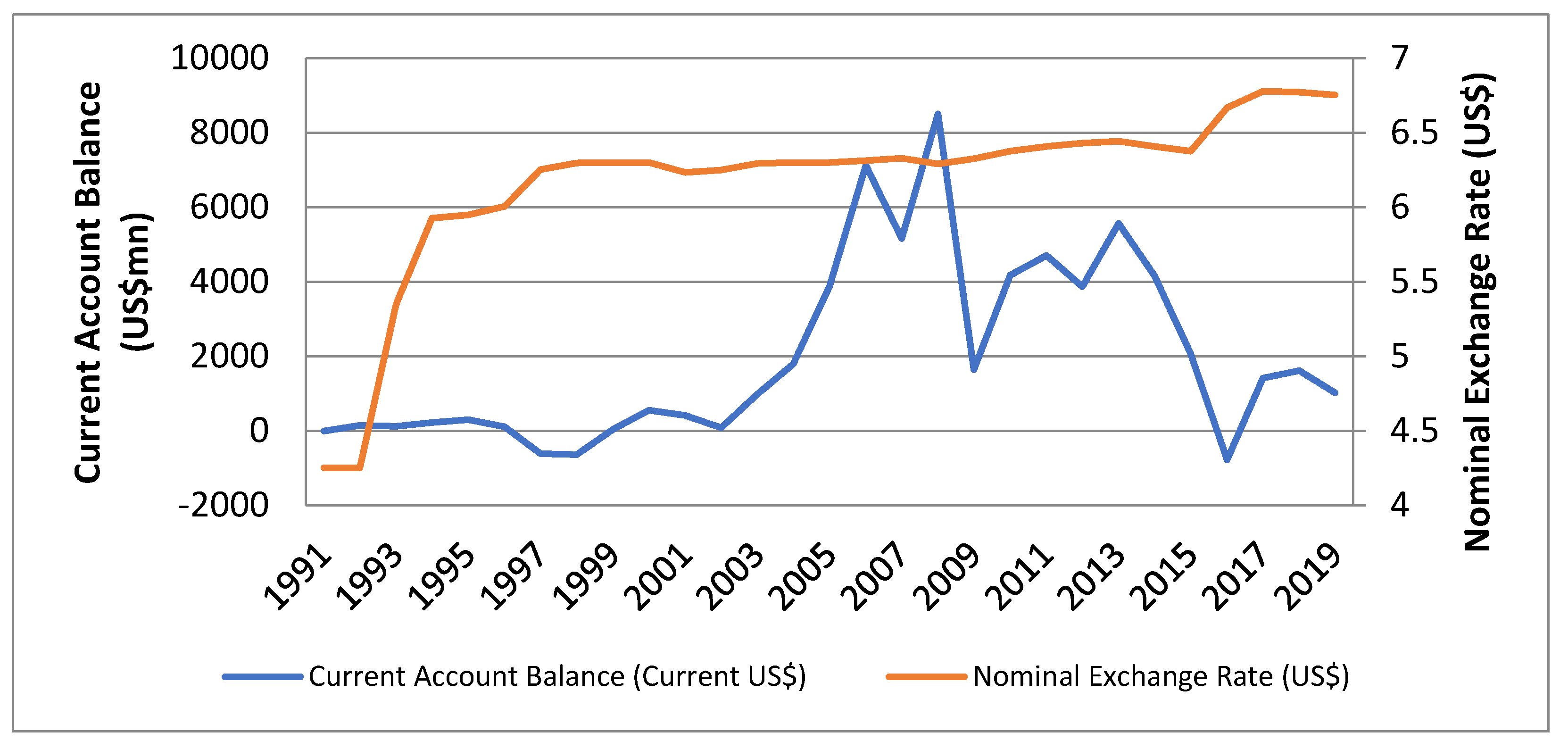

:1. Introduction

- (i)

- Does devaluing the TT dollar have a significant impact on aggregate trade?

- (ii)

- Is devaluation a feasible alternative in promoting non-energy exports?

- (iii)

- Is import substitution feasible in promoting the growth of non-energy trade?

- (iv)

- What other measures can be adopted in tandem with a devaluation of the currency if feasible, to promote non-energy exports?

2. Literature Review: Examining the Marshall–Lerner Condition in Various Countries

3. Data

Data Collection and Variables

4. Empirical Model

5. Empirical Findings

5.1. Aggregate Trade

5.2. Non-Energy Trade

5.3. Alternative Specification

5.4. What Measures Can Be Implemented along with a Devaluation of the Currency to Stimulate Non-Energy Trade in T&T?

5.4.1. Is There Potential for Import Substitution?

5.4.2. Improving the Ease of Doing Business in T&T

5.4.3. Assessing Current and Potential Markets

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Levin, Lin and Chu (LLC) | Im, Pesaran and Shin (IPS) | ||||

|---|---|---|---|---|---|---|

| Level | 1st Difference | Order of Variable | Level | 1st Difference | Order of Variable | |

| LAGTR | 0.7073 (0.7603) | −4.4551 (0.0000) *** | I(1) | −1.4605 (0.0721) * | I(0) | |

| LNETR | −2.5726 (0.0050) *** | I(0) | −4.1949 (0.0000) *** | I(0) | ||

| LAGEX | −1.0328 (0.1509) | −6.1059 (0.0000) *** | I(1) | −2.2854 (0.0111) ** | I(0) | |

| LAGIM | −2.5831 (0.0049) ** | I(0) | −2.7691 (0.0028) *** | I(0) | ||

| LNEEX | −4.2239 (0.0000) *** | I(0) | −3.1097 (0.0009) ** | I(0) | ||

| LNEIM | −2.5759 (0.0050) ** | I(0) | −3.2667 (0.0005) *** | I(0) | ||

| LNER | −35.5429 (0.0000) *** | I(0) | −8.1769 (0.0000) *** | I(0) | ||

| LMS | −0.6392 (0.2614) | −5.5264 (0.0000) *** | I(1) | 5.2510 (1.0000) | −5.4482 (0.0000) *** | I(1) |

| GDPD | −0.6278 (0.2651) | −8.2015 (0.0000) *** | I(1) | −4.2770 (0.0000) *** | I(0) | |

| GDPF | −4.3661 (0.0000) *** | I(0) | −5.9940 (0.0000) *** | I(0) | ||

| NGB | 0.1989 (0.5788) | −6.4334 (0.0000) *** | I(1) | 0.1312 (0.5522) | −6.4550 (0.0000) *** | I(1) |

| Aggregate Trade Balance Ratio Model (I) | Aggregate Exports Model (II) | Aggregate Imports Model (III) | ||||||

|---|---|---|---|---|---|---|---|---|

| LAGTR | Coef. | p-Value | LAGEX | Coef. | p-Value | LAGIM | Coef. | p-Value |

| Long run | ||||||||

| LNER | 2.235 | 0.299 | LNER | 1.282 | 0.676 | LNER | −0.501 | 0.811 |

| LMS | 0.259 | 0.255 | LMS | 1.071 | 0.016 ** | LMS | 0.795 | 0.001 *** |

| GDPD | −0.017 | 0.431 | GDPD | −0.022 | 0.529 | GDPD | 0.026 | 0.020 ** |

| GDPF | 0.041 | 0.224 | GDPF | 0.031 | 0.379 | GDPF | −0.016 | 0.524 |

| NGB | 0.214 | 0.224 | NGB | 0.320 | 0.084 * | NGB | −0.049 | 0.502 |

| Short run | ||||||||

| EC | −0.232 | 0.000 *** | EC | −0.380 | 0.000 *** | EC | −0.300 | 0.002 *** |

| ΔLNER | 1.279 | 0.103 | ΔLNER | −4.595 | 0.130 | ΔLNER | −0.832 | 0.224 |

| ΔLMS | −0.555 | 0.057 * | ΔLMS | −2.789 | 0.102 | ΔLMS | 0.529 | 0.154 |

| ΔGDPD | 0.005 | 0.163 | ΔGDPD | −0.010 | 0.410 | ΔGDPD | −0.002 | 0.430 |

| ΔGDPF | −0.002 | 0.535 | ΔGDPF | 0.026 | 0.127 | ΔGDPF | 0.010 | 0.090 * |

| ΔNGB | −0.042 | 0.011 ** | ΔNGB | −0.046 | 0.723 | ΔNGB | 0.000 | 0.998 |

| _cons | −0.715 | 0.028 ** | _cons | −1.254 | 0.273 | _cons | −0.086 | 0.878 |

| Non-Energy Trade Balance Ratio Model (IV) | Non-Energy Exports Model (V) | Non-Energy Imports Model (VI) | ||||||

|---|---|---|---|---|---|---|---|---|

| Non-Energy Ratio | Coef. | p-Value | Non- Energy Exports | Coef. | p-Value | Non- Energy Imports | Coef. | p-Value |

| Long run | ||||||||

| LNER | 1.288 | 0.025 ** | LNER | 7.655 | 0.092 * | LNER | −0.743 | 0.710 |

| LMS | −0.098 | 0.220 | LMS | 0.197 | 0.605 | LMS | 0.689 | 0.002 ** |

| GDPD | −0.000 | 0.980 | GDPD | 0.020 | 0.331 | GDPD | 0.027 | 0.051 * |

| GDPF | 0.020 | 0.080 * | GDPF | 0.077 | 0.014 ** | GDPF | −0.026 | 0.362 |

| NGB | 0.015 | 0.647 | NGB | 0.196 | 0.508 | NGB | −0.082 | 0.327 |

| Short run | ||||||||

| EC | −0.458 | 0.000 *** | EC | −0.443 | 0.000 *** | EC | −0.305 | 0.002 *** |

| ΔLNER | −0.317 | 0.514 | ΔLNER | −0.913 | 0.639 | ΔLNER | −1.041 | 0.042 ** |

| ΔLMS | −0.356 | 0.072 * | ΔLMS | −1.466 | 0.310 | ΔLMS | 0.513 | 0.178 |

| ΔGDPD | −0.001 | 0.384 | ΔGDPD | −0.013 | 0.163 | ΔGDPD | −0.004 | 0.070 * |

| ΔGDPF | −0.004 | 0.277 | ΔGDPF | 0.014 | 0.476 | ΔGDPF | 0.013 | 0.059 * |

| ΔNGB | −0.055 | 0.149 | ΔNGB | −0.246 | 0.047 ** | ΔNGB | −0.014 | 0.498 |

| _cons | −0.045 | 0.883 | _cons | −1.652 | 0.238 | _cons | 0.168 | 0.772 |

| Country | 2004 | 2006 | 2008 | 2010 | 2012 | 2015 | 2017 | 2019 |

|---|---|---|---|---|---|---|---|---|

| Trinidad and Tobago (%) | 26.38 | 37.44 | 43.00 | 30.58 | 51.76 | 33.98 | 20.79 | 21.71 |

| Trinidad and Tobago without minerals (%) | 3.93 | 4.30 | 9.15 | 13.19 | 17.57 | 7.96 | 4.94 | 6.81 |

| Ease of Doing Business (EODB) Rankingfor T&T 2014–2020 | Suggestions to Improve EODB Rankings as Performed by Other Caribbean Countries and SIDS | |||

|---|---|---|---|---|

| TT EODB Ranking | 2014 | 2020 | ||

| Global Rank | 66 | 105 | Worsened | |

| Starting a Business | 67 | 76 | Decline | —Make starting a business faster by improving the exchange of information between public entities involved in company incorporation (Antigua and Barbuda, Doing Business 2020, World Bank 2020). —Make starting a business faster by reducing the registration time for the business license and value added tax and by eliminating the business registration fee (The Bahamas, Doing Business 2020, World Bank 2020). —Make starting a business easier by reducing the minimum capital requirement (Dominican Republic, Doing Business 2020, World Bank 2020). |

| Dealing with Construction Permits | 77 | 125 | Decline | —Make dealing with construction permits easier by enhancing its risk-based approach to inspections, improving public access to soil information, and streamlining the process to obtain a construction permit (Singapore, Doing Business 2020, World Bank 2020). —Make dealing with construction permits faster by streamlining internal processes (The Seychelles, Doing Business 2020, World Bank 2020). |

| Getting Electricity | 10 | 41 | Decline | —Make getting electricity more transparent by publishing electricity tariffs online (The Bahamas, Doing Business 2020, World Bank 2020). —Make getting electricity faster by deploying new software to process applications, increasing the stock of material needed for external connection works, and offering training programs to the utility’s engineers (Barbados, Doing Business 2020, World Bank 2020). —Belize made getting electricity faster by offering training to its utility field engineers and upgrading its geographic information system to map the electricity distribution network (Belize, Doing Business 2020, World Bank 2020). |

| Getting Credit | 28 | 60 | Decline | —Improve access to credit information through the introduction of regulations that govern the licensing and functioning of credit bureaus (St. Kitts and Nevis, Doing Business 2020, World Bank 2020). |

| Protecting Minority Investors | 22 | 57 | Decline | —Strengthen minority investor protections by increasing disclosure requirements for conflicts of interest, clarifying ownership and control structures, and requiring greater corporate transparency (The Bahamas, Doing Business 2020, World Bank 2020). |

| Paying Taxes | 97 | 166 | Decline | —Make paying taxes easier by enhancing the online valueadded tax reporting system and making it more accessible to taxpayers (The Bahamas, Doing Business 2020, World Bank 2020). —Make paying taxes less costly by reducing the corporate income tax rate (St. Vincent and the Grenadines, Doing Business 2020, World Bank 2020). |

| Trading across Borders | 73 | 130 | Decline | —Make trading across borders easier by streamlining inspections by port authorities and introducing an electronic system for documentary compliance (Barbados, Doing Business 2020, World Bank 2020). |

| Enforcing Contracts | 174 | 174 | No change | —Make enforcing contracts easier by adopting a law that regulates all aspects of mediation as an alternative dispute resolution mechanism (Barbados, Doing Business 2020, World Bank 2020). —Make enforcing contracts easier by introducing a judicial performance measurement mechanism that provides publicly available information on time to disposition and clearance rate (Jamaica, Doing Business 2020, World Bank 2020). |

| US Market | |||||

|---|---|---|---|---|---|

| SITC R3 | RCA Index | Missed Opportunities | SITC R3 | RCA Index | Rising Stars |

| 91 | 1.498 | Margarine and shortening | 278 | 13.191 | Other crude minerals. |

| 334 | 3.889 | Petroleum oils or bituminous minerals >70% oil | 282 | 1.475 | Ferrous waste, scrap; remelting ingots, iron, steel. |

| 522 | 127.838 | Inorganic chemical elements, oxides and halogen salts | 289 | 3.047 | Ores and concentrates of precious metals; waste, scrap. |

| 562 | 22.390 | Fertilizers (other than those of group 272) | |||

| 671 | 34.753 | Pig iron and spiegeleisen, sponge iron, powder and granu. | |||

| EU market | |||||

| 676 | 4.625 | Iron and steel bars, rods, angles, shapes and sections | 342 | 4.560 | Liquefied propane and butane. |

| 343 | 33.288 | Natural gas, whether or not liquefied. | |||

| 512 | 96.9435 | Alcohols, phenols, halogenat. sulfonat., nitrat. der. | |||

| 522 | 8.7611 | Inorganic chemical elements, oxides and halogen salts. | |||

| 562 | 4.5489 | Fertilizers (other than those of group 272). | |||

| Guyana market | |||||

|---|---|---|---|---|---|

| SITC R3 | RCA Index | Missed Opportunities | SITC R3 | RCA Index | Rising Stars |

| 17 | 1.949 | Meat, edible meat offal, prepared, preserved, n.e.s. | 98 | 1.061 | Edible products and preparations, n.e.s. |

| 278 | 1.209 | Other crude minerals. | |||

| 642 | 1.916 | Paper and paperboard, cut to shape or size, articles. | |||

| 661 | 1.422 | Lime, cement, fabrica. constr. mat. (excluding glass, clay). | |||

| 665 | 1.178 | Glassware | |||

| 676 | 1.633 | Iron and steel bars, rods, angles, shapes and sections. | |||

| Jamaica market | |||||

| 48 | 5.228 | Cereal preparations, flour of fruits or vegetables | 122 | 10.161 | Tobacco, manufactured |

| 533 | 1.120 | Pigments, paints, varnishes and related materials. | |||

| 581 | 2.823 | Tubes, pipes and hoses of plastics. | |||

| Dominican Republic market | |||||

| 111 | 1.197 | Non-alcoholic beverages, n.e.s. | 893 | 1.177 | Articles, n.e.s., of plastics. |

References

- Adhikari, Deergha Raj. 2018. Testing the Marshall–Lerner Condition and the J–Curve Effect on U.S–China Trade. Journal of Applied Business and Economics 20: 11–18. [Google Scholar] [CrossRef]

- Akoto, Linda. 2016. An Empirical Analysis of the Determinants of Trade Balance in Post–Liberalisation Ghana. Master of Philosophy thesis, Kwame Nkrumah University of Science and Technology, Kumasi, Ghana. [Google Scholar]

- Arruda, Elano, Pablo Urano De Carvalho Castelar, and Gabriel Martins. 2019. The J-Curve and the Marshall-Lerner condition: Evidence from net exports in the Southern Region of Brazil. Journal of Planning and Public Policies 52: 17–48. [Google Scholar]

- Bahmani, Mohsen, Hanafiah Harvey, and Scott W. Hegerty. 2013. Empirical Tests of the Marshall–Lerner Condition: A Literature Review. Journal of Economic Studies 40: 411–43. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, Mohsen, and Janardhanan Alse. 1994. Short-run versus long-run effects of devaluation: error correction modeling and cointegration. Eastern Economic Journal 20: 453–64. [Google Scholar]

- Bahmani-Oskooee, Mohsen, and Amr Sadek Hosny. 2013. Long–Run Price Elasticities and the Marshall–Lerner Condition: Evidence from Egypt–EU Commodity Trade. The European Journal of Development Research 25: 695–713. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, Mohsen, and Tachawan Kantipong. 2001. Bilateral J-Curve Between Thailand and Her Trading Partners. Journal of Economic Development 26: 107–117. [Google Scholar]

- Bahmani-Oskooee, Mohsen, and Artatrana Ratha. 2004. The J-Curve Dynamics of U.S. Bilateral Trade. Journal of Economics and Finance 28: 32–38. [Google Scholar] [CrossRef]

- Behar, Alberto, and Armand Fouejieu. 2018. External Adjustment in Oil Exporters: The Role of Fiscal Policy and the Exchange Rate. The World Economy 41: 926–57. [Google Scholar] [CrossRef]

- Boyd, Derick, and Ron Smith. 2005. The Marshall-Lerner Condition and the J-Curve Effect: Balance of Payments Adjustment in the Caribbean. Caribbean Dialogue 10: 31–46. [Google Scholar]

- Boyd, Derick, Gugielmo Maria Caporale, and Ron Smith. 2001. Real Exchange Rate Effects on the Balance of Trade: Cointegration and the Marshall–Lerner Condition. International Journal of Finance & Economics 6: 197–200. [Google Scholar] [CrossRef]

- Cambazoglu, Birgul, and Sevcan Gunes. 2016. Marshall–Lerner Condition Analysis: Turkey Case. Economics, Management, and Financial Markets 11: 272–83. [Google Scholar]

- Caporale, Guglielmo Maria, Robert Mudida, and Luis Alberiko Gil-Alana. 2015. Testing the Marshall–Lerner Condition in Kenya. South African Journal of Economics 83: 253–68. [Google Scholar] [CrossRef] [Green Version]

- Central Bank of Trinidad and Tobago. 2016. 2016 Annual Economic Survey. Port of Spain: Central Bank of Trinidad of Tobago. [Google Scholar]

- Chebbi, Houssem Eddine, and Marcelo Olarreaga. 2019. Investigating Exchange Rate Shocks on Agricultural Trade Balance: The Case of Tunisia. The Journal of International Trade & Economic Development 28: 628–47. [Google Scholar] [CrossRef]

- Corden, W. Max, and J. Peter Neary. 1982. Booming Sector and De–Industrialisation in a Small Open Economy. The Economic Journal 92: 825–48. [Google Scholar] [CrossRef] [Green Version]

- Dongfack, Laetitia P. Sokeng, and Hongbing Ouyang. 2019. The Impact of Real Exchange Rate Depreciation on Cameroon’s Trade Balance: Is Devaluation a Remedy for Persistent Trade Deficits? Journal of Economic Integration 34: 189–213. [Google Scholar] [CrossRef] [Green Version]

- Eita, Joel Hinaunye. 2013. Estimation of The Marshall–Lerner Condition for Namibia. International Business & Economics Research Journal (IBER) 12: 510–18. [Google Scholar] [CrossRef] [Green Version]

- Engle, Robert, and C. W. Granger. 1987. Co-Integration and Error Correction: Representation, Estimation and Testing. Econometrica 55: 251–76. [Google Scholar] [CrossRef]

- Erdem, Ekrem, Gulbahar Ucler, and Umit Bulut. 2014. Impact of Domestic Credits on the Current Account Balance: A Panel ARDL Analysis for 15 OECD Countries. Actual Problems of Economics 15: 408–16. [Google Scholar]

- Guo, Geato. 2020. Estimating the Marshall-Lerner Condition of China. Journal of Economics and International Finance 12: 48–56. [Google Scholar]

- Halicioglu, Ferda. 2008. The J-curve dynamics of Turkey: an application of ARDL model. Applied Economics 40: 2439–29. [Google Scholar] [CrossRef] [Green Version]

- Hsing, Yu. 2010. Test of the Marshall–Lerner Condition for Eight Selected Asian Countries and Policy Implications. Global Economic Review 39: 91–98. [Google Scholar] [CrossRef]

- Im, Kyung So, Hashem Pesaran, and Yongcheol Shin. 2003. Testing for unit roots in heterogeneous panels. Journal of Econometrics 115: 53–74. [Google Scholar] [CrossRef]

- International Monetary Fund. 2016. Trinidad and Tobago 2016 Article IV Consultation–Press Release and Staff Report. IMF Country Report No. 16/204. Washington, DC: International Monetary Fund. [Google Scholar]

- International Monetary Fund. 2018. Trinidad and Tobago 2018 Article IV Consultation–Press Release and Staff Report. IMF Country Report No. 18/285. Washington, DC: International Monetary Fund. [Google Scholar]

- Johansen, Søren. 1991. Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models. Econometrica 59: 1551–80. [Google Scholar] [CrossRef]

- Krugman, Paul, and Maurice Obstfeld. 2000. International Economics, 5th ed. Reading: Addison–Wesley. [Google Scholar]

- Lal, Anil K., and Thomas C. Lowinger. 2002. The J-Curve: Evidence from East Asia. Journal of Economic Integration 17: 397–415. [Google Scholar] [CrossRef] [Green Version]

- Levin, Andrew, Chien-Fu Chin, and Chia-Shang James Chu. 2002. Unit root tests in panel data: asymptotic and finite-sample properties. Journal of Econometrics 108: 1–24. [Google Scholar] [CrossRef]

- Moore, Winston, Jamila Beckles, and DeLisle Worrell. 2015. Size Structure and Devaluation. Wanstead: The University of the West Indies, Cave Hill Campus Barbados. [Google Scholar]

- Nolazco, Jose. 2012. Re–Examination of the Marshall–Lerner Condition in Peru at a Disaggregated Level: An Analysis in the Unbalanced Panel. SSRN. [Google Scholar] [CrossRef]

- Nusair, Salah. 2017. The J-Curve phenomenon in European transition economies: A nonlinear ARDL approach. International Review of Applied Economics 31: 1–26. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, and Yongcheol Shin. 1999. An autoregressive distributed lag modeling approach to cointegration analysis. In Econometrics and Economic Theory in 20th Century: the Ragnar Frisch Centennial Symposium. Edited by S. Strom. Cambridge: Cambridge University Press. [Google Scholar]

- Pesaran, M. Hashem, Yongcheol Shin, and Ron P. Smith. 1999. Pooled Mean Group Estimation of Dynamic Heterogeneous Panels. Journal of the American Statistical Association 94: 621–34. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Ron P. Smith. 2001. Bound testing approaches to the analysis of level relationship. Journal of Applied Economics 16: 289–326. [Google Scholar] [CrossRef]

- Petrovic, Pavle, and Mirjana Gligoric. 2010. Exchange Rate and Trade Balance: J–Curve Effect. Panoeconomicus 1: 23–41. [Google Scholar] [CrossRef]

- Phillips, Peter, and Bruce Hansen. 1990. Statistical Inference in Instrumental Variables Regression with I(1) process. Review of Economic Studies 87: 99–123. [Google Scholar] [CrossRef]

- Regis, Kyron. 2020. Economists: Devaluing TT Dollar Not the Best Option. Trinidad and Tobago Guardian, December 24. [Google Scholar]

- Richards, Dawn. 1996. The Trade Adjustment Debate and Its Implications for Caribbean Economies: The Case of Jamaica, 1962–1991. ProQuest Dissertations and Theses, UMI Microform, Ann Arbor, MI, USA. [Google Scholar]

- Shahzad, Adnan, Bilal Nafees, and Nazar Farid. 2017. Marshall–Lerner Condition for South Asia: A Panel Study Analysis. Pakistan Journal of Commerce and Social Sciences 11: 559–75. [Google Scholar]

- Straughn, Ryan. 2004. Estimating Long Run Relationships between the Trade Balance and the Terms of Trade in Selected CARICOM Countries. Working Paper 2003-6. Bridgetown: Central Bank of Barbados, pp. 67–86. [Google Scholar]

- Turkay, Hakan. 2014. The Validity of Marshall–Lerner Condition in Turkey: A Cointegration Approach. Theoretical and Applied Economics XXI 10: 21–32. [Google Scholar]

- Usui, Norio. 1997. Dutch Disease and Policy Adjustments to the Oil Boom. Kokusai Keizai 48: 136–37. [Google Scholar] [CrossRef]

- Vieira, Flavio, and Cleomar Gomes Da Silva. 2019. The Role of International Reserves on Real Exchange Rate: A Panel ARDL Model. Approach. ANPEC 2019: 1–16. [Google Scholar]

- Whitehall, Peter. 1986. Devaluation and Export Earnings in Small Economies: The Marshall-Lerner Insight. Bridgetown: Central Bank of Barbados, pp. 132–35. [Google Scholar]

- Wilson, Shelly-Ann, and Esmond McLean. 2014. Understanding the impact of Exchange Rate Adjustment on the Trade Balance of Selected Caribbean Countries. Working Paper. Kingston: Bank of Jamaica, p. 134. [Google Scholar]

- World Bank. 2020. Doing Business 2020. Washington, DC: World Bank. [Google Scholar]

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Logged variables (L) | |||||

| LAGTR | 290 | 0.577 | 0.482 | 0 | 1.899 |

| LAGEX | 290 | 4.749 | 1.208 | 0 | 6.933 |

| LAGIM | 290 | 4.665 | 0.807 | 2.417 | 6.554 |

| LNETR | 290 | 0.305 | 0.358 | 0 | 1.289 |

| LNEEX | 290 | 3.974 | 1.257 | 0 | 5.945 |

| LNEIM | 290 | 4.548 | 0.815 | 2.330 | 6.402 |

| LNER | 290 | 0.788 | 0.048 | 0.628 | 0.831 |

| LMS | 290 | 6.773 | 0.360 | 6.287 | 7.229 |

| Unlogged variables | |||||

| GDPD | 290 | 3.883 | 4.810 | −5.602 | 14.441 |

| GDPF | 290 | 3.738 | 3.487 | −5.693 | 14.231 |

| Dummy variable | |||||

| NGB | 290 | 0.414 | 0.493 | 0 | 1 |

| Aggregate Trade Balance Ratio Model (I) | Aggregate Exports Model (II) | Aggregate Imports Model (III) | ||||||

|---|---|---|---|---|---|---|---|---|

| LAGTR | Coef. | p-Value | LAGEX | Coef. | p-Value | LAGIM | Coef. | p-Value |

| Long run | ||||||||

| LNER | 0.267 | 0.561 | LNER | −0.174 | 0.762 | LNER | −0.162 | 0.734 |

| LMS | 0.154 | 0.011 ** | LMS | 0.811 | 0.000 *** | LMS | 0.504 | 0.000 *** |

| GDPD | −0.004 | 0.460 | GDPD | 0.012 | 0.034 ** | GDPD | 0.016 | 0.000 *** |

| GDPF | 0.017 | 0.028 ** | GDPF | 0.021 | 0.042 ** | GDPF | 0.012 | 0.188 |

| NGB | 0.190 | 0.000 *** | NGB | 0.214 | 0.000 *** | NGB | −0.066 | 0.035 ** |

| Short run | ||||||||

| EC | −0.442 | 0.000 *** | EC | −0.530 | 0.000 *** | EC | −0.388 | 0.000 *** |

| ΔLNER | 0.845 | 0.130 | ΔLNER | −6.447 | 0.127 | ΔLNER | −1.350 | 0.089 * |

| ΔLMS | −0.639 | 0.263 | ΔLMS | −3.228 | 0.066 * | ΔLMS | 0.632 | 0.053 * |

| ΔGDPD | 0.002 | 0.466 | ΔGDPD | −0.025 | 0.088 * | ΔGDPD | −0.003 | 0.159 |

| ΔGDPF | −0.002 | 0.657 | ΔGDPF | 0.019 | 0.162 | ΔGDPF | 0.002 | 0.656 |

| ΔNGB | −0.094 | 0.000 *** | ΔNGB | −0.136 | 0.334 | ΔNGB | 0.017 | 0.496 |

| _cons | −0.296 | 0.000 *** | _cons | −0.139 | 0.289 | _cons | 0.658 | 0.008 *** |

| Non-Energy Trade Balance Ratio Model (IV) | Non-Energy Exports Model (V) | Non-Energy Imports Model (VI) | ||||||

|---|---|---|---|---|---|---|---|---|

| Non- Energy Ratio | Coef. | p-Value | Non- Energy Exports | Coef. | p-Value | Non- Energy Imports | Coef. | p-Value |

| Long run | ||||||||

| LNER | 0.548 | 0.041 ** | LNER | 3.153 | 0.000 *** | LNER | −0.281 | 0.573 |

| LMS | −0.064 | 0.014 ** | LMS | 0.105 | 0.105 | LMS | 0.473 | 0.000 *** |

| GDPD | −0.003 | 0.169 | GDPD | 0.007 | 0.171 | GDPD | 0.018 | 0.000 *** |

| GDPF | 0.014 | 0.000 *** | GDPF | 0.011 | 0.172 | GDPF | 0.016 | 0.117 |

| NGB | −0.001 | 0.967 | NGB | −0.017 | 0.609 | NGB | −0.070 | 0.041 ** |

| Short run | ||||||||

| EC | −0.411 | 0.000 *** | EC | −0.431 | 0.000 *** | EC | −0.368 | 0.000 *** |

| ΔLNER | −0.130 | 0.553 | ΔLNER | −3.695 | 0.139 | ΔLNER | −1.506 | 0.043 ** |

| ΔLMS | −0.210 | 0.101 | ΔLMS | −0.624 | 0.437 | ΔLMS | 0.613 | 0.021 ** |

| ΔGDPD | 0.000 | 0.718 | ΔGDPD | −0.014 | 0.051 * | ΔGDPD | −0.006 | 0.001 *** |

| ΔGDPF | −0.003 | 0.200 | ΔGDPF | 0.020 | 0.357 | ΔGDPF | 0.003 | 0.494 |

| ΔNGB | −0.039 | 0.218 | ΔNGB | −0.126 | 0.216 | ΔNGB | −0.006 | 0.767 |

| _cons | 0.101 | 0.011** | _cons | 0.302 | 0.248 | _cons | 0.683 | 0.007 *** |

| Top Five Imported Commodities | Import Value (USD 000s) | % of Total Imports | Export Value ^ (USD 000s) | Max Import Substitution Value ^^ (USD 000s) |

|---|---|---|---|---|

| Machinery, mechanical appliances, boilers ... parts thereof | 1,194,861 | 17.13 | 340,181 | 340,181 |

| Mineral fuels, mineral oils and products of their distillation; bituminous substances; mineral ... | 1,115,367 | 15.99 | 5,658,571 | 1,115,367 |

| Vehicles other than railway or tramway rolling stock, and parts and accessories thereof | 404,326 | 5.80 | 7414 | 7414 |

| Electrical machinery and equipment and parts thereof; sound recorders and reproducers, televisions ... | 356,202 | 5.11 | 38,035 | 38,035 |

| Ores, slag and ash | 353,123 | 5.06 | 13,114 | 13,114 |

| Total imports | 6,974,900 | 49.09 | 1,514,111 | |

| Potential for import substitution industrialization | % | |||

| Max import substitutes as a % of total imports with minerals | 21.71 | |||

| Max import substitutes as a % of total imports without minerals | 6.81 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hosein, R.; Boodram, L.; Saridakis, G. Stimulating Non-Energy Exports in Trinidad and Tobago: Evidence from a Small Petroleum-Exporting Economy Experiencing the Dutch Disease. J. Risk Financial Manag. 2022, 15, 36. https://doi.org/10.3390/jrfm15010036

Hosein R, Boodram L, Saridakis G. Stimulating Non-Energy Exports in Trinidad and Tobago: Evidence from a Small Petroleum-Exporting Economy Experiencing the Dutch Disease. Journal of Risk and Financial Management. 2022; 15(1):36. https://doi.org/10.3390/jrfm15010036

Chicago/Turabian StyleHosein, Roger, Leera Boodram, and George Saridakis. 2022. "Stimulating Non-Energy Exports in Trinidad and Tobago: Evidence from a Small Petroleum-Exporting Economy Experiencing the Dutch Disease" Journal of Risk and Financial Management 15, no. 1: 36. https://doi.org/10.3390/jrfm15010036

APA StyleHosein, R., Boodram, L., & Saridakis, G. (2022). Stimulating Non-Energy Exports in Trinidad and Tobago: Evidence from a Small Petroleum-Exporting Economy Experiencing the Dutch Disease. Journal of Risk and Financial Management, 15(1), 36. https://doi.org/10.3390/jrfm15010036