Wealth Inequality in South Africa—The Role of Government Policy

Abstract

:1. Introduction

2. Literature Review

2.1. Theoretical Literature Review

2.2. Empirical Literature Review

2.3. Contribution to Literature

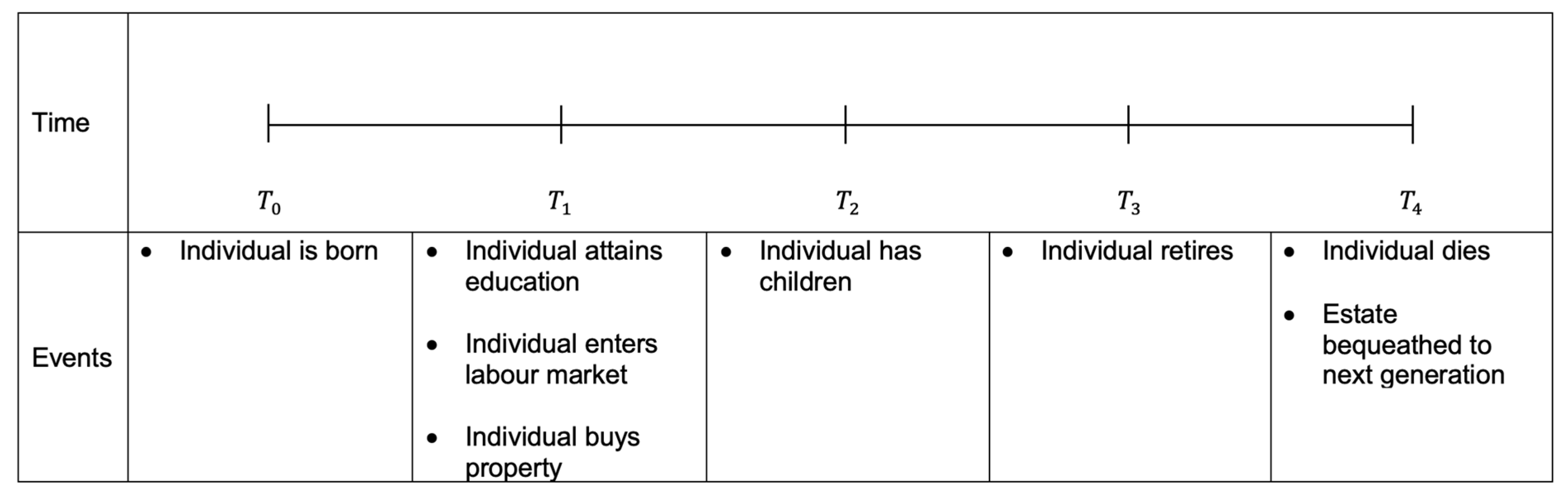

3. Model Framework

3.1. Quality of Life, Cost of Living, and Lifetime Level of Accumulated Wealth

3.2. Macro-Economic Wealth Inequality Model

4. Data Analysis and Results

4.1. Quality of Life, Cost of Living, and Lifetime Level of Accumulated Wealth

4.2. Macro-Economic Wealth Inequality Model

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Arendse, Jackie, and Lilla Stack. 2018. Investigating a new wealth tax in South Africa: Lessons from international experience. Journal of Economic and Financial Sciences 11: 1–12. [Google Scholar] [CrossRef]

- Bagchi, Sutirtha, and Jan Svejnar. 2015. Does wealth inequality matter for growth? The effect of billionaire wealth, income distribution, and poverty. Journal of Comparative Economics 43: 505–30. [Google Scholar] [CrossRef] [Green Version]

- Bluestone, Barry, Irving Bluestone, and Bennett Harrison. 1982. The Deindustrialization of America. New York: Basic Books. [Google Scholar]

- Bond, Patrick, and Christopher Malikane. 2019. Inequality caused by macro-economic policies during over-accumulation crisis. Development Southern Africa 36: 803–20. [Google Scholar] [CrossRef]

- Browning, Martin, and Thomas F. Crossley. 2001. The life-cycle model of consumption and saving. Journal of Economic Perspectives 15: 3–22. [Google Scholar] [CrossRef] [Green Version]

- Causa, Orsetta, Anna Vindics, and Oguzhan Akgun. 2018. An Empirical Investigation on the Drivers of Income Redistribution Across OECD Countries. Working Paper Number 1488. Paris: Organisation for Economic Co-operation and Development. [Google Scholar]

- Černiauskas, Nerijus, Denisa M. Sologon, Cathal O’Donoghue, and Linas Tarasonis. 2022. Income inequality and redistribution in Lithuania: The role of policy, labor market, income, and demographics. Review of Income and Wealth 68: 131–66. [Google Scholar] [CrossRef]

- Chatterjee, Aroop. 2019. Measuring wealth inequality in South Africa: An agenda. Development Southern Africa 36: 839–59. [Google Scholar] [CrossRef] [Green Version]

- Chatterjee, Aroop, Léo Czajka, and Amory Gethin. 2020. Estimating the Distribution of Household Wealth in South Africa. Working Paper Number 2020/06. Johannesburg: Southern Centre for Inequality Studies. [Google Scholar]

- Chatterjee, Aroop, Léo Czajka, and Amory Gethin. 2021. Can Redistribution Keep Up with Inequality? Evidence from South Africa, 1993–2019. Working Paper Number 2021/20. Paris: World Inequality Lab. [Google Scholar]

- Costanza, Robert, Brendan Fisher, Saleem Ali, Caroline Beer, Lynne Bond, Roelof Boumans, Nicholas L. Danigelis, Jennifer Dickinson, Carolyn Elliott, Joshua Farley, and et al. 2007. Quality of life: An approach integrating opportunities, human needs and subjective well-being. Ecological Economics 61: 267–76. [Google Scholar] [CrossRef]

- Dickens, William T., Robert K. Triest, and Rachel B. Sederberg. 2017. The changing consequences of unemployment for household finances. Journal of the Social Sciences 3: 202–21. [Google Scholar] [CrossRef]

- Dickman, Samuel L., David U. Himmelstein, and Steffie Woolhandler. 2017. Inequality and the health-care system in the USA. The Lancet 389: 1431–41. [Google Scholar] [CrossRef]

- Fortuin, Marlin. Jason. 2021. Macro-Economic Policy and Personal Finance Influences on Wealth in South Africa. Unpublished Master’s dissertation, University of South Africa, Pretoria, South Afria. [Google Scholar]

- Galor, Oded, and Omer Moav. 2006. Das human-kapital: A theory of demise of the class structure. Review of Economic Studies 73: 85–117. [Google Scholar] [CrossRef]

- Griesdorn, Tim, Jean M. Lown, Sharon A. DeVaney, Soo Hyun Cho, and David Evans. 2014. Association between behavioral life-cycle constructs and financial risk tolerance of low- to moderate-income households. Journal of Financial Counselling and Planning 25: 27–39. Available online: https://ssrn.com/abstract=2466555 (accessed on 25 March 2021).

- Konstantakopoulou, Ioanna. 2020. Further evidence on import demand function and income inequality. Economies 8: 91. [Google Scholar] [CrossRef]

- Korzeniewicz, Roberto Patricio, and Timothy Patrick Moran. 2005. Theorizing the relationship between inequality and economic growth. Theory and Society 34: 277–316. [Google Scholar] [CrossRef]

- Krivo, Lauren J., and Robert L. Kaufman. 2004. Housing and wealth inequality: Racial-ethnic differences in home equity in the United States. Demography 41: 585–605. [Google Scholar] [CrossRef] [PubMed]

- Lannegren, Olivia, and Hiroshi Ito. 2017. The end of the ANC era: An analysis of corruption and inequality in South Africa. Journal of Politics and Law 10: 55–59. [Google Scholar] [CrossRef] [Green Version]

- Leibbrandt, Murray, Arden Finn, and Ingrid Woolard. 2012. Describing and decomposing post-apartheid income inequality in South Africa. Development Southern Africa 29: 19–34. [Google Scholar] [CrossRef]

- Lentz, Rasmus, and Torben Tranaes. 2005. Job search and saving: Wealth effects and duration dependence. Journal of Labor Economics 23: 467–89. [Google Scholar] [CrossRef] [Green Version]

- Levin, Laurence. 1998. Are assets fungible? Testing the behavioural theory of life-cycle savings. Journal of Economic Behaviour & Organization 36: 59–83. [Google Scholar] [CrossRef]

- Lindbeck, Assar. 1983. Budget expansion and inflation cost. American Economic Review: Papers and Proceedings 73: 285–296. [Google Scholar]

- Lupu, Noam, and Jonas Pontusson. 2011. The structure of inequality and the politics of redistribution. American Political Science Review 105: 316–36. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, Pierre-Carl Michaud, and Olivia S. Mitchell. 2017. Optimal financial knowledge and wealth inequality. Journal of Political Economy 125: 431–77. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Mdluli, Phindile, Precious Mncayi, and Thabang Mc Camel. 2019. Examining factors that drive government spending in South Africa. Paper presented at International Academic Conferences 9912246, Barcelona, Spain, October; International Institute of Social and Economic Science. [Google Scholar]

- Michie, Jonathan. 2020. Why did the ANC fail to deliver redistribution? International Review of Applied Economics 34: 522–27. [Google Scholar] [CrossRef]

- Mumtaz, Haroon, and Angeliki Theophilopoulou. 2020. Monetary policy and wealth inequality over the great recession in the UK. An empirical analysis. European Economic Review 130: 103598. [Google Scholar] [CrossRef]

- National Treasury. 2020. Fiscal Outlook: Taking Action to Stabilise Public Debt. Available online: http://www.treasury.gov.za/documents/national%20budget/2020S/review/Chapter%204.pdf (accessed on 14 September 2021).

- National Treasury. 2022. Documents—National Budget. Available online: http://www.treasury.gov.za/documents/national%20budget/default.aspx (accessed on 2 April 2022).

- Nowatzki, Nadine. R. 2012. Wealth inequality and health: A political economy perspective. International Journal of Health Services 42: 403–24. [Google Scholar] [CrossRef]

- O’Farrell, Rory, and Lukasz Rawdanowicz. 2017. Monetary policy and inequality: Financial channels. International Finance 20: 174–88. [Google Scholar] [CrossRef]

- Okun, Arthur. M. 1975. Equality and Efficiency: The Big Trade-Off. Washington, DC: Brookings Institution Press. [Google Scholar]

- Omilola, Babatunde, and Olusegun A. Akanbi. 2014. Impact of macroeconomic, institutional and structural factors on inequality in South Africa. Development 57: 559–77. Available online: https://ideas.repec.org/a/pal/develp/v57y2014i3-4p559-577.html (accessed on 7 June 2020). [CrossRef]

- Padayachee, Vishnu. 2019. Can progressive macroeconomic policy address growth and employment while reducing inequality in South Africa? The Economic and Labour Relations Review 30: 3–21. [Google Scholar] [CrossRef]

- Pfeffer, Fabian T. 2018. Growing wealth gaps in education. Demography 55: 1033–68. [Google Scholar] [CrossRef]

- Piketty, Thomas. 2014. Capital in the Twenty-First Century. Cambridge: Belknap Press of Harvard University Press. [Google Scholar]

- Polus, Andrzej, Dominik Kopiński, and Wojciech Tycholiz. 2021. Reproduction and convertibility: Examining wealth inequalities in South Africa. Third World Quarterly 42: 292–311. [Google Scholar] [CrossRef]

- Ringen, Stein. 1991. Households, standard of living, and inequality. Review of Income and Wealth 37: 1–13. [Google Scholar] [CrossRef]

- Saiki, Ayako, and Jon Frost. 2014. Does unconventional monetary policy affect inequality? Evidence from Japan. Applied Economics 46: 4445–54. [Google Scholar] [CrossRef]

- Schooley, Diane K., and Debra Drecnik Worden. 2008. A behavioural life-cycle approach to understanding the wealth effect. Business Economics 43: 7–15. [Google Scholar] [CrossRef]

- Shefrin, Hersh M., and Richard H. Thaler. 1988. The behavioural life-cycle hypothesis. Economic Inquiry 26: 609–43. [Google Scholar] [CrossRef]

- Statistics South Africa. 2021. General Household Survey (GHS), 2020. Available online: https://www.statssa.gov.za/?page_id=1854&PPN=P0318&SCH=73007 (accessed on 20 April 2022).

- Subramanian, Sreenivasan, and Dhairiyarayar Jayaraj. 2013. The evolution of consumption and wealth inequality in India: A quantitative assessment. Journal of Globalization and Development 4: 253–81. [Google Scholar] [CrossRef]

- Susniene, Dalia, and Algirdas Jurkauskas. 2009. The concepts of quality of life and happiness–correlation and differences. Engineering Economics 63: 59–66. Available online: https://www.inzeko.ktu.lt/index.php/EE/article/view/11648 (accessed on 2 April 2022).

- Tyler, Theodore, and Louis Felix. 2020. Wealth inequality and its effects on society. Journal of Applied Sciences 5: 26–31. Available online: https://www.idosr.org/wp-content/uploads/2020/09/IDOSR-JAS-52-26-31-2020.pdf (accessed on 2 April 2022).

- von Fintel, Dieter, and Anna Orthofer. 2020. Wealth inequality and financial inclusion: Evidence from South African tax and survey records. Economic Modelling 91: 568–78. [Google Scholar] [CrossRef]

- Wolff, Edward N., and Ajit Zacharias. 2007. The distributional consequences of government spending and taxation in the U.S., 1989 and 2000. Review of Income and Wealth 53: 692–715. [Google Scholar] [CrossRef]

{kind=link}

| Year | q1 (ZAR) | q2 (ZAR) | q3 (ZAR) | q4 (ZAR) | q5 (%) | (ZAR) |

|---|---|---|---|---|---|---|

| 2010 | 8,108,224 | 2,816,900 | 946,734 | 2,644,016 | 49.7 | 17,773,438 |

| 2011 | 6,480,462 | 2,922,634 | 837,898 | 2,299,716 | 50.1 | 15,367,950 |

| 2012 | 5,894,897 | 2,982,316 | 752,682 | 2,110,880 | 49.7 | 14,418,277 |

| 2013 | 6,433,143 | 3,335,832 | 783,642 | 2,374,146 | 47.4 | 15,556,807 |

| 2014 | 6,948,248 | 3,661,267 | 861,002 | 2,515,992 | 47.1 | 16,872,728 |

| 2015 | 7,800,180 | 4,141,359 | 879,790 | 2,718,180 | 45.4 | 18,664,229 |

| 2016 | 8,374,092 | 4,335,774 | 814,602 | 2,829,587 | 46.3 | 19,781,370 |

| 2017 | 8,193,179 | 4,752,234 | 832,123 | 2,724,402 | 44.7 | 19,931,661 |

| 2018 | 10,714,026 | 4,985,666 | 890,485 | 3,913,170 | 44.8 | 24,027,591 |

| 2019 | 9,509,116 | 5,256,561 | 954,278 | 3,375,730 | 45.3 | 22,842,512 |

| Year | (ZAR) | (ZAR) | (ZAR) | (ZAR) | (ZAR) |

|---|---|---|---|---|---|

| 2010 | 0 | 923,506 | 4,488,777 | 35,951,182 | 1,084,633 |

| 2011 | 0 | 552,126 | 2,832,832 | 23,416,578 | 1,196,454 |

| 2012 | 0 | 370,246 | 2,248,147 | 20,532,971 | 1,306,807 |

| 2013 | 0 | 362,556 | 2,221,121 | 20,237,569 | 1,374,112 |

| 2014 | 0 | 365,749 | 2,269,376 | 20,623,813 | 1,497,411 |

| 2015 | 0 | 383,790 | 2,381,316 | 21,641,105 | 1,673,409 |

| 2016 | 0 | 399,391 | 2,478,120 | 22,520,854 | 1,794,887 |

| 2017 | 0 | 399,318 | 2,477,662 | 22,516,689 | 1,848,064 |

| 2018 | 0 | 400,219 | 2,483,258 | 22,567,546 | 1,924,657 |

| 2019 | 0 | 396,591 | 2,460,746 | 22,362,961 | 1,972,229 |

| Year | ||||||

|---|---|---|---|---|---|---|

| 2010 | 379,437 | 290,783 | 777,482 | 498,866 | 1,946,568 | 14,742,237 |

| 2011 | 393,851 | 310,205 | 823,132 | 572,443 | 2,099,632 | 12,071,864 |

| 2012 | 410,648 | 329,887 | 855,758 | 633,635 | 2,229,927 | 10,881,543 |

| 2013 | 443,251 | 358,822 | 900,865 | 594,472 | 2,297,410 | 11,885,285 |

| 2014 | 473,336 | 386,352 | 975,671 | 634,131 | 2,469,490 | 12,905,827 |

| 2015 | 504,686 | 425,221 | 1,038,699 | 592,512 | 2,561,117 | 14,429,703 |

| 2016 | 524,920 | 458,921 | 1,117,020 | 508,492 | 2,609,354 | 15,377,129 |

| 2017 | 574,990 | 505,071 | 1,189,139 | 529,321 | 2,798,522 | 15,285,076 |

| 2018 | 617,643 | 540,150 | 1,260,058 | 502,851 | 2,920,703 | 19,182,231 |

| 2019 | 656,616 | 570,184 | 1,341,443 | 520,392 | 3,088,635 | 17,781,648 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fortuin, M.J.; Grebe, G.P.M.; Makoni, P.L. Wealth Inequality in South Africa—The Role of Government Policy. J. Risk Financial Manag. 2022, 15, 243. https://doi.org/10.3390/jrfm15060243

Fortuin MJ, Grebe GPM, Makoni PL. Wealth Inequality in South Africa—The Role of Government Policy. Journal of Risk and Financial Management. 2022; 15(6):243. https://doi.org/10.3390/jrfm15060243

Chicago/Turabian StyleFortuin, Marlin Jason, Gerhard Philip Maree Grebe, and Patricia Lindelwa Makoni. 2022. "Wealth Inequality in South Africa—The Role of Government Policy" Journal of Risk and Financial Management 15, no. 6: 243. https://doi.org/10.3390/jrfm15060243

APA StyleFortuin, M. J., Grebe, G. P. M., & Makoni, P. L. (2022). Wealth Inequality in South Africa—The Role of Government Policy. Journal of Risk and Financial Management, 15(6), 243. https://doi.org/10.3390/jrfm15060243