Net Impact of COVID-19 on REIT Returns

Abstract

:1. Introduction

2. Literature

3. Data

3.1. Quarterly Returns of Listed Equity REIT

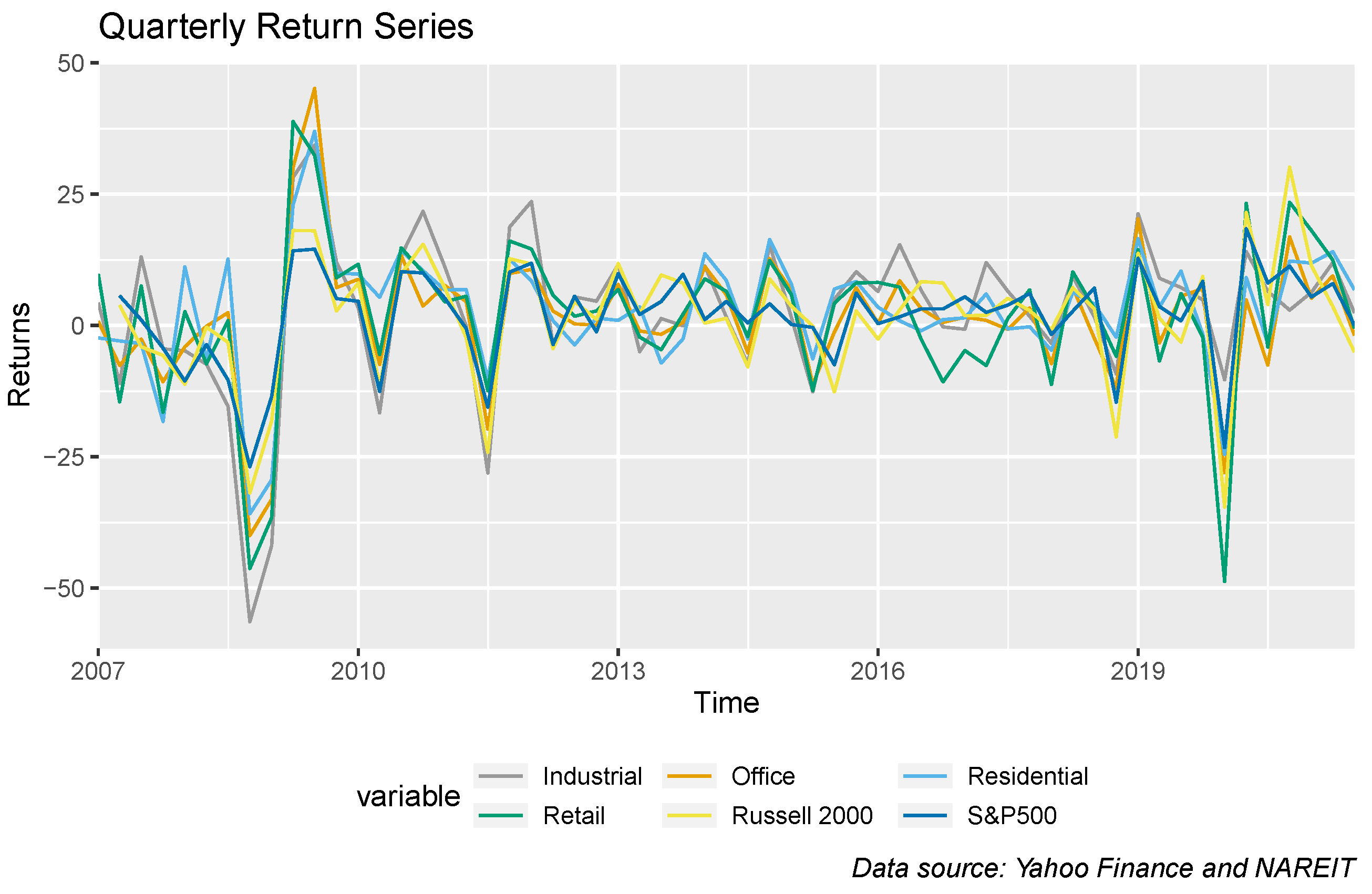

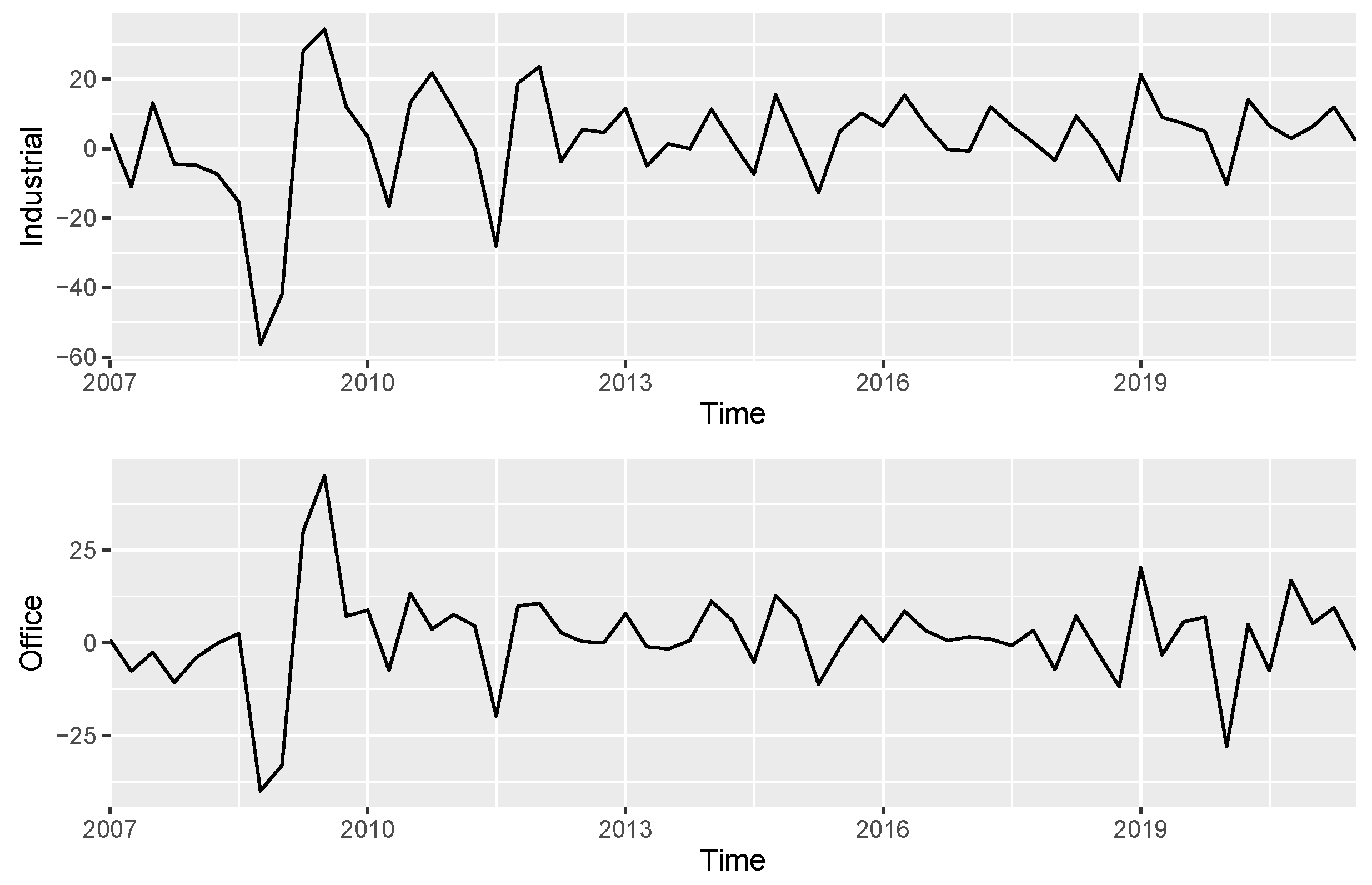

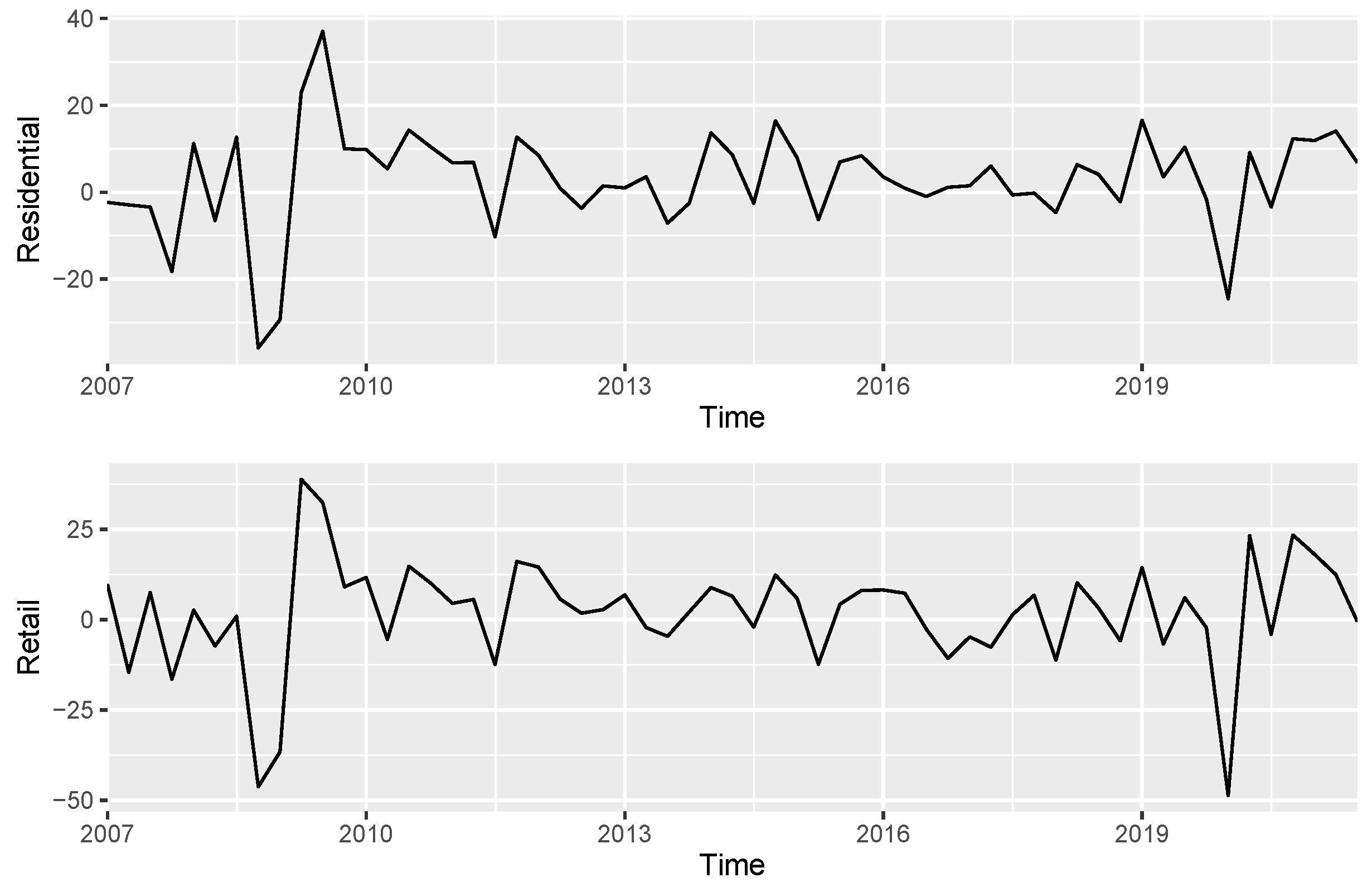

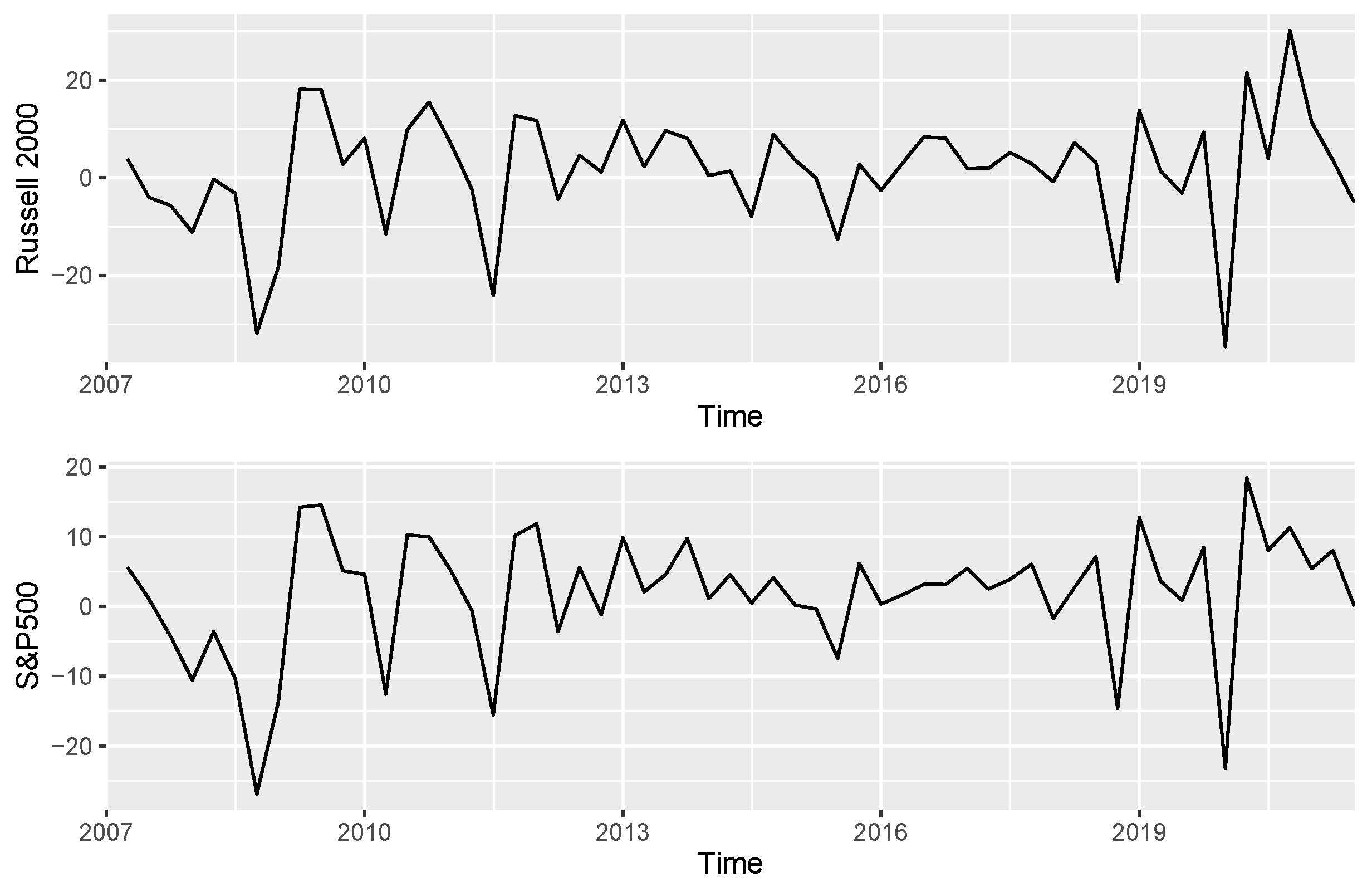

3.2. Main Market Indices and REIT Returns by Property Type

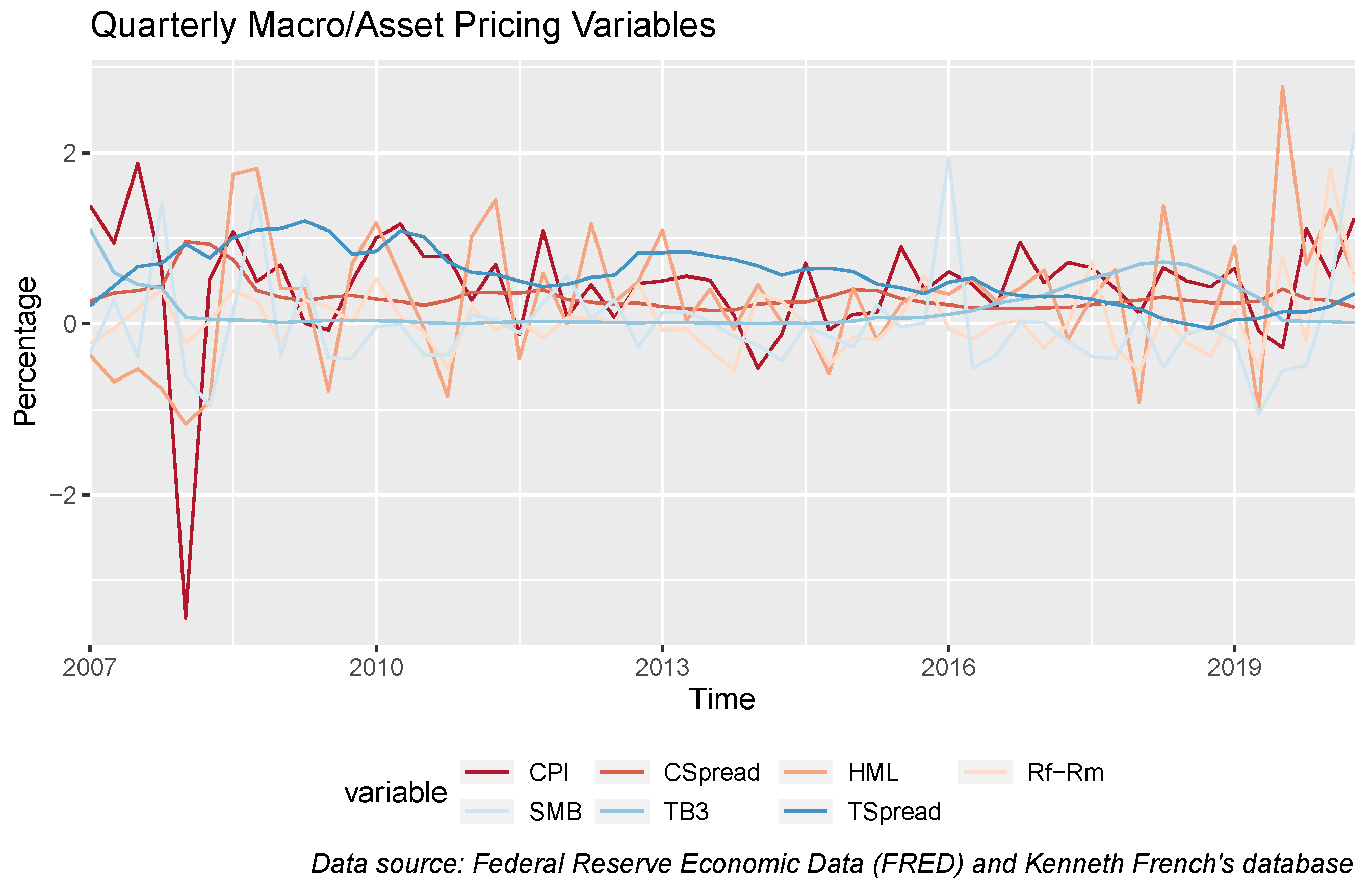

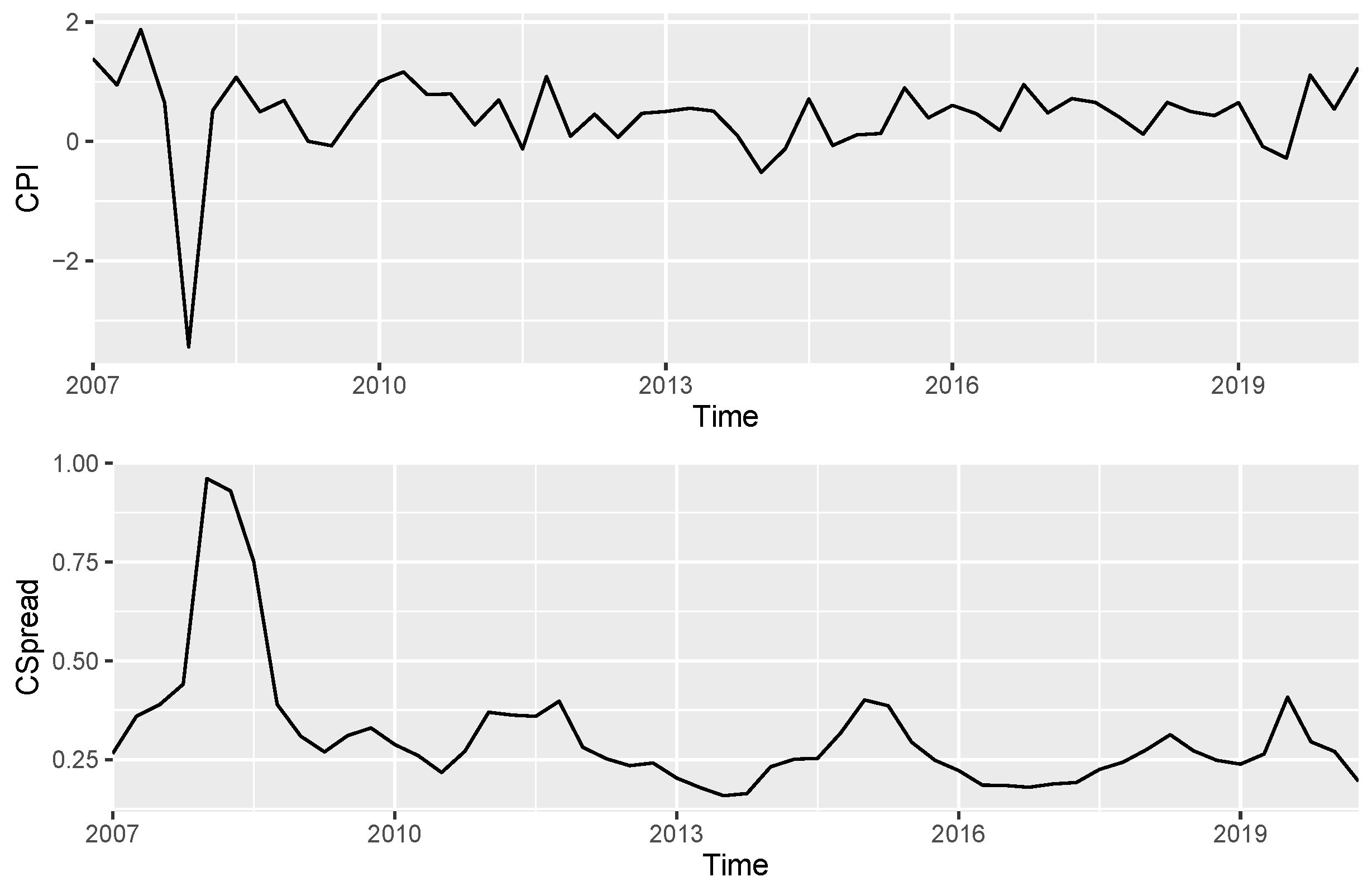

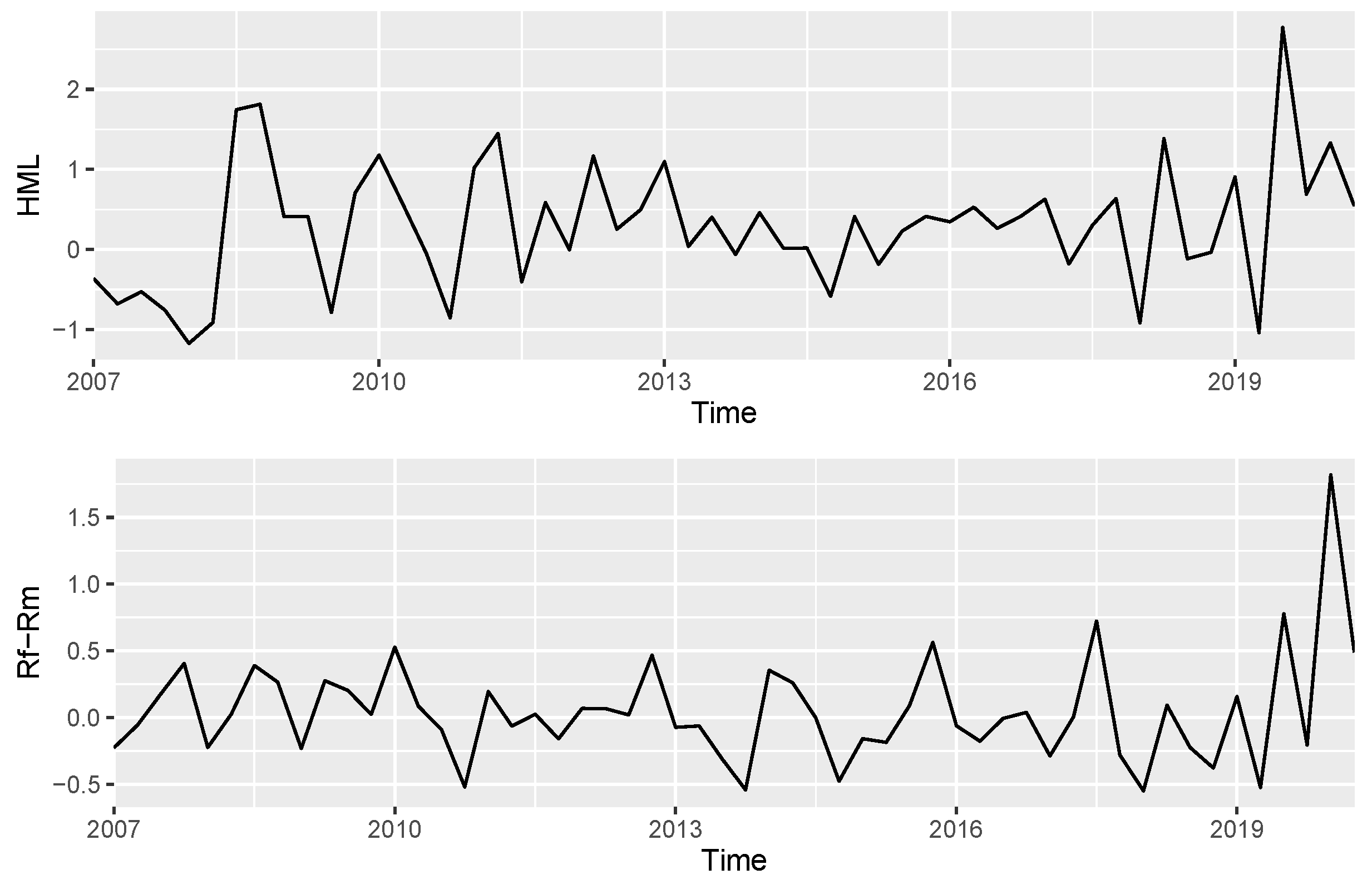

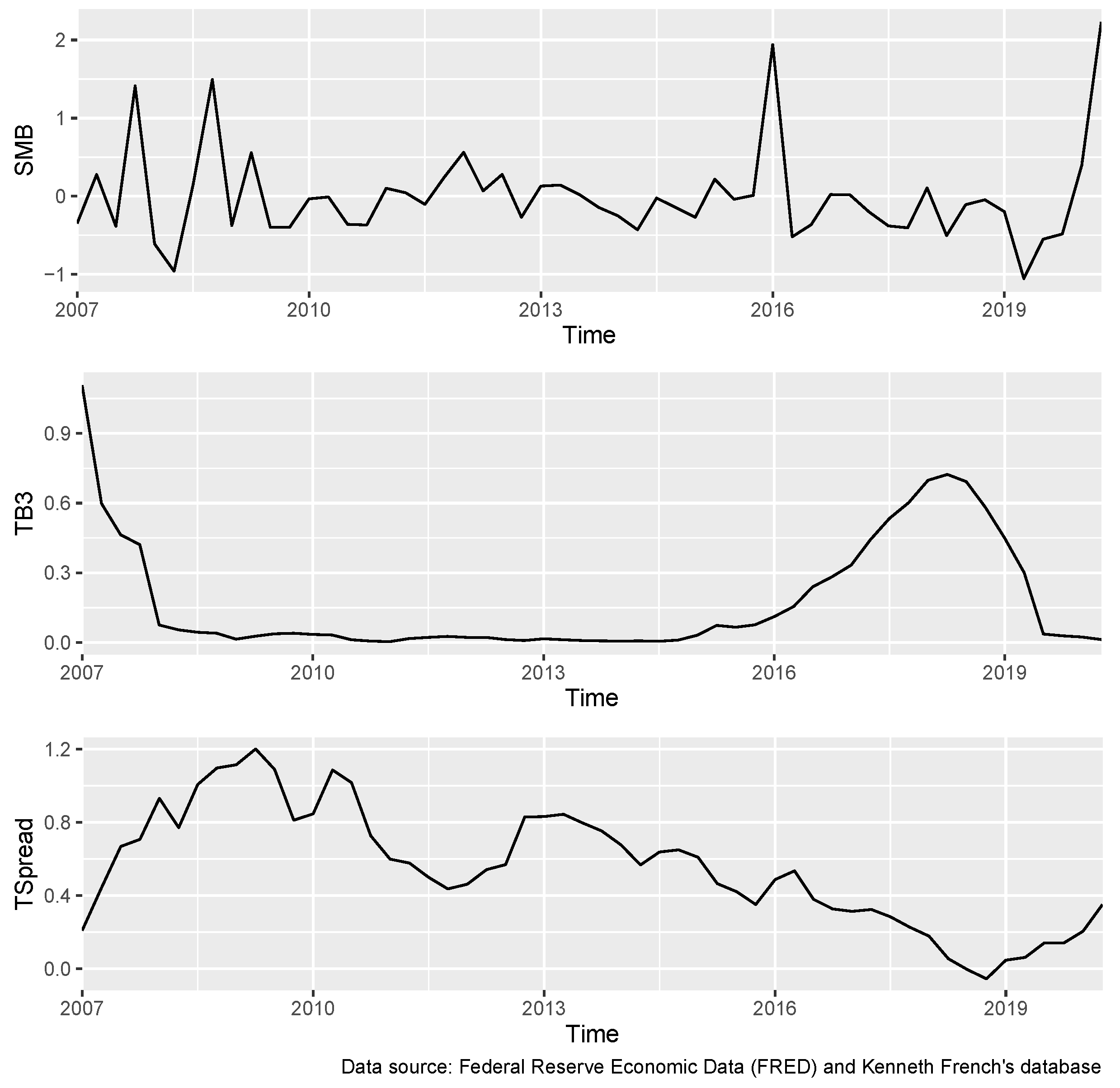

3.3. Macro/Asset-Pricing Variables

3.4. Firm Accounting Variables

4. Hypotheses, Model, and Estimation and Testing Strategies

4.1. Hypotheses

4.2. Model

4.3. Estimation and Testing Strategies

- In specification 1, the excess returns for each type k of REIT are regressed on all macro/asset-pricing variables and the two dummy variables ( and ) in the extended Fama–French model to infer the net impacts of the COVID-19 pandemic in particular and that of recessions in general.

- In specification 2, the interaction terms between macro/asset-pricing variables and are added to the model in specification 1 to allow structural changes in the macro/asset-pricing variables caused by recessions.

- In specification 3, the firm accounting variables are added to the model in specification 1 to accommodate the impacts of these firm accounting variables.

- In specification 4, the interaction terms between firm accounting variables and are added to the model in specification 3 to allow structural changes in these firm accounting variables caused by recessions.

- In specification 5, the interaction terms between macro/asset-pricing variables and are added to the model in specification 4 to allow structural changes in both macro/asset-pricing and firm accounting variables caused by recessions.

5. Empirical Results

- Industrial REITsOur first alternative hypothesis is that the net impact of the COVID-19 pandemic on industrial REIT returns is positive (). As shown in Table 6, while the net impact of recessions (BEAR) on industrial REIT returns is negative but statistically insignificant, the net impact of the COVID-19 pandemic (COVID) on industrial REIT returns is positive and statistically significant at the level of 1%. This provides strong evidence for rejecting the first null hypothesis () and favoring the first alternative hypothesis ().

- Office REITsOur second alternative hypothesis that the net impact of the COVID-19 pandemic on office REIT returns is negative (). As shown in Table 6, while the net impact of recessions (BEAR) on office REIT returns is negative and statistically significant at the level of 5%, the net impact of the COVID-19 pandemic (COVID) on office REIT returns is positive and statistically significant at the level of 1%. This provides strong evidence against the second null hypothesis () but it does not favor the second alternative hypothesis () either. The net impact of the COVID-19 pandemic offsets that of recessions for office REITs. This is perhaps caused by both existing office leases and the percentage rent clause for commercial properties during the COVID-19 pandemic.

- Residential REITsOur third alternative hypothesis is that the net impact of the COVID-19 pandemic on residential REIT returns is negative (). As shown in Table 6, while the net impact of recessions (BEAR) on residential REIT returns is negative and statistically significant at the level of 0.1%, the net impact of the COVID-19 pandemic (COVID) on residential REIT returns is positive and statistically significant at the level of 1%. This provides strong evidence against the third null hypothesis () but it does not favor the third alternative hypothesis () either. The net impact of offsets that of recessions for residential REITs. This is perhaps caused by both existing residential leases and the grace period for renting residential properties during the COVID-19 pandemic.

- Retail REITsOur fourth alternative hypothesis is that the net impact of COVID-19 on retail REIT returns is negative (). As shown in Table 6, while the net impact of recessions (BEAR) on retail REIT returns is negative and statistically insignificant, the net impact of the COVID-19 pandemic (COVID) on residential REIT returns is positive and statistically insignificant. Therefore, we find evidence for the fourth null hypothesis () but against the fourth alternative hypothesis (). When all control variables and structural changes are taken into consideration, retail REIT returns are exposed to a long and enduring impact of the boom and bust cycle rather than an isolated impact from recessions.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Real Estate Investment Trusts

Appendix B. Descriptive Statistics for the Whole Sample and the GFC Period

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Ticker | Mean | StDev | Max | Min | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| Office REITs | |||||||

| ARE | 2.8547 | 14.5500 | 51.7189 | −45.5372 | −0.2368 | 3.6655 | |

| BDN | 2.9118 | 29.1159 | 159.5305 | −60.2510 | 2.7757 | 14.6294 | |

| BXP | 1.7269 | 14.0439 | 38.7742 | −37.6219 | −0.2647 | 1.9103 | |

| CLI | 0.1325 | 13.6442 | 40.3821 | −33.5106 | 0.1562 | 0.5684 | |

| CMCT | −0.8898 | 16.6981 | 24.6782 | −67.3734 | −1.5178 | 3.4748 | |

| COR | 6.9007 | 13.7323 | 38.4508 | −19.3713 | 0.1723 | −0.5570 | |

| CUZ | 0.4411 | 16.4673 | 38.3901 | −49.3766 | −0.7582 | 1.3598 | |

| DEI | 2.3281 | 14.6217 | 34.4217 | −40.9819 | −0.7328 | 1.5619 | |

| DLR | 4.2847 | 11.0080 | 27.8279 | −27.7777 | −0.2396 | 0.0809 | |

| EQC | 2.3261 | 17.2572 | 78.8871 | −47.9605 | 1.3705 | 7.3319 | |

| FSP | −0.1511 | 11.0972 | 19.4852 | −31.0184 | −0.3377 | −0.1867 | |

| HIW | 2.2922 | 12.8104 | 41.5983 | −26.1230 | 0.2608 | 0.3337 | |

| HPP | 2.9321 | 11.9807 | 31.7526 | −30.7772 | −0.3014 | 0.9052 | |

| KRC | 2.2844 | 14.3783 | 33.6959 | −45.3855 | −0.4959 | 1.3719 | |

| OFC | 0.9743 | 13.3771 | 31.0601 | −29.6474 | −0.2449 | −0.2558 | |

| OPI | 0.4094 | 13.2421 | 30.4217 | −34.3418 | −0.3813 | 0.1969 | |

| PDM | 1.4408 | 8.8092 | 25.6796 | −20.7514 | −0.0549 | 0.7093 | |

| SLG | 2.4659 | 27.1965 | 115.7642 | −58.0747 | 1.5342 | 6.4323 | |

| VNO | 0.7056 | 15.3110 | 43.2096 | −42.0379 | −0.4198 | 1.9204 | |

| WRE | 1.3885 | 12.7644 | 34.8668 | −35.4600 | 0.0043 | 0.9906 | |

| Total | 1.8879 | 16.7010 | 159.5305 | −67.3734 | |||

| Residential REITs | |||||||

| ACC | 2.0866 | 12.6062 | 31.1331 | −37.5701 | −0.6852 | 1.7511 | |

| AIV | 3.0546 | 19.4856 | 65.8137 | −55.6760 | 0.0976 | 4.1606 | |

| AVB | 2.4223 | 12.2378 | 31.4347 | −34.2577 | −0.5676 | 0.9316 | |

| BRT | 1.5193 | 18.0936 | 62.7630 | −57.9067 | 0.0532 | 3.4117 | |

| CPT | 2.7593 | 13.3600 | 46.2630 | −28.0321 | 0.1519 | 1.5253 | |

| ELS | 4.1070 | 10.2253 | 23.3373 | −25.6081 | −0.5704 | 0.4126 | |

| EQR | 3.0930 | 13.0872 | 38.9513 | −33.3628 | −0.3534 | 0.9319 | |

| ESS | 2.8923 | 11.8776 | 28.7085 | −33.0791 | −0.5949 | 0.8883 | |

| MAA | 3.2774 | 10.1852 | 23.6235 | −21.8510 | −0.2309 | −0.4465 | |

| SUI | 5.2670 | 13.9928 | 61.7645 | −27.9983 | 0.8280 | 4.1418 | |

| UDR | 3.5285 | 14.4289 | 51.0507 | −37.5984 | −0.0053 | 2.4846 | |

| UMH | 1.7158 | 14.1154 | 48.0407 | −30.9556 | 0.5684 | 1.0699 | |

| Total | 2.9769 | 15.2254 | 65.8137 | −57.9067 |

| Ticker | Mean | StDev | Max | Min | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| Industrial REITs | |||||||

| CUBE | 5.2122 | 24.9711 | 130.5632 | −62.2723 | 1.8501 | 11.5480 | |

| DRE | 3.1649 | 18.2856 | 69.1153 | −52.1461 | 0.0697 | 3.8656 | |

| EGP | 3.3216 | 10.5428 | 26.6931 | −24.5426 | −0.2391 | 0.0495 | |

| EXR | 5.9095 | 14.7262 | 48.0496 | −43.2287 | −0.4385 | 2.2473 | |

| FR | 3.8671 | 24.8732 | 74.0000 | −72.5040 | −0.1675 | 2.7670 | |

| LSI | 3.4206 | 12.3558 | 24.9511 | −40.4685 | −0.7547 | 1.3797 | |

| MNR | 2.6510 | 10.4763 | 21.8227 | −23.5695 | −0.3355 | −0.5305 | |

| PLD | 2.9370 | 15.2507 | 30.8977 | −45.4079 | −0.8883 | 1.4347 | |

| PSA | 3.5185 | 10.9112 | 28.0474 | −26.1591 | −0.1844 | −0.0792 | |

| SELF | 1.2395 | 10.4171 | 32.4426 | −20.7264 | 0.6313 | 0.9637 | |

| TRNO | 3.6917 | 9.6963 | 25.9567 | −24.7066 | −0.0617 | 0.8042 | |

| Total | 3.5394 | 17.3884 | 130.5632 | −72.5040 | |||

| Retail REITs | |||||||

| ADC | 3.9960 | 12.0946 | 28.9803 | −31.9524 | −0.2290 | 0.2793 | |

| AKR | 0.5417 | 13.6315 | 22.4949 | −50.0699 | −1.3886 | 3.0777 | |

| ALX | 1.7149 | 15.1373 | 66.8213 | −32.3965 | 1.4026 | 5.5885 | |

| BFS | 0.7607 | 12.7837 | 29.3959 | −39.6840 | −0.7676 | 1.9624 | |

| CDR | 0.9840 | 32.6169 | 158.2858 | −74.7942 | 1.8184 | 9.2329 | |

| EPR | 2.3739 | 19.4314 | 65.5889 | −62.2106 | −0.3778 | 3.3772 | |

| FRT | 1.2115 | 11.8980 | 23.8856 | −39.5257 | −0.8232 | 1.4176 | |

| GTY | 2.3646 | 15.7512 | 56.7043 | −41.9437 | 0.0448 | 2.7386 | |

| HMG | 5.7331 | 50.4824 | 317.3038 | −48.9437 | 4.8027 | 26.4067 | |

| KIM | 0.6083 | 19.1336 | 48.2300 | −58.1319 | −0.8292 | 1.6435 | |

| KRG | −0.8554 | 19.2107 | 39.1975 | −54.5032 | −0.6209 | 0.9215 | |

| MAC | 1.5937 | 31.5421 | 148.2265 | −76.0571 | 1.5574 | 8.5333 | |

| NNN | 2.5249 | 11.3476 | 22.8775 | −36.5346 | −0.8599 | 1.4235 | |

| O | 3.3809 | 10.6379 | 23.3780 | −26.2444 | −0.2758 | −0.4406 | |

| PEI | −0.9268 | 25.6138 | 56.7872 | −80.9082 | −0.4330 | 1.2677 | |

| REG | 0.9381 | 13.7124 | 33.4912 | −38.2903 | −0.6203 | 0.7877 | |

| ROIC | 1.3598 | 10.9249 | 16.1900 | −51.4322 | −2.6922 | 10.7390 | |

| RPT | 1.3724 | 20.8537 | 70.4861 | −70.2108 | −0.5969 | 4.0528 | |

| SITC | 1.4689 | 31.9213 | 144.6002 | −84.1559 | 1.4696 | 7.4044 | |

| SKT | −0.3709 | 13.1306 | 22.9726 | −62.3287 | −1.9607 | 7.6797 | |

| SPG | 1.7145 | 17.1956 | 56.4830 | −60.6230 | −0.5734 | 4.1293 | |

| UBA | 1.4796 | 11.4137 | 28.6008 | −39.2738 | −0.6615 | 1.7949 | |

| UBP | 1.1351 | 10.1621 | 18.1103 | −39.4589 | −1.2143 | 3.1563 | |

| WSR | 1.7020 | 14.5270 | 25.8728 | −54.4217 | −1.4469 | 3.9257 | |

| Total | 1.5336 | 21.74876 | 317.3038 | −84.1559 |

| Ticker | Mean | StDev | Max | Min | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| Office REIITs | |||||||

| ARE | −12.1080 | 23.8650 | 14.8134 | −45.5371 | −0.3243 | −1.8612 | |

| BDN | −24.2486 | 26.1066 | 2.6906 | −60.2511 | −0.2649 | −1.9593 | |

| BXP | −14.2955 | 17.7885 | 3.4963 | −37.6219 | −0.3822 | −1.9428 | |

| CLI | −10.2607 | 12.0565 | 7.1086 | −25.9595 | 0.1401 | −1.6911 | |

| CMCT | −9.3319 | 17.8808 | 14.1507 | −34.9850 | −0.1063 | −1.6899 | |

| CUZ | −17.0190 | 26.4821 | 12.6597 | −49.3766 | −0.0530 | −1.9777 | |

| DEI | −15.5815 | 20.0851 | 4.3568 | −40.9819 | −0.4018 | −1.9597 | |

| DLR | −1.6305 | 15.6116 | 13.9407 | −27.7777 | −0.5129 | −1.4296 | |

| EQC | −13.2783 | 19.3694 | 1.6468 | −47.9605 | −0.8018 | −1.1474 | |

| FSP | −3.8904 | 12.2030 | 15.5627 | −17.6064 | 0.3760 | −1.5863 | |

| HIW | −5.9295 | 13.5408 | 13.8862 | −18.4943 | 0.3513 | −1.8896 | |

| KRC | −16.6140 | 17.0939 | 2.3671 | −45.3855 | −0.5612 | −1.3614 | |

| OFC | −5.2421 | 16.1407 | 18.0014 | −23.2311 | 0.2656 | −1.8459 | |

| SLG | −28.0343 | 23.0645 | −3.5048 | −58.0747 | −0.3615 | −1.9301 | |

| VNO | −16.0524 | 18.7998 | 3.5462 | −41.5100 | −0.1805 | −2.0292 | |

| WRE | −7.5266 | 20.5645 | 22.0146 | −35.4600 | 0.1130 | −1.6262 | |

| Residential REIITs | |||||||

| ACC | −4.7138 | 19.4518 | 20.8862 | −37.5702 | −0.4018 | −1.1301 | |

| AIV | −20.6544 | 28.3528 | 10.3532 | −55.6760 | −0.2042 | −1.9727 | |

| AVB | −11.7278 | 17.2916 | 10.4230 | −34.2578 | 0.1342 | −1.8342 | |

| BRT | −21.8410 | 20.3626 | −4.6439 | −57.9067 | −0.7376 | −1.1877 | |

| CPT | −13.3783 | 16.7510 | 9.5205 | −28.0321 | 0.3847 | −1.9667 | |

| ELS | −3.4423 | 17.3655 | 20.6353 | −25.6081 | 0.0890 | −1.8393 | |

| EQR | −9.6003 | 21.7813 | 17.6250 | −33.3628 | 0.2242 | −1.9469 | |

| ESS | −9.0813 | 20.1735 | 20.0573 | −33.0791 | 0.3009 | −1.7759 | |

| MAA | −6.1843 | 13.3413 | 17.5702 | −21.8510 | 0.6364 | −0.9878 | |

| SUI | −10.4351 | 15.7439 | 10.9078 | −27.9983 | 0.1238 | −1.8706 | |

| UDR | −9.8020 | 26.3602 | 24.8475 | −37.5984 | 0.2254 | −1.9367 | |

| UMH | −13.4541 | 3.3236 | −9.2985 | −17.4119 | 0.0945 | −1.9190 |

| Ticker | Mean | StDev | Max | Min | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| Industrial REITs | |||||||

| CUBE | −17.7816 | 35.6673 | 26.7337 | −62.2723 | −0.0858 | −1.9666 | |

| DRE | −21.2786 | 23.9878 | 7.2249 | −52.1461 | −0.2150 | −1.9240 | |

| EGP | −5.5953 | 16.0488 | 14.0243 | −24.5426 | 0.2581 | −1.9060 | |

| EXR | −11.9119 | 21.7652 | 17.8891 | −43.2288 | −0.1152 | −1.6088 | |

| FR | −26.7531 | 33.2755 | 6.6800 | −72.5040 | −0.4414 | −1.9093 | |

| LSI | −9.6275 | 18.3405 | 9.3819 | −40.4684 | −0.4770 | −1.3397 | |

| MNR | −1.6514 | 12.9107 | 21.2035 | −18.3893 | 0.5539 | −0.8898 | |

| PLD | −19.5168 | 17.4147 | −3.5620 | −45.4079 | −0.5252 | −1.8303 | |

| PSA | −3.5900 | 20.4966 | 22.5199 | −26.1591 | 0.3081 | −1.9443 | |

| SELF | −6.9138 | 8.6385 | 1.2382 | −20.7264 | −0.4209 | −1.6493 | |

| Retail REITs | |||||||

| ADC | −7.8000 | 18.9355 | 23.9916 | −31.9524 | 0.3829 | −1.1906 | |

| AKR | −11.8736 | 17.1373 | 8.6325 | −39.7331 | −0.4529 | −1.4425 | |

| ALX | −10.0678 | 23.1941 | 30.0136 | −32.3965 | 0.5765 | −1.2379 | |

| BFS | −10.5942 | 17.0689 | 5.7341 | −39.6840 | −0.5479 | −1.3122 | |

| CDR | −18.0185 | 36.6466 | 18.3193 | −74.7942 | −0.3856 | −1.7038 | |

| EPR | −13.6500 | 24.7016 | 10.9202 | −43.8499 | −0.3107 | −1.9816 | |

| FRT | −8.7707 | 17.7520 | 23.8857 | −25.7457 | 0.8285 | −0.9063 | |

| GTY | −0.7304 | 31.1557 | 56.7043 | −38.1245 | 0.7482 | −0.7269 | |

| HMG | −20.8979 | 9.9473 | −11.7647 | −36.6667 | −0.4981 | −1.6452 | |

| KIM | −20.8181 | 27.7749 | 8.9675 | −58.1319 | −0.1790 | −1.8999 | |

| KRG | −26.3465 | 20.0154 | −9.0023 | −54.5033 | −0.4651 | −1.9203 | |

| MAC | −26.8989 | 31.8427 | 3.7898 | −69.2977 | −0.3770 | −1.9386 | |

| NNN | −4.8112 | 13.3081 | 15.9095 | −25.6970 | −0.0148 | −1.0084 | |

| O | −3.4659 | 10.2113 | 13.1100 | −13.3510 | 0.4929 | −1.5825 | |

| PEI | −27.2595 | 19.3297 | −8.8207 | −55.9151 | −0.4690 | −1.8310 | |

| REG | −12.9714 | 18.6849 | 13.2789 | −38.2903 | 0.0672 | −1.6737 | |

| RPT | −14.9210 | 30.7502 | 8.6207 | −70.2108 | −0.8405 | −1.1373 | |

| SITC | −29.9659 | 34.1199 | 11.8780 | −84.1558 | −0.3351 | −1.4920 | |

| SKT | −2.5249 | 13.9360 | 22.9725 | −14.8276 | 0.8615 | −0.9940 | |

| SPG | −12.7024 | 21.1286 | 9.6799 | −42.4063 | −0.1908 | −1.8395 | |

| UBA | −1.1097 | 16.6176 | 28.6008 | −14.9493 | 0.7424 | −1.1314 | |

| UBP | −1.8467 | 11.3101 | 13.8327 | −15.5306 | 0.2917 | −1.8121 |

Appendix C. Main Market Indices and REIT Returns by Property Type

Appendix D. Quarterly Macro/Asset Pricing Variables

Appendix E. Model Results: Specifications 1–4

| Variable | Industrial | Office | Residential | Retail |

|---|---|---|---|---|

| TSpread | * | |||

| CPI | * | |||

| CSpread | ||||

| Rm-Rf | ** | *** | * | ** |

| SMB | *** | *** | *** | *** |

| HML | *** | *** | *** | *** |

| BEAR | ** | |||

| COVID:BEAR | ** | *** | ||

| R | ||||

| Adj. R | ||||

| N | 11 | 20 | 12 | 24 |

| T | 40–50 | 38–50 | 50 | 38–50 |

| Num. obs. | 540 | 960 | 600 | 1179 |

| F-statistic | ||||

| p-value | 1.8586 | 9.05642 | 3.99434 | 6.73672 |

| Variable | Industrial | Office | Residential | Retail |

|---|---|---|---|---|

| TSpread | * | |||

| CPI | * | *** | *** | *** |

| CSpread | *** | *** | *** | *** |

| Rm-Rf | * | * | ||

| SMB | ** | * | ||

| HML | *** | *** | *** | *** |

| BEAR | ** | * | *** | |

| COVID:BEAR | *** | *** | *** | |

| TSpread:BEAR | *** | ** | *** | |

| CPI:BEAR | *** | ** | *** | ** |

| CSpread:BEAR | *** | *** | * | |

| Rm-Rf:BEAR | *** | * | *** | |

| SMB:BEAR | *** | ** | *** | *** |

| HML:BEAR | ** | ** | ||

| R | ||||

| Adj. R | ||||

| N | 11 | 20 | 12 | 24 |

| T(Unbalanced Panel) | 40–50 | 38–50 | 50 | 38–50 |

| Num. obs. | 540 | 960 | 600 | 1179 |

| F Statistics | ||||

| p-value | 2.09606 | 2.2447 | 1.59762 | 8.3471 |

| Variable | Industrial | Office | Residential | Retail |

|---|---|---|---|---|

| ROA | ||||

| ROE | * | |||

| ROI | ||||

| EBITDAMA | ** | |||

| CR | ||||

| NCATA | ||||

| LTDE | ||||

| TDE | ||||

| TAT | * | |||

| CET | ||||

| CFPS | ** | |||

| BVPS | ||||

| TSpread | ||||

| CPI | ||||

| CSpread | ||||

| Rm-Rf | * | ** | ** | |

| SMB | *** | *** | *** | *** |

| HML | *** | *** | *** | *** |

| BEAR | * | |||

| COVID:BEAR | *** | |||

| R | ||||

| Adj. R | ||||

| N | 8 | 15 | 9 | 19 |

| T(Unbalanced Panel) | 50 | 47–50 | 36–50 | 1–50 |

| Num. obs. | 400 | 742 | 420 | 889 |

| F Statistics | ||||

| p-value | 2.15879 | 2.1024 | 5.82583 | 1.10981 |

| Variable | Industrial | Office | Residential | Retail |

|---|---|---|---|---|

| ROA | ||||

| ROE | ||||

| ROI | ||||

| EBITDAMA | ** | |||

| CR | ||||

| NCATA | ||||

| LTDE | ||||

| TDE | ||||

| TAT | * | |||

| CET | ||||

| CFPS | ||||

| BVPS | ||||

| TSpread | ||||

| CPI | * | |||

| CSpread | ||||

| Rm-Rf | * | ** | ** | |

| SMB | ** | *** | *** | *** |

| HML | *** | *** | *** | *** |

| BEAR | ||||

| COVID:BEAR | * | *** | ||

| ROA:BEAR | *** | ** | * | |

| ROE:BEAR | *** | * | ** | |

| ROI:BEAR | ||||

| EBITDAMA:BEAR | * | * | * | |

| CR:BEAR | * | |||

| NCATA:BEAR | ||||

| LTDE:BEAR | ** | |||

| TDE:BEAR | * | |||

| TAT:BEAR | * | |||

| CET:BEAR | *** | |||

| CFPS:BEAR | ||||

| BVPS:BEAR | ||||

| R | ||||

| Adj. R | ||||

| N | 8 | 15 | 9 | 19 |

| T(Unbalanced Panel) | 50 | 47–50 | 35–50 | 1–50 |

| Num. obs. | 400 | 742 | 420 | 889 |

| F Statistics | ||||

| p-value | 3.15954 | 1.36026 | 1.90128 | 4.31564 |

| 1 | See https://www.who.int/emergencies/diseases/novel-coronavirus-2019/interactive-timeline, accessed on 12 October 2021. |

| 2 | See https://stats.oecd.org/Index.aspx?QueryName=350, accessed on 12 October 2021. |

| 3 | Gross fixed capital formation refers to the value of acquisitions of new or existing fixed assets less disposals of fixed assets. |

| 4 | See https://ca.finance.yahoo.com/, accessed on 12 October 2021. |

| 5 | See Appendix A for a detailed discussion on REITs. |

| 6 | As shown in Feng et al. (2007), the debt ratio on average in the REITs industry increased from 50% (at IPOs) to 65% in 10 years. This could repeat itself during the COVID-19 pandemic. |

| 7 | See https://www.reit.com/data-research/research/nareit-research/2021-reit-outlook-economy-commercial-real-estate, accessed on 12 October 2021. |

| 8 | See https://www.reit.com/data-research/research/nareit-research/2021-reit-outlook-economy-commercial-real-estate, accessed on 12 October 2021. |

| 9 | See https://www.nber.org/research/business-cycle-dating accessed on 12 October 2021. |

| 10 | The market portfolio’s excess return (Rm-Rf) is the value-weighted return on all NYSE, AMEX, and NASDAQ stocks minus the one-month Treasury bill rate. |

| 11 | SMB is the difference between the return on small and big stock portfolios and captures the return attributable to the size factor. |

| 12 | HML is the difference between the return on high and low BE/ME portfolios and captures the return attributable to the value factor. |

| 13 | TSpread—the difference between the long and short bond interest rates. |

| 14 | CSpread—the difference between the low- and high-rating bond interest rates. |

| 15 | The dividend yield (or current yield) on an REIT is calculated by dividing the annualized dividends by its current REIT price. |

| 16 | Leverage can enlarge gain and loss but higher leverage comes with a higher risk. Shareholders have the residual claim on earnings and assets and higher leverage means higher interest and principal payments, less financial flexibility, and a greater probability of default during recessions. The debt-to-total market capitalization and debt-to-tangible book value ratios are two commonly-used leverage metrics. The payout ratio is defined as the proportion of net income a company pays out to its shareholders as a dividend. The REIT’s expected dividend payout ratio is obtained by dividing the current annualized dividend by an estimate of next year’s expected fund from operation (FFO) per share. The dividend/FFO payout ratio signals the ability of an REIT to pay its current dividend. |

| 17 | See https://www.reit.com/nareit/advocacy/policy/nareit-ffo-white-paper-and-related-implementation, accessed on 22 October 2021. |

| 18 | See https://www.reit.com/data-research/reit-market-data/reit-industry-financial-snapshot, accessed on 19 November 2021. |

| 19 | See https://stockmarketmba.com/whatisareit.php, accessed on 19 November 2021. |

| 20 | |

| 21 | Figure A1 and Figure A2 in Appendix C show the individual figure for each and every total return series. |

| 22 | See https://www.reit.com/data-research/reit-indices/historical-reit-returns/performance-property-sector-subsector, accessed on 15 October 2021. |

| 23 | Figure A3 and Figure A4 and in Appendix D show the individual figure for each and every macro/asset-pricing variable. |

| 24 | See https://fred.stlouisfed.org/series/CPIAUCSL, accessed on 15 October 2021. |

| 25 | http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html, accessed on 15 October 2021. |

| 26 | This is for return on investment. |

| 27 | For more information on the accounting data, please see Table 3. |

| 28 | See https://www.pwc.com/us/en/library/covid-19/us-remote-work-survey.html, accessed on 2 November 2021. |

| 29 | |

| 30 | These two dummy variables are defined based on the chronology provided by the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER). A recession is defined as the period between a peak of economic activity and its subsequent trough according to the NBER. The first recession in our sample was caused by the GFC in which excessive leverage, the overheated housing market, and financial crisis started from December 2007 (2007 Q4) to June 2009 (2009 Q2), and the second recession was induced by the COVID-19 pandemic from February 2020 to April 2020. |

| 31 | This is the heteroskedasticity and serial correlation consistent variance-covariance matrix; see (Newey and West 1987). |

| 32 | |

| 33 | See https://en.wikipedia.org/wiki/Homer_Hoyt 12 October 2021. |

| 34 | See https://www.pwc.com/us/en/library/covid-19/us-remote-work-survey.html accessed on 12 October 2021. |

| 35 | See https://www.deskmag.com/en/coworking-news/2019-state-of-coworking-spaces-2-million-members-growth-crisis-market-report-survey-study accessed on 12 October 2021. |

| 36 | See https://www.ft.com/content/83decf7a-c04d-11e9-b350-db00d509634e accessed on 12 October 2021. |

| 37 | See https://www.reit.com/news/blog/market-commentary/reits-have-limited-exposure-to-wework accessed on 12 October 2021. |

References

- Akinsomi, Omokolade. 2021. How resilient are REITs to a pandemic? The Covid-19 effect. Journal of Property Investment & Finance 39: 19–24. [Google Scholar]

- Alhenawi, Yasser. 2011. The determinants of capital structure in real estate investment trusts. Global Journal of Finance and Economics 8: 119–28. [Google Scholar]

- Block, Ralph L. 2011. Investing in REITs: Real Estate Investment Trusts. Hoboken: John Wiley & Sons. [Google Scholar]

- Chan, K. C., Patric H. Hendershott, and Anthony B. Sanders. 1990. Risk and return on real estate: Evidence from equity REITs. Real Estate Economics 18: 431–52. [Google Scholar] [CrossRef]

- Chen, Nai-Fu, Richard Roll, and Stephen A. Ross. 1986. Economic forces and the stock market. Journal of Business 59: 383–403. [Google Scholar] [CrossRef]

- Chiang, Kevin C.H. 2015. What drives REIT prices? The time-varying informational content of dividend yields. Journal of Real Estate Research 37: 173–90. [Google Scholar] [CrossRef]

- Clayton, Jim, and Grey MacKinnon. 2003. The relative importance of stock, bond and real estate factors in explaining REIT returns. Journal of Real Estate Finance and Economics 27: 39–60. [Google Scholar] [CrossRef]

- Emmerling, Thomas J., Eunkyu Lee, Crocker Herbert Liu, and Yildiray Yildirim. 2022. RETurning to REITs. SSRN. Available online: https://ssrn.com/abstract=4100623 (accessed on 4 May 2022).

- Fama, Eugene F., and Kenneth R. French. 1992. The cross-section of expected stock returns. Journal of Finance 47: 427–65. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1993. Common risk factors in the returns on stocks and bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Feng, Zhilan, Chinmoy Ghosh, and C. F. Sirmans. 2007. On the capital structure of real estate investment trusts (REITs). Journal of Real Estate Finance and Economics 34: 81–105. [Google Scholar] [CrossRef]

- Feng, Zhilan, S. McKay Price, and C. F. Sirmans. 2011. Review articles: An overview of equity real estate investment trusts (REITs): 1993–2009. Journal of Real Estate Literature 19: 307–43. [Google Scholar] [CrossRef]

- Gyourko, Joseph, and Edward Nelling. 1996. Systematic risk and diversification in the equity REIT market. Real Estate Economics 24: 493–515. [Google Scholar] [CrossRef]

- Lin, Yu-Cheng, Chyi Lin Lee, and Graeme Newell. 2020. The added-value role of industrial and logistics REITs in the Pacific Rim region. Journal of Property Investment & Finance 38: 597–616. [Google Scholar]

- Ling, David C., Chongyu Wang, and Tingyu Zhou. 2020. A first look at the impact of COVID-19 on commercial real estate prices: Asset-level evidence. Review of Asset Pricing Studies 10: 669–704. [Google Scholar] [CrossRef]

- Milcheva, Stanimira. 2022. Volatility and the cross-section of real estate equity returns during Covid-19. Journal of Real Estate Finance and Economics 65: 293–320. [Google Scholar] [CrossRef]

- Mueller, Glenn. 1995. Understanding real estate’s physical and financial market cycles. Real Estate Finance 12: 47. [Google Scholar]

- Newey, Whithey K., and Kenneth D. West. 1987. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55: 703–8. [Google Scholar] [CrossRef]

- Peterson, James D., and Cheng-Ho Hsieh. 1997. Do common risk factors in the returns on stocks and bonds explain returns on REITs? Real Estate Economics 25: 321–45. [Google Scholar] [CrossRef]

- Redman, Arnold L., and Herman Manakyan. 1995. A multivariate analysis of REIT performance by financial and real asset portfolio characteristics. Journal of Real Estate Finance and Economics 10: 169–75. [Google Scholar] [CrossRef]

- Reilly, Frank K., Keith C. Brown, and S. Leeds. 2018. Investment Analysis and Portfolio Management. Mason, OH: Cengage. [Google Scholar]

- Roll, Richard, and Stephen A. Ross. 1995. The arbitrage pricing theory approach to strategic portfolio. Financial Analysts Journal 51: 122. [Google Scholar] [CrossRef]

- Ross, Stephen A. 1976. The arbitrage theory of capital asset pricing. Journal of Economic Theory 13: 341–60. [Google Scholar] [CrossRef]

- Schnure, Calvin, Stephanie Krewson-Kelly, Merrie S. Frankel, and Glenn R. Mueller. 2020. Educated REIT Investing. Hoboken: John Wiley & Sons. [Google Scholar]

- Vincent, Linda. 1999. The information content of funds from operations (FFO) for real estate investment trusts (REITs). Journal of Accounting and Economics 26: 69–104. [Google Scholar] [CrossRef]

- Wheaton, William C. 1987. The cyclic behavior of the national office market. Real Estate Economics 15: 281–99. [Google Scholar]

| Office | Retail | Industrial | Residential | S&P500 | Russell 2000 | |

|---|---|---|---|---|---|---|

| Office | 1.0000 | 0.9070 | 0.8574 | 0.9080 | 0.7797 | 0.7991 |

| (0.0000) | (0.0558) | (0.0682) | (0.0555) | (0.0829) | (0.0796) | |

| Retail | 1.0000 | 0.8043 | 0.8923 | 0.7683 | 0.7763 | |

| (0.0000) | (0.0787) | (0.0598) | (0.0848) | (0.0835) | ||

| Industrial | 1.0000 | 0.7788 | 0.8040 | 0.7375 | ||

| (0.0000) | (0.0831) | (0.0788) | (0.0895) | |||

| Residential | 1.0000 | 0.6493 | 0.6641 | |||

| (0.0000) | (0.1007) | (0.0990) | ||||

| S&P500 | 1.0000 | 0.9329 | ||||

| (0.0000) | (0.0477) | |||||

| Russell 2000 | 1.0000 | |||||

| (0.0000) |

| TSpread | TB3 | CPI | CSpread | Rm-Rf | SMB | HML | |

|---|---|---|---|---|---|---|---|

| TSpread | 1.0000 | −0.5878 | −0.1170 | 0.2568 | 0.0205 | 0.1052 | −0.0288 |

| (0.0000) | (0.1122) | (0.1377) | (0.1340) | (0.1386) | (0.1379) | (0.1386) | |

| TB3 | 1.0000 | 0.2151 | −0.1071 | −0.1888 | −0.1269 | −0.2355 | |

| (0.0000) | (0.1354) | (0.1379) | (0.1362) | (0.1376) | (0.1348) | ||

| CPI | 1.0000 | −0.3907 | 0.0990 | 0.2058 | 0.2199 | ||

| (0.0000) | (0.1277) | (0.1380) | (0.1357) | (0.1353) | |||

| CSpread | 1.0000 | 0.0474 | −0.1606 | −0.1358 | |||

| (0.0000) | (0.1385) | (0.1369) | (0.1374) | ||||

| Rm−Rf | 1.0000 | 0.2408 | 0.4792 | ||||

| (0.0000) | (0.1346) | (0.1217) | |||||

| SMB | 1.0000 | 0.1747 | |||||

| (0.0000) | (0.1365) | ||||||

| HML | 1.0000 | ||||||

| (0.0000) |

| Symbol | Variable | Definition and Formula |

|---|---|---|

| Basic Series | ||

| NS | Net Sales | Revenue − Sale Returns − Allowances − Discounts |

| CA | Current Assets | Cash and Cash Equivalents + Short-term Investment |

| + Net Receivables + Inventories | ||

| SE | Shareholder Equity | Total Assets—Total Liabilities |

| CL | Current Liabilities | Obligations that are due within the next 12 months |

| LL | Long-term Liabilities | Obligations that are not due within the next 12 months |

| DP | Dividend Paid Out | The company’s earnings to distributed to its shareholders |

| OP | Operating Income | Net Earnings + Interest Expense + Income Taxes |

| EBITDA | Earning Before Interest, Tax, | Operating Income + Depreciation + Amortization |

| Depreciation, and Amortization | ||

| IT | Income Tax | Corporate Income Tax |

| Derived Series | ||

| Profitability Ratios | ||

| ROA | Return on Asset | |

| ROE | Return on Equity | |

| ROI | Return on Investment | |

| EBITDAMA | EBITDA Margin | |

| Liquidity Ratios | ||

| CR | Current Ratio | |

| NCATA | Net Current Assets % TA | |

| Financial Risk | ||

| LTDE | LT Debt to Equity Ratio | |

| TDE | Total Debt to Equity Ratio | |

| Asset Management | ||

| TAT | Total Asset Turnover | |

| CET | Cash and Equivalents Turnover | |

| Per Share | ||

| CFPS | Cash Flow per Share | |

| BVPS | Book Value per Share |

| Comparison | p-Value | p-Value | |||||

|---|---|---|---|---|---|---|---|

| Specification 1 vs. Specification 2 | |||||||

| Industrial REITs | 147.99 | 6 | 378 | 5.52731 | 887.94 | 6 | 1.52024 |

| Office REITs | 30.07 | 6 | 713 | 3.17588 | 180.42 | 6 | 2.76313 |

| Residential REITs | 87.188 | 6 | 376 | 4.01726 | 523.13 | 6 | 8.73401 |

| Retail REITs | 150.37 | 6 | 856 | 2.95958 | 902.19 | 6 | 1.26288 |

| Specification 1 vs. Specification 3 | |||||||

| Industrial REITs | 2.8861 | 12 | 372 | 0.000792541 | 34.634 | 12 | 0.0005355 |

| Office REITs | 1.5226 | 12 | 707 | 0.110737 | 18.271 | 12 | 0.107706 |

| Residential REITs | 1.6315 | 12 | 391 | 0.0805092 | 19.578 | 12 | 0.0755018 |

| Retail REITs | 0.675 | 12 | 850 | 0.776558 | 8.0997 | 12 | 0.777291 |

| Specification 3 vs. Specification 4 | |||||||

| Industrial REITs | 2.3618 | 12 | 360 | 0.00620854 | 28.341 | 12 | 0.00493029 |

| Office REITs | 2.7998 | 12 | 695 | 0.000952317 | 33.598 | 12 | 0.000780314 |

| Residential REITs | 2.4492 | 12 | 379 | 0.00439962 | 29.39 | 12 | 0.00344691 |

| Retail REITs | 0.5881 | 12 | 838 | 0.852987 | 7.0576 | 12 | 0.853784 |

| Specification 4 vs. Specification 5 | |||||||

| Industrial REITs | 36.566 | 6 | 354 | 2.00801 | 219.39 | 6 | 1.40387 |

| Office REITs | 26.455 | 6 | 689 | 2.06362 | 158.73 | 6 | 1.09999 |

| Residential REITs | 61.554 | 6 | 373 | 8.00936 | 369.32 | 6 | 1.09547 |

| Retail REITs | 73.918 | 6 | 832 | 6.81906 | 443.51 | 6 | 1.22366 |

| Specification | Industrial | Office | Residential | Retail |

|---|---|---|---|---|

| 5 | 0.56 | 0.54 | 0.55 | 0.52 |

| 4 | 0.39 | 0.47 | 0.40 | 0.39 |

| 3 | 0.38 | 0.44 | 0.38 | 0.38 |

| 2 | 0.48 | 0.46 | 0.55 | 0.41 |

| 1 | 0.31 | 0.38 | 0.41 | 0.31 |

| Variable | Industrial | Office | Residential | Retail |

|---|---|---|---|---|

| ROA | ||||

| ROE | ||||

| ROI | ||||

| EBITDAMA | *** | |||

| CR | ||||

| NCATA | ||||

| LTDE | ||||

| TDE | ||||

| TAT | * | |||

| CET | ||||

| CFPS | ||||

| BVPS | ||||

| TSpread | * | |||

| CPI | * | *** | *** | *** |

| CSpread | *** | *** | *** | *** |

| Rm-Rf | ||||

| SMB | ** | |||

| HML | *** | *** | *** | *** |

| BEAR | * | *** | ||

| COVID:BEAR | *** | ** | ** | |

| ROA:BEAR | * | |||

| ROE:BEAR | * | |||

| ROI:BEAR | ||||

| EBITDAMA:BEAR | * | |||

| CR:BEAR | ||||

| NCATA:BEAR | ||||

| LTDE:BEAR | ** | |||

| TDE:BEAR | * | |||

| TAT:BEAR | * | |||

| CET:BEAR | ** | |||

| CFPS:BEAR | ||||

| BVPS:BEAR | ||||

| TSpread:BEAR | *** | ** | *** | |

| CPI:BEAR | ** | *** | *** | ** |

| CSpread:BEAR | *** | *** | ** | |

| Rm-Rf:BEAR | ** | * | *** | |

| SMB:BEAR | *** | ** | *** | 28.40 *** |

| HML:BEAR | ** | *** | ||

| R | ||||

| Adj. R | ||||

| N | 8 | 15 | 9 | 19 |

| T(Unbalanced Panel) | 50 | 47–50 | 36–50 | 1–50 |

| Num. obs. | 400 | 742 | 420 | 889 |

| F Statistics | ||||

| p-value | 2.61132 | 3.15609 | 2.63781 | 2.72225 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cai, Y.; Xu, K. Net Impact of COVID-19 on REIT Returns. J. Risk Financial Manag. 2022, 15, 359. https://doi.org/10.3390/jrfm15080359

Cai Y, Xu K. Net Impact of COVID-19 on REIT Returns. Journal of Risk and Financial Management. 2022; 15(8):359. https://doi.org/10.3390/jrfm15080359

Chicago/Turabian StyleCai, Yongpei, and Kuan Xu. 2022. "Net Impact of COVID-19 on REIT Returns" Journal of Risk and Financial Management 15, no. 8: 359. https://doi.org/10.3390/jrfm15080359

APA StyleCai, Y., & Xu, K. (2022). Net Impact of COVID-19 on REIT Returns. Journal of Risk and Financial Management, 15(8), 359. https://doi.org/10.3390/jrfm15080359